H16026: Audit, Assurance And Compliance

VerifiedAdded on 2023/06/05

|18

|3996

|359

AI Summary

The report is intended to adhere key role and responsibilities of auditors by analyzing auditing and assurance service of financial report of CSR Limited. Evaluation has also been made regarding control of its internal environment.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running ead A D ASS RA C A D C M A CH : H16026: U IT, U N E N O PLI N E

Audit Assurance And ComplianceH16026: ,

ame of the StudentN

ame of the niversityN U

Author note

Course DI

Audit Assurance And ComplianceH16026: ,

ame of the StudentN

ame of the niversityN U

Author note

Course DI

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

Executive Summary

he report is intended to adhere key role and resonsibilities of auditors by anayzing auditiinbg andT

assurance servuce of fi anncial report of CSR imited valuation has also been made regardingL . E

control of its internal environment rom the annual report of specific section related to. F 2018 ,

auditing has been picked up for the analysis he comcerned report covers different auditig asoects. T

of CSR imited he independent aspect of the company s auditor Delittre has been e amined inL . T ’ , x

line with the auditing standard of Australia he report identifies key matters of auditing relevant for. T

the organization with respect to the operation of business he report has found that there is a. T

consideranle fall in remauration given to the auditors in the year compared to the last year2018 .

he report thus is useful to provude useful insights to assess the the standard of latest auditingT

report for CSR imitedL .

Executive Summary

he report is intended to adhere key role and resonsibilities of auditors by anayzing auditiinbg andT

assurance servuce of fi anncial report of CSR imited valuation has also been made regardingL . E

control of its internal environment rom the annual report of specific section related to. F 2018 ,

auditing has been picked up for the analysis he comcerned report covers different auditig asoects. T

of CSR imited he independent aspect of the company s auditor Delittre has been e amined inL . T ’ , x

line with the auditing standard of Australia he report identifies key matters of auditing relevant for. T

the organization with respect to the operation of business he report has found that there is a. T

consideranle fall in remauration given to the auditors in the year compared to the last year2018 .

he report thus is useful to provude useful insights to assess the the standard of latest auditingT

report for CSR imitedL .

2A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

Table of Contents

ntrodutionI .........................................................................................................................................3

Compliance with auditor’s independent requirement....................................................................3

Services that are non auditable- .......................................................................................................4

valuation of remuneration of auditorsE ..............................................................................................5

Aspects related to key auditing matters..............................................................................................6

Auditing committee..............................................................................................................................8

pinion to AuditO ..............................................................................................................................8

Variances in the responsibilities between management and directors and auditors.......................9

Subsequent material event...........................................................................................................10

valuation of effective material informationE .........................................................................................11

Material information that are either missing not fully disclosed or e plained and or under, x /

reported.........................................................................................................................................11

uestions for follow upQ - ...................................................................................................................11

Conclusion......................................................................................................................................12

ist of ReferencesL ...........................................................................................................................14

Table of Contents

ntrodutionI .........................................................................................................................................3

Compliance with auditor’s independent requirement....................................................................3

Services that are non auditable- .......................................................................................................4

valuation of remuneration of auditorsE ..............................................................................................5

Aspects related to key auditing matters..............................................................................................6

Auditing committee..............................................................................................................................8

pinion to AuditO ..............................................................................................................................8

Variances in the responsibilities between management and directors and auditors.......................9

Subsequent material event...........................................................................................................10

valuation of effective material informationE .........................................................................................11

Material information that are either missing not fully disclosed or e plained and or under, x /

reported.........................................................................................................................................11

uestions for follow upQ - ...................................................................................................................11

Conclusion......................................................................................................................................12

ist of ReferencesL ...........................................................................................................................14

3A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

Introdution

Auditing refers to a fi nancial process where investigation is conducted in an organization s’

statement corresponding to fi nancial facts with an objective of ensuring fair treatment along with

maintaining accuracy in all the claimed fi nancial transaction he fairness can only be ensured by. T

revealing all the important fi nancial information that corresponds to a company s fi nancial’

statement Auditor is the person who has the responsibility to improvise quality of an audit.

report he stakeholders related the business directly or indirectly need to reveal the relevant. T

fi

nancial information with transparency or maintain a good quality in the audit report several. F

initiatives are currently undertaken by the responsible auditing committees ( ayH 2015) he report. T

concerns with auditing report of one of the established manufacturing organization of Australia,

namely CSR imited he present report would scrutinize aspects related to the auditing of CSRL . T

limited by evaluating annual report of the concerned organization or the fi nancial year of. F 2018,

auditing partner of CSR is Deloitte.

Compliance with auditor’s independent requirement

he published annual report of CSR imited for the year revealed that there wereT L 2018 ,

no actively involved member of Deloitte in operation of business of CSR either there were any. N

evidences regarding significant role of Deloitte members the organized audit group in the current

year he declaration was made under the act named. T “ ection of the Corporations ctS 342A A 2001”.

