Audit 10: Evaluating Financial Reports for Audit Planning at DIPL

VerifiedAdded on 2020/03/13

|13

|2653

|73

Report

AI Summary

This report analyzes the audit of Double Ink Printers Ltd (DIPL), focusing on preliminary analytical procedures, risk assessment, and potential fraud activities. It begins by calculating and interpreting key financial ratios for 2013-2015, including liquidity, profitability, efficiency, and capital structure ratios, to evaluate DIPL's financial performance. The report then identifies and discusses inherent risks, such as financial and operating risks, and their impact on financial statements. Furthermore, it explores two potential fraud activities related to CEO performance bonuses and loan acquisition, identifying the causes behind these risks. The analysis highlights the implications of these findings on audit planning and the need for auditors to focus on high-risk areas, such as debt, profitability, and efficiency.

Audit 1

Audit, Assurance, and Compliance

Audit, Assurance, and Compliance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit 2

Table of Contents

Introduction:...............................................................................................................................3

Case Analysis:............................................................................................................................4

Question 1:..............................................................................................................................4

Question 2:..............................................................................................................................6

Question 3:..............................................................................................................................6

A) Two possible fraud activities:........................................................................................6

B) Cause of fraud identified:..............................................................................................7

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Introduction:...............................................................................................................................3

Case Analysis:............................................................................................................................4

Question 1:..............................................................................................................................4

Question 2:..............................................................................................................................6

Question 3:..............................................................................................................................6

A) Two possible fraud activities:........................................................................................6

B) Cause of fraud identified:..............................................................................................7

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

Audit 3

Introduction:

The main purpose of this report is to develop the understanding and knowledge about the

analytical procedure for evaluating the impact o0f financial reports on the audit planning

decision. It discusses the important ratio in relation to DIPL that are important for the

building the audit planning decision. Along with this, report discusses about the two inherent

risks that may arise from the nature of DIPL business operations and impact of risks on the

financial reports or statements. At the same time, it also discusses about the two different

fraud risks that may occurred from the business operations relating to misstatements from the

financial reporting activities. Furthermore, it also represents the cause of the fraud in the

financial reporting transactions in relation to business operations of DIPL. It also describes

the impact of the fraud activities on the audit planning and audit work.

Introduction:

The main purpose of this report is to develop the understanding and knowledge about the

analytical procedure for evaluating the impact o0f financial reports on the audit planning

decision. It discusses the important ratio in relation to DIPL that are important for the

building the audit planning decision. Along with this, report discusses about the two inherent

risks that may arise from the nature of DIPL business operations and impact of risks on the

financial reports or statements. At the same time, it also discusses about the two different

fraud risks that may occurred from the business operations relating to misstatements from the

financial reporting activities. Furthermore, it also represents the cause of the fraud in the

financial reporting transactions in relation to business operations of DIPL. It also describes

the impact of the fraud activities on the audit planning and audit work.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit 4

Case Analysis:

Question 1:

Preliminary Analytical procedures:

This method enhances the efficiency of auditor in relation to audit of company financial

statements. Preliminary Analytical procedures involve the evaluations of the company

financial statements or information through measuring relationship between both financial

and non-financial data. This procedure supports in planning, collecting the evidence and final

review of the audit work. Along with this, analytical procedure helps the auditors in

determining the timing, nature, and scope of their auditing procedure (Humpherys et al,

2011). The main purpose of this procedure is to develop the understanding of the auditors

about the client and measuring audit risks through using the unexpected or expected data or

balances.

Along with this, procedure involves the different tools such as account balance comparison,

calculation of significant ratios, regression analysis, and ratio calculation through using the

financial and non-financial information (Brazel et al, 2013). These different tools support the

auditors in audit planning. The main purpose of this procedure is to find out the potential

account errors and understand business and its transactions.

The analysis of ratio in analytical procedures for the DIPL financial report information for the

year 2013, 2014, and 2015 is as below:

Double Ink Printers Ltd

Name of ratio 2013 2014 2015

liquidity ratio:

Case Analysis:

Question 1:

Preliminary Analytical procedures:

This method enhances the efficiency of auditor in relation to audit of company financial

statements. Preliminary Analytical procedures involve the evaluations of the company

financial statements or information through measuring relationship between both financial

and non-financial data. This procedure supports in planning, collecting the evidence and final

review of the audit work. Along with this, analytical procedure helps the auditors in

determining the timing, nature, and scope of their auditing procedure (Humpherys et al,

2011). The main purpose of this procedure is to develop the understanding of the auditors

about the client and measuring audit risks through using the unexpected or expected data or

balances.

