High-Risk Investment: Risks, Returns, Ethical Violations and Analysis

VerifiedAdded on 2020/02/24

|11

|2666

|100

Report

AI Summary

This report delves into the realm of high-risk investments, exploring the inherent risks and potential returns associated with various investment vehicles, including exchange-traded derivatives. It examines the risk/return trade-off and factors influencing investor preferences, such as market trends and investment duration. The report analyzes the ethical violations committed by JPMorgan Chase, highlighting the implications for investors and the need for stricter financial regulations. It also discusses the challenges in regulating complex global financial firms and suggests measures for improved transparency, macro-prudential regulation, and coordination among regulatory bodies. The report further provides insights into scenarios where high-risk investments can be beneficial, such as long-term equity stock investments, emphasizing the importance of diversification and understanding market dynamics.

HIGH-RISK INVESTMENT

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

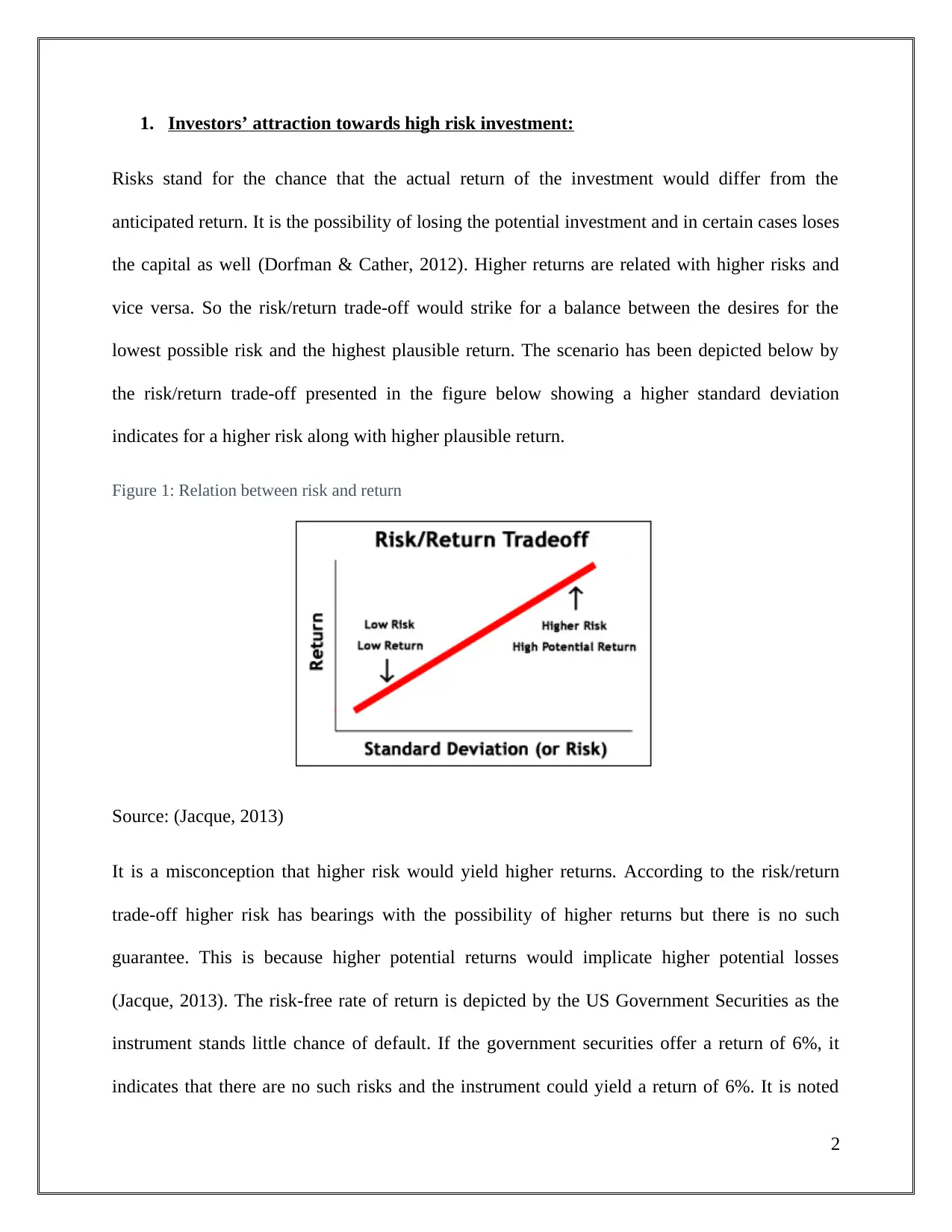

1. Investors’ attraction towards high risk investment:

Risks stand for the chance that the actual return of the investment would differ from the

anticipated return. It is the possibility of losing the potential investment and in certain cases loses

the capital as well (Dorfman & Cather, 2012). Higher returns are related with higher risks and

vice versa. So the risk/return trade-off would strike for a balance between the desires for the

lowest possible risk and the highest plausible return. The scenario has been depicted below by

the risk/return trade-off presented in the figure below showing a higher standard deviation

indicates for a higher risk along with higher plausible return.

Figure 1: Relation between risk and return

Source: (Jacque, 2013)

It is a misconception that higher risk would yield higher returns. According to the risk/return

trade-off higher risk has bearings with the possibility of higher returns but there is no such

guarantee. This is because higher potential returns would implicate higher potential losses

(Jacque, 2013). The risk-free rate of return is depicted by the US Government Securities as the

instrument stands little chance of default. If the government securities offer a return of 6%, it

indicates that there are no such risks and the instrument could yield a return of 6%. It is noted

2

Risks stand for the chance that the actual return of the investment would differ from the

anticipated return. It is the possibility of losing the potential investment and in certain cases loses

