Audit and Assurance: Key Matters and Responsibilities of Auditors

VerifiedAdded on 2023/06/04

|15

|3406

|104

AI Summary

This article discusses the key audit matters and responsibilities of auditors in ensuring the accuracy and reliability of financial reports. It covers the independence declaration, non-audit services, remuneration, and role of auditors in reviewing key audit matters. The article also includes a case study of AGL Energy Limited.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDIT AND ASSURANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT AND ASSURANCE: 1

Executive summary

The new audit program released after 2015 pertains to communicate key audit matters in the

independence report of Auditor. It includes the obligation of the auditor to communicate the

key audit matters with the report of judgment regarding the performance of financial report

especially for accuracy. The purpose of involving the key matter is to increase the value of

communication of auditors. This enables more transparency in the auditor`s work.

Executive summary

The new audit program released after 2015 pertains to communicate key audit matters in the

independence report of Auditor. It includes the obligation of the auditor to communicate the

key audit matters with the report of judgment regarding the performance of financial report

especially for accuracy. The purpose of involving the key matter is to increase the value of

communication of auditors. This enables more transparency in the auditor`s work.

AUDIT AND ASSURANCE: 2

Contents

Executive summary...............................................................................................................................1

Introduction...........................................................................................................................................3

Auditor’s Independence Declaration.....................................................................................................3

Independent auditor’s report..................................................................................................................4

Non-Audit services performed by the Auditor.......................................................................................4

Auditors’ remuneration..........................................................................................................................5

Director`s responsibility differs from auditor`s responsibility for financial reports...............................6

Functions of Auditor..............................................................................................................................7

Composition of the Audit Committee....................................................................................................7

Role of Auditor......................................................................................................................................7

Auditor`s responsibility related to financial report-...........................................................................7

Independent Auditors report to the members.........................................................................................8

Review all Key Audit Matters noted and the associated audit procedures.............................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Contents

Executive summary...............................................................................................................................1

Introduction...........................................................................................................................................3

Auditor’s Independence Declaration.....................................................................................................3

Independent auditor’s report..................................................................................................................4

Non-Audit services performed by the Auditor.......................................................................................4

Auditors’ remuneration..........................................................................................................................5

Director`s responsibility differs from auditor`s responsibility for financial reports...............................6

Functions of Auditor..............................................................................................................................7

Composition of the Audit Committee....................................................................................................7

Role of Auditor......................................................................................................................................7

Auditor`s responsibility related to financial report-...........................................................................7

Independent Auditors report to the members.........................................................................................8

Review all Key Audit Matters noted and the associated audit procedures.............................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

AUDIT AND ASSURANCE: 3

Introduction

These days, the role of transparency plays an important role in maintain trust among the

stakeholders. To meet this purpose, companies releases its Annual report and to check hoe far

these reports are reliable, company hires a team of auditors in order to keep a review over the

executive members. The report has detailed information of various relevant topics related to

auditor`s declaration, report of independent auditor, non-audit services delegated by auditors,

remuneration of Auditor, roles and responsibilities of auditor and finally review of auditor`s

report after analysing the annual reports. By delegating and communication the key audit

matters to the stakeholders and users of the annual reports, it help them in make an

appropriate investment decision. By communicating the annual reports, a user can apprehend

the diverse nature of the organisation. The below discussion brings out the analysis of

auditor`s report of AGL ENERGY LIMITED. The report answer what auditing aspect do the

company follows and what are the objectives of hiring independent auditors (Ajmi, and

Saudagaran, 2011).

Auditor’s Independence Declaration

The essential service commission prioritises the implication of retail audit program in the

company. The aim of the audit report is to provide commission and consumers of energy with

the independent assurance. These energy retail licensees have suitable system, policies, and

processes on the workplace. Moreover, the auditor should make assure that the company

complies with the necessary regulatory compliances and obligations. When the breaches on

part of the company occurs, the retail audit has to identify and compensate the breach.

Apart from this, the auditors has announced an unbiased and a clear opinion of the financial

situation of the AGL as per their knowledge and experience criteria. According to auditors of

the company, the financial statements are prepared by following proper accounting standards.

Introduction

These days, the role of transparency plays an important role in maintain trust among the

stakeholders. To meet this purpose, companies releases its Annual report and to check hoe far

these reports are reliable, company hires a team of auditors in order to keep a review over the

executive members. The report has detailed information of various relevant topics related to

auditor`s declaration, report of independent auditor, non-audit services delegated by auditors,

remuneration of Auditor, roles and responsibilities of auditor and finally review of auditor`s

report after analysing the annual reports. By delegating and communication the key audit

matters to the stakeholders and users of the annual reports, it help them in make an

appropriate investment decision. By communicating the annual reports, a user can apprehend

the diverse nature of the organisation. The below discussion brings out the analysis of

auditor`s report of AGL ENERGY LIMITED. The report answer what auditing aspect do the

company follows and what are the objectives of hiring independent auditors (Ajmi, and

Saudagaran, 2011).

Auditor’s Independence Declaration

The essential service commission prioritises the implication of retail audit program in the

company. The aim of the audit report is to provide commission and consumers of energy with

the independent assurance. These energy retail licensees have suitable system, policies, and

processes on the workplace. Moreover, the auditor should make assure that the company

complies with the necessary regulatory compliances and obligations. When the breaches on

part of the company occurs, the retail audit has to identify and compensate the breach.