Along with this, procedure involves the different tools such as account balance comparison,

calculation of significant ratios, regression analysis, and ratio calculation through using the

financial and non-financial information (Brazel et al, 2013). These different tools support the

auditors in audit planning. The main purpose of this procedure is to find out the potential

account errors and understand business and its transactions.

The analysis of ratio in analytical procedures for the DIPL financial report information for the

year 2013, 2014, and 2015 is as below:

Double Ink Printers Ltd

Name of ratio 2013 2014 2015

liquidity ratio:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit 5

current ratio = Current assets / current liabilities 1.425 1.467 1.501

Current Assets 53,85,938 75,09,150 96,00,929

Current Liabilities 37,80,000 5120250 6397500

Quick ratio = current assets - inventories/ current

liabilities

0.828 0.945 0.847

Current Assets 53,85,938 75,09,150 96,00,929

Current Liabilities 37,80,000 5120250 6397500

Inventory 22,56,188 26,71,362 41,80,500

Profitability ratio:

Gross profit margin = gross profit/ revenue * 100 17.551 16.126 15.197

Gross profit 60,04,500 60,79,500 66,04,500

revenue 3,42,12,00

0

3,76,99,50

0

4,34,59,50

0

Net profit margin= net profit / revenue * 100 6.896 6.078 6.839

Net profit 23,59,190 22,91,362 29,72,183

revenue 3,42,12,00

0

3,76,99,50

0

4,34,59,50

0

Operating profit margin ratio = Operating profit /

revenue * 100

9.851 8.683 7.039

Operating profit 33,70,271 32,73,374 30,59,299

revenue 3,42,12,00

0

3,76,99,50

0

4,34,59,50

0

Efficiency Ratio:

current ratio = Current assets / current liabilities 1.425 1.467 1.501

Current Assets 53,85,938 75,09,150 96,00,929

Current Liabilities 37,80,000 5120250 6397500

Quick ratio = current assets - inventories/ current

liabilities

0.828 0.945 0.847

Current Assets 53,85,938 75,09,150 96,00,929

Current Liabilities 37,80,000 5120250 6397500

Inventory 22,56,188 26,71,362 41,80,500

Profitability ratio:

Gross profit margin = gross profit/ revenue * 100 17.551 16.126 15.197

Gross profit 60,04,500 60,79,500 66,04,500

revenue 3,42,12,00

0

3,76,99,50

0

4,34,59,50

0

Net profit margin= net profit / revenue * 100 6.896 6.078 6.839

Net profit 23,59,190 22,91,362 29,72,183

revenue 3,42,12,00

0

3,76,99,50

0

4,34,59,50

0

Operating profit margin ratio = Operating profit /

revenue * 100

9.851 8.683 7.039

Operating profit 33,70,271 32,73,374 30,59,299

revenue 3,42,12,00

0

3,76,99,50

0

4,34,59,50

0

Efficiency Ratio:

