Wesfarmers Limited Audit Report: Evaluating Auditor's Independence

VerifiedAdded on 2021/06/14

|13

|3461

|87

Report

AI Summary

This report provides an in-depth analysis of the auditor's role within Wesfarmers Limited, focusing on key aspects such as auditor independence, compliance with accounting standards, and adherence to the Corporation Act 2001. It examines non-audit services, auditor remuneration, and key audit matters, including the methodologies used for audit planning and risk assessment. The report highlights the differences between management's responsibilities and those of the auditors, material subsequent events, and the effectiveness of auditor's material information. It also addresses potential issues of under-reporting or missing material information, concluding with an overall assessment of the audit function's impact on corporate governance and stakeholder confidence. The report emphasizes the importance of a robust audit function in ensuring the accuracy and reliability of Wesfarmers' financial reporting.

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmrtyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

AUDIT & ASSURANCE

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmrtyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

AUDIT & ASSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Wesfarmers Ltd

Executive Summary

The role of auditors assumes a place of special importance because it is in direct link with the

ethics and functioning of the company. The corporate governance of the company relies on

the function of the auditor. Moreover, the auditor report lays a strong foundation when it

comes to the concept of a stakeholder. In this report, selection of Wesfarmers Limited is done

for the purpose of the report and the role of the auditor is studied in an elaborate manner. The

report begins with the introduction of the company and then spreads to concept such as

auditor’s independence, key audit matters, and the audit committee. Apart from this, the

remuneration and audit opinion is provided due emphasis.

2

Executive Summary

The role of auditors assumes a place of special importance because it is in direct link with the

ethics and functioning of the company. The corporate governance of the company relies on

the function of the auditor. Moreover, the auditor report lays a strong foundation when it

comes to the concept of a stakeholder. In this report, selection of Wesfarmers Limited is done

for the purpose of the report and the role of the auditor is studied in an elaborate manner. The

report begins with the introduction of the company and then spreads to concept such as

auditor’s independence, key audit matters, and the audit committee. Apart from this, the

remuneration and audit opinion is provided due emphasis.

2

Wesfarmers Ltd

Contents

Introduction...........................................................................................................................................2

Compliance with the independent requirements..................................................................................2

Non audit services.................................................................................................................................2

Analysis of the Auditor remuneration...................................................................................................4

Nature of the audit services..................................................................................................................4

Key Audit matters..................................................................................................................................4

Difference in management’s responsibilities from that of the auditors................................................6

Material subsequent events..................................................................................................................7

Effectiveness of auditor’s material information....................................................................................7

Whether material information is missing/under-reported....................................................................8

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

3

Contents

Introduction...........................................................................................................................................2

Compliance with the independent requirements..................................................................................2

Non audit services.................................................................................................................................2

Analysis of the Auditor remuneration...................................................................................................4

Nature of the audit services..................................................................................................................4

Key Audit matters..................................................................................................................................4

Difference in management’s responsibilities from that of the auditors................................................6

Material subsequent events..................................................................................................................7

Effectiveness of auditor’s material information....................................................................................7

Whether material information is missing/under-reported....................................................................8

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Wesfarmers Ltd

Introduction

Audit report and audit function is the need of the hour because it denotes the authenticity of

the company’s performance. Wesfarmers has provided a true and fair view of the state of

affairs of the company. This is by dint of strong audit planning and control. Further, the

compliance with the accounting standard and the Corporation regulation 2001 has ensured an

effective mechanism (Wesfarmer, 2017). The report will reflect the functioning of the

company together with a strong emphasis on various areas such as audit control,

remuneration, and key audit matters, etc.

Compliance with the independent requirements

From the annual report it is noted that the audit was done in tune to the Australian

Accounting Standards. The independent requirements are followed and the same has been

stated in the Audit report. The auditor independence requirement was followed as per the

needs of the Corporation Act 2001 and the ethical needs that has been stated by the

Professional and Ethical Standard Board APES 110 code of Ethics for Professional

Accountants that are necessary for the audit of the financial report. All other responsibilities

has been fulfilled that are in tune to the code (Wesfarmer, 2017).

