Advice on Expectation Gap and Audit Independence

VerifiedAdded on 2022/10/12

|9

|1812

|480

AI Summary

This memo provides advice on expectation gap and audit independence. It explains the concept of audit expectation gap and how it can affect the audit engagement. It also discusses the threats to audit independence and the necessary safeguards against these threats. The memo is addressed to William Albanese, the Audit Manager of Samway Baker Fitzgerald (SBF).

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDIT

Audit

Name of the Student

Name of the University

Author’s Note

Audit

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUDIT

MEMO

To: William Albanese

From: Audit Manager of Samway Baker Fitzgerald (SBF)

Date: 01.09.2019

Subject: Advice on Expectation Gap and Audit Independence

There are certain aspects that the audit engagement officer is required to take into

consideration at the time of undertaking the audit. Two of these crucial areas are the

Expectation Gap and Threats to Audit Independence along with their Safeguards. Advice

about these two aspects are mentioned below.

Audit Expectation Gap

Audit expectation gap is considered as an important consideration that needs to be covered by

the audit engagement partners. The presence of a difference can be seen between the

expectation of the users of the financial statements regarding the responsibility of the auditors

and the actual responsibility of the auditors. The audit expectation gas occurs when the

expectations of the users of the financial statements does not match with the outcome of

audit. The presence of certain users of the financial statements can be seen which extract

information from the financial statements in order to make different decisions (Humphrey,

Samsonova & Siddiqui, 2013). According to the provided information, Bletchington Limited

(Bletchington) is an innovative defence industry manufacturing company and one of the

largest clients of SBF in terms of fee revenue. Bletchington does business with the companies

that have recognized democratically elected government and its product is highly specialized

in nature. For this reason, these governments are the main customers of Bletchington who

MEMO

To: William Albanese

From: Audit Manager of Samway Baker Fitzgerald (SBF)

Date: 01.09.2019

Subject: Advice on Expectation Gap and Audit Independence

There are certain aspects that the audit engagement officer is required to take into

consideration at the time of undertaking the audit. Two of these crucial areas are the

Expectation Gap and Threats to Audit Independence along with their Safeguards. Advice

about these two aspects are mentioned below.

Audit Expectation Gap

Audit expectation gap is considered as an important consideration that needs to be covered by

the audit engagement partners. The presence of a difference can be seen between the

expectation of the users of the financial statements regarding the responsibility of the auditors

and the actual responsibility of the auditors. The audit expectation gas occurs when the

expectations of the users of the financial statements does not match with the outcome of

audit. The presence of certain users of the financial statements can be seen which extract

information from the financial statements in order to make different decisions (Humphrey,

Samsonova & Siddiqui, 2013). According to the provided information, Bletchington Limited

(Bletchington) is an innovative defence industry manufacturing company and one of the

largest clients of SBF in terms of fee revenue. Bletchington does business with the companies

that have recognized democratically elected government and its product is highly specialized

in nature. For this reason, these governments are the main customers of Bletchington who

2AUDIT

have immense interest in the company’s financial statements. Other users of the financial

statements of Bletchington are the management, investors, lenders, suppliers and employees.

Now, these users of the financial statements have certain expectations from the auditors

related to the audit of the financial statements. This expectations lead to the development of

audit expectation gap where the beliefs of the users of the financial statements do not align

with the audit performance. This can also be happened with the audit engagement of SBF

with Bletchington due to the presence of the desire to want more from the auditors. These

users of the financial reports of Bletchington can bring unrealistic demand from the auditors.

For this reason, the audit partner of Bletchington may have to face impractical demand from

these users (Cordoş & Fülöp, 2015).

