Audit and Assurance Report: Cloud 9 Pty. Ltd Case Study Analysis

VerifiedAdded on 2023/04/23

|18

|2991

|223

Report

AI Summary

This report delves into the realm of audit and assurance, beginning with an executive summary that outlines the analytical procedures followed by auditors, a case study analysis of Cloud 9 Pty. Ltd, and the determination of overall materiality. Part A defines and explores the concept of materiality, explaining its significance in financial reporting and providing the steps to determine overall materiality. Part B focuses on analytical procedures, key business risks like compliance and financial risks, and effective control risk mitigation strategies. The report also includes ratio analysis to assess financial performance. Part C discusses executive remuneration in ASX-listed companies, specifically Wesfarmers, Woolworths, and Caltex, examining their compensation structures and relevant corporate governance requirements. The report concludes by emphasizing the importance of external audits in maintaining trust and transparency in the business world.

Running head: AUDIT AND AASURANCE

Audit and Assurance

Name of the Student:

Name of the University:

Author Note:

Audit and Assurance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT AND ASSURANCE

Table of Contents

Introduction................................................................................................................................3

Part A.........................................................................................................................................4

Materiality..................................................................................................................................4

Determining the overall materiality.......................................................................................4

Overall Materiality.................................................................................................................5

Part B..........................................................................................................................................6

Analytical Procedure..............................................................................................................6

Key Business Risk..................................................................................................................6

Part C..........................................................................................................................................8

Conclusion..................................................................................................................................9

Reference..................................................................................................................................10

Appendix:.................................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Part A.........................................................................................................................................4

Materiality..................................................................................................................................4

Determining the overall materiality.......................................................................................4

Overall Materiality.................................................................................................................5

Part B..........................................................................................................................................6

Analytical Procedure..............................................................................................................6

Key Business Risk..................................................................................................................6

Part C..........................................................................................................................................8

Conclusion..................................................................................................................................9

Reference..................................................................................................................................10

Appendix:.................................................................................................................................10

2AUDIT AND ASSURANCE

Executive Summary:

The report is about the analytical procedure an auditor shall follow. On the base of a case

study of Cloud 9 Pty.Ltd business risk assignment is assessed as well overall materiality is

concluded. In the other part of the report analytical procedure is discussed. The last part of

the report discusses about the remuneration of executives of the companies that are listed in

the ASX. For this the company selected is from the retail industry Wesfarmers, Woolworth

and Caltex. ltd

Introduction

Auditing is a prearranged form of examination and confirmation of bookkeeping

proceedings and reports, in command to appraise and evaluate the genuineness of the

proceedings and accounts. Auditing is a perception, which is designed on the source of

bookkeeping and spins from place to place the thought of inspection of books of financial

records and declarations, in command to assess whether these declarations and accounts

portray a true and fair image of an administration’s books of justification. Auditing is usually

assumed to evaluate the profit and loss declaration as well as appraise the image portrayed by

the balance sheet of a society. The determination of auditing is accompanying an inspection

and examination on the genuineness and the precision of the material represented by the

accounts of financial records of a group.

Executive Summary:

The report is about the analytical procedure an auditor shall follow. On the base of a case

study of Cloud 9 Pty.Ltd business risk assignment is assessed as well overall materiality is

concluded. In the other part of the report analytical procedure is discussed. The last part of

the report discusses about the remuneration of executives of the companies that are listed in

the ASX. For this the company selected is from the retail industry Wesfarmers, Woolworth

and Caltex. ltd

Introduction

Auditing is a prearranged form of examination and confirmation of bookkeeping

proceedings and reports, in command to appraise and evaluate the genuineness of the

proceedings and accounts. Auditing is a perception, which is designed on the source of

bookkeeping and spins from place to place the thought of inspection of books of financial

records and declarations, in command to assess whether these declarations and accounts

portray a true and fair image of an administration’s books of justification. Auditing is usually

assumed to evaluate the profit and loss declaration as well as appraise the image portrayed by

the balance sheet of a society. The determination of auditing is accompanying an inspection

and examination on the genuineness and the precision of the material represented by the

accounts of financial records of a group.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT AND ASSURANCE

Part A

Materiality

As per International Accounting Standard Board an information is considered as

material when an omission or misstatement is present. It manipulates the judgement

regarding the economic decision that the user take on the base of monetary statements.

Materiality size is depended on the size of the article or fault that is been pointed in the

particular situations due its omission as well as misstatement. There is threshold point

provided by the materiality slightly than actuality being of qualitative feature that the data is

useful. At the time of preparing the financial report the company should conclude the

materiality in order to be sure that the financial statement are correct in case of materiality.

