Taxation Law: Analysis of Deductions, GST, and Legal Expenses

VerifiedAdded on 2020/04/07

|13

|2637

|126

Homework Assignment

AI Summary

This taxation law assignment analyzes various aspects of tax regulations, focusing on allowable deductions and input tax credits under the Income Tax Assessment Act 1997 and the GST Act 1999. The assignment addresses specific issues, including the deductibility of costs related to moving machinery, revaluation of assets, and legal expenses incurred in business operations. It also examines the eligibility of a company, Big Bank Limited, to claim input tax credit on advertisement expenses. The analysis incorporates relevant case law and taxation rulings to determine the applicability of deductions and credits in each scenario, providing a comprehensive overview of tax implications for different business activities and expenditures. The assignment also explores legal expenses in the context of opposing the winding up of a business and other legal costs for various purposes, determining their eligibility for permissible deduction. The document provides a detailed explanation of the regulations and their application to the given scenarios, offering a clear understanding of the tax law principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Author’s Note

Taxation Law

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer to Question 1

Requirement 1

Issue: This particular issue is related with the generation of costs incurred out of the moving of

machinery under “Section 8-1 of the Income Tax Assessment Act 1997”.

Regulations: Followings are the required legislations:

a. Section 8-1 of the Income Tax Assessment Act 1997

b. British Insulated & Helsby Cables

Application: It is the right of the individual taxpayer to claim for their permissible deduction

from their incurred cost under “Section 8-1 of the Income Tax Assessment Act 1997”. In

“Section 8-1 of the Income Tax Assessment Act 1997”, it is mentioned that the cost incurred

for moving machinery will be applicable for permissible deduction in case the taxpayer uses the

machinery for generating taxable income (Tiley & Barbara Abraham 2013). In the present case,

the cost to move the machinery to a new site will not be applicable for allowable deduction as

this process increased the cost of the machinery.

From the case of British Insulated & Helsby Cables”, the fact is visible that the

transportation cost incurred in the shifting of the depreciable asset provided the business with

constant extra benefits. In this situation, “Taxation ruling of TD 92/126” describes the fact that

the installation of machinery and starting functions of its will be considered for cost when it is

done for the revenue generation. In case of the present scenario, the cost involved with the

moving of machinery to a new site is capital expenditure and thus is not under allowable

deduction (Kenny 2013).

Answer to Question 1

Requirement 1

Issue: This particular issue is related with the generation of costs incurred out of the moving of

machinery under “Section 8-1 of the Income Tax Assessment Act 1997”.

Regulations: Followings are the required legislations:

a. Section 8-1 of the Income Tax Assessment Act 1997

b. British Insulated & Helsby Cables

Application: It is the right of the individual taxpayer to claim for their permissible deduction

from their incurred cost under “Section 8-1 of the Income Tax Assessment Act 1997”. In

“Section 8-1 of the Income Tax Assessment Act 1997”, it is mentioned that the cost incurred

for moving machinery will be applicable for permissible deduction in case the taxpayer uses the

machinery for generating taxable income (Tiley & Barbara Abraham 2013). In the present case,

the cost to move the machinery to a new site will not be applicable for allowable deduction as

this process increased the cost of the machinery.

From the case of British Insulated & Helsby Cables”, the fact is visible that the

transportation cost incurred in the shifting of the depreciable asset provided the business with

constant extra benefits. In this situation, “Taxation ruling of TD 92/126” describes the fact that

the installation of machinery and starting functions of its will be considered for cost when it is

done for the revenue generation. In case of the present scenario, the cost involved with the

moving of machinery to a new site is capital expenditure and thus is not under allowable

deduction (Kenny 2013).

2TAXATION LAW

Conclusion: Thus, based on the above discussion, it can be concluded that as per “Section 8-1

of the Income Tax Assessment Act 1997”, the cost to move the machinery will not be subject

to allowable deduction as it is a capital expenditure.

Requirement 2

Issue: The issue is related with the revaluation of assets that affects the insurance cover. It needs

to be determined that whether the cost to revaluation is applicable for allowable deduction as per

“Section 8-1 of the Income Tax Assessment Act 1997”.

Regulations: The relevant regulation is “Section 8-1 of the Income Tax Assessment Act

1997”.

