Auditing and Assurance Process

VerifiedAdded on 2020/10/22

|12

|3358

|243

AI Summary

The assignment provides a comprehensive overview of the auditing process and assurance methods used by KPMG, including a detailed report on the audit findings and conclusions. The document also discusses key questions that can be asked by the auditor at Appen Limited's annual general meeting, highlighting the importance of transparency and accuracy in financial reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Audit, Assurance and

Compliance

Compliance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

This project report is summarises that auditing is a concept which helps in investigating

the accuracy of the financial statements of an organisation. Appen limited is an organisation

which is listed on Australian stock exchange is chosen in order to better understand the topic of

auditing. Audit report and opinions provided by KPMG are analysed and interpreted in order to

ascertain various issues regarding the process of auditing.

This project report is summarises that auditing is a concept which helps in investigating

the accuracy of the financial statements of an organisation. Appen limited is an organisation

which is listed on Australian stock exchange is chosen in order to better understand the topic of

auditing. Audit report and opinions provided by KPMG are analysed and interpreted in order to

ascertain various issues regarding the process of auditing.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Independence requirements compiled by auditor.......................................................................1

Non audit services and there nature............................................................................................2

Analysis of Auditor's remuneration and their comparisons........................................................3

Key audit matters........................................................................................................................4

Audit committee..........................................................................................................................5

Audit opinion..............................................................................................................................5

Responsibilities of Directors, Management and Auditors..........................................................6

Material subsequent events.........................................................................................................7

Assessment of the effectiveness of material information reported by Auditor as a stakeholder 7

Material information...................................................................................................................7

Questions which could be asked by the auditor at the company's annual general meeting........7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Independence requirements compiled by auditor.......................................................................1

Non audit services and there nature............................................................................................2

Analysis of Auditor's remuneration and their comparisons........................................................3

Key audit matters........................................................................................................................4

Audit committee..........................................................................................................................5

Audit opinion..............................................................................................................................5

Responsibilities of Directors, Management and Auditors..........................................................6

Material subsequent events.........................................................................................................7

Assessment of the effectiveness of material information reported by Auditor as a stakeholder 7

Material information...................................................................................................................7

Questions which could be asked by the auditor at the company's annual general meeting........7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION

Audit is an official financial inspection of a company which is conducted by auditors.

Here, auditors can be internal or external. Companies which are listed on a stock exchange of

any country has to conduct a compulsory audit. In this project report, significance of audit

process is discussed in detail by analysing various audit matters. In order to better understand

this topic a company is selected named Appen Limited which is listed on Australian Stock

Exchange. Various documents such as Auditor's Independence Declaration, Independent

auditor's report and Auditor's remuneration are analysed in order to evaluate auditor's assurance

services performed for Appen. KPMG, an auditor's organisation has conducted the process of

audit of this company in order to serve true and fair performance and position of this company

(Mills, 2012).

MAIN BODY

Independence requirements compiled by auditor

According to independence declaration under section 307c of Corporations act 2001, an

audit or review must be conducted of the financial reports for the financial year at the end of

financial period or an audit of financial report half yearly. A declaration in written which depicts

that, to the best of individual auditor's knowledge and belief there have been No contraventions

of auditors independence requirements of this act related to audit or review and no

contraventions of any applicable code of professional conduct in relation to the audit or review.

Another declaration in written which depicts that,to the best of individual auditor's knowledge

and belief, the only contraventions of An auditor independence requirement of this act regarding

audit or review; or any applicable code of professional conduct regarding audit or review are

those contravention details of which are set out in declaration. Declaration either must be given

when the audit report is given to the directors ,registered scheme and disclosing entity, or must

satisfy the conditions of subsection 5(a), also must be signed by the person making the

declaration. By assessing annual report of Appen Limited it has been observed that the auditor

from KPMG (an auditing firm) has complied the independence requirements of corporation act

2001, regarding the audit or review of financial report ,the auditor declares in his written

statement that “to the best of my knowledge and belief in relation to the audit of Appen Limited

for the financial year ending in 31 December 2017, there have been

1

Audit is an official financial inspection of a company which is conducted by auditors.

