Audit, Assurance, and Compliance Report: DIPL Financial Risks

VerifiedAdded on 2020/03/04

|10

|2418

|34

Report

AI Summary

This report provides a comprehensive analysis of audit, assurance, and compliance practices, focusing on a case study of Double Ink Printers Limited (DIPL). It examines the benefits of analytical procedures in audit planning, including benchmarking and ratio analysis, and their impact on evaluating financial performance. The report identifies and assesses inherent risks within DIPL, such as management failures, employee workload, and CEO succession issues. It further explores fraudulent risks, financial reporting procedures, and the impact of financial ratios on loan agreements and investor confidence. The report also suggests methods for mitigating these risks through continuous monitoring of IT systems and thorough assessment of financial statements. The report uses the case study to highlight the importance of effective financial management and the need for robust audit and compliance processes to ensure financial stability and transparency.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................4

Answer to Question 3:................................................................................................................5

Answer to Part A:...................................................................................................................5

Answer to Part B:...................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................4

Answer to Question 3:................................................................................................................5

Answer to Part A:...................................................................................................................5

Answer to Part B:...................................................................................................................8

References:.................................................................................................................................9

2AUDIT, ASSURANCE AND COMPLIANCE

Answer to Question 1:

While developing the plan of audit relating to Double Ink Printers Limited (DIPL),

the analytical procedure related to financial information offers great benefits. On the other

hand, the plan of audit offers the needed guidelines and directions to the auditors during the

operations of audit. In other words, the plan of audit helps the auditors to maintain the audit

cost in a certain limit to curb confusion with the audit clients (Carson, Redmayne and Liao

2014). The procedure of evaluating the financial performance of the organisation could be

formed with the help of various mechanisms.

It has become possible for the financial analysts and accountants to utilise the

financial information in order to make various business decisions through the analytical

method. The common size analytical method helps in the process of evaluating the financial

declaration of the organisation from the prevalent referential points. The fundamental merit is

that it lends support to compare the financial statement from different financial timelines.

The financial analysts and accountants could make use of various lines of items from

the financial statements and accordingly, the base of preparation could be made for the firms.

For example, the process of registration of various accounting and financial items in the

financial statements like owner’s equity, overall liabilities and assets could be taken into

account along with the dissection of digression from the normal position (Carson et al. 2014).

One of the primary analytical processes related to financial information is benchmarking,

which could be used to evaluate the plan of audit. In addition, ratio analysis is a fundamental

analytical procedure associated with the financial information of a firm, as it could be used to

compare the performance of the firm with its competitors to develop the audit plan (Cohen

and Simnett 2014).

Answer to Question 1:

While developing the plan of audit relating to Double Ink Printers Limited (DIPL),

the analytical procedure related to financial information offers great benefits. On the other

hand, the plan of audit offers the needed guidelines and directions to the auditors during the

operations of audit. In other words, the plan of audit helps the auditors to maintain the audit

cost in a certain limit to curb confusion with the audit clients (Carson, Redmayne and Liao

2014). The procedure of evaluating the financial performance of the organisation could be

formed with the help of various mechanisms.

It has become possible for the financial analysts and accountants to utilise the

financial information in order to make various business decisions through the analytical

method. The common size analytical method helps in the process of evaluating the financial

declaration of the organisation from the prevalent referential points. The fundamental merit is

that it lends support to compare the financial statement from different financial timelines.

The financial analysts and accountants could make use of various lines of items from

the financial statements and accordingly, the base of preparation could be made for the firms.

For example, the process of registration of various accounting and financial items in the

financial statements like owner’s equity, overall liabilities and assets could be taken into

account along with the dissection of digression from the normal position (Carson et al. 2014).