Audit 6

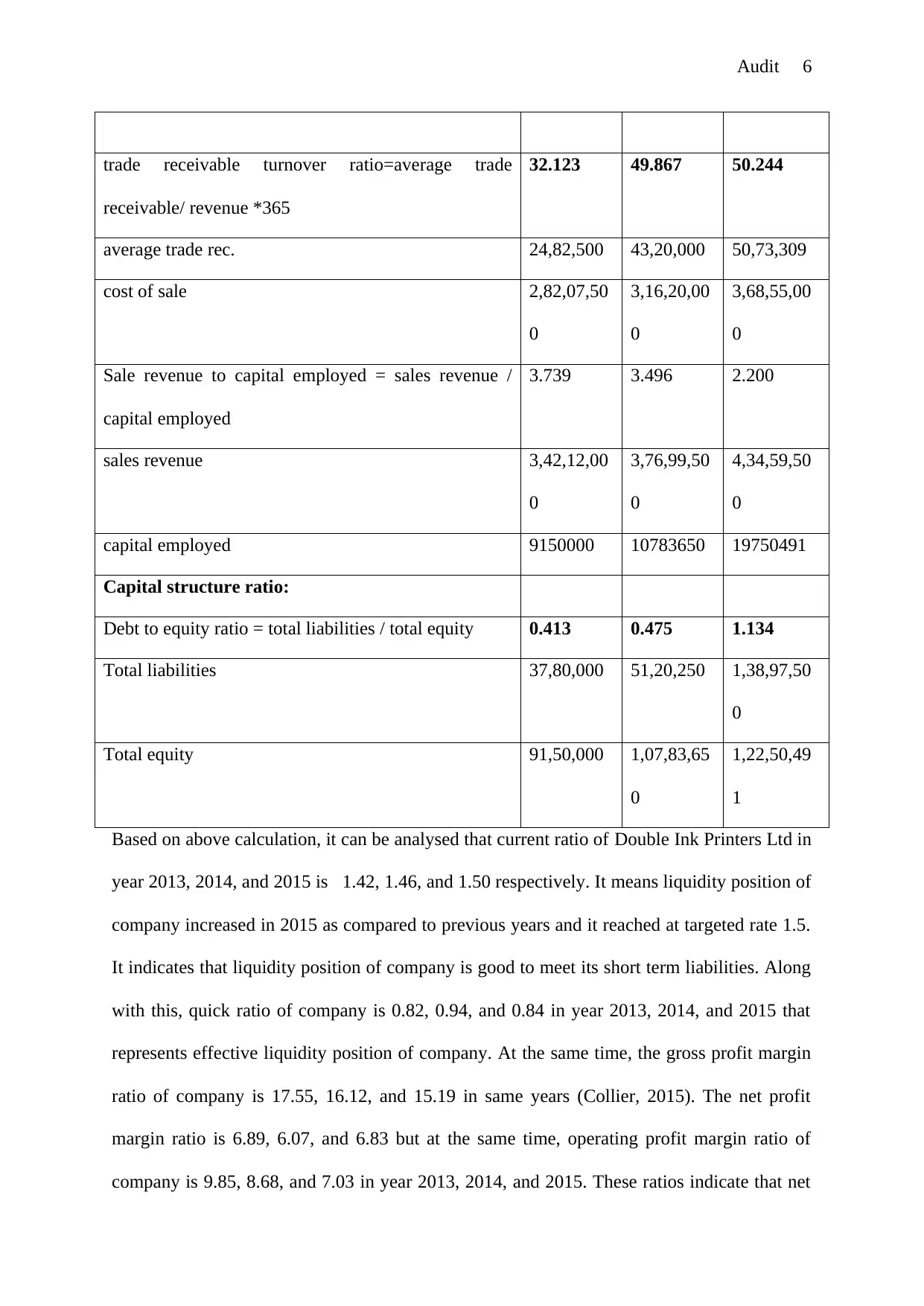

trade receivable turnover ratio=average trade

receivable/ revenue *365

32.123 49.867 50.244

average trade rec. 24,82,500 43,20,000 50,73,309

cost of sale 2,82,07,50

0

3,16,20,00

0

3,68,55,00

0

Sale revenue to capital employed = sales revenue /

capital employed

3.739 3.496 2.200

sales revenue 3,42,12,00

0

3,76,99,50

0

4,34,59,50

0

capital employed 9150000 10783650 19750491

Capital structure ratio:

Debt to equity ratio = total liabilities / total equity 0.413 0.475 1.134

Total liabilities 37,80,000 51,20,250 1,38,97,50

0

Total equity 91,50,000 1,07,83,65

0

1,22,50,49

1

Based on above calculation, it can be analysed that current ratio of Double Ink Printers Ltd in

year 2013, 2014, and 2015 is 1.42, 1.46, and 1.50 respectively. It means liquidity position of

company increased in 2015 as compared to previous years and it reached at targeted rate 1.5.

