University Audit, Assurance, and Compliance Report Analysis

VerifiedAdded on 2019/11/19

|8

|1053

|450

Report

AI Summary

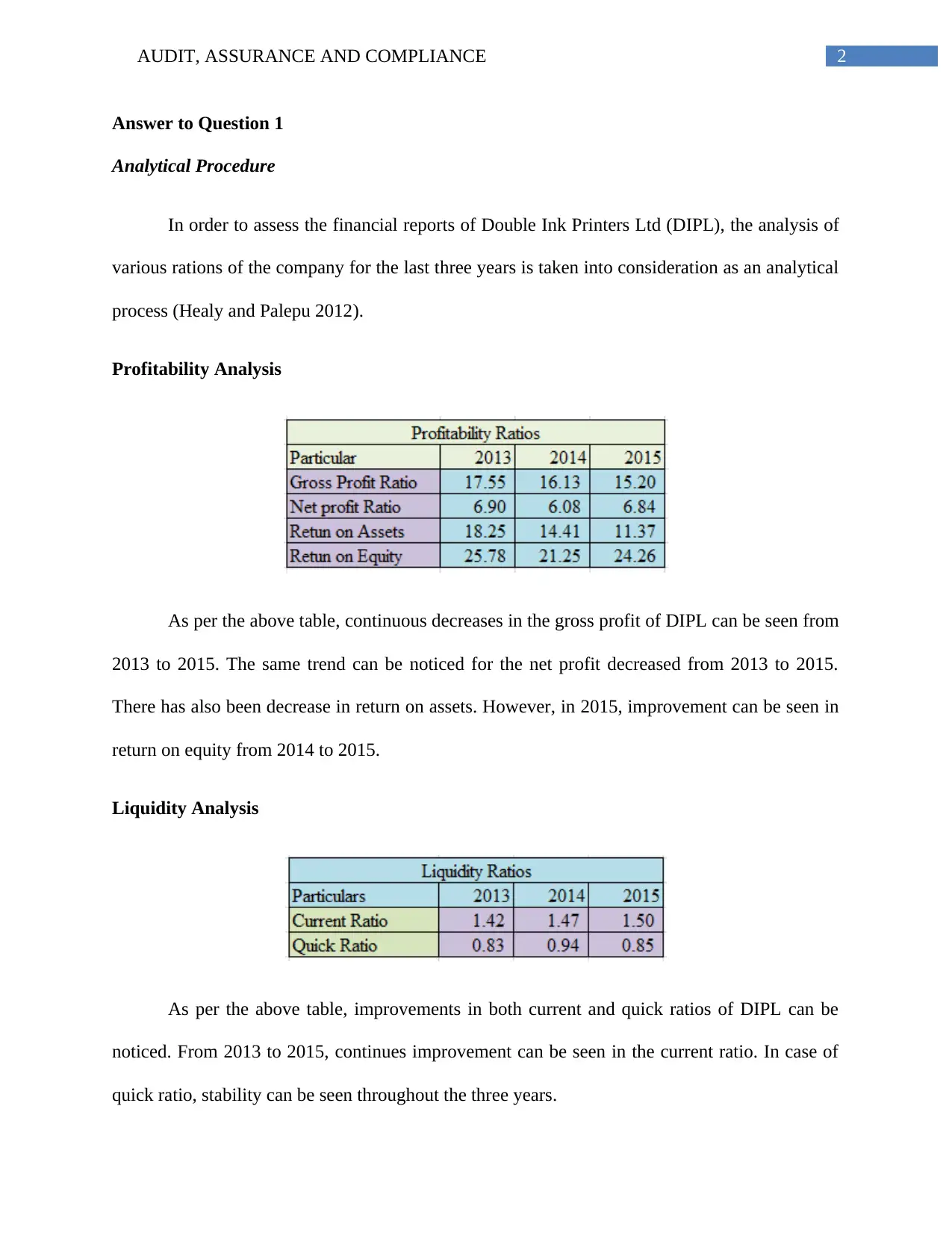

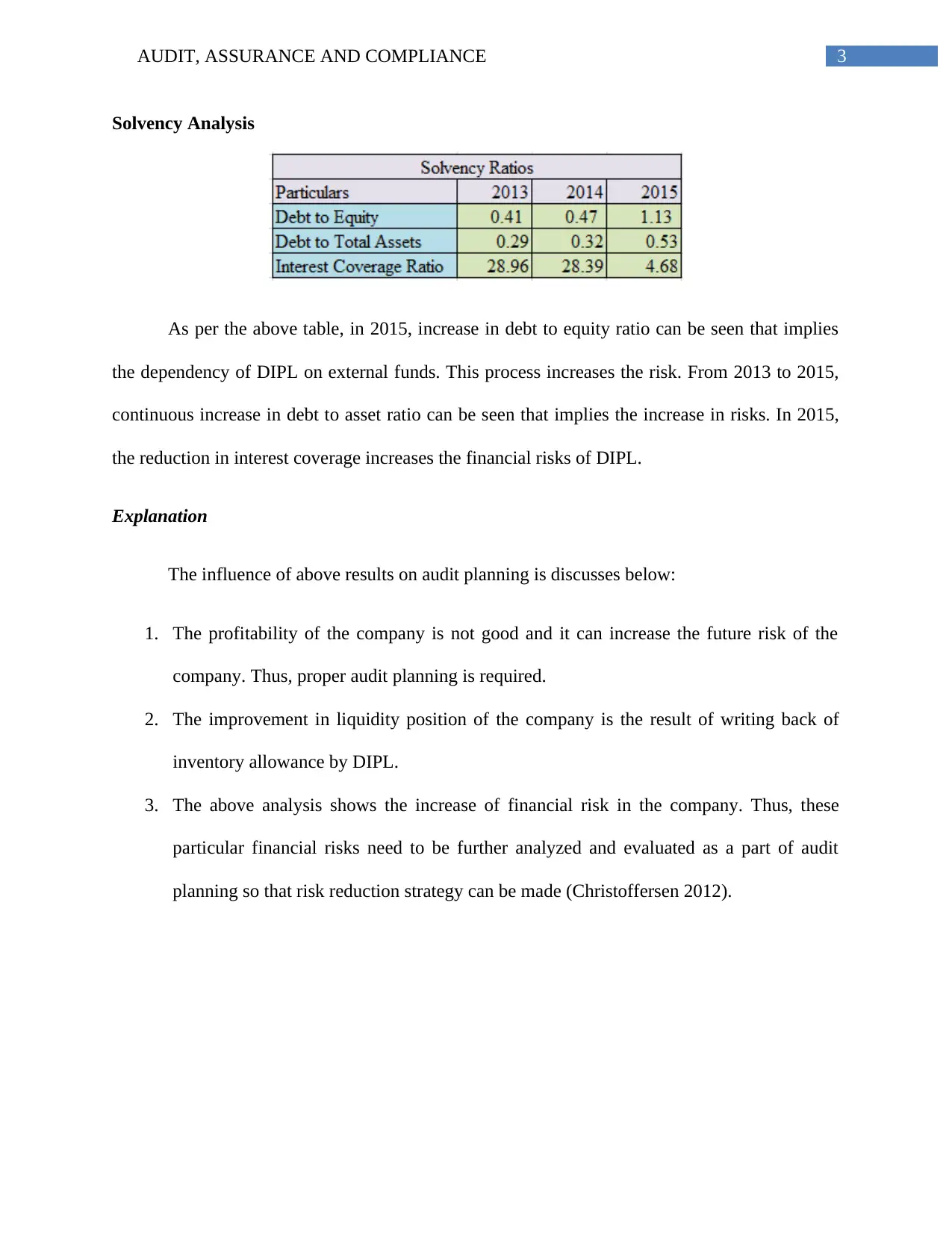

This report provides a detailed analysis of the financial performance and risk factors of Double Ink Printers Ltd (DIPL). It begins with an analytical procedure using financial ratios to assess profitability, liquidity, and solvency over a three-year period. The analysis reveals declining profitability, improved liquidity, and increasing financial risks. The report then identifies inherent risks, including financial risk due to increased debt and information technology risks. It also examines fraud risk factors, such as debt agreements and the control environment, highlighting potential manipulations. The report suggests corroboration between financial figures to detect manipulation and emphasizes the importance of examining inventory and aligning purchases. The report concludes by referencing several academic sources to support its findings.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.