For example, as per the unrealistic demand of the users, the auditor music provide the

guaranteed future viability of the business of Bletchington. After that, complete assurance

must be provided from the side of the auditors. Moreover, it is the job of the auditors to state

that the fact that all the financial accounts are wholly appropriate through providing the

unmodified audit report. Each financial frauds must be detected by the auditors in the

financial reports. Lastly, the auditors are responsible to check every financial transaction of

the companies. In actual, this is not the case as the above are not the responsibility of the

auditors (George-Silviu & Melinda-Timea, 2015). As per the auditing rules related to the

auditors’ responsibilities, it is the responsibility of the auditor to provide only reasonable

assurance, not complete assurance; and they are not responsible for providing the guarantee

of the future feasibility of the company. As per the audit rules, the auditors are only allowed

to issue unmodified audit opinion when all the financial accounts are correct which is proven

by audit test. It is not the respobslity of the auditors to provide guarantee on the aspect that

financial statements are free from fraud, but they are responsible for unfolding the frauds in

the financial statements with the assistance of required audit tests. Moreover, testing the

have immense interest in the company’s financial statements. Other users of the financial

statements of Bletchington are the management, investors, lenders, suppliers and employees.

Now, these users of the financial statements have certain expectations from the auditors

related to the audit of the financial statements. This expectations lead to the development of

audit expectation gap where the beliefs of the users of the financial statements do not align

with the audit performance. This can also be happened with the audit engagement of SBF

with Bletchington due to the presence of the desire to want more from the auditors. These

users of the financial reports of Bletchington can bring unrealistic demand from the auditors.

For this reason, the audit partner of Bletchington may have to face impractical demand from

these users (Cordoş & Fülöp, 2015).

For example, as per the unrealistic demand of the users, the auditor music provide the

guaranteed future viability of the business of Bletchington. After that, complete assurance

must be provided from the side of the auditors. Moreover, it is the job of the auditors to state

that the fact that all the financial accounts are wholly appropriate through providing the

unmodified audit report. Each financial frauds must be detected by the auditors in the

financial reports. Lastly, the auditors are responsible to check every financial transaction of

the companies. In actual, this is not the case as the above are not the responsibility of the

auditors (George-Silviu & Melinda-Timea, 2015). As per the auditing rules related to the

auditors’ responsibilities, it is the responsibility of the auditor to provide only reasonable

assurance, not complete assurance; and they are not responsible for providing the guarantee

of the future feasibility of the company. As per the audit rules, the auditors are only allowed

to issue unmodified audit opinion when all the financial accounts are correct which is proven

by audit test. It is not the respobslity of the auditors to provide guarantee on the aspect that

financial statements are free from fraud, but they are responsible for unfolding the frauds in

the financial statements with the assistance of required audit tests. Moreover, testing the