Non audit services

The audit and this committee of Wesfarmers Limited have provided the board with legal

advice for the non-audit services provided by it in a written form so as to comply with the

passing of the resolution for a committee. The advice of the risk committee has been

considered by the board and they are clearly satisfied with the thought of compatibility of the

decision of the non-audit services that will be provided to them (Wesfarmer, 2017). There are

various types of standards that are needed to be accepted by an auditor in order to make such

decisions which are stated under the corporation's act 2001:

The auditor will not be allowed to review any work or acting in a management that has been

conducted by him and thus he is not going to provide any type of review on the non-audit

services.

The audit and the committee of the organization have clearly reviewed all the non-audit

services for their structural integrity and objectivity towards the organization so that they do

4

Introduction

Audit report and audit function is the need of the hour because it denotes the authenticity of

the company’s performance. Wesfarmers has provided a true and fair view of the state of

affairs of the company. This is by dint of strong audit planning and control. Further, the

compliance with the accounting standard and the Corporation regulation 2001 has ensured an

effective mechanism (Wesfarmer, 2017). The report will reflect the functioning of the

company together with a strong emphasis on various areas such as audit control,

remuneration, and key audit matters, etc.

Compliance with the independent requirements

From the annual report it is noted that the audit was done in tune to the Australian

Accounting Standards. The independent requirements are followed and the same has been

stated in the Audit report. The auditor independence requirement was followed as per the

needs of the Corporation Act 2001 and the ethical needs that has been stated by the

Professional and Ethical Standard Board APES 110 code of Ethics for Professional

Accountants that are necessary for the audit of the financial report. All other responsibilities

has been fulfilled that are in tune to the code (Wesfarmer, 2017).

Non audit services

The audit and this committee of Wesfarmers Limited have provided the board with legal

advice for the non-audit services provided by it in a written form so as to comply with the

passing of the resolution for a committee. The advice of the risk committee has been

considered by the board and they are clearly satisfied with the thought of compatibility of the

decision of the non-audit services that will be provided to them (Wesfarmer, 2017). There are

various types of standards that are needed to be accepted by an auditor in order to make such

decisions which are stated under the corporation's act 2001:

The auditor will not be allowed to review any work or acting in a management that has been

conducted by him and thus he is not going to provide any type of review on the non-audit

services.

The audit and the committee of the organization have clearly reviewed all the non-audit

services for their structural integrity and objectivity towards the organization so that they do

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Wesfarmers Ltd

not harm any corporate governance procedures or policies that have been adopted by the

company. The integrity of the auditor’s independence should not be questioned because the

declaration is already provided.

