Audit, Assurance and Compliance Report

VerifiedAdded on 2020/12/10

|13

|3465

|229

Report

AI Summary

This report analyzes the audit, assurance, and compliance practices of Wesfarmers Ltd, a leading Australian company. It examines key audit matters, auditor independence, non-audit services, auditor remuneration, and the role of the audit committee. The report also discusses the responsibilities of directors, managers, and auditors in financial reporting and the assessment of the effectiveness of material information reported by the auditor to stakeholders. Desklib provides past papers and solved assignments for students.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Audit, Assurance and

Compliance

Compliance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Overview of the company...........................................................................................................1

Non audit services.......................................................................................................................2

Auditor's remuneration................................................................................................................2

Role, functions and composition of the audit committee............................................................4

Audit committee helps the board in doing their responsibilities such as overlook on the

company's financial reports, compliance with general laws and regulations..............................4

Audit Opinion..............................................................................................................................5

Key Audit Matters.......................................................................................................................5

Responsibilities of Director, manager and auditor......................................................................6

Material subsequent events.........................................................................................................7

Assessment of the effectiveness of the material information reported by the auditor................8

Follow up questions from auditor in AGM.................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................3

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Overview of the company...........................................................................................................1

Non audit services.......................................................................................................................2

Auditor's remuneration................................................................................................................2

Role, functions and composition of the audit committee............................................................4

Audit committee helps the board in doing their responsibilities such as overlook on the

company's financial reports, compliance with general laws and regulations..............................4

Audit Opinion..............................................................................................................................5

Key Audit Matters.......................................................................................................................5

Responsibilities of Director, manager and auditor......................................................................6

Material subsequent events.........................................................................................................7

Assessment of the effectiveness of the material information reported by the auditor................8

Follow up questions from auditor in AGM.................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY

This project consist of various audit, assurance and compliance concepts. In this project,

the annual report of Wesfarmers are analysed in way to provide an understanding regarding

auditing process. Various key audit matters are discussed in below report along with audit

opinion and committee so audit report of company can be examined.

This project consist of various audit, assurance and compliance concepts. In this project,

the annual report of Wesfarmers are analysed in way to provide an understanding regarding

auditing process. Various key audit matters are discussed in below report along with audit

opinion and committee so audit report of company can be examined.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Auditing is a process of analysing and evaluating financial report of an organisation to

determine statements accuracy. Auditor is an individual who is appointed by company to conduct

audit. The auditor person is responsible for planing and performing audit to obtain correct

financial statements which is free from error or fraud. Internal and external auditors examine

statements on the basis of company's rules and regulations. Internal employee who examine

records and assist in improving inside processes like risk management, operations, internal

control etc. is known as internal auditor. A person comes from outside the company for

examining financial and accounting records and recommend independent opinion for statements

is known as external auditors.

In this report, company's annual report is reviewed and analysed with key areas such as

auditor's independence declaration, non audit services, auditor's remuneration. Function, role,

composition of audit committee is also examine. In last independent auditors report to

stakeholders and all key matters are identified during auditing procedure also covered in report

(Arens, Elder and Mark, 2012).

MAIN BODY

Overview of the company

Wesfarmers Ltd is one of the leading Australian company listed under ASX. It engaged

in several operations such as energy, fertilizers, safety & industrial products, coal, liquor,

convenience stores and hotels etc. Company has approximately 223000 employees throughout 25

locations. It generates majority of its revenue from grocery and supermarkets in Australia. It is

ranked first among top 2000 companies. In 2018 organisation generate total sales revenue of

$66,608,000,000. Mr Rob Scott is the chief executive and Mr Michael Chaney is the chaiirman

of Wesfarmers Ltd. The retail department deals with operations from departmental and

supermarket to office and hardware supplies. Its also operates in industrials division such as

resources, chemicals and fertilizers (Louwers and et. al., 2015).

Auditor's declaration complied with independence requirements

Auditor's independence: It refers to independence of an internal and external auditor

from stakeholders who have financial interest in an organisation. The term independence refers

to integrity as well as an objective approach to audit process. Ernst & Young and DS Lewsen are

1

Auditing is a process of analysing and evaluating financial report of an organisation to

determine statements accuracy. Auditor is an individual who is appointed by company to conduct

audit. The auditor person is responsible for planing and performing audit to obtain correct

financial statements which is free from error or fraud. Internal and external auditors examine

statements on the basis of company's rules and regulations. Internal employee who examine

records and assist in improving inside processes like risk management, operations, internal

control etc. is known as internal auditor. A person comes from outside the company for

examining financial and accounting records and recommend independent opinion for statements

is known as external auditors.