Apart from this, the auditors has announced an unbiased and a clear opinion of the financial

situation of the AGL as per their knowledge and experience criteria. According to auditors of

the company, the financial statements are prepared by following proper accounting standards.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT AND ASSURANCE: 4

The auditors have advised the company to improve its calculation methodology of assets and

liabilities and asked to resubmit the revised document as per the KPI. Auditors expect

independence during the audit. In addition to this, auditors experienced and embraced

independence delegated by directors (AGL, 2018).

Independent auditor’s report

While conducting the AGL`s audit, the auditors are complied to the independence

requirements of Corporation Act 2001. The independence policy has the details of the

procedures for the recruiting, appointing, and reviewing the independence of external auditor.

The audit and risk committee has conducted a tender process related to the provision of

external audit services. According to the independence policy, external auditor has prohibited

to provide any service that could hamper and threaten their independence through conflicts

and compliance role. As per the audit executed by the Australian auditing standards, these

auditors do not use their independence in a wrong way. Auditors exercise professional

evaluation and maintain professional scepticism during the whole audit (Auditing and

Assurance Standards Board, 2015).

Non-Audit services performed by the Auditor

As per the annual report of the AGL ENERGY LIMITED (2013), external auditors named

Deloitte touche tohmatsu provided the non-audit services to the company. Although, the

company has the formal policy for the provision of auditing services. Moreover, the directors

of the company are satisfied as the provision of $107000 of non-audit services are provided

by the external auditors (Deloitte, 2017). The policy and procedure reviewed by Audit and

Risk Management committee managed to conclude from the director`s side that the non-audit

services provided do not hamper independence requirement of external auditor in the

corporation Act. No executive member of the company is the part of Audit and risk

The auditors have advised the company to improve its calculation methodology of assets and

liabilities and asked to resubmit the revised document as per the KPI. Auditors expect

independence during the audit. In addition to this, auditors experienced and embraced

independence delegated by directors (AGL, 2018).

Independent auditor’s report

While conducting the AGL`s audit, the auditors are complied to the independence

requirements of Corporation Act 2001. The independence policy has the details of the

procedures for the recruiting, appointing, and reviewing the independence of external auditor.

The audit and risk committee has conducted a tender process related to the provision of

external audit services. According to the independence policy, external auditor has prohibited

to provide any service that could hamper and threaten their independence through conflicts

and compliance role. As per the audit executed by the Australian auditing standards, these

auditors do not use their independence in a wrong way. Auditors exercise professional

evaluation and maintain professional scepticism during the whole audit (Auditing and

Assurance Standards Board, 2015).

Non-Audit services performed by the Auditor

As per the annual report of the AGL ENERGY LIMITED (2013), external auditors named

Deloitte touche tohmatsu provided the non-audit services to the company. Although, the

company has the formal policy for the provision of auditing services. Moreover, the directors

of the company are satisfied as the provision of $107000 of non-audit services are provided

by the external auditors (Deloitte, 2017). The policy and procedure reviewed by Audit and

Risk Management committee managed to conclude from the director`s side that the non-audit

services provided do not hamper independence requirement of external auditor in the

corporation Act. No executive member of the company is the part of Audit and risk

AUDIT AND ASSURANCE: 5

committee. Some non-audit services provided by the auditor include tax planning,

consultancy services, system integration, advice related to wealth maximisation, consulting

related to insolvency case and the project that are not connected to the audit or review of an

company`s financial statements. The non-audit services do not affect the general principles

related to their independence is detailed in APES 110 code of conduct for the professional

accountants (Goh, Krishnan, and Li, 2013).