3AUDIT

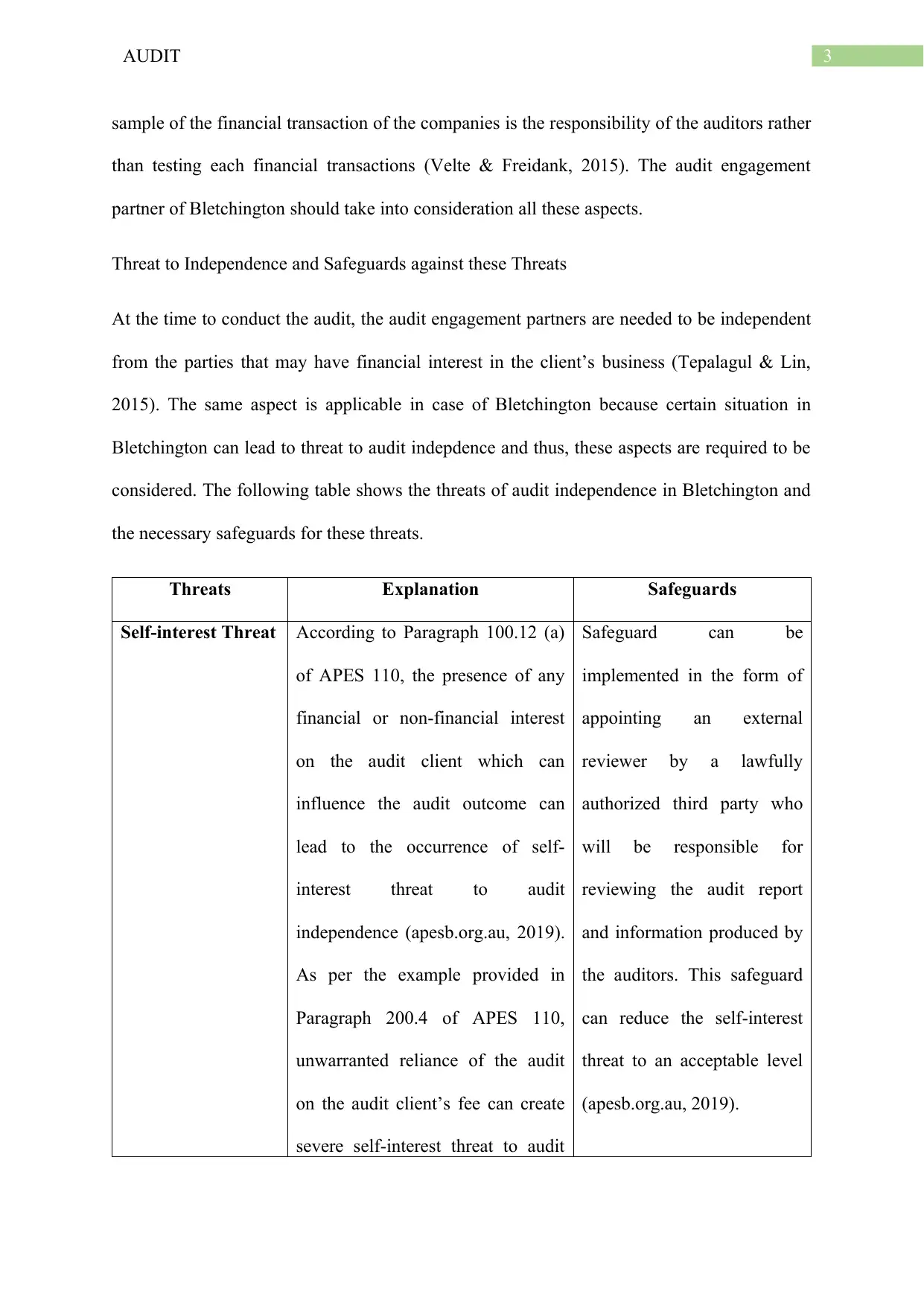

sample of the financial transaction of the companies is the responsibility of the auditors rather

than testing each financial transactions (Velte & Freidank, 2015). The audit engagement

partner of Bletchington should take into consideration all these aspects.

Threat to Independence and Safeguards against these Threats

At the time to conduct the audit, the audit engagement partners are needed to be independent

from the parties that may have financial interest in the client’s business (Tepalagul & Lin,

2015). The same aspect is applicable in case of Bletchington because certain situation in

Bletchington can lead to threat to audit indepdence and thus, these aspects are required to be

considered. The following table shows the threats of audit independence in Bletchington and

the necessary safeguards for these threats.

Threats Explanation Safeguards

Self-interest Threat According to Paragraph 100.12 (a)

of APES 110, the presence of any

financial or non-financial interest

on the audit client which can

influence the audit outcome can

lead to the occurrence of self-

interest threat to audit

independence (apesb.org.au, 2019).

As per the example provided in

Paragraph 200.4 of APES 110,

unwarranted reliance of the audit

on the audit client’s fee can create

severe self-interest threat to audit

Safeguard can be

implemented in the form of

appointing an external

reviewer by a lawfully

authorized third party who

will be responsible for

reviewing the audit report

and information produced by

the auditors. This safeguard

can reduce the self-interest

threat to an acceptable level

(apesb.org.au, 2019).

sample of the financial transaction of the companies is the responsibility of the auditors rather

than testing each financial transactions (Velte & Freidank, 2015). The audit engagement

partner of Bletchington should take into consideration all these aspects.

