HI6026 Audit, Assurance & Compliance: Enhanced Reporting

VerifiedAdded on 2023/06/04

|18

|4421

|208

Report

AI Summary

This report evaluates enhanced auditor reporting in Australia, focusing on the roles and duties of auditors in providing assurance on financial statements, using CSR Limited as a case study. It examines compliance with Australian auditing standards, identifies key audit matters such as asset valuation and product liability provisions, and analyzes the auditor's (Deloitte) independence and remuneration. The report also discusses the audit committee's role, the audit opinion, and the responsibilities of management, directors, and auditors. Furthermore, it addresses material subsequent events, the effectiveness of material information, and any missing or under-reported aspects. The analysis offers insights into the quality of auditor's reports and their impact on stakeholders' decision-making.

Running head: AUDIT AND ASSURANCE

Audit and Assurance

Name of the Student

Name of the University

Author Note

Audit and Assurance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT AND ASSURANCE

Executive Summary

The auditors, in the contemporary periods, play crucial roles in accounting and

financial aspects of corporate scenarios in the global framework. The concerned report, in

this context, tries to analyse the roles and duties which the auditors play in the aspects of

assurance provision on the financial statements of the company into consideration, the CSR

Limited. For the purpose of the same, the important audit issues of the concerned company

are taken for analysis. The auditor in this case being Deloitte, the same has been analysed in

compliance with the Australian auditing standards. The report also emphasises on

identifying the key audit matters of the concerned company in its operational framework.

The report, thus, helps the readers to gain timely and appropriate information about the

auditor’s report quality regarding the concerned company, CSR Limited.

Executive Summary

The auditors, in the contemporary periods, play crucial roles in accounting and

financial aspects of corporate scenarios in the global framework. The concerned report, in

this context, tries to analyse the roles and duties which the auditors play in the aspects of

assurance provision on the financial statements of the company into consideration, the CSR

Limited. For the purpose of the same, the important audit issues of the concerned company

are taken for analysis. The auditor in this case being Deloitte, the same has been analysed in

compliance with the Australian auditing standards. The report also emphasises on

identifying the key audit matters of the concerned company in its operational framework.

The report, thus, helps the readers to gain timely and appropriate information about the

auditor’s report quality regarding the concerned company, CSR Limited.

2AUDIT AND ASSURANCE

Table of Contents

Introduction...............................................................................................................................3

Compliance with Auditor’s independence requirements..........................................................4

Services related to non-audit aspects........................................................................................4

Remuneration of the Auditor: Analysis......................................................................................5

Key Audit Matters......................................................................................................................7

a. Valuation of the assets.......................................................................................................7

b. Provision for product liability.............................................................................................8

Auditing Committee...................................................................................................................9

Audit Opinion...........................................................................................................................10

Responsibilities of management, directors, auditors: Differences..........................................11

Material Subsequent Event......................................................................................................11

Material information effectiveness: Assessment....................................................................12

Missing, under-reported or not fully reported aspects...........................................................12

Questions related to follow-up................................................................................................13

Conclusion................................................................................................................................13

References................................................................................................................................15

Table of Contents

Introduction...............................................................................................................................3

Compliance with Auditor’s independence requirements..........................................................4

Services related to non-audit aspects........................................................................................4

Remuneration of the Auditor: Analysis......................................................................................5

Key Audit Matters......................................................................................................................7

a. Valuation of the assets.......................................................................................................7

b. Provision for product liability.............................................................................................8

Auditing Committee...................................................................................................................9

Audit Opinion...........................................................................................................................10

Responsibilities of management, directors, auditors: Differences..........................................11

Material Subsequent Event......................................................................................................11

Material information effectiveness: Assessment....................................................................12

Missing, under-reported or not fully reported aspects...........................................................12

Questions related to follow-up................................................................................................13

Conclusion................................................................................................................................13

References................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT AND ASSURANCE

Introduction

The global business scenario has developed and has become more integrated,

inclusive as well as interconnected owing to factors like Globalisation, trade liberalisation

and technological and infrastructural developments. With the businesses going global and

becoming more complex, it has become immensely important for the same to have proper

accounting and financial framework, which gets monitored appropriately and regularly

(Kose, Otrok & Prasad, 2012). In this context, the term “Audit” comes into significance and

the same can be referred to as the process of analysis and interpretation of the financial

activities and statements of the companies for the purpose of ensuring accuracy and

appropriateness of the transactions recorded. The auditors, thus, are bestowed with the

role of revealing the relevant information related to the materialistic aspects of financial

activities and statements of the companies (Arens, Elder & Mark, 2012).