Here, auditors can be internal or external. Companies which are listed on a stock exchange of

any country has to conduct a compulsory audit. In this project report, significance of audit

process is discussed in detail by analysing various audit matters. In order to better understand

this topic a company is selected named Appen Limited which is listed on Australian Stock

Exchange. Various documents such as Auditor's Independence Declaration, Independent

auditor's report and Auditor's remuneration are analysed in order to evaluate auditor's assurance

services performed for Appen. KPMG, an auditor's organisation has conducted the process of

audit of this company in order to serve true and fair performance and position of this company

(Mills, 2012).

MAIN BODY

Independence requirements compiled by auditor

According to independence declaration under section 307c of Corporations act 2001, an

audit or review must be conducted of the financial reports for the financial year at the end of

financial period or an audit of financial report half yearly. A declaration in written which depicts

that, to the best of individual auditor's knowledge and belief there have been No contraventions

of auditors independence requirements of this act related to audit or review and no

contraventions of any applicable code of professional conduct in relation to the audit or review.

Another declaration in written which depicts that,to the best of individual auditor's knowledge

and belief, the only contraventions of An auditor independence requirement of this act regarding

audit or review; or any applicable code of professional conduct regarding audit or review are

those contravention details of which are set out in declaration. Declaration either must be given

when the audit report is given to the directors ,registered scheme and disclosing entity, or must

satisfy the conditions of subsection 5(a), also must be signed by the person making the

declaration. By assessing annual report of Appen Limited it has been observed that the auditor

from KPMG (an auditing firm) has complied the independence requirements of corporation act

2001, regarding the audit or review of financial report ,the auditor declares in his written

statement that “to the best of my knowledge and belief in relation to the audit of Appen Limited

for the financial year ending in 31 December 2017, there have been

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

no contraventions of auditors independence requirements as set out in corporation act 2001, in

relation to the audit, no contraventions of any applicable code of professional conduct in relation

to the audit of financial report (Ryan, 2012).

Non audit services and their nature

KPMG is a group auditor which has conducted the process of auditing from Appen

Limited. Non audit services are those which are done in addition to the audit and which are not

related with reviewing of financial statements of an organisation. This audit group has conducted

various non audit services for Appen Limited such as transfer pricing, employee share scheme,

transaction assistance and taxation services. This information about non audit services is gained

from Auditor's Independent report and Independence declaration. Nature of these services are

discussed below:

Transfer pricing – Transfer pricing is a process in which good and services are

exchanged within an organisation. These legal entities can be parent and subsidiary companies.

KPMG, the auditor group of Appen Limited has provided service of transfer pricing according to

which prices are fixed by which an organisation can transfer their goods and services with their

organisation (Prempeh, Twumasi and Kyeremeh, 2015).

Employee share scheme – This service is provided by the auditor to Appen Limited.

According to this service, company provides an option to their employees to buy a sum of shares

in less cost and sometimes even for free. KPMG group has provided this service to facilitate

Appen Limited to provides employee stock exchange schemes.

Transaction assistance – These are the services which are provided by KPMG in order

to facilitate their clients. By these service of transaction assistance, various challenges can be

faced by an organisation by developing effective strategy. This service is not included in audit

services but are performed by KPMG for Appen Limited.

Taxation services – As it name suggests, these services are related with the taxation and

compliances which are mandatory to be done by an organisation. Auditor group of Appen

Limited provides these facilities to them.

The above mentioned services which are provided by KPMG group to Appen Limited are

non audit services. But due to performance of these services, auditor is evidently paid for these

services also. From the annual reports of Appen Limited, it can be said that KPMG has paid

value of 226264 dollars. This amount is mentioned in the auditor's remuneration report.

2

relation to the audit, no contraventions of any applicable code of professional conduct in relation

to the audit of financial report (Ryan, 2012).

Non audit services and their nature

KPMG is a group auditor which has conducted the process of auditing from Appen

Limited. Non audit services are those which are done in addition to the audit and which are not

related with reviewing of financial statements of an organisation. This audit group has conducted

various non audit services for Appen Limited such as transfer pricing, employee share scheme,

transaction assistance and taxation services. This information about non audit services is gained

from Auditor's Independent report and Independence declaration. Nature of these services are

discussed below:

Transfer pricing – Transfer pricing is a process in which good and services are

exchanged within an organisation. These legal entities can be parent and subsidiary companies.