(Australia.gov.au. 2019).

Determining the overall materiality

The materiality for financial report is been set by the auditors on overall basis during

the planning stage. The foremost reason for setting out the materiality during planning the

audit is just for recognizing the materiality performance so that an auditor can plan the

procedure for auditing. This include an evidently unimportant threshold for collecting

misstatements. This approach is not mandatory to follow. The three key steps for calculating

the overall materiality is-

Selection of appropriate benchmark

Determine certain level of percentage of benchmark.

Explaining the choice.

Part A

Materiality

As per International Accounting Standard Board an information is considered as

material when an omission or misstatement is present. It manipulates the judgement

regarding the economic decision that the user take on the base of monetary statements.

Materiality size is depended on the size of the article or fault that is been pointed in the

particular situations due its omission as well as misstatement. There is threshold point

provided by the materiality slightly than actuality being of qualitative feature that the data is

useful. At the time of preparing the financial report the company should conclude the

materiality in order to be sure that the financial statement are correct in case of materiality.

(Australia.gov.au. 2019).

Determining the overall materiality

The materiality for financial report is been set by the auditors on overall basis during

the planning stage. The foremost reason for setting out the materiality during planning the

audit is just for recognizing the materiality performance so that an auditor can plan the

procedure for auditing. This include an evidently unimportant threshold for collecting

misstatements. This approach is not mandatory to follow. The three key steps for calculating

the overall materiality is-

Selection of appropriate benchmark

Determine certain level of percentage of benchmark.

Explaining the choice.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT AND ASSURANCE

In this area auditor shall be concern and shall wisely select the options as he need to set

specific level of materiality in case of particular balances, groups of transactions as well

as disclosure even the short as well as long times of accounts.

Overall Materiality

The vital sum of data that is omitted, wrongly recorded, or that is not even disclosed

that contains information that effects the decision of the user of financial report or the release

of answerability by organisation or those stimulating with domination. While determining the

overall materiality the auditor shall keep in mind about the things such that user of fiscal

report, information that affects or is a base of decision, in adding to measureable sums, what

qualitative features might influence upon the operators fiscal recording supplies as they relate

to materiality. The audit team engage in auditing should use the template of materiality at the

time of conducting the audit. The below table shows the benchmark level of the materiality

misstatement.

Figure1: Materiality Template

(Source: Icac.nsw.gov.au. 2019).

There are several methods of calculating the materiality. The materiality calculated for Cloud

9 Pty. Ltd by W&S Partners is $ 1,49,02,552.50 (Appendix-1) as to perform the audit

In this area auditor shall be concern and shall wisely select the options as he need to set

specific level of materiality in case of particular balances, groups of transactions as well

as disclosure even the short as well as long times of accounts.

Overall Materiality

The vital sum of data that is omitted, wrongly recorded, or that is not even disclosed

that contains information that effects the decision of the user of financial report or the release

of answerability by organisation or those stimulating with domination. While determining the

overall materiality the auditor shall keep in mind about the things such that user of fiscal

report, information that affects or is a base of decision, in adding to measureable sums, what

qualitative features might influence upon the operators fiscal recording supplies as they relate

to materiality. The audit team engage in auditing should use the template of materiality at the

time of conducting the audit. The below table shows the benchmark level of the materiality

misstatement.

Figure1: Materiality Template

(Source: Icac.nsw.gov.au. 2019).

There are several methods of calculating the materiality. The materiality calculated for Cloud

9 Pty. Ltd by W&S Partners is $ 1,49,02,552.50 (Appendix-1) as to perform the audit

5AUDIT AND ASSURANCE

procedure of the company. As there is vast fluctuation seen in the balance sheet of Cloud 9

Pty.Ltd. Audit needs to inspect he key areas of report as well as critically annualizing the

records that support the figures those are mentioned in the balance sheet. Total asset amount

is considered for overall materiality as the earnings of revenue is depended on assets mainly.

Part B

Analytical Procedure

The auditing standard in Australia gives number of needs as well as application

towards different responsibilities of auditor. It states the responsibilities of auditor that he or

she is needed to perform during the analysis of financial statement. There are certain

obligations on the part of an auditor at time of reviewing the past records of accounting of the

company. The standards gives the Performa of presenting and recording of financial

statement and the way in which auditor shall express it opinion about the financial statement.

An auditor shall abide the rules stated in the standard. AASB suggest the guidelines that an

auditor complies so that the objective of an audit is meet.The general purposes to be

accomplished by a self-regulating accountant have been placed down in the auditing

standards. The standard put down down in AASB is applicable to the legal, specialised and

supervisory obligations. The morals will improve the level of self-assurance of the auditors.