In this report, company's annual report is reviewed and analysed with key areas such as

auditor's independence declaration, non audit services, auditor's remuneration. Function, role,

composition of audit committee is also examine. In last independent auditors report to

stakeholders and all key matters are identified during auditing procedure also covered in report

(Arens, Elder and Mark, 2012).

MAIN BODY

Overview of the company

Wesfarmers Ltd is one of the leading Australian company listed under ASX. It engaged

in several operations such as energy, fertilizers, safety & industrial products, coal, liquor,

convenience stores and hotels etc. Company has approximately 223000 employees throughout 25

locations. It generates majority of its revenue from grocery and supermarkets in Australia. It is

ranked first among top 2000 companies. In 2018 organisation generate total sales revenue of

$66,608,000,000. Mr Rob Scott is the chief executive and Mr Michael Chaney is the chaiirman

of Wesfarmers Ltd. The retail department deals with operations from departmental and

supermarket to office and hardware supplies. Its also operates in industrials division such as

resources, chemicals and fertilizers (Louwers and et. al., 2015).

Auditor's declaration complied with independence requirements

Auditor's independence: It refers to independence of an internal and external auditor

from stakeholders who have financial interest in an organisation. The term independence refers

to integrity as well as an objective approach to audit process. Ernst & Young and DS Lewsen are

1

the two auditors of Wesfarmers who are responsible of presenting accurate information to

company's shareholders. Below are the declaration that have been given by Ernst & Young at the

end of financial year 30 June 2018:

No contraventions of the auditor's independence according to Australian Corporations

Act 2001 in relation to the audit.

No contraventions of some applicable code of professional conduct in relation to audit.

These declarations have been made under section 324DAC of the Corporations Act 2001. Mr

Lewsen also play a important role in company's auditing process.

Non audit services

Non-audit service: It is a professional service which are non included in audit process at

the time of reviewing organisation's financial statements. These are services other than audit

work. Business consulting, payroll preparation, tax planning, accounting services etc. are some

non audit services (Mills, 2012).

Tax compliance and other are the non audit services of Wesfarmers Ltd provided by

Ernst & Young. The total non audit service is $1026000 which consist of $683000 as tax

compliance fee and $ 343000 is other. Total non-audit services fees represent 12% of total fees

paid to auditor and relevant practices for the financial year ended on June 2018. Audit and risk

committee give advice to board about the provision of non audit services. Taxation services

which are provided by the auditor are mandatory to be conducted due to regulations of

governmental authorities, these services are compulsory in nature. The general standard related

to auditor's independence are imposed by Australian Corporations Act, 2001 on the basis of

below reasons:

Non audit services rendered don't involve reviewing auditor's work in company's decision

making process.

These services were dependent on corporate governance policies and procedures adopted

by Wesfarmers and review by Audit and risk committee in way that they doesn't affect

the objectivity and integrity of Ernst & Young.

No reason to argue the truthfulness of auditor's independence declaration (Ryan and et.

al., 2012).

2

company's shareholders. Below are the declaration that have been given by Ernst & Young at the

end of financial year 30 June 2018:

No contraventions of the auditor's independence according to Australian Corporations

Act 2001 in relation to the audit.

No contraventions of some applicable code of professional conduct in relation to audit.

These declarations have been made under section 324DAC of the Corporations Act 2001. Mr

Lewsen also play a important role in company's auditing process.

Non audit services

Non-audit service: It is a professional service which are non included in audit process at

the time of reviewing organisation's financial statements. These are services other than audit

work. Business consulting, payroll preparation, tax planning, accounting services etc. are some

non audit services (Mills, 2012).

Tax compliance and other are the non audit services of Wesfarmers Ltd provided by

Ernst & Young. The total non audit service is $1026000 which consist of $683000 as tax

compliance fee and $ 343000 is other. Total non-audit services fees represent 12% of total fees

paid to auditor and relevant practices for the financial year ended on June 2018. Audit and risk

committee give advice to board about the provision of non audit services. Taxation services

which are provided by the auditor are mandatory to be conducted due to regulations of

governmental authorities, these services are compulsory in nature. The general standard related

to auditor's independence are imposed by Australian Corporations Act, 2001 on the basis of

below reasons:

Non audit services rendered don't involve reviewing auditor's work in company's decision

making process.