Application: From the provided information about the case, it can be seen that the cost is

generated out of the revaluation of the assets and this cost affects the insurance cover. It needs to

be mentioned that this cost of revelation of assets will be applicable for allowable deduction as

this particular cost of occurred repetitively under “Section 8-1 of the Income Tax Assessment

Act 1997” (Martin 2015). Apart from this fact, it needs to be mentioned that the asset

revaluation cost that can affect the insurance cover has direct relation with the fixed assets. It is

required for the taxpayer at the time to compute the tax return to determine the deductible nature

of the expenditure. More precisely, it needs to be ascertained that whether the revaluation cost of

the assets occurred due to the generation of taxable income of it is occurred in order to safeguard

the assets. In case of this particular situation, the revaluation cost of the machinery contributed to

the temporary benefit of the company and this particular cost is repetitive in nature. For this

reason, this revaluation cost of assets will be applicable for permissible deduction under

“Section 8-1 of the Income Tax Assessment Act 1997” (Bevacqua 2015).

Conclusion: Thus, based on the above discussion, it can be concluded that as per “Section 8-1

of the Income Tax Assessment Act 1997”, the cost to move the machinery will not be subject

to allowable deduction as it is a capital expenditure.

Requirement 2

Issue: The issue is related with the revaluation of assets that affects the insurance cover. It needs

to be determined that whether the cost to revaluation is applicable for allowable deduction as per

“Section 8-1 of the Income Tax Assessment Act 1997”.

Regulations: The relevant regulation is “Section 8-1 of the Income Tax Assessment Act

1997”.

Application: From the provided information about the case, it can be seen that the cost is

generated out of the revaluation of the assets and this cost affects the insurance cover. It needs to

be mentioned that this cost of revelation of assets will be applicable for allowable deduction as

this particular cost of occurred repetitively under “Section 8-1 of the Income Tax Assessment

Act 1997” (Martin 2015). Apart from this fact, it needs to be mentioned that the asset

revaluation cost that can affect the insurance cover has direct relation with the fixed assets. It is

required for the taxpayer at the time to compute the tax return to determine the deductible nature

of the expenditure. More precisely, it needs to be ascertained that whether the revaluation cost of

the assets occurred due to the generation of taxable income of it is occurred in order to safeguard

the assets. In case of this particular situation, the revaluation cost of the machinery contributed to

the temporary benefit of the company and this particular cost is repetitive in nature. For this

reason, this revaluation cost of assets will be applicable for permissible deduction under

“Section 8-1 of the Income Tax Assessment Act 1997” (Bevacqua 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Conclusion: As per the above discussion, it can be seen that the revaluation cots of the assets is

repetitive in nature that occurs frequently. Thus, it can be concluded that this particular cost will

be subject to allowable deduction as per “Section 8-1 of the Income Tax Assessment Act

1997”.

Requirement 3

Issue: This particular case puts emphasis on the fact that whether legal expenses to oppose

winding up of business are applicable for permissible deduction or not under “Section 8-1 of the

Income Tax Assessment Act 1997”.

Regulations: Followings are the required legislations:

a. Section 8-1 of the Income Tax Assessment Act 1997

b. FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)

Application: In “Section 8-1 of the Income Tax Assessment Act 1997”, the fact is described

that the cost to winding up of the businesses is considered as business expenditures for the reason

of its derivation from business operation and thus, this cost will not be applicable for permissible

deduction. In this situation, it is described in “Taxation ruling of ID 2004/367” that the amount

of expenses incurred at the time to discharge the business operations legally needs to be

considered for permissible deduction (Middleton 2015). This expense will be considered for

allowable deduction as it is occurred at the time of revenue generation.

As per the verdict in “FC of T v Snowden and Wilson Pty Ltd (1958)”, it can be said

that the expenditure that is not usual for the taxpayer and the taxpayer has not occurred these

types of expenditures before will not be applicable for allowable deduction (Pagura 2014). In the

provided case, the legal expenses occurred to oppose the winding up of business would not be

Conclusion: As per the above discussion, it can be seen that the revaluation cots of the assets is

repetitive in nature that occurs frequently. Thus, it can be concluded that this particular cost will

be subject to allowable deduction as per “Section 8-1 of the Income Tax Assessment Act

1997”.

