Audit and Assurance - Threats, Safeguards, and Independence

VerifiedAdded on 2020/02/24

|6

|1041

|156

Homework Assignment

AI Summary

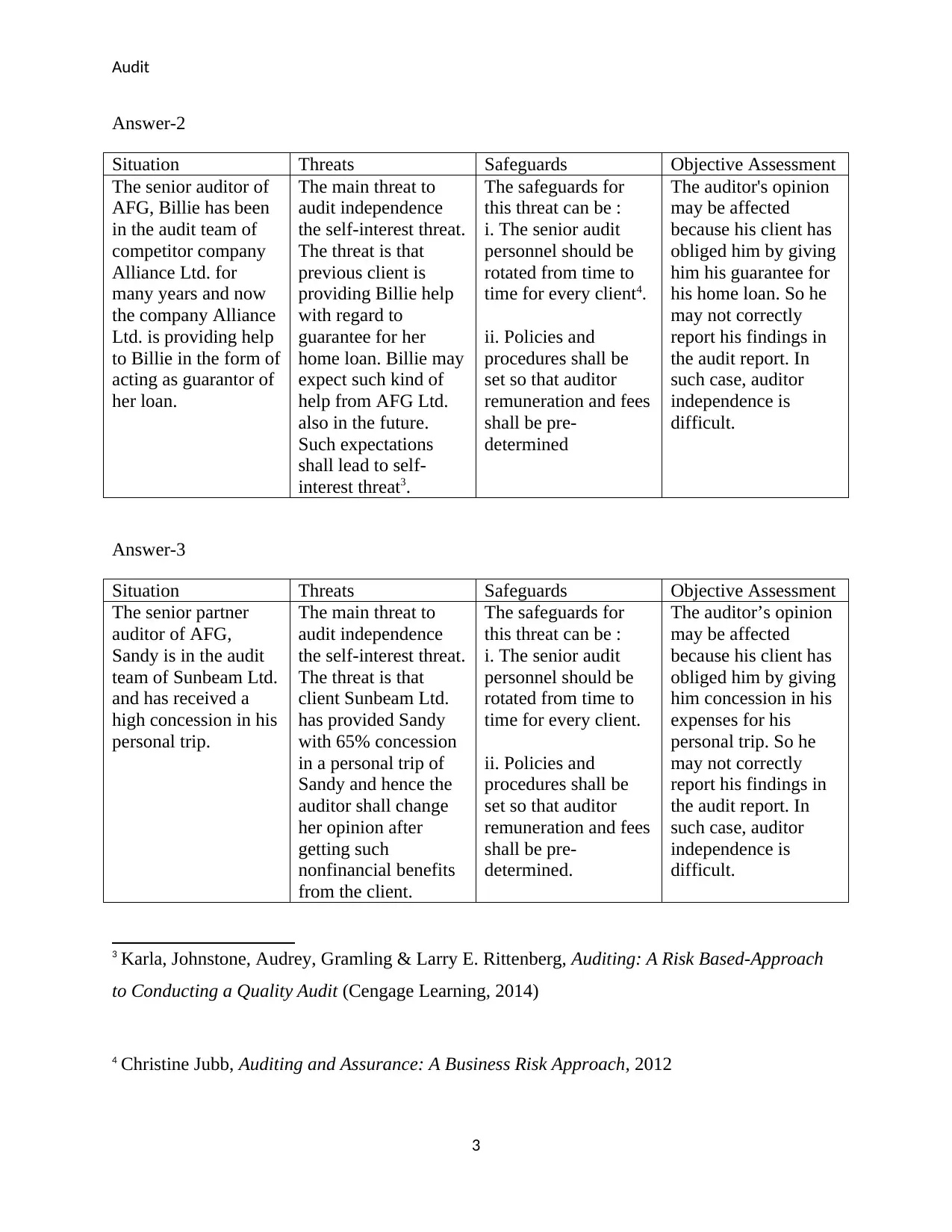

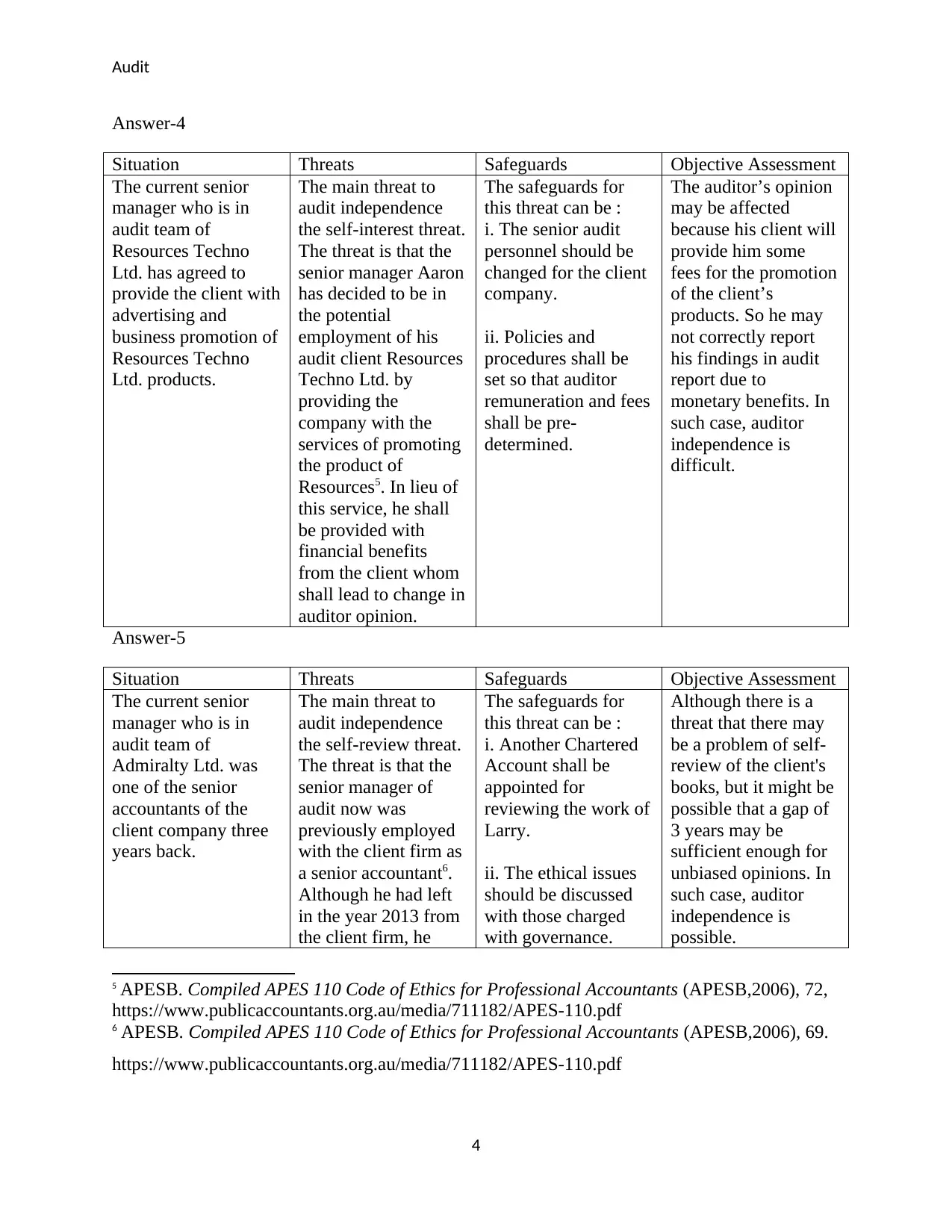

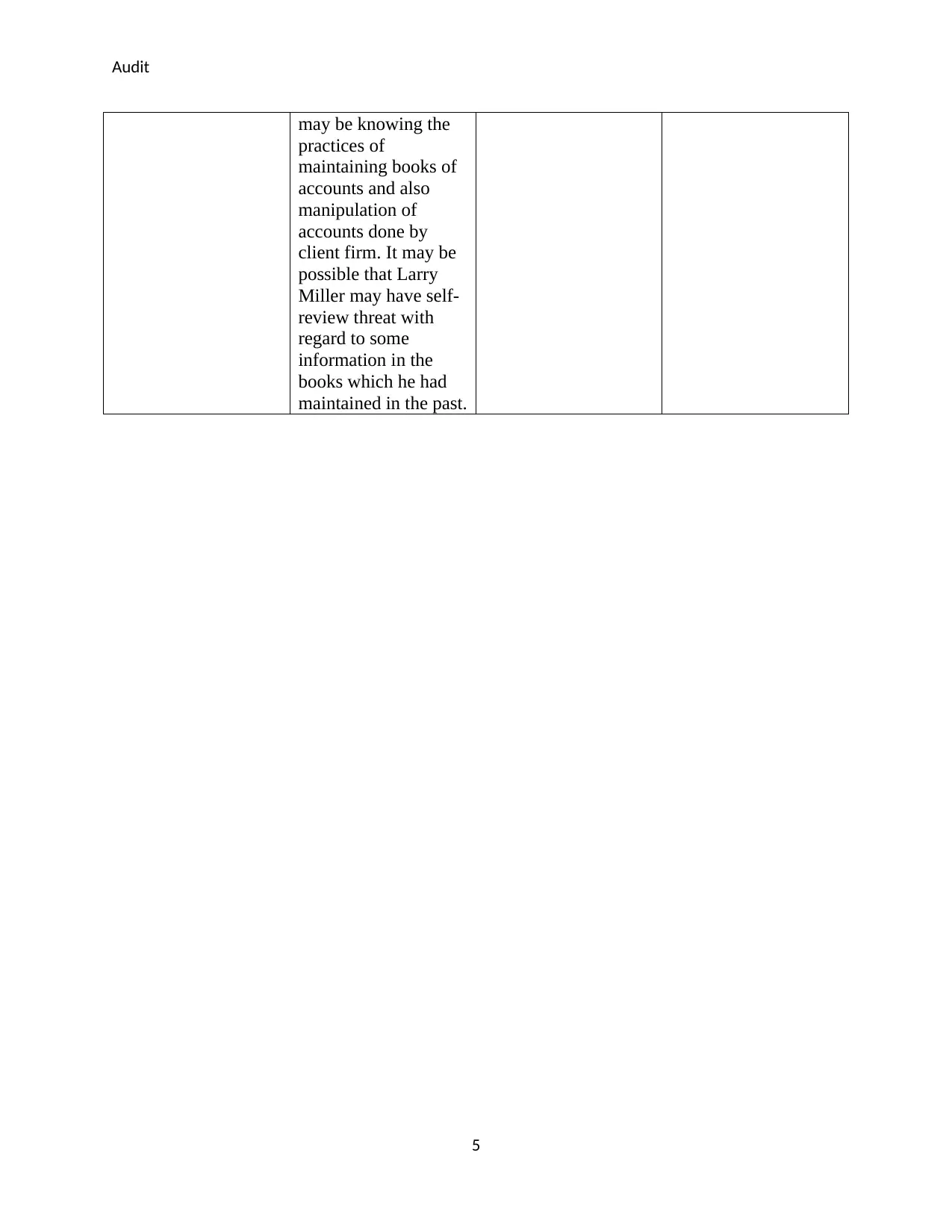

This assignment solution addresses various scenarios related to audit and assurance, focusing on threats to auditor independence and the implementation of safeguards. The solution analyzes five distinct situations, each presenting a potential threat to auditor objectivity, such as self-review and self-interest threats. For each scenario, the assignment identifies the specific threat, assesses its potential impact on the auditor's opinion, and proposes safeguards to mitigate the risk. These safeguards include measures like rotating audit personnel, assigning tasks to third parties, and establishing clear policies on auditor remuneration and benefits. The assignment also considers the impact of previous employment relationships and personal relationships on auditor independence, providing a comprehensive overview of ethical considerations in auditing. The analysis highlights the importance of maintaining objectivity and the challenges auditors face in upholding their professional responsibilities.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.