Threat to Independence and Safeguards against these Threats

At the time to conduct the audit, the audit engagement partners are needed to be independent

from the parties that may have financial interest in the client’s business (Tepalagul & Lin,

2015). The same aspect is applicable in case of Bletchington because certain situation in

Bletchington can lead to threat to audit indepdence and thus, these aspects are required to be

considered. The following table shows the threats of audit independence in Bletchington and

the necessary safeguards for these threats.

Threats Explanation Safeguards

Self-interest Threat According to Paragraph 100.12 (a)

of APES 110, the presence of any

financial or non-financial interest

on the audit client which can

influence the audit outcome can

lead to the occurrence of self-

interest threat to audit

independence (apesb.org.au, 2019).

As per the example provided in

Paragraph 200.4 of APES 110,

unwarranted reliance of the audit

on the audit client’s fee can create

severe self-interest threat to audit

Safeguard can be

implemented in the form of

appointing an external

reviewer by a lawfully

authorized third party who

will be responsible for

reviewing the audit report

and information produced by

the auditors. This safeguard

can reduce the self-interest

threat to an acceptable level

(apesb.org.au, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUDIT

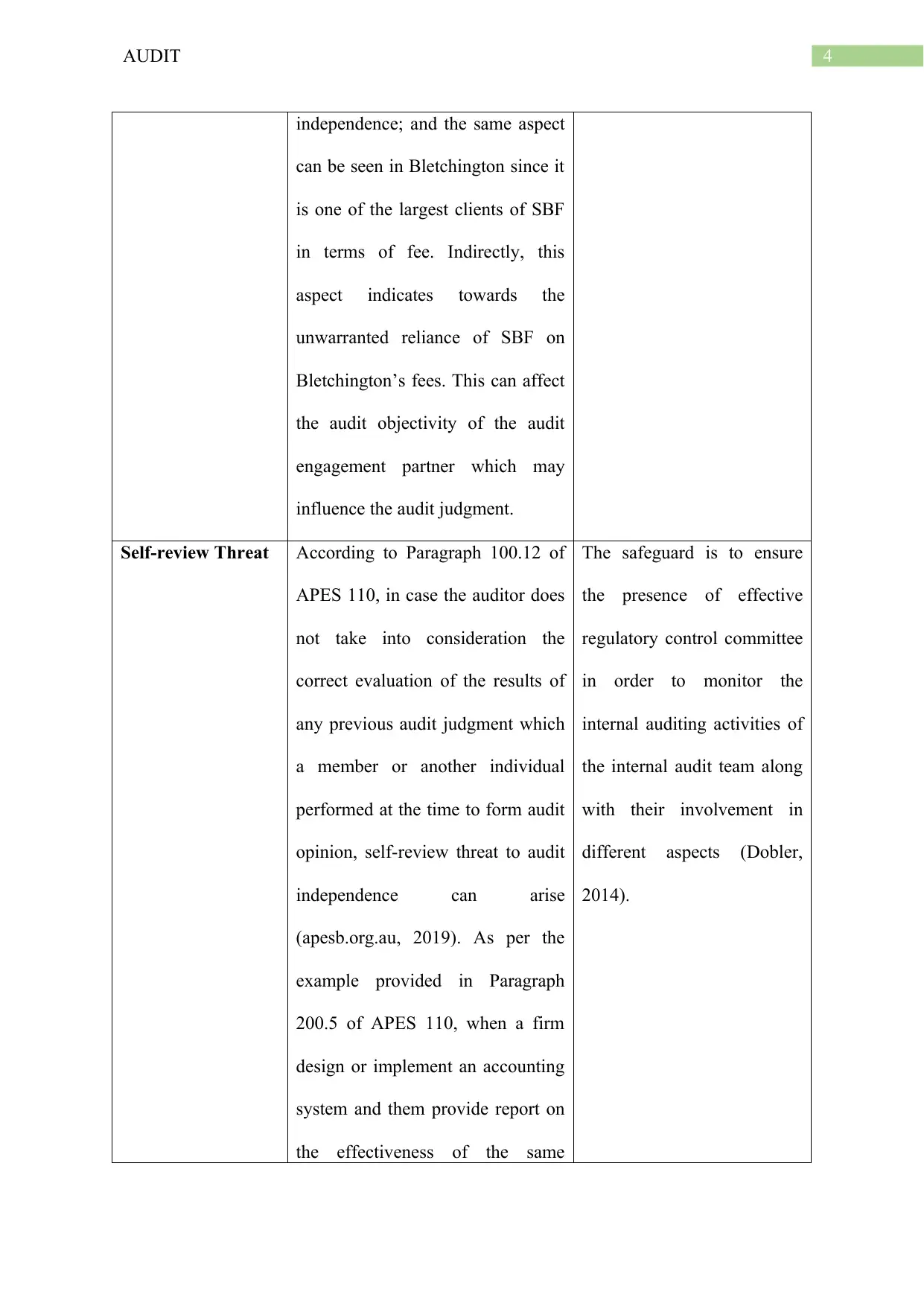

independence; and the same aspect

can be seen in Bletchington since it

is one of the largest clients of SBF

in terms of fee. Indirectly, this

aspect indicates towards the

unwarranted reliance of SBF on

Bletchington’s fees. This can affect

the audit objectivity of the audit

engagement partner which may

influence the audit judgment.