One of the primary analytical processes related to financial information is benchmarking,

which could be used to evaluate the plan of audit. In addition, ratio analysis is a fundamental

analytical procedure associated with the financial information of a firm, as it could be used to

compare the performance of the firm with its competitors to develop the audit plan (Cohen

and Simnett 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

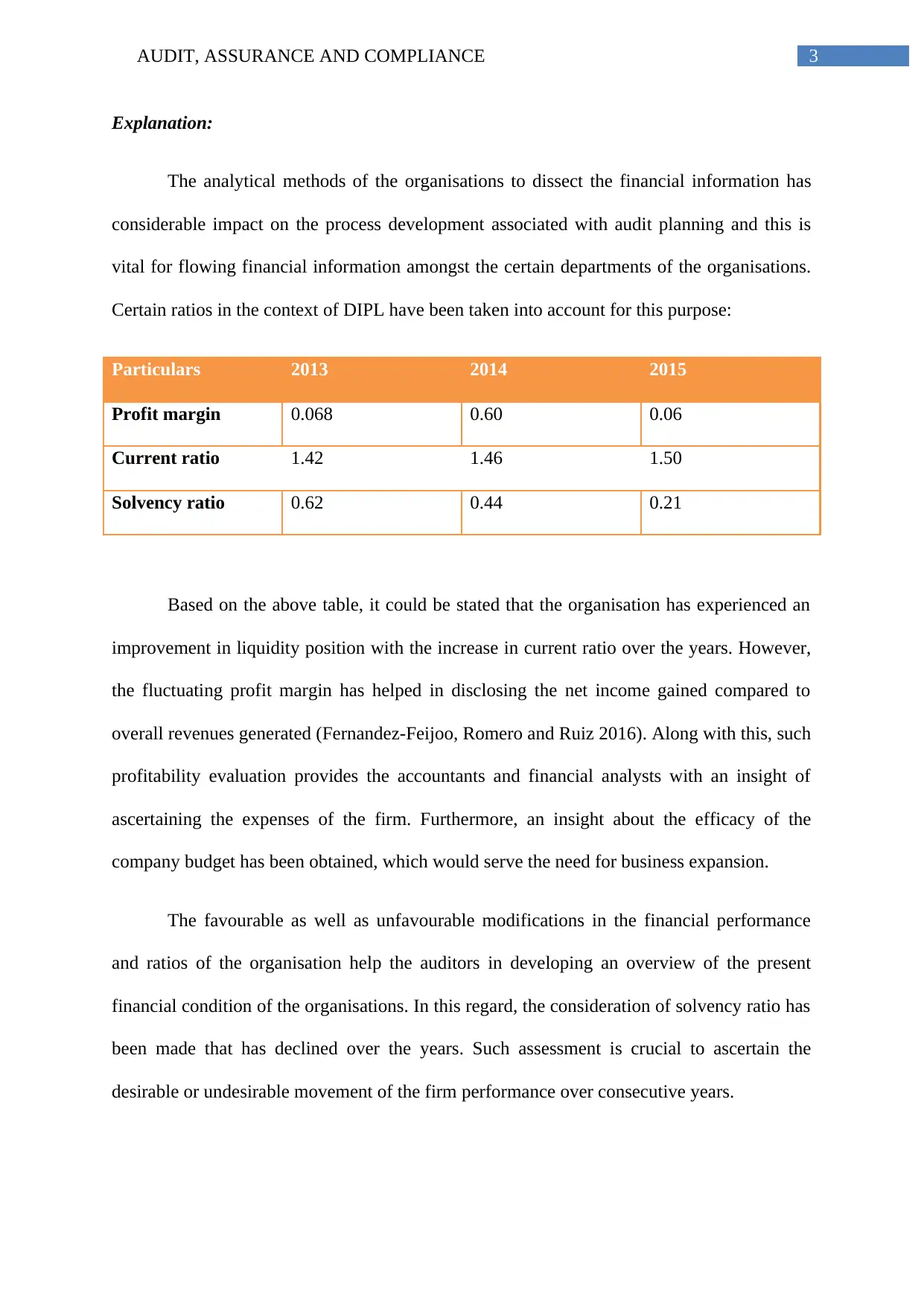

Explanation:

The analytical methods of the organisations to dissect the financial information has

considerable impact on the process development associated with audit planning and this is

vital for flowing financial information amongst the certain departments of the organisations.