These services were dependent on corporate governance policies and procedures adopted

by Wesfarmers and review by Audit and risk committee in way that they doesn't affect

the objectivity and integrity of Ernst & Young.

No reason to argue the truthfulness of auditor's independence declaration (Ryan and et.

al., 2012).

2

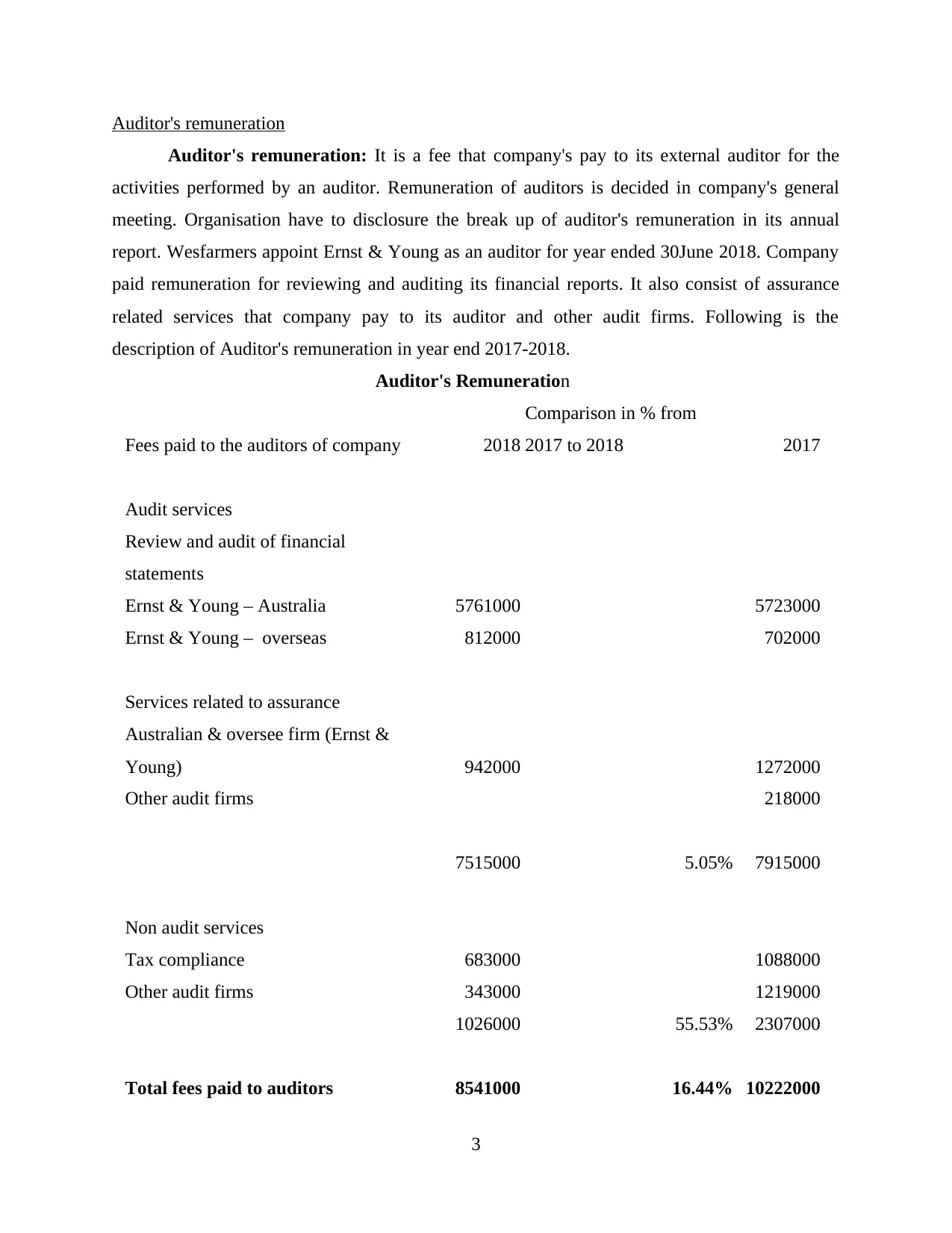

Auditor's remuneration

Auditor's remuneration: It is a fee that company's pay to its external auditor for the

activities performed by an auditor. Remuneration of auditors is decided in company's general

meeting. Organisation have to disclosure the break up of auditor's remuneration in its annual

report. Wesfarmers appoint Ernst & Young as an auditor for year ended 30June 2018. Company

paid remuneration for reviewing and auditing its financial reports. It also consist of assurance

related services that company pay to its auditor and other audit firms. Following is the

description of Auditor's remuneration in year end 2017-2018.