The context of the auditing standards would determine that if the fiscal report has been

arranged in a reasonable way as well as in accordance by means of the numerous standards of

accounting. The principled necessities have to be satisfied by the auditor in accordance to the

Australian Auditing Standards. The accountant of a company prepares the statement in the

year end. The AASB do not have any legal obligations on the internal managers of the

company so as necessary to prepare the statement by them. The standard is formulated in

such way that is easier on the auditor`s part to frame its opinion on the outcome derived from

the financial statement and discharge his duties unbiasedly (Australia.gov.au. 2019).

procedure of the company. As there is vast fluctuation seen in the balance sheet of Cloud 9

Pty.Ltd. Audit needs to inspect he key areas of report as well as critically annualizing the

records that support the figures those are mentioned in the balance sheet. Total asset amount

is considered for overall materiality as the earnings of revenue is depended on assets mainly.

Part B

Analytical Procedure

The auditing standard in Australia gives number of needs as well as application

towards different responsibilities of auditor. It states the responsibilities of auditor that he or

she is needed to perform during the analysis of financial statement. There are certain

obligations on the part of an auditor at time of reviewing the past records of accounting of the

company. The standards gives the Performa of presenting and recording of financial

statement and the way in which auditor shall express it opinion about the financial statement.

An auditor shall abide the rules stated in the standard. AASB suggest the guidelines that an

auditor complies so that the objective of an audit is meet.The general purposes to be

accomplished by a self-regulating accountant have been placed down in the auditing

standards. The standard put down down in AASB is applicable to the legal, specialised and

supervisory obligations. The morals will improve the level of self-assurance of the auditors.

The context of the auditing standards would determine that if the fiscal report has been

arranged in a reasonable way as well as in accordance by means of the numerous standards of

accounting. The principled necessities have to be satisfied by the auditor in accordance to the

Australian Auditing Standards. The accountant of a company prepares the statement in the

year end. The AASB do not have any legal obligations on the internal managers of the

company so as necessary to prepare the statement by them. The standard is formulated in

such way that is easier on the auditor`s part to frame its opinion on the outcome derived from

the financial statement and discharge his duties unbiasedly (Australia.gov.au. 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT AND ASSURANCE