This is immensely important in the sense that the information is required by the

different stakeholders, who are associated with the businesses, for their decision-making

purposes. The audit companies pay immense importance to enhancement of the quality of

their reports, especially in the contemporary period of upsurge and complexities in business

activities, such that the stakeholders are increasingly benefitted (Louwers et al., 2015).

Keeping this into consideration, the concerned report aims to evaluate the latest annual

report of the concerned company, the CSR Limited, an Australian company venturing in the

production of building products, in the aspects of auditing, the audit partner of the company

for the year 2018, being Deloitte.

Introduction

The global business scenario has developed and has become more integrated,

inclusive as well as interconnected owing to factors like Globalisation, trade liberalisation

and technological and infrastructural developments. With the businesses going global and

becoming more complex, it has become immensely important for the same to have proper

accounting and financial framework, which gets monitored appropriately and regularly

(Kose, Otrok & Prasad, 2012). In this context, the term “Audit” comes into significance and

the same can be referred to as the process of analysis and interpretation of the financial

activities and statements of the companies for the purpose of ensuring accuracy and

appropriateness of the transactions recorded. The auditors, thus, are bestowed with the

role of revealing the relevant information related to the materialistic aspects of financial

activities and statements of the companies (Arens, Elder & Mark, 2012).

This is immensely important in the sense that the information is required by the

different stakeholders, who are associated with the businesses, for their decision-making

purposes. The audit companies pay immense importance to enhancement of the quality of

their reports, especially in the contemporary period of upsurge and complexities in business

activities, such that the stakeholders are increasingly benefitted (Louwers et al., 2015).

Keeping this into consideration, the concerned report aims to evaluate the latest annual

report of the concerned company, the CSR Limited, an Australian company venturing in the

production of building products, in the aspects of auditing, the audit partner of the company

for the year 2018, being Deloitte.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT AND ASSURANCE

Compliance with Auditor’s independence requirements

None of the members of the auditing company, Deloitte, were involved in any kind

of business related operations of the CSR Limited, as can be observed from the company’s

latest annual report (2018). There was also no presence of significant role played by any

particular employee in the auditing group, on the auditing actions of the concerned

company, which thus, goes in accordance to the “Section 342A of the Corporations Act

2001” (Javed, 2018). The auditing company also complies with the different requirements

which are present under the “Section 307C of the Corporations Act 2001”, the primary ones

of the requirements being as follows:

The applicable codes related to the professional conducts, mentioned in the

concerned section of the Corporations Act, have been abided by for the audit related

activities and operations of the CSR Limited Company (J. Clout, Chapple & Gandhi,

2013).

The requirement of independence of the auditors for the audit related operations in

the concerned organizations has also been abided by as there is no presence of

contraventions recorded in this aspect.

Services related to non-audit aspects

The auditing company, Deloitte, can also be seen to be providing different non-audit

related services to the CSR Limited, as is evident from the 2018 annual report of the

concerned business organization. These non-audit services are as follows:

Carbon and sustainability related assurance (Bae Choi, Lee & Psaros, 2013)

Other advisory and assurance related services

Compliance with Auditor’s independence requirements

None of the members of the auditing company, Deloitte, were involved in any kind

of business related operations of the CSR Limited, as can be observed from the company’s

latest annual report (2018). There was also no presence of significant role played by any

particular employee in the auditing group, on the auditing actions of the concerned

company, which thus, goes in accordance to the “Section 342A of the Corporations Act

2001” (Javed, 2018). The auditing company also complies with the different requirements

which are present under the “Section 307C of the Corporations Act 2001”, the primary ones

of the requirements being as follows:

The applicable codes related to the professional conducts, mentioned in the

concerned section of the Corporations Act, have been abided by for the audit related

activities and operations of the CSR Limited Company (J. Clout, Chapple & Gandhi,

2013).

The requirement of independence of the auditors for the audit related operations in

the concerned organizations has also been abided by as there is no presence of

contraventions recorded in this aspect.

