Audit, Assurance and Compliance

VerifiedAdded on 2023/06/12

|15

|3249

|439

AI Summary

The report analyses the compliance of ASX corporate governance principles by Qantas Airways and the risk involved in the business of the company. It also states the business strategies, market overview and industry overview of the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, assurance and compliance

Name of the student

Name of the university

Student ID

Author note

Audit, assurance and compliance

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

1. Executive summary.............................................................................................................2

2. ASX Corporate Governance Principles..............................................................................3

3. Risk assessment..................................................................................................................7

Reference..................................................................................................................................13

Table of Contents

1. Executive summary.............................................................................................................2

2. ASX Corporate Governance Principles..............................................................................3

3. Risk assessment..................................................................................................................7

Reference..................................................................................................................................13

2AUDIT, ASSURANCE AND COMPLIANCE

1. Executive summary

The main objective of the report is to analyse the compliance of ASX corporate governance

principles by Qantas Airways and the risk involved in the business of the company. The

report will also state the business strategies, market overview and industry overview of the

company. Qantas airways complies with all the ASX listed Corporate Governance principles.

Further, the risk that is found while auditing the company is that the company is highly

leveraged and not earning sufficient profit. Further, the short term assets of the company are

not sufficient to pay off its liabilities.

1. Executive summary

The main objective of the report is to analyse the compliance of ASX corporate governance

principles by Qantas Airways and the risk involved in the business of the company. The

report will also state the business strategies, market overview and industry overview of the

company. Qantas airways complies with all the ASX listed Corporate Governance principles.

Further, the risk that is found while auditing the company is that the company is highly

leveraged and not earning sufficient profit. Further, the short term assets of the company are

not sufficient to pay off its liabilities.

3AUDIT, ASSURANCE AND COMPLIANCE

2. ASX Corporate Governance Principles

1. Lay solid foundations for the management and oversight

The board of Qantas airways adopted the formal charter that can be obtained from the

official website of the company under section of corporate governance. Board is answerable

for setting up and reviewing strategic direction of the company and thereby monitoring

implementation strategy by the management (Bottomley 2016). Further, the CEO is

accountable for day to day management of the company with all the discretions, power and

authorised delegations by the board from time to time. The secretary of the company is

directly responsible to the board through Chairman for all the concerned matters for doing

those with proper activities of board.

2. Structure of board for adding value

At present the company has 10 directors on their board. Among those 9 directors are

non-executive independent director who were elected by the shareholders. The CEO of the

company is an executive director; however, he is not independent (Chan, Watson and

Woodliff 2014). The board of the company gas 4 committees – Audit committee,

remuneration committee, nomination committee and environment, health, safety and security

committee. Each of these committees helps the board for particular responsibilities that are

decided under the charters committee and it is approved and delegated by board.

3. Act ethically as well as responsibly

The board of Qantas Airways formed the corporate governance framework that

includes group policies and non-negotiable principles for business that establishes the

foundation for the manner in which the company undertakes its business (Christensen et al.

2015). Group policies and principles that include the ethics and code of conduct for the

2. ASX Corporate Governance Principles

1. Lay solid foundations for the management and oversight

The board of Qantas airways adopted the formal charter that can be obtained from the

official website of the company under section of corporate governance. Board is answerable

for setting up and reviewing strategic direction of the company and thereby monitoring

implementation strategy by the management (Bottomley 2016). Further, the CEO is

accountable for day to day management of the company with all the discretions, power and

authorised delegations by the board from time to time. The secretary of the company is

directly responsible to the board through Chairman for all the concerned matters for doing

those with proper activities of board.

2. Structure of board for adding value

At present the company has 10 directors on their board. Among those 9 directors are

non-executive independent director who were elected by the shareholders. The CEO of the

company is an executive director; however, he is not independent (Chan, Watson and

Woodliff 2014). The board of the company gas 4 committees – Audit committee,

remuneration committee, nomination committee and environment, health, safety and security

committee. Each of these committees helps the board for particular responsibilities that are

decided under the charters committee and it is approved and delegated by board.

3. Act ethically as well as responsibly

The board of Qantas Airways formed the corporate governance framework that

includes group policies and non-negotiable principles for business that establishes the

foundation for the manner in which the company undertakes its business (Christensen et al.

2015). Group policies and principles that include the ethics and code of conduct for the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUDIT, ASSURANCE AND COMPLIANCE

company are stated in detail under the practice document of Qantas Airways. The framework

is supported by the rigorous program of whistleblower that provides protected process of

disclosures for the employees. The share trading policies of the employees are stated in the

guideline that is designed for protecting the directors and employees from unintentional as

well as intentional breaching of law. It further, disallows the employees to deal in securities

of any group listed company of Qantas while having information that is material and non-

public. Apart from this, few nominated employees are not allowed to enter into the margin

lending or hedging or granting the chance over the securities of any group of Qantas group

where the control on sales procedures associated with securities may be lost (Council and

Exchange 2014).

4. Safeguard integrity under corporate reporting

The audit committee and the board of the company closely monitor the external

auditor’s independence. Regular reviews are carried out for safeguarding the independence of

internal auditor. Further the company rotates its lead partner for audit in each 5 years and

imposes the restrictions on engagement of the personnel those were previously engaged by

external auditor (Council 2014). The policies of the company are appropriately applied for

putting the restrictions on non-audit services that can be provided by the external auditors.