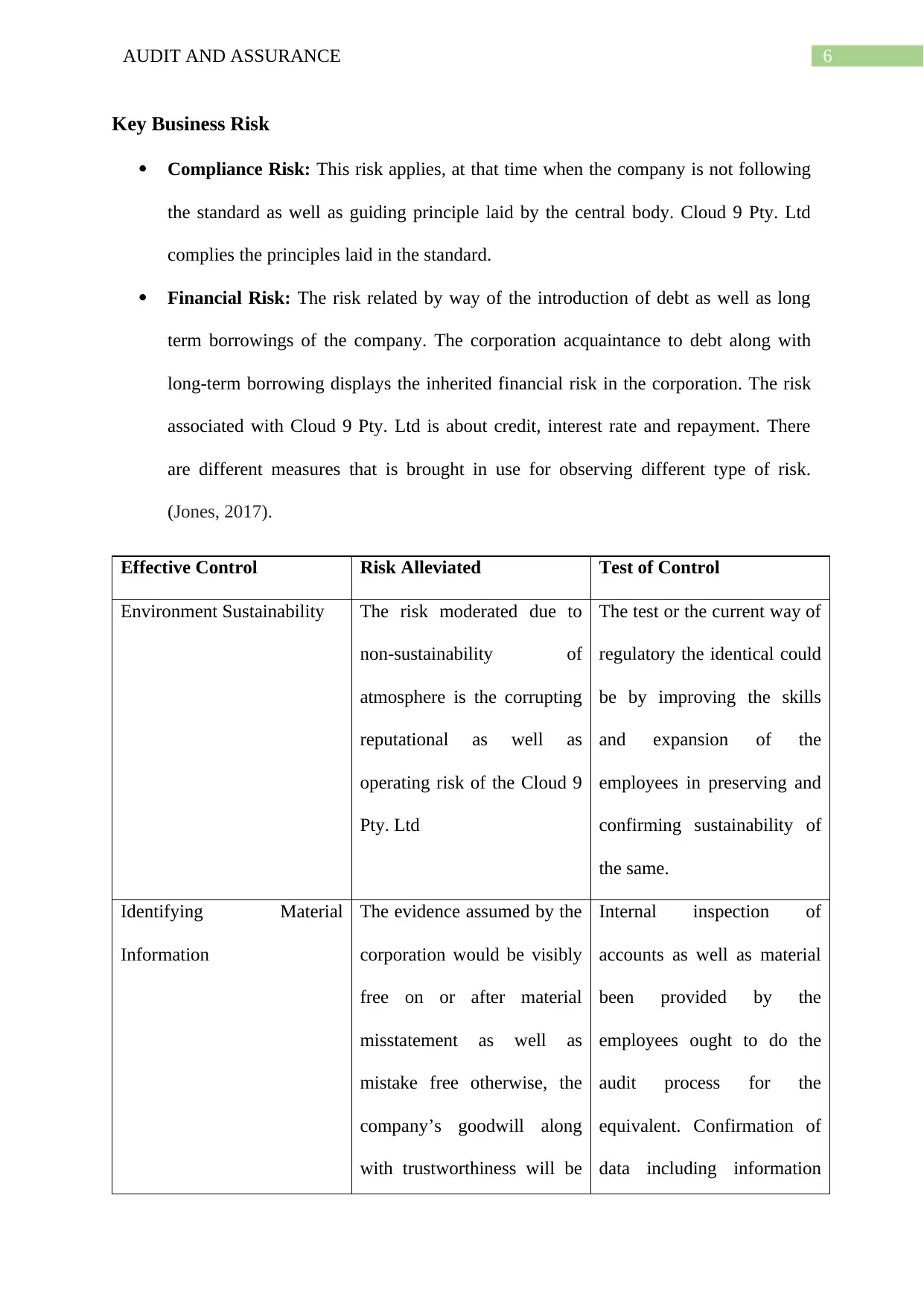

Key Business Risk

Compliance Risk: This risk applies, at that time when the company is not following

the standard as well as guiding principle laid by the central body. Cloud 9 Pty. Ltd

complies the principles laid in the standard.

Financial Risk: The risk related by way of the introduction of debt as well as long

term borrowings of the company. The corporation acquaintance to debt along with

long-term borrowing displays the inherited financial risk in the corporation. The risk

associated with Cloud 9 Pty. Ltd is about credit, interest rate and repayment. There

are different measures that is brought in use for observing different type of risk.

(Jones, 2017).

Effective Control Risk Alleviated Test of Control

Environment Sustainability The risk moderated due to

non-sustainability of

atmosphere is the corrupting

reputational as well as

operating risk of the Cloud 9

Pty. Ltd

The test or the current way of

regulatory the identical could

be by improving the skills

and expansion of the

employees in preserving and

confirming sustainability of

the same.

Identifying Material

Information

The evidence assumed by the

corporation would be visibly

free on or after material

misstatement as well as

mistake free otherwise, the

company’s goodwill along

with trustworthiness will be

Internal inspection of

accounts as well as material

been provided by the

employees ought to do the

audit process for the

equivalent. Confirmation of

data including information

Key Business Risk

Compliance Risk: This risk applies, at that time when the company is not following

the standard as well as guiding principle laid by the central body. Cloud 9 Pty. Ltd

complies the principles laid in the standard.

Financial Risk: The risk related by way of the introduction of debt as well as long

term borrowings of the company. The corporation acquaintance to debt along with

long-term borrowing displays the inherited financial risk in the corporation. The risk

associated with Cloud 9 Pty. Ltd is about credit, interest rate and repayment. There

are different measures that is brought in use for observing different type of risk.

(Jones, 2017).

Effective Control Risk Alleviated Test of Control

Environment Sustainability The risk moderated due to

non-sustainability of

atmosphere is the corrupting

reputational as well as

operating risk of the Cloud 9

Pty. Ltd

The test or the current way of

regulatory the identical could

be by improving the skills

and expansion of the

employees in preserving and

confirming sustainability of

the same.

Identifying Material

Information

The evidence assumed by the

corporation would be visibly

free on or after material

misstatement as well as

mistake free otherwise, the

company’s goodwill along

with trustworthiness will be

Internal inspection of

accounts as well as material

been provided by the

employees ought to do the

audit process for the

equivalent. Confirmation of

data including information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT AND ASSURANCE

caught up. must be done.

Monitoring The company’s procedures

including financials of the

entity should be well

measured in command to

reduce the business risk of

the corporation.

There must be operative

monitoring processes and

phases laid down in direction

to decrease the business plus

financial risk of the

corporation.