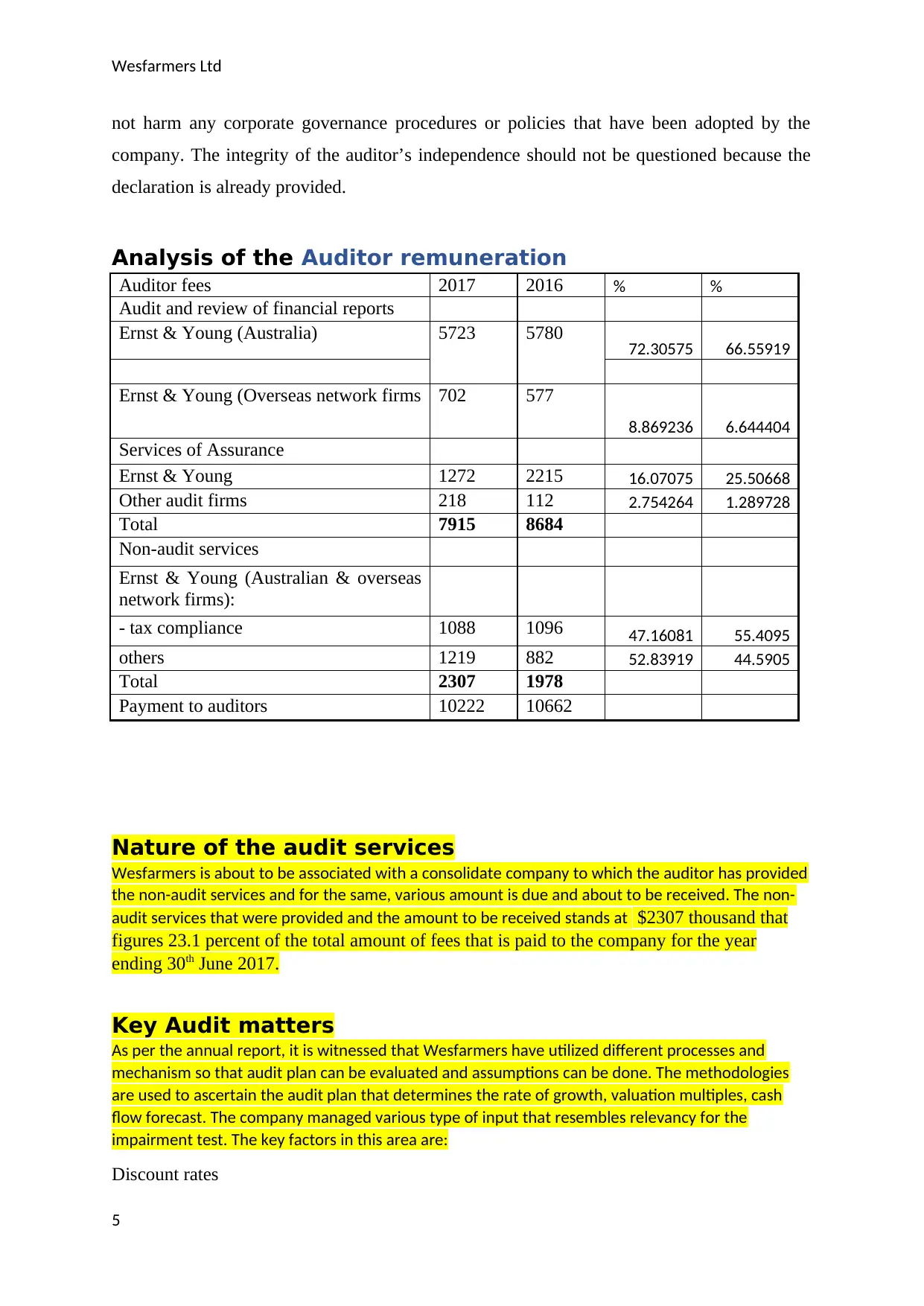

Analysis of the Auditor remuneration

Auditor fees 2017 2016 % %

Audit and review of financial reports

Ernst & Young (Australia) 5723 5780 72.30575 66.55919

Ernst & Young (Overseas network firms 702 577

8.869236 6.644404

Services of Assurance

Ernst & Young 1272 2215 16.07075 25.50668

Other audit firms 218 112 2.754264 1.289728

Total 7915 8684

Non-audit services

Ernst & Young (Australian & overseas

network firms):

- tax compliance 1088 1096 47.16081 55.4095

others 1219 882 52.83919 44.5905

Total 2307 1978

Payment to auditors 10222 10662

Nature of the audit services

Wesfarmers is about to be associated with a consolidate company to which the auditor has provided

the non-audit services and for the same, various amount is due and about to be received. The non-

audit services that were provided and the amount to be received stands at $2307 thousand that

figures 23.1 percent of the total amount of fees that is paid to the company for the year

ending 30th June 2017.

Key Audit matters

As per the annual report, it is witnessed that Wesfarmers have utilized different processes and

mechanism so that audit plan can be evaluated and assumptions can be done. The methodologies

are used to ascertain the audit plan that determines the rate of growth, valuation multiples, cash

flow forecast. The company managed various type of input that resembles relevancy for the

impairment test. The key factors in this area are:

Discount rates

5

not harm any corporate governance procedures or policies that have been adopted by the

company. The integrity of the auditor’s independence should not be questioned because the

declaration is already provided.

Analysis of the Auditor remuneration

Auditor fees 2017 2016 % %

Audit and review of financial reports

Ernst & Young (Australia) 5723 5780 72.30575 66.55919

Ernst & Young (Overseas network firms 702 577

8.869236 6.644404

Services of Assurance

Ernst & Young 1272 2215 16.07075 25.50668

Other audit firms 218 112 2.754264 1.289728

Total 7915 8684

Non-audit services

Ernst & Young (Australian & overseas

network firms):

- tax compliance 1088 1096 47.16081 55.4095

others 1219 882 52.83919 44.5905

Total 2307 1978

Payment to auditors 10222 10662

Nature of the audit services

Wesfarmers is about to be associated with a consolidate company to which the auditor has provided

the non-audit services and for the same, various amount is due and about to be received. The non-

audit services that were provided and the amount to be received stands at $2307 thousand that

figures 23.1 percent of the total amount of fees that is paid to the company for the year

ending 30th June 2017.

