Audit, Assurance and Compliance in Wesfarmers Limited

VerifiedAdded on 2023/06/05

|16

|3660

|467

AI Summary

This report analyses the audit report of Wesfarmers Limited and discusses key audit matters, non-audit services, auditor's remuneration, audit committee, material subsequent events, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, assurance and compliance

Name of the student

Name of the university

Author note

Audit, assurance and compliance

Name of the student

Name of the university

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2IntroductionIntroduction

Table of Contents

Introduction...........................................................................................................................................4

Independent auditor’s report................................................................................................................4

Non-audit services performed by the auditor.......................................................................................5

Auditor’s remuneration.........................................................................................................................6

key audit matters:..................................................................................................................................6

Impairment of non currant assets which includes intangible assets in the Target:...............................7

The rebates of the suppliers:.................................................................................................................7

Discussion of obsolete operations pertaining to Curragh......................................................................8

Discussion of obsolete operations pertaining to Bunnings UK and Ireland (BUKI):...............................8

Audit committee:...................................................................................................................................9

Audit opinion:......................................................................................................................................10

Responsibility segregation among auditor and management.............................................................10

Material subsequent events:...............................................................................................................11

Examining the material evidence pertaining to the auditors...............................................................11

Absence of material evidences............................................................................................................12

Question to be considered for follow-up.............................................................................................12

Conclusion...........................................................................................................................................13

References...........................................................................................................................................14

Table of Contents

Introduction...........................................................................................................................................4

Independent auditor’s report................................................................................................................4

Non-audit services performed by the auditor.......................................................................................5

Auditor’s remuneration.........................................................................................................................6

key audit matters:..................................................................................................................................6

Impairment of non currant assets which includes intangible assets in the Target:...............................7

The rebates of the suppliers:.................................................................................................................7

Discussion of obsolete operations pertaining to Curragh......................................................................8

Discussion of obsolete operations pertaining to Bunnings UK and Ireland (BUKI):...............................8

Audit committee:...................................................................................................................................9

Audit opinion:......................................................................................................................................10

Responsibility segregation among auditor and management.............................................................10

Material subsequent events:...............................................................................................................11

Examining the material evidence pertaining to the auditors...............................................................11

Absence of material evidences............................................................................................................12

Question to be considered for follow-up.............................................................................................12

Conclusion...........................................................................................................................................13

References...........................................................................................................................................14

3IntroductionIntroduction

Executive summary

The report states the context of Wesfarmers Limited where detailed study of the audit

report has been conducted which has taken into account the currant report of the

Wesfarmers of 2018. It has also shown that the auditor, Ernst & Young have included all the

material aspects which consists of material collision on the financial reporting of the

concerned organization. all the information have been revealed and explained by the

auditor of Wesfarmers which takes into account the material factors.

Executive summary

The report states the context of Wesfarmers Limited where detailed study of the audit

report has been conducted which has taken into account the currant report of the

Wesfarmers of 2018. It has also shown that the auditor, Ernst & Young have included all the

material aspects which consists of material collision on the financial reporting of the

concerned organization. all the information have been revealed and explained by the

auditor of Wesfarmers which takes into account the material factors.

4IntroductionIntroduction

Introduction

Auditing can be termed as analysing the monetary reports that are published by the

organizations in order to make sure that the reports does not contain any kind of frauds,

misstatements of materials or mistakes. Therefore, it is the duty of the auditors to provide a

good quality which is relevant to the information relating to the financial statements. The

auditors should also provide information to the stakeholders in such a language which will

be not difficult to understand. In the present situation, the audit committee have done

many things in order to make good quality audit report. Therefore, the auditors should take

into account the issues which is present in the financial statements which will also make a

better quality audit (Wesfarmers.com.au. 2018.). The following report emphasizes on the

currant report of the Wesfarmers Limited which linked with large number of aspects of

audit of the financial reports. In this case the audit partner here is Ernst and Young.

Independent auditor’s report

Before the production of audit service, the auditing firms present should maintain all

the rules and regulations which are related to the independence of the auditor. The auditors

therefore, are required to be linked with the audit client while providing audit operations.

The section of the latest report of Wesfarmers of the year 2018, Ernst & Young states that it

did not have any agreement in association with the Corporations Act 2001, when the audit

operations is to be provided (Zhou, Simnett and Hoang 2018). The directors of Wesfarmers

stated that the auditor Ernst & Young had maintained all the important professional

principles which are related to the standards of auditing. Some of which relates to the

guidelines of “ Accounting Professional and Ethical Standards Board’s APES 110 Code of

Ethics for Professional Accountants” and “ Corporations Act 2001”. The above mentioned

Introduction

Auditing can be termed as analysing the monetary reports that are published by the

organizations in order to make sure that the reports does not contain any kind of frauds,

misstatements of materials or mistakes. Therefore, it is the duty of the auditors to provide a

good quality which is relevant to the information relating to the financial statements. The

auditors should also provide information to the stakeholders in such a language which will

be not difficult to understand. In the present situation, the audit committee have done

many things in order to make good quality audit report. Therefore, the auditors should take

into account the issues which is present in the financial statements which will also make a

better quality audit (Wesfarmers.com.au. 2018.). The following report emphasizes on the

currant report of the Wesfarmers Limited which linked with large number of aspects of

audit of the financial reports. In this case the audit partner here is Ernst and Young.

