Audit Assurance and Compliance: DIPL Financial Analysis Report

VerifiedAdded on 2020/03/02

|9

|2081

|78

Homework Assignment

AI Summary

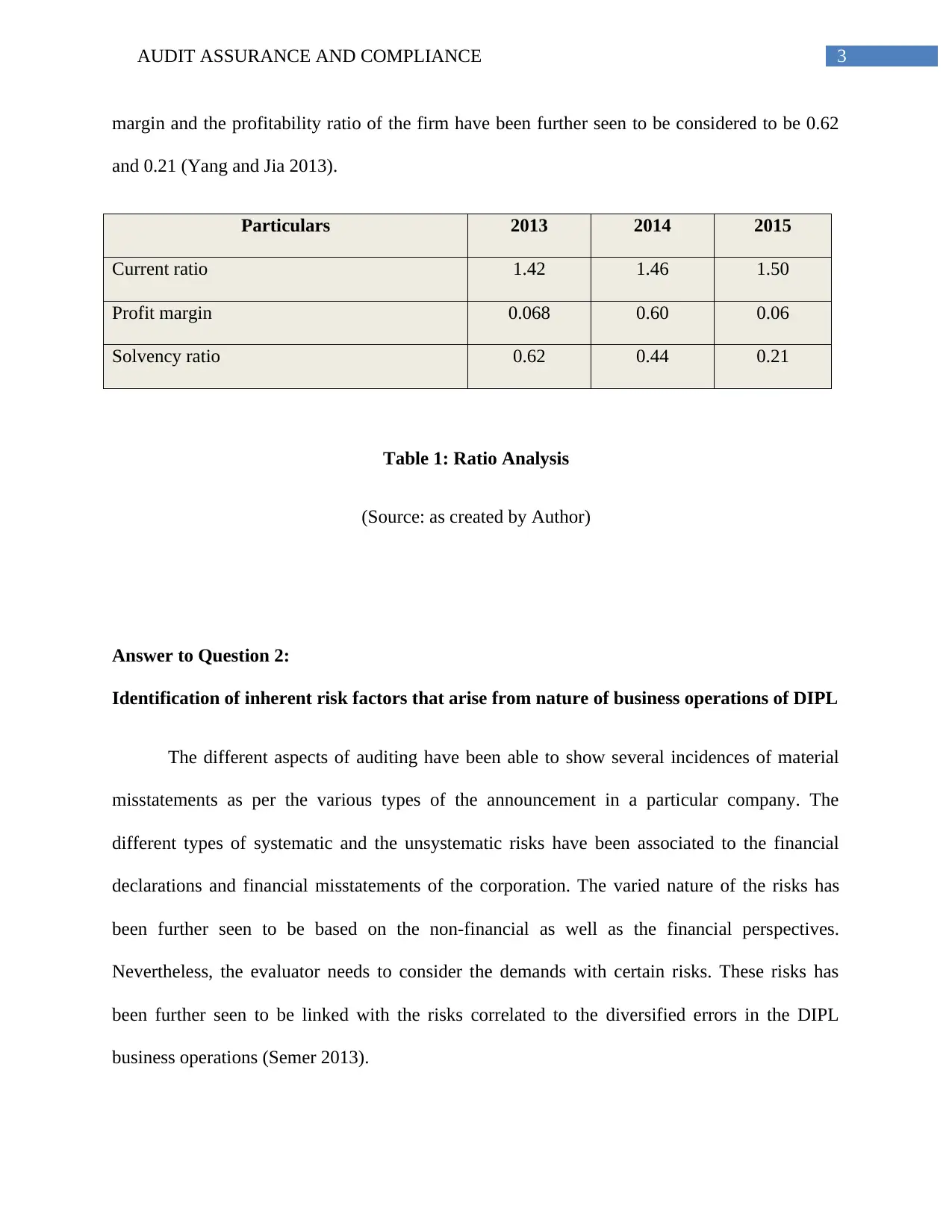

This assignment delves into the realm of audit assurance and compliance, focusing on the financial report of DIPL. It commences with an application of analytical procedures to DIPL's financial information, examining the implications of the audit plan and the dissemination of financial statements. The analysis includes ratio analysis of current ratio, profit margin and solvency ratio over a period of three years (2013-2015). The assignment then identifies inherent risk factors arising from the nature of DIPL's business operations, such as potential misstatements due to omissions by accountants, IT implementation issues, and staff handling of cash receipts. Furthermore, it explores how these risks can affect material misstatements in financial reports, considering factors like pressure on employees, management integrity, and the nature of the business. Finally, the assignment identifies and explains two key fraud risk factors relating to misstatements from fraudulent financial reporting, including asset loss and workforce engagement and the improper financial announcements. The analysis draws on various research articles and provides a comprehensive understanding of the audit process and the associated risks.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.