Key Audit matters

As per the annual report, it is witnessed that Wesfarmers have utilized different processes and

mechanism so that audit plan can be evaluated and assumptions can be done. The methodologies

are used to ascertain the audit plan that determines the rate of growth, valuation multiples, cash

flow forecast. The company managed various type of input that resembles relevancy for the

impairment test. The key factors in this area are:

Discount rates

5

Wesfarmers Ltd

Terminal growth rates

Assumptions of Long-term inflation and growth rate

Assumptions of the price of the commodity

Market evidence of industry revenues valuation multiples

Forecast exchange rate assumptions

The preparation of the financial report has been done in accordance as per the guidelines and

has been projected by the testing approach of impairment, key assumptions and the

sensitivities.

The company also followed the various types of auditory tasks in order to respect the

commercial income that has been earned by them. Some of them are: Assessment of each and

every type of material that has helped in order to produce commercial income has been made

including the signed agreements that have taken place during the year (Matthew, 2015). The

company has also tried to regulate corporate and design an effective and relevant control

system in which it can try to relate places with the help of recognition and measurement of

the different discounted amount (Geoffrey et. al, 2016).

Wesfarmers Limited have also tried to compare various discounted arrangements after

learning from the previous year’s budget which has helped them to include analysis of aging

profiles and various material variances with the help of supporting evidence.

The supporting documents to the discount provided to suppliers were also sent for tests. An

analysis was made on the suppliers and different promotional credits strategies so that the

supporting documentation can be processed (Niemi & Sundgren, 2012).

The company have also tried to implement many new material contracts both before and after

the balancing of the statements which clearly states that an assessment should be made in

relation to the treatment that has been adopted by the group. Also, the appropriateness of this

statement should be analyzed (Livne, 2015).

A legal counsel was also enquired to find out any other terms for a condition that have been

existed other than the rebate contracts or any unusual contract in which the company has

taken part.

6

Terminal growth rates

Assumptions of Long-term inflation and growth rate

Assumptions of the price of the commodity

Market evidence of industry revenues valuation multiples

Forecast exchange rate assumptions

The preparation of the financial report has been done in accordance as per the guidelines and

has been projected by the testing approach of impairment, key assumptions and the

sensitivities.

The company also followed the various types of auditory tasks in order to respect the

commercial income that has been earned by them. Some of them are: Assessment of each and

every type of material that has helped in order to produce commercial income has been made

including the signed agreements that have taken place during the year (Matthew, 2015). The

company has also tried to regulate corporate and design an effective and relevant control

system in which it can try to relate places with the help of recognition and measurement of

the different discounted amount (Geoffrey et. al, 2016).

Wesfarmers Limited have also tried to compare various discounted arrangements after

learning from the previous year’s budget which has helped them to include analysis of aging

profiles and various material variances with the help of supporting evidence.

The supporting documents to the discount provided to suppliers were also sent for tests. An

analysis was made on the suppliers and different promotional credits strategies so that the

supporting documentation can be processed (Niemi & Sundgren, 2012).

The company have also tried to implement many new material contracts both before and after

the balancing of the statements which clearly states that an assessment should be made in

relation to the treatment that has been adopted by the group. Also, the appropriateness of this

statement should be analyzed (Livne, 2015).

A legal counsel was also enquired to find out any other terms for a condition that have been

existed other than the rebate contracts or any unusual contract in which the company has

taken part.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Wesfarmers Ltd

Further, inquiry was even done on the various facts of the business that contains products,

merchandise, supply chain, staff so that the existence of nonstandard agreement can be

satisfied where the company contains its name.

All these or matters should be clearly analyzed by the company and actions should be

processed by them in order to correct these problems in time.