Independent auditor’s report

Before the production of audit service, the auditing firms present should maintain all

the rules and regulations which are related to the independence of the auditor. The auditors

therefore, are required to be linked with the audit client while providing audit operations.

The section of the latest report of Wesfarmers of the year 2018, Ernst & Young states that it

did not have any agreement in association with the Corporations Act 2001, when the audit

operations is to be provided (Zhou, Simnett and Hoang 2018). The directors of Wesfarmers

stated that the auditor Ernst & Young had maintained all the important professional

principles which are related to the standards of auditing. Some of which relates to the

guidelines of “ Accounting Professional and Ethical Standards Board’s APES 110 Code of

Ethics for Professional Accountants” and “ Corporations Act 2001”. The above mentioned

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5IntroductionIntroduction

things are need to be followed so that the auditor’s independence can be properly

maintained.

Non-audit services performed by the auditor

There are mainly two different types of audit which are based on the latest report of

Wesfarmers in the currant year. The two types of services include services related to the

compliance of tax and the other different services. In order to perform tax compliance

service, the auditor is been provided with an amount of $683,000 and for the other service

it has been provided with $343,000. Therefore, the non audit service fees of the

Wesfarmers have been $1,026,000 in the currant year which is 12.01% of the audit fees

which is incurred in the year 2018 (Wesfarmers.com.au. 2018.). Although, all the necessary

compliances for Ernst &Young have been ensured by Wesfarmers while obtaining the non

audit services which indicates that the auditor has not comprised as per the regulations

mentioned in Corporations Act 2001. The auditors were also not provided any amount of

work that may involve the review of the work by Wesfarmers while taking any kind of

management decisions. While doing the non audit services, different kinds of guidelines

and governance norms have been followed which implies that there is a presence of

independence of the auditor.

things are need to be followed so that the auditor’s independence can be properly

maintained.

Non-audit services performed by the auditor

There are mainly two different types of audit which are based on the latest report of

Wesfarmers in the currant year. The two types of services include services related to the

compliance of tax and the other different services. In order to perform tax compliance

service, the auditor is been provided with an amount of $683,000 and for the other service

it has been provided with $343,000. Therefore, the non audit service fees of the

Wesfarmers have been $1,026,000 in the currant year which is 12.01% of the audit fees

which is incurred in the year 2018 (Wesfarmers.com.au. 2018.). Although, all the necessary

compliances for Ernst &Young have been ensured by Wesfarmers while obtaining the non

audit services which indicates that the auditor has not comprised as per the regulations

mentioned in Corporations Act 2001. The auditors were also not provided any amount of

work that may involve the review of the work by Wesfarmers while taking any kind of

management decisions. While doing the non audit services, different kinds of guidelines

and governance norms have been followed which implies that there is a presence of

independence of the auditor.