Further, the detailed analysis of non-audit fees paid to external auditors are carried on half –

yearly basis. In every meeting the audit committee privately meets with the executive

management without including the external auditor and with external and internal auditors

without including the executive management (Du Plessis, Hargovan and Harris 2018).

5. Make timely and balanced disclosures

The company is committed to assure that the trading in the share takes place in

informed and orderly market through availing consistent and transparent communication with

company are stated in detail under the practice document of Qantas Airways. The framework

is supported by the rigorous program of whistleblower that provides protected process of

disclosures for the employees. The share trading policies of the employees are stated in the

guideline that is designed for protecting the directors and employees from unintentional as

well as intentional breaching of law. It further, disallows the employees to deal in securities

of any group listed company of Qantas while having information that is material and non-

public. Apart from this, few nominated employees are not allowed to enter into the margin

lending or hedging or granting the chance over the securities of any group of Qantas group

where the control on sales procedures associated with securities may be lost (Council and

Exchange 2014).

4. Safeguard integrity under corporate reporting

The audit committee and the board of the company closely monitor the external

auditor’s independence. Regular reviews are carried out for safeguarding the independence of

internal auditor. Further the company rotates its lead partner for audit in each 5 years and

imposes the restrictions on engagement of the personnel those were previously engaged by

external auditor (Council 2014). The policies of the company are appropriately applied for

putting the restrictions on non-audit services that can be provided by the external auditors.

Further, the detailed analysis of non-audit fees paid to external auditors are carried on half –

yearly basis. In every meeting the audit committee privately meets with the executive

management without including the external auditor and with external and internal auditors

without including the executive management (Du Plessis, Hargovan and Harris 2018).

5. Make timely and balanced disclosures

The company is committed to assure that the trading in the share takes place in

informed and orderly market through availing consistent and transparent communication with

5AUDIT, ASSURANCE AND COMPLIANCE

all the shareholders. The company has an established procedure to assure that it fulfils with

the obligation related to continuous disclosures all the time and includes half yearly

confirmation through all executive management that the sectors for which they are

answerable are complied with continuous disclosure policy of the company (Gitman, Juchau

and Flanagan 2015). Further, the company communicates with its shareholders actively

through ASX and web based newsroom along with all the materials issued by the company

that are made available to the shareholders simultaneously.

6. Respect the rights of the shareholders

The company has a policy for shareholder’s communication that promotes 2 way

efficient communications with the shareholders and wider community for investment and

influences the participant at the general meetings (Klettner, Clarke and Boersma 2014).

External auditor presents at AGM and are available for answering the questions from

shareholders that are appropriate for the audit. The shareholders are also able to receive the

communication and send communication to the company and electronically to the share

registry that includes email notification with regard to significant announcement in the

market (Lama and Anderson 2015).

7. Recognise and manage risk

The company is committed towards implementation of the practices of risk

management for supporting the business objectives achievements and complying with the the

obligations of corporate governance. Further, the board is accountable for overseeing and

reviewing the strategies associated with the management of risk and assuring that the

company has proper structure for corporate governance (Tao and Hutchinson 2013). The

management of the company has implemented and designed an internal control and risk

management system for managing the material risks of the business. Audit committee of the

all the shareholders. The company has an established procedure to assure that it fulfils with

the obligation related to continuous disclosures all the time and includes half yearly

confirmation through all executive management that the sectors for which they are

answerable are complied with continuous disclosure policy of the company (Gitman, Juchau

and Flanagan 2015). Further, the company communicates with its shareholders actively

through ASX and web based newsroom along with all the materials issued by the company

that are made available to the shareholders simultaneously.

6. Respect the rights of the shareholders

The company has a policy for shareholder’s communication that promotes 2 way

efficient communications with the shareholders and wider community for investment and

influences the participant at the general meetings (Klettner, Clarke and Boersma 2014).

External auditor presents at AGM and are available for answering the questions from

shareholders that are appropriate for the audit. The shareholders are also able to receive the

communication and send communication to the company and electronically to the share

registry that includes email notification with regard to significant announcement in the

market (Lama and Anderson 2015).

7. Recognise and manage risk

The company is committed towards implementation of the practices of risk

management for supporting the business objectives achievements and complying with the the

obligations of corporate governance. Further, the board is accountable for overseeing and

reviewing the strategies associated with the management of risk and assuring that the

company has proper structure for corporate governance (Tao and Hutchinson 2013). The

management of the company has implemented and designed an internal control and risk

management system for managing the material risks of the business. Audit committee of the

6AUDIT, ASSURANCE AND COMPLIANCE

company authorises risk internal audit charter and group audit that offers full access to the

company records, functions, personnel, and property and independence requirements.

Further, the audit committee authorises the replacements, appointments and remuneration for

the internal auditor. Internal auditors are supposed to report to the audit committee directly

and it also delivers report with regard to health, safety, security and environment committee.

The functions of internal audit are carried out by the group audit and risk and the group is

independent of external auditor. The group further offers objective assurance, consulting

services and independence with respect to governance, internal control and risk management

of Qantas airways.