Difference in management’s responsibilities from that of

the auditors

In relation to Wesfarmers’ financial report, management of the same is the primary duty of

the directors or management but expressing an opinion on the same is the auditor’s task. The

auditor’s task is to perform and undertake the audit process to attain reasonable assurance

about whether the company’s financials are free from any material misstatements. In contrast

to this, when it comes to the directors and management of the company, it is their task to

adopt sound and effective accounting estimates and polices, thereby facilitating in the

establishment of internal control functions that can in turn assist in recording, initiating,

processing, and reporting transactions in alignment with their assertions declared in the

financial report (Viney, 2010). Furthermore, the company’s transactions and their associated

assets or liabilities together with the equities are within the direct purview and control of the

management. Besides, the knowledge of auditor’s regarding these matters and internal

control mechanisms are limited to that procured through the process of audit (Wesfarmers,

2017). Nevertheless, the fair representation of financial reports in alignment with the relevant

accounting principles is a significant and implicit responsibility of the management. In

contrast to this, the auditor may also take significant suggestions about the content or form of

such financial report, or draft them, in part or whole by depending on the information

procured from the management during audit procedure. Furthermore, the auditor’s duty for

such financial report he or she has undertaken is totally confined to the presentation or

assertation of his or her opinion on the same (Gay & Simnet, 2015). Moreover, the auditor of

Wesfarmers clearly does not have any kind of responsibility to perform and plan the audit to

procure reasonable assurance that the material misstatements whether caused by frauds or

errors are detected or identified. Therefore, the directors’ and managements’ responsibilities

are clearly distinct from that of the auditors when it comes to financial reporting

(Wesfarmers, 2017).

7

Further, inquiry was even done on the various facts of the business that contains products,

merchandise, supply chain, staff so that the existence of nonstandard agreement can be

satisfied where the company contains its name.

All these or matters should be clearly analyzed by the company and actions should be

processed by them in order to correct these problems in time.

Difference in management’s responsibilities from that of

the auditors

In relation to Wesfarmers’ financial report, management of the same is the primary duty of

the directors or management but expressing an opinion on the same is the auditor’s task. The

auditor’s task is to perform and undertake the audit process to attain reasonable assurance

about whether the company’s financials are free from any material misstatements. In contrast

to this, when it comes to the directors and management of the company, it is their task to

adopt sound and effective accounting estimates and polices, thereby facilitating in the

establishment of internal control functions that can in turn assist in recording, initiating,

processing, and reporting transactions in alignment with their assertions declared in the

financial report (Viney, 2010). Furthermore, the company’s transactions and their associated

assets or liabilities together with the equities are within the direct purview and control of the

management. Besides, the knowledge of auditor’s regarding these matters and internal

control mechanisms are limited to that procured through the process of audit (Wesfarmers,

2017). Nevertheless, the fair representation of financial reports in alignment with the relevant

accounting principles is a significant and implicit responsibility of the management. In

contrast to this, the auditor may also take significant suggestions about the content or form of

such financial report, or draft them, in part or whole by depending on the information

procured from the management during audit procedure. Furthermore, the auditor’s duty for

such financial report he or she has undertaken is totally confined to the presentation or

assertation of his or her opinion on the same (Gay & Simnet, 2015). Moreover, the auditor of

Wesfarmers clearly does not have any kind of responsibility to perform and plan the audit to

procure reasonable assurance that the material misstatements whether caused by frauds or

errors are detected or identified. Therefore, the directors’ and managements’ responsibilities

are clearly distinct from that of the auditors when it comes to financial reporting

(Wesfarmers, 2017).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Wesfarmers Ltd

Material subsequent events

It can be observed from the annual report of Wesfarmers that there are only two material

subsequent events that the company had experienced and that could have resulted in a big

impact on its financials. In tune to this, it should be recognized that the material subsequent

events are those that happens after the reporting date but before the financials for the period

of the issuance. The most vital event is observed in the annual report of the company where it

is seen that a fully franked and final ordinary dividend is paid after the period of reporting.

Moreover, payment of dividend is a potential factor that can easily affect the company’s

financial statements and overall performance on a whole (Wesfarmers, 2017). The main

factor behind such a matter can be attributed to the fact that the payment of dividend reflects

the ability of the company to attain prescribed EPS and ROI that helps the company to pay a

portion of the profit in terms of dividend. Therefore, since the company had paid a dividend

of 120 cents per share in the year 2017 after the reporting period, the same could have

affected its financial performance if it had occurred prior to the reporting period.