the capital as well (Dorfman & Cather, 2012). Higher returns are related with higher risks and

vice versa. So the risk/return trade-off would strike for a balance between the desires for the

lowest possible risk and the highest plausible return. The scenario has been depicted below by

the risk/return trade-off presented in the figure below showing a higher standard deviation

indicates for a higher risk along with higher plausible return.

Figure 1: Relation between risk and return

Source: (Jacque, 2013)

It is a misconception that higher risk would yield higher returns. According to the risk/return

trade-off higher risk has bearings with the possibility of higher returns but there is no such

guarantee. This is because higher potential returns would implicate higher potential losses

(Jacque, 2013). The risk-free rate of return is depicted by the US Government Securities as the

instrument stands little chance of default. If the government securities offer a return of 6%, it

indicates that there are no such risks and the instrument could yield a return of 6%. It is noted

2

that the index fund which generally gives a return for 12% contains substantial risk as it return

varies every year. It is supposed the investors in this case are exposed to a greater risk owing to

financial volatility though it carries a comparative higher return than the government securities

(Oikonomou, et al., 2012). The additional return out of the risk premium has been 6% (12% -

6%). So the risk appetite of the investors varies from individual to individual based on his goals,

income and background.

There are certain factors that determine the preferences of the investors such as:

Market trends–The market is supposed to repeat its performance and the investors need

to understand the implications of the different asset classes that has left its impression in

the past.

Risk appetite – The risk taking capability of the investors varies from person to person.

It is very much influenced by the financial responsibilities, goals in life and personality

of the individual investors to make a suitable investment decision (Kimyagarov &

Shivdasani, 2013).

Investment duration –It depends on the nature of the investor that how long he would be

keeping the investment in the market. It seems longer the duration of the investment the

better would be the return as the risk element reduces substantially.

Surplus of investments –The investible surpluses are supposed to play a crucial factor in

selection of the different asset classes because of the differentiation of the minimum

investment amount along with its risk and return (Erkens, et al., 2012).