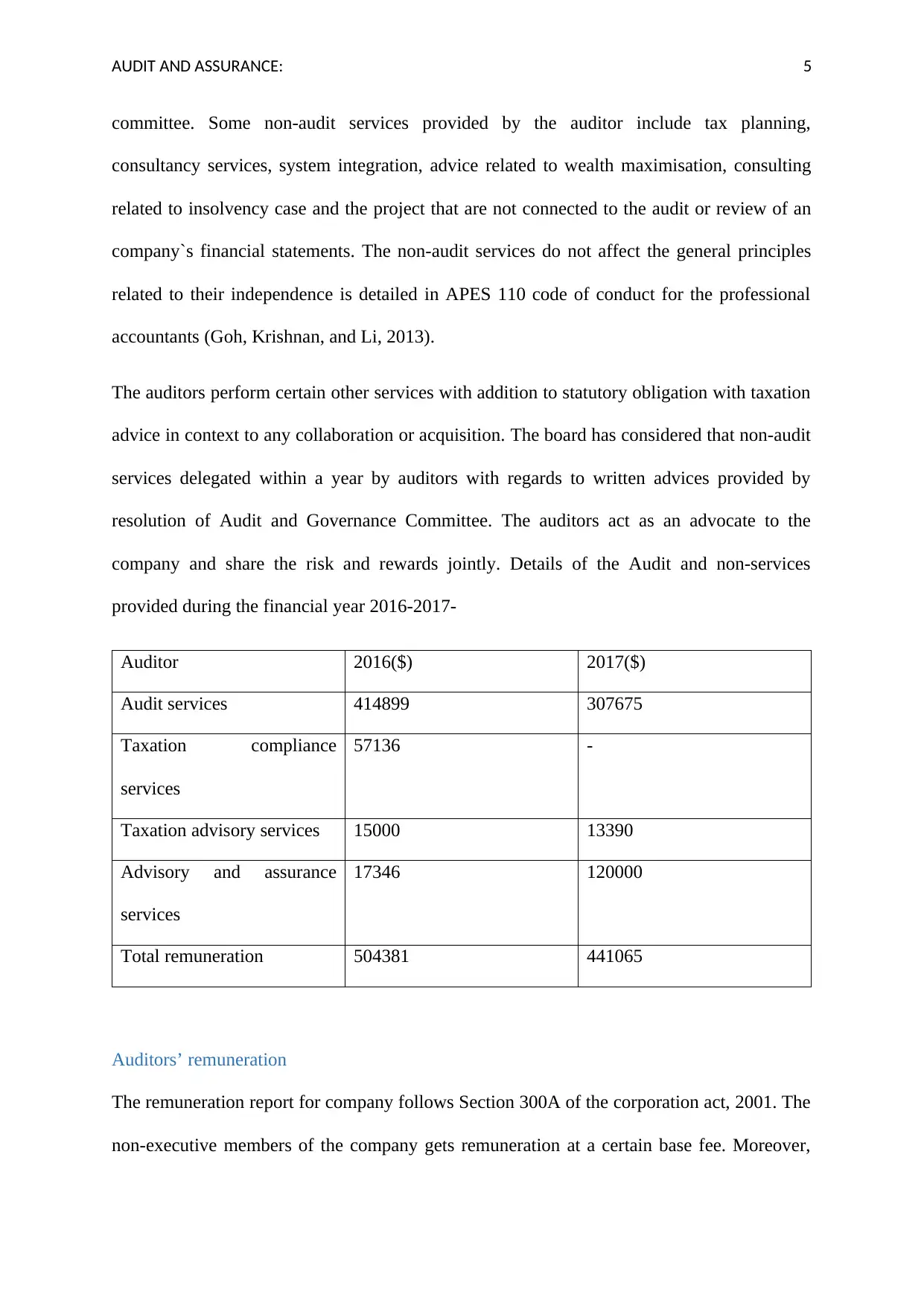

The auditors perform certain other services with addition to statutory obligation with taxation

advice in context to any collaboration or acquisition. The board has considered that non-audit

services delegated within a year by auditors with regards to written advices provided by

resolution of Audit and Governance Committee. The auditors act as an advocate to the

company and share the risk and rewards jointly. Details of the Audit and non-services

provided during the financial year 2016-2017-

Auditor 2016($) 2017($)

Audit services 414899 307675

Taxation compliance

services

57136 -

Taxation advisory services 15000 13390

Advisory and assurance

services

17346 120000

Total remuneration 504381 441065

Auditors’ remuneration

The remuneration report for company follows Section 300A of the corporation act, 2001. The

non-executive members of the company gets remuneration at a certain base fee. Moreover,

committee. Some non-audit services provided by the auditor include tax planning,

consultancy services, system integration, advice related to wealth maximisation, consulting

related to insolvency case and the project that are not connected to the audit or review of an

company`s financial statements. The non-audit services do not affect the general principles

related to their independence is detailed in APES 110 code of conduct for the professional

accountants (Goh, Krishnan, and Li, 2013).

The auditors perform certain other services with addition to statutory obligation with taxation

advice in context to any collaboration or acquisition. The board has considered that non-audit

services delegated within a year by auditors with regards to written advices provided by

resolution of Audit and Governance Committee. The auditors act as an advocate to the

company and share the risk and rewards jointly. Details of the Audit and non-services

provided during the financial year 2016-2017-

Auditor 2016($) 2017($)

Audit services 414899 307675

Taxation compliance

services

57136 -

Taxation advisory services 15000 13390

Advisory and assurance

services

17346 120000

Total remuneration 504381 441065

Auditors’ remuneration

The remuneration report for company follows Section 300A of the corporation act, 2001. The

non-executive members of the company gets remuneration at a certain base fee. Moreover,

AUDIT AND ASSURANCE: 6

when it is found that they are facing huge workload and more responsibilities by participating

in board committee. They also receive committee fee. The chairman of the committee tend to

attract high rated remuneration and several short and long-term incentives. Whereas, the

chairman of board receives no extra for operating and heading committees. The remuneration

to non-executive directors is $2.5 million every year and this amount is discussed and

approved by general meetings with shareholders (AGL`s Annual report, 2017). Auditor and

non-executive member`s fees follows the board`s advice from the independent advisers of

remuneration that include market comparison of amount paid to directors as a remuneration

in a comparator group of same sized companies.