Certain ratios in the context of DIPL have been taken into account for this purpose:

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

Solvency ratio 0.62 0.44 0.21

Based on the above table, it could be stated that the organisation has experienced an

improvement in liquidity position with the increase in current ratio over the years. However,

the fluctuating profit margin has helped in disclosing the net income gained compared to

overall revenues generated (Fernandez-Feijoo, Romero and Ruiz 2016). Along with this, such

profitability evaluation provides the accountants and financial analysts with an insight of

ascertaining the expenses of the firm. Furthermore, an insight about the efficacy of the

company budget has been obtained, which would serve the need for business expansion.

The favourable as well as unfavourable modifications in the financial performance

and ratios of the organisation help the auditors in developing an overview of the present

financial condition of the organisations. In this regard, the consideration of solvency ratio has

been made that has declined over the years. Such assessment is crucial to ascertain the

desirable or undesirable movement of the firm performance over consecutive years.

Explanation:

The analytical methods of the organisations to dissect the financial information has

considerable impact on the process development associated with audit planning and this is

vital for flowing financial information amongst the certain departments of the organisations.

Certain ratios in the context of DIPL have been taken into account for this purpose:

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

Solvency ratio 0.62 0.44 0.21

Based on the above table, it could be stated that the organisation has experienced an

improvement in liquidity position with the increase in current ratio over the years. However,

the fluctuating profit margin has helped in disclosing the net income gained compared to

overall revenues generated (Fernandez-Feijoo, Romero and Ruiz 2016). Along with this, such

profitability evaluation provides the accountants and financial analysts with an insight of

ascertaining the expenses of the firm. Furthermore, an insight about the efficacy of the

company budget has been obtained, which would serve the need for business expansion.

The favourable as well as unfavourable modifications in the financial performance

and ratios of the organisation help the auditors in developing an overview of the present

financial condition of the organisations. In this regard, the consideration of solvency ratio has

been made that has declined over the years. Such assessment is crucial to ascertain the

desirable or undesirable movement of the firm performance over consecutive years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

In other words, it could be stated that the evaluation and comparison of ratios and

financial performance help the accountants and financial analysts to determine the relative

financial condition of the organisation over the years. It helps to determine whether the

current financial condition of the firm is feasible or not. If the condition is not feasible, the

management needs to implement corrective measures to improve its financial performance.

Hence, the analytical process associated with financial information has immense value (Gu,

Simunic and Stein 2017).

Answer to Question 2:

Based on the provided case, the management has failed to record certain business

transactions. Such method has direct association with the inconsistencies associated with the

planning of various sales and marketing activities of the organisation (Hardy 2014). The

financial evaluation of DIPL implies that the profit level is inadequate when compared with

the overall revenues generated. The fundamental cause is the inefficiency and ineffectiveness

of the management in handling its business operations. In addition, the organisation has not

been able in measuring the influence of various macro and micro-economic factors on the

business functioning of DIPL. Thus, these factors have lead to lead inherent risk for the

organisation (Jones 2016).

In addition, the employees of DIPL have grown rapidly resulting in increased inherent

risk. The lack of experience and professionalism of the staffs of the organisation has

increased the level of inherent risk, as they could conduct serious mistakes. According to the

provided case study, the problems could be identified in the CEO succession procedure of the

organisation. Due to this, such procedure has lead to increase in inherent risk of the

organisation. However, this procedure has not been effective in DIPL.

In other words, it could be stated that the evaluation and comparison of ratios and

financial performance help the accountants and financial analysts to determine the relative

financial condition of the organisation over the years. It helps to determine whether the

current financial condition of the firm is feasible or not. If the condition is not feasible, the

management needs to implement corrective measures to improve its financial performance.

Hence, the analytical process associated with financial information has immense value (Gu,

Simunic and Stein 2017).