Requirement 3

Issue: This particular case puts emphasis on the fact that whether legal expenses to oppose

winding up of business are applicable for permissible deduction or not under “Section 8-1 of the

Income Tax Assessment Act 1997”.

Regulations: Followings are the required legislations:

a. Section 8-1 of the Income Tax Assessment Act 1997

b. FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)

Application: In “Section 8-1 of the Income Tax Assessment Act 1997”, the fact is described

that the cost to winding up of the businesses is considered as business expenditures for the reason

of its derivation from business operation and thus, this cost will not be applicable for permissible

deduction. In this situation, it is described in “Taxation ruling of ID 2004/367” that the amount

of expenses incurred at the time to discharge the business operations legally needs to be

considered for permissible deduction (Middleton 2015). This expense will be considered for

allowable deduction as it is occurred at the time of revenue generation.

As per the verdict in “FC of T v Snowden and Wilson Pty Ltd (1958)”, it can be said

that the expenditure that is not usual for the taxpayer and the taxpayer has not occurred these

types of expenditures before will not be applicable for allowable deduction (Pagura 2014). In the

provided case, the legal expenses occurred to oppose the winding up of business would not be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

subject to allowable deduction even after the meeting of positive limbs. The reason for not

considering this cost for allowable deddduction is that this cost form the deep structure of the

business. apart from this, this particular legal cost for opposing the winding up of business is

capital expenditure.

Conclusion: Thus, based on the above discussion, it can be observed that the legal cost to

oppose the wind up petition of the business will not be considered for permissible deduction

under “Section 8-1 of the Income Tax Assessment Act 1997” as it is a capital expenditure and

forms the deep structure of the business.

Requirement 4

Issue: The issue is related with the ascertainment of allowable deduction on the legal expense of

the solicitor for various purposes under “Section 8-1 of the Income Tax Assessment Act

1997”.

Regulations: The required regulation is “Section 8-1 of the Income Tax Assessment Act

1997”.

Application: As per the provided case study, it can be seen that the legal expenses occurred

from the business activities will be subject to allowable deduction as per “Section 8-1 of the

Income Tax Assessment Act 1997” (Woellner et al. 2016). For this, the legal expenses must be

occurred for the generation of assessable income. In this case, it needs to be mentioned that the

legal expenses of the taxpayers that are capital expenditure and are personal as well as domestic

in nature will not be applicable for allowable deduction and they are non-exempted income.

Thus, from the above analysis, it can be seen that the legal expenses occurred by the

taxpayer that do not fall under the purview of the business activities would not be applicable for

subject to allowable deduction even after the meeting of positive limbs. The reason for not

considering this cost for allowable deddduction is that this cost form the deep structure of the

business. apart from this, this particular legal cost for opposing the winding up of business is

capital expenditure.

Conclusion: Thus, based on the above discussion, it can be observed that the legal cost to

oppose the wind up petition of the business will not be considered for permissible deduction

under “Section 8-1 of the Income Tax Assessment Act 1997” as it is a capital expenditure and

forms the deep structure of the business.

Requirement 4

Issue: The issue is related with the ascertainment of allowable deduction on the legal expense of

the solicitor for various purposes under “Section 8-1 of the Income Tax Assessment Act

1997”.

Regulations: The required regulation is “Section 8-1 of the Income Tax Assessment Act

1997”.

Application: As per the provided case study, it can be seen that the legal expenses occurred

from the business activities will be subject to allowable deduction as per “Section 8-1 of the

Income Tax Assessment Act 1997” (Woellner et al. 2016). For this, the legal expenses must be

occurred for the generation of assessable income. In this case, it needs to be mentioned that the

legal expenses of the taxpayers that are capital expenditure and are personal as well as domestic

in nature will not be applicable for allowable deduction and they are non-exempted income.

Thus, from the above analysis, it can be seen that the legal expenses occurred by the

taxpayer that do not fall under the purview of the business activities would not be applicable for

5TAXATION LAW

permissible deduction. In case of the provided case study, it can be seen that the legal expenses

of the solicitors for various purpose are associated with the business activities and the generation

of taxable income will be treated as permissible deduction under “Section 8-1 of the Income

Tax Assessment Act 1997” (Barkoczy 2016).