KPMG, the auditor group of Appen Limited has provided service of transfer pricing according to

which prices are fixed by which an organisation can transfer their goods and services with their

organisation (Prempeh, Twumasi and Kyeremeh, 2015).

Employee share scheme – This service is provided by the auditor to Appen Limited.

According to this service, company provides an option to their employees to buy a sum of shares

in less cost and sometimes even for free. KPMG group has provided this service to facilitate

Appen Limited to provides employee stock exchange schemes.

Transaction assistance – These are the services which are provided by KPMG in order

to facilitate their clients. By these service of transaction assistance, various challenges can be

faced by an organisation by developing effective strategy. This service is not included in audit

services but are performed by KPMG for Appen Limited.

Taxation services – As it name suggests, these services are related with the taxation and

compliances which are mandatory to be done by an organisation. Auditor group of Appen

Limited provides these facilities to them.

The above mentioned services which are provided by KPMG group to Appen Limited are

non audit services. But due to performance of these services, auditor is evidently paid for these

services also. From the annual reports of Appen Limited, it can be said that KPMG has paid

value of 226264 dollars. This amount is mentioned in the auditor's remuneration report.

2

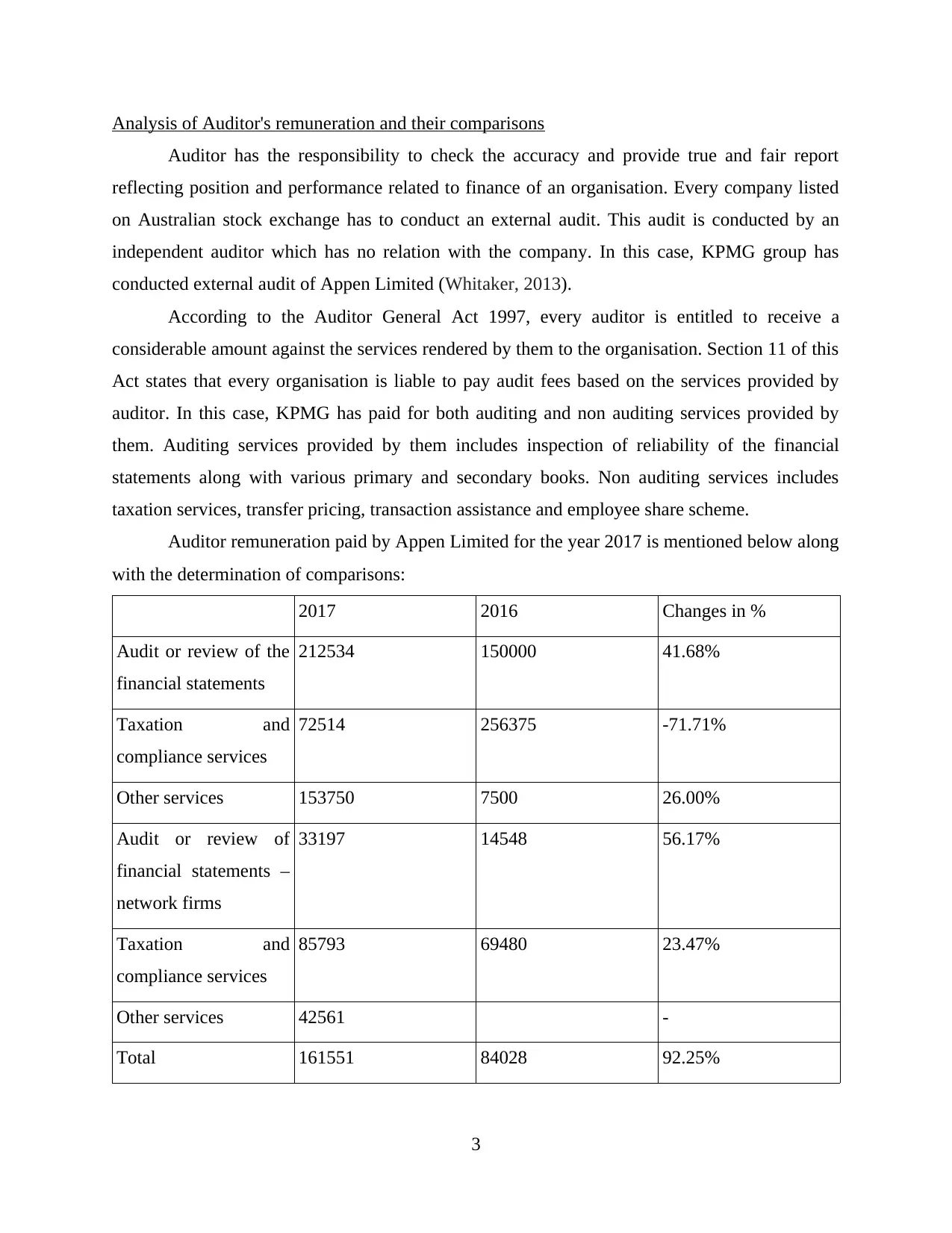

Analysis of Auditor's remuneration and their comparisons

Auditor has the responsibility to check the accuracy and provide true and fair report

reflecting position and performance related to finance of an organisation. Every company listed

on Australian stock exchange has to conduct an external audit. This audit is conducted by an

independent auditor which has no relation with the company. In this case, KPMG group has

conducted external audit of Appen Limited (Whitaker, 2013).

According to the Auditor General Act 1997, every auditor is entitled to receive a

considerable amount against the services rendered by them to the organisation. Section 11 of this

Act states that every organisation is liable to pay audit fees based on the services provided by

auditor. In this case, KPMG has paid for both auditing and non auditing services provided by

them. Auditing services provided by them includes inspection of reliability of the financial

statements along with various primary and secondary books. Non auditing services includes

taxation services, transfer pricing, transaction assistance and employee share scheme.

Auditor remuneration paid by Appen Limited for the year 2017 is mentioned below along