Needs of investment –It is unto the desire of the investor to fulfil on his goals in life and

invest in a systematic way to achieve the same.

3

varies every year. It is supposed the investors in this case are exposed to a greater risk owing to

financial volatility though it carries a comparative higher return than the government securities

(Oikonomou, et al., 2012). The additional return out of the risk premium has been 6% (12% -

6%). So the risk appetite of the investors varies from individual to individual based on his goals,

income and background.

There are certain factors that determine the preferences of the investors such as:

Market trends–The market is supposed to repeat its performance and the investors need

to understand the implications of the different asset classes that has left its impression in

the past.

Risk appetite – The risk taking capability of the investors varies from person to person.

It is very much influenced by the financial responsibilities, goals in life and personality

of the individual investors to make a suitable investment decision (Kimyagarov &

Shivdasani, 2013).

Investment duration –It depends on the nature of the investor that how long he would be

keeping the investment in the market. It seems longer the duration of the investment the

better would be the return as the risk element reduces substantially.

Surplus of investments –The investible surpluses are supposed to play a crucial factor in

selection of the different asset classes because of the differentiation of the minimum

investment amount along with its risk and return (Erkens, et al., 2012).

Needs of investment –It is unto the desire of the investor to fulfil on his goals in life and

invest in a systematic way to achieve the same.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Returns –The expected return is a crucial factor and is directly related to the investment

choice (Lins, et al., 2011). For instance, a young investor would be opting for risky

investments like equities as he has the risk taking ability and longer duration to

neutralise the market risks. Again an aged investor on the verge of retirement would

avoid equity and look for debt instruments like government securities which would offer

a safe haven to his investment for a shorter period.

2. Risks associated with exchange-traded derivatives:

Exchange traded investments like futures and options as an investment asset are considered to be

riskier on likes with other instruments like equities and currencies. The US Treasury bond

futures contract are considered to be one of the most traded investment across the globe but the

prices of the futures contract are volatile. In lines with equities, the futures and options too, carry

more risks than the fixed income investments. The trading futures are considered to be quite

riskier due to the leverages associated to it. Leverages are the ability to margin investments on

the basis of fraction of its total value (Arnold, 2014).In case of stocks the maximum leverage

could go unto 50% while that of futures it might raise unto 90%-95%. It implies that the investor

can invest in the futures contract by investing 10% of the actual value of the contract.

The leverages intensify the consequences of the changes in prices in respect to relatively smaller

changes in prices to represent considerable profits or losses (Coles, et al., 2012). The

involvement of the leverages in future trading has possibility to sustain greater losses than the

initial investment. Contrarily, the futures could also come up with substantial returns as the risks

involved with it depends on the process in which the futures contract are being traded. The

4

choice (Lins, et al., 2011). For instance, a young investor would be opting for risky

investments like equities as he has the risk taking ability and longer duration to

neutralise the market risks. Again an aged investor on the verge of retirement would

avoid equity and look for debt instruments like government securities which would offer

a safe haven to his investment for a shorter period.

2. Risks associated with exchange-traded derivatives:

Exchange traded investments like futures and options as an investment asset are considered to be

riskier on likes with other instruments like equities and currencies. The US Treasury bond

futures contract are considered to be one of the most traded investment across the globe but the

prices of the futures contract are volatile. In lines with equities, the futures and options too, carry

more risks than the fixed income investments. The trading futures are considered to be quite

riskier due to the leverages associated to it. Leverages are the ability to margin investments on

the basis of fraction of its total value (Arnold, 2014).In case of stocks the maximum leverage

could go unto 50% while that of futures it might raise unto 90%-95%. It implies that the investor

can invest in the futures contract by investing 10% of the actual value of the contract.