Auditor's Remuneration

Fees paid to the auditors of company 2018

Comparison in % from

2017 to 2018 2017

Audit services

Review and audit of financial

statements

Ernst & Young – Australia 5761000 5723000

Ernst & Young – overseas 812000 702000

Services related to assurance

Australian & oversee firm (Ernst &

Young) 942000 1272000

Other audit firms 218000

7515000 5.05% 7915000

Non audit services

Tax compliance 683000 1088000

Other audit firms 343000 1219000

1026000 55.53% 2307000

Total fees paid to auditors 8541000 16.44% 10222000

3

Auditor's remuneration: It is a fee that company's pay to its external auditor for the

activities performed by an auditor. Remuneration of auditors is decided in company's general

meeting. Organisation have to disclosure the break up of auditor's remuneration in its annual

report. Wesfarmers appoint Ernst & Young as an auditor for year ended 30June 2018. Company

paid remuneration for reviewing and auditing its financial reports. It also consist of assurance

related services that company pay to its auditor and other audit firms. Following is the

description of Auditor's remuneration in year end 2017-2018.

Auditor's Remuneration

Fees paid to the auditors of company 2018

Comparison in % from

2017 to 2018 2017

Audit services

Review and audit of financial

statements

Ernst & Young – Australia 5761000 5723000

Ernst & Young – overseas 812000 702000

Services related to assurance

Australian & oversee firm (Ernst &

Young) 942000 1272000

Other audit firms 218000

7515000 5.05% 7915000

Non audit services

Tax compliance 683000 1088000

Other audit firms 343000 1219000

1026000 55.53% 2307000

Total fees paid to auditors 8541000 16.44% 10222000

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above table of remuneration, it has been concluded that total fees paid to auditor

in year 2018 i.e. 8571000 is less than 2017 which is 1022200. There was a 16.44% of reduction

in total audit fees that Wesfarmers was paid to auditors. Fees paid for reviewing and auditing

Australia also declines from last year that was 5723000 in 2017 and 5761000 in 2018. For

oversee it was increased by 110000 from year 2017 to 2018. Assurance services to Ernst &

Young decreased from 1272000 in 2017 to 942000 in year 2018. Company didn't paid to other

audit firms in 2018 but they paid in 2017 which was 218000. Total percentage change in audit

service is 5.05% and total percentage change in non audit service is 55.53%.

Role, functions and composition of the audit committee

Audit committee: It is group of members selected by company's board of directors who

are responsible for tracking its financial records. All organisation form a audit committee for

controlling its activities. Company select members from its present board of directors and they

take help of other auditors to interpret the corrective measures of its transactions (Prempeh,

Twumasi, and Kyeremeh, 2015).

There is a audit committee in Wesfarmers Ltd to examine the transparency in its financial

reports. Audit committee in Wesfermer includes nine board or director, eight out of them are

non-executive director. These committee member are group of people who posses proper mix of

skills, experience, knowledge and expertise. They also enable the board to more focus on current

businesses operation like, supermarkets, hotels, various comfort store. These audit committee

also work on the study and measure of financial statements, as it help them to know the current

position of company (Wesfarmers, 2018).

Role,function and responsibilities of audit committee.

Audit committee helps the board in doing their responsibilities such as overlook on the

company's financial reports, compliance with general laws and regulations.

They also assist board to actively manage the all teams and their system of internal

control and also manage financial and non financial risk management.

Member of this committee supervise the group's cyber safety that includes data

protection , third party data security management and also develop escalation process on

audit risk.

They monitor the ethical communicator of various product for resale through retail

network (Whitaker, 2013).

4

in year 2018 i.e. 8571000 is less than 2017 which is 1022200. There was a 16.44% of reduction

in total audit fees that Wesfarmers was paid to auditors. Fees paid for reviewing and auditing

Australia also declines from last year that was 5723000 in 2017 and 5761000 in 2018. For

oversee it was increased by 110000 from year 2017 to 2018. Assurance services to Ernst &

Young decreased from 1272000 in 2017 to 942000 in year 2018. Company didn't paid to other

audit firms in 2018 but they paid in 2017 which was 218000. Total percentage change in audit

service is 5.05% and total percentage change in non audit service is 55.53%.