Nevertheless, it has paid a dividend of $1361 million that was declared for the payment date

of September 2017. Furthermore, the company had not paid dividend for the year 2017 that

may have affected its financials in a negative way. Further, Kmart which is known as the

department store acquired the brand in New Zealand and Australia.. This event can be

regarded as material in nature because Wesfarmers utilized such departmental store under a

licence-agreement that was long-term in nature and costed around hundred million dollars to

it (Wesfarmers, 2017). Even though based on the company’s statement, such transaction

could not possess a material impact on the earnings of Kmart, yet it could have affected the

share prices and earnings if the same occurred before the reporting date.

Effectiveness of auditor’s material information

It is observable from the auditor’s report of Wesfarmers that even though the auditors have

asserted that they audited the financial report of the company and it has complied with the

Corporations Act 2001 and AAS, yet the effectiveness of such material information cannot be

entirely seen. The primary reason behind this can be attributed to the fact that auditors have

only reflected few key audit matters in their report and have highlighted the process of how

they have undertaken the audit in relation to addressing such key audit matters. In addition,

such key audit matters are not properly described or explained by them and instead, only why

this key matter has been accounted for, has been portrayed (Wesfarmers, 2017). Therefore, if

the key audit matters are not explained effectively, it will become complicated for the users to

8

Material subsequent events

It can be observed from the annual report of Wesfarmers that there are only two material

subsequent events that the company had experienced and that could have resulted in a big

impact on its financials. In tune to this, it should be recognized that the material subsequent

events are those that happens after the reporting date but before the financials for the period

of the issuance. The most vital event is observed in the annual report of the company where it

is seen that a fully franked and final ordinary dividend is paid after the period of reporting.

Moreover, payment of dividend is a potential factor that can easily affect the company’s

financial statements and overall performance on a whole (Wesfarmers, 2017). The main

factor behind such a matter can be attributed to the fact that the payment of dividend reflects

the ability of the company to attain prescribed EPS and ROI that helps the company to pay a

portion of the profit in terms of dividend. Therefore, since the company had paid a dividend

of 120 cents per share in the year 2017 after the reporting period, the same could have

affected its financial performance if it had occurred prior to the reporting period.

Nevertheless, it has paid a dividend of $1361 million that was declared for the payment date

of September 2017. Furthermore, the company had not paid dividend for the year 2017 that

may have affected its financials in a negative way. Further, Kmart which is known as the

department store acquired the brand in New Zealand and Australia.. This event can be

regarded as material in nature because Wesfarmers utilized such departmental store under a

licence-agreement that was long-term in nature and costed around hundred million dollars to

it (Wesfarmers, 2017). Even though based on the company’s statement, such transaction

could not possess a material impact on the earnings of Kmart, yet it could have affected the

share prices and earnings if the same occurred before the reporting date.

Effectiveness of auditor’s material information

It is observable from the auditor’s report of Wesfarmers that even though the auditors have

asserted that they audited the financial report of the company and it has complied with the

Corporations Act 2001 and AAS, yet the effectiveness of such material information cannot be

entirely seen. The primary reason behind this can be attributed to the fact that auditors have

only reflected few key audit matters in their report and have highlighted the process of how

they have undertaken the audit in relation to addressing such key audit matters. In addition,

such key audit matters are not properly described or explained by them and instead, only why

this key matter has been accounted for, has been portrayed (Wesfarmers, 2017). Therefore, if

the key audit matters are not explained effectively, it will become complicated for the users to

8

Wesfarmers Ltd

determine the nature of such matter, thereby resulting in improper decision-making on their

part. However, they have effectively disclosed the process on how such matter has been taken

into consideration that is a positive indicator on the part of users. Furthermore, when it comes

to an interested third-party stakeholder, it must be noted that highlighting any issue as

material information also necessitates proper and adequate details regarding the same

(Kaplan, 2011). However, the same is absent from the auditors’ report that is a problematic

scenario as users may face problems while making decisions (Wesfarmers, 2017).

Nonetheless, the auditors have not provided complete information in relation to such key

audit matters, yet they have disclosed details of footnotes and notes wherein information

regarding the same can be found. Overall, the effectiveness of auditor’s material information

can be considered risky in nature and any third-party stakeholder may not rely upon such

details to make appropriate decisions.