The leverages intensify the consequences of the changes in prices in respect to relatively smaller

changes in prices to represent considerable profits or losses (Coles, et al., 2012). The

involvement of the leverages in future trading has possibility to sustain greater losses than the

initial investment. Contrarily, the futures could also come up with substantial returns as the risks

involved with it depends on the process in which the futures contract are being traded. The

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

futures traders could handle the additional leverage quite wisely with the relevance of the

superior level of financial management. This could be done by using the prudent stop-loss orders

by limiting the potential losses (Lins, et al., 2011). The futures trader does not over-margin

themselves but tries to maintain uncommitted investment capital for the protection of the

investments.

3. Challenges and suggestions to regulate a complex global financial firm:

Globalisation has made the financial market more complex. The global financial firms are facing

different political as well as geographical and economic diversity. The availability of versatile

financial products into the global financial market is demanding a stricter and dynamic

regulatory environment to protect the interest of the stakeholders of the financial market

(Chandra, 2011). In absence of global government followings are the key challenges to regulate a

global financial firm in this era of globalisation:

Transparency – The financial products must be bringing into the regime of the monitoring and

being regulated. The contracts of financial products shall not escape standardization and should

be bring into the regulatory net. Over-the-Counter (OTC) contracts needs to be brought into the

line of technical trading platform so that the systematic risk can be avoided (Hill, et al., 2013).

Macro-prudential regulation – The financial firms should be regulated as a whole; the risk

shall be handled and managed taking into consideration of the aggregate adverse consequences.

The financial firms should be governed at the systematic level rather than taking care of an

individual institution (Erkens, et al., 2012). The different financial institutions should be bringing

into an identical reporting requirements and governing system.

5

superior level of financial management. This could be done by using the prudent stop-loss orders

by limiting the potential losses (Lins, et al., 2011). The futures trader does not over-margin

themselves but tries to maintain uncommitted investment capital for the protection of the

investments.

3. Challenges and suggestions to regulate a complex global financial firm:

Globalisation has made the financial market more complex. The global financial firms are facing

different political as well as geographical and economic diversity. The availability of versatile

financial products into the global financial market is demanding a stricter and dynamic

regulatory environment to protect the interest of the stakeholders of the financial market

(Chandra, 2011). In absence of global government followings are the key challenges to regulate a

global financial firm in this era of globalisation:

Transparency – The financial products must be bringing into the regime of the monitoring and

being regulated. The contracts of financial products shall not escape standardization and should

be bring into the regulatory net. Over-the-Counter (OTC) contracts needs to be brought into the

line of technical trading platform so that the systematic risk can be avoided (Hill, et al., 2013).

Macro-prudential regulation – The financial firms should be regulated as a whole; the risk

shall be handled and managed taking into consideration of the aggregate adverse consequences.

The financial firms should be governed at the systematic level rather than taking care of an

individual institution (Erkens, et al., 2012). The different financial institutions should be bringing

into an identical reporting requirements and governing system.

5

Co-ordination – with the rise of globalisation the financial institutions are now operating into

the different geographical regions and abide to the different regulatory systems. The Co-

ordination between the different regulators is the key to mitigate the systematic risk of the

financial market (Kramer, 2012). The uniform reporting requirements and sharing of information

between the regulatory authorities is necessary to identify the risk at the earliest and to manage it

at the aggregate level.

4. Analysis the Ethical Violation by JPMorgan Chase:

The JP Morgan Chase is one of the biggest names in the financial market of US. The company is

engaged not only into the ordinary consumer banking operation but also offering various

financial services. Before 2008 crisis in the US the large banks like JP Morgan Chase were

engaged into the business of “Mortgage Securitization”. The banks then sold those Mortgages in

the form of underlying securities to the investors (Brigham & Houston, 2011).

JPMorgan Chase has sold these mortgage backed securities, many of which were bad loans. The

investors have purchased those mortgage backed securities considering that they are investing

into a lower risk securities. However, the JPMorgan Chase has cheated the investors by showing

them the high value of the backed mortgage security. The company has been fined $13 billion by

the US government.