Services related to non-audit aspects

The auditing company, Deloitte, can also be seen to be providing different non-audit

related services to the CSR Limited, as is evident from the 2018 annual report of the

concerned business organization. These non-audit services are as follows:

Carbon and sustainability related assurance (Bae Choi, Lee & Psaros, 2013)

Other advisory and assurance related services

5AUDIT AND ASSURANCE

For the former non-audit related service provided by Deloitte, the company has

received $77,108 from the CSR Limited and for the second service, Deloitte has received

$9,000 from the concerned client company. The amounts, in total, is nearly 10.40% of the

total remuneration amount which has been received by Deloitte for auditing the financial

aspects of the CSR Limited in the current year (2018). Both the organizations (the CSR

Limited as well as Deloitte) can be seen to be complying by the standards in the aspects of

receiving as well as providing the above-mentioned non-audit services.

As the non-audit services have complied to the general standard for the same (which

can be seen in the Corporations Act, 2001), the same has satisfied the directors, as per the

Risk and Audit Committee’s written report. It has also been ensured by the Directors of the

concerned client company, the CSR Limited, that the non-audit services provided by

Deloitte, does not include any kind of self-work review of the auditing personnel regarding

the aspects of management decision undertaking and similar domains (Junior, Best & Cotter,

2014). The regulatory framework present in the aspects of the corporate governance in the

domain of non-audit services have also been strictly followed and abided by the concerned

organization. These aspects, cumulatively, has made the role and the independence of the

concerned auditor in case of the latest auditing of the CSR Limited, unquestionable (Knechel

& Salterio, 2016).

Remuneration of the Auditor: Analysis

The remuneration received by Deloitte, for providing services to the CSR Limited, in

the period 2017-2018, can be seen to be as follows:

For the former non-audit related service provided by Deloitte, the company has

received $77,108 from the CSR Limited and for the second service, Deloitte has received

$9,000 from the concerned client company. The amounts, in total, is nearly 10.40% of the

total remuneration amount which has been received by Deloitte for auditing the financial

aspects of the CSR Limited in the current year (2018). Both the organizations (the CSR

Limited as well as Deloitte) can be seen to be complying by the standards in the aspects of

receiving as well as providing the above-mentioned non-audit services.

As the non-audit services have complied to the general standard for the same (which

can be seen in the Corporations Act, 2001), the same has satisfied the directors, as per the

Risk and Audit Committee’s written report. It has also been ensured by the Directors of the

concerned client company, the CSR Limited, that the non-audit services provided by

Deloitte, does not include any kind of self-work review of the auditing personnel regarding

the aspects of management decision undertaking and similar domains (Junior, Best & Cotter,

2014). The regulatory framework present in the aspects of the corporate governance in the

domain of non-audit services have also been strictly followed and abided by the concerned

organization. These aspects, cumulatively, has made the role and the independence of the

concerned auditor in case of the latest auditing of the CSR Limited, unquestionable (Knechel

& Salterio, 2016).

Remuneration of the Auditor: Analysis

The remuneration received by Deloitte, for providing services to the CSR Limited, in

the period 2017-2018, can be seen to be as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT AND ASSURANCE

