Auditing Issues & Auditor's Responsibilities

VerifiedAdded on 2020/02/19

|11

|2704

|27

AI Summary

This assignment delves into the crucial role of auditors in detecting potential financial statement manipulation and ensuring the accuracy of reported figures. It emphasizes the importance of rigorous audit procedures in safeguarding against fraudulent activities and maintaining the integrity of financial reporting. The discussion highlights the challenges auditors face when dealing with flawed accounting systems and inadequate evidence, emphasizing the need for professional judgment and skillful execution of audit processes.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDITING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing

Answer to 1

In relation to decision-making, analytical processes can prove to be of significant value to both

the management and the auditor. Besides, not only financial decisions but also non-financial

decisions can be taken with the help of analytical processes. In the given case of DIPL Ltd, such

analytical processes have been performed in order to highlight the true performance of the

company and thereafter, make decisions based on the same. Moreover, if there are any material

misstatements forming part of the company’s financials, implementation of such processes can

assist in identifying the same in order to safeguard any fraudulent affairs (Church et. al, 2008).

Nevertheless, based on the background information of the company, such processes can be

performed in order to achieve the intended results.

The first analytical process conducted in relation to DIPL Ltd is an analysis of its trends. In this

process, the financial information forming part of the company’s financials is compared with the

last year figures so that variations can be identified, thereby resulting in effective decision-

making. In simple words, the patterns or trends can be taken into account for making relevant

decisions (Heeler, 2009). Besides, reasons behind major differences in the trends can be easily

evaluated so that future complications can be prevented. Nevertheless, from the financials of

DIPL Ltd, it can be identified that there was a massive enhancement in the sale figures of the

company that is a good indicator in terms of performance. However, one important consideration

must be noticed in this scenario. If the sale figures are compared with the underlying stocks of

the company, it can be seen that the difference is huge despite such enhanced sales. This

becomes a matter of issue for the company, as the stocks must have declined owing to

enhancement in the sale figures. Hence, the auditor must evaluate such trend to find the reason

behind inflation of stocks even though the company achieved greater sales (Johnstone et. al,

2014).

In the second process, evaluation of ratios has been conducted in order to ascertain the true

financial position of the company. For such purpose, various ratios can be calculated and

compared with that of the last years in order to find the true nature of the company’s operations.

Based on the trend and profitability of DIPL Ltd, solvency, liquidity, and profitability ratios can

prove to of immense importance. Liquidity ratios will assist in determining the liquidity position

of the company whether it is able to repay its obligations, Solvency ratios will assist in

Answer to 1

In relation to decision-making, analytical processes can prove to be of significant value to both

the management and the auditor. Besides, not only financial decisions but also non-financial

decisions can be taken with the help of analytical processes. In the given case of DIPL Ltd, such

analytical processes have been performed in order to highlight the true performance of the

company and thereafter, make decisions based on the same. Moreover, if there are any material

misstatements forming part of the company’s financials, implementation of such processes can

assist in identifying the same in order to safeguard any fraudulent affairs (Church et. al, 2008).

Nevertheless, based on the background information of the company, such processes can be

performed in order to achieve the intended results.

The first analytical process conducted in relation to DIPL Ltd is an analysis of its trends. In this

process, the financial information forming part of the company’s financials is compared with the

last year figures so that variations can be identified, thereby resulting in effective decision-

making. In simple words, the patterns or trends can be taken into account for making relevant

decisions (Heeler, 2009). Besides, reasons behind major differences in the trends can be easily

evaluated so that future complications can be prevented. Nevertheless, from the financials of

DIPL Ltd, it can be identified that there was a massive enhancement in the sale figures of the

company that is a good indicator in terms of performance. However, one important consideration

must be noticed in this scenario. If the sale figures are compared with the underlying stocks of

the company, it can be seen that the difference is huge despite such enhanced sales. This

becomes a matter of issue for the company, as the stocks must have declined owing to

enhancement in the sale figures. Hence, the auditor must evaluate such trend to find the reason

behind inflation of stocks even though the company achieved greater sales (Johnstone et. al,

2014).