Requirement in accordance to “ ection C of the Corporations ctS 307 A 2001 has been fully”

complied by Deloitte iven below are some specific points covered under the act. G

Introdution

Auditing refers to a fi nancial process where investigation is conducted in an organization s’

statement corresponding to fi nancial facts with an objective of ensuring fair treatment along with

maintaining accuracy in all the claimed fi nancial transaction he fairness can only be ensured by. T

revealing all the important fi nancial information that corresponds to a company s fi nancial’

statement Auditor is the person who has the responsibility to improvise quality of an audit.

report he stakeholders related the business directly or indirectly need to reveal the relevant. T

fi

nancial information with transparency or maintain a good quality in the audit report several. F

initiatives are currently undertaken by the responsible auditing committees ( ayH 2015) he report. T

concerns with auditing report of one of the established manufacturing organization of Australia,

namely CSR imited he present report would scrutinize aspects related to the auditing of CSRL . T

limited by evaluating annual report of the concerned organization or the fi nancial year of. F 2018,

auditing partner of CSR is Deloitte.

Compliance with auditor’s independent requirement

he published annual report of CSR imited for the year revealed that there wereT L 2018 ,

no actively involved member of Deloitte in operation of business of CSR either there were any. N

evidences regarding significant role of Deloitte members the organized audit group in the current

year he declaration was made under the act named. T “ ection of the Corporations ctS 342A A 2001”.

Requirement in accordance to “ ection C of the Corporations ctS 307 A 2001 has been fully”

complied by Deloitte iven below are some specific points covered under the act. G

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

he act specified that all the possible codes of conducts those are applicable needs to beT

conducted under in reference to the operation of the company

here should not be any breaches related to auditor s independent prerequisites inT ’

relation to company s audit’ (Mubako and DonnellO' 2018).

Services that are non-auditable

As followed from the annual report of the company in the accounting year of two2018,

kinds of non auditing services have been provided by Deloitte ne is assurance related to- . O

sustainability and carbon disclosure he other one is related to advisory and other assurance. T

services or the former the organization has paid while for the latter service an amount. F , $77,108

of has been provided to Deloitte by CSR imited he amount paid for non audit services$9000 L . T -

constitute percent of the total remuneration to the auditor n the transaction of non auditing10.40 . I -

services both the auditor and the company has complied to all the requirement to maintain

transparency.

he Risk and Audit committee has advised that directors of the company are satisfied by theT

non audit service of Deloitte his is due to the fact that auditors group of Deloitte followed all the- . T ;

independent standard as set the by the Corporation Act of for all the auditors n addition2001 . I ,

these services have not adhered to the independent auditor s requirement as stated in the’

above mentioned standard in reference to the material amounts nature of used services and the,

development process of monitoring independent auditors ( ay nechel and illekensH , K W 2014) t. I

is further assured by the directors of the organization the assessment of non audit service would0

not include review of the independent works of the auditors who are engaged in taking

he act specified that all the possible codes of conducts those are applicable needs to beT

conducted under in reference to the operation of the company

here should not be any breaches related to auditor s independent prerequisites inT ’

relation to company s audit’ (Mubako and DonnellO' 2018).

Services that are non-auditable

As followed from the annual report of the company in the accounting year of two2018,

kinds of non auditing services have been provided by Deloitte ne is assurance related to- . O

sustainability and carbon disclosure he other one is related to advisory and other assurance. T

services or the former the organization has paid while for the latter service an amount. F , $77,108

of has been provided to Deloitte by CSR imited he amount paid for non audit services$9000 L . T -

constitute percent of the total remuneration to the auditor n the transaction of non auditing10.40 . I -

services both the auditor and the company has complied to all the requirement to maintain

transparency.

he Risk and Audit committee has advised that directors of the company are satisfied by theT

non audit service of Deloitte his is due to the fact that auditors group of Deloitte followed all the- . T ;

independent standard as set the by the Corporation Act of for all the auditors n addition2001 . I ,

these services have not adhered to the independent auditor s requirement as stated in the’

above mentioned standard in reference to the material amounts nature of used services and the,

development process of monitoring independent auditors ( ay nechel and illekensH , K W 2014) t. I

is further assured by the directors of the organization the assessment of non audit service would0

not include review of the independent works of the auditors who are engaged in taking

5A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

decision related to management he non audit services of CSR imited have complied. T - L

regulations as followed by the standard of corporate governance All these point to questioning.

the auditor s independence in the CSR imited’ L .