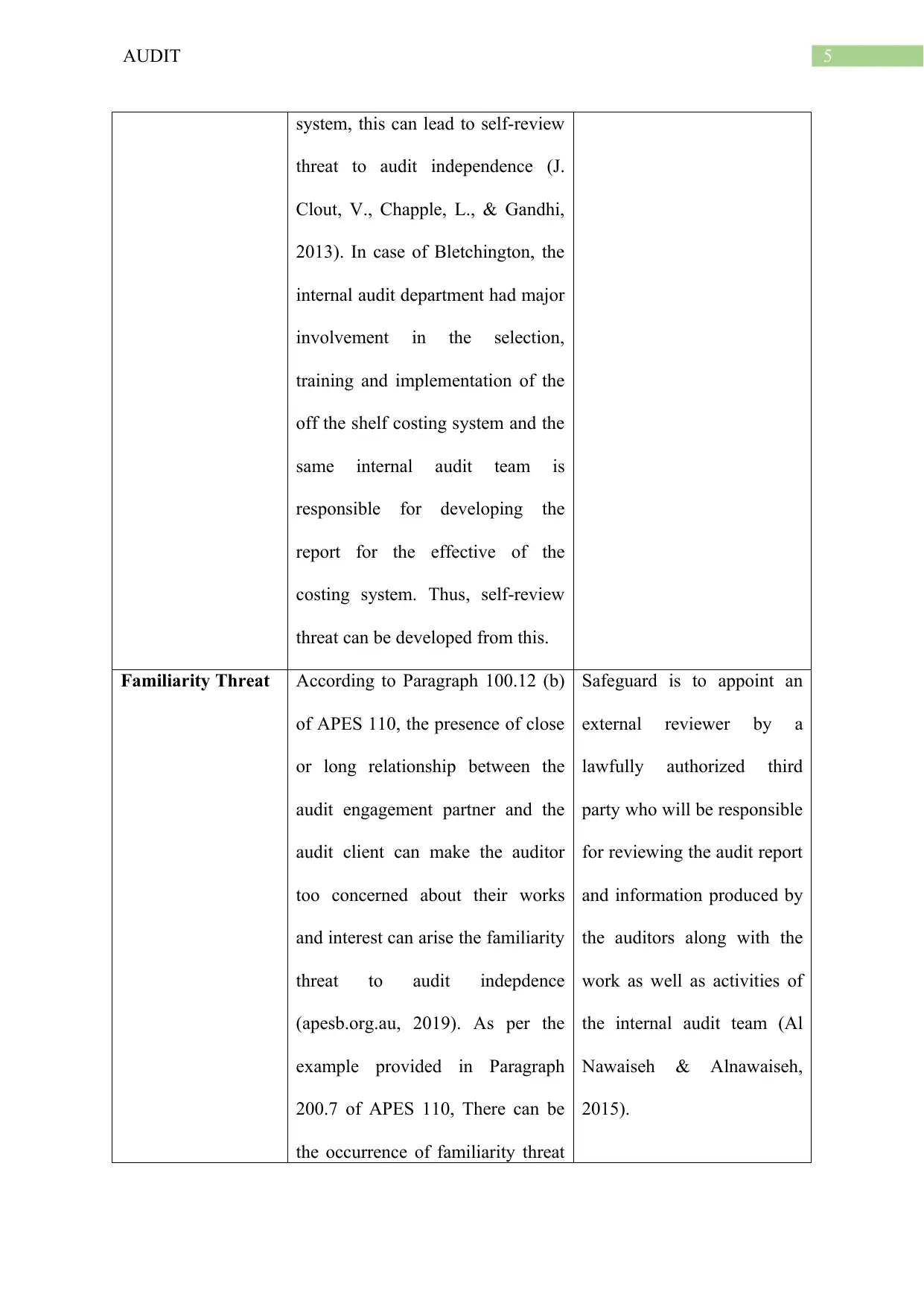

Self-review Threat According to Paragraph 100.12 of

APES 110, in case the auditor does

not take into consideration the

correct evaluation of the results of

any previous audit judgment which

a member or another individual

performed at the time to form audit

opinion, self-review threat to audit

independence can arise

(apesb.org.au, 2019). As per the

example provided in Paragraph

200.5 of APES 110, when a firm

design or implement an accounting

system and them provide report on

the effectiveness of the same

The safeguard is to ensure

the presence of effective

regulatory control committee

in order to monitor the

internal auditing activities of

the internal audit team along

with their involvement in

different aspects (Dobler,

2014).

independence; and the same aspect

can be seen in Bletchington since it

is one of the largest clients of SBF

in terms of fee. Indirectly, this

aspect indicates towards the

unwarranted reliance of SBF on

Bletchington’s fees. This can affect

the audit objectivity of the audit

engagement partner which may

influence the audit judgment.

Self-review Threat According to Paragraph 100.12 of

APES 110, in case the auditor does

not take into consideration the

correct evaluation of the results of

any previous audit judgment which

a member or another individual

performed at the time to form audit

opinion, self-review threat to audit

independence can arise

(apesb.org.au, 2019). As per the

example provided in Paragraph

200.5 of APES 110, when a firm

design or implement an accounting

system and them provide report on

the effectiveness of the same

The safeguard is to ensure

the presence of effective

regulatory control committee

in order to monitor the