6IntroductionIntroduction

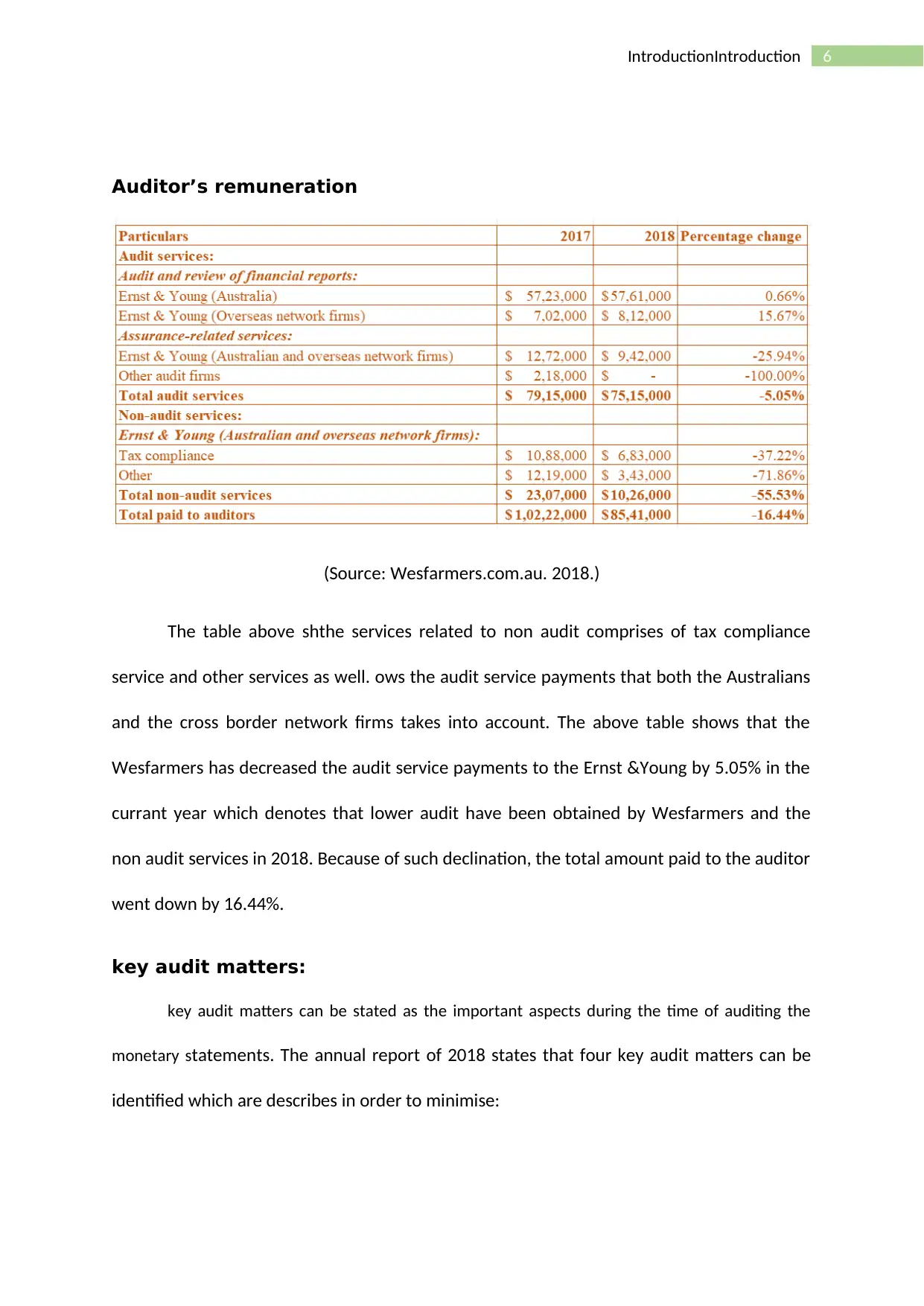

Auditor’s remuneration

(Source: Wesfarmers.com.au. 2018.)

The table above shthe services related to non audit comprises of tax compliance

service and other services as well. ows the audit service payments that both the Australians

and the cross border network firms takes into account. The above table shows that the

Wesfarmers has decreased the audit service payments to the Ernst &Young by 5.05% in the

currant year which denotes that lower audit have been obtained by Wesfarmers and the

non audit services in 2018. Because of such declination, the total amount paid to the auditor

went down by 16.44%.

key audit matters:

key audit matters can be stated as the important aspects during the time of auditing the

monetary statements. The annual report of 2018 states that four key audit matters can be

identified which are describes in order to minimise:

Auditor’s remuneration

(Source: Wesfarmers.com.au. 2018.)

The table above shthe services related to non audit comprises of tax compliance

service and other services as well. ows the audit service payments that both the Australians

and the cross border network firms takes into account. The above table shows that the

Wesfarmers has decreased the audit service payments to the Ernst &Young by 5.05% in the

currant year which denotes that lower audit have been obtained by Wesfarmers and the

non audit services in 2018. Because of such declination, the total amount paid to the auditor

went down by 16.44%.

key audit matters:

key audit matters can be stated as the important aspects during the time of auditing the

monetary statements. The annual report of 2018 states that four key audit matters can be

identified which are describes in order to minimise:

7IntroductionIntroduction

Impairment of non currant assets which includes intangible

assets in the Target:

The Wesfarmers are required to establish the amount of property that can be

recovered along with equipment and plants, goodwill and assets that are intangible in the

light of significant judgement. It has been observed by the auditors that Target has an

amount that can be recovered which is more than the carrying amount which would result

in impairment of the cash generating unit of Target. In order to deal with this matter, the

auditor has looked into the assumptions and the methodologies which are associated with

the cash generating unit, growth rate as well as estimating the cash flows. Along with that

the adequacy of the monetary statements which relates to the impairment test, sensitivities

and assumptions are also used by the auditors which can be stated as analytical procedures.