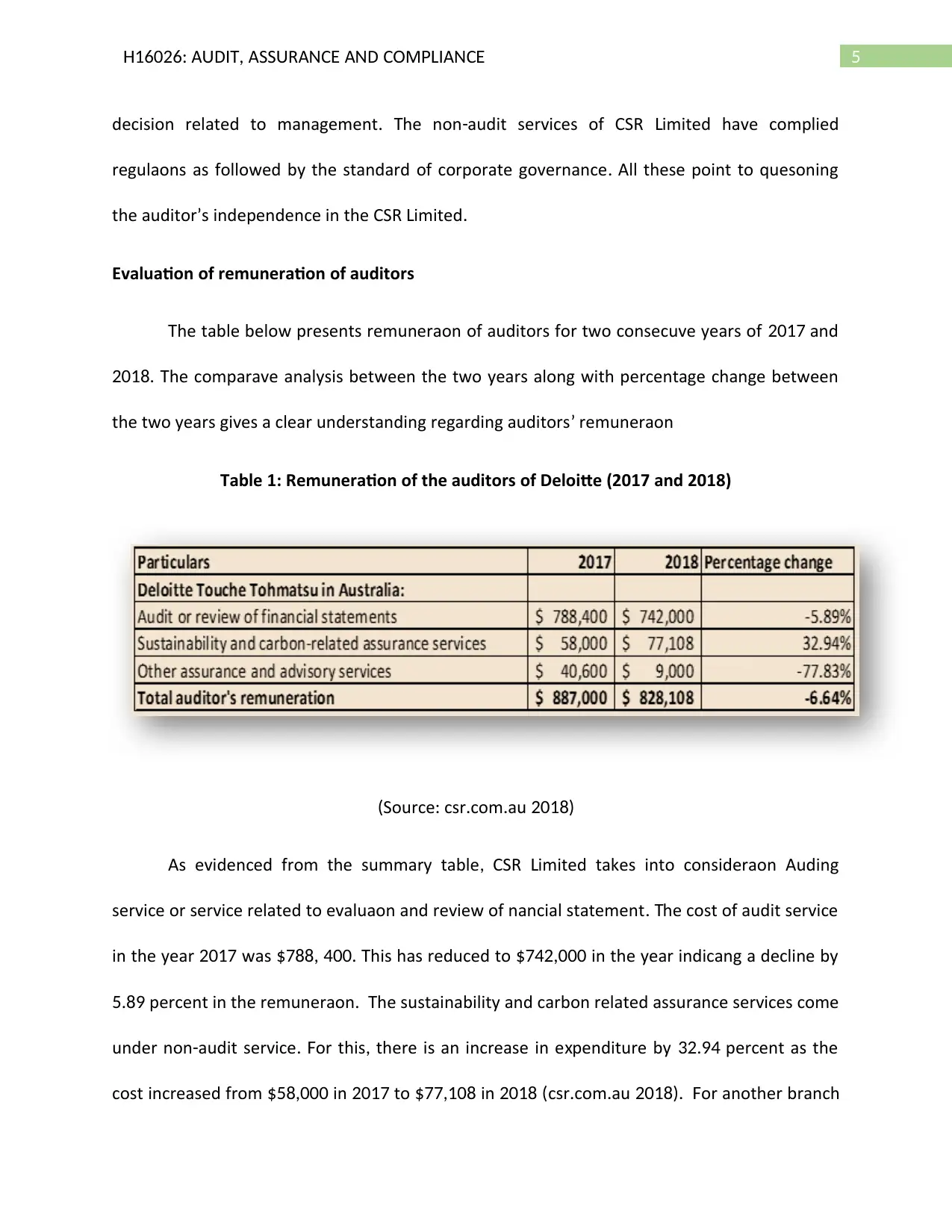

Evaluation of remuneration of auditors

he table below presents remuneration of auditors for two consecutive years of andT 2017

he comparative analysis between the two years along with percentage change between2018. T

the two years gives a clear understanding regarding auditors remuneration’

Table 1: Remuneration of the auditors of Deloitte (2017 and 2018)

Source( : csr com au. . 2018)

As evidenced from the summary table CSR imited takes into consideration Auditing, L

service or service related to evaluation and review of fi nancial statement he cost of audit service. T

in the year was his has reduced to in the year indicating a decline by2017 $788, 400. T $742,000

percent in the remuneration he sustainability and carbon related assurance services come5.89 . T

under non audit service or this there is an increase in e penditure by percent as the- . F , x 32.94

cost increased from in to in$58,000 2017 $77,108 2018 (csr com au. . 2018) or another branch. F

decision related to management he non audit services of CSR imited have complied. T - L

regulations as followed by the standard of corporate governance All these point to questioning.

the auditor s independence in the CSR imited’ L .

Evaluation of remuneration of auditors

he table below presents remuneration of auditors for two consecutive years of andT 2017

he comparative analysis between the two years along with percentage change between2018. T

the two years gives a clear understanding regarding auditors remuneration’

Table 1: Remuneration of the auditors of Deloitte (2017 and 2018)

Source( : csr com au. . 2018)

As evidenced from the summary table CSR imited takes into consideration Auditing, L

service or service related to evaluation and review of fi nancial statement he cost of audit service. T

in the year was his has reduced to in the year indicating a decline by2017 $788, 400. T $742,000

percent in the remuneration he sustainability and carbon related assurance services come5.89 . T

under non audit service or this there is an increase in e penditure by percent as the- . F , x 32.94

cost increased from in to in$58,000 2017 $77,108 2018 (csr com au. . 2018) or another branch. F

6A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

of non audit service containing advisory and other assurance services cist has significantly-

lowered by percent from to n general there is a percent decline77.83 ( $40,600 $9,000). I , 6.64

in auditors remuneration between and’ 2017 2018.

Aspects related to key auditing matters

ne significant aspect of auditing fi nancial statement of an organization is carefulO

consideration of the key matters related to auditing ( ong and MillingtonW 2014) Sourced from.

CSR s annual report two auditing matters have been found namely’ , –

provision of product liability

and

valuation of assets iven below are the detailed procedures of the two key matters. G .

Provision of Product Liability

As accounted on 31st March CSR imited recognized million worth for its, 2018 L $289

liability provision he liability provision of CSR imited is connected to revealed and future. T L

foreseen claims he management hired e perts from SA and Australia to take certain. T x U

decision in this matter he liability provision is subject to the assessment for settlement of. T

amounts and the probable claims to be made in the future ( radbury Raftery and ScottB , 2018) n. I

estimation of the provision rate of discount and movement of relative price of currencies play a

significant role he assumptions however are likely to be comple and differs in size aking into. T x . T

consideration this provision of product liability is taken as one form of key audit matter, .

he issues have been dealt with e perts of Deloitte in association with e pertise of e ternalT x x x

auditors he report is prepared with appropriate assumption and suitable methodology A. T .

number of parameters needs to be considered here hese include appropriateness of chosen. T

methodology used in computing liability provision setting benchmark for the discount rate and,

of non audit service containing advisory and other assurance services cist has significantly-

lowered by percent from to n general there is a percent decline77.83 ( $40,600 $9,000). I , 6.64

in auditors remuneration between and’ 2017 2018.