Answer to Question 2:

Based on the provided case, the management has failed to record certain business

transactions. Such method has direct association with the inconsistencies associated with the

planning of various sales and marketing activities of the organisation (Hardy 2014). The

financial evaluation of DIPL implies that the profit level is inadequate when compared with

the overall revenues generated. The fundamental cause is the inefficiency and ineffectiveness

of the management in handling its business operations. In addition, the organisation has not

been able in measuring the influence of various macro and micro-economic factors on the

business functioning of DIPL. Thus, these factors have lead to lead inherent risk for the

organisation (Jones 2016).

In addition, the employees of DIPL have grown rapidly resulting in increased inherent

risk. The lack of experience and professionalism of the staffs of the organisation has

increased the level of inherent risk, as they could conduct serious mistakes. According to the

provided case study, the problems could be identified in the CEO succession procedure of the

organisation. Due to this, such procedure has lead to increase in inherent risk of the

organisation. However, this procedure has not been effective in DIPL.

5AUDIT, ASSURANCE AND COMPLIANCE

Along with this, it could be seen that DIPL does not have adequate employees in

handling its business operations, which has again lead to increased inherent risk in the entire

business operations of the organisation. Therefore, from the above assessment, it has been

found that these are the fundamental reasons of increase in inherent risks in the business

functioning of DIPL (Junior, Best and Cotter 2014).

Explanation:

As observed from the case study, the amount of work pressure on the employees of

DIPL is extremely high. The rising workload leads to inaccurate bookkeeping of the firm and

this issue further leads to various cash flow problems, ineffective solvency and liquidity

positions along with unsuitable operating results for the organisation. Along with this, the

error risk could be represented in the financial reports because of inappropriate interpretation.

In this regard, the management of the organisation has a significant role to play. However,

there is lack of integrity and accountability in the management of DIPL and because of this

reason; they are facing the concern of reputation loss in the business community. The higher

structure of incentive associated with management develops extra pressure on the

management due to which there has been material misstatement in the financial reports

(Kend, Houghton and Jubb 2014).

Answer to Question 3:

Answer to Part A:

In the present day business organisations, fraudulent risk is considered as the primary

risk in the context of the same. Because of the occurrence of such risk, the business firm

often face huge losses in its business assets (Rahim and Idowu 2015). In most of the

situations, the basic dissatisfaction could be seen among the workforce and such

Along with this, it could be seen that DIPL does not have adequate employees in

handling its business operations, which has again lead to increased inherent risk in the entire

business operations of the organisation. Therefore, from the above assessment, it has been

found that these are the fundamental reasons of increase in inherent risks in the business

functioning of DIPL (Junior, Best and Cotter 2014).

Explanation:

As observed from the case study, the amount of work pressure on the employees of

DIPL is extremely high. The rising workload leads to inaccurate bookkeeping of the firm and

this issue further leads to various cash flow problems, ineffective solvency and liquidity

positions along with unsuitable operating results for the organisation. Along with this, the

error risk could be represented in the financial reports because of inappropriate interpretation.

In this regard, the management of the organisation has a significant role to play. However,

there is lack of integrity and accountability in the management of DIPL and because of this

reason; they are facing the concern of reputation loss in the business community. The higher

structure of incentive associated with management develops extra pressure on the

management due to which there has been material misstatement in the financial reports

(Kend, Houghton and Jubb 2014).

Answer to Question 3:

Answer to Part A:

In the present day business organisations, fraudulent risk is considered as the primary

risk in the context of the same. Because of the occurrence of such risk, the business firm

often face huge losses in its business assets (Rahim and Idowu 2015). In most of the

situations, the basic dissatisfaction could be seen among the workforce and such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

dissatisfaction often force them to involve in different kinds of frauds in firms. Another cause

of fraud is to meet the needs of the investors associated with an organisation. This is because

it often promises to accomplish a specific financial position; thereby, leading to higher level

of fraud (Shah and Nair 2013).

Types of risk Identification

Fraudulent risk In the context of the business functioning of

DIPL, the major risk that could happen from

the business operations is the engagement of

the staffs in different types of fraud activities.