Role, functions and composition of the audit committee

Audit committee: It is group of members selected by company's board of directors who

are responsible for tracking its financial records. All organisation form a audit committee for

controlling its activities. Company select members from its present board of directors and they

take help of other auditors to interpret the corrective measures of its transactions (Prempeh,

Twumasi, and Kyeremeh, 2015).

There is a audit committee in Wesfarmers Ltd to examine the transparency in its financial

reports. Audit committee in Wesfermer includes nine board or director, eight out of them are

non-executive director. These committee member are group of people who posses proper mix of

skills, experience, knowledge and expertise. They also enable the board to more focus on current

businesses operation like, supermarkets, hotels, various comfort store. These audit committee

also work on the study and measure of financial statements, as it help them to know the current

position of company (Wesfarmers, 2018).

Role,function and responsibilities of audit committee.

Audit committee helps the board in doing their responsibilities such as overlook on the

company's financial reports, compliance with general laws and regulations.

They also assist board to actively manage the all teams and their system of internal

control and also manage financial and non financial risk management.

Member of this committee supervise the group's cyber safety that includes data

protection , third party data security management and also develop escalation process on

audit risk.

They monitor the ethical communicator of various product for resale through retail

network (Whitaker, 2013).

4

Audit committee review and assess the team process in Wesfermer that assure the

honesty of the final account and reports.

This committee control different compliance with the accounting system, check legal

requirement for audit in the company.

Member of audit committee review the process of control around the identification of

mercantile income by the selling section that is further used to check that identification is

related to the accounting standard.

They also review and calculate the quality of the team or group protection arrangements

to make sure that appropriate cover are provided for functional and concern risks.

Main responsibilities of this committee is to manage and display the company tax

agreement program in Australia and foreign part , it also includes checking of transverse

intra group transactions (Knechel and Salterio, 2016).

Audit Opinion

The auditors of Wesfarmers Ltd gives various opinions on the company's annual report

and that are mentioned below:

The financial statements shows the true and fair view of each transactions for year

ended 30 June 2018.

The financial managers prepare a accurate consolidated income statement and balance

sheet of the organisation.

The annual reports of company are generate as per the Australian Corporations Act,

2001.

The financial statements are prepared as per the accounting standards of Australia.

Key Audit Matters

Key audit matters are those which are matters which holds most significance in the audit

of financial statements. This matters are identified by the auditors and are communicated with

the organisational authorities. According to the annual report of Wesfarmers Limited, various

key audit matters are identified by the auditor of this company which are mentioned below along

with its audit procedures:

The first most and primary key audit matter of Wesfarmers is Impairment of non current

assets including intangible assets in target. This matter is considered as important as

5

honesty of the final account and reports.

This committee control different compliance with the accounting system, check legal

requirement for audit in the company.

Member of audit committee review the process of control around the identification of

mercantile income by the selling section that is further used to check that identification is

related to the accounting standard.

They also review and calculate the quality of the team or group protection arrangements

to make sure that appropriate cover are provided for functional and concern risks.

Main responsibilities of this committee is to manage and display the company tax

agreement program in Australia and foreign part , it also includes checking of transverse

intra group transactions (Knechel and Salterio, 2016).

Audit Opinion

The auditors of Wesfarmers Ltd gives various opinions on the company's annual report

and that are mentioned below:

The financial statements shows the true and fair view of each transactions for year

ended 30 June 2018.

The financial managers prepare a accurate consolidated income statement and balance

sheet of the organisation.

The annual reports of company are generate as per the Australian Corporations Act,

2001.

The financial statements are prepared as per the accounting standards of Australia.

Key Audit Matters

Key audit matters are those which are matters which holds most significance in the audit

of financial statements. This matters are identified by the auditors and are communicated with

the organisational authorities. According to the annual report of Wesfarmers Limited, various

key audit matters are identified by the auditor of this company which are mentioned below along

with its audit procedures:

The first most and primary key audit matter of Wesfarmers is Impairment of non current

assets including intangible assets in target. This matter is considered as important as

5

determination of recoverable amounts of property, plant and equipment and other

intangible assets requires judgement.

Procedure - In order to avoid the impairment assessment charges it is important to

address this matter with audit procedures. To tackle this matter impairment tests such as discount

tests, terminal growth rates, market evidences of industry earnings, long term inflation and

growth are used (Fiolleau and et. al ., 2013).

Another key audit matter of Wesfarmers is Supplier rebates which is significant for

auditors as rebates received by the group of suppliers associated with its retail

operations.