In the second process, evaluation of ratios has been conducted in order to ascertain the true

financial position of the company. For such purpose, various ratios can be calculated and

compared with that of the last years in order to find the true nature of the company’s operations.

Based on the trend and profitability of DIPL Ltd, solvency, liquidity, and profitability ratios can

prove to of immense importance. Liquidity ratios will assist in determining the liquidity position

of the company whether it is able to repay its obligations, Solvency ratios will assist in

Auditing

ascertaining whether there is a proper balance in the capital structure of the company,

profitability ratios focuses on the revenues attained by the company.

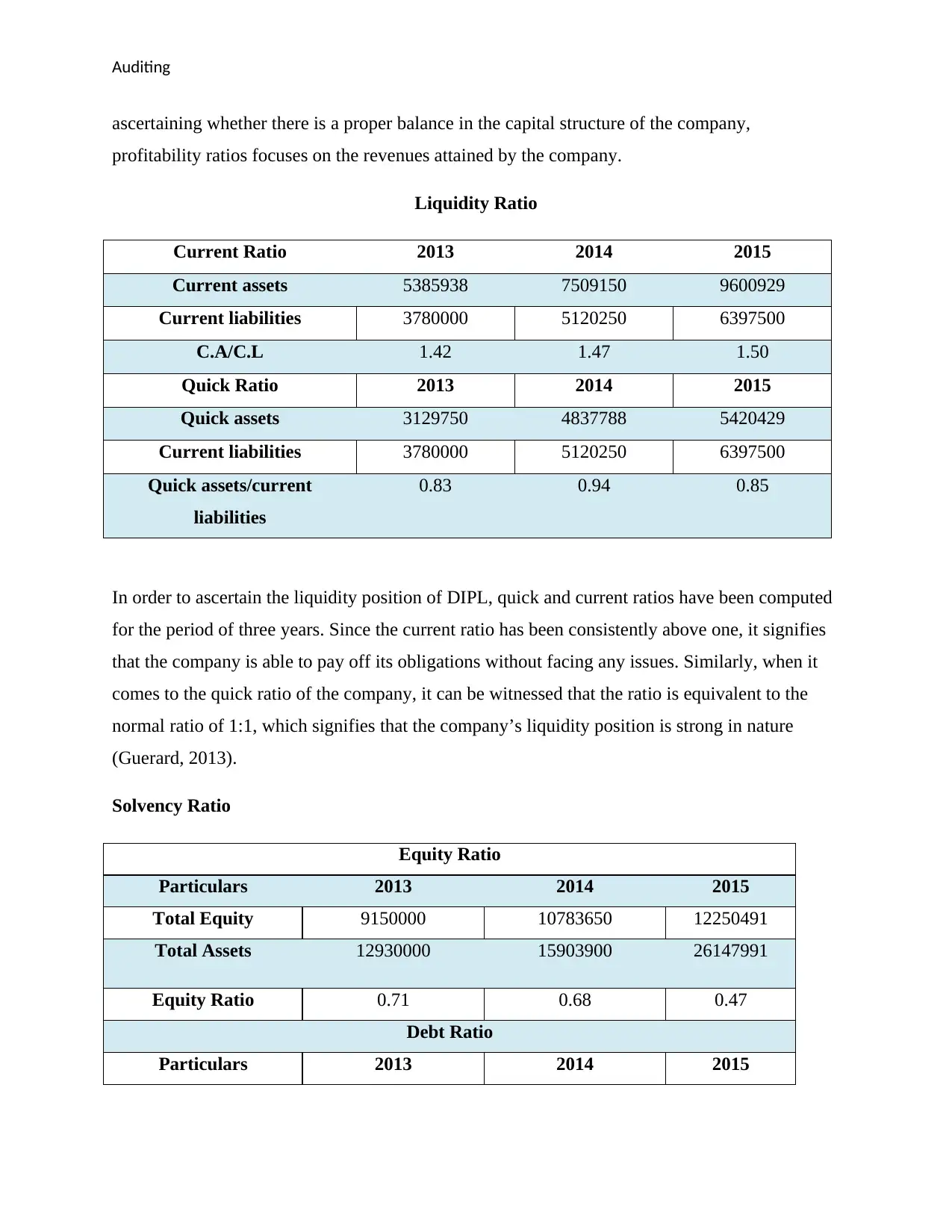

Liquidity Ratio

Current Ratio 2013 2014 2015

Current assets 5385938 7509150 9600929

Current liabilities 3780000 5120250 6397500

C.A/C.L 1.42 1.47 1.50

Quick Ratio 2013 2014 2015

Quick assets 3129750 4837788 5420429

Current liabilities 3780000 5120250 6397500

Quick assets/current

liabilities

0.83 0.94 0.85

In order to ascertain the liquidity position of DIPL, quick and current ratios have been computed

for the period of three years. Since the current ratio has been consistently above one, it signifies

that the company is able to pay off its obligations without facing any issues. Similarly, when it