This mainly arises with the fall in satisfaction

level of the staffs. According to the case

study of DIPL, it could be stated that the

board of the organisation has exerted

excessive pressure in adopting a new

accounting system. The adoption of such

system creates a huge pressure on the

workforce of the organisation and this

pressure has lead to fraud. Hence, it is

evident that for dealing with such pressure of

reconciliation, the staffs might adopt

unscrupulous behaviour leading to wrong

handling of the overall process, which further

results in material misstatement (Singh et al.

2014).

dissatisfaction often force them to involve in different kinds of frauds in firms. Another cause

of fraud is to meet the needs of the investors associated with an organisation. This is because

it often promises to accomplish a specific financial position; thereby, leading to higher level

of fraud (Shah and Nair 2013).

Types of risk Identification

Fraudulent risk In the context of the business functioning of

DIPL, the major risk that could happen from

the business operations is the engagement of

the staffs in different types of fraud activities.

This mainly arises with the fall in satisfaction

level of the staffs. According to the case

study of DIPL, it could be stated that the

board of the organisation has exerted

excessive pressure in adopting a new

accounting system. The adoption of such

system creates a huge pressure on the

workforce of the organisation and this

pressure has lead to fraud. Hence, it is

evident that for dealing with such pressure of

reconciliation, the staffs might adopt

unscrupulous behaviour leading to wrong

handling of the overall process, which further

results in material misstatement (Singh et al.

2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

Based on the case study, it could be seen that

the process of ineffective handling in

implementing the new information

technology leads to inaccurate treatment of

accounting transactions at the year end. Such

procedure might lead to loss of financial

information and material misstatements.

Procedure of financial reporting One of the primary audit risks is related to

the process of financial reporting. The

additional risk of incorrect financial

announcements could be observed, if extra

expectations could be seen from various

stakeholders for the financial announcements.

This holds good in case of management

announcements for accomplishing a specific

target of the goals for acquisition of debt.

Depending on the financial statements of

DIPL, it could be viewed that there is

increase in revenue from 2013 to 2015.

Along with this, the gross income and net

income of the organisation have increased in

tandem. The information collected from the

case study states that DIPL has obtained a

loan amount of 7.5 million from BDO

Finance in 2015.

Based on the case study, it could be seen that

the process of ineffective handling in

implementing the new information

technology leads to inaccurate treatment of

accounting transactions at the year end. Such

procedure might lead to loss of financial

information and material misstatements.

Procedure of financial reporting One of the primary audit risks is related to

the process of financial reporting. The

additional risk of incorrect financial

announcements could be observed, if extra

expectations could be seen from various

stakeholders for the financial announcements.

This holds good in case of management

announcements for accomplishing a specific

target of the goals for acquisition of debt.

Depending on the financial statements of

DIPL, it could be viewed that there is

increase in revenue from 2013 to 2015.

Along with this, the gross income and net

income of the organisation have increased in

tandem. The information collected from the

case study states that DIPL has obtained a

loan amount of 7.5 million from BDO

Finance in 2015.

8AUDIT, ASSURANCE AND COMPLIANCE

The case study further reveals that the DIPL

needs to maintain a current ratio of 1.5 and

debt-to-equity ratio of below 1. The need of

this specific arrangement might be to exert

pressure on the firm to repay the loan

according to the agreed timeline. These

requirements could lead to fraudulent

activities, as DIPL could manipulate its

financial statements to win the trust and

confidence of its investors. In case, it is

unable in maintaining the desired benchmark,

BDO Finance might not grant any further

loan to the organisation (Stewart, Kent and

Routledge 2015).

Answer to Part B:

According to the provided case, it has been assessed that the procedure of valuation

associated with the raw materials of the organisation depending on average cost is not

appropriate, since the current cost of paper exceeds the average cost. The primary risk in the

identification of fraudulent activities of its staffs to implement new system of information

technology could be detected through continual monitoring of the same in different job

phrases. Alongside this risk, the risk pertaining to the procedure of financial reporting could

be identified through assessment of the various financial statements and reports of the

organisations and the responsibility lies on the financial analysts and accountants with the

help of various analytical and control procedures. This process of reviewing as well as

The case study further reveals that the DIPL

needs to maintain a current ratio of 1.5 and

debt-to-equity ratio of below 1. The need of

this specific arrangement might be to exert

pressure on the firm to repay the loan

according to the agreed timeline. These

requirements could lead to fraudulent

activities, as DIPL could manipulate its

financial statements to win the trust and

confidence of its investors. In case, it is

unable in maintaining the desired benchmark,

BDO Finance might not grant any further

loan to the organisation (Stewart, Kent and

Routledge 2015).