The act of JPMorgan Chase has affected the US economy adversely. As the investors thought

that they are investing into AAA rating securities which were turned out junk. The various

investors have suffered huge losses (Coles, et al., 2012). The faith of the investors into the US

financial market has declined. Over statement of the value of the mortgages not only affected

6

the different geographical regions and abide to the different regulatory systems. The Co-

ordination between the different regulators is the key to mitigate the systematic risk of the

financial market (Kramer, 2012). The uniform reporting requirements and sharing of information

between the regulatory authorities is necessary to identify the risk at the earliest and to manage it

at the aggregate level.

4. Analysis the Ethical Violation by JPMorgan Chase:

The JP Morgan Chase is one of the biggest names in the financial market of US. The company is

engaged not only into the ordinary consumer banking operation but also offering various

financial services. Before 2008 crisis in the US the large banks like JP Morgan Chase were

engaged into the business of “Mortgage Securitization”. The banks then sold those Mortgages in

the form of underlying securities to the investors (Brigham & Houston, 2011).

JPMorgan Chase has sold these mortgage backed securities, many of which were bad loans. The

investors have purchased those mortgage backed securities considering that they are investing

into a lower risk securities. However, the JPMorgan Chase has cheated the investors by showing

them the high value of the backed mortgage security. The company has been fined $13 billion by

the US government.

The act of JPMorgan Chase has affected the US economy adversely. As the investors thought

that they are investing into AAA rating securities which were turned out junk. The various

investors have suffered huge losses (Coles, et al., 2012). The faith of the investors into the US

financial market has declined. Over statement of the value of the mortgages not only affected

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the investors by huge losses but also it is an eye opener for the regulatory authority as well. The

placement of a rigid law is necessary to avoid such practices. The “due diligence” has to be

conducted in the manner that should be independent and qualified enough to mitigate such

situations of crisis (Titman, et al., 2015).

5. Implications for trading in high risk investments:

In 2013, a federal jury in New York returned a prosecution of two senior executives from JP

Morgan, Javier Martin-Artajo and Julien Grout. They were held responsible for the valuation of

the credit derivatives that the financial institution bought resulting in a loss for $6 billion. Both

of them were charged with conspiracy, false entries in the banking records and false statement to

the Securities and Exchange Commission. The public notion goes along with the verdict as it is

admitted of a violation, the aspect of corporate criminal investigation brought up in the scenario

is totally justified (Jacque, 2013). The charges filed in this case would supposedly cause a

significant damage to the reputation of the executive withholding his lucrative career from the

financial glamour of the banking industry.

The management of the organisation also suffered a huge blow as most of its senior management

got removed or charged with criminal conspiracies for contemplating financial misconducts. The

ratings of the institution fell drastically and it was charged with a hefty fine worth $2 billion for

engaging in financial scandal. The implications were also felt on the brokers of JP Morgan Chase

involved in high risk investments. The organisation expelled its head of the government debt

trading desk and other employees intensifying the complexity of the banking compliance as the

management entered into disagreement with such parties. The traders wanted to enhance the size

7

placement of a rigid law is necessary to avoid such practices. The “due diligence” has to be

conducted in the manner that should be independent and qualified enough to mitigate such

situations of crisis (Titman, et al., 2015).

5. Implications for trading in high risk investments:

In 2013, a federal jury in New York returned a prosecution of two senior executives from JP

Morgan, Javier Martin-Artajo and Julien Grout. They were held responsible for the valuation of

the credit derivatives that the financial institution bought resulting in a loss for $6 billion. Both

of them were charged with conspiracy, false entries in the banking records and false statement to

the Securities and Exchange Commission. The public notion goes along with the verdict as it is

admitted of a violation, the aspect of corporate criminal investigation brought up in the scenario

is totally justified (Jacque, 2013). The charges filed in this case would supposedly cause a

significant damage to the reputation of the executive withholding his lucrative career from the

financial glamour of the banking industry.