Whether material information is missing/under-reported

Furthermore, there are various things that had to be disclosed by the company but it failed to

do so. Moreover, absence of such information can result in complications on the part of users

in effective decision-making. For instance, it can be seen from the financial statements of the

company that there are no footnotes to such financial statements that may create an issue for

users to ascertain the relation of any transaction. However, there are notes to financial

statements that have been properly addressed by the company and that is a positive step on its

part but absence of adequate footnotes to the financials are not appropriate for the intended

users (Wesfarmers, 2017). Furthermore, other material information like sustainability,

corporate governance, risk factors, etc are adequately disclosed by the company that can

facilitate in proper decisions on the part of intended users. In addition to these, there are few

details that are under-reported by the company. For instance, when it comes to the principal

affairs of entities within the consolidated group, the company has not disclosed adequate

information (Hoffelder, 2012). It has only mentioned slight details of the activities that are

not enough in nature because users demand proper disclosure for undertaking decision-

making processes. In addition, material information regarding the company’s diversity is also

not prevalent in the annual report and the same has been disclosed separately on the website

that may result in absence of material information (Rezaee &Kedia, 2012).

Apart from these issues, only the key audit matters are inaccurately disclosed by the auditors

that can have a material impact on the financials of the company. If the auditors had provided

9

determine the nature of such matter, thereby resulting in improper decision-making on their

part. However, they have effectively disclosed the process on how such matter has been taken

into consideration that is a positive indicator on the part of users. Furthermore, when it comes

to an interested third-party stakeholder, it must be noted that highlighting any issue as

material information also necessitates proper and adequate details regarding the same

(Kaplan, 2011). However, the same is absent from the auditors’ report that is a problematic

scenario as users may face problems while making decisions (Wesfarmers, 2017).

Nonetheless, the auditors have not provided complete information in relation to such key

audit matters, yet they have disclosed details of footnotes and notes wherein information

regarding the same can be found. Overall, the effectiveness of auditor’s material information

can be considered risky in nature and any third-party stakeholder may not rely upon such

details to make appropriate decisions.

Whether material information is missing/under-reported

Furthermore, there are various things that had to be disclosed by the company but it failed to

do so. Moreover, absence of such information can result in complications on the part of users

in effective decision-making. For instance, it can be seen from the financial statements of the

company that there are no footnotes to such financial statements that may create an issue for

users to ascertain the relation of any transaction. However, there are notes to financial

statements that have been properly addressed by the company and that is a positive step on its

part but absence of adequate footnotes to the financials are not appropriate for the intended

users (Wesfarmers, 2017). Furthermore, other material information like sustainability,

corporate governance, risk factors, etc are adequately disclosed by the company that can

facilitate in proper decisions on the part of intended users. In addition to these, there are few

details that are under-reported by the company. For instance, when it comes to the principal

affairs of entities within the consolidated group, the company has not disclosed adequate

information (Hoffelder, 2012). It has only mentioned slight details of the activities that are

not enough in nature because users demand proper disclosure for undertaking decision-

making processes. In addition, material information regarding the company’s diversity is also

not prevalent in the annual report and the same has been disclosed separately on the website

that may result in absence of material information (Rezaee &Kedia, 2012).

Apart from these issues, only the key audit matters are inaccurately disclosed by the auditors

that can have a material impact on the financials of the company. If the auditors had provided

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Wesfarmers Ltd

more information regarding their key audit matters rather than focusing on why such

information was significant, then it may have resulted in more effectiveness. Nevertheless,

compliance with the AAS and generally accepted accounting principles shed light on the fact

that the company has been consistent in its duties to attain intended objectives (Baldwin,

2010). However, if these facts were given due consideration, the annual report would become

more beneficial to the entire group of stakeholders.