comes to the quick ratio of the company, it can be witnessed that the ratio is equivalent to the

normal ratio of 1:1, which signifies that the company’s liquidity position is strong in nature

(Guerard, 2013).

Solvency Ratio

Equity Ratio

Particulars 2013 2014 2015

Total Equity 9150000 10783650 12250491

Total Assets 12930000 15903900 26147991

Equity Ratio 0.71 0.68 0.47

Debt Ratio

Particulars 2013 2014 2015

ascertaining whether there is a proper balance in the capital structure of the company,

profitability ratios focuses on the revenues attained by the company.

Liquidity Ratio

Current Ratio 2013 2014 2015

Current assets 5385938 7509150 9600929

Current liabilities 3780000 5120250 6397500

C.A/C.L 1.42 1.47 1.50

Quick Ratio 2013 2014 2015

Quick assets 3129750 4837788 5420429

Current liabilities 3780000 5120250 6397500

Quick assets/current

liabilities

0.83 0.94 0.85

In order to ascertain the liquidity position of DIPL, quick and current ratios have been computed

for the period of three years. Since the current ratio has been consistently above one, it signifies

that the company is able to pay off its obligations without facing any issues. Similarly, when it

comes to the quick ratio of the company, it can be witnessed that the ratio is equivalent to the

normal ratio of 1:1, which signifies that the company’s liquidity position is strong in nature

(Guerard, 2013).