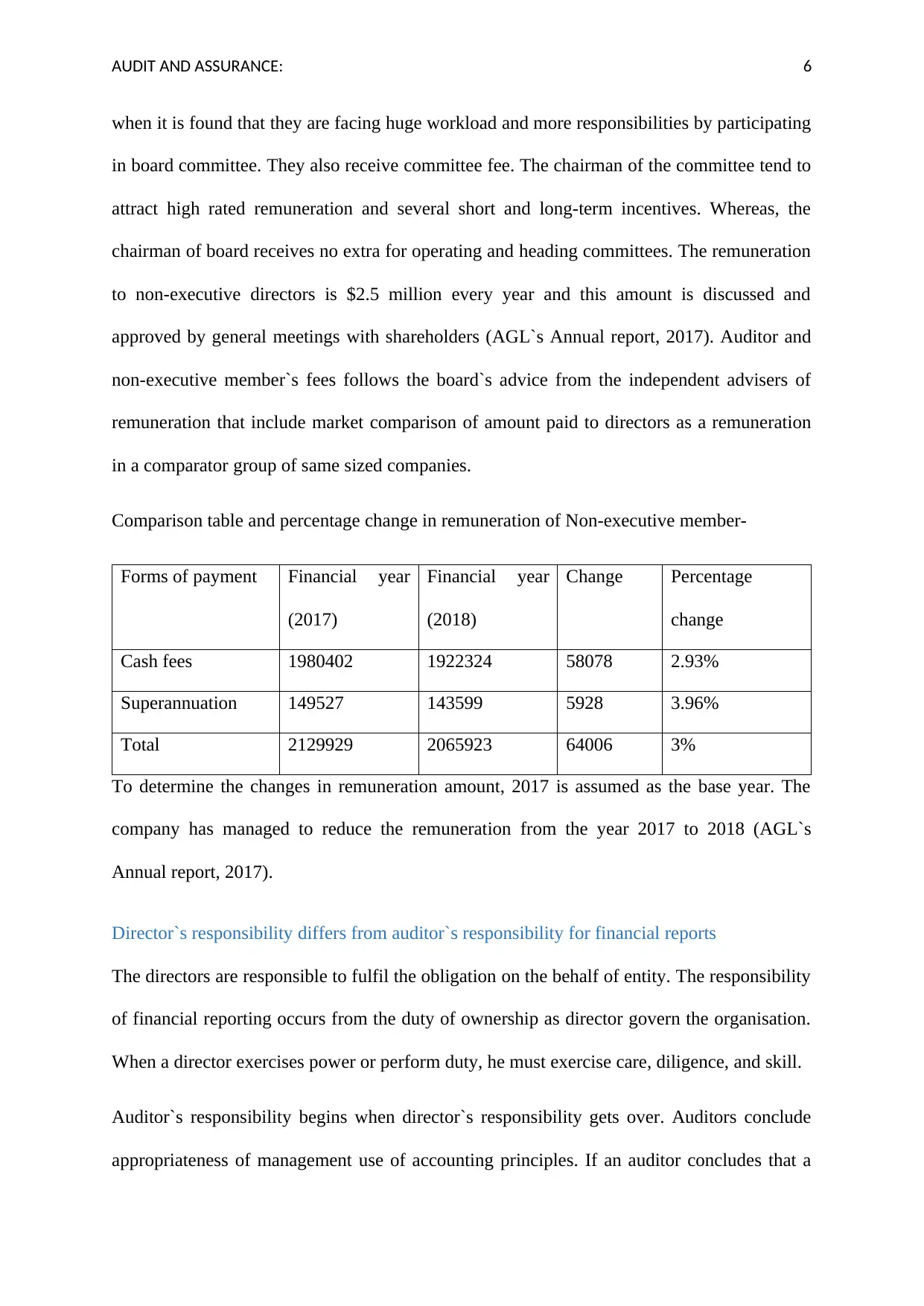

Comparison table and percentage change in remuneration of Non-executive member-

Forms of payment Financial year

(2017)

Financial year

(2018)

Change Percentage

change

Cash fees 1980402 1922324 58078 2.93%

Superannuation 149527 143599 5928 3.96%

Total 2129929 2065923 64006 3%

To determine the changes in remuneration amount, 2017 is assumed as the base year. The

company has managed to reduce the remuneration from the year 2017 to 2018 (AGL`s

Annual report, 2017).

Director`s responsibility differs from auditor`s responsibility for financial reports

The directors are responsible to fulfil the obligation on the behalf of entity. The responsibility

of financial reporting occurs from the duty of ownership as director govern the organisation.

When a director exercises power or perform duty, he must exercise care, diligence, and skill.

Auditor`s responsibility begins when director`s responsibility gets over. Auditors conclude

appropriateness of management use of accounting principles. If an auditor concludes that a

when it is found that they are facing huge workload and more responsibilities by participating

in board committee. They also receive committee fee. The chairman of the committee tend to

attract high rated remuneration and several short and long-term incentives. Whereas, the

chairman of board receives no extra for operating and heading committees. The remuneration

to non-executive directors is $2.5 million every year and this amount is discussed and

approved by general meetings with shareholders (AGL`s Annual report, 2017). Auditor and

non-executive member`s fees follows the board`s advice from the independent advisers of

remuneration that include market comparison of amount paid to directors as a remuneration

in a comparator group of same sized companies.