Physical monitoring and

controlling

The internal controller of the

corporation ought to be such

that the risk evaluated in

assets because of robbery,

forfeiture of goods,

impairment are certain of the

internal risk connected with

the company

Verification as well as

journal review of the assets

of the corporation shall be

done in order to escape

manipulation of resources

(Jones, 2017)

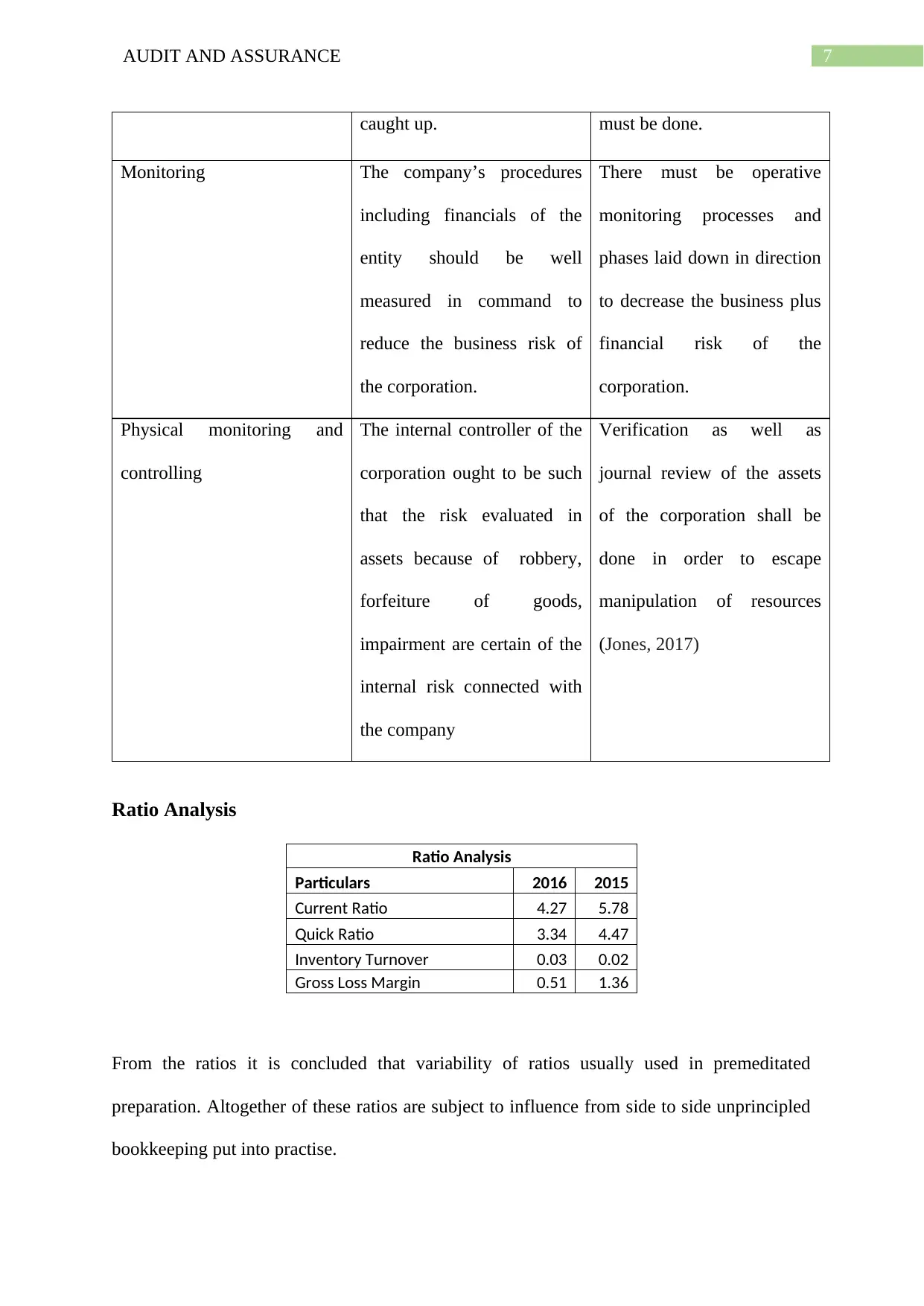

Ratio Analysis

Ratio Analysis

Particulars 2016 2015

Current Ratio 4.27 5.78

Quick Ratio 3.34 4.47

Inventory Turnover 0.03 0.02

Gross Loss Margin 0.51 1.36

From the ratios it is concluded that variability of ratios usually used in premeditated

preparation. Altogether of these ratios are subject to influence from side to side unprincipled

bookkeeping put into practise.

caught up. must be done.

Monitoring The company’s procedures

including financials of the

entity should be well

measured in command to

reduce the business risk of

the corporation.

There must be operative

monitoring processes and

phases laid down in direction

to decrease the business plus

financial risk of the

corporation.