Solvency Ratio

Equity Ratio

Particulars 2013 2014 2015

Total Equity 9150000 10783650 12250491

Total Assets 12930000 15903900 26147991

Equity Ratio 0.71 0.68 0.47

Debt Ratio

Particulars 2013 2014 2015

Auditing

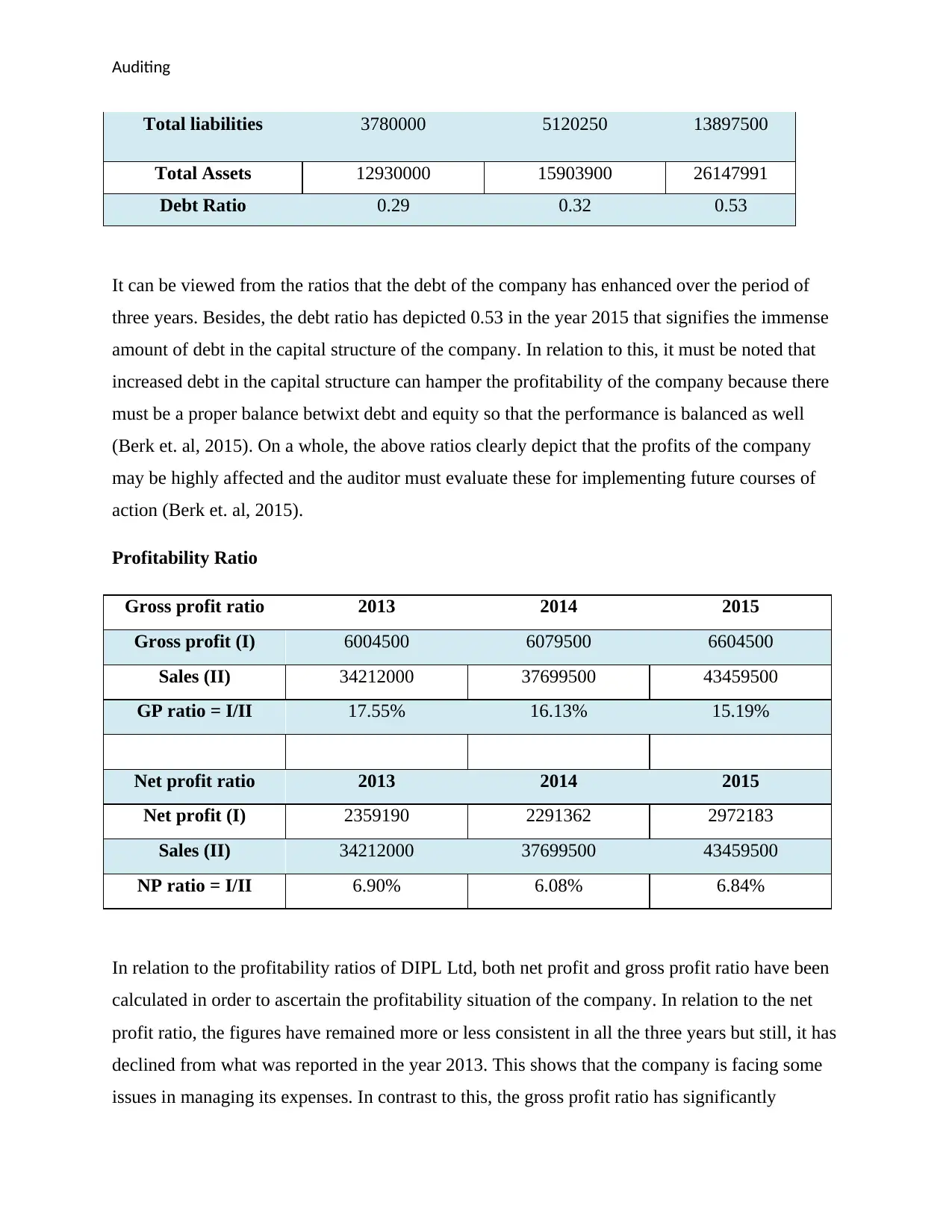

Total liabilities 3780000 5120250 13897500

Total Assets 12930000 15903900 26147991

Debt Ratio 0.29 0.32 0.53

It can be viewed from the ratios that the debt of the company has enhanced over the period of

three years. Besides, the debt ratio has depicted 0.53 in the year 2015 that signifies the immense

amount of debt in the capital structure of the company. In relation to this, it must be noted that

increased debt in the capital structure can hamper the profitability of the company because there

must be a proper balance betwixt debt and equity so that the performance is balanced as well

(Berk et. al, 2015). On a whole, the above ratios clearly depict that the profits of the company

may be highly affected and the auditor must evaluate these for implementing future courses of

action (Berk et. al, 2015).

Profitability Ratio

Gross profit ratio 2013 2014 2015

Gross profit (I) 6004500 6079500 6604500

Sales (II) 34212000 37699500 43459500

GP ratio = I/II 17.55% 16.13% 15.19%

Net profit ratio 2013 2014 2015

Net profit (I) 2359190 2291362 2972183

Sales (II) 34212000 37699500 43459500

NP ratio = I/II 6.90% 6.08% 6.84%

In relation to the profitability ratios of DIPL Ltd, both net profit and gross profit ratio have been

calculated in order to ascertain the profitability situation of the company. In relation to the net

profit ratio, the figures have remained more or less consistent in all the three years but still, it has

declined from what was reported in the year 2013. This shows that the company is facing some

issues in managing its expenses. In contrast to this, the gross profit ratio has significantly

Total liabilities 3780000 5120250 13897500

Total Assets 12930000 15903900 26147991

Debt Ratio 0.29 0.32 0.53

It can be viewed from the ratios that the debt of the company has enhanced over the period of

three years. Besides, the debt ratio has depicted 0.53 in the year 2015 that signifies the immense

amount of debt in the capital structure of the company. In relation to this, it must be noted that

increased debt in the capital structure can hamper the profitability of the company because there

must be a proper balance betwixt debt and equity so that the performance is balanced as well

(Berk et. al, 2015). On a whole, the above ratios clearly depict that the profits of the company

may be highly affected and the auditor must evaluate these for implementing future courses of

action (Berk et. al, 2015).