internal auditing activities of

the internal audit team along

with their involvement in

different aspects (Dobler,

2014).

5AUDIT

system, this can lead to self-review

threat to audit independence (J.

Clout, V., Chapple, L., & Gandhi,

2013). In case of Bletchington, the

internal audit department had major

involvement in the selection,

training and implementation of the

off the shelf costing system and the

same internal audit team is

responsible for developing the

report for the effective of the

costing system. Thus, self-review

threat can be developed from this.

Familiarity Threat According to Paragraph 100.12 (b)

of APES 110, the presence of close

or long relationship between the

audit engagement partner and the

audit client can make the auditor

too concerned about their works

and interest can arise the familiarity

threat to audit indepdence

(apesb.org.au, 2019). As per the

example provided in Paragraph

200.7 of APES 110, There can be

the occurrence of familiarity threat

Safeguard is to appoint an

external reviewer by a

lawfully authorized third

party who will be responsible

for reviewing the audit report

and information produced by

the auditors along with the

work as well as activities of

the internal audit team (Al

Nawaiseh & Alnawaiseh,

2015).

system, this can lead to self-review

threat to audit independence (J.

Clout, V., Chapple, L., & Gandhi,

2013). In case of Bletchington, the

internal audit department had major

involvement in the selection,

training and implementation of the

off the shelf costing system and the

same internal audit team is

responsible for developing the

report for the effective of the

costing system. Thus, self-review

threat can be developed from this.