Conclusion: From the above discussion, it can be concluded that the legal expenses of solicitor

for various purpose are related with the business operations of the company and thus, these

expenses will be allowable for permissible deduction as per “Section 8-1 of the Income Tax

Assessment Act 1997”.

Answer to Question 2

Issue: The issue is related with the determination of input tax credit of Big Bank Limited related

with the advertisement expenses under “GST Act 1999”.

Regulations: Followings are the required legislations:

a. Goods and Service taxation ruling of GSTR 2006/3

b. Ronpibon Tin NL v. FC of T

c. GST Act 1999

d. paragraphs 11-5 and 15-5

e. subsection 15-25

Application: In the ruling of “Goods and Service Act 1999”, it is stated that the business

organizations are eligible to claim their input tax credit on the expenses generated out of the

ordinary course of business, but the expenses need to be inclusive of GST. As per the provided

case study, Big Bank Limited provides various financial services and the company has more 50

permissible deduction. In case of the provided case study, it can be seen that the legal expenses

of the solicitors for various purpose are associated with the business activities and the generation

of taxable income will be treated as permissible deduction under “Section 8-1 of the Income

Tax Assessment Act 1997” (Barkoczy 2016).

Conclusion: From the above discussion, it can be concluded that the legal expenses of solicitor

for various purpose are related with the business operations of the company and thus, these

expenses will be allowable for permissible deduction as per “Section 8-1 of the Income Tax

Assessment Act 1997”.

Answer to Question 2

Issue: The issue is related with the determination of input tax credit of Big Bank Limited related

with the advertisement expenses under “GST Act 1999”.

Regulations: Followings are the required legislations:

a. Goods and Service taxation ruling of GSTR 2006/3

b. Ronpibon Tin NL v. FC of T

c. GST Act 1999

d. paragraphs 11-5 and 15-5

e. subsection 15-25

Application: In the ruling of “Goods and Service Act 1999”, it is stated that the business

organizations are eligible to claim their input tax credit on the expenses generated out of the

ordinary course of business, but the expenses need to be inclusive of GST. As per the provided

case study, Big Bank Limited provides various financial services and the company has more 50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

branches countrywide. Along with providing loans and deposits, Big Bank also provides the

services of insurance and home content. All the regulations and guidelines related to the

procedures and implementation of input tax credit of the companies are described in “Goods and

Service Taxation Ruling of GSTR 2006/3” (Campbell 2016).

The ruling of “Division 11-15 and 129 of the GST Act 1999” includes the extent of

creditable purpose and original implementation (Braithwaite 2017). This ruling is applicable for

taxable entities. In addition, this ruling is applicable for the business entities that are registered

under income tax or about to be registered for the acquisition of financial supplies that have

already crossed the limit of financial acquisition and they are within the range of input tax credit

or lower input tax credit.

The provided case study includes the case of Big Bank Limited that has an advertisement

expenses inclusive of GST. For this reason, the GST ruling of “GSTR 2006/3” can be applied in

the case of Big Bank. This is because of the eligibility of Big Bank for claiming input tax credit.

As per the ruling of “GSTR 2006/3”, in case an organization is registered for taxation and is

eligible for the registration, then the organization needs to pay the amount of GST on the

financial supplies they made (Davis et al. 2015). Thus, it can be said that the GST ruling

provides the taxable entities the right to bring forward the claim for input tax credit related with

the financial supplies and that is inclusive of GST. In case, the business organizations make

financial supplies and the amount of financial supplies crosses the limit for prescribed financial

supplies, then these business organizations will not be able to bring forward their claims for input

tax credit under GST ruling. However, they are able to recover some part of the input tax claim.

branches countrywide. Along with providing loans and deposits, Big Bank also provides the

services of insurance and home content. All the regulations and guidelines related to the

procedures and implementation of input tax credit of the companies are described in “Goods and

Service Taxation Ruling of GSTR 2006/3” (Campbell 2016).

The ruling of “Division 11-15 and 129 of the GST Act 1999” includes the extent of

creditable purpose and original implementation (Braithwaite 2017). This ruling is applicable for

taxable entities. In addition, this ruling is applicable for the business entities that are registered

under income tax or about to be registered for the acquisition of financial supplies that have

already crossed the limit of financial acquisition and they are within the range of input tax credit

or lower input tax credit.