8. Remunerate fairly and responsibly

The main objective of the framework for executive remuneration are to motivate,

attract, retain and reward appropriately to the executive team. This objective is attained

through setting the pay opportunity at appropriate level and through linking the remuneration

outcomes with the performance of the company (Tricker and Tricker 2015). While setting up

the remuneration strategy the company keeps the following things in mind –

Motivate, attract, retain and reward appropriately to the executive team

Link the remuneration outcomes with the business performance and executive’s

performance

Motivating executive team for achieving the company’s unique challenges as the

major Australia based international airline

Further, the non-executive directors are eligible to get certain travel concessions and

statutory superannuation that are paid reasonably and as per the standard practice of aviation

industry. However, the on-executive directors are not entitled to any remuneration based on

performance.

company authorises risk internal audit charter and group audit that offers full access to the

company records, functions, personnel, and property and independence requirements.

Further, the audit committee authorises the replacements, appointments and remuneration for

the internal auditor. Internal auditors are supposed to report to the audit committee directly

and it also delivers report with regard to health, safety, security and environment committee.

The functions of internal audit are carried out by the group audit and risk and the group is

independent of external auditor. The group further offers objective assurance, consulting

services and independence with respect to governance, internal control and risk management

of Qantas airways.

8. Remunerate fairly and responsibly

The main objective of the framework for executive remuneration are to motivate,

attract, retain and reward appropriately to the executive team. This objective is attained

through setting the pay opportunity at appropriate level and through linking the remuneration

outcomes with the performance of the company (Tricker and Tricker 2015). While setting up

the remuneration strategy the company keeps the following things in mind –

Motivate, attract, retain and reward appropriately to the executive team

Link the remuneration outcomes with the business performance and executive’s

performance

Motivating executive team for achieving the company’s unique challenges as the

major Australia based international airline

Further, the non-executive directors are eligible to get certain travel concessions and

statutory superannuation that are paid reasonably and as per the standard practice of aviation

industry. However, the on-executive directors are not entitled to any remuneration based on

performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

3. Risk assessment

Nature of the company

Qantas Airways influenced development of global aviation industry from its

establishment in the year 1920. At present the company is globally competitive and strong

aviation company that serves Australia and connects Australians with the world. Most

importantly, the company is full of passionate, diverse and skilled workforce. All of the

employees are responsible towards for realising the potentials of the company. Each of the

Qantas Group is custodian of great Australian entities (Qantas.com 2018).

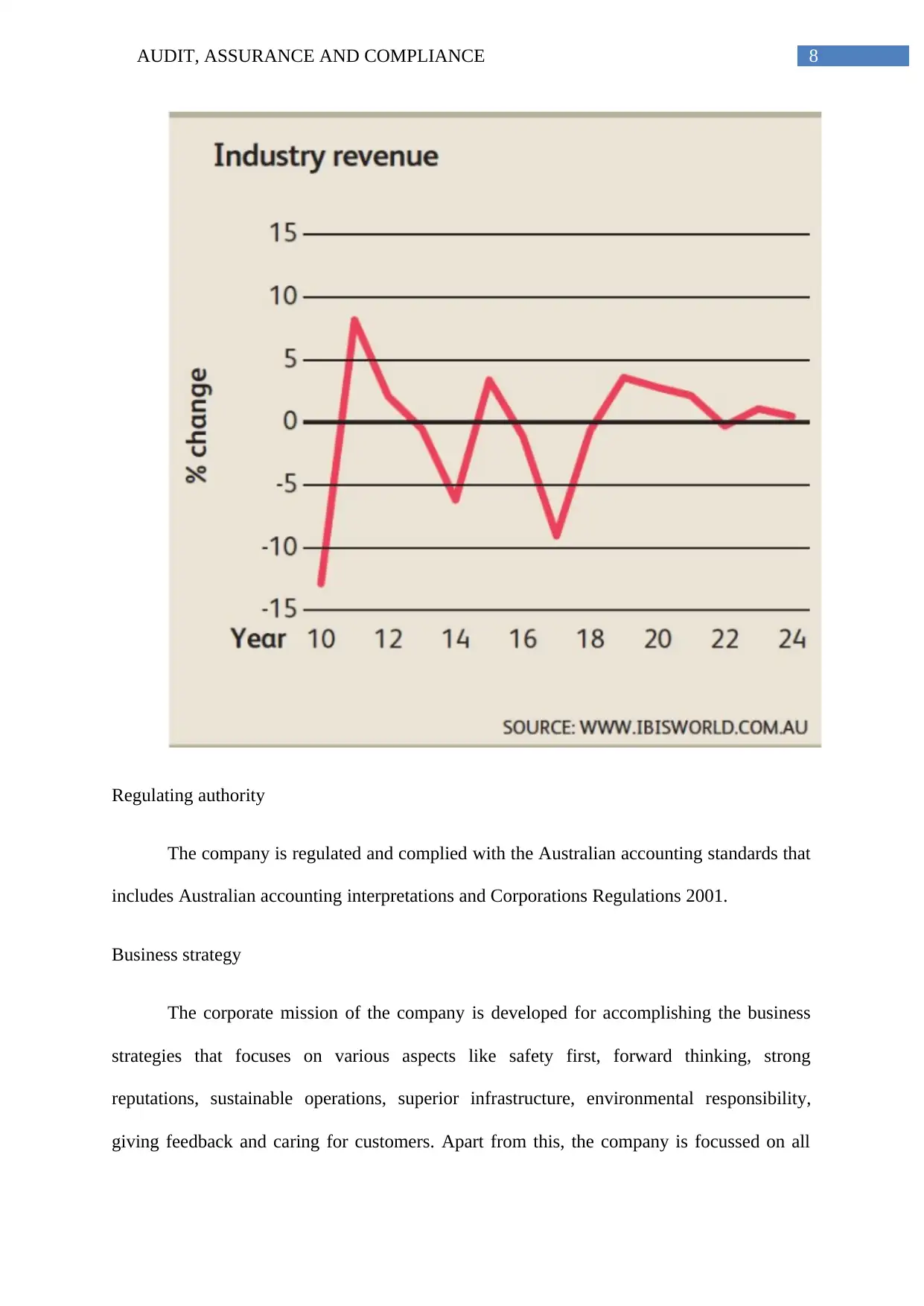

Market overview

The domestic industry for airline in Australia is duopoly with Virgin Australia and