Profitability Ratio

Gross profit ratio 2013 2014 2015

Gross profit (I) 6004500 6079500 6604500

Sales (II) 34212000 37699500 43459500

GP ratio = I/II 17.55% 16.13% 15.19%

Net profit ratio 2013 2014 2015

Net profit (I) 2359190 2291362 2972183

Sales (II) 34212000 37699500 43459500

NP ratio = I/II 6.90% 6.08% 6.84%

In relation to the profitability ratios of DIPL Ltd, both net profit and gross profit ratio have been

calculated in order to ascertain the profitability situation of the company. In relation to the net

profit ratio, the figures have remained more or less consistent in all the three years but still, it has

declined from what was reported in the year 2013. This shows that the company is facing some

issues in managing its expenses. In contrast to this, the gross profit ratio has significantly

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing

decreased over the years that signify issues in the management of cost of sales of the company

(Guerard, 2013). Therefore, the auditor must evaluate this scenario so that better decisions can be

implemented based on this information. In addition, corrective actions are very important in this

scenario so that the company does not deteriorate its entire resource base.

decreased over the years that signify issues in the management of cost of sales of the company

(Guerard, 2013). Therefore, the auditor must evaluate this scenario so that better decisions can be

implemented based on this information. In addition, corrective actions are very important in this

scenario so that the company does not deteriorate its entire resource base.

Auditing

Answer to 2

In relation to inherent risks, such risks cannot be easily rid of because they will be present in the

financials of a company. Besides, internal control policies and audit processes also cannot

restrict the prevalence of such risks. This is because of the fact that such risks do not depend on

any material misstatement or error. The inherent risks prevailing in the financials of DIPL Ltd

are as follows:

Immoral appointment standards

In relation to the appointment of an executive, it must be noted that a person who does not

possess any kind of interest within the company must undertake the appointment. Therefore,

when it comes to the appointment of CEO in DIPL Ltd, the person undertaking the appointment

must not possess any financial interest with the company. However, the contrary has been

witnessed in the case of the company. It has happened that the company’s CEO can obtain a ten

percent share of the profits if the company witnesses a growth of ten percent or more in its

operations. This poses a very big threat to the company because the CEO is in a position wherein

he can manipulate the business affairs in a way that can grant him the agreed share in profits

(Matthew, 2015). Besides, for such manipulation, he may even tamper the financial records in a

way that may fetch him profits even though the company has not earned revenues in reality.

Improper recording of accounts receivable

The cashier of the company records the accounts receivables on a regular basis but recognition of

the same is done through received mails. This means that he debtors enclose their cheque

through mail and the same is forwarded to the company wherein the cashier does further

recording and encashment. This signifies that the company’s policy does not have any

correlation with the adjustment of receivables and cheque encashment, thereby resulting in huge

variations. Further, a different official undertakes the job of reconciling the bank statement every

month. This depicts the fact that the company has not been following a systematic method of

recording the receivables and reconciling the same with the bank statements (Matthew, 2015).

As a result, there may be massive variations in the company’s financials and if the auditors do

not evaluate these concerns in a thorough way, he may be misguided and an incorrect judgement

Answer to 2

In relation to inherent risks, such risks cannot be easily rid of because they will be present in the

financials of a company. Besides, internal control policies and audit processes also cannot

restrict the prevalence of such risks. This is because of the fact that such risks do not depend on

any material misstatement or error. The inherent risks prevailing in the financials of DIPL Ltd

are as follows:

Immoral appointment standards

In relation to the appointment of an executive, it must be noted that a person who does not

possess any kind of interest within the company must undertake the appointment. Therefore,

when it comes to the appointment of CEO in DIPL Ltd, the person undertaking the appointment

must not possess any financial interest with the company. However, the contrary has been

witnessed in the case of the company. It has happened that the company’s CEO can obtain a ten

percent share of the profits if the company witnesses a growth of ten percent or more in its

operations. This poses a very big threat to the company because the CEO is in a position wherein

he can manipulate the business affairs in a way that can grant him the agreed share in profits

(Matthew, 2015). Besides, for such manipulation, he may even tamper the financial records in a

way that may fetch him profits even though the company has not earned revenues in reality.