The provided case study includes the case of Big Bank Limited that has an advertisement

expenses inclusive of GST. For this reason, the GST ruling of “GSTR 2006/3” can be applied in

the case of Big Bank. This is because of the eligibility of Big Bank for claiming input tax credit.

As per the ruling of “GSTR 2006/3”, in case an organization is registered for taxation and is

eligible for the registration, then the organization needs to pay the amount of GST on the

financial supplies they made (Davis et al. 2015). Thus, it can be said that the GST ruling

provides the taxable entities the right to bring forward the claim for input tax credit related with

the financial supplies and that is inclusive of GST. In case, the business organizations make

financial supplies and the amount of financial supplies crosses the limit for prescribed financial

supplies, then these business organizations will not be able to bring forward their claims for input

tax credit under GST ruling. However, they are able to recover some part of the input tax claim.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

The verdict in the case of “Ronpibon Tin NL v FC of T” contains the aspects of ‘extent’

and ‘to the extent’ that can be applied in the ruling of GST (Burkhauser, Hahn and Wilkins

2015). This particular ruling provides the taxpayers with the fair and reasonable methods for the

computation of GST for the firms. The ruling under “Para 11-5 and 15-5” states that the

creditable acquisition need to be partly or fully for the qualification of these acquisitions as

creditable purpose. Other kinds of regulations can be seen to make an acquisition for creditable

purpose under the ruling of “Para 11-5 and 15-5”. It needs to be mentioned that the financial

acquisition needs to be entirely creditable (Daley and Coates 2015). As per this rule, for the

partial creditable purpose acquisitions, it is needed for them to mention the degree of partial

acquisition. In addition, in case an acquisition is found to be partial creditable purpose, they must

be considered as entirely creditable. “Section 11-5 and 15-10” states that the financial

acquisition needs to be considered as creditable acquisition in case the amount of financial

supplies includes the amount of input tax credit. In case of Big Bank Limited, the advertisement

expenses of the company are related with creditable purpose. As per “GSTR ruling of 2000/3”,

Big Bank has crossed the limit of financial acquisition and thus, the company is eligible for input

tax credit under GST act (Cao et al. 2015).

Conclusion: Thus, based on the above discussion, it can be said that Big Bank is eligible for the

claiming of input tax credit on the advertisement expenses under “GSTR ruling of 2000/3”.

The verdict in the case of “Ronpibon Tin NL v FC of T” contains the aspects of ‘extent’

and ‘to the extent’ that can be applied in the ruling of GST (Burkhauser, Hahn and Wilkins

2015). This particular ruling provides the taxpayers with the fair and reasonable methods for the

computation of GST for the firms. The ruling under “Para 11-5 and 15-5” states that the

creditable acquisition need to be partly or fully for the qualification of these acquisitions as

creditable purpose. Other kinds of regulations can be seen to make an acquisition for creditable

purpose under the ruling of “Para 11-5 and 15-5”. It needs to be mentioned that the financial

acquisition needs to be entirely creditable (Daley and Coates 2015). As per this rule, for the

partial creditable purpose acquisitions, it is needed for them to mention the degree of partial

acquisition. In addition, in case an acquisition is found to be partial creditable purpose, they must

be considered as entirely creditable. “Section 11-5 and 15-10” states that the financial

acquisition needs to be considered as creditable acquisition in case the amount of financial

supplies includes the amount of input tax credit. In case of Big Bank Limited, the advertisement

expenses of the company are related with creditable purpose. As per “GSTR ruling of 2000/3”,

Big Bank has crossed the limit of financial acquisition and thus, the company is eligible for input

tax credit under GST act (Cao et al. 2015).

Conclusion: Thus, based on the above discussion, it can be said that Big Bank is eligible for the

claiming of input tax credit on the advertisement expenses under “GSTR ruling of 2000/3”.

