Audit, Assurance, and Compliance: Individual Assignment Report

VerifiedAdded on 2020/02/24

|10

|1424

|48

Report

AI Summary

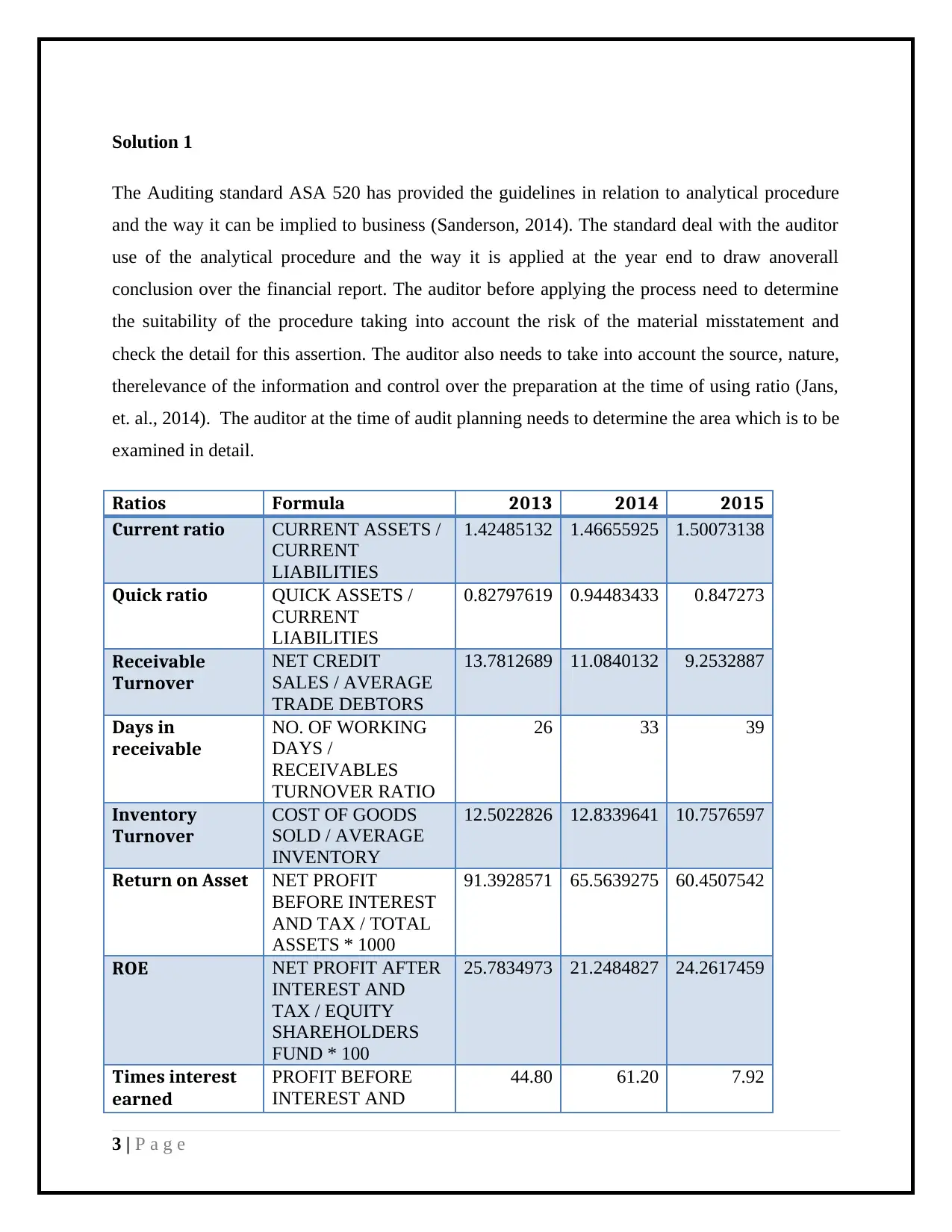

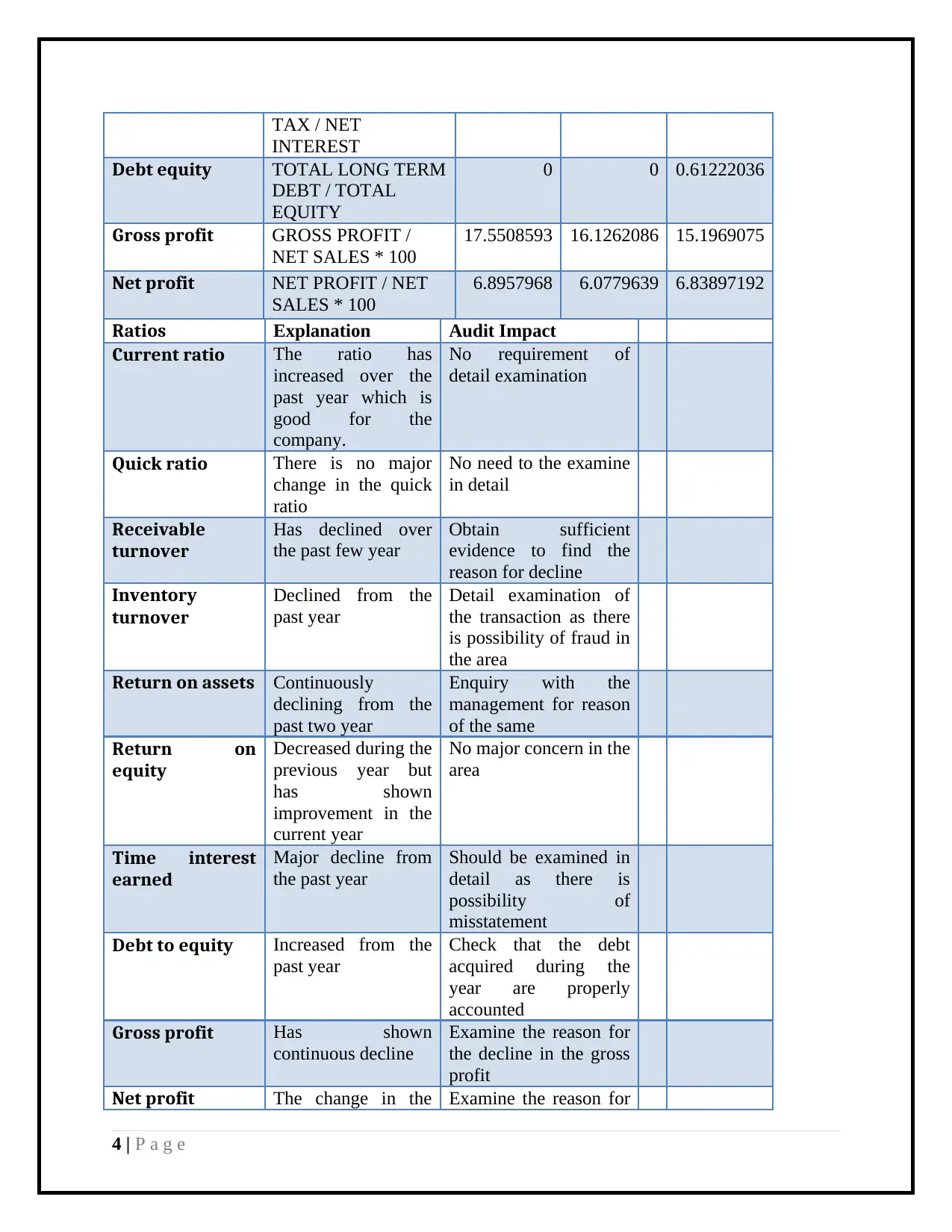

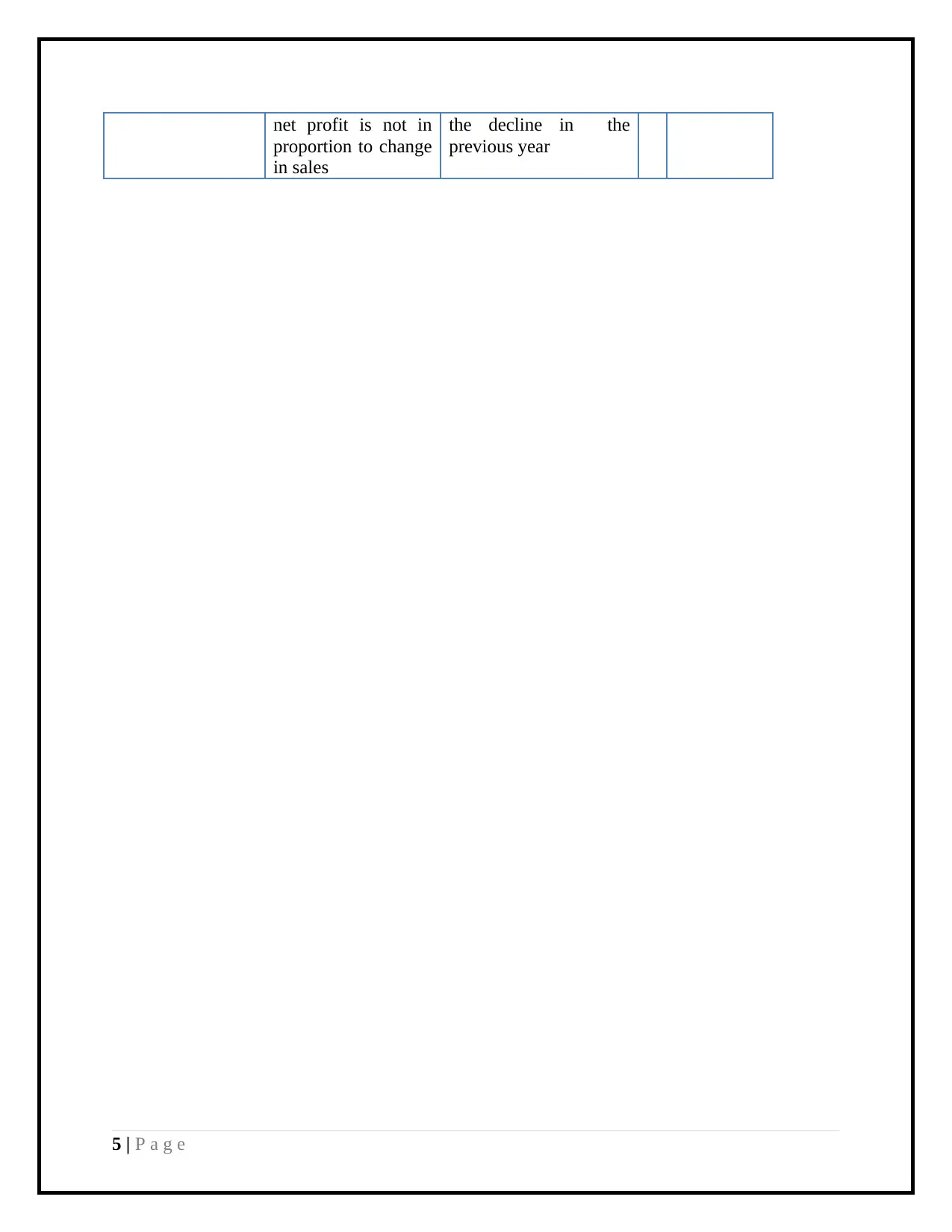