Aspects related to key auditing matters

ne significant aspect of auditing fi nancial statement of an organization is carefulO

consideration of the key matters related to auditing ( ong and MillingtonW 2014) Sourced from.

CSR s annual report two auditing matters have been found namely’ , –

provision of product liability

and

valuation of assets iven below are the detailed procedures of the two key matters. G .

Provision of Product Liability

As accounted on 31st March CSR imited recognized million worth for its, 2018 L $289

liability provision he liability provision of CSR imited is connected to revealed and future. T L

foreseen claims he management hired e perts from SA and Australia to take certain. T x U

decision in this matter he liability provision is subject to the assessment for settlement of. T

amounts and the probable claims to be made in the future ( radbury Raftery and ScottB , 2018) n. I

estimation of the provision rate of discount and movement of relative price of currencies play a

significant role he assumptions however are likely to be comple and differs in size aking into. T x . T

consideration this provision of product liability is taken as one form of key audit matter, .

he issues have been dealt with e perts of Deloitte in association with e pertise of e ternalT x x x

auditors he report is prepared with appropriate assumption and suitable methodology A. T .

number of parameters needs to be considered here hese include appropriateness of chosen. T

methodology used in computing liability provision setting benchmark for the discount rate and,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

most importantly contrasting the historical claims to that of the projection of future one n this. I

regard a sample test has been conducted by Deloitte to include correct assumption and e clude, x

claims that are connected to asbestos in the management s liability database n the audit’ . I

proceeding this plays a considerable role because liability provision builds the basis of audit

report ( ay Stewart and otica RedmayneH , B 2017) he auditor further discusses with appointed. T

e ternal e perts and other legal counsel related to the organization Deloitte has evaluatedx x .

appropriateness of the disclosure that are pertinent to the fi nancial reports of the company .

Valuation of assets

rom the annual report of CSR of goodwill of the organization valued millionF 2018, $98.1 .

cept goodwill other intangible assets valued million roperty plants and equipmentEx , $45.8 . P ,

including several cash generating units together valued million he impairment evaluation$834 . T

of the concerned assets balance involves crucial judgement n this regard the significant. I ,

assumptions include assumption of rate of inflation rate of growth change in building cycles and, ,

discount tasks and estimated cash fl ow for future ( umphrey oft and Samsonova addeiH , L -T 2014).

oard of management of the company developed an impairment assessment trigger in order toB

identify units those are generating cash to be accounted to assessing future impairment t has. I

been observed that impairment evaluation is further needed for Viridian unit t is regarded as. I

one key audit matter since value judgement is related to future cash fl ow estimation and choice of

other relevant assumption.

o handle the key auditing matter Deloitte has critically evaluated management procedure ofT ,

CSR imited for determining cash generating units that are further needed for assessingL

most importantly contrasting the historical claims to that of the projection of future one n this. I

regard a sample test has been conducted by Deloitte to include correct assumption and e clude, x

claims that are connected to asbestos in the management s liability database n the audit’ . I

proceeding this plays a considerable role because liability provision builds the basis of audit

report ( ay Stewart and otica RedmayneH , B 2017) he auditor further discusses with appointed. T

e ternal e perts and other legal counsel related to the organization Deloitte has evaluatedx x .

appropriateness of the disclosure that are pertinent to the fi nancial reports of the company .

Valuation of assets

rom the annual report of CSR of goodwill of the organization valued millionF 2018, $98.1 .

cept goodwill other intangible assets valued million roperty plants and equipmentEx , $45.8 . P ,

including several cash generating units together valued million he impairment evaluation$834 . T

of the concerned assets balance involves crucial judgement n this regard the significant. I ,

assumptions include assumption of rate of inflation rate of growth change in building cycles and, ,

discount tasks and estimated cash fl ow for future ( umphrey oft and Samsonova addeiH , L -T 2014).

oard of management of the company developed an impairment assessment trigger in order toB

identify units those are generating cash to be accounted to assessing future impairment t has. I

been observed that impairment evaluation is further needed for Viridian unit t is regarded as. I

one key audit matter since value judgement is related to future cash fl ow estimation and choice of

other relevant assumption.

o handle the key auditing matter Deloitte has critically evaluated management procedure ofT ,

CSR imited for determining cash generating units that are further needed for assessingL

8A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

impairment n the procedure of impairment testing the auditor has a critical insight on aspects. I ,

like annual fi nancial performance reporting of consistency distribution of goodwill among the cash, ,

generating assets and e ternal market scenariox (Tricker and Tricker 2015) he auditor in addition. T

has considered other relevant factors to initiate test methodology for developing model of

impairment and associated assumptions he mathematical accuracy has been checked by. T

conducting sample testing.