Procedure - In order to address this matter, various procedures are used such as assessment of

effectiveness of relevant controls and inspection of sample of materials new contracts.

Discontinued operations is also an important key audit matter for auditors of

Wesfarmers. This key audit matter is important as this company has entered into an

agreement to sell the coal mine. This agreement also includes a value share mechanism

linked to future coal prices.

Procedure - In order to tackle this situation, auditor of this company has obtained

procedures of assessing purchase and sale agreements of this company. Auditor has evaluated the

key inputs of the post tax gain on sale calculation. Tax specialists of this audit group has

considered tax impacts of the divestment including considering external advice obtained by the

group (Tepalagul and Lin, 2015).

Another key audit matter is discontinued operations of Bunnings UK and Ireland. This

matters is considered as key audit matter because ample of amount has been paid by the

company due to this impairment.

Procedure - In order to tackle this issue, auditor of this company has assessed the

appropriateness of impairment recognition. Audit group has evaluated the appropriateness of key

inputs by including discount rates, terminal growth rates, market evidences of industry earnings

and many more. Audit procedures for this issue are assessing financial statements disclosures

including the classification of both continued and discontinued operations.

Responsibilities of Director, manager and auditor

Responsibilities of auditors differs from responsibilities of directors and management in

financial reporting by following reasons:

6

intangible assets requires judgement.

Procedure - In order to avoid the impairment assessment charges it is important to

address this matter with audit procedures. To tackle this matter impairment tests such as discount

tests, terminal growth rates, market evidences of industry earnings, long term inflation and

growth are used (Fiolleau and et. al ., 2013).

Another key audit matter of Wesfarmers is Supplier rebates which is significant for

auditors as rebates received by the group of suppliers associated with its retail

operations.

Procedure - In order to address this matter, various procedures are used such as assessment of

effectiveness of relevant controls and inspection of sample of materials new contracts.

Discontinued operations is also an important key audit matter for auditors of

Wesfarmers. This key audit matter is important as this company has entered into an

agreement to sell the coal mine. This agreement also includes a value share mechanism

linked to future coal prices.

Procedure - In order to tackle this situation, auditor of this company has obtained

procedures of assessing purchase and sale agreements of this company. Auditor has evaluated the

key inputs of the post tax gain on sale calculation. Tax specialists of this audit group has

considered tax impacts of the divestment including considering external advice obtained by the

group (Tepalagul and Lin, 2015).

Another key audit matter is discontinued operations of Bunnings UK and Ireland. This

matters is considered as key audit matter because ample of amount has been paid by the

company due to this impairment.

Procedure - In order to tackle this issue, auditor of this company has assessed the

appropriateness of impairment recognition. Audit group has evaluated the appropriateness of key

inputs by including discount rates, terminal growth rates, market evidences of industry earnings

and many more. Audit procedures for this issue are assessing financial statements disclosures

including the classification of both continued and discontinued operations.

Responsibilities of Director, manager and auditor

Responsibilities of auditors differs from responsibilities of directors and management in

financial reporting by following reasons:

6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

No specific responsibility to substantiate other information but should review such

information to ensure it does not contain maternal inconsistencies or misstatements of

facts.

If revision of other information is necessary and management refuses, the auditor should

an OM paragraph.

Most annual reports includes information that is not a part of financial reports, much

which contains of financial information {for example , summarising past year's operating

results, director's and manager's report (Jones, 2017).

Statutory auditors are required to make a statement in their auditors report, whether the

company has adequate IFC system in place and the operating effectiveness of such

controls.

Directors and managers have to select and apply accounting policies,as director's are

responsible for keeping proper financial records which disclose with reasonable accuracy

at any time for financial position of company, for safeguarding the assets, for taking

reasonable steps for preventing and detecting of fraud or other irregularities for the

preparation of director's and manager's remuneration and performance report (Ng, Chong

and Ismail, 2012).

Responsibilities of management and director's differs from the responsibilities of

auditors in financial reporting:

Managers are responsible for providing financial statements to directors, creditors and

others.

Managers may acknowledge their responsibility by including several statements in annual

reports.

Directors responsibility statement that they have laid down internal financial controls to

be followed and that such IFCs are adequate and operating effectively.

Requires the board of directors' report of all companies to tom state in details the

adequacy of internal financial controls with reference to the financial statements.

Auditor's responsibilities differs from director's responsibilities, as they have to perform

internal and external audit functions (Greiner, Kohlbeck and Smith, 2013).