The management of the organisation also suffered a huge blow as most of its senior management

got removed or charged with criminal conspiracies for contemplating financial misconducts. The

ratings of the institution fell drastically and it was charged with a hefty fine worth $2 billion for

engaging in financial scandal. The implications were also felt on the brokers of JP Morgan Chase

involved in high risk investments. The organisation expelled its head of the government debt

trading desk and other employees intensifying the complexity of the banking compliance as the

management entered into disagreement with such parties. The traders wanted to enhance the size

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the reserves which the management opposed owing to violation of the internal banking

processes (Coles, et al., 2012). These steps were to be followed as the crisis engulfed the

scenario totally and the institution was not in a mood to endanger its brand reputation and stake

in the financial market.

6. Scenario where high risk Investment would be beneficial:

Investment in high risk investment could be beneficial if an investor ready to hold the investment

in long run. The holding period of an investment is crucial. The equity stocks are termed to be

the more risky than the other form of securities, although has more liquidity. An investor desired

to take high risk can opt for the equity stock investment (Moyer, et al., 2011). A perfect diverse

portfolio of the equity stock not only provides the good return on investment but also it is

proving out to be the wealth creation in long run. The risk associated with the equity stocks can

also be mitigated in long run. Some of the benefits of investing in equity stocks are:

Increase wealth - The history the stock market is suggested that the equity shares have increased

in value in long run, even though the stock market crashes various times. The equity stock may

fluctuate but it is prove to be beneficial in long term (Lasher, 2013).

Regular Income - Equity shares generally generate income in the form of dividends. Holding

the equity in long run can out to be more beneficial than any other form of investment. A regular

income and wealth creation both are achievable (Titman, et al., 2015).

High Liquidity - The equity stock is highly liquid investment tool. The equity stock can be

termed to be the next cash option in the hand of investors. The equity stock can be easily buy,

sell and lien.

8

processes (Coles, et al., 2012). These steps were to be followed as the crisis engulfed the

scenario totally and the institution was not in a mood to endanger its brand reputation and stake

in the financial market.

6. Scenario where high risk Investment would be beneficial:

Investment in high risk investment could be beneficial if an investor ready to hold the investment

in long run. The holding period of an investment is crucial. The equity stocks are termed to be

the more risky than the other form of securities, although has more liquidity. An investor desired

to take high risk can opt for the equity stock investment (Moyer, et al., 2011). A perfect diverse

portfolio of the equity stock not only provides the good return on investment but also it is

proving out to be the wealth creation in long run. The risk associated with the equity stocks can

also be mitigated in long run. Some of the benefits of investing in equity stocks are:

Increase wealth - The history the stock market is suggested that the equity shares have increased

in value in long run, even though the stock market crashes various times. The equity stock may

fluctuate but it is prove to be beneficial in long term (Lasher, 2013).

Regular Income - Equity shares generally generate income in the form of dividends. Holding

the equity in long run can out to be more beneficial than any other form of investment. A regular

income and wealth creation both are achievable (Titman, et al., 2015).

High Liquidity - The equity stock is highly liquid investment tool. The equity stock can be

termed to be the next cash option in the hand of investors. The equity stock can be easily buy,

sell and lien.

8

Diversification – An investor can achieve diversification by investing into the equity stock. A

portfolio of investment in different industry can be easily achieved by the investor (Madura,

2012). The industry specific risk can be mitigated through well diversify investment.

9

portfolio of investment in different industry can be easily achieved by the investor (Madura,

2012). The industry specific risk can be mitigated through well diversify investment.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Arnold, G., 2014. Corporate financial management. London: Pearson Higher Ed.

Brigham, E. & Houston, J., 2011. Fundamentals of financial management. London: Cengage

Learning.

Chandra, P., 2011. Financial management. London: Tata McGraw-Hill Education.

Coles, J. L., Lemmon, M. L. & Meschke, J. F., 2012. Structural models and endogeneity in

corporate finance: The link between managerial ownership and corporate performance. Journal

of Financial Economics, 103(1), pp. 149-168.