Auditing committee

n accordance to the annual report the Risk and Audit Committee of the CSR imited hasI , L

been established by the board of directors of the company he concerned committee has the. T

responsibility to assess procedures and policies as connected to internal control for protection of

assets and liabilities of the business aiming to ensure an integrity to the fi nancial reporting of the

company (Du lessis argovan and arrisP , H H 2018) n the Risk and Audit Committee of CSR there. I ,

are four non e ecutive directors hey are- x . T ohn illam enny inn Matthew uinn and MikeJ G , P W , Q

hlein he committee analyses auditing procedure to maintain integrity in the reporting of fi nancialI . T

statement assesses influential dynamics in order to estimate commercial income and also reviews,

the structure of managing audit risk here are however no evidences in company s annual. T ’

report about charter of the audit committee of CSR imitedL .

Opinion to Audit

ollowing the independent report of auditor of CSR it is opined that remuneration reportF ,

of the company is prepared with adherence to the standard act of “ ection of theS 300A

Corporations ctA 2001 Additionally principles as stated in”. , “ ustralian ccounting tandardsA A S

impairment n the procedure of impairment testing the auditor has a critical insight on aspects. I ,

like annual fi nancial performance reporting of consistency distribution of goodwill among the cash, ,

generating assets and e ternal market scenariox (Tricker and Tricker 2015) he auditor in addition. T

has considered other relevant factors to initiate test methodology for developing model of

impairment and associated assumptions he mathematical accuracy has been checked by. T

conducting sample testing.

Auditing committee

n accordance to the annual report the Risk and Audit Committee of the CSR imited hasI , L

been established by the board of directors of the company he concerned committee has the. T

responsibility to assess procedures and policies as connected to internal control for protection of

assets and liabilities of the business aiming to ensure an integrity to the fi nancial reporting of the

company (Du lessis argovan and arrisP , H H 2018) n the Risk and Audit Committee of CSR there. I ,

are four non e ecutive directors hey are- x . T ohn illam enny inn Matthew uinn and MikeJ G , P W , Q

hlein he committee analyses auditing procedure to maintain integrity in the reporting of fi nancialI . T

statement assesses influential dynamics in order to estimate commercial income and also reviews,

the structure of managing audit risk here are however no evidences in company s annual. T ’

report about charter of the audit committee of CSR imitedL .

Opinion to Audit

ollowing the independent report of auditor of CSR it is opined that remuneration reportF ,

of the company is prepared with adherence to the standard act of “ ection of theS 300A

Corporations ctA 2001 Additionally principles as stated in”. , “ ustralian ccounting tandardsA A S

9A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

oardB (AASB)”, “ nternational ccounting tandards oardI A S B (IASB)” and nternational inancialI F

eporting tandardsR S (IFRS) are followed in the development and presentation of the different”

fi

nancial reports (Choi et al. 2018) t is further confirmed by the auditor that there is no material. I

mismatch in CSR s reporting of fi nancial statement he auditing report od CSR imited thus’ . T L

represents true health of the company in the fi nancial market t can therefore be said that an. I

unqualified audit opinion has been e pressed by Deloitte after audit of the organization s fi nancialx ’

report he auditing group has prepared pertinent note regarding accounting system of the. T

company ( sipouridou and SpathisT 2014) Considerable support has been gathered through.

appropriate fi eldwork and conducting suitable test to e amine effectiveness of the proceduresx .

Variances in the responsibilities between management and directors and auditors

he assigned responsibilities to the company directors members of management andT ,

auditor differ significantly as evidenced from the recent annual report of the organization here. T

responsibilities differ in terms of development and presentation of company s report of fi nancial’

report t is the responsibility of management and director to prepare company s fi nancial report. I ’

by following the accounting standard and regulation as stated in the Australian accounting standard

( ibby Rennekamp and SeybertL , 2015) esides capability of the organization is also reviewed by. B

the directors depending on the current accounting basis n general auditors have a different set. I ,

of responsibilities compared to that of the directors hile the directors look after the preparation. W

of fi nancial statement auditors ensure that there is no misstatement either resulting from an,

error or fraudulence of any other issues iven below the are list of responsibilities as performed. G

by auditors of Deloitte

oardB (AASB)”, “ nternational ccounting tandards oardI A S B (IASB)” and nternational inancialI F

eporting tandardsR S (IFRS) are followed in the development and presentation of the different”

fi

nancial reports (Choi et al. 2018) t is further confirmed by the auditor that there is no material. I

mismatch in CSR s reporting of fi nancial statement he auditing report od CSR imited thus’ . T L

represents true health of the company in the fi nancial market t can therefore be said that an. I

unqualified audit opinion has been e pressed by Deloitte after audit of the organization s fi nancialx ’

report he auditing group has prepared pertinent note regarding accounting system of the. T

company ( sipouridou and SpathisT 2014) Considerable support has been gathered through.

appropriate fi eldwork and conducting suitable test to e amine effectiveness of the proceduresx .

Variances in the responsibilities between management and directors and auditors

he assigned responsibilities to the company directors members of management andT ,

auditor differ significantly as evidenced from the recent annual report of the organization here. T

responsibilities differ in terms of development and presentation of company s report of fi nancial’

report t is the responsibility of management and director to prepare company s fi nancial report. I ’

by following the accounting standard and regulation as stated in the Australian accounting standard

( ibby Rennekamp and SeybertL , 2015) esides capability of the organization is also reviewed by. B

the directors depending on the current accounting basis n general auditors have a different set. I ,

of responsibilities compared to that of the directors hile the directors look after the preparation. W

of fi nancial statement auditors ensure that there is no misstatement either resulting from an,

error or fraudulence of any other issues iven below the are list of responsibilities as performed. G

by auditors of Deloitte

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

Auditors identify and evaluate risks generated from the misstatement in material

reporting.

hey e amine the suitable applications of policies related to accounting standardT x .

he auditors assesse formulation and presentation of the company s fi nancial statementT ’ .