Auditing compliance with laws and regulations, they have to follow.

7

information to ensure it does not contain maternal inconsistencies or misstatements of

facts.

If revision of other information is necessary and management refuses, the auditor should

an OM paragraph.

Most annual reports includes information that is not a part of financial reports, much

which contains of financial information {for example , summarising past year's operating

results, director's and manager's report (Jones, 2017).

Statutory auditors are required to make a statement in their auditors report, whether the

company has adequate IFC system in place and the operating effectiveness of such

controls.

Directors and managers have to select and apply accounting policies,as director's are

responsible for keeping proper financial records which disclose with reasonable accuracy

at any time for financial position of company, for safeguarding the assets, for taking

reasonable steps for preventing and detecting of fraud or other irregularities for the

preparation of director's and manager's remuneration and performance report (Ng, Chong

and Ismail, 2012).

Responsibilities of management and director's differs from the responsibilities of

auditors in financial reporting:

Managers are responsible for providing financial statements to directors, creditors and

others.

Managers may acknowledge their responsibility by including several statements in annual

reports.

Directors responsibility statement that they have laid down internal financial controls to

be followed and that such IFCs are adequate and operating effectively.

Requires the board of directors' report of all companies to tom state in details the

adequacy of internal financial controls with reference to the financial statements.

Auditor's responsibilities differs from director's responsibilities, as they have to perform

internal and external audit functions (Greiner, Kohlbeck and Smith, 2013).

Auditing compliance with laws and regulations, they have to follow.

7

Material subsequent events

Subsequent events: There are certain significant events has been arisen since the closing

of the accounting period within Wesfarmer company. some of them are:

Dividend: According to the annual report prepared as on 17th August, 2017 provide a

fully-franked final dividend of 120% per share resulting in a total dividend of $1.361 million was

declared by the company. The payment made on 28th September, 2017. This dividend has been

not declared for the entire financial period. This event of dividend declaration will be recorded as

foot note in financial statements.

Kmart brand name acquisition: In the month of August, 2017, Kmart acquired the brand

name with various nations such as Australia and New Zealand which as earlier used by the

business under a long-term agreement for $100 million. These transactions are not being taken

into account a material implication on overall earning of the Kmart (Sarkar and Sarkar, 2012).

Assessment of the effectiveness of the material information reported by the auditor to the

stakeholders

Stakeholders such as suppliers and investors are concerned with the true and fair financial

reporting of the company. As the effectiveness of these reports can help them in taking various

decisions such as investment and credit decisions (Nicolăescu, 2013).

Follow up questions from auditor in AGM

Q1. Were appropriate resources dedicated to the audit or not ?

Q2. Did the audit team pertains experienced auditors or not?

Q3. Did the audit provide the details on quality of organisation's financial reporting ?

Q4. Are they free from errors and fraud or not?

CONCLUSION

From the above project report, it has been concluded that company's financial statement

is analysed and evaluated by auditor which help in enhancing audit, assurance and compliance.

Various key audit matters are examine that associated in audit procedures. Tax compliance and

other are the non audit services that are performed by auditor. From the above project report, it

has been seen that the concept of audit is the most significant process which helps in

investigating and checking financial position of an organisation.

8

Subsequent events: There are certain significant events has been arisen since the closing

of the accounting period within Wesfarmer company. some of them are:

Dividend: According to the annual report prepared as on 17th August, 2017 provide a

fully-franked final dividend of 120% per share resulting in a total dividend of $1.361 million was

declared by the company. The payment made on 28th September, 2017. This dividend has been

not declared for the entire financial period. This event of dividend declaration will be recorded as

foot note in financial statements.

Kmart brand name acquisition: In the month of August, 2017, Kmart acquired the brand

name with various nations such as Australia and New Zealand which as earlier used by the

business under a long-term agreement for $100 million. These transactions are not being taken

into account a material implication on overall earning of the Kmart (Sarkar and Sarkar, 2012).

Assessment of the effectiveness of the material information reported by the auditor to the

stakeholders

Stakeholders such as suppliers and investors are concerned with the true and fair financial

reporting of the company. As the effectiveness of these reports can help them in taking various

decisions such as investment and credit decisions (Nicolăescu, 2013).

Follow up questions from auditor in AGM

Q1. Were appropriate resources dedicated to the audit or not ?

Q2. Did the audit team pertains experienced auditors or not?

Q3. Did the audit provide the details on quality of organisation's financial reporting ?