Comparison table and percentage change in remuneration of Non-executive member-

Forms of payment Financial year

(2017)

Financial year

(2018)

Change Percentage

change

Cash fees 1980402 1922324 58078 2.93%

Superannuation 149527 143599 5928 3.96%

Total 2129929 2065923 64006 3%

To determine the changes in remuneration amount, 2017 is assumed as the base year. The

company has managed to reduce the remuneration from the year 2017 to 2018 (AGL`s

Annual report, 2017).

Director`s responsibility differs from auditor`s responsibility for financial reports

The directors are responsible to fulfil the obligation on the behalf of entity. The responsibility

of financial reporting occurs from the duty of ownership as director govern the organisation.

When a director exercises power or perform duty, he must exercise care, diligence, and skill.

Auditor`s responsibility begins when director`s responsibility gets over. Auditors conclude

appropriateness of management use of accounting principles. If an auditor concludes that a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT AND ASSURANCE: 7

material uncertainty exists that are related to events and conditions that may impose

significant doubt on the ability of the company to maintain the financial statements (Chan and

Vasarhelyi, 2018).

Functions of Auditor

The primary function of establishing an Audit and Risk management committee by the board

is to assist the board of directors to fulfil, assist, and reflect the fair and reliable financial

reports to protect the interest of shareholders, customers, and employees. Despite these, it

protects the broader community through effective identification, monitoring, assessment, and

management of risks (CPA Australia, 2014).

The auditor make sure that notices sent to AGL`s shareholders related to financial reporting

comply with the guidelines issued by ASX. Shareholder has the right to submit written

questions to the auditor in context to conduct of audit and independence report. In addition to

this, shareholders are given an opportunity to ask some relevant question regarding the

conduct of audit and accounting policies followed by the organisation (Annual report, 2016).

Composition of the Audit Committee

Under the company`s charter, the composition of the audit and risk management committee

must be in such a manner at least three members where all of them should be independent

and non-executive directors. The charter ensures that all of the members of the audit

committee should have strong knowledge base of basic accounting and finance practises. The

committee comprises of five members named John Stanhope, Bruce Phillips, Les Hosking,

Belinda Hutchinson and Sandra McPhee. John is the chairperson of the committee who has

expertise in finance as a qualified accountant. Bruce Phillips and Les Hosking has worked in

energy sector before. Sandra McPhee was the director of the same company since 2006 and

has an extensive knowledge and experience of consumer-oriented businesses.

material uncertainty exists that are related to events and conditions that may impose

significant doubt on the ability of the company to maintain the financial statements (Chan and

Vasarhelyi, 2018).

Functions of Auditor

The primary function of establishing an Audit and Risk management committee by the board

is to assist the board of directors to fulfil, assist, and reflect the fair and reliable financial

reports to protect the interest of shareholders, customers, and employees. Despite these, it

protects the broader community through effective identification, monitoring, assessment, and

management of risks (CPA Australia, 2014).

The auditor make sure that notices sent to AGL`s shareholders related to financial reporting

comply with the guidelines issued by ASX. Shareholder has the right to submit written

questions to the auditor in context to conduct of audit and independence report. In addition to

this, shareholders are given an opportunity to ask some relevant question regarding the

conduct of audit and accounting policies followed by the organisation (Annual report, 2016).

Composition of the Audit Committee

Under the company`s charter, the composition of the audit and risk management committee

must be in such a manner at least three members where all of them should be independent

and non-executive directors. The charter ensures that all of the members of the audit

committee should have strong knowledge base of basic accounting and finance practises. The

committee comprises of five members named John Stanhope, Bruce Phillips, Les Hosking,

Belinda Hutchinson and Sandra McPhee. John is the chairperson of the committee who has

expertise in finance as a qualified accountant. Bruce Phillips and Les Hosking has worked in

energy sector before. Sandra McPhee was the director of the same company since 2006 and

has an extensive knowledge and experience of consumer-oriented businesses.

AUDIT AND ASSURANCE: 8

Role of Auditor

Auditor`s responsibility related to financial report-

The role of auditor is to monitor the reliability of financial reporting and review the corporate

reporting according to the required applicable framework.

To analyse whether the book value of assets and the liabilities is accounted fairly or not

(Deumes et al., 2012).

Apart from the audit services, auditors also undertakes and delegates non-audit services to the

organisation. The audit and charter committee gives the advice on laws and compliance and

make familiar the remaining management staff about the new statutory regulations (Buckless,

Krawczyk, and Showalter, 2014).

To review how far the estimated policies and accounting judgements are applied to the

financial statements of the organisation.

Audit and risk committee recommend and recruit new independent auditors to work with the

internal auditing team.

Independent Auditors report to the members

AGL`s external auditors attend the annual general meeting. The auditors ensure that they not

only work for the organisation rather they represent the financial condition of the company to

the shareholders. An auditor is a trust holder, who set a link between organisation and

shareholders. Auditors identify the risk association of material misstatement of the financial

statements due to fraud (Auditing and Assurance Standards Board, 2013). Auditors perform

those audit procedures, which are responsive to risk to obtain and detect whether the audit

evidence is capable enough to provide a viewpoint to the shareholders. The risk occurred due

to error, forgery, misrepresentation, override of internal control audit, international omission,

and a fraud might involve collusion (George, Theofanis, and Konstantinos, 2015). External

Role of Auditor

Auditor`s responsibility related to financial report-

The role of auditor is to monitor the reliability of financial reporting and review the corporate

reporting according to the required applicable framework.