It indicates that liquidity position of company is good to meet its short term liabilities. Along

with this, quick ratio of company is 0.82, 0.94, and 0.84 in year 2013, 2014, and 2015 that

represents effective liquidity position of company. At the same time, the gross profit margin

ratio of company is 17.55, 16.12, and 15.19 in same years (Collier, 2015). The net profit

margin ratio is 6.89, 6.07, and 6.83 but at the same time, operating profit margin ratio of

company is 9.85, 8.68, and 7.03 in year 2013, 2014, and 2015. These ratios indicate that net

trade receivable turnover ratio=average trade

receivable/ revenue *365

32.123 49.867 50.244

average trade rec. 24,82,500 43,20,000 50,73,309

cost of sale 2,82,07,50

0

3,16,20,00

0

3,68,55,00

0

Sale revenue to capital employed = sales revenue /

capital employed

3.739 3.496 2.200

sales revenue 3,42,12,00

0

3,76,99,50

0

4,34,59,50

0

capital employed 9150000 10783650 19750491

Capital structure ratio:

Debt to equity ratio = total liabilities / total equity 0.413 0.475 1.134

Total liabilities 37,80,000 51,20,250 1,38,97,50

0

Total equity 91,50,000 1,07,83,65

0

1,22,50,49

1

Based on above calculation, it can be analysed that current ratio of Double Ink Printers Ltd in

year 2013, 2014, and 2015 is 1.42, 1.46, and 1.50 respectively. It means liquidity position of

company increased in 2015 as compared to previous years and it reached at targeted rate 1.5.

It indicates that liquidity position of company is good to meet its short term liabilities. Along

with this, quick ratio of company is 0.82, 0.94, and 0.84 in year 2013, 2014, and 2015 that

represents effective liquidity position of company. At the same time, the gross profit margin

ratio of company is 17.55, 16.12, and 15.19 in same years (Collier, 2015). The net profit

margin ratio is 6.89, 6.07, and 6.83 but at the same time, operating profit margin ratio of

company is 9.85, 8.68, and 7.03 in year 2013, 2014, and 2015. These ratios indicate that net

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit 7

profit of company is continuously increasing but operating efficiency of the company is

decreased.

Furthermore, trade receivable turnover ratio of company is 32.12, 49.86, and 50.24

respectively. The ratio of company is continuously increasing that means company is

inefficient in collecting the payment from the debtors that may increase the debt of company.

at the same time, the sales to capital employed ratio of company is 3.73, 3.49, and 2.20 in

year 2013,2014, and 2015. It represents that ratio of company is continuously decreasing that

means company is not effective in generating sales through utilizing its assets. The trade

receivable turnover and sales revenue to capital employed ratio of company is indicating that

efficiency of company decreased (Brigham and Houston, 2012). Apart from this, debt to

equity ratio of company in year 2013, 2014, and 2015 is 0.414, 0.47, and 1.13 respectively

but company wants to maintain ratio less than 1. It means ratio of debt of company increased

but equity of company is decreased in current year.

The fluctuation in the performance affects the planning decision for the auditing for the year.

The profitability of the company over the years is decreasing. The gross profit and operating

profit in 2014 and 2015 has been decreased while the liquidity condition is improving. This

affects the planning decision for the auditing in the organization. This kind of situation can

force for auditing in these financial aspects as well. This will lead the auditing of the

operating expenses and short term financial obligation of the DIPL (Hammersley, 2011). The

reduced financial performance affects dept financial planning that lead the auditing in the

company.

Every company wants to earn profit and want to report to the public and shareholders but the

performance of the company has been decreased and the long term liability has been

increased. Apart from this, this will cause the revision of the earlier audit plan for DIPL.

profit of company is continuously increasing but operating efficiency of the company is

decreased.

Furthermore, trade receivable turnover ratio of company is 32.12, 49.86, and 50.24

respectively. The ratio of company is continuously increasing that means company is

inefficient in collecting the payment from the debtors that may increase the debt of company.

at the same time, the sales to capital employed ratio of company is 3.73, 3.49, and 2.20 in

year 2013,2014, and 2015. It represents that ratio of company is continuously decreasing that

means company is not effective in generating sales through utilizing its assets. The trade

receivable turnover and sales revenue to capital employed ratio of company is indicating that

efficiency of company decreased (Brigham and Houston, 2012). Apart from this, debt to

equity ratio of company in year 2013, 2014, and 2015 is 0.414, 0.47, and 1.13 respectively

but company wants to maintain ratio less than 1. It means ratio of debt of company increased

but equity of company is decreased in current year.

The fluctuation in the performance affects the planning decision for the auditing for the year.

The profitability of the company over the years is decreasing. The gross profit and operating

profit in 2014 and 2015 has been decreased while the liquidity condition is improving. This

affects the planning decision for the auditing in the organization. This kind of situation can

force for auditing in these financial aspects as well. This will lead the auditing of the

operating expenses and short term financial obligation of the DIPL (Hammersley, 2011). The

reduced financial performance affects dept financial planning that lead the auditing in the

company.