Q4. Are they free from errors and fraud or not?

CONCLUSION

From the above project report, it has been concluded that company's financial statement

is analysed and evaluated by auditor which help in enhancing audit, assurance and compliance.

Various key audit matters are examine that associated in audit procedures. Tax compliance and

other are the non audit services that are performed by auditor. From the above project report, it

has been seen that the concept of audit is the most significant process which helps in

investigating and checking financial position of an organisation.

8

REFERENCES

Books and Journals

Arens, A. A., Elder, R. J. and Mark, B., 2012. Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Louwers, T. J., and et. al., 2015. Auditing & assurance services. McGraw-Hill Education.

Mills, J., 2012. Quality auditing. Springer Science & Business Media.

Ryan, K., and et. al., 2012. Development of a standardised approach to observing hand hygiene

compliance in Australia. Healthcare infection. 17(4). pp.115-121.

Prempeh, K. B., Twumasi, P. and Kyeremeh, K., 2015. Assessment of financial control practices

in Polytechnics in Ghana. A case study of Sunyani Polytechnic.

Whitaker, S., 2013. PMP Rapid Review. Microsoft Press.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk. Routledge.

Fiolleau, K., and et. al ., 2013. How do regulatory reforms to enhance auditor independence work

in practice?. Contemporary Accounting Research. 30(3). pp.864-890.

Tepalagul, N. and Lin, L., 2015. Auditor independence and audit quality: A literature review.

Journal of Accounting, Auditing & Finance. 30(1). pp.101-121.

Jones, P., 2017. Statistical sampling and risk analysis in auditing. Routledge.

Ng, T. H., Chong, L. L. and Ismail, H., 2012. Is the risk management committee only a

procedural compliance? An insight into managing risk taking among insurance

companies in Malaysia. The Journal of Risk Finance. 14(1). pp.71-86.

Sarkar, J. and Sarkar, S., 2012. Auditor and audit committee independence in India.

Greiner, A., Kohlbeck, M. and Smith, T., 2013. Do auditors perceive real earnings management

as a business risk?.

Nicolăescu, E., 2013. Understanding Risk Factors for Weaknesses in Internal Controls over

Financial Reporting. Journal of Self-Governance and Management Economics. 1(3).

pp.38-43.

Online

Wesfarmers. 2018. [Online]. Available through:

<http://www.wesfarmers.com.au/util/news-media/article/2018/09/16/release-of-the-

2018-annual-report-and-shareholder-review>.

9

Books and Journals

Arens, A. A., Elder, R. J. and Mark, B., 2012. Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Louwers, T. J., and et. al., 2015. Auditing & assurance services. McGraw-Hill Education.

Mills, J., 2012. Quality auditing. Springer Science & Business Media.

Ryan, K., and et. al., 2012. Development of a standardised approach to observing hand hygiene

compliance in Australia. Healthcare infection. 17(4). pp.115-121.

Prempeh, K. B., Twumasi, P. and Kyeremeh, K., 2015. Assessment of financial control practices

in Polytechnics in Ghana. A case study of Sunyani Polytechnic.

Whitaker, S., 2013. PMP Rapid Review. Microsoft Press.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk. Routledge.

Fiolleau, K., and et. al ., 2013. How do regulatory reforms to enhance auditor independence work

in practice?. Contemporary Accounting Research. 30(3). pp.864-890.

Tepalagul, N. and Lin, L., 2015. Auditor independence and audit quality: A literature review.

Journal of Accounting, Auditing & Finance. 30(1). pp.101-121.

Jones, P., 2017. Statistical sampling and risk analysis in auditing. Routledge.

Ng, T. H., Chong, L. L. and Ismail, H., 2012. Is the risk management committee only a

procedural compliance? An insight into managing risk taking among insurance

companies in Malaysia. The Journal of Risk Finance. 14(1). pp.71-86.

Sarkar, J. and Sarkar, S., 2012. Auditor and audit committee independence in India.

Greiner, A., Kohlbeck, M. and Smith, T., 2013. Do auditors perceive real earnings management

as a business risk?.

Nicolăescu, E., 2013. Understanding Risk Factors for Weaknesses in Internal Controls over

Financial Reporting. Journal of Self-Governance and Management Economics. 1(3).

pp.38-43.

Online

Wesfarmers. 2018. [Online]. Available through:

<http://www.wesfarmers.com.au/util/news-media/article/2018/09/16/release-of-the-

2018-annual-report-and-shareholder-review>.

9

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.