To analyse whether the book value of assets and the liabilities is accounted fairly or not

(Deumes et al., 2012).

Apart from the audit services, auditors also undertakes and delegates non-audit services to the

organisation. The audit and charter committee gives the advice on laws and compliance and

make familiar the remaining management staff about the new statutory regulations (Buckless,

Krawczyk, and Showalter, 2014).

To review how far the estimated policies and accounting judgements are applied to the

financial statements of the organisation.

Audit and risk committee recommend and recruit new independent auditors to work with the

internal auditing team.

Independent Auditors report to the members

AGL`s external auditors attend the annual general meeting. The auditors ensure that they not

only work for the organisation rather they represent the financial condition of the company to

the shareholders. An auditor is a trust holder, who set a link between organisation and

shareholders. Auditors identify the risk association of material misstatement of the financial

statements due to fraud (Auditing and Assurance Standards Board, 2013). Auditors perform

those audit procedures, which are responsive to risk to obtain and detect whether the audit

evidence is capable enough to provide a viewpoint to the shareholders. The risk occurred due

to error, forgery, misrepresentation, override of internal control audit, international omission,

and a fraud might involve collusion (George, Theofanis, and Konstantinos, 2015). External

AUDIT AND ASSURANCE: 9

auditors obtain a understanding of internal auditors that control and relating it to audit in

order to design the procedures of audit which are appropriate in the certain situations.

However, not from the purpose of appreciating the opinion`s effectiveness of the group`s

internal control. Nevertheless, mainly for the purpose to provide a satisfaction to shareholders

(Auditing and Assurance Standards Board, 2015). Evaluation of the appropriateness of the

director`s statement to use the going concern feature of the business. While checking whether

appropriateness of director is through the accounting, audit service. To check whether there

exist a material uncertainty and how it to related to events and conditions that may cause

doubt on the group`s ability to manipulate the books of accounts (Chan, and Vasarhelyi,

2018).

Review all Key Audit Matters noted and the associated audit procedures

Since from 2015, international Auditing and Assurance standard board has been established

which has new requirements. From this time, the auditors of an Australian company was

obliged to report the key audit matters and auditors of all the company will have to make

important changes as per the guidelines in IAASB (essential services commission victoria,

2014).

The auditors have recommended that AGL ensure the methodology of calculation to be

accurate in future. The auditor has asked to resubmit the updated KPI data and save the

modified version of KPI data to support the submission. The auditor discovers a potential

weakness in managing the prices to the price comparator website (CPA Australia Ltd, 2018).

The scope of company`s auditor responded to these key Audit Matters-

The review was not only limited to understand the key control management but determined

the estimation of cost accrual. The key audit matters understand and challenge management’s

estimation regarding the volume and tariffs that are used in the distributing cost accruals. The

auditors obtain a understanding of internal auditors that control and relating it to audit in

order to design the procedures of audit which are appropriate in the certain situations.

However, not from the purpose of appreciating the opinion`s effectiveness of the group`s

internal control. Nevertheless, mainly for the purpose to provide a satisfaction to shareholders

(Auditing and Assurance Standards Board, 2015). Evaluation of the appropriateness of the

director`s statement to use the going concern feature of the business. While checking whether

appropriateness of director is through the accounting, audit service. To check whether there

exist a material uncertainty and how it to related to events and conditions that may cause

doubt on the group`s ability to manipulate the books of accounts (Chan, and Vasarhelyi,

2018).

Review all Key Audit Matters noted and the associated audit procedures

Since from 2015, international Auditing and Assurance standard board has been established

which has new requirements. From this time, the auditors of an Australian company was

obliged to report the key audit matters and auditors of all the company will have to make

important changes as per the guidelines in IAASB (essential services commission victoria,

2014).

The auditors have recommended that AGL ensure the methodology of calculation to be

accurate in future. The auditor has asked to resubmit the updated KPI data and save the

modified version of KPI data to support the submission. The auditor discovers a potential

weakness in managing the prices to the price comparator website (CPA Australia Ltd, 2018).

The scope of company`s auditor responded to these key Audit Matters-

The review was not only limited to understand the key control management but determined

the estimation of cost accrual. The key audit matters understand and challenge management’s

estimation regarding the volume and tariffs that are used in the distributing cost accruals. The

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT AND ASSURANCE: 10

audit committee agrees that the volume data that has been underlying in the calculation of

volumes into sales, purchases, and other systems (AGL Energy Limited, 2013). Moreover,

auditor compare the prices by individual distributor and tariff tables. Auditors play an

important role in assessing the appropriate AGL`s unbilled distribution cost. Apart from this,

auditors perform sensitivity analysis near the key drivers of long-term growth that is used to

forecast the cash flow and discount rate. More in depth analysis of auditor`s report reveals

that on February, 2016, AGL has admitted that it has adopted strategic decision that

production and exploration related to natural gas assets will be no longer a core operating

business of the company.