Familiarity Threat According to Paragraph 100.12 (b)

of APES 110, the presence of close

or long relationship between the

audit engagement partner and the

audit client can make the auditor

too concerned about their works

and interest can arise the familiarity

threat to audit indepdence

(apesb.org.au, 2019). As per the

example provided in Paragraph

200.7 of APES 110, There can be

the occurrence of familiarity threat

Safeguard is to appoint an

external reviewer by a

lawfully authorized third

party who will be responsible

for reviewing the audit report

and information produced by

the auditors along with the

work as well as activities of

the internal audit team (Al

Nawaiseh & Alnawaiseh,

2015).

6AUDIT

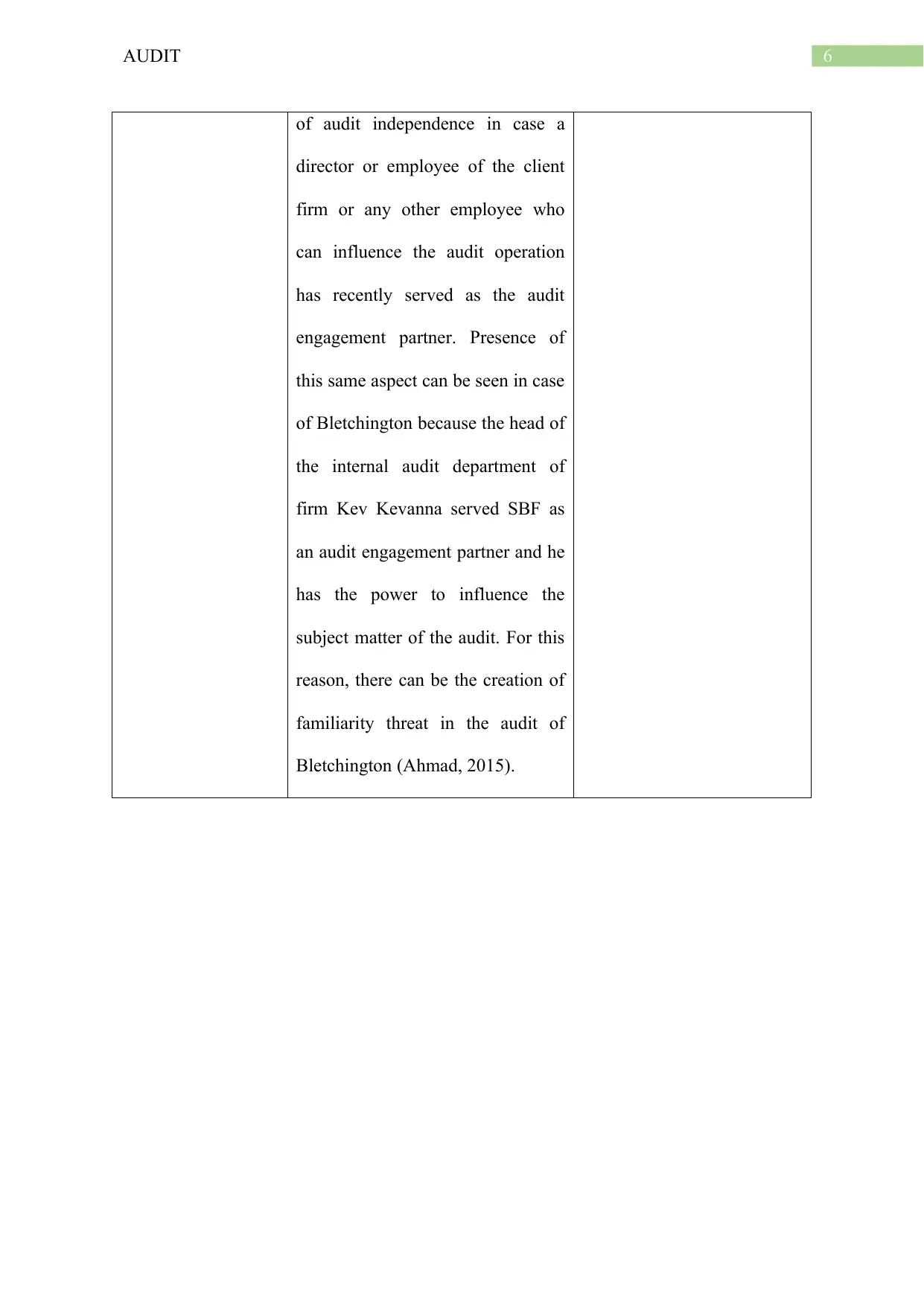

of audit independence in case a

director or employee of the client

firm or any other employee who

can influence the audit operation

has recently served as the audit

engagement partner. Presence of

this same aspect can be seen in case

of Bletchington because the head of

the internal audit department of

firm Kev Kevanna served SBF as

an audit engagement partner and he

has the power to influence the

subject matter of the audit. For this

reason, there can be the creation of

familiarity threat in the audit of

Bletchington (Ahmad, 2015).

of audit independence in case a

director or employee of the client

firm or any other employee who

can influence the audit operation

has recently served as the audit

engagement partner. Presence of

this same aspect can be seen in case

of Bletchington because the head of

the internal audit department of

firm Kev Kevanna served SBF as

an audit engagement partner and he

has the power to influence the

subject matter of the audit. For this

reason, there can be the creation of

familiarity threat in the audit of

Bletchington (Ahmad, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT

References

Ahmad, M. (2015). The impact of ex-auditors’ employment with audit clients on perceptions

of auditor independence. Procedia-Social and Behavioral Sciences, 172, 479-486.

Al Nawaiseh, M. A. L., & Alnawaiseh, M. (2015). The Effects of the Threats on the Auditor's