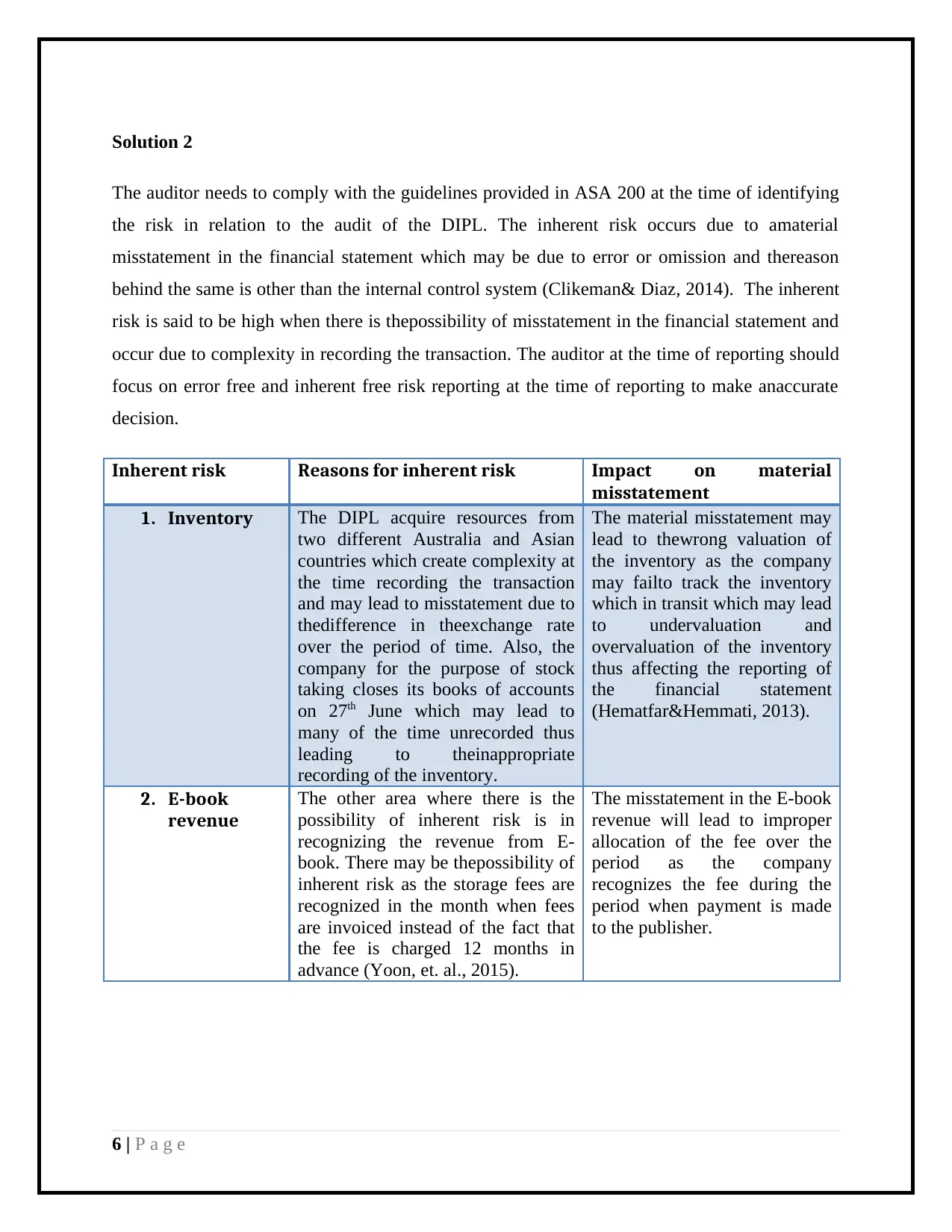

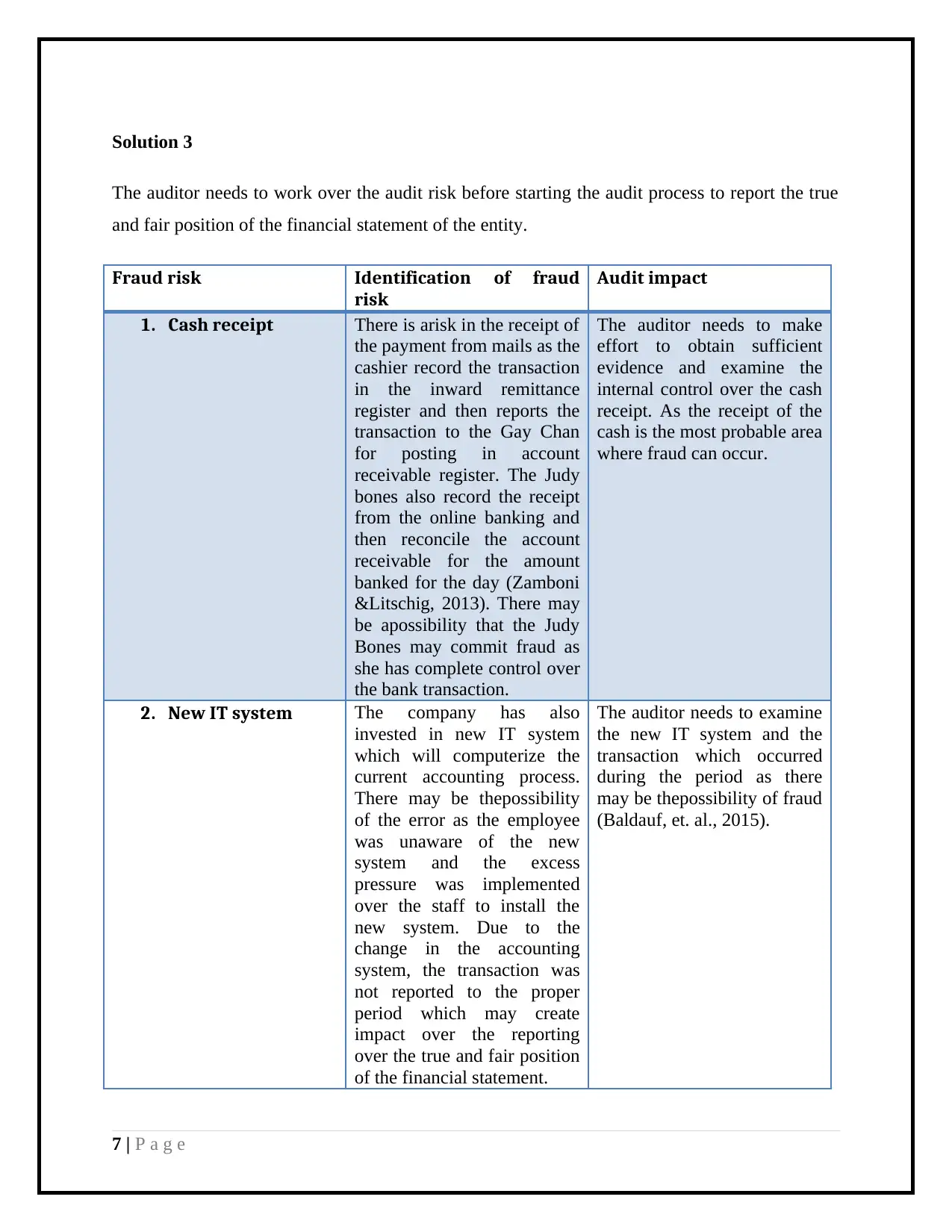

This individual assignment report focuses on audit, assurance, and compliance, providing a detailed analysis of financial statements. The report begins with an analysis of various financial ratios, including current ratio, quick ratio, and inventory turnover, evaluating their trends over a three-year period and assessing their audit implications. The second part of the report delves into inherent risks, identifying potential misstatements related to inventory valuation and e-book revenue recognition. The report highlights complexities in transaction recording and revenue allocation. The final section addresses fraud risks, specifically examining cash receipt processes and the implementation of a new IT system, along with their impact on the audit process. The report provides a thorough examination of audit procedures, risk assessment, and compliance considerations.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.