with the determination of comparisons:

2017 2016 Changes in %

Audit or review of the

financial statements

212534 150000 41.68%

Taxation and

compliance services

72514 256375 -71.71%

Other services 153750 7500 26.00%

Audit or review of

financial statements –

network firms

33197 14548 56.17%

Taxation and

compliance services

85793 69480 23.47%

Other services 42561 -

Total 161551 84028 92.25%

3

Auditor has the responsibility to check the accuracy and provide true and fair report

reflecting position and performance related to finance of an organisation. Every company listed

on Australian stock exchange has to conduct an external audit. This audit is conducted by an

independent auditor which has no relation with the company. In this case, KPMG group has

conducted external audit of Appen Limited (Whitaker, 2013).

According to the Auditor General Act 1997, every auditor is entitled to receive a

considerable amount against the services rendered by them to the organisation. Section 11 of this

Act states that every organisation is liable to pay audit fees based on the services provided by

auditor. In this case, KPMG has paid for both auditing and non auditing services provided by

them. Auditing services provided by them includes inspection of reliability of the financial

statements along with various primary and secondary books. Non auditing services includes

taxation services, transfer pricing, transaction assistance and employee share scheme.

Auditor remuneration paid by Appen Limited for the year 2017 is mentioned below along

with the determination of comparisons:

2017 2016 Changes in %

Audit or review of the

financial statements

212534 150000 41.68%

Taxation and

compliance services

72514 256375 -71.71%

Other services 153750 7500 26.00%

Audit or review of

financial statements –

network firms

33197 14548 56.17%

Taxation and

compliance services

85793 69480 23.47%

Other services 42561 -

Total 161551 84028 92.25%

3

In the above table, auditor's remuneration is analysed by ascertaining the changes in

current year remuneration and past year's remuneration. It has been evaluated that besides

payment of taxation services, all the payment for other audit and non audit services has been

increased. Total auditor's remuneration which is paid to KPMG by Appen Limited in the year of

2016 was 84028 dollars. Whereas in the year of 2017, this amount increased and valued at

161551 which 92.25% higher than last year. The reasons for this change are, higher non audit

services rendered by auditor such as employee stock option and transfer pricing. Higher auditor's

remuneration in the year 2017 can be justified by higher rates provided by Audit General and

increased functions of Appen Limited (Knechel and Salterio, 2016).