Every company wants to earn profit and want to report to the public and shareholders but the

performance of the company has been decreased and the long term liability has been

increased. Apart from this, this will cause the revision of the earlier audit plan for DIPL.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit 8

Auditors uses analytical procedure to plan nature, timing and extent of the auditing. This

result will make the auditor mostly focus on the debt, profitability and efficiency (Bagshaw,

2013). It will make the researcher to be focused on the high material risk areas. In the

previous audit plan, it was expected that 10% increment in the profitability in 2015, but it did

not happen so. This can lead the revision in the previous audit plan.

Question 2:

Risk assessment supports in measuring or analyzing the business operations risks and risks

may affect the business operations or growth of company negatively. Along with this, risk

assessment also significant in planning for the audit. In the provided information about the

DIPL, there is two various inherent risks are available such as financial risk and audit risks

(Knechel and Salterio, 2016). The financial risk arises from the decrease in the liquidity

position of the company, operating risks from managing the inventory and foreign exchange

risks from the foreign transactions.

The financial risk is an risk type that has negative impact on the reliability of financial

statements and growth of DIPL. It involves the operating risk, credit risk, foreign exchange

risk, which may affect the risk of material misstatement in the DIPL financial statements. The

quick ratio of company decreased in year 2015 that means liquidity position of company is

ineffective to meet the short term liabilities (Arens et al, 2012). Along with this, operating

risk also may arise as company not have inventory to fulfill the client order because company

provides the on demand services. The company purchases inventory such as paper, ink and

binding materials from the Asian and Australia.

In this way, it is risk that to show the operating efficiency, company can record the higher

inventory into financial statements that may increase the operational efficiency of company.

Along with this, credit risk also may arise as debtor receivable turnover time of company is

Auditors uses analytical procedure to plan nature, timing and extent of the auditing. This

result will make the auditor mostly focus on the debt, profitability and efficiency (Bagshaw,

2013). It will make the researcher to be focused on the high material risk areas. In the

previous audit plan, it was expected that 10% increment in the profitability in 2015, but it did

not happen so. This can lead the revision in the previous audit plan.

Question 2:

Risk assessment supports in measuring or analyzing the business operations risks and risks

may affect the business operations or growth of company negatively. Along with this, risk

assessment also significant in planning for the audit. In the provided information about the

DIPL, there is two various inherent risks are available such as financial risk and audit risks

(Knechel and Salterio, 2016). The financial risk arises from the decrease in the liquidity

position of the company, operating risks from managing the inventory and foreign exchange

risks from the foreign transactions.

The financial risk is an risk type that has negative impact on the reliability of financial

statements and growth of DIPL. It involves the operating risk, credit risk, foreign exchange

risk, which may affect the risk of material misstatement in the DIPL financial statements. The

quick ratio of company decreased in year 2015 that means liquidity position of company is

ineffective to meet the short term liabilities (Arens et al, 2012). Along with this, operating

risk also may arise as company not have inventory to fulfill the client order because company

provides the on demand services. The company purchases inventory such as paper, ink and

binding materials from the Asian and Australia.

In this way, it is risk that to show the operating efficiency, company can record the higher

inventory into financial statements that may increase the operational efficiency of company.

Along with this, credit risk also may arise as debtor receivable turnover time of company is

Audit 9

also increasing in every year that means company is ineffective in colleting the payment from

the creditors (Griffiths, 2012). Due to credit risk also may arise that affect the business

operations and company also can decrease the creditors in its financial statement to show the

company worth higher.

Apart from this, based on the provided information, audit risk also may be raised. It is

because DIPL has appointed a new chief executive and board decided to provide the

remuneration package as company will provide bonus to CEO when the total revenue and net

profit after tax of company will increased by 10%. Therefore, CEO can meet with the internal

accounts and auditors to show the company growth and increase the company revenue by

10% with their mutual concern. In this way, accountants or CEO can make the fraud in the

company accounts to get the financial benefits (Leung et al, 2012). Along with this, it is

possibility that internal auditor of company would not be effective to detect the material

misstatement in company accounts as he is working for four big audit firm and two chartered

accountants. Due to the work pressure of auditor the audit risk may arise in DIPL.

Question 3:

A) Two possible fraud activities:

As per the given information about the DIPL business operations, two possible fraud risk

identified is that fraud of CEO to get the performance bonus as board decided to provide the

bonus when the total revenue and net income of company would increased by 10%.