Qantas and their combined market share is 90%. Over the last 5 years, the aviation industry in

Australia experienced steady decline in the revenue and the reason behind that is that Virgin

and Qantas are always involved in price war. Qantas Airways is the 3rd oldest airline

company all over the world after Aviancia and KLM. The company focuses on differentiating

and cost advantages for reaching the competitive advantage. Therefore, the company is

concerned about the competitive advantage that will look for differentiating the advantages

and cost advantages. However the aviation industry in Australia is mature but growing at

slower rates. Through Qantas has exceptional market share and are growing continuously.

Shareholders returns of the company were goods and are expected to continue at the same

rate and the valuations reveals that the shares of the company are not trading at discount

(Qantas.com 2018).

3. Risk assessment

Nature of the company

Qantas Airways influenced development of global aviation industry from its

establishment in the year 1920. At present the company is globally competitive and strong

aviation company that serves Australia and connects Australians with the world. Most

importantly, the company is full of passionate, diverse and skilled workforce. All of the

employees are responsible towards for realising the potentials of the company. Each of the

Qantas Group is custodian of great Australian entities (Qantas.com 2018).

Market overview

The domestic industry for airline in Australia is duopoly with Virgin Australia and

Qantas and their combined market share is 90%. Over the last 5 years, the aviation industry in

Australia experienced steady decline in the revenue and the reason behind that is that Virgin

and Qantas are always involved in price war. Qantas Airways is the 3rd oldest airline

company all over the world after Aviancia and KLM. The company focuses on differentiating

and cost advantages for reaching the competitive advantage. Therefore, the company is

concerned about the competitive advantage that will look for differentiating the advantages

and cost advantages. However the aviation industry in Australia is mature but growing at

slower rates. Through Qantas has exceptional market share and are growing continuously.

Shareholders returns of the company were goods and are expected to continue at the same

rate and the valuations reveals that the shares of the company are not trading at discount

(Qantas.com 2018).

8AUDIT, ASSURANCE AND COMPLIANCE

Regulating authority

The company is regulated and complied with the Australian accounting standards that

includes Australian accounting interpretations and Corporations Regulations 2001.

Business strategy

The corporate mission of the company is developed for accomplishing the business

strategies that focuses on various aspects like safety first, forward thinking, strong

reputations, sustainable operations, superior infrastructure, environmental responsibility,

giving feedback and caring for customers. Apart from this, the company is focussed on all

Regulating authority

The company is regulated and complied with the Australian accounting standards that

includes Australian accounting interpretations and Corporations Regulations 2001.

Business strategy

The corporate mission of the company is developed for accomplishing the business

strategies that focuses on various aspects like safety first, forward thinking, strong

reputations, sustainable operations, superior infrastructure, environmental responsibility,

giving feedback and caring for customers. Apart from this, the company is focussed on all

9AUDIT, ASSURANCE AND COMPLIANCE

kinds of business a strategy like cost leadership and therefore, the company is focussed on

differentiating itself from other airlines (Qantas.com 2018).