The rebates of the suppliers:

The rebates of the suppliers are those which the Wesfarmers have obtained from

the suppliers which are related to the operations of the retail. The rebates of the suppliers

considers a key audit matter because of the supplier rebate quantam that id realised in the

period and the perception is required to be exercised by taking into account few factors. In

order to deal with this kind of issue , Ernst & Young has taken into account t the audit

procedures. In addition to this, these practices are also depicted to include the testing

standard for providing supplier rebates and ensuring suppliers have a promotional credit for

analyzing the sample is associated with new contracts for the materials. These practices are

also necessary for assessing the inquisitive legal counsel pertaining to the business

representatives. Therefore, it is important to categorize the procedures such as control tests

with a considerable level of detail among the substantive balance required for analytical test

of procedure (Council 2014).

Impairment of non currant assets which includes intangible

assets in the Target:

The Wesfarmers are required to establish the amount of property that can be

recovered along with equipment and plants, goodwill and assets that are intangible in the

light of significant judgement. It has been observed by the auditors that Target has an

amount that can be recovered which is more than the carrying amount which would result

in impairment of the cash generating unit of Target. In order to deal with this matter, the

auditor has looked into the assumptions and the methodologies which are associated with

the cash generating unit, growth rate as well as estimating the cash flows. Along with that

the adequacy of the monetary statements which relates to the impairment test, sensitivities

and assumptions are also used by the auditors which can be stated as analytical procedures.

The rebates of the suppliers:

The rebates of the suppliers are those which the Wesfarmers have obtained from

the suppliers which are related to the operations of the retail. The rebates of the suppliers

considers a key audit matter because of the supplier rebate quantam that id realised in the

period and the perception is required to be exercised by taking into account few factors. In

order to deal with this kind of issue , Ernst & Young has taken into account t the audit

procedures. In addition to this, these practices are also depicted to include the testing

standard for providing supplier rebates and ensuring suppliers have a promotional credit for

analyzing the sample is associated with new contracts for the materials. These practices are

also necessary for assessing the inquisitive legal counsel pertaining to the business

representatives. Therefore, it is important to categorize the procedures such as control tests

with a considerable level of detail among the substantive balance required for analytical test

of procedure (Council 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8IntroductionIntroduction

Discussion of obsolete operations pertaining to Curragh

Wesfarmers had agreed for disposing the coal mines of Curragh in return of $700

million in 2018. This agreement was conducive in promoting the mechanism of sharing value

related to the future prices of metallurgical coal. Moreover, it is also discerned that

organisation has taken into consideration PAT of $ 250 million associated with discontinued

operation from the mine (Krishnan and Wang 2014). There are also several considerations

based on trading outcome which are related to disposing the gains, which form as the main

reason for why E&Y has regarded it in their KAM. The supervision of this matter taken into

account with sale agreement and purchases which are to be referred with the

documentation which are required for computing and evaluating the gains from post-tax

disposal (PTDG). Secondly, it is also identified various inputs from PTDG calculation

pertaining to which it is able to make sure that the liability and asset values are the

recognized. The next important step has considered the engagement of tax specialists in

identifying the tax impacts associated with the investment and various types of financial

statement disclosures which are also discussed to Curragh (Baatwah, Salleh and Ahmad

2015).

Discussion of obsolete operations pertaining to Bunnings UK and

Ireland (BUKI):

In the first half of 2018, there are several instances which has led to the recognition

related to impairment charge for BUKI amounting to $953 million. On 25th May 2018

Wesfarmers to the decision of divesting their operations for a nominal price. The financial

Discussion of obsolete operations pertaining to Curragh

Wesfarmers had agreed for disposing the coal mines of Curragh in return of $700

million in 2018. This agreement was conducive in promoting the mechanism of sharing value

related to the future prices of metallurgical coal. Moreover, it is also discerned that

organisation has taken into consideration PAT of $ 250 million associated with discontinued

operation from the mine (Krishnan and Wang 2014). There are also several considerations

based on trading outcome which are related to disposing the gains, which form as the main

reason for why E&Y has regarded it in their KAM. The supervision of this matter taken into

account with sale agreement and purchases which are to be referred with the

documentation which are required for computing and evaluating the gains from post-tax

disposal (PTDG). Secondly, it is also identified various inputs from PTDG calculation

pertaining to which it is able to make sure that the liability and asset values are the

recognized. The next important step has considered the engagement of tax specialists in

identifying the tax impacts associated with the investment and various types of financial

statement disclosures which are also discussed to Curragh (Baatwah, Salleh and Ahmad

2015).

Discussion of obsolete operations pertaining to Bunnings UK and

Ireland (BUKI):

In the first half of 2018, there are several instances which has led to the recognition

related to impairment charge for BUKI amounting to $953 million. On 25th May 2018

Wesfarmers to the decision of divesting their operations for a nominal price. The financial

9IntroductionIntroduction

statement published by the company in 2018 showed that Wesfarmers had incurred a loss

of 1.66 billion from discontinued operations. This has considered the impairment charge

which were realised during the beginning of six-month period as a result of trade outcome.