Key audit matters

According to the annual report of “Appen limited company”, an auditor need to analyse

certain key matters those are taken from the financial report of the company. It is basically

associated with the substantial amount of group earnings those are related to the revenue

generated from the execution of services. “Appen limited company” aimed on revenue

recognition as a primary audit matter because of the significance audit effort needed to test the

varied earning streams in the company. The two major streams are discussed below:

Revenue from the execution of language resources services (Fiolleau and et. al., 2013).

Income generated from relevance of services.

At the closing of the year, an important value of work in progress (WIP) is been

associated with the revenue incurred from language resources services and receivables are

taken into account.

There is certain procedure which has been followed in order to addressed in the company

audit. Some of them are mentioned below:

Auditors used to test key measures and control in the group income process which

consists of administration approval of sales invoices and reviews. It will be useful while

preparing monthly project reporting at the closing of the month.

Auditor selected a numerical samples of language resources projects that is based on the

quantitative nature of WIP at the end of accounting period.

In order to select sample, auditor perform necessary procedures in context to the

management recognition of incomes such as auditor used to compare the total time and costs of

4

current year remuneration and past year's remuneration. It has been evaluated that besides

payment of taxation services, all the payment for other audit and non audit services has been

increased. Total auditor's remuneration which is paid to KPMG by Appen Limited in the year of

2016 was 84028 dollars. Whereas in the year of 2017, this amount increased and valued at

161551 which 92.25% higher than last year. The reasons for this change are, higher non audit

services rendered by auditor such as employee stock option and transfer pricing. Higher auditor's

remuneration in the year 2017 can be justified by higher rates provided by Audit General and

increased functions of Appen Limited (Knechel and Salterio, 2016).

Key audit matters

According to the annual report of “Appen limited company”, an auditor need to analyse

certain key matters those are taken from the financial report of the company. It is basically

associated with the substantial amount of group earnings those are related to the revenue

generated from the execution of services. “Appen limited company” aimed on revenue

recognition as a primary audit matter because of the significance audit effort needed to test the

varied earning streams in the company. The two major streams are discussed below:

Revenue from the execution of language resources services (Fiolleau and et. al., 2013).

Income generated from relevance of services.

At the closing of the year, an important value of work in progress (WIP) is been

associated with the revenue incurred from language resources services and receivables are

taken into account.

There is certain procedure which has been followed in order to addressed in the company

audit. Some of them are mentioned below:

Auditors used to test key measures and control in the group income process which

consists of administration approval of sales invoices and reviews. It will be useful while

preparing monthly project reporting at the closing of the month.

Auditor selected a numerical samples of language resources projects that is based on the

quantitative nature of WIP at the end of accounting period.

In order to select sample, auditor perform necessary procedures in context to the

management recognition of incomes such as auditor used to compare the total time and costs of

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budget to accomplish a customer project between the customer contract and detailed given by the

project in-charges.

Another key audit matter which is impacted judgement of auditor is determination of

purchase consideration for which KPMG obtained purchase agreement to understand the

structure and nature of certain payments. To ascertain consideration of purchases, auditor has

evaluated accounting treatment of acquisition and transaction costs against accounting standards.

Disclosure of acquisition in the financial statements is also a key audit matter for Auditors of

Appen Limited (Key audit matters, 2018).

Audit committee

Audit committee is a group of individuals which inspect and check the accuracy and

effectiveness of financial statements of an organisation. Audit committee may include non

executive directors and charter. In the case of Appen Limited, there is an audit committee which

has one chairman and two members. From the annual report of Appen Limited, it can be said that

Robin Low is the chairman of the audit committee. Two members of this committee are Chris

Vonwiller and Deena Shiff.

Non executive directors are external directors which has independent nature and does not

has any relation with the company. These directors are the members of board of directors who

does not form part of the executive management team. In the case of Appen Limited, there are

six non executive directors which are paid according to their chairmanship. These non executive

directors are entitle to have a fee of 70000 dollars.

From the annual reports of Appen limited, it has been observed that there is no Audit

committee charter. Audit committee of this company is independent and so its roles which

includes developing audit report, serving true and fair perspective about financial position and

investigating the financial statements (Tepalagul, 2015).