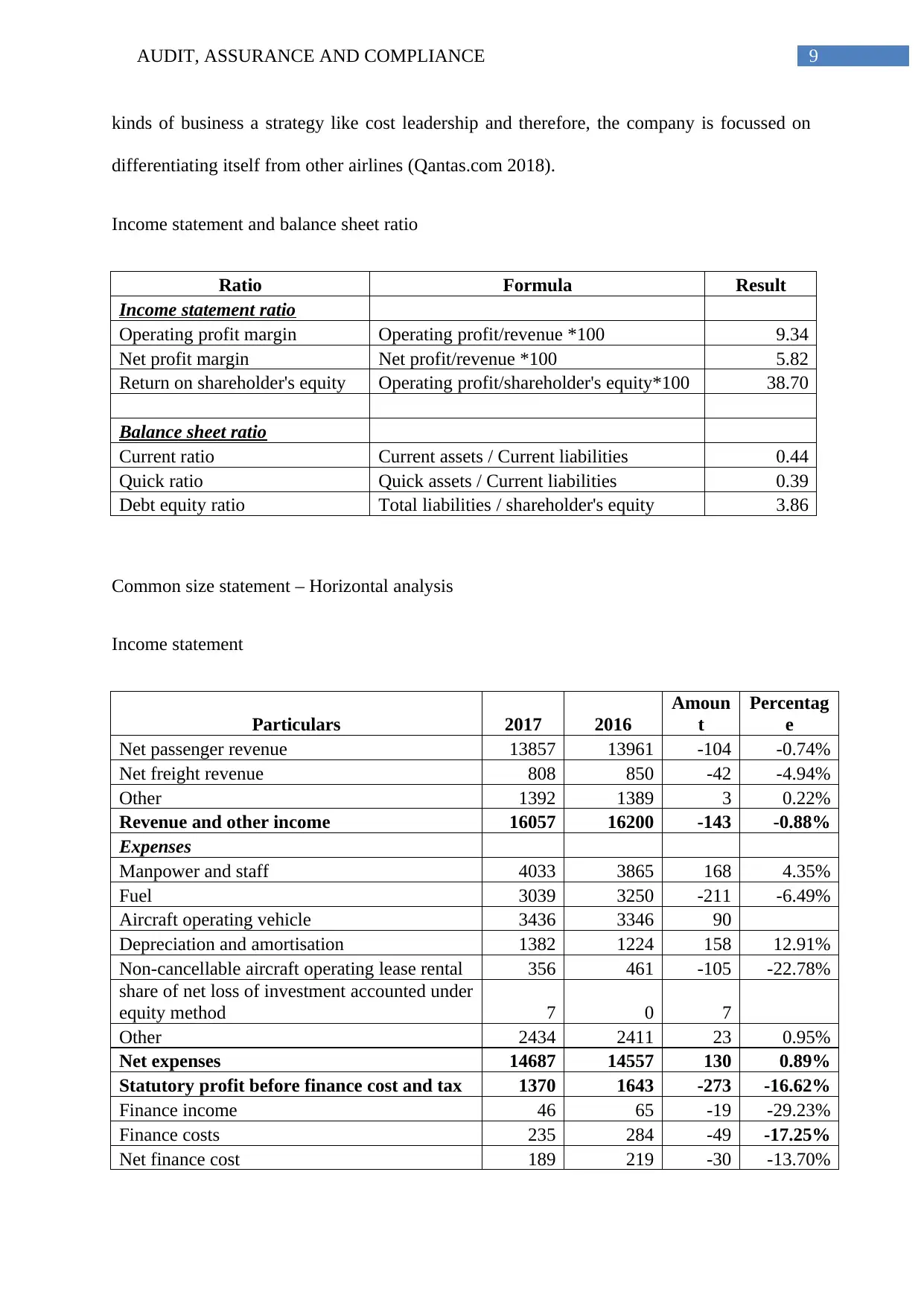

Income statement and balance sheet ratio

Ratio Formula Result

Income statement ratio

Operating profit margin Operating profit/revenue *100 9.34

Net profit margin Net profit/revenue *100 5.82

Return on shareholder's equity Operating profit/shareholder's equity*100 38.70

Balance sheet ratio

Current ratio Current assets / Current liabilities 0.44

Quick ratio Quick assets / Current liabilities 0.39

Debt equity ratio Total liabilities / shareholder's equity 3.86

Common size statement – Horizontal analysis

Income statement

Particulars 2017 2016

Amoun

t

Percentag

e

Net passenger revenue 13857 13961 -104 -0.74%

Net freight revenue 808 850 -42 -4.94%

Other 1392 1389 3 0.22%

Revenue and other income 16057 16200 -143 -0.88%

Expenses

Manpower and staff 4033 3865 168 4.35%

Fuel 3039 3250 -211 -6.49%

Aircraft operating vehicle 3436 3346 90

Depreciation and amortisation 1382 1224 158 12.91%

Non-cancellable aircraft operating lease rental 356 461 -105 -22.78%

share of net loss of investment accounted under

equity method 7 0 7

Other 2434 2411 23 0.95%

Net expenses 14687 14557 130 0.89%

Statutory profit before finance cost and tax 1370 1643 -273 -16.62%

Finance income 46 65 -19 -29.23%

Finance costs 235 284 -49 -17.25%

Net finance cost 189 219 -30 -13.70%

kinds of business a strategy like cost leadership and therefore, the company is focussed on

differentiating itself from other airlines (Qantas.com 2018).

Income statement and balance sheet ratio

Ratio Formula Result

Income statement ratio

Operating profit margin Operating profit/revenue *100 9.34

Net profit margin Net profit/revenue *100 5.82

Return on shareholder's equity Operating profit/shareholder's equity*100 38.70

Balance sheet ratio

Current ratio Current assets / Current liabilities 0.44

Quick ratio Quick assets / Current liabilities 0.39

Debt equity ratio Total liabilities / shareholder's equity 3.86

Common size statement – Horizontal analysis

Income statement

Particulars 2017 2016

Amoun

t

Percentag

e

Net passenger revenue 13857 13961 -104 -0.74%

Net freight revenue 808 850 -42 -4.94%

Other 1392 1389 3 0.22%

Revenue and other income 16057 16200 -143 -0.88%

Expenses

Manpower and staff 4033 3865 168 4.35%

Fuel 3039 3250 -211 -6.49%

Aircraft operating vehicle 3436 3346 90

Depreciation and amortisation 1382 1224 158 12.91%

Non-cancellable aircraft operating lease rental 356 461 -105 -22.78%

share of net loss of investment accounted under

equity method 7 0 7

Other 2434 2411 23 0.95%

Net expenses 14687 14557 130 0.89%

Statutory profit before finance cost and tax 1370 1643 -273 -16.62%

Finance income 46 65 -19 -29.23%

Finance costs 235 284 -49 -17.25%

Net finance cost 189 219 -30 -13.70%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10AUDIT, ASSURANCE AND COMPLIANCE