This was also effective at the time of disposal point and during disposal loss. This needs to

be also considered as the important rationale for why such a case was included by E&Y in

their KAM (Aobdia, Siddiqui and Vinelli 2016).

In order to handle such a situation of KAM, E&Y had tried to assess the precision of

impairment testing. It realized this with the application of several assumptions and

methodologies. The significant inputs were considered with assumptions pertaining to

commodity prices, discount rates, growth rates and rate of inflation (Amin, Krishnan and

Yang 2014). In addition to this, it was also understood by the auditor that the sale

agreement and purchases related with the documents they required for evaluation and

computation of disposal gains from tax. Secondly, it was also assessed that the inputs

pertaining to post-tax sales loss computations had confirmed the derecognition of liability

and asset values. The next important step was seen with engaging the tax specialists for

identifying the effects of taxation and divestment. This was finally stated under the

disclosures made in the financial statement (Drayson, Cranston and Krosch 2015).

statement published by the company in 2018 showed that Wesfarmers had incurred a loss

of 1.66 billion from discontinued operations. This has considered the impairment charge

which were realised during the beginning of six-month period as a result of trade outcome.

This was also effective at the time of disposal point and during disposal loss. This needs to

be also considered as the important rationale for why such a case was included by E&Y in

their KAM (Aobdia, Siddiqui and Vinelli 2016).

In order to handle such a situation of KAM, E&Y had tried to assess the precision of

impairment testing. It realized this with the application of several assumptions and

methodologies. The significant inputs were considered with assumptions pertaining to

commodity prices, discount rates, growth rates and rate of inflation (Amin, Krishnan and

Yang 2014). In addition to this, it was also understood by the auditor that the sale

agreement and purchases related with the documents they required for evaluation and

computation of disposal gains from tax. Secondly, it was also assessed that the inputs

pertaining to post-tax sales loss computations had confirmed the derecognition of liability

and asset values. The next important step was seen with engaging the tax specialists for

identifying the effects of taxation and divestment. This was finally stated under the

disclosures made in the financial statement (Drayson, Cranston and Krosch 2015).

10IntroductionIntroduction

Audit committee:

The last annual report published by Wesfarmers Limited had identified that

management related to the organization has formed a risk and audit committee and also

stated about its role in carrying out and monitoring of several types of procedures leading to

internal control and protection of the assets thereby confirming the integrity among

financial reporting standards. The aforementioned committee is recognised with two non-

executive directors- J.A. Westacott and D.L. Smith Gander. The important expanses for the

evaluation of the committee has regarded constituting of compliance with financial

reporting, integrity and reviewing the influential dynamics on the commercial incomes. The

framework is also seen to be playing a pivotal role for conducting a risk management plan

and incorporating the same into audit (Simnett and Huggins 2014).

Audit opinion:

The evidence is on audit opinion is recognised under the independent report

published by the auditors of Wesfarmers Ltd in 2018. The various disclosures of this report

have stated about conforming to the guidelines as prescribed under “Section 300A of the

Corporations Act 2001”. In addition to this, the opinion of E&Y has been also built a state

about development of financial reporting in such a manner which will be conducive for

regulating the AAS and other regulations which comply to Wesfarmers. Therefore, in the

given case it is seen that E&Y has passed an unqualified audit opinion on the company

(Drayson, Cranston and Krosch 2015).

Responsibility segregation among auditor and management

The information given in the latest financial report of Wesfarmers have shown the

differing responsibilities of auditor and management. This is mainly seen with financial

Audit committee:

The last annual report published by Wesfarmers Limited had identified that

management related to the organization has formed a risk and audit committee and also

stated about its role in carrying out and monitoring of several types of procedures leading to

internal control and protection of the assets thereby confirming the integrity among

financial reporting standards. The aforementioned committee is recognised with two non-

executive directors- J.A. Westacott and D.L. Smith Gander. The important expanses for the

evaluation of the committee has regarded constituting of compliance with financial

reporting, integrity and reviewing the influential dynamics on the commercial incomes. The

framework is also seen to be playing a pivotal role for conducting a risk management plan

and incorporating the same into audit (Simnett and Huggins 2014).

Audit opinion:

The evidence is on audit opinion is recognised under the independent report

published by the auditors of Wesfarmers Ltd in 2018. The various disclosures of this report

have stated about conforming to the guidelines as prescribed under “Section 300A of the

Corporations Act 2001”. In addition to this, the opinion of E&Y has been also built a state

about development of financial reporting in such a manner which will be conducive for

regulating the AAS and other regulations which comply to Wesfarmers. Therefore, in the

given case it is seen that E&Y has passed an unqualified audit opinion on the company

(Drayson, Cranston and Krosch 2015).