Answer to Part B:

According to the provided case, it has been assessed that the procedure of valuation

associated with the raw materials of the organisation depending on average cost is not

appropriate, since the current cost of paper exceeds the average cost. The primary risk in the

identification of fraudulent activities of its staffs to implement new system of information

technology could be detected through continual monitoring of the same in different job

phrases. Alongside this risk, the risk pertaining to the procedure of financial reporting could

be identified through assessment of the various financial statements and reports of the

organisations and the responsibility lies on the financial analysts and accountants with the

help of various analytical and control procedures. This process of reviewing as well as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

monitoring is needed to be carried out in a timely fashion (Sutherland 2017). Thus, it has

become possible for the financial analysts and accountants to utilise the financial information

in order to make various business decisions through the analytical method.

References:

Carson, E., Redmayne, N.B. and Liao, L., 2014. Audit market structure and competition in

Australia. Australian Accounting Review, 24(4), pp.298-312.

Carson, E., Simnett, R., Trompeter, G. and Vanstraelen, A., 2014. The Impact of Group Audit

Arrangements on Audit Quality and Pricing.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing:

A Journal of Practice & Theory, 34(1), pp.59-74.

Fernandez-Feijoo, B., Romero, S. and Ruiz, S., 2016. The assurance market of sustainability

reports: What do accounting firms do?. Journal of Cleaner Production, 139, pp.1128-1137.

Gu, T., Simunic, D.A. and Stein, M.T., 2017. Fixed Costs, Audit Production, and Audit

Markets: Theory and Evidence.

Hardy, C.A., 2014. The messy matters of continuous assurance: Findings from exploratory

research in Australia. Journal of Information Systems, 28(2), pp.357-377.

Jones, P., 2016. Internal audit: An integrated approach. Company Director, 32(5), p.50.

Junior, R.M., Best, P.J. and Cotter, J., 2014. Sustainability reporting and assurance: A

historical analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), pp.1-11.

Kend, M., Houghton, K.A. and Jubb, C., 2014. Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4), pp.313-

320.

monitoring is needed to be carried out in a timely fashion (Sutherland 2017). Thus, it has

become possible for the financial analysts and accountants to utilise the financial information

in order to make various business decisions through the analytical method.

References:

Carson, E., Redmayne, N.B. and Liao, L., 2014. Audit market structure and competition in

Australia. Australian Accounting Review, 24(4), pp.298-312.

Carson, E., Simnett, R., Trompeter, G. and Vanstraelen, A., 2014. The Impact of Group Audit

Arrangements on Audit Quality and Pricing.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing:

A Journal of Practice & Theory, 34(1), pp.59-74.

Fernandez-Feijoo, B., Romero, S. and Ruiz, S., 2016. The assurance market of sustainability

reports: What do accounting firms do?. Journal of Cleaner Production, 139, pp.1128-1137.

Gu, T., Simunic, D.A. and Stein, M.T., 2017. Fixed Costs, Audit Production, and Audit

Markets: Theory and Evidence.

Hardy, C.A., 2014. The messy matters of continuous assurance: Findings from exploratory

research in Australia. Journal of Information Systems, 28(2), pp.357-377.

Jones, P., 2016. Internal audit: An integrated approach. Company Director, 32(5), p.50.

Junior, R.M., Best, P.J. and Cotter, J., 2014. Sustainability reporting and assurance: A

historical analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), pp.1-11.

Kend, M., Houghton, K.A. and Jubb, C., 2014. Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4), pp.313-

320.

1 out of 10