Statutory profit before and tax 1181 1424 -243 -17.06%

Income tax expenses 328 395 -67 -16.96%

Statutory profit for the year 853 1029 -176 -17.10%

Balance sheet

Assets 2017 2016

Amoun

t

Percentag

e

Current assets

Cash and cash equivalents 1775 1980 -205 -10%

Trade and other receivables 784 795 -11 -1%

Other financial assets 100 229 -129 -56%

Inventories 351 336 15 4%

Assets classified as held for sale 12 17 -5 -29%

Other 97 101 -4 -4%

Total current assets 3119 3458 -339 -10%

Non-current assets

Receivables 123 134 -11 -8%

Other financial assets 43 46 -3 -7%

Investment accounted under equity

method 214 197 17 9%

Property, plant and equipment 12253 11670 583 5%

Intangible assets 1025 909 116

Deferred tax assets 0 39 -39 -100%

Other 444 252 192 76%

Total non-current assets 14102 13247 855 6%

Total assets 17221 16705 516 3%

Liabilities

Current liabilities

Payables 2067 1986 81 4%

Revenue received in advance 3685 3525 160 5%

Interest-bearing liabilities 433 441 -8 -2%

Other financial liabilities 69 203 -134 -66%

Provisions 841 873 -32 -4%

Total current liabilities 7095 7028 67 1%

Non-current liabilities 0

Revenue received in advance 1424 1521 -97 -6%

Interest bearing liabilities 4405 4421 -16 0%

Other financial liabilities 56 61 -5 -8%

Provisions 348 414 -66 -16%

Deferred tax liabilities 353 0 353

Total non-current liabilities 6586 6417 169 3%

Statutory profit before and tax 1181 1424 -243 -17.06%

Income tax expenses 328 395 -67 -16.96%

Statutory profit for the year 853 1029 -176 -17.10%

Balance sheet

Assets 2017 2016

Amoun

t

Percentag

e

Current assets

Cash and cash equivalents 1775 1980 -205 -10%

Trade and other receivables 784 795 -11 -1%

Other financial assets 100 229 -129 -56%

Inventories 351 336 15 4%

Assets classified as held for sale 12 17 -5 -29%

Other 97 101 -4 -4%

Total current assets 3119 3458 -339 -10%

Non-current assets

Receivables 123 134 -11 -8%

Other financial assets 43 46 -3 -7%

Investment accounted under equity

method 214 197 17 9%

Property, plant and equipment 12253 11670 583 5%

Intangible assets 1025 909 116

Deferred tax assets 0 39 -39 -100%

Other 444 252 192 76%

Total non-current assets 14102 13247 855 6%

Total assets 17221 16705 516 3%

Liabilities

Current liabilities

Payables 2067 1986 81 4%

Revenue received in advance 3685 3525 160 5%

Interest-bearing liabilities 433 441 -8 -2%

Other financial liabilities 69 203 -134 -66%

Provisions 841 873 -32 -4%

Total current liabilities 7095 7028 67 1%

Non-current liabilities 0

Revenue received in advance 1424 1521 -97 -6%

Interest bearing liabilities 4405 4421 -16 0%

Other financial liabilities 56 61 -5 -8%

Provisions 348 414 -66 -16%

Deferred tax liabilities 353 0 353

Total non-current liabilities 6586 6417 169 3%

11AUDIT, ASSURANCE AND COMPLIANCE

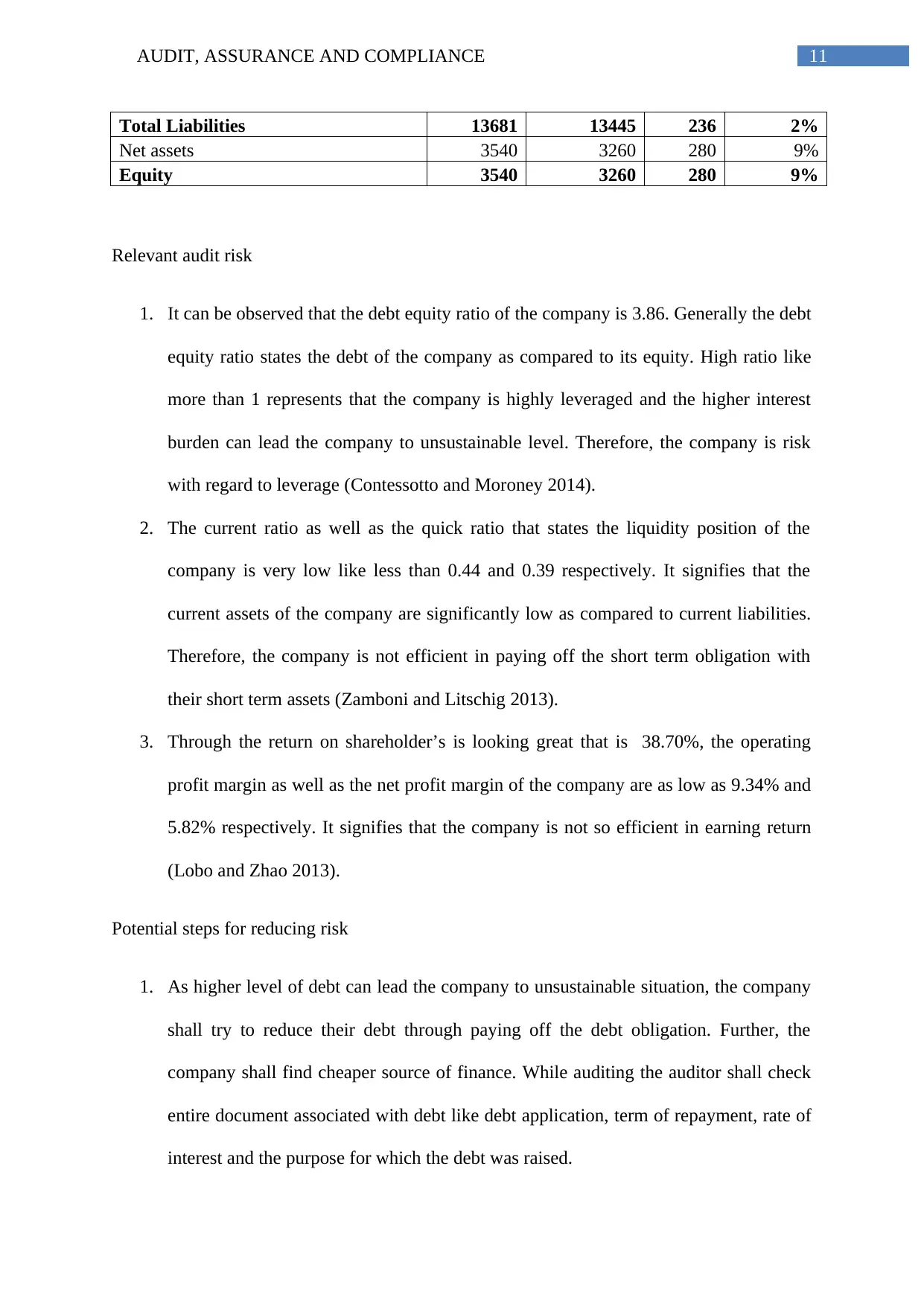

Total Liabilities 13681 13445 236 2%

Net assets 3540 3260 280 9%

Equity 3540 3260 280 9%

Relevant audit risk

1. It can be observed that the debt equity ratio of the company is 3.86. Generally the debt

equity ratio states the debt of the company as compared to its equity. High ratio like

more than 1 represents that the company is highly leveraged and the higher interest

burden can lead the company to unsustainable level. Therefore, the company is risk

with regard to leverage (Contessotto and Moroney 2014).

2. The current ratio as well as the quick ratio that states the liquidity position of the

company is very low like less than 0.44 and 0.39 respectively. It signifies that the

current assets of the company are significantly low as compared to current liabilities.

Therefore, the company is not efficient in paying off the short term obligation with