Responsibility segregation among auditor and management

The information given in the latest financial report of Wesfarmers have shown the

differing responsibilities of auditor and management. This is mainly seen with financial

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11IntroductionIntroduction

statements. The directors along with the managers are needed to ensure that the financial

reports are able to portray accurate picture of compliance with the regulations under

Australian accounting standards and Corporations Act 2001. More importantly, the

accountability of the directors is also essential to know about the ability of an organisation

to operate as per the going concern criteria. Moreover, there are other responsibilities

which are not similar to each other (Simnett, Carson and Vanstraelen 2016).

It is the responsibility of the auditors for assessing and investigating the financial

reports. These include confirming whether the reports are free of errors, frauds and

material misstatements. In addition to this, some of the other responsibilities of the

auditors are concerned with risk evaluation which are relevant with obtaining adequate

information on the internal control procedures and catalyzing the effectivity of accounting

policies which will be able to appropriately address the going concern criteria. These forms

the main accounting base for the directors. However, directors are not depicted to carry

such rules. The auditors are also accountable presentation of financial statements (Simnett

and Huggins 2015).

Material subsequent events:

It is worth mentioning that there are two main events which are considered by

Wesfarmers in 2018. Firstly, it is important to depict the demerger with Coles in March

2018. Despite of such a decision by the management E&Y has not included this event under

material value as there is not a significant impact of materiality in the financial statement of

Wesfarmers. The executive directors of Wesfarmers have also declared about fully franked

ordinary dividend amounting to 120c for each share. Due to this, the total amount

pertaining to the final dividend which was to be paid to the shareholders amounted to 223c

statements. The directors along with the managers are needed to ensure that the financial

reports are able to portray accurate picture of compliance with the regulations under

Australian accounting standards and Corporations Act 2001. More importantly, the

accountability of the directors is also essential to know about the ability of an organisation

to operate as per the going concern criteria. Moreover, there are other responsibilities

which are not similar to each other (Simnett, Carson and Vanstraelen 2016).

It is the responsibility of the auditors for assessing and investigating the financial

reports. These include confirming whether the reports are free of errors, frauds and

material misstatements. In addition to this, some of the other responsibilities of the

auditors are concerned with risk evaluation which are relevant with obtaining adequate

information on the internal control procedures and catalyzing the effectivity of accounting

policies which will be able to appropriately address the going concern criteria. These forms

the main accounting base for the directors. However, directors are not depicted to carry

such rules. The auditors are also accountable presentation of financial statements (Simnett

and Huggins 2015).

Material subsequent events:

It is worth mentioning that there are two main events which are considered by

Wesfarmers in 2018. Firstly, it is important to depict the demerger with Coles in March

2018. Despite of such a decision by the management E&Y has not included this event under

material value as there is not a significant impact of materiality in the financial statement of

Wesfarmers. The executive directors of Wesfarmers have also declared about fully franked

ordinary dividend amounting to 120c for each share. Due to this, the total amount

pertaining to the final dividend which was to be paid to the shareholders amounted to 223c

12IntroductionIntroduction

on 27th September 2018. This amount of dividend is yet to be distributed among the

shareholders (Drayson, Cranston and Krosch 2015).

Examining the material evidence pertaining to the auditors

As opined by the third-party stakeholders, it is evident that E&Y is having an efficient

role in terms of interpreting material information of Wesfarmers Ltd in its latest publication

of financial reports. Moreover, the appropriateness of adherence is understood with the

compliance of Corporations Act 2001 and APES 110 standards (Kass 2017). Furthermore, it

can be stated that auditors have identified four KAM from the financial statement and taken

several ramifications which led to minimizing the impacts as well. These considerations

clearly identified that E&Y was efficient in handling of material evidence (Knechel and

Salterio 2016).

Absence of material evidences

The thorough perusal of several excerpts of the annual report for Wesfarmers Ltd

published in 2018 shows that it’s auditor E&Y has not failed to consider any material

evidences or aspects which may take the form of material collision in the financial

statements. Moreover, every aspect of evidences was disclosed and inspected appropriately

by the auditors thereby stating about the factors associated to materiality which could have

adverse implication on the business (Australia and Australia 2015).

Question to be considered for follow-up

There may be numerous questions raised by the shareholders of Wesfarmers at the

time of annual general meeting. Some of the questions are listed as follows:

what are the initial motivations for carrying out the audit process?

on 27th September 2018. This amount of dividend is yet to be distributed among the

shareholders (Drayson, Cranston and Krosch 2015).

Examining the material evidence pertaining to the auditors

As opined by the third-party stakeholders, it is evident that E&Y is having an efficient

role in terms of interpreting material information of Wesfarmers Ltd in its latest publication

of financial reports. Moreover, the appropriateness of adherence is understood with the

compliance of Corporations Act 2001 and APES 110 standards (Kass 2017). Furthermore, it

can be stated that auditors have identified four KAM from the financial statement and taken

several ramifications which led to minimizing the impacts as well. These considerations

clearly identified that E&Y was efficient in handling of material evidence (Knechel and

Salterio 2016).