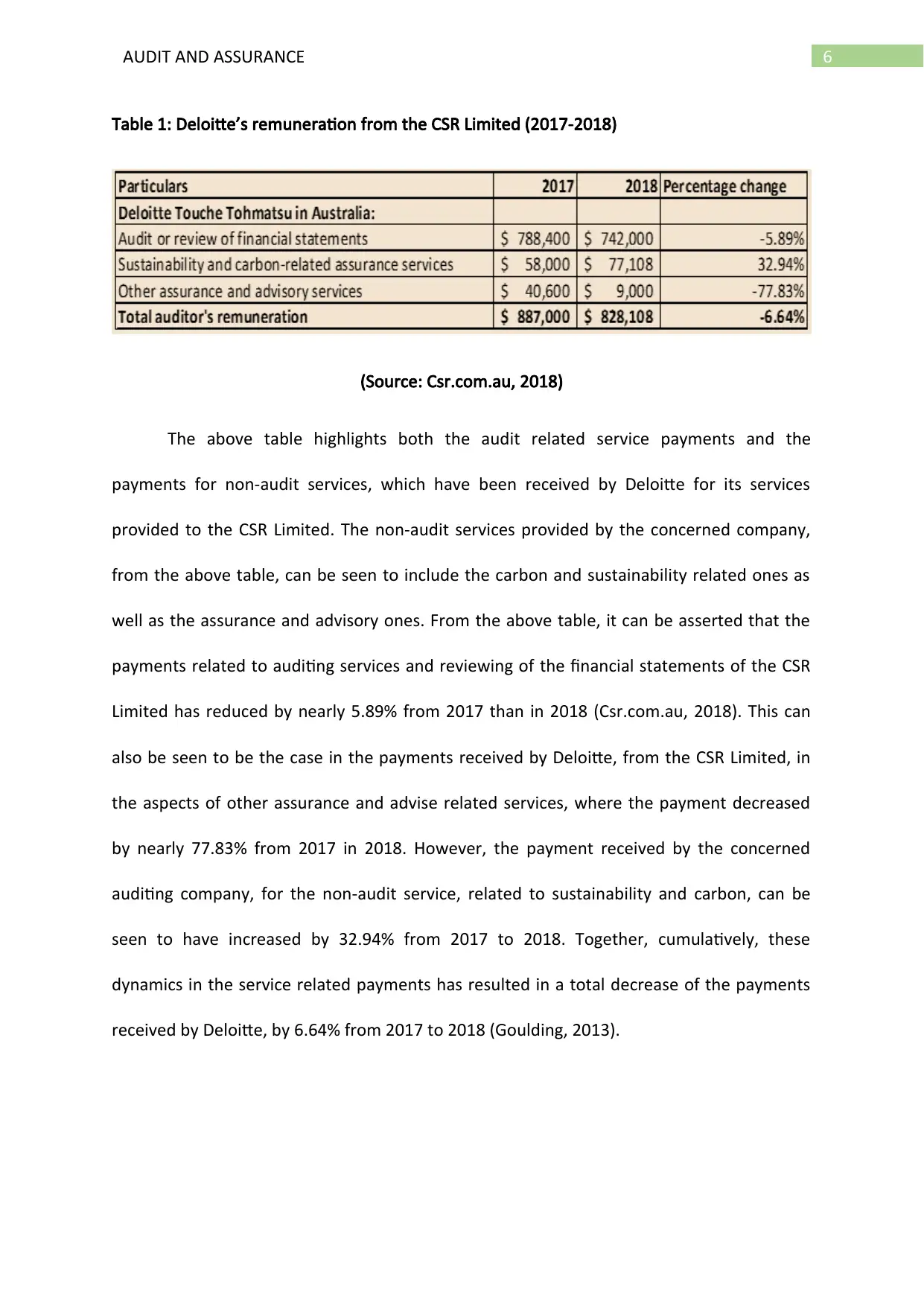

Table 1: Deloitte’s remuneration from the CSR Limited (2017-2018)

(Source: Csr.com.au, 2018)

The above table highlights both the audit related service payments and the

payments for non-audit services, which have been received by Deloitte for its services

provided to the CSR Limited. The non-audit services provided by the concerned company,

from the above table, can be seen to include the carbon and sustainability related ones as

well as the assurance and advisory ones. From the above table, it can be asserted that the

payments related to auditing services and reviewing of the financial statements of the CSR

Limited has reduced by nearly 5.89% from 2017 than in 2018 (Csr.com.au, 2018). This can

also be seen to be the case in the payments received by Deloitte, from the CSR Limited, in

the aspects of other assurance and advise related services, where the payment decreased

by nearly 77.83% from 2017 in 2018. However, the payment received by the concerned

auditing company, for the non-audit service, related to sustainability and carbon, can be

seen to have increased by 32.94% from 2017 to 2018. Together, cumulatively, these

dynamics in the service related payments has resulted in a total decrease of the payments

received by Deloitte, by 6.64% from 2017 to 2018 (Goulding, 2013).

Table 1: Deloitte’s remuneration from the CSR Limited (2017-2018)

(Source: Csr.com.au, 2018)

The above table highlights both the audit related service payments and the

payments for non-audit services, which have been received by Deloitte for its services

provided to the CSR Limited. The non-audit services provided by the concerned company,

from the above table, can be seen to include the carbon and sustainability related ones as

well as the assurance and advisory ones. From the above table, it can be asserted that the

payments related to auditing services and reviewing of the financial statements of the CSR

Limited has reduced by nearly 5.89% from 2017 than in 2018 (Csr.com.au, 2018). This can

also be seen to be the case in the payments received by Deloitte, from the CSR Limited, in

the aspects of other assurance and advise related services, where the payment decreased

by nearly 77.83% from 2017 in 2018. However, the payment received by the concerned

auditing company, for the non-audit service, related to sustainability and carbon, can be

seen to have increased by 32.94% from 2017 to 2018. Together, cumulatively, these

dynamics in the service related payments has resulted in a total decrease of the payments

received by Deloitte, by 6.64% from 2017 to 2018 (Goulding, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT AND ASSURANCE