Physical monitoring and

controlling

The internal controller of the

corporation ought to be such

that the risk evaluated in

assets because of robbery,

forfeiture of goods,

impairment are certain of the

internal risk connected with

the company

Verification as well as

journal review of the assets

of the corporation shall be

done in order to escape

manipulation of resources

(Jones, 2017)

Ratio Analysis

Ratio Analysis

Particulars 2016 2015

Current Ratio 4.27 5.78

Quick Ratio 3.34 4.47

Inventory Turnover 0.03 0.02

Gross Loss Margin 0.51 1.36

From the ratios it is concluded that variability of ratios usually used in premeditated

preparation. Altogether of these ratios are subject to influence from side to side unprincipled

bookkeeping put into practise.

8AUDIT AND ASSURANCE

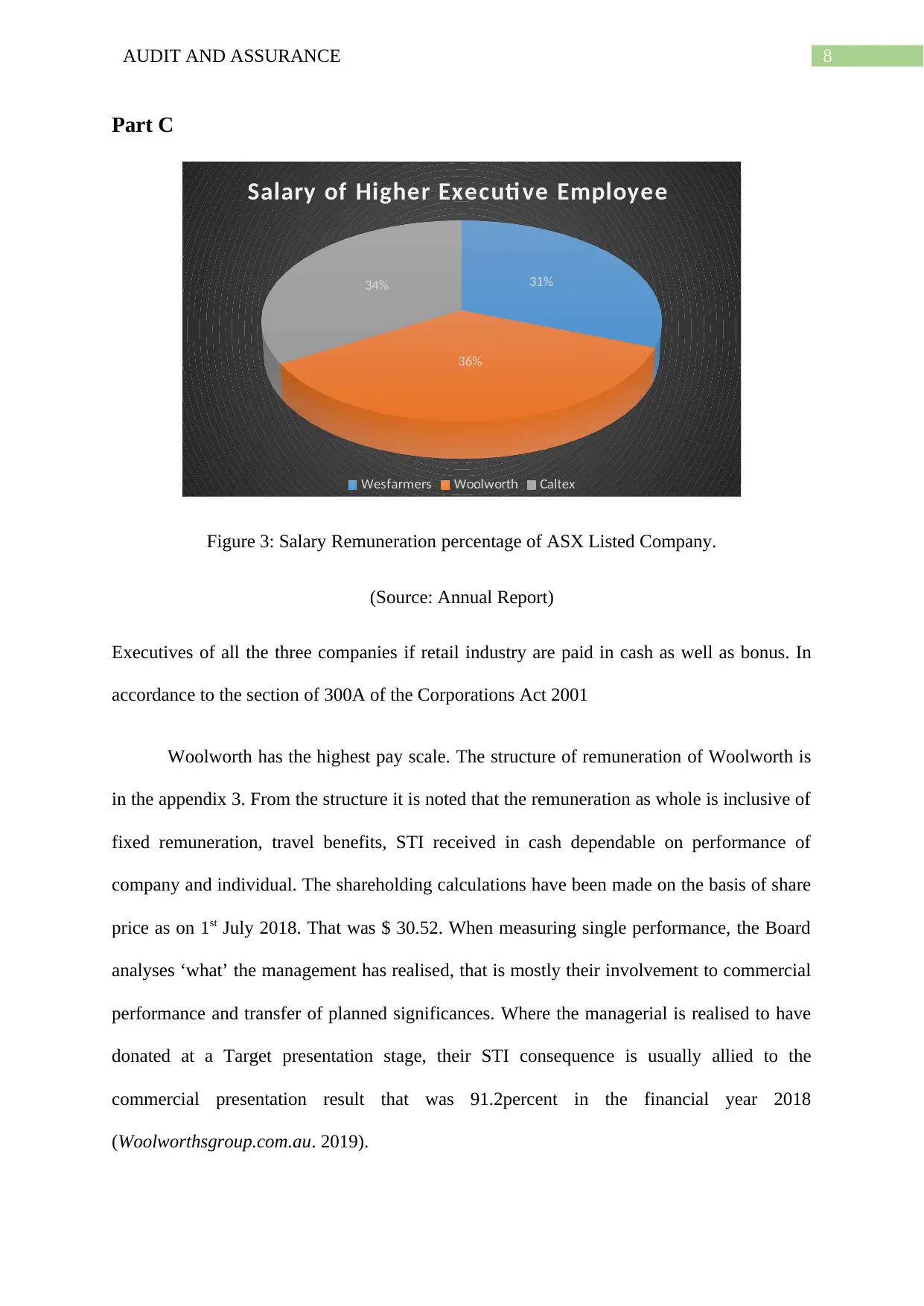

Part C

31%

36%

34%

Salary of Higher Executi ve Employee

Wesfarmers Woolworth Caltex

Figure 3: Salary Remuneration percentage of ASX Listed Company.