Auditors e amine the suitability of the basic accounted standard as adapted by thex

directors ( isenbergE 2017).

t is responsibility of the auditors to clearly understand internal control of theI

organization.

n addition auditors collect sufficient evidences of auditI , .

Subsequent material event

he current annual report of the chose organization has mentioned two subsequentT

material events f the two one is the selling of land that are surplus to the company at orsley. O H

ark t is on theP . I 3rd April in this year when CSR imited has announced this transaction in ew, L N

South ales As stated in the terms of selling the company has to account around millionW . , $30

income before payment of ta in its statement during the period ended by Marchx 30th, 2019.

his settlement is e pected to materialize in the month of April of So far as secondT x 2019.

material subsequent event is concerned it is the declaration related to dividend CSR imited has, . L

declared per share contribution to the dividend valued million as percent$68.1 13.5 (csr com au. .

2018) he date of payment has been announced as. T 3rd of uly he dividend payment isJ , 2018. T

to be as a part of the organization.

Evaluation of effective material information

Auditors identify and evaluate risks generated from the misstatement in material

reporting.

hey e amine the suitable applications of policies related to accounting standardT x .

he auditors assesse formulation and presentation of the company s fi nancial statementT ’ .

Auditors e amine the suitability of the basic accounted standard as adapted by thex

directors ( isenbergE 2017).

t is responsibility of the auditors to clearly understand internal control of theI

organization.

n addition auditors collect sufficient evidences of auditI , .

Subsequent material event

he current annual report of the chose organization has mentioned two subsequentT

material events f the two one is the selling of land that are surplus to the company at orsley. O H

ark t is on theP . I 3rd April in this year when CSR imited has announced this transaction in ew, L N

South ales As stated in the terms of selling the company has to account around millionW . , $30

income before payment of ta in its statement during the period ended by Marchx 30th, 2019.

his settlement is e pected to materialize in the month of April of So far as secondT x 2019.

material subsequent event is concerned it is the declaration related to dividend CSR imited has, . L

declared per share contribution to the dividend valued million as percent$68.1 13.5 (csr com au. .

2018) he date of payment has been announced as. T 3rd of uly he dividend payment isJ , 2018. T

to be as a part of the organization.

Evaluation of effective material information

11A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

As viewed from the perspective of a third party shareholder it can be mentioned that the,

Deloitte s member related to auditing activity of CSR have efficiently and properly analyzed all the’

material information n this procedure the auditor has to comply with the states principles and. I ,

regulations as underlined in the A S Corporations Act Australian Auditing StandardsPE 110, 2001,

and others t has been also found that two matters of auditing have been identified by members of. I

Deloitte Such steps are also necessary to reduce the auditing matters All these indicate effectiveness. .

of Deloitte s auditing members in dealing with relevant material information of the company’ (Chen

et al. 2014).

Material information that are either missing, not fully disclosed or explained and/or under

reported

here are various material aspects and information that could result in risk arising fromT

material misstatement in reporting fi nancial statement of the company o he auditor of(H 2017). T

the company has e plained sufficient disclosure for confronting the material facts of CSR imitedx L .

he transparency of auditing service can be stated to be maintained no information has neitherT

omitted nor hide by the auditors in reporting of material statement of CSR imitedL .

Questions for follow-up

he auditor has been asked several questions in the general meeting held annuallyT

regarding review of procedure for auditing ilkinson and Coetzee n case of Deloitte(W 2015). I ,

which is the auditor of the chosen the possible questions for follow up are stated below

hat is the scope of the audit planW ?

As viewed from the perspective of a third party shareholder it can be mentioned that the,

Deloitte s member related to auditing activity of CSR have efficiently and properly analyzed all the’

material information n this procedure the auditor has to comply with the states principles and. I ,

regulations as underlined in the A S Corporations Act Australian Auditing StandardsPE 110, 2001,

and others t has been also found that two matters of auditing have been identified by members of. I

Deloitte Such steps are also necessary to reduce the auditing matters All these indicate effectiveness. .

of Deloitte s auditing members in dealing with relevant material information of the company’ (Chen

et al. 2014).

Material information that are either missing, not fully disclosed or explained and/or under

reported

here are various material aspects and information that could result in risk arising fromT

material misstatement in reporting fi nancial statement of the company o he auditor of(H 2017). T

the company has e plained sufficient disclosure for confronting the material facts of CSR imitedx L .

he transparency of auditing service can be stated to be maintained no information has neitherT

omitted nor hide by the auditors in reporting of material statement of CSR imitedL .

Questions for follow-up

he auditor has been asked several questions in the general meeting held annuallyT

regarding review of procedure for auditing ilkinson and Coetzee n case of Deloitte(W 2015). I ,

which is the auditor of the chosen the possible questions for follow up are stated below

hat is the scope of the audit planW ?

12A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

hether there is a scope of discussion reacted to accounting or auditing aspects with theW

company s management before the retention takes place’ ?

Does the organization have any e ternal auditorx ?

Does there e it any activity or subsidiary which the company has not disclosed in thex

auditing Duff? ( 2016)

hat do you think ensure effectiveness of auditing service identifying errors in materialW

information any act that is illicit or fraudulent, ?

hether the management face any issue in controlling business procedureW ?