Audit procedure include indicator of impairment that company has utilised its valuation

experts to help the auditors in calculating some key assumption and their impact on carrying

value of assets. Some indicators to carry out impairment activities include forecasting of gas

prices, gas production capacity, discount rate, estimated cost of reintegration, various capital

expenditure estimates (Petraşcu, and Tieanu, 2014).

Conclusion

From the above discussion, it can be concluded that after going through the financial

statements of the AGL Energy Limited, Auditor`s performance tend to be perfect. The

auditors advice the company to change its calculation methodology. All the mandatory

information required by the stakeholders is clearly and concise mentioned. Rather using the

more technical terms, the auditors have provided the advantage to shareholders to ask the

questions regarding their independence or accounting principles. The report has a

comparative analysis of remuneration of current fiscal years 2017 and 2018. Undoubtedly,

the assessed material information helps the stakeholders to make their investment decision.

Auditor undertake the responsibility to undertake and increase the overall result and

efficiency by valuing effective retail audit program. There are such questions that are not

audit committee agrees that the volume data that has been underlying in the calculation of

volumes into sales, purchases, and other systems (AGL Energy Limited, 2013). Moreover,

auditor compare the prices by individual distributor and tariff tables. Auditors play an

important role in assessing the appropriate AGL`s unbilled distribution cost. Apart from this,

auditors perform sensitivity analysis near the key drivers of long-term growth that is used to

forecast the cash flow and discount rate. More in depth analysis of auditor`s report reveals

that on February, 2016, AGL has admitted that it has adopted strategic decision that

production and exploration related to natural gas assets will be no longer a core operating

business of the company.

Audit procedure include indicator of impairment that company has utilised its valuation

experts to help the auditors in calculating some key assumption and their impact on carrying

value of assets. Some indicators to carry out impairment activities include forecasting of gas

prices, gas production capacity, discount rate, estimated cost of reintegration, various capital

expenditure estimates (Petraşcu, and Tieanu, 2014).

Conclusion

From the above discussion, it can be concluded that after going through the financial

statements of the AGL Energy Limited, Auditor`s performance tend to be perfect. The

auditors advice the company to change its calculation methodology. All the mandatory

information required by the stakeholders is clearly and concise mentioned. Rather using the

more technical terms, the auditors have provided the advantage to shareholders to ask the

questions regarding their independence or accounting principles. The report has a

comparative analysis of remuneration of current fiscal years 2017 and 2018. Undoubtedly,

the assessed material information helps the stakeholders to make their investment decision.

Auditor undertake the responsibility to undertake and increase the overall result and

efficiency by valuing effective retail audit program. There are such questions that are not

AUDIT AND ASSURANCE: 11

answered by the auditors of the company. Moreover, after answering the questions, the

auditor also advice the company to use appropriate method of accounting principles.

answered by the auditors of the company. Moreover, after answering the questions, the

auditor also advice the company to use appropriate method of accounting principles.

AUDIT AND ASSURANCE: 12

References

AGL Energy Limited, (2013) AGL Energy Limited 2013 Annual Report. [online] Available

on:

http://www.annualreports.com/HostedData/AnnualReportArchive/a/ASX_AGK.AX_2013.pd

f [Accessed on 20/09/18]

AGL, (2018) Annual report, (2018) [online] Available on:

https://www.agl.com.au/-/media/aglmedia/documents/about-agl/investors/annual-reports/

180809-2018annualreport1829055.pdf?

la=en&hash=E788FF0DAEEC20BB5C21C9C232396170880D78AE [Accessed on 20/09/18]

AGL`s Annual report, (2017) Annual report. [online] Available on:

http://agl2017.reportonline.com.au/sites/agl2017.reportonline.com.au/files/agl_ar_2017.pdf

Ajmi, A. J., and Saudagaran, S. (2011). Perceptions of Auditors and Financial-Statement

Users Regarding Auditor Independence in Bahrain. Managerial Auditing Journal, Vol. 26,

No. 2, pp. 130-160.

Annual report, (2016) Independent Auditor`s report. [online] Available on:

http://agl2016.annual-report.com.au/financials/independent-auditors-report [Accessed on

20/09/18]

Auditing and Assurance Standards Board (2013) Auditing Standard ASA 315 Identifying and

Assessing the Risks of Material Misstatement through Understanding the Entity and Its

Environment [online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_A

SA_315.pdf [Accessed 14th September , 2018].

References

AGL Energy Limited, (2013) AGL Energy Limited 2013 Annual Report. [online] Available

on:

http://www.annualreports.com/HostedData/AnnualReportArchive/a/ASX_AGK.AX_2013.pd

f [Accessed on 20/09/18]

AGL, (2018) Annual report, (2018) [online] Available on:

https://www.agl.com.au/-/media/aglmedia/documents/about-agl/investors/annual-reports/

180809-2018annualreport1829055.pdf?

la=en&hash=E788FF0DAEEC20BB5C21C9C232396170880D78AE [Accessed on 20/09/18]

AGL`s Annual report, (2017) Annual report. [online] Available on:

http://agl2017.reportonline.com.au/sites/agl2017.reportonline.com.au/files/agl_ar_2017.pdf

Ajmi, A. J., and Saudagaran, S. (2011). Perceptions of Auditors and Financial-Statement

Users Regarding Auditor Independence in Bahrain. Managerial Auditing Journal, Vol. 26,

No. 2, pp. 130-160.