(Source: Annual Report)

Executives of all the three companies if retail industry are paid in cash as well as bonus. In

accordance to the section of 300A of the Corporations Act 2001

Woolworth has the highest pay scale. The structure of remuneration of Woolworth is

in the appendix 3. From the structure it is noted that the remuneration as whole is inclusive of

fixed remuneration, travel benefits, STI received in cash dependable on performance of

company and individual. The shareholding calculations have been made on the basis of share

price as on 1st July 2018. That was $ 30.52. When measuring single performance, the Board

analyses ‘what’ the management has realised, that is mostly their involvement to commercial

performance and transfer of planned significances. Where the managerial is realised to have

donated at a Target presentation stage, their STI consequence is usually allied to the

commercial presentation result that was 91.2percent in the financial year 2018

(Woolworthsgroup.com.au. 2019).

Part C

31%

36%

34%

Salary of Higher Executi ve Employee

Wesfarmers Woolworth Caltex

Figure 3: Salary Remuneration percentage of ASX Listed Company.

(Source: Annual Report)

Executives of all the three companies if retail industry are paid in cash as well as bonus. In

accordance to the section of 300A of the Corporations Act 2001

Woolworth has the highest pay scale. The structure of remuneration of Woolworth is

in the appendix 3. From the structure it is noted that the remuneration as whole is inclusive of

fixed remuneration, travel benefits, STI received in cash dependable on performance of

company and individual. The shareholding calculations have been made on the basis of share

price as on 1st July 2018. That was $ 30.52. When measuring single performance, the Board

analyses ‘what’ the management has realised, that is mostly their involvement to commercial

performance and transfer of planned significances. Where the managerial is realised to have

donated at a Target presentation stage, their STI consequence is usually allied to the

commercial presentation result that was 91.2percent in the financial year 2018

(Woolworthsgroup.com.au. 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT AND ASSURANCE

Compensation

There are two major zones subject to corporate governance necessities that is

executive remuneration disclosure as well as the payments at the termination level.

The Corporations Act needs that the yearly director’s statement comprise a

remuneration report, conversed in further part. As per application to the Corporations Act and

related Corporations Regulations 2001, resolution-making termination disbursements are

covered at a sum comparable to twelve months of a manager’s base income, through any

closure compensation more than the cap necessitating stockholder endorsement.

The Corporations Act states that the directors of a business are to be remunerated on the

terms as decided by the resolution. It is mandatory for the company to disclose the

remuneration amount paid when members cast 5 percent of vote in the general meeting or

there are hundred member present in the meeting. In relation to public company other than

reasonable payment of remuneration shareholders permission is needed.

The compensation of Woolworths under self-insurance were regarding the provision

of self-insured risk that is related to the estimation of liability that is related to the workers

including the claims and compensation of liability (Woolworthsgroup.com.au. 2019).

An onerous contract is an agreement in this agreement the inevitable value of meeting

the responsibilities under the agreement exceeding the monetary advantage predictable to be

established under it. The unescapable underneath an agreement replicate the tiniest net charge

of withdrawing from the agreement hat is the subordinate of the price of satisfying it as well

as whichever compensation or consequences rising from disappointment to accomplish it

(Woolworthsgroup.com.au. 2019).

Compensation

There are two major zones subject to corporate governance necessities that is

executive remuneration disclosure as well as the payments at the termination level.

The Corporations Act needs that the yearly director’s statement comprise a

remuneration report, conversed in further part. As per application to the Corporations Act and

related Corporations Regulations 2001, resolution-making termination disbursements are

covered at a sum comparable to twelve months of a manager’s base income, through any

closure compensation more than the cap necessitating stockholder endorsement.

The Corporations Act states that the directors of a business are to be remunerated on the

terms as decided by the resolution. It is mandatory for the company to disclose the

remuneration amount paid when members cast 5 percent of vote in the general meeting or

there are hundred member present in the meeting. In relation to public company other than

reasonable payment of remuneration shareholders permission is needed.

The compensation of Woolworths under self-insurance were regarding the provision

of self-insured risk that is related to the estimation of liability that is related to the workers

including the claims and compensation of liability (Woolworthsgroup.com.au. 2019).

An onerous contract is an agreement in this agreement the inevitable value of meeting

the responsibilities under the agreement exceeding the monetary advantage predictable to be

established under it. The unescapable underneath an agreement replicate the tiniest net charge

of withdrawing from the agreement hat is the subordinate of the price of satisfying it as well

as whichever compensation or consequences rising from disappointment to accomplish it

(Woolworthsgroup.com.au. 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT AND ASSURANCE

Conclusion

External audit show business significant character in the commercial world.