Improper recording of accounts receivable

The cashier of the company records the accounts receivables on a regular basis but recognition of

the same is done through received mails. This means that he debtors enclose their cheque

through mail and the same is forwarded to the company wherein the cashier does further

recording and encashment. This signifies that the company’s policy does not have any

correlation with the adjustment of receivables and cheque encashment, thereby resulting in huge

variations. Further, a different official undertakes the job of reconciling the bank statement every

month. This depicts the fact that the company has not been following a systematic method of

recording the receivables and reconciling the same with the bank statements (Matthew, 2015).

As a result, there may be massive variations in the company’s financials and if the auditors do

not evaluate these concerns in a thorough way, he may be misguided and an incorrect judgement

Auditing

may be provided on his part. Hence, the auditors must analyze these issues and make further

judgements.

These two inherent risks are a massive problem for the company because it may not only hamper

the company’s financials but also misguide the auditors in offering an improper judgement.

Moreover, the profit figures may be badly influenced because of such risks that may hamper the

company’s goodwill in the upcoming tenure if the auditor gets hold of such fraudulent measures.

may be provided on his part. Hence, the auditors must analyze these issues and make further

judgements.

These two inherent risks are a massive problem for the company because it may not only hamper

the company’s financials but also misguide the auditors in offering an improper judgement.

Moreover, the profit figures may be badly influenced because of such risks that may hamper the

company’s goodwill in the upcoming tenure if the auditor gets hold of such fraudulent measures.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

Answer to 3(a)

Fraud risks are the risks that prevail within the company’s financials because of some fraudulent

activities are undertaken by the management or by its official. The key fraud risks in the case of

DIPL are as follows:

Inventory valuation

Based on the financial information of the company, it can be seen that its sale figures have

depicted a positive and enhanced performance over the years. However, the main area of concern

is that even though the company attained good sales over the years, yet its stock balances have

not depicted a downward trend and instead, an upward trend in stock figures can be seen. This is

a big issue for the company because the enhancement in the level of inventories must have been

done through manipulation on the part of the management or accountant so that the accounts are

tampered and it fetches good profits (Gilbert et. al 2005).

Mail revenue recognition

Since the cashier undertakes the job of encashment of the cheques attained through mail basis, it

may create many difficulties for the company. The reason behind this can be attributed to the fact

that prior verification from the bank is missing in this scenario and that can result in fraud on the

part of the management or its officials. It is therefore required prior verification from bank

statements must be undertaken so that efficacy of the transaction can be achieved. Moreover, if

such system is not in place, the officials of the company might be in a position to deport the

company’s resources and credit the same to an unwanted person’s account. This will not only

deteriorate the financial resources of the company but also hamper its financial statements.

Hence, it is required that the company must undertake proper bank reconciliation systems within

its operations so that the possibilities of fraud are minimized to the fullest (Geoffrey et. al, 2016).

Moreover, this will also result in strong corporate governance within the company because of

transparency.

Therefore, these two fraud risks pose a big threat to the company’s affairs wherein both the

management and its officials are in a position to tamper the accounts for their own benefits. As a

result, the auditor’s judgement may be deteriorated because they may not identify the fraud done

Answer to 3(a)

Fraud risks are the risks that prevail within the company’s financials because of some fraudulent

activities are undertaken by the management or by its official. The key fraud risks in the case of

DIPL are as follows:

Inventory valuation

Based on the financial information of the company, it can be seen that its sale figures have

depicted a positive and enhanced performance over the years. However, the main area of concern

is that even though the company attained good sales over the years, yet its stock balances have

not depicted a downward trend and instead, an upward trend in stock figures can be seen. This is

a big issue for the company because the enhancement in the level of inventories must have been

done through manipulation on the part of the management or accountant so that the accounts are

tampered and it fetches good profits (Gilbert et. al 2005).