8TAXATION LAW

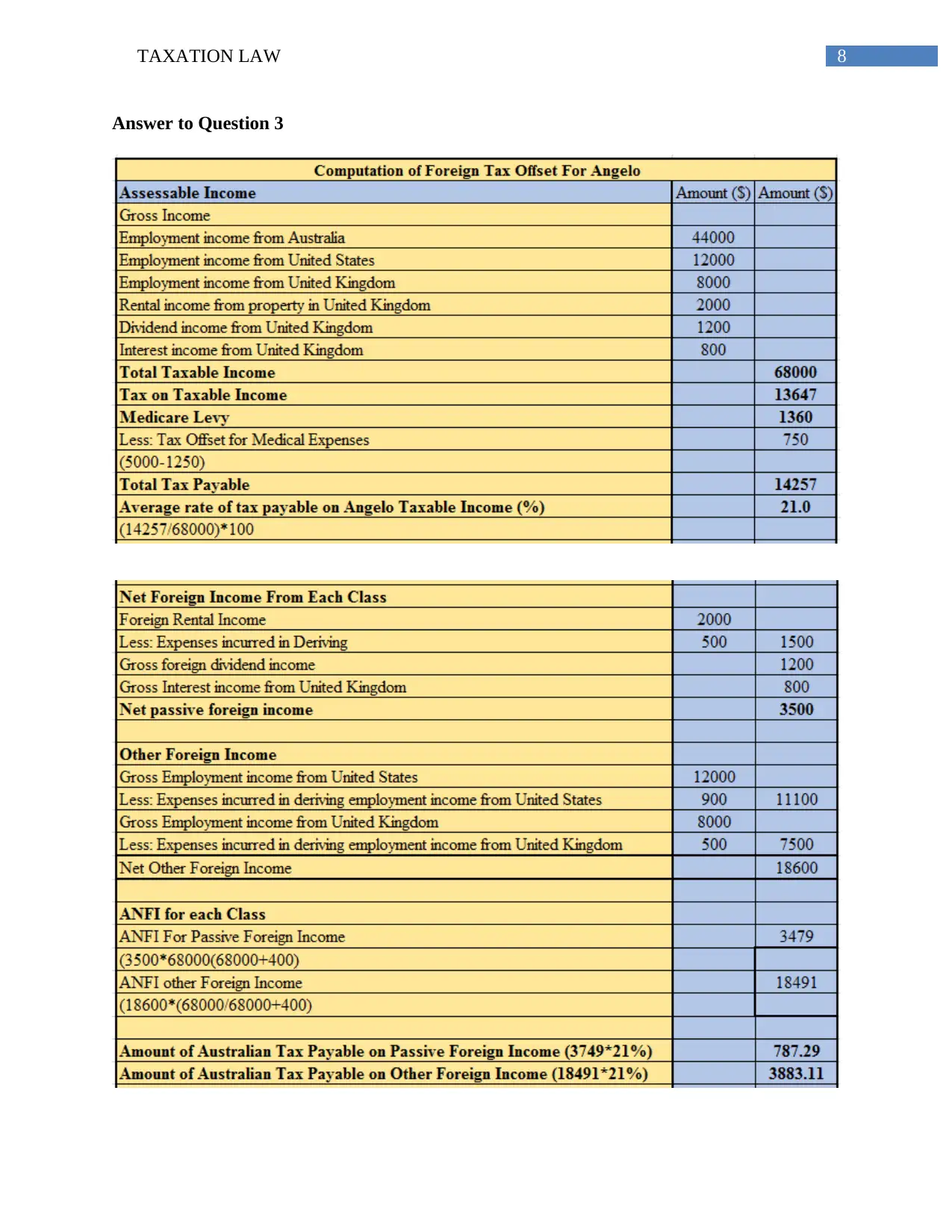

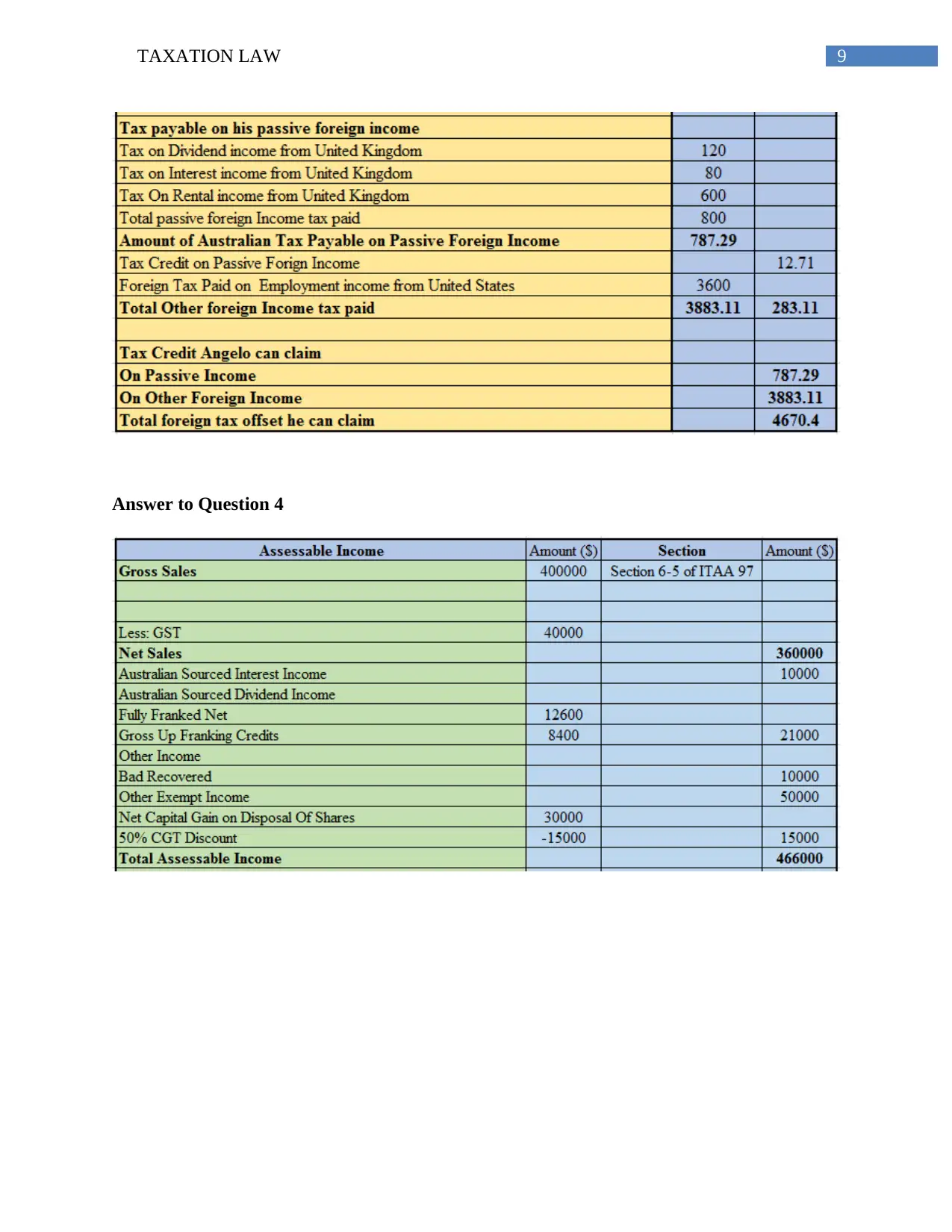

Answer to Question 3

Answer to Question 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

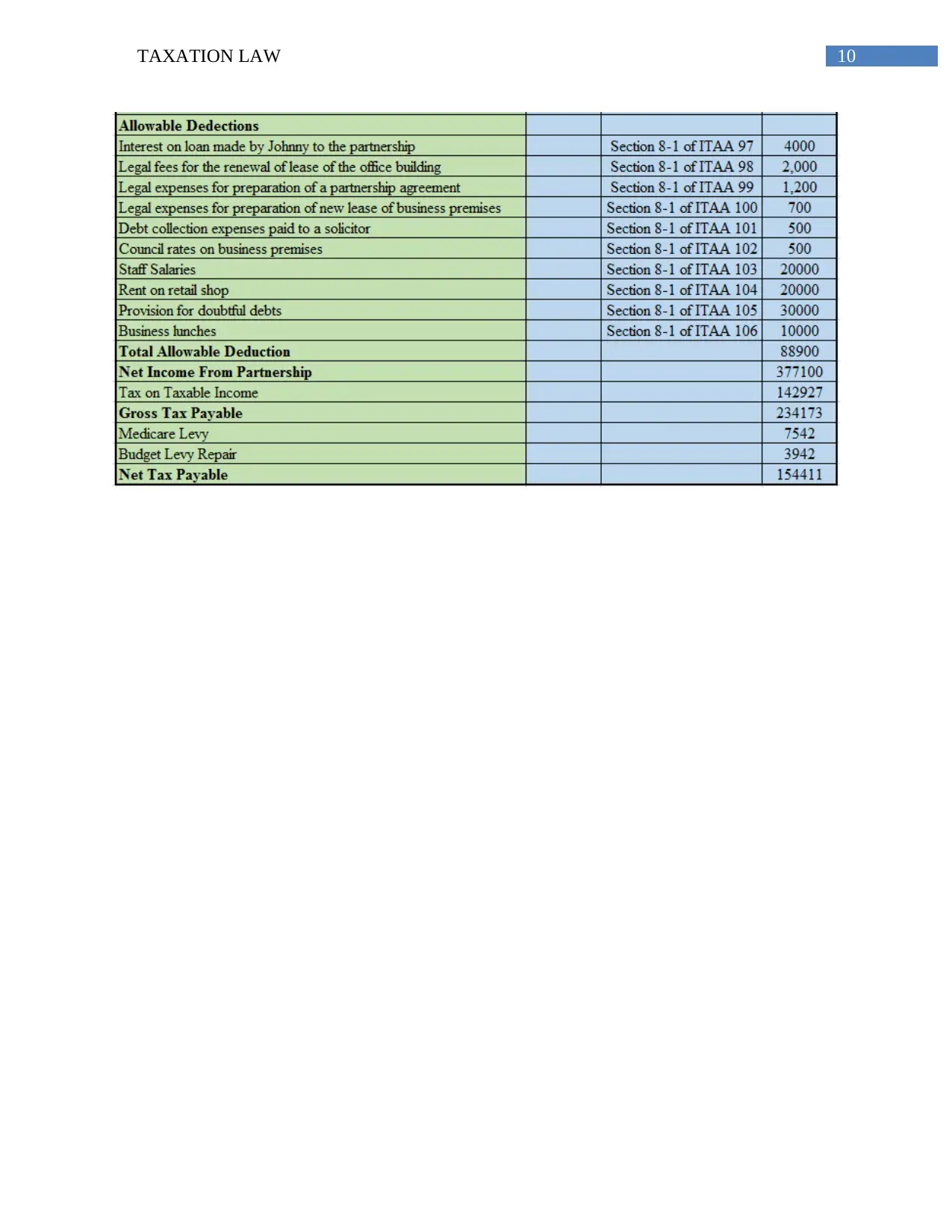

Answer to Question 4

Answer to Question 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

11TAXATION LAW

References

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Bevacqua, John, 2015. ATO accountability and taxpayer fairness: An assessment of the proposal

to split the Australian taxation office. University of New South Wales Law Journal, The, 38(3),

pp.995–1014.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Campbell, T.D., 2016. The legal theory of ethical positivism. Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and Wende,

