Assignment On Taxation Theory ,Practice & Law

11 Pages3388 Words466 Views

Added on 2020-10-05

Assignment On Taxation Theory ,Practice & Law

Added on 2020-10-05

ShareRelated Documents

TAXATION THEORY, PRACTICE& LAW

Table of ContentsINTRODUCTION...........................................................................................................................1QUESTION 1...................................................................................................................................1a) Block of land...........................................................................................................................1b) Antique bed.............................................................................................................................2c) Painting...................................................................................................................................3d) Shares......................................................................................................................................4e) Violin......................................................................................................................................5QUESTION 2...................................................................................................................................6a) Suggestion regarding consequences while calculating FBT...................................................6b) Changes in answer if purchase $50000 of the shares............................................................8CONCLUSION................................................................................................................................8REFERENCES................................................................................................................................9

INTRODUCTION Tax is considered as a financial liability to be paid by individual to government, which isutilised further to fulfil the public expenditure and projects. Taxation office of the governedauthority that provides rules and legislations related to tax collection, determining the taxliability and finance charge for a particular time period (Burton, 2012). this report is divided inmajor two parts in first part taxable criteria and calculations subject to capital gain or losses aremade for Mayfield firm as a tax consultant. Second part contains the analysis of assessable tax for Rapid heat Pty Ltd an electricheater manufacturer firm. A study on Fringe benefit tax is critically evaluated to attain tax credit.Suggestions are provided in respect of consequences while calculating the tax liabilities fordifferent case scenarios and transactions. There are some transactions are given to determine thetax accessibility and determine the total tax liability are considered in this report.QUESTION 1There are type of taxation rules are formed in Australia to ascertain the tax liability. Asan tax consultant of the region, advises and recommendations are asked and relate with the lawsform with the organisation. Diverse taxation rules and policies related to income tax and otherlaws are considered viable for addressing public expenditure requirements (Tricker and Tricker,2015). Solutions and remedies provided for treatment of different monetary and non monetarytransactions with in and outside the organisation. a) Block of landCase study: As an tax consultant in Mafirld, New south Wales, it is required to analysethe transaction of block of land. On 3 June of the current tax year a contract of sale of block ofland was considered that contains cost of $320000 for block f land. The cost of acquisition inJanuary was $100000 and cost was incurred as $20000 in local council, water and sewerage ratesas deposit. A capital gain would be occurred in this case and a taxable amount will be paid byclient for current assessment year. Rules and legislations related to tax: In the above case, it is determined that the capitalgain will be payable to the government of the Australia by the assesses. Block of land will becountable as an immovable property owned by the organisation or individual as an investment orfor residential purpose (Capital gain tax. 2018). In the above case the block of land acquired1

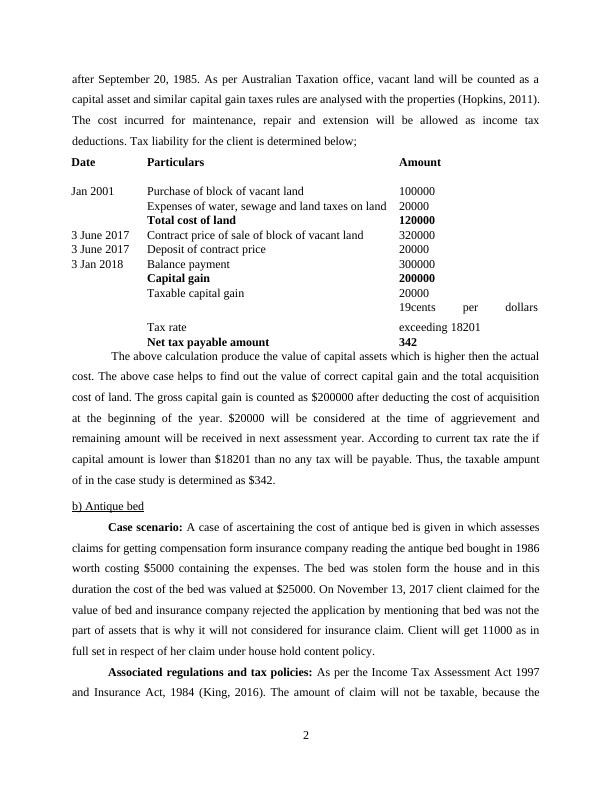

after September 20, 1985. As per Australian Taxation office, vacant land will be counted as acapital asset and similar capital gain taxes rules are analysed with the properties (Hopkins, 2011).The cost incurred for maintenance, repair and extension will be allowed as income taxdeductions. Tax liability for the client is determined below;DateParticularsAmountJan 2001Purchase of block of vacant land100000Expenses of water, sewage and land taxes on land20000Total cost of land 1200003 June 2017Contract price of sale of block of vacant land3200003 June 2017Deposit of contract price200003 Jan 2018Balance payment 300000Capital gain 200000Taxable capital gain 20000Tax rate 19cents per dollarsexceeding 18201Net tax payable amount342 The above calculation produce the value of capital assets which is higher then the actualcost. The above case helps to find out the value of correct capital gain and the total acquisitioncost of land. The gross capital gain is counted as $200000 after deducting the cost of acquisitionat the beginning of the year. $20000 will be considered at the time of aggrievement andremaining amount will be received in next assessment year. According to current tax rate the ifcapital amount is lower than $18201 than no any tax will be payable. Thus, the taxable ampuntof in the case study is determined as $342. b) Antique bedCase scenario: A case of ascertaining the cost of antique bed is given in which assessesclaims for getting compensation form insurance company reading the antique bed bought in 1986worth costing $5000 containing the expenses. The bed was stolen form the house and in thisduration the cost of the bed was valued at $25000. On November 13, 2017 client claimed for thevalue of bed and insurance company rejected the application by mentioning that bed was not thepart of assets that is why it will not considered for insurance claim. Client will get 11000 as infull set in respect of her claim under house hold content policy.Associated regulations and tax policies: As per the Income Tax Assessment Act 1997and Insurance Act, 1984 (King, 2016). The amount of claim will not be taxable, because the2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Taxation in Theory and Practicelg...

|12

|3325

|48

Taxation Theory Practice and Lawlg...

|13

|3626

|110

(Solution) Taxation Theory, Practice & Lawlg...

|12

|3278

|377

Taxation Theory Practice and Law pdflg...

|12

|3457

|328

Taxation Theory, Practice & Lawlg...

|12

|3237

|342

Assignment on Taxation PDFlg...

|9

|2527

|19