Therefore, its possibility that CEO can conduct the fraud in misrepresenting the company

expenses to get bonus (Prawitt et al, 2012). The second possible fraud can be conducted by

the company management and accounts to maintain the current ratio at least 1.5 to borrow

fund of 7.5 million from BDO Finance Ltd.

also increasing in every year that means company is ineffective in colleting the payment from

the creditors (Griffiths, 2012). Due to credit risk also may arise that affect the business

operations and company also can decrease the creditors in its financial statement to show the

company worth higher.

Apart from this, based on the provided information, audit risk also may be raised. It is

because DIPL has appointed a new chief executive and board decided to provide the

remuneration package as company will provide bonus to CEO when the total revenue and net

profit after tax of company will increased by 10%. Therefore, CEO can meet with the internal

accounts and auditors to show the company growth and increase the company revenue by

10% with their mutual concern. In this way, accountants or CEO can make the fraud in the

company accounts to get the financial benefits (Leung et al, 2012). Along with this, it is

possibility that internal auditor of company would not be effective to detect the material

misstatement in company accounts as he is working for four big audit firm and two chartered

accountants. Due to the work pressure of auditor the audit risk may arise in DIPL.

Question 3:

A) Two possible fraud activities:

As per the given information about the DIPL business operations, two possible fraud risk

identified is that fraud of CEO to get the performance bonus as board decided to provide the

bonus when the total revenue and net income of company would increased by 10%.

Therefore, its possibility that CEO can conduct the fraud in misrepresenting the company

expenses to get bonus (Prawitt et al, 2012). The second possible fraud can be conducted by

the company management and accounts to maintain the current ratio at least 1.5 to borrow

fund of 7.5 million from BDO Finance Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit 10

B) Cause of fraud identified:

The newly appointed CEO of company William Jackson also can make the fraud in the

company to get the performance bonus. It is because management decided to provide the

performance bonus to CEO when the total revenue and net profit after tax of company

increased by 10%. In this way, based on the information about the business operations of

DIPL, the revenue of company increases in year 2014 increased by 3,487,500 but in year

2015 it increased by 5,760,000. This increase rate of revenue is very higher as compare to

previous year’s rates; the result may arise due to fraud of CEO to get the performance bonus.

Along with this, net profit after tax of DIPL in year 2013 was 2359190 that was decrease in

year 2014 by 67828 but profit of company increased in year 2015 with a higher rate as

680,821. Based on this, it is analyzed that CEO make the fraud in accounts through showing

the decreasing the company expenses to represent the growth in company net profit. Apart

from this, based on the provided information in the financial statements it is possibility that

company conduct fraud in relation to get the loan of 1.5 million. It is because bank decided

that if the current ratio of company would be at least 1.5 and debt to equity ratio would be

less than 1 to get the loan. In this way, the current ratio of DIPL was 1.42 and 1.46 in year

2013 and 2014 but in year 2015 it would become 1.50 that is required by the bank to provide

the loan of 1.5 million worth. The company can conduct fraud in the financial statements in

relation to company current assets through showing the higher value of company assets.

B) Cause of fraud identified:

The newly appointed CEO of company William Jackson also can make the fraud in the

company to get the performance bonus. It is because management decided to provide the

performance bonus to CEO when the total revenue and net profit after tax of company

increased by 10%. In this way, based on the information about the business operations of

DIPL, the revenue of company increases in year 2014 increased by 3,487,500 but in year

2015 it increased by 5,760,000. This increase rate of revenue is very higher as compare to

previous year’s rates; the result may arise due to fraud of CEO to get the performance bonus.

Along with this, net profit after tax of DIPL in year 2013 was 2359190 that was decrease in

year 2014 by 67828 but profit of company increased in year 2015 with a higher rate as

680,821. Based on this, it is analyzed that CEO make the fraud in accounts through showing

the decreasing the company expenses to represent the growth in company net profit. Apart

from this, based on the provided information in the financial statements it is possibility that

company conduct fraud in relation to get the loan of 1.5 million. It is because bank decided

that if the current ratio of company would be at least 1.5 and debt to equity ratio would be

less than 1 to get the loan. In this way, the current ratio of DIPL was 1.42 and 1.46 in year

2013 and 2014 but in year 2015 it would become 1.50 that is required by the bank to provide

the loan of 1.5 million worth. The company can conduct fraud in the financial statements in

relation to company current assets through showing the higher value of company assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit 11

Conclusion:

From the analysis of above report, it can be concluded that Analytical procedures involves

the different tools such as account balance comparison, calculation of ratios, regression

analysis, which can be used in audit planning for the analysis of financial statements. Along

with this, DIPL can face the financial risk and audit risks based on the provided information

that may affect the reliability and accuracy of DIPL financial statements negatively.