Audit opinion

Audit opinion is a document which states unbiased and qualified evaluation of the

company. This document includes interpretation of accuracy and completeness of a company's

financial statements and practices. There various types of Audit opinion such as Unmodified

opinion, adverse opinion, qualified opinion and disclaimer of opinion.

In the case of Appen Limited, KPMG has provided Unmodified opinion. According to

this opinion auditor has all the sufficient and appropriate information about the company and

5

project in-charges.

Another key audit matter which is impacted judgement of auditor is determination of

purchase consideration for which KPMG obtained purchase agreement to understand the

structure and nature of certain payments. To ascertain consideration of purchases, auditor has

evaluated accounting treatment of acquisition and transaction costs against accounting standards.

Disclosure of acquisition in the financial statements is also a key audit matter for Auditors of

Appen Limited (Key audit matters, 2018).

Audit committee

Audit committee is a group of individuals which inspect and check the accuracy and

effectiveness of financial statements of an organisation. Audit committee may include non

executive directors and charter. In the case of Appen Limited, there is an audit committee which

has one chairman and two members. From the annual report of Appen Limited, it can be said that

Robin Low is the chairman of the audit committee. Two members of this committee are Chris

Vonwiller and Deena Shiff.

Non executive directors are external directors which has independent nature and does not

has any relation with the company. These directors are the members of board of directors who

does not form part of the executive management team. In the case of Appen Limited, there are

six non executive directors which are paid according to their chairmanship. These non executive

directors are entitle to have a fee of 70000 dollars.

From the annual reports of Appen limited, it has been observed that there is no Audit

committee charter. Audit committee of this company is independent and so its roles which

includes developing audit report, serving true and fair perspective about financial position and

investigating the financial statements (Tepalagul, 2015).

Audit opinion

Audit opinion is a document which states unbiased and qualified evaluation of the

company. This document includes interpretation of accuracy and completeness of a company's

financial statements and practices. There various types of Audit opinion such as Unmodified

opinion, adverse opinion, qualified opinion and disclaimer of opinion.

In the case of Appen Limited, KPMG has provided Unmodified opinion. According to

this opinion auditor has all the sufficient and appropriate information about the company and

5

there is no need to further change the financial statements of the company. This auditor's opinion

is procured from independent auditors report to the members or shareholders. KPMG has

provided their opinion in the audit report which states that all the financial statements and reports

of Appen Limited are preprepared according to the Corporations Act and all the compliances

which are needed to be fulfilled are presented in the prescribed manner (Jones, 2017).

Responsibilities of Directors, Management and Auditors

Directors and management of the company are the internal parties which are responsible

for the internal affairs of an organisation. From the annual reports of Appen Limited it can be

said that roles of directors include:

Directors of an organisations should ensure that financial report gives true and fair view

of financial performance and are prepared according to the Australian Accounting

standards and the Corporations act 2001.

Management and directors should ensure that financial reports are prepared from

complying effective internal control and there is no material misstatement.

Selecting an appropriate method and strategy for the organisation is also a responsibility

of directors. For example, In the case of Appen Limited directors has to decide whether

they has to use going concern method or any other method so that they can provide

benefit to their organisation (Ng, Chong and Ismail, 2012).

Responsibilities of Auditors are different from the responsibilities of directors as auditors

are the external independent parties which has concerned their goals towards providing true and

fair opinion about the company. Some of the responsibilities of auditors which are different from

directors are mentioned below:

Auditor has primary responsibility to obtain reasonable assurance about whether financial

report has any material misstatement or not. If there is any misstatement, then they are

responsible to determine its causes such as fraud or mistake.

Responsibilities of auditor are different from directors, as it includes providing an

opinion about the company which can only be done by some external parties which does

not hold any interest in the company.

From the above points and evidences from annual reports of Appen Limited it can be said

that responsibilities of directors or management and auditors are way different as they are

different parties and has different interests in the organisation.

6

is procured from independent auditors report to the members or shareholders. KPMG has

provided their opinion in the audit report which states that all the financial statements and reports

of Appen Limited are preprepared according to the Corporations Act and all the compliances

which are needed to be fulfilled are presented in the prescribed manner (Jones, 2017).