Principally in the fast-changing including unbalanced monetary atmosphere, there is a

constant requirement for agreement facilities of the dominance and reliability for

corporation’s fiscal statements, completely in corporations registered on stock exchange.

Development and clearness of the corporation`s communal appearance is enormously

safeguarded by the procedure of exterior audit. While carrying out audit various problem

concerning the inner regulator is predictable and is informed to the organization of the

corporation with the confidence of enhancement within the corporation. At present, the

inspection stays predominantly grounded on the audit risk method accordingly, from the

inspection company’s point of interpretation, it is serious to realize the risk valuation

procedures sufficiently and appropriately in preparation phase because it would decrease the

exertions and prosperity in the following rankings. Basically, audit firm desires to achieve

their deliberate fees to customer in direction to tolerate uncertain in the group. In other words,

further inclusive the inspection risk calculation is, the enhanced the prosperity such as period,

currency and hard work are applied.

Conclusion

External audit show business significant character in the commercial world.

Principally in the fast-changing including unbalanced monetary atmosphere, there is a

constant requirement for agreement facilities of the dominance and reliability for

corporation’s fiscal statements, completely in corporations registered on stock exchange.

Development and clearness of the corporation`s communal appearance is enormously

safeguarded by the procedure of exterior audit. While carrying out audit various problem

concerning the inner regulator is predictable and is informed to the organization of the

corporation with the confidence of enhancement within the corporation. At present, the

inspection stays predominantly grounded on the audit risk method accordingly, from the

inspection company’s point of interpretation, it is serious to realize the risk valuation

procedures sufficiently and appropriately in preparation phase because it would decrease the

exertions and prosperity in the following rankings. Basically, audit firm desires to achieve

their deliberate fees to customer in direction to tolerate uncertain in the group. In other words,

further inclusive the inspection risk calculation is, the enhanced the prosperity such as period,

currency and hard work are applied.

11AUDIT AND ASSURANCE

Reference

(2019). Microsites.caltex.com.au. Retrieved 27 January 2019, from

http://microsites.caltex.com.au/annualreports/2017/documents/17168_CALTEX_AS

X.pdf

(2019). Wesfarmers.com.au. Retrieved 27 January 2019, from

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-

annual-report.pdf?sfvrsn=0

(2019). Woolworthsgroup.com.au. Retrieved 27 January 2019, from

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

Australia.gov.au. (2019). Australian Accounting Standards Board | australia.gov.au. [online]

Available at: https://www.australia.gov.au/directories/australia/aasb [Accessed 26 Jan.

2019].

Houston, R.W., Peters, M.F. & Pratt, J.H., 1999. The audit risk model, business risk and

audit-planning decisions. The Accounting Review, 74(3), pp.281-298.

Icac.nsw.gov.au. (2019). [online] Available at: https://www.icac.nsw.gov.au/images/Ricco

%20Public%20Website/Exhibit%20R97.pdf [Accessed 26 Jan. 2019].

Icaew.com. (2019). [online] Available at:

https://www.icaew.com/-/media/corporate/files/technical/iaa/materiality-in-the-audit-

of-financial-statements.ashx [Accessed 25 Jan. 2019].

Johnstone, K., Gramling, A. & Rittenberg, L.E., 2013. Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Knechel, W.R.& Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Reference

(2019). Microsites.caltex.com.au. Retrieved 27 January 2019, from

http://microsites.caltex.com.au/annualreports/2017/documents/17168_CALTEX_AS

X.pdf

(2019). Wesfarmers.com.au. Retrieved 27 January 2019, from

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-

annual-report.pdf?sfvrsn=0

(2019). Woolworthsgroup.com.au. Retrieved 27 January 2019, from

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

Australia.gov.au. (2019). Australian Accounting Standards Board | australia.gov.au. [online]

Available at: https://www.australia.gov.au/directories/australia/aasb [Accessed 26 Jan.

2019].

Houston, R.W., Peters, M.F. & Pratt, J.H., 1999. The audit risk model, business risk and

audit-planning decisions. The Accounting Review, 74(3), pp.281-298.

Icac.nsw.gov.au. (2019). [online] Available at: https://www.icac.nsw.gov.au/images/Ricco

%20Public%20Website/Exhibit%20R97.pdf [Accessed 26 Jan. 2019].

Icaew.com. (2019). [online] Available at:

https://www.icaew.com/-/media/corporate/files/technical/iaa/materiality-in-the-audit-

of-financial-statements.ashx [Accessed 25 Jan. 2019].

Johnstone, K., Gramling, A. & Rittenberg, L.E., 2013. Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Knechel, W.R.& Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.