10

more information regarding their key audit matters rather than focusing on why such

information was significant, then it may have resulted in more effectiveness. Nevertheless,

compliance with the AAS and generally accepted accounting principles shed light on the fact

that the company has been consistent in its duties to attain intended objectives (Baldwin,

2010). However, if these facts were given due consideration, the annual report would become

more beneficial to the entire group of stakeholders.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Wesfarmers Ltd

Conclusion

Form the overall report, it comes to the conclusion that the audit report and the audit function

of Wesfarmers is placed in an effective manner. It signifies the fact that the company has

complied with the Corporation Act 2001 and the Professional and Ethical Standard Board

APES 110. Hence, the audit structure of the company has been highly effective. All the

responsibilities in the Auditor Responsibilities has been fulfilled and the audit is designed in a

manner that responds to the risk assessment and misstatement in the financial report. Overall,

the company has projected a strong audit report and it is by dint of proper planning and

adherence to the regulations.

11

Conclusion

Form the overall report, it comes to the conclusion that the audit report and the audit function

of Wesfarmers is placed in an effective manner. It signifies the fact that the company has

complied with the Corporation Act 2001 and the Professional and Ethical Standard Board

APES 110. Hence, the audit structure of the company has been highly effective. All the

responsibilities in the Auditor Responsibilities has been fulfilled and the audit is designed in a

manner that responds to the risk assessment and misstatement in the financial report. Overall,

the company has projected a strong audit report and it is by dint of proper planning and

adherence to the regulations.

11

Wesfarmers Ltd

References

Baldwin, S. (2010) Doing a content audit or inventory. Pearson Press.

Gay, G. and Simnet, R. (2015) Auditing and Assurance Services. McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S. and David A. W. (2016) Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors. Accounting

Horizons. [online] 30(1), pp. 143-156. Available from https://doi.org/10.2308/acch-51309

[Accessed 4 August 2018]

Hoffelder, K. (2012) New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011) Accounting scholarship that advances professional knowledge and

practice. The Accounting Review [online]. 86(2), pp. 367–383. Available from

https://doi.org/10.2308/accr.00000031

Lapsley, I. (2012) Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management. [online]. 9(3), pp. 291-292. Available from

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015) Threats to Auditor Independence and Possible Remedies. [online] Available

from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full [Accessed 4 August 2018]

Matthew, S. E. (2015) Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review. [online]. 90(2), pp. 495-527. Available from

https://doi.org/10.2308/accr-50871 [Accessed 4 August 2018]

Pilbeam, K. (2009) Finance and Financial Markets. Palgrave Macmillan

Rezaee, Z & Kedia, B. L. (2012) Role of Corporate Governance Participants in Preventing

and Detecting Financial Statement Fraud. Journal of Forensic & Investigative Accounting.

[online]. 4(2), pp. 176-205. Available from: doi: 10.1016/j.sbspro.2014.06.041 [Accessed 4

August 2018]

Viney, C. (2010) McGrath’s Financial Institutions, Instruments and Markets, Sydney

Niemi, L. and Sundgren, S. (2012) Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review. [online]. 21(4), p. 767-

12

References

Baldwin, S. (2010) Doing a content audit or inventory. Pearson Press.

Gay, G. and Simnet, R. (2015) Auditing and Assurance Services. McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S. and David A. W. (2016) Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors. Accounting

Horizons. [online] 30(1), pp. 143-156. Available from https://doi.org/10.2308/acch-51309

[Accessed 4 August 2018]

Hoffelder, K. (2012) New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011) Accounting scholarship that advances professional knowledge and

practice. The Accounting Review [online]. 86(2), pp. 367–383. Available from

https://doi.org/10.2308/accr.00000031

Lapsley, I. (2012) Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management. [online]. 9(3), pp. 291-292. Available from

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015) Threats to Auditor Independence and Possible Remedies. [online] Available

from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full [Accessed 4 August 2018]

Matthew, S. E. (2015) Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review. [online]. 90(2), pp. 495-527. Available from

https://doi.org/10.2308/accr-50871 [Accessed 4 August 2018]

Pilbeam, K. (2009) Finance and Financial Markets. Palgrave Macmillan

Rezaee, Z & Kedia, B. L. (2012) Role of Corporate Governance Participants in Preventing

and Detecting Financial Statement Fraud. Journal of Forensic & Investigative Accounting.

[online]. 4(2), pp. 176-205. Available from: doi: 10.1016/j.sbspro.2014.06.041 [Accessed 4

August 2018]

Viney, C. (2010) McGrath’s Financial Institutions, Instruments and Markets, Sydney

Niemi, L. and Sundgren, S. (2012) Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review. [online]. 21(4), p. 767-

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.