Key Audit Matters

The key audit matters, in general, refer to the significant aspects which exist in the

domain of auditing and financial activities of an organization and which are thus needed to

be taken into consideration (Bédard, Gonthier-Besacier & Schatt, 2014). In this context, two

particular key audit matters can be seen to be observed, as per the 2018 annual report of

the concerned organization, the CSR Limited, which are discussed as follows:

a. Valuation of the assets

The annual report of the CSR Limited, 2018, highlights the presence of the following

assets valuation for the concerned company:

Goodwill amount – $98.1 million

Intangible assets (others) - $45.8 million

Plant, equipment and property- $834 million

Considerable clarity in the judgements is required for the purpose of analysing the

presence of any kind of impairments in such assets and their balances. For judging the same,

the aspects like discount tasks, inflation, growth rates, changes in building cycles as well as

the future cash flows estimation need to be incorporated in the judgement (Kachelmeier,

Schmidt & Valentine, 2017). For the purpose of detection of any kind of impairment in these

cash generating units, the CSR Limited can be seen to have designed an impairment

triggering assessment. The Viridian cash generating ones can be seen to be generating very

low returns on the capital employed, which in turn indicates towards the fact that further

evaluation of impairment is required in these cash generating units (Holm & Zaman, 2012).

Thus, due to the presence of the judgement related to the future cash flows in the

Key Audit Matters

The key audit matters, in general, refer to the significant aspects which exist in the

domain of auditing and financial activities of an organization and which are thus needed to

be taken into consideration (Bédard, Gonthier-Besacier & Schatt, 2014). In this context, two

particular key audit matters can be seen to be observed, as per the 2018 annual report of

the concerned organization, the CSR Limited, which are discussed as follows:

a. Valuation of the assets

The annual report of the CSR Limited, 2018, highlights the presence of the following

assets valuation for the concerned company:

Goodwill amount – $98.1 million

Intangible assets (others) - $45.8 million

Plant, equipment and property- $834 million

Considerable clarity in the judgements is required for the purpose of analysing the

presence of any kind of impairments in such assets and their balances. For judging the same,

the aspects like discount tasks, inflation, growth rates, changes in building cycles as well as

the future cash flows estimation need to be incorporated in the judgement (Kachelmeier,

Schmidt & Valentine, 2017). For the purpose of detection of any kind of impairment in these

cash generating units, the CSR Limited can be seen to have designed an impairment

triggering assessment. The Viridian cash generating ones can be seen to be generating very

low returns on the capital employed, which in turn indicates towards the fact that further

evaluation of impairment is required in these cash generating units (Holm & Zaman, 2012).

Thus, due to the presence of the judgement related to the future cash flows in the

8AUDIT AND ASSURANCE

concerned organization, this can be seen to be considered as one of the key audit matters of

the CSR Limited.

The auditing company, Deloitte, can be seen to be considering this key audit matter

and for the purpose of dealing with the same, it can be seen to analyse the management

process of its client company, with the aim of pointing out those cash generating units in

which further impairment assessment is required. In this process, insights about the annual

financial performance, consistency in segmental reporting, external market situations as

well as goodwill allocation to the cash generating units (especially those requiring further

impairment assessment) have been gained by the auditor, who in turn, can be seen to have

critically analysed the impairment model and impairment assessment methods and

assumptions of the company (Bell & Griffin, 2012). The accuracy and mathematical

efficiency of the cash flow models can also be seen to be examined with the help of sample

testing, thereby analysing the appropriateness of the aspects of disclosures in the

concerned client organization’s financial statements.

b. Provision for product liability

As per 31st March, 2018, the CSR Limited recognised a $289 million liability provision,

related to the disclosed as well as future claim which are foreseeable, linked to asbestos.

The advice of management appointed external advisors in the USA and Australia, has been

incorporated for ensuring the same. Thus, considerable judgement is required for the

purpose of ascertaining the future claim’s profitability in case of the provision and the

provision estimate is also influenced significantly by the assumptions related to the discount

rate as well as movements of the exchange rates over time. The variance in the complexities

concerned organization, this can be seen to be considered as one of the key audit matters of

the CSR Limited.