Do you fi nd any scope for improvement in the organization to minimize auditing ti me?

hat techniques do you use in assessing risk for the organizationW ?

Do you fi nd any comple ities in current year s audit abuyex ’ ? (K et al. 2017)

Do you have any unsolved question that is subject to previous year s auditing’ ?

Conclusion

ased on the analysis so far has been made it can be concluded that auditor of CSRB ,

imited that is Deloitte has complied with underlined regulation in A S AS CorporationsL PE 110, I B, “

Act RS and other relevant standard principle of accounting during auditing of fi nancial2001”, IF

state report of the organization he auditing standard of Australia has laid out highest ethics. T

levels in the non audit service he analysis of auditor s remuneration reveal that as a whole- . T ’

there is percent fall in the same during the accounting year of Deloitte has identified and6.64 2018.

effectively handled two key auditing matters ransparency of the audit report has been maintained. T

as the auditors reveal all the relevant information in the annual report of Conclusively2018. ,

hether there is a scope of discussion reacted to accounting or auditing aspects with theW

company s management before the retention takes place’ ?

Does the organization have any e ternal auditorx ?

Does there e it any activity or subsidiary which the company has not disclosed in thex

auditing Duff? ( 2016)

hat do you think ensure effectiveness of auditing service identifying errors in materialW

information any act that is illicit or fraudulent, ?

hether the management face any issue in controlling business procedureW ?

Do you fi nd any scope for improvement in the organization to minimize auditing ti me?

hat techniques do you use in assessing risk for the organizationW ?

Do you fi nd any comple ities in current year s audit abuyex ’ ? (K et al. 2017)

Do you have any unsolved question that is subject to previous year s auditing’ ?

Conclusion

ased on the analysis so far has been made it can be concluded that auditor of CSRB ,

imited that is Deloitte has complied with underlined regulation in A S AS CorporationsL PE 110, I B, “

Act RS and other relevant standard principle of accounting during auditing of fi nancial2001”, IF

state report of the organization he auditing standard of Australia has laid out highest ethics. T

levels in the non audit service he analysis of auditor s remuneration reveal that as a whole- . T ’

there is percent fall in the same during the accounting year of Deloitte has identified and6.64 2018.

effectively handled two key auditing matters ransparency of the audit report has been maintained. T

as the auditors reveal all the relevant information in the annual report of Conclusively2018. ,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

some of the specific follow up questions are outlined that could be possibly asked to the auditor in

the general annual meeting.

some of the specific follow up questions are outlined that could be possibly asked to the auditor in

the general annual meeting.

14A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

List of References

radbury M Raftery A and Scott nowledge spillover from other assuranceB , .E., , . , T., 2018. K

services. ournal of Contemporary ccounting EconomicsJ A & , 14 pp(1), .52-64.

Chen Smith A Cao and ia nformation technology capability internal control, Y., , .L., , J. X , W., 2014. I ,

effectiveness and audit fees and delays, . ournal of nformation ystemsJ I S , 28 pp(2), .149-180.

Choi Chung Sonu C and ang pinion Shopping to Avoid a oing Concern, J.H., , H., , .H. Z , Y., 2018. O G

Audit pinion and Subsequent Audit ualityO Q . uditing ournal of Practice and heoryA : A J T .

Csr com au Annual Meetings and Reports online Available at. . ., 2018. . [ ] :

https www csr com au investor relations and news annual meetings and reports Accessed:// . . . / - - - / - - - [ 21

Sep. 2018].

Csr com au CSR uilding roducts a leading building products brand in Australia ew. . ., 2018. B P - & N

ealand online Available at https www csr com au Accessed SepZ . [ ] : :// . . . / [ 21 . 2018].

Du lessis argovan A and arrisP , J.J., H , . H , J., 2018. Principles of contemporary corporate

governance Cambridge niversity ress. U P .

Duff A Corporate social responsibility reporting in professional accounting fi rms, ., 2016. . he ritishT B

ccounting evieA R w, 48 pp(1), .74-86.

isenberg M A egal models of management structure in the modern corporation ffi cersE , . ., 2017. L : O ,

directors and accountants n, . I Corporate Governance pp ower( . 103-167). G .

ay D he frontiers of auditing researchH , ., 2015. T . Meditari ccountancy esearchA R , 23 pp(2), .158-

174.

List of References

radbury M Raftery A and Scott nowledge spillover from other assuranceB , .E., , . , T., 2018. K

services. ournal of Contemporary ccounting EconomicsJ A & , 14 pp(1), .52-64.

Chen Smith A Cao and ia nformation technology capability internal control, Y., , .L., , J. X , W., 2014. I ,

effectiveness and audit fees and delays, . ournal of nformation ystemsJ I S , 28 pp(2), .149-180.

Choi Chung Sonu C and ang pinion Shopping to Avoid a oing Concern, J.H., , H., , .H. Z , Y., 2018. O G

Audit pinion and Subsequent Audit ualityO Q . uditing ournal of Practice and heoryA : A J T .

Csr com au Annual Meetings and Reports online Available at. . ., 2018. . [ ] :

https www csr com au investor relations and news annual meetings and reports Accessed:// . . . / - - - / - - - [ 21

Sep. 2018].