Mail revenue recognition

Since the cashier undertakes the job of encashment of the cheques attained through mail basis, it

may create many difficulties for the company. The reason behind this can be attributed to the fact

that prior verification from the bank is missing in this scenario and that can result in fraud on the

part of the management or its officials. It is therefore required prior verification from bank

statements must be undertaken so that efficacy of the transaction can be achieved. Moreover, if

such system is not in place, the officials of the company might be in a position to deport the

company’s resources and credit the same to an unwanted person’s account. This will not only

deteriorate the financial resources of the company but also hamper its financial statements.

Hence, it is required that the company must undertake proper bank reconciliation systems within

its operations so that the possibilities of fraud are minimized to the fullest (Geoffrey et. al, 2016).

Moreover, this will also result in strong corporate governance within the company because of

transparency.

Therefore, these two fraud risks pose a big threat to the company’s affairs wherein both the

management and its officials are in a position to tamper the accounts for their own benefits. As a

result, the auditor’s judgement may be deteriorated because they may not identify the fraud done

Auditing

on the part of the management, thereby representing a bad auditor opinion (Geoffrey et. al,

2016).

Answer to 3(b)

Fraudulent measures play a key role in affecting the entire audit process because the auditor may

be influenced due to manipulation done in the company’s accounts and therefore, they may

provide an ineffective audit judgement. Similarly, in relation to the fraud risks recognized above,

it must be taken into consideration that such risks may negatively influence the company’s

financial statements because of the ill intention on the company’s part to attain maximum

revenues. Owing to an insignificant number of transactions in a company, if the system of

recording receivables is not done in a proper manner, the auditor may prove incapable of

identifying falsification in the financials (Elder et. al, 2010). This is because every entry will

become necessary to be verified and since the transaction was entered in the wrong period, the

auditor may not identify the truthfulness of such claim. Moreover, in case of lack of evidence,

the auditor is in no position to provide an ineffective judgement on the company’s financials. If

variations or differences can be witnessed in the financial statements, then the auditor may

question the same and provide a qualified opinion. Furthermore, the inventory valuation system

has also been a concern for the company and the auditor must evaluate the cause of such

enhancement in figures even after the increase in sales. It may happen that the company to value

inventories has done falsification and since the auditor has relied upon the same; he may offer an

unqualified opinion (Gay & Simnet, 2015). For such purpose, the auditor must implement proper

judgement and skills to conduct the audit process.

on the part of the management, thereby representing a bad auditor opinion (Geoffrey et. al,

2016).

Answer to 3(b)

Fraudulent measures play a key role in affecting the entire audit process because the auditor may

be influenced due to manipulation done in the company’s accounts and therefore, they may

provide an ineffective audit judgement. Similarly, in relation to the fraud risks recognized above,

it must be taken into consideration that such risks may negatively influence the company’s

financial statements because of the ill intention on the company’s part to attain maximum

revenues. Owing to an insignificant number of transactions in a company, if the system of

recording receivables is not done in a proper manner, the auditor may prove incapable of

identifying falsification in the financials (Elder et. al, 2010). This is because every entry will

become necessary to be verified and since the transaction was entered in the wrong period, the

auditor may not identify the truthfulness of such claim. Moreover, in case of lack of evidence,

the auditor is in no position to provide an ineffective judgement on the company’s financials. If

variations or differences can be witnessed in the financial statements, then the auditor may

question the same and provide a qualified opinion. Furthermore, the inventory valuation system

has also been a concern for the company and the auditor must evaluate the cause of such

enhancement in figures even after the increase in sales. It may happen that the company to value

inventories has done falsification and since the auditor has relied upon the same; he may offer an

unqualified opinion (Gay & Simnet, 2015). For such purpose, the auditor must implement proper

judgement and skills to conduct the audit process.