Absence of material evidences

The thorough perusal of several excerpts of the annual report for Wesfarmers Ltd

published in 2018 shows that it’s auditor E&Y has not failed to consider any material

evidences or aspects which may take the form of material collision in the financial

statements. Moreover, every aspect of evidences was disclosed and inspected appropriately

by the auditors thereby stating about the factors associated to materiality which could have

adverse implication on the business (Australia and Australia 2015).

Question to be considered for follow-up

There may be numerous questions raised by the shareholders of Wesfarmers at the

time of annual general meeting. Some of the questions are listed as follows:

what are the initial motivations for carrying out the audit process?

13IntroductionIntroduction

How will you verify the level of materiality in three KAM as stated in the annual

report?

What are the opportunities pertaining to external audit services?

What is the role of other auditors who may be involved in examining of financial

reports of the company?

Conclusion

The discourse of the study has been conducive in the eviction of several audit

services which are provided by the audit firms and conform about the guidelines pertaining

to the independence of the auditors. In the recent publication of financial statement

published by Wesfarmers Ltd it is evident that the company has appointed a team of audit

risk committee for monitoring and protecting of several types of internal control procedures

which will ensure overall fairness and integrity of financial reporting. In addition to this, the

directors and managers have also confirmed whether the financial statements are in

compliance to the Australian accounting standards and Corporations Act 2001.

Furthermore, the learnings from the study have stated about the accountability of the

directors in ensuring operations of the company as per going concern criteria.

How will you verify the level of materiality in three KAM as stated in the annual

report?

What are the opportunities pertaining to external audit services?

What is the role of other auditors who may be involved in examining of financial

reports of the company?

Conclusion

The discourse of the study has been conducive in the eviction of several audit

services which are provided by the audit firms and conform about the guidelines pertaining

to the independence of the auditors. In the recent publication of financial statement

published by Wesfarmers Ltd it is evident that the company has appointed a team of audit

risk committee for monitoring and protecting of several types of internal control procedures

which will ensure overall fairness and integrity of financial reporting. In addition to this, the

directors and managers have also confirmed whether the financial statements are in

compliance to the Australian accounting standards and Corporations Act 2001.

Furthermore, the learnings from the study have stated about the accountability of the

directors in ensuring operations of the company as per going concern criteria.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14IntroductionIntroduction

References

Amin, K., Krishnan, J. and Yang, J.S., 2014. Going concern opinion and cost of equity.

Auditing: A Journal of Practice & Theory, 33(4), pp.1-39.

Aobdia, D., Siddiqui, S. and Vinelli, A.G., 2016. Does engagement partner perceived

expertise matter? Evidence from the US operations of the Big 4 audit firms.

Australia, I. and Australia, D.I., 2015. RE: Australian Infrastructure Audit.

Baatwah, S.R., Salleh, Z. and Ahmad, N., 2015. CEO characteristics and audit report

timeliness: do CEO tenure and financial expertise matter?. Managerial Auditing

Journal, 30(8/9), pp.998-1022.

Council, F.R., 2014. Audit Quality Inspections: Annual Report 2012/13. London: FRC.

Drayson, N., Cranston, P.S. and Krosch, M.N., 2015. Taxonomic review of the chironomid

genus Cricotopus vd Wulp (Diptera: Chironomidae) from Australia: keys to males, females,

pupae and larvae, description of ten new species and comments on Paratrichocladius Santos

Abreu. Zootaxa, 3919(1), pp.1-40.

Drayson, N., Cranston, P.S. and Krosch, M.N., 2015. Taxonomic review of the chironomid

genus Cricotopus vd Wulp (Diptera: Chironomidae) from Australia: keys to males, females,

pupae and larvae, description of ten new species and comments on Paratrichocladius Santos

Abreu. Zootaxa, 3919(1), pp.1-40.

Drayson, N., Cranston, P.S. and Krosch, M.N., 2015. Taxonomic review of the chironomid

genus Cricotopus vd Wulp (Diptera: Chironomidae) from Australia: keys to males, females,

References

Amin, K., Krishnan, J. and Yang, J.S., 2014. Going concern opinion and cost of equity.

Auditing: A Journal of Practice & Theory, 33(4), pp.1-39.

Aobdia, D., Siddiqui, S. and Vinelli, A.G., 2016. Does engagement partner perceived

expertise matter? Evidence from the US operations of the Big 4 audit firms.

Australia, I. and Australia, D.I., 2015. RE: Australian Infrastructure Audit.

Baatwah, S.R., Salleh, Z. and Ahmad, N., 2015. CEO characteristics and audit report

timeliness: do CEO tenure and financial expertise matter?. Managerial Auditing

Journal, 30(8/9), pp.998-1022.