Csr com au CSR uilding roducts a leading building products brand in Australia ew. . ., 2018. B P - & N

ealand online Available at https www csr com au Accessed SepZ . [ ] : :// . . . / [ 21 . 2018].

Du lessis argovan A and arrisP , J.J., H , . H , J., 2018. Principles of contemporary corporate

governance Cambridge niversity ress. U P .

Duff A Corporate social responsibility reporting in professional accounting fi rms, ., 2016. . he ritishT B

ccounting evieA R w, 48 pp(1), .74-86.

isenberg M A egal models of management structure in the modern corporation ffi cersE , . ., 2017. L : O ,

directors and accountants n, . I Corporate Governance pp ower( . 103-167). G .

ay D he frontiers of auditing researchH , ., 2015. T . Meditari ccountancy esearchA R , 23 pp(2), .158-

174.

15A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

ay D nechel R and illekens M edsH , ., K , W. . W , . ., 2014. he outledge companion to auditingT R .

Routledge.

ay D Stewart and otica Redmayne he Role of Auditing in Corporate overnanceH , ., , J. B , N., 2017. T G

in Australia and ew ealand A Research SynthesisN Z : . ustralian ccounting evieA A R w, 27(4),

pp.457-479.

o V Comply or e plain and the future of nonfinancial reportingH , .H., 2017. x . e is ClarL w & k L.

evR ., 21 p, .317.

umphrey C oft A and Samsonova addei A ot just a standard story he rise ofH , ., L , . -T , ., 2014. N : T

international standards on auditing n. I he outledge Companion to uditingT R A pp( . 183-200).

Routledge.

abuye kundabanyanga S piso and akabuye nternal audit organisationalK , F., N , .K., O , J. N , Z., 2017. I

status competencies activities and fraud management in the fi nancial services sector, , . Managerial

uditing ournalA J , 32 pp(9), .924-944.

ibby R Rennekamp M and Seybert Regulation and the interdependent roles ofL , ., , K. . , N., 2015.

managers auditors and directors in earnings management and accounting choice, , . ccountingA ,

rgani ations and ocietyO z S , 47 pp, .25-42.

Mubako and Donnell ff ect of fraud risk assessments on auditor skepticism, G. O' , E., 2018. E :

nintended consequences on evidence evaluationU . nternational ournal of uditingI J A , 22 pp(1), .55-

64.

ay D nechel R and illekens M edsH , ., K , W. . W , . ., 2014. he outledge companion to auditingT R .

Routledge.

ay D Stewart and otica Redmayne he Role of Auditing in Corporate overnanceH , ., , J. B , N., 2017. T G

in Australia and ew ealand A Research SynthesisN Z : . ustralian ccounting evieA A R w, 27(4),

pp.457-479.

o V Comply or e plain and the future of nonfinancial reportingH , .H., 2017. x . e is ClarL w & k L.

evR ., 21 p, .317.

umphrey C oft A and Samsonova addei A ot just a standard story he rise ofH , ., L , . -T , ., 2014. N : T

international standards on auditing n. I he outledge Companion to uditingT R A pp( . 183-200).

Routledge.

abuye kundabanyanga S piso and akabuye nternal audit organisationalK , F., N , .K., O , J. N , Z., 2017. I

status competencies activities and fraud management in the fi nancial services sector, , . Managerial

uditing ournalA J , 32 pp(9), .924-944.

ibby R Rennekamp M and Seybert Regulation and the interdependent roles ofL , ., , K. . , N., 2015.

managers auditors and directors in earnings management and accounting choice, , . ccountingA ,

rgani ations and ocietyO z S , 47 pp, .25-42.

Mubako and Donnell ff ect of fraud risk assessments on auditor skepticism, G. O' , E., 2018. E :

nintended consequences on evidence evaluationU . nternational ournal of uditingI J A , 22 pp(1), .55-

64.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

Tricker, R.B. and Tricker, R.I., 2015. Corporate governance Principles policies and practices: , , .

ford niversity ress SAOx U P , U .

sipouridou M and Spathis C March Audit opinion and earnings managementT , . , ., 2014, . :

vidence from reece nE G . I ccounting orumA F Vol o pp lsevier( . 38, N . 1, . 38-54). E .

ilkinson and Coetzee nternal Audit Assurance or Consulting Services Rendered onW , N. , P., 2015. I

overnance ow Does ne DecideG : H O ?. ournal of Governance and egulationJ R p, .186.

ong R and Millington A Corporate social disclosures a user perspective onW , . , ., 2014. :

assurance. ccounting uditing ccounta ility ournalA , A & A b J , 27 pp(5), .863-887.

Tricker, R.B. and Tricker, R.I., 2015. Corporate governance Principles policies and practices: , , .

ford niversity ress SAOx U P , U .

sipouridou M and Spathis C March Audit opinion and earnings managementT , . , ., 2014, . :

vidence from reece nE G . I ccounting orumA F Vol o pp lsevier( . 38, N . 1, . 38-54). E .

ilkinson and Coetzee nternal Audit Assurance or Consulting Services Rendered onW , N. , P., 2015. I

overnance ow Does ne DecideG : H O ?. ournal of Governance and egulationJ R p, .186.

ong R and Millington A Corporate social disclosures a user perspective onW , . , ., 2014. :

assurance. ccounting uditing ccounta ility ournalA , A & A b J , 27 pp(5), .863-887.

17A D ASS RA C A D C M A CH16026: U IT, U N E N O PLI N E

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.