Annual report, (2016) Independent Auditor`s report. [online] Available on:

http://agl2016.annual-report.com.au/financials/independent-auditors-report [Accessed on

20/09/18]

Auditing and Assurance Standards Board (2013) Auditing Standard ASA 315 Identifying and

Assessing the Risks of Material Misstatement through Understanding the Entity and Its

Environment [online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_A

SA_315.pdf [Accessed 14th September , 2018].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT AND ASSURANCE: 13

Auditing and Assurance Standards Board (2015) Auditing Standard ASA 200 Overall

Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with

Australian Auditing Standards [online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_200_Compiled_2015.pdf

[Accessed 14th September , 2018].

Auditing and Assurance Standards Board (2015) Auditing Standard ASA 570 Going Concern

[online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [Accessed 14th

September , 2018].

Buckless, F. A., Krawczyk, K. and Showalter, D. S., (2014) Using virtual worlds to simulate

real-world audit procedures. Issues in Accounting Education, 29(3), pp. 389-417.

Chan, D. Y. and Vasarhelyi, M. A., (2018) Innovation and practice of continuous auditing. In

Continuous Auditing: Theory and Application. UK: Emerald Publishing Limited.

CPA Australia (2014) A guide to understanding annual reports: Australian Listed

Companies. CPA Australia Ltd.

CPA Australia Ltd, (2018) Audit & Risk Committee Charter. Available on:

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/about/audit-risk-

committee-charter.pdf [Accessed on 20/09/18]

Deloitte (2017) Australian financial reporting guide financial reporting periods ending on or

after 31 December 2016. Deloitte Touche Tohmatsu.

Deumes, R., Schelleman, C., Vander Bauwhede, H. and Vanstraelen, A. ( 2012) Audit firm

governance: Do transparency reports reveal audit quality?. Auditing: A Journal of Practice &

Theory, 31(4), pp. 193-214.

Auditing and Assurance Standards Board (2015) Auditing Standard ASA 200 Overall

Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with

Australian Auditing Standards [online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_200_Compiled_2015.pdf

[Accessed 14th September , 2018].

Auditing and Assurance Standards Board (2015) Auditing Standard ASA 570 Going Concern

[online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [Accessed 14th

September , 2018].

Buckless, F. A., Krawczyk, K. and Showalter, D. S., (2014) Using virtual worlds to simulate

real-world audit procedures. Issues in Accounting Education, 29(3), pp. 389-417.

Chan, D. Y. and Vasarhelyi, M. A., (2018) Innovation and practice of continuous auditing. In

Continuous Auditing: Theory and Application. UK: Emerald Publishing Limited.

CPA Australia (2014) A guide to understanding annual reports: Australian Listed

Companies. CPA Australia Ltd.

CPA Australia Ltd, (2018) Audit & Risk Committee Charter. Available on:

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/about/audit-risk-

committee-charter.pdf [Accessed on 20/09/18]

Deloitte (2017) Australian financial reporting guide financial reporting periods ending on or

after 31 December 2016. Deloitte Touche Tohmatsu.

Deumes, R., Schelleman, C., Vander Bauwhede, H. and Vanstraelen, A. ( 2012) Audit firm

governance: Do transparency reports reveal audit quality?. Auditing: A Journal of Practice &

Theory, 31(4), pp. 193-214.

AUDIT AND ASSURANCE: 14

ESSENTIAL SERVICES COMMISSION VICTORIA, (2014) AGL AUDIT REPORT

SUMMARY AND COMMISSION RESPONSE. [online] Available on:

https://www.esc.vic.gov.au/sites/default/files/documents/AGL-Audit-Report-Summary.pdf

[Accessed on 20/09/18]

George, D., Theofanis, K. and Konstantinos, A., (2015) Factors associated with internal audit

effectiveness: Evidence from Greece. Journal of Accounting and Taxation, 7(7), pp. 113-122.

Goh, B.W., Krishnan, J. and Li, D. (2013) Auditor reporting under Section 404: The

association between the internal control and going concern audit opinions. Contemporary

Accounting Research, 30(3), pp. 970-995.

Petraşcu, D. and Tieanu, A., (2014) The role of internal audit in fraud prevention and

detection. Procedia Economics and Finance, 16, pp. 489-497.

ESSENTIAL SERVICES COMMISSION VICTORIA, (2014) AGL AUDIT REPORT

SUMMARY AND COMMISSION RESPONSE. [online] Available on:

https://www.esc.vic.gov.au/sites/default/files/documents/AGL-Audit-Report-Summary.pdf

[Accessed on 20/09/18]

George, D., Theofanis, K. and Konstantinos, A., (2015) Factors associated with internal audit

effectiveness: Evidence from Greece. Journal of Accounting and Taxation, 7(7), pp. 113-122.

Goh, B.W., Krishnan, J. and Li, D. (2013) Auditor reporting under Section 404: The

association between the internal control and going concern audit opinions. Contemporary

Accounting Research, 30(3), pp. 970-995.

Petraşcu, D. and Tieanu, A., (2014) The role of internal audit in fraud prevention and

detection. Procedia Economics and Finance, 16, pp. 489-497.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.