Council, F.R., 2014. Audit Quality Inspections: Annual Report 2012/13. London: FRC.

Drayson, N., Cranston, P.S. and Krosch, M.N., 2015. Taxonomic review of the chironomid

genus Cricotopus vd Wulp (Diptera: Chironomidae) from Australia: keys to males, females,

pupae and larvae, description of ten new species and comments on Paratrichocladius Santos

Abreu. Zootaxa, 3919(1), pp.1-40.

Drayson, N., Cranston, P.S. and Krosch, M.N., 2015. Taxonomic review of the chironomid

genus Cricotopus vd Wulp (Diptera: Chironomidae) from Australia: keys to males, females,

pupae and larvae, description of ten new species and comments on Paratrichocladius Santos

Abreu. Zootaxa, 3919(1), pp.1-40.

Drayson, N., Cranston, P.S. and Krosch, M.N., 2015. Taxonomic review of the chironomid

genus Cricotopus vd Wulp (Diptera: Chironomidae) from Australia: keys to males, females,

15IntroductionIntroduction

pupae and larvae, description of ten new species and comments on Paratrichocladius Santos

Abreu. Zootaxa, 3919(1), pp.1-40.

Kass, D., 2017. Educational Reform and Environmental Concern: A History of School Nature

Study in Australia. Routledge.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Krishnan, G.V. and Wang, C., 2014. The relation between managerial ability and audit fees

and going concern opinions. Auditing: A Journal of Practice & Theory, 34(3), pp.139-160.

Simnett, R. and Huggins, A., 2014. Enhancing the auditor's report: to what extent is there

support for the IAASB's proposed changes?. Accounting Horizons, 28(4), pp.719-747.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can research

add value?. Sustainability Accounting, Management and Policy Journal, 6(1), pp.29-53.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International archival auditing and

assurance research: Trends, methodological issues, and opportunities. Auditing: A Journal of

Practice & Theory, 35(3), pp.1-32.

Soh, D.S. and Martinov-Bennie, N., 2015. Internal auditors’ perceptions of their role in

environmental, social and governance assurance and consulting. Managerial Auditing

Journal, 30(1), pp.80-111.

Stewart, J., Kent, P. and Routledge, J., 2015. The association between audit partner rotation

and audit fees: Empirical evidence from the Australian market. Auditing: A Journal of

Practice & Theory, 35(1), pp.181-197.

pupae and larvae, description of ten new species and comments on Paratrichocladius Santos

Abreu. Zootaxa, 3919(1), pp.1-40.

Kass, D., 2017. Educational Reform and Environmental Concern: A History of School Nature

Study in Australia. Routledge.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Krishnan, G.V. and Wang, C., 2014. The relation between managerial ability and audit fees

and going concern opinions. Auditing: A Journal of Practice & Theory, 34(3), pp.139-160.

Simnett, R. and Huggins, A., 2014. Enhancing the auditor's report: to what extent is there

support for the IAASB's proposed changes?. Accounting Horizons, 28(4), pp.719-747.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can research

add value?. Sustainability Accounting, Management and Policy Journal, 6(1), pp.29-53.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International archival auditing and

assurance research: Trends, methodological issues, and opportunities. Auditing: A Journal of

Practice & Theory, 35(3), pp.1-32.

Soh, D.S. and Martinov-Bennie, N., 2015. Internal auditors’ perceptions of their role in

environmental, social and governance assurance and consulting. Managerial Auditing

Journal, 30(1), pp.80-111.

Stewart, J., Kent, P. and Routledge, J., 2015. The association between audit partner rotation

and audit fees: Empirical evidence from the Australian market. Auditing: A Journal of

Practice & Theory, 35(1), pp.181-197.

16IntroductionIntroduction

Wesfarmers.com.au., 2018. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-

report.pdf?sfvrsn=4 [Accessed 20 Sep. 2018].

Wesfarmers.com.au., 2018. [online] Available at: http://www.wesfarmers.com.au/

[Accessed 20 Sep. 2018].

Zhou, S., Simnett, R. and Hoang, H., 2018. Evaluating Combined Assurance as a New

Credibility Enhancement Technique. Auditing: A Journal of Practice and Theory, 21(7),

pp.143-171.

Wesfarmers.com.au., 2018. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-

report.pdf?sfvrsn=4 [Accessed 20 Sep. 2018].

Wesfarmers.com.au., 2018. [online] Available at: http://www.wesfarmers.com.au/

[Accessed 20 Sep. 2018].

Zhou, S., Simnett, R. and Hoang, H., 2018. Evaluating Combined Assurance as a New

Credibility Enhancement Technique. Auditing: A Journal of Practice and Theory, 21(7),

pp.143-171.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.