The auditing company, Deloitte, can be seen to be considering this key audit matter

and for the purpose of dealing with the same, it can be seen to analyse the management

process of its client company, with the aim of pointing out those cash generating units in

which further impairment assessment is required. In this process, insights about the annual

financial performance, consistency in segmental reporting, external market situations as

well as goodwill allocation to the cash generating units (especially those requiring further

impairment assessment) have been gained by the auditor, who in turn, can be seen to have

critically analysed the impairment model and impairment assessment methods and

assumptions of the company (Bell & Griffin, 2012). The accuracy and mathematical

efficiency of the cash flow models can also be seen to be examined with the help of sample

testing, thereby analysing the appropriateness of the aspects of disclosures in the

concerned client organization’s financial statements.

b. Provision for product liability

As per 31st March, 2018, the CSR Limited recognised a $289 million liability provision,

related to the disclosed as well as future claim which are foreseeable, linked to asbestos.

The advice of management appointed external advisors in the USA and Australia, has been

incorporated for ensuring the same. Thus, considerable judgement is required for the

purpose of ascertaining the future claim’s profitability in case of the provision and the

provision estimate is also influenced significantly by the assumptions related to the discount

rate as well as movements of the exchange rates over time. The variance in the complexities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT AND ASSURANCE

of the assumptions, thus, make this aspect one of the key audit matters, taken into

consideration by Deloitte (Gimbar, Hansen & Ozlanski, 2015).

The independence and the level of expertise and knowledge of the company hired

external experts can be seen to be evaluated by the auditing company, Deloitte, which also

critically analyses the suitability and appropriateness of the methodology and the

assumptions taken into consideration by these external experts. For assessing the

consideration and exclusions of the asbestos related claims, the company can also be seen

to be using the sample testing method. The provisions, being designed and formulated on

the basis of the reports, this becomes extremely significant for the auditing aspects and

procedures. Deloitte has also conducted enquiry about both the external experts appointed

by the CSR Limited as well as the internal and the external legal counsel for the concerned

company. The auditor can also be seen to analyse the level of suitability of those of the

pertinent disclosures which are present in the financial statements of the concerned client

company.

Auditing Committee

The Directors of the concerned organization, as per the annual report (2018) of the

same, can be seen to have developed the “Risk and Audit Committee”, with the primary aim

of the same being that of reviewing the procedures and policy frameworks of the companies

in the aspects of imposition of internal controls for the asset and liability protection and

ensuring integrity in the aspects of financial reporting of the CSR Limited (Lary & Taylor,

2012). The four non-executive directors of the company, in their Risk and Audit Committee

are:

John Gillam

of the assumptions, thus, make this aspect one of the key audit matters, taken into

consideration by Deloitte (Gimbar, Hansen & Ozlanski, 2015).

The independence and the level of expertise and knowledge of the company hired

external experts can be seen to be evaluated by the auditing company, Deloitte, which also

critically analyses the suitability and appropriateness of the methodology and the

assumptions taken into consideration by these external experts. For assessing the

consideration and exclusions of the asbestos related claims, the company can also be seen

to be using the sample testing method. The provisions, being designed and formulated on

the basis of the reports, this becomes extremely significant for the auditing aspects and

procedures. Deloitte has also conducted enquiry about both the external experts appointed

by the CSR Limited as well as the internal and the external legal counsel for the concerned

company. The auditor can also be seen to analyse the level of suitability of those of the

pertinent disclosures which are present in the financial statements of the concerned client

company.

Auditing Committee

The Directors of the concerned organization, as per the annual report (2018) of the

same, can be seen to have developed the “Risk and Audit Committee”, with the primary aim

of the same being that of reviewing the procedures and policy frameworks of the companies

in the aspects of imposition of internal controls for the asset and liability protection and

ensuring integrity in the aspects of financial reporting of the CSR Limited (Lary & Taylor,

2012). The four non-executive directors of the company, in their Risk and Audit Committee

are:

John Gillam

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT AND ASSURANCE

Penny Winn

Matthew Quinn

Mike Ihlein

The primary roles of the concerned committee can be seen to be as follows:

Analysing the assuring procedures of the integrity in the aspects of financial

reporting of the concerned company

Analysing and evaluating the audit risk management framework present within the

concerned company (Brennan & Kirwan, 2015)

Evaluation and assessment of the dynamics related to that of commercial income

realisation and any kind of influences working in this aspect in the concerned

company

The annual report of the CSR Limited, in 2018, however, does not show any evidence

regarding that of the charter of the concerned audit committee.