Dorfman, M. S. & Cather, D., 2012. Introduction to risk management and insurance. London:

Pearson Higher Ed.

Erkens, D., Hung, M. & Matos, P., 2012. Corporate governance in the 2007–2008 financial

crisis: Evidence from financial institutions worldwide. Journal of Corporate Finance, 18(2), pp.

389-411.

Hill, M., Kelly, G., Lockhart, G. & Ness, R., 2013. Determinants and effects of corporate

lobbying. Financial Management, 42(4), pp. 931-957.

Jacque, L. L., 2013. Management and control of foreign exchange risk. London: Springer

Science & Business Media.

Kimyagarov, G. & Shivdasani, A., 2013. Managing Pension Risks: A Corporate Finance

Perspective. Journal of Applied Corporate Finance, 25(4), pp. 41-49.

Kramer, M. M., 2012. Financial advice and individual investor portfolio performance. Financial

Management, 41(2), pp. 395-428.

10

Arnold, G., 2014. Corporate financial management. London: Pearson Higher Ed.

Brigham, E. & Houston, J., 2011. Fundamentals of financial management. London: Cengage

Learning.

Chandra, P., 2011. Financial management. London: Tata McGraw-Hill Education.

Coles, J. L., Lemmon, M. L. & Meschke, J. F., 2012. Structural models and endogeneity in

corporate finance: The link between managerial ownership and corporate performance. Journal

of Financial Economics, 103(1), pp. 149-168.

Dorfman, M. S. & Cather, D., 2012. Introduction to risk management and insurance. London:

Pearson Higher Ed.

Erkens, D., Hung, M. & Matos, P., 2012. Corporate governance in the 2007–2008 financial

crisis: Evidence from financial institutions worldwide. Journal of Corporate Finance, 18(2), pp.

389-411.

Hill, M., Kelly, G., Lockhart, G. & Ness, R., 2013. Determinants and effects of corporate

lobbying. Financial Management, 42(4), pp. 931-957.

Jacque, L. L., 2013. Management and control of foreign exchange risk. London: Springer

Science & Business Media.

Kimyagarov, G. & Shivdasani, A., 2013. Managing Pension Risks: A Corporate Finance

Perspective. Journal of Applied Corporate Finance, 25(4), pp. 41-49.

Kramer, M. M., 2012. Financial advice and individual investor portfolio performance. Financial

Management, 41(2), pp. 395-428.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lasher, W., 2013. Practical financial management. London: Nelson Education.

Lins, K. V., Servaes, H. & Tamayo, A., 2011. Does fair value reporting affect risk management?

International survey evidence. Financial management, 40(3), pp. 525-551.

Madura, J., 2012. International financial management. London: Cengage Learning.

Moyer, R. C., McGuigan, J., Rao, R. & Kretlow, W., 2011. Contemporary financial

management. London: Cengage Learning.

Oikonomou, I., Brooks, C. & Pavelin, S., 2012. The impact of corporate social performance on

financial risk and utility: A longitudinal analysis. Financial Management, 41(2), pp. 483-515.

Titman, S., Keown, A. & Martin, J., 2015. Financial management: Principles and applications.

London: Pearson.

11

Lins, K. V., Servaes, H. & Tamayo, A., 2011. Does fair value reporting affect risk management?

International survey evidence. Financial management, 40(3), pp. 525-551.

Madura, J., 2012. International financial management. London: Cengage Learning.

Moyer, R. C., McGuigan, J., Rao, R. & Kretlow, W., 2011. Contemporary financial

management. London: Cengage Learning.

Oikonomou, I., Brooks, C. & Pavelin, S., 2012. The impact of corporate social performance on

financial risk and utility: A longitudinal analysis. Financial Management, 41(2), pp. 483-515.

Titman, S., Keown, A. & Martin, J., 2015. Financial management: Principles and applications.

London: Pearson.

11

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.