Furthermore, in the case of DIPL the CEO of company and management or accountant can

make the fraud to get the benefit of performance bonus and to borrow funds from the bank.

Conclusion:

From the analysis of above report, it can be concluded that Analytical procedures involves

the different tools such as account balance comparison, calculation of ratios, regression

analysis, which can be used in audit planning for the analysis of financial statements. Along

with this, DIPL can face the financial risk and audit risks based on the provided information

that may affect the reliability and accuracy of DIPL financial statements negatively.

Furthermore, in the case of DIPL the CEO of company and management or accountant can

make the fraud to get the benefit of performance bonus and to borrow funds from the bank.

Audit 12

References:

Arens, A.A., Elder, R.J. and Mark, B., (2012) Auditing and assurance services: an integrated

approach. USA: Boston: Prentice Hall.

Bagshaw, K., (2013) Audit and Assurance Essentials: For Professional Accountancy Exams.

USA: John Wiley & Sons.

Brazel, J.F., Jones, K.L. and Prawitt, D.F., (2013) Auditors' reactions to inconsistencies

between financial and nonfinancial measures: The interactive effects of fraud risk assessment

and a decision prompt. Behavioral Research in Accounting, 26(1), pp. 131-156.

Brigham, E.F. and Houston, J.F., (2012) Fundamentals of financial management. USA:

Cengage Learning.

Collier, P.M., (2015) Accounting for managers: Interpreting accounting information for

decision making. UK: John Wiley & Sons.

Griffiths, M.P., (2012) Risk-based auditing. UK: Gower Publishing, Ltd.

Hammersley, J.S., (2011) A review and model of auditor judgments in fraud-related planning

tasks. Auditing: A Journal of Practice & Theory, 30(4), pp.101-128.

Humpherys, S.L., Moffitt, K.C., Burns, M.B., Burgoon, J.K. and Felix, W.F., (2011)

Identification of fraudulent financial statements using linguistic credibility analysis. Decision

Support Systems, 50(3), pp. 585-594.

Knechel, W.R. and Salterio, S.E., (2016) Auditing: Assurance and risk. UK: Taylor &

Francis.

Leung, P., Coram, P. and Cooper, B. (2012) Modern Auditing and Assurance Services. AU:

John Wiley & Sons.

References:

Arens, A.A., Elder, R.J. and Mark, B., (2012) Auditing and assurance services: an integrated

approach. USA: Boston: Prentice Hall.

Bagshaw, K., (2013) Audit and Assurance Essentials: For Professional Accountancy Exams.

USA: John Wiley & Sons.

Brazel, J.F., Jones, K.L. and Prawitt, D.F., (2013) Auditors' reactions to inconsistencies

between financial and nonfinancial measures: The interactive effects of fraud risk assessment

and a decision prompt. Behavioral Research in Accounting, 26(1), pp. 131-156.

Brigham, E.F. and Houston, J.F., (2012) Fundamentals of financial management. USA:

Cengage Learning.

Collier, P.M., (2015) Accounting for managers: Interpreting accounting information for

decision making. UK: John Wiley & Sons.

Griffiths, M.P., (2012) Risk-based auditing. UK: Gower Publishing, Ltd.

Hammersley, J.S., (2011) A review and model of auditor judgments in fraud-related planning

tasks. Auditing: A Journal of Practice & Theory, 30(4), pp.101-128.

Humpherys, S.L., Moffitt, K.C., Burns, M.B., Burgoon, J.K. and Felix, W.F., (2011)

Identification of fraudulent financial statements using linguistic credibility analysis. Decision

Support Systems, 50(3), pp. 585-594.

Knechel, W.R. and Salterio, S.E., (2016) Auditing: Assurance and risk. UK: Taylor &

Francis.

Leung, P., Coram, P. and Cooper, B. (2012) Modern Auditing and Assurance Services. AU:

John Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.