Audit Opinion

The report of the independent auditor highlights that the concerned organization

has abided by the “Section 300A of the Corporations Act 2001”, for the purpose of

formation of the remuneration report. The financial reports and statements of the

organization, as per the independent auditor, have also been formed, under the regulatory

framework of the “International Accounting Standards Board”, “Australian Accounting

Standards Board” and the “International Financial Reporting Standards” (Shah, 2012). The

financial conditions and dynamics of the CSR Limited has been accurately represented in its

financial reports, as per the assertions of the independent auditor as there is no presence of

wrong statements and claims. Thus, unqualified opinions can be seen to be provided by

Penny Winn

Matthew Quinn

Mike Ihlein

The primary roles of the concerned committee can be seen to be as follows:

Analysing the assuring procedures of the integrity in the aspects of financial

reporting of the concerned company

Analysing and evaluating the audit risk management framework present within the

concerned company (Brennan & Kirwan, 2015)

Evaluation and assessment of the dynamics related to that of commercial income

realisation and any kind of influences working in this aspect in the concerned

company

The annual report of the CSR Limited, in 2018, however, does not show any evidence

regarding that of the charter of the concerned audit committee.

Audit Opinion

The report of the independent auditor highlights that the concerned organization

has abided by the “Section 300A of the Corporations Act 2001”, for the purpose of

formation of the remuneration report. The financial reports and statements of the

organization, as per the independent auditor, have also been formed, under the regulatory

framework of the “International Accounting Standards Board”, “Australian Accounting

Standards Board” and the “International Financial Reporting Standards” (Shah, 2012). The

financial conditions and dynamics of the CSR Limited has been accurately represented in its

financial reports, as per the assertions of the independent auditor as there is no presence of

wrong statements and claims. Thus, unqualified opinions can be seen to be provided by

11AUDIT AND ASSURANCE

Deloitte, regarding that of the CSR Limited, after analysing their financial aspects and after

conducting fieldwork in their effectiveness testing (Mock et al., 2012).

Responsibilities of management, directors, auditors: Differences

There exist different variations in the roles and responsibilities of the directors,

management and the auditors, in the aspects of development of the financial reports for the

concerned organization, the CSR Limited, as is evident from the latest annual report of the

concerned company. One of the primary responsibilities of the directors of the concerned

company is that of analysing the organization’s capacity to continue as a growing concern

(Nobes, 2014). Moreover, the management and the directors of the company also need to

formulate the financial statements and reports of the CSR Limited, in compliance to the

regulations and the accounting standards which prevail in the country (Australia) where the

company ventures.

The auditors, however, have different responsibilities, in the sense that it is their role

to effectively assure whether the financial reports formed by the concerned company, are

devoid of erroneous statements or not. Apart from this main role, the auditors, in this case,

also have several other responsibilities like that of detection of risks which arise from

misstatements of the company, examining the appropriateness of the accounting policies,

analysing the internal control, evaluating the accounting basis used by the company’s

directors, collecting relevant audit evidences and also examining the representation of the

financial reports and statements as formed by the concerned client organization, the CSR

Limited.

Deloitte, regarding that of the CSR Limited, after analysing their financial aspects and after

conducting fieldwork in their effectiveness testing (Mock et al., 2012).

Responsibilities of management, directors, auditors: Differences

There exist different variations in the roles and responsibilities of the directors,

management and the auditors, in the aspects of development of the financial reports for the

concerned organization, the CSR Limited, as is evident from the latest annual report of the

concerned company. One of the primary responsibilities of the directors of the concerned

company is that of analysing the organization’s capacity to continue as a growing concern

(Nobes, 2014). Moreover, the management and the directors of the company also need to

formulate the financial statements and reports of the CSR Limited, in compliance to the

regulations and the accounting standards which prevail in the country (Australia) where the

company ventures.

The auditors, however, have different responsibilities, in the sense that it is their role

to effectively assure whether the financial reports formed by the concerned company, are

devoid of erroneous statements or not. Apart from this main role, the auditors, in this case,

also have several other responsibilities like that of detection of risks which arise from

misstatements of the company, examining the appropriateness of the accounting policies,

analysing the internal control, evaluating the accounting basis used by the company’s

directors, collecting relevant audit evidences and also examining the representation of the

financial reports and statements as formed by the concerned client organization, the CSR

Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.