Responsibilities of Directors, Management and Auditors

Directors and management of the company are the internal parties which are responsible

for the internal affairs of an organisation. From the annual reports of Appen Limited it can be

said that roles of directors include:

Directors of an organisations should ensure that financial report gives true and fair view

of financial performance and are prepared according to the Australian Accounting

standards and the Corporations act 2001.

Management and directors should ensure that financial reports are prepared from

complying effective internal control and there is no material misstatement.

Selecting an appropriate method and strategy for the organisation is also a responsibility

of directors. For example, In the case of Appen Limited directors has to decide whether

they has to use going concern method or any other method so that they can provide

benefit to their organisation (Ng, Chong and Ismail, 2012).

Responsibilities of Auditors are different from the responsibilities of directors as auditors

are the external independent parties which has concerned their goals towards providing true and

fair opinion about the company. Some of the responsibilities of auditors which are different from

directors are mentioned below:

Auditor has primary responsibility to obtain reasonable assurance about whether financial

report has any material misstatement or not. If there is any misstatement, then they are

responsible to determine its causes such as fraud or mistake.

Responsibilities of auditor are different from directors, as it includes providing an

opinion about the company which can only be done by some external parties which does

not hold any interest in the company.

From the above points and evidences from annual reports of Appen Limited it can be said

that responsibilities of directors or management and auditors are way different as they are

different parties and has different interests in the organisation.

6

Material subsequent events

According to the Corporations Act 2001, material subsequent events are those

circumstances which occurs after the reporting period of an organisation but before issuing the

financial statements (Sarkar and Sarkar, 2012). These events are typically presented and

disclosed in an annual report of an organisation. From the annual reports of Appen Limited, it

can be said that there is only a event which is reported after the reporting period which is

dividend declaration.

Annual reports of this company states that on February 2018, company has declared a

final dividend for the year ended 31 December 2017 of 3.0 cents per share. This information is a

material subsequent event.

Assessment of the effectiveness of material information reported by Auditor as a stakeholder

Stakeholders of an organisation can be investors, suppliers and many more. From the

view point of a stakeholder it can be said that material information such as profitability and ratios

and sales budgets should be assessed effectively so that reliable results of the organisation can be

ascertained (Greiner, 2013).

Material information

KPMG, auditor group of Appen Limited has provided an auditor report which states that

every information is present in the annual report which can affect the performance or position of

an organisation. From the audit report of this company it can be said that there is no material

information which is suppressed by the organisation (Nicolăescu, 2013).

Questions which could be asked by the auditor at the company's annual general meeting

At the annual general meeting of Appen Limited, various questions can be asked from the

auditor group that is KPMG and some of those questions are:

Does all the accounting standards are compiled and followed by Appen Limited?

Is audit team able to compare the accounting policies with performed practices?

Is audit team was aware about changes in accounting principles and auditing standards of

Appen Limited?

CONCLUSION

From the above project report, it can be concluded that auditing is the most significant

process which helps in investigating and checking the reliability and accuracy of the financial

7

According to the Corporations Act 2001, material subsequent events are those

circumstances which occurs after the reporting period of an organisation but before issuing the

financial statements (Sarkar and Sarkar, 2012). These events are typically presented and

disclosed in an annual report of an organisation. From the annual reports of Appen Limited, it

can be said that there is only a event which is reported after the reporting period which is

dividend declaration.

Annual reports of this company states that on February 2018, company has declared a

final dividend for the year ended 31 December 2017 of 3.0 cents per share. This information is a

material subsequent event.

Assessment of the effectiveness of material information reported by Auditor as a stakeholder

Stakeholders of an organisation can be investors, suppliers and many more. From the

view point of a stakeholder it can be said that material information such as profitability and ratios

and sales budgets should be assessed effectively so that reliable results of the organisation can be

ascertained (Greiner, 2013).

Material information

KPMG, auditor group of Appen Limited has provided an auditor report which states that

every information is present in the annual report which can affect the performance or position of

an organisation. From the audit report of this company it can be said that there is no material

information which is suppressed by the organisation (Nicolăescu, 2013).

Questions which could be asked by the auditor at the company's annual general meeting

At the annual general meeting of Appen Limited, various questions can be asked from the

auditor group that is KPMG and some of those questions are:

Does all the accounting standards are compiled and followed by Appen Limited?