their short term assets (Zamboni and Litschig 2013).

3. Through the return on shareholder’s is looking great that is 38.70%, the operating

profit margin as well as the net profit margin of the company are as low as 9.34% and

5.82% respectively. It signifies that the company is not so efficient in earning return

(Lobo and Zhao 2013).

Potential steps for reducing risk

1. As higher level of debt can lead the company to unsustainable situation, the company

shall try to reduce their debt through paying off the debt obligation. Further, the

company shall find cheaper source of finance. While auditing the auditor shall check

entire document associated with debt like debt application, term of repayment, rate of

interest and the purpose for which the debt was raised.

Total Liabilities 13681 13445 236 2%

Net assets 3540 3260 280 9%

Equity 3540 3260 280 9%

Relevant audit risk

1. It can be observed that the debt equity ratio of the company is 3.86. Generally the debt

equity ratio states the debt of the company as compared to its equity. High ratio like

more than 1 represents that the company is highly leveraged and the higher interest

burden can lead the company to unsustainable level. Therefore, the company is risk

with regard to leverage (Contessotto and Moroney 2014).

2. The current ratio as well as the quick ratio that states the liquidity position of the

company is very low like less than 0.44 and 0.39 respectively. It signifies that the

current assets of the company are significantly low as compared to current liabilities.

Therefore, the company is not efficient in paying off the short term obligation with

their short term assets (Zamboni and Litschig 2013).

3. Through the return on shareholder’s is looking great that is 38.70%, the operating

profit margin as well as the net profit margin of the company are as low as 9.34% and

5.82% respectively. It signifies that the company is not so efficient in earning return

(Lobo and Zhao 2013).

Potential steps for reducing risk

1. As higher level of debt can lead the company to unsustainable situation, the company

shall try to reduce their debt through paying off the debt obligation. Further, the

company shall find cheaper source of finance. While auditing the auditor shall check

entire document associated with debt like debt application, term of repayment, rate of

interest and the purpose for which the debt was raised.

12AUDIT, ASSURANCE AND COMPLIANCE

2. To check the current ratio status of the company the short term assets like cash,

receivables shall be verified. As the current assets of the company is lower as

compared to the current liabilities. Therefore, the auditor shall check the cash register

and reconcile it with the bank statement. Further, the receivables shall be verified with

regard to all the details like days allowed for payment, chances of bad debts and

amount of receivables along with the name of debtors to check that all the details are

stated correctly.

3. To increase the profits it shall try to minimize the expenses wherever possible and

shall be verified all the vouchers related to expenses and payments to ensure that all

the details are correct.

2. To check the current ratio status of the company the short term assets like cash,

receivables shall be verified. As the current assets of the company is lower as

compared to the current liabilities. Therefore, the auditor shall check the cash register

and reconcile it with the bank statement. Further, the receivables shall be verified with

regard to all the details like days allowed for payment, chances of bad debts and

amount of receivables along with the name of debtors to check that all the details are

stated correctly.