S., 2015. Understanding the economy-wide efficiency and incidence of major Australian

taxes. Treasury WP, 1.

Daley, J. and Coates, B., 2015. Property taxes. Grattan Institute.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), pp.47-68.

Kenny, P., 2013. Australian tax 2013 10th ed.]., Chatswood, N.S.W.: LexisNexis Butterworths.

Martin, F., 2015. Has the Charities Act 2013 changed the common law concept of charitable

"public benefit" and, if so, how? Australian Tax Forum, 30(1), pp.65–87.

References

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Bevacqua, John, 2015. ATO accountability and taxpayer fairness: An assessment of the proposal

to split the Australian taxation office. University of New South Wales Law Journal, The, 38(3),

pp.995–1014.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Campbell, T.D., 2016. The legal theory of ethical positivism. Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and Wende,

S., 2015. Understanding the economy-wide efficiency and incidence of major Australian

taxes. Treasury WP, 1.

Daley, J. and Coates, B., 2015. Property taxes. Grattan Institute.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), pp.47-68.

Kenny, P., 2013. Australian tax 2013 10th ed.]., Chatswood, N.S.W.: LexisNexis Butterworths.

Martin, F., 2015. Has the Charities Act 2013 changed the common law concept of charitable

"public benefit" and, if so, how? Australian Tax Forum, 30(1), pp.65–87.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.