Is audit team able to compare the accounting policies with performed practices?

Is audit team was aware about changes in accounting principles and auditing standards of

Appen Limited?

CONCLUSION

From the above project report, it can be concluded that auditing is the most significant

process which helps in investigating and checking the reliability and accuracy of the financial

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

information of an organisation. By analysing the annual reports of Appen Limited it can be said

that their auditor group that is KPMG has provided opinion that all the financial statements of

this company are developed according to the international accounting standards.

8

that their auditor group that is KPMG has provided opinion that all the financial statements of

this company are developed according to the international accounting standards.

8

REFERENCES

Books and Journals:

Mills, J., 2012. Quality auditing. Springer Science & Business Media.

Ryan, K., and et. al., 2012. Development of a standardised approach to observing hand hygiene

compliance in Australia. Healthcare infection. 17(4). pp.115-121.

Prempeh, K. B., Twumasi, P. and Kyeremeh, K., 2015. Assessment of financial control practices

in Polytechnics in Ghana. A case study of Sunyani Polytechnic.

Whitaker, S., 2013. PMP Rapid Review. Microsoft Press.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk. Routledge.

Fiolleau, K., and et. al ., 2013. How do regulatory reforms to enhance auditor independence work

in practice?. Contemporary Accounting Research. 30(3). pp.864-890.

Tepalagul, N. and Lin, L., 2015. Auditor independence and audit quality: A literature review.

Journal of Accounting, Auditing & Finance. 30(1). pp.101-121.

Jones, P., 2017. Statistical sampling and risk analysis in auditing. Routledge.

Ng, T. H., Chong, L. L. and Ismail, H., 2012. Is the risk management committee only a

procedural compliance? An insight into managing risk taking among insurance

companies in Malaysia. The Journal of Risk Finance. 14(1). pp.71-86.

Sarkar, J. and Sarkar, S., 2012. Auditor and audit committee independence in India.

Greiner, A., Kohlbeck, M. and Smith, T., 2013. Do auditors perceive real earnings management

as a business risk?.

Nicolăescu, E., 2013. Understanding Risk Factors for Weaknesses in Internal Controls over

Financial Reporting. Journal of Self-Governance and Management Economics. 1(3).

Online

Key audit matters. 2018. [Online]. Available through: <https://cleartax.in/s/sa-701-

communicating-key-audit-matters>

9

Books and Journals:

Mills, J., 2012. Quality auditing. Springer Science & Business Media.

Ryan, K., and et. al., 2012. Development of a standardised approach to observing hand hygiene

compliance in Australia. Healthcare infection. 17(4). pp.115-121.

Prempeh, K. B., Twumasi, P. and Kyeremeh, K., 2015. Assessment of financial control practices

in Polytechnics in Ghana. A case study of Sunyani Polytechnic.

Whitaker, S., 2013. PMP Rapid Review. Microsoft Press.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk. Routledge.

Fiolleau, K., and et. al ., 2013. How do regulatory reforms to enhance auditor independence work

in practice?. Contemporary Accounting Research. 30(3). pp.864-890.

Tepalagul, N. and Lin, L., 2015. Auditor independence and audit quality: A literature review.

Journal of Accounting, Auditing & Finance. 30(1). pp.101-121.

Jones, P., 2017. Statistical sampling and risk analysis in auditing. Routledge.

Ng, T. H., Chong, L. L. and Ismail, H., 2012. Is the risk management committee only a

procedural compliance? An insight into managing risk taking among insurance

companies in Malaysia. The Journal of Risk Finance. 14(1). pp.71-86.

Sarkar, J. and Sarkar, S., 2012. Auditor and audit committee independence in India.

Greiner, A., Kohlbeck, M. and Smith, T., 2013. Do auditors perceive real earnings management

as a business risk?.

Nicolăescu, E., 2013. Understanding Risk Factors for Weaknesses in Internal Controls over

Financial Reporting. Journal of Self-Governance and Management Economics. 1(3).

Online

Key audit matters. 2018. [Online]. Available through: <https://cleartax.in/s/sa-701-

communicating-key-audit-matters>

9

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.