Auditing

References

Berk, J, DeMarzo, P & Stangeland, D 2015, Corporate Finance, Canadian Toronto: Pearson

Canada.

Church, B, Davis, S & McCracken, S 2008, ‘The auditor’s reporting model: A literature

overview and research synthesis’, Accounting Horizons vol. 22, no. 1, pp. 69-90.

Elder, J. R, Beasley S. M.& Arens A. A 2010, Auditing and Assurance Services, Person

Education, New Jersey: USA

Gay, G & Simnet, R 2015, Auditing and Assurance Services, McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S & David A. W 2016, ‘Attracting Applicants for In-House

and Outsourced Internal Audit Positions: Views from External Auditors’, Accounting Horizons,

vol. 30, no. 1, pp. 143-156.

Gilbert, W. Joseph J & Terry J. E., 2005. The Use of Control Self-Assessment by Independent

Auditors. The CPA Journal, 3, pp. 66-92

Guerard, J. 2013, Introduction to financial forecasting in investment analysis, New York, NY:

Springer, pp. 78-81

Heeler, D 2009, Audit Principles, Risk Assessment & Effective Reporting. Pearson Press

Johnstone, K, Gramling, A & Rittenberg, L.E 2014, Auditing: A Risk Based-Approach to

Conducting a Quality Audit, 10th Edition, Cengage Learning

Matthew S. E 2015, ‘ Does Internal Audit Function Quality Deter Management Misconduct?’,

The Accounting Review, vol. 90, no. 2, pp. 495-527

Reding, H.R, Sobel, P.J, Anderson, U.L, Head,M.J, Ramamoorti, S, Salamasick,M &

Riddle, C 2015, Internal Auditing: Assurance & Advisory Services, Third Edition 3rd Edition,

The Institute of Internal Auditor Research Foundation

Ruhnke, K & Schmidt, M 2014, The audit expectation gap: existence, causes, and the impact of

changes, Accounting and Business Research, vol. 44, no. 5, pp. 572-601.

References

Berk, J, DeMarzo, P & Stangeland, D 2015, Corporate Finance, Canadian Toronto: Pearson

Canada.

Church, B, Davis, S & McCracken, S 2008, ‘The auditor’s reporting model: A literature

overview and research synthesis’, Accounting Horizons vol. 22, no. 1, pp. 69-90.

Elder, J. R, Beasley S. M.& Arens A. A 2010, Auditing and Assurance Services, Person

Education, New Jersey: USA

Gay, G & Simnet, R 2015, Auditing and Assurance Services, McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S & David A. W 2016, ‘Attracting Applicants for In-House

and Outsourced Internal Audit Positions: Views from External Auditors’, Accounting Horizons,

vol. 30, no. 1, pp. 143-156.

Gilbert, W. Joseph J & Terry J. E., 2005. The Use of Control Self-Assessment by Independent

Auditors. The CPA Journal, 3, pp. 66-92

Guerard, J. 2013, Introduction to financial forecasting in investment analysis, New York, NY:

Springer, pp. 78-81

Heeler, D 2009, Audit Principles, Risk Assessment & Effective Reporting. Pearson Press

Johnstone, K, Gramling, A & Rittenberg, L.E 2014, Auditing: A Risk Based-Approach to

Conducting a Quality Audit, 10th Edition, Cengage Learning

Matthew S. E 2015, ‘ Does Internal Audit Function Quality Deter Management Misconduct?’,

The Accounting Review, vol. 90, no. 2, pp. 495-527

Reding, H.R, Sobel, P.J, Anderson, U.L, Head,M.J, Ramamoorti, S, Salamasick,M &

Riddle, C 2015, Internal Auditing: Assurance & Advisory Services, Third Edition 3rd Edition,

The Institute of Internal Auditor Research Foundation

Ruhnke, K & Schmidt, M 2014, The audit expectation gap: existence, causes, and the impact of

changes, Accounting and Business Research, vol. 44, no. 5, pp. 572-601.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.