3. To increase the profits it shall try to minimize the expenses wherever possible and

shall be verified all the vouchers related to expenses and payments to ensure that all

the details are correct.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13AUDIT, ASSURANCE AND COMPLIANCE

Reference

Bottomley, S., 2016. The constitutional corporation: Rethinking corporate governance.

Routledge.

Chan, M.C., Watson, J. and Woodliff, D., 2014. Corporate governance quality and CSR

disclosures. Journal of Business Ethics, 125(1), pp.59-73.

Christensen, J., Kent, P., Routledge, J. and Stewart, J., 2015. Do corporate governance

recommendations improve the performance and accountability of small listed

companies?. Accounting & Finance, 55(1), pp.133-164.

Contessotto, C. and Moroney, R., 2014. The association between audit committee

effectiveness and audit risk. Accounting & Finance, 54(2), pp.393-418.

Council, A.C.G. and Exchange, A.S., 2014. Corporate governance principles and

recommendations . ASX Corporate Governance Council.

Council, A.C.G., 2014. Corporate Governance Principles and Recommendations, 3rd edn

(ASX, Sydney).

Du Plessis, J.J., Hargovan, A. and Harris, J., 2018. Principles of contemporary corporate

governance. Cambridge University Press.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Jbhifi.com.au. (2018). JB Hi-Fi | JB Hi-Fi - Australia's Largest Home Entertainment Retailer.

[online] Available at: https://www.jbhifi.com.au/ [Accessed 20 Apr. 2018].

Reference

Bottomley, S., 2016. The constitutional corporation: Rethinking corporate governance.

Routledge.

Chan, M.C., Watson, J. and Woodliff, D., 2014. Corporate governance quality and CSR

disclosures. Journal of Business Ethics, 125(1), pp.59-73.

Christensen, J., Kent, P., Routledge, J. and Stewart, J., 2015. Do corporate governance

recommendations improve the performance and accountability of small listed

companies?. Accounting & Finance, 55(1), pp.133-164.

Contessotto, C. and Moroney, R., 2014. The association between audit committee

effectiveness and audit risk. Accounting & Finance, 54(2), pp.393-418.

Council, A.C.G. and Exchange, A.S., 2014. Corporate governance principles and

recommendations . ASX Corporate Governance Council.

Council, A.C.G., 2014. Corporate Governance Principles and Recommendations, 3rd edn

(ASX, Sydney).

Du Plessis, J.J., Hargovan, A. and Harris, J., 2018. Principles of contemporary corporate

governance. Cambridge University Press.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Jbhifi.com.au. (2018). JB Hi-Fi | JB Hi-Fi - Australia's Largest Home Entertainment Retailer.

[online] Available at: https://www.jbhifi.com.au/ [Accessed 20 Apr. 2018].

14AUDIT, ASSURANCE AND COMPLIANCE

Klettner, A., Clarke, T. and Boersma, M., 2014. The governance of corporate sustainability:

Empirical insights into the development, leadership and implementation of responsible

business strategy. Journal of Business Ethics, 122(1), pp.145-165.

Lama, T. and Anderson, W.W., 2015. Company characteristics and compliance with ASX

corporate governance principles. Pacific Accounting Review, 27(3), pp.373-392.

Lobo, G.J. and Zhao, Y., 2013. Relation between audit effort and financial report

misstatements: Evidence from quarterly and annual restatements. The Accounting

Review, 88(4), pp.1385-1412.

Qantas.com., 2018. Fly with one of the world’s most experienced airlines | Qantas IN.

[online] Available at: https://www.qantas.com/in/en.html [Accessed 24 Apr. 2018].

Tao, N.B. and Hutchinson, M., 2013. Corporate governance and risk management: The role

of risk management and compensation committees. Journal of Contemporary Accounting &

Economics, 9(1), pp.83-99.

Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies, and

practices. Oxford University Press, USA.

Zamboni, Y. and Litschig, S., 2013. Audit risk and rent extraction: Evidence from a

randomized evaluation in Brazil. Universitat Pompeu Fabra, 1.

Klettner, A., Clarke, T. and Boersma, M., 2014. The governance of corporate sustainability:

Empirical insights into the development, leadership and implementation of responsible

business strategy. Journal of Business Ethics, 122(1), pp.145-165.

Lama, T. and Anderson, W.W., 2015. Company characteristics and compliance with ASX

corporate governance principles. Pacific Accounting Review, 27(3), pp.373-392.

Lobo, G.J. and Zhao, Y., 2013. Relation between audit effort and financial report

misstatements: Evidence from quarterly and annual restatements. The Accounting

Review, 88(4), pp.1385-1412.

Qantas.com., 2018. Fly with one of the world’s most experienced airlines | Qantas IN.

[online] Available at: https://www.qantas.com/in/en.html [Accessed 24 Apr. 2018].

Tao, N.B. and Hutchinson, M., 2013. Corporate governance and risk management: The role

of risk management and compensation committees. Journal of Contemporary Accounting &

Economics, 9(1), pp.83-99.

Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies, and

practices. Oxford University Press, USA.

Zamboni, Y. and Litschig, S., 2013. Audit risk and rent extraction: Evidence from a

randomized evaluation in Brazil. Universitat Pompeu Fabra, 1.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.