Audit, Assurance, and Compliance Report: DIPL Financial Review

VerifiedAdded on 2020/03/02

|7

|1704

|38

Report

AI Summary

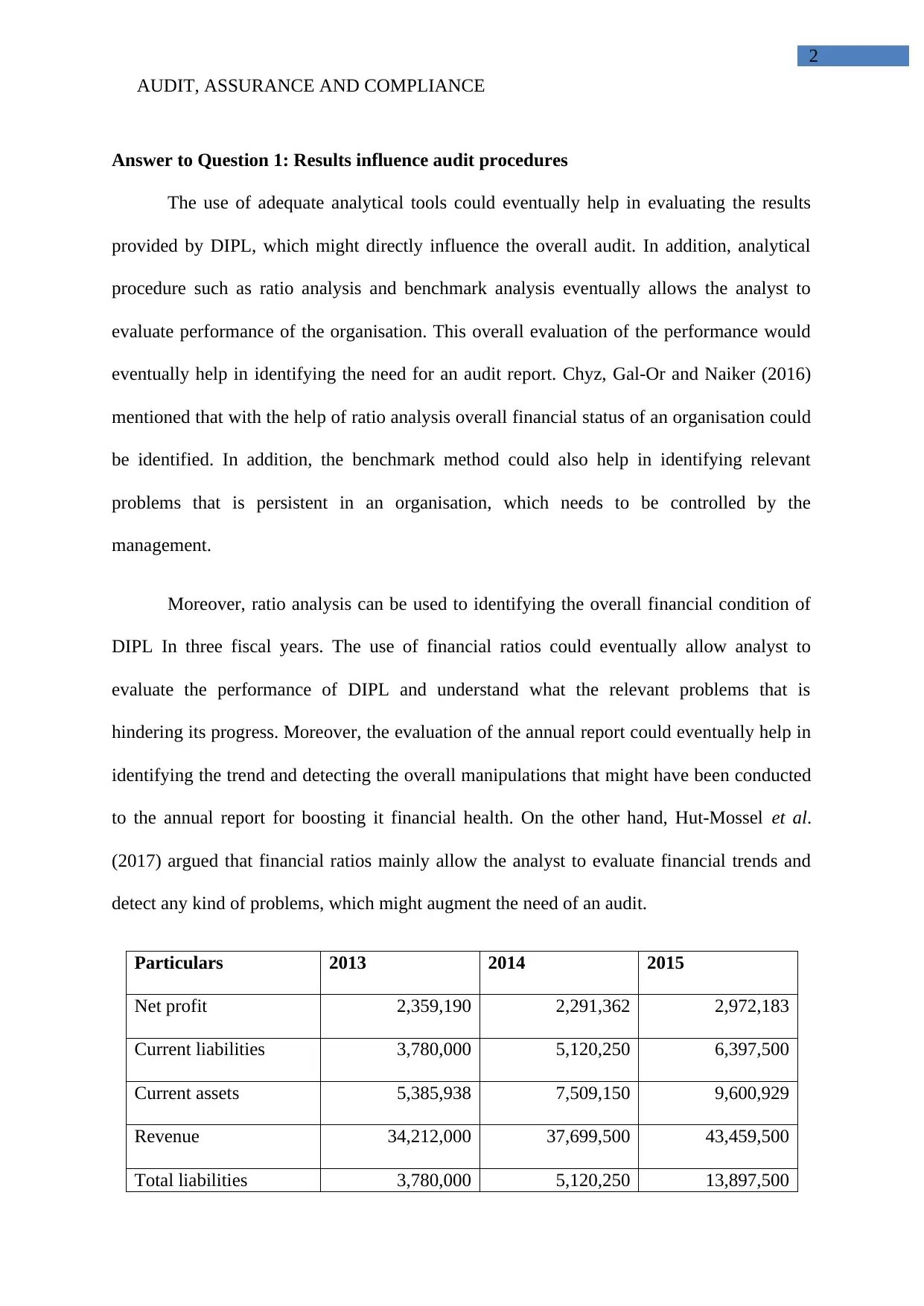

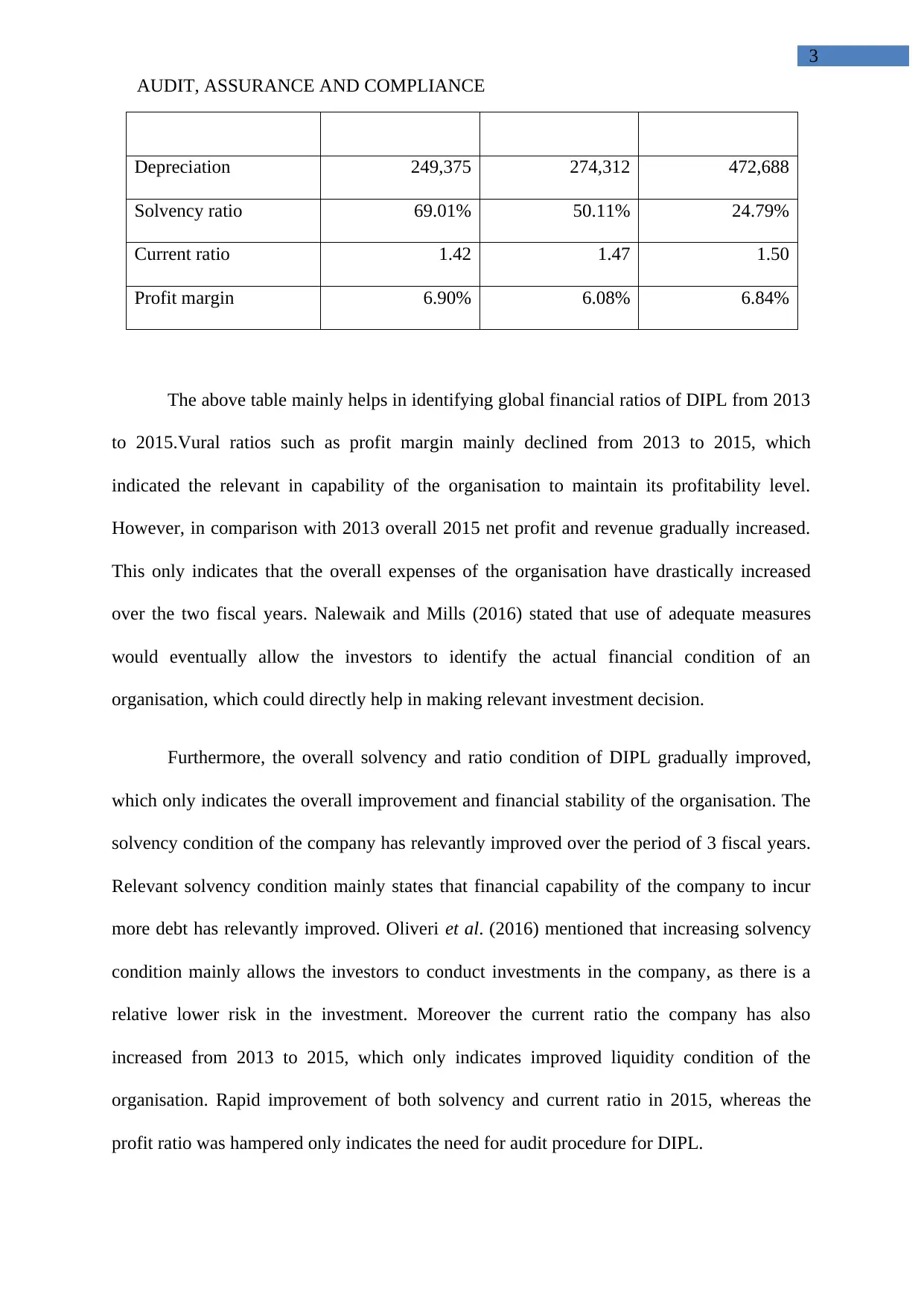

This report provides a comprehensive analysis of an audit, assurance, and compliance case study focusing on Double Ink Printers Limited (DIPL). The report begins by evaluating how analytical tools influence audit procedures, using ratio analysis and benchmark analysis to assess DIPL's financial performance from 2013 to 2015. It then identifies material misstatements, including financial and information technology risks, and explores fraudulent risks stemming from employee actions and financial report manipulations. The analysis includes an examination of DIPL's financial ratios, such as profit margin, solvency ratio, and current ratio, highlighting trends and potential areas of concern. The report also discusses the impact of debt covenants and the control environment on audit plans, emphasizing the importance of identifying and mitigating risks to ensure the accuracy and reliability of financial reporting. The findings underscore the need for robust audit procedures to address the identified risks and ensure compliance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.