ACCT20075 - Audit Assignment 1: JB Hi-Fi Financial Report Analysis

VerifiedAdded on 2023/06/07

|14

|2571

|446

Report

AI Summary

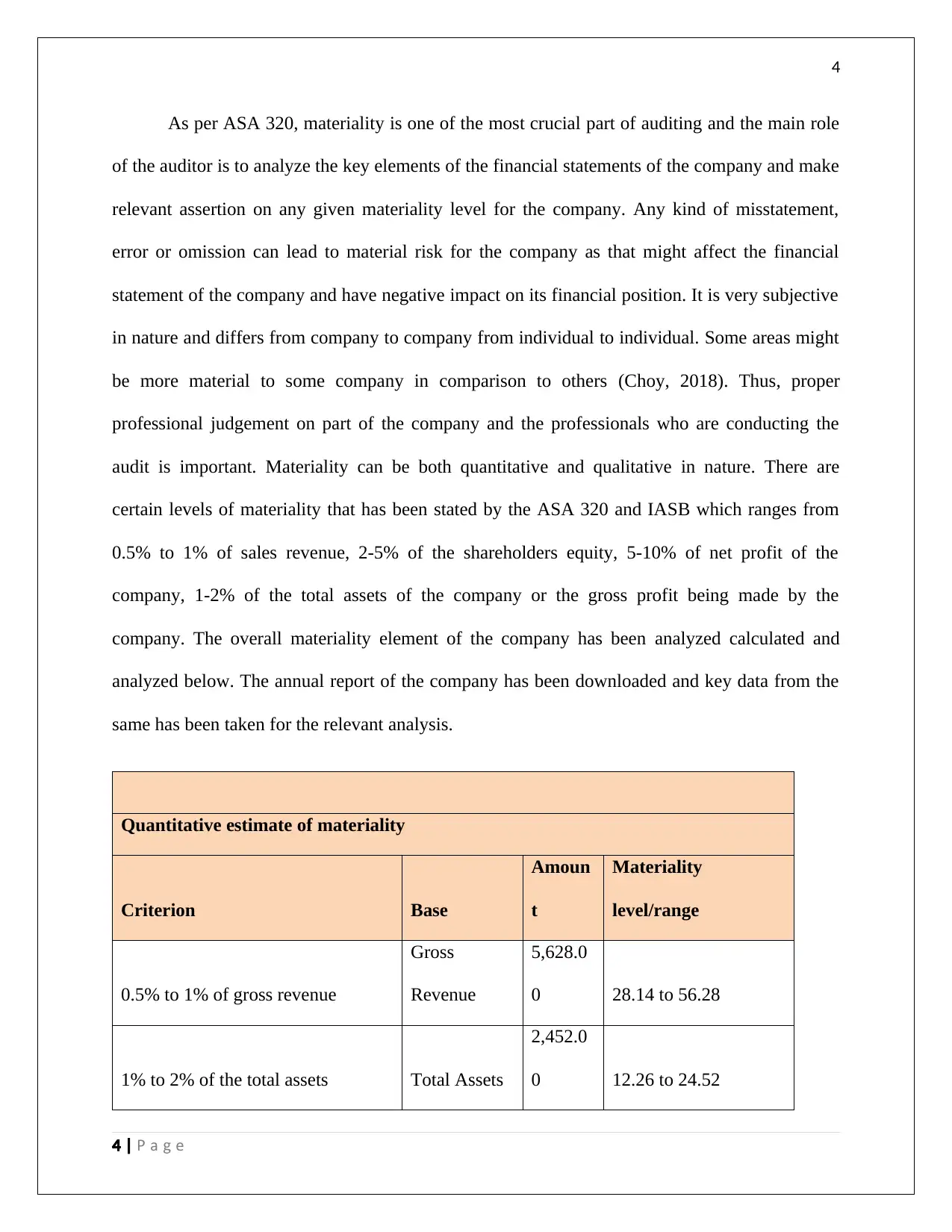

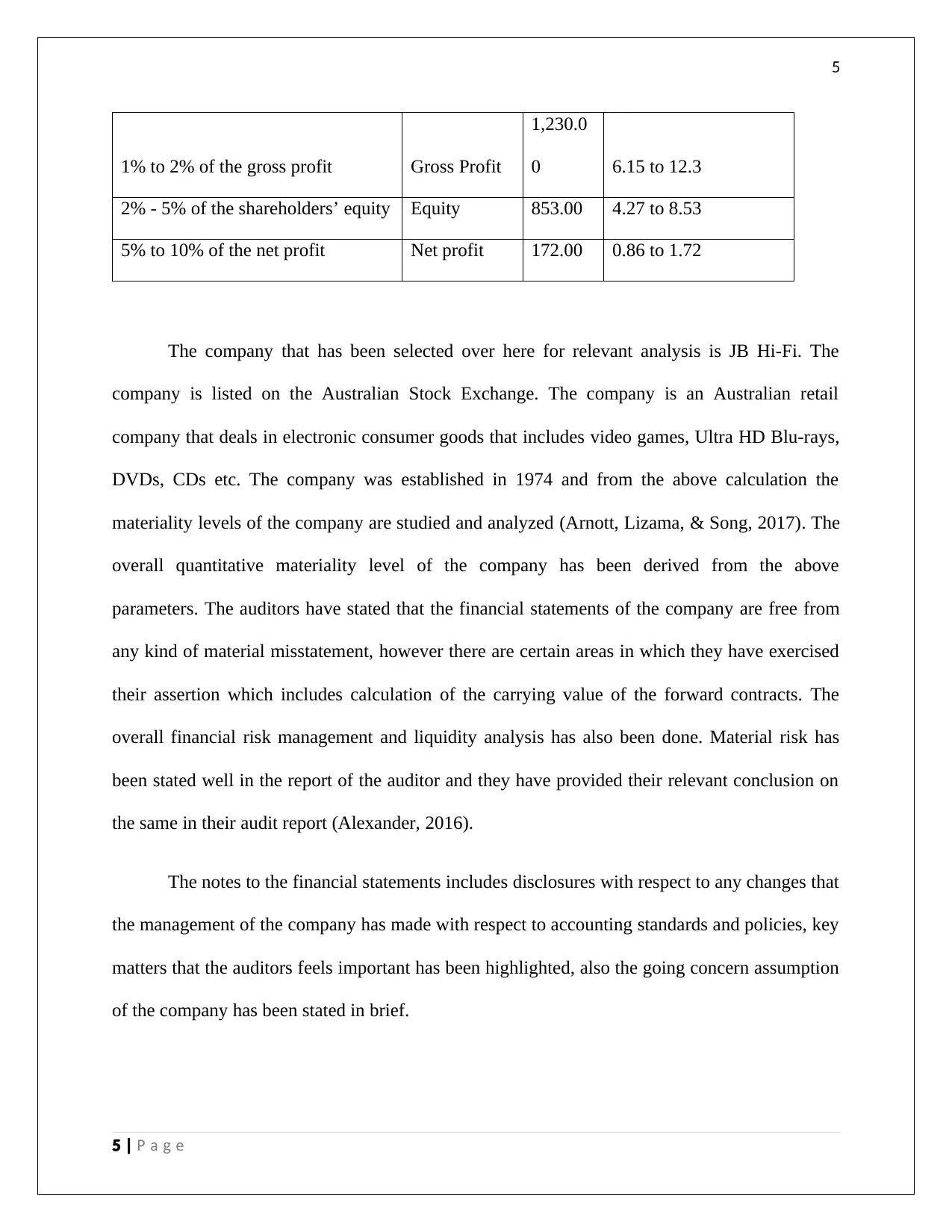

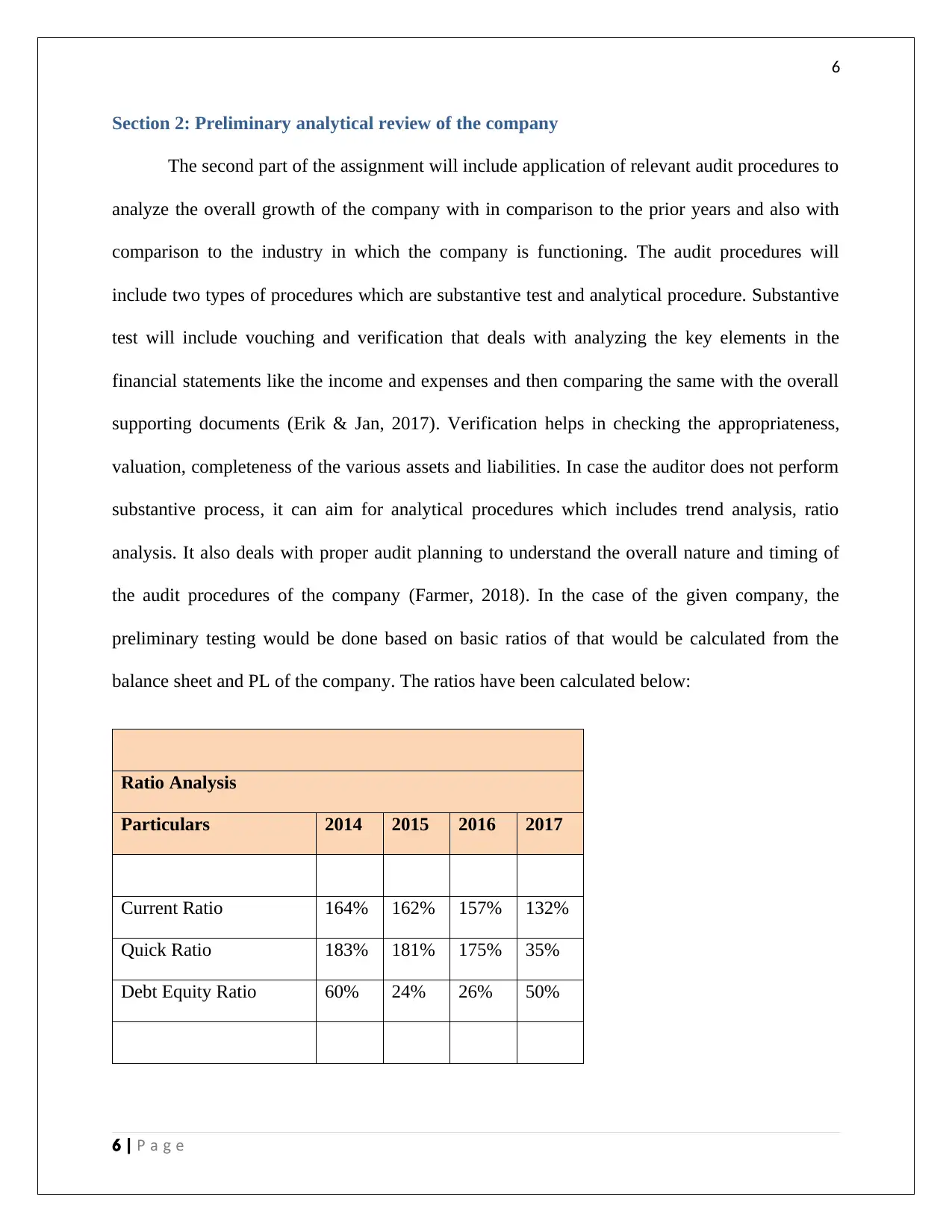

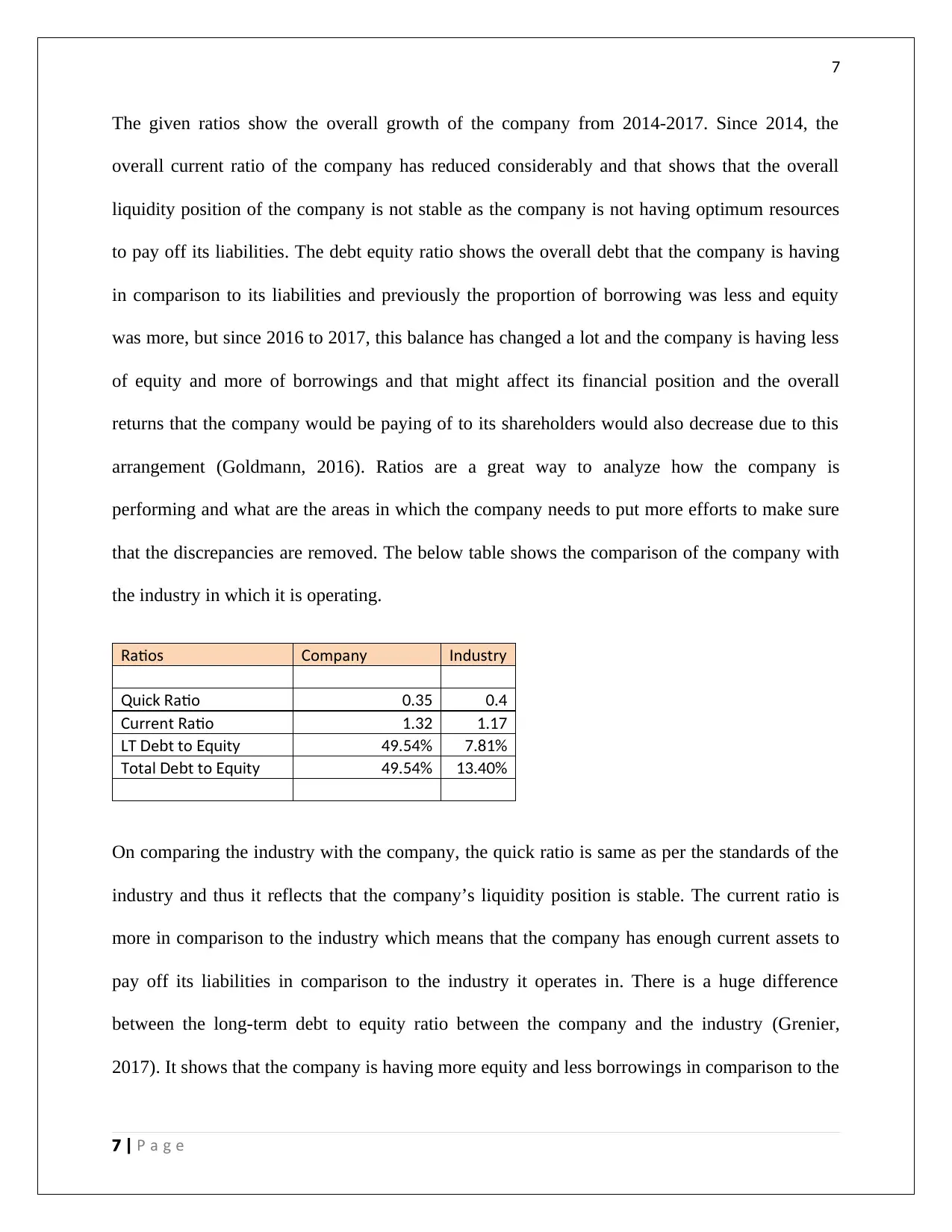

This report presents an analysis of JB Hi-Fi's financial position, based on its 2017 annual report. The assignment is divided into three sections: materiality analysis, preliminary analytical review using ratio analysis, and a review of the cash flow statement. The materiality section examines quantitative and qualitative aspects, calculating materiality levels based on revenue, assets, profit, and equity. The analytical review section includes ratio analysis of current, quick, and debt-to-equity ratios to assess the company's liquidity and financial leverage. It also compares JB Hi-Fi's ratios with industry benchmarks. The final section reviews the cash flow statement, highlighting the major sources and uses of cash. The report concludes that the company is performing well, with few areas requiring significant changes, considering industry standards. Key audit risks and relevant assertions, along with proposed audit procedures, are also outlined.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.