Independence. International Business Research, 8(8), 141.

Apesb.org.au. (2019). APES 110 Code of Ethics for Professional Accountants. Retrieved 1

August 2019, from

https://www.apesb.org.au/uploads/standards/apesb_standards/standardc1.pdf

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Dobler, M. (2014). Auditor-provided non-audit services in listed and private family

firms. Managerial Auditing Journal, 29(5), 427-454.

George-Silviu, C., & Melinda-Timea, F. (2015). New audit reporting challenges: auditing the

going concern basis of accounting. Procedia Economics and Finance, 32, 216-224.

Humphrey, C., Samsonova, A., & Siddiqui, J. (2013). Auditing, regulation and the

persistence of the expectations gap. In The Routledge Companion to Accounting,

Reporting and Regulation (pp. 185-206). Routledge.

J. Clout, V., Chapple, L., & Gandhi, N. (2013). The impact of auditor independence

regulations on established and emerging firms. Accounting Research Journal, 26(2),

88-108.

Tepalagul, N., & Lin, L. (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), 101-121.

References

Ahmad, M. (2015). The impact of ex-auditors’ employment with audit clients on perceptions

of auditor independence. Procedia-Social and Behavioral Sciences, 172, 479-486.

Al Nawaiseh, M. A. L., & Alnawaiseh, M. (2015). The Effects of the Threats on the Auditor's

Independence. International Business Research, 8(8), 141.

Apesb.org.au. (2019). APES 110 Code of Ethics for Professional Accountants. Retrieved 1

August 2019, from

https://www.apesb.org.au/uploads/standards/apesb_standards/standardc1.pdf

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Dobler, M. (2014). Auditor-provided non-audit services in listed and private family

firms. Managerial Auditing Journal, 29(5), 427-454.

George-Silviu, C., & Melinda-Timea, F. (2015). New audit reporting challenges: auditing the

going concern basis of accounting. Procedia Economics and Finance, 32, 216-224.

Humphrey, C., Samsonova, A., & Siddiqui, J. (2013). Auditing, regulation and the

persistence of the expectations gap. In The Routledge Companion to Accounting,

Reporting and Regulation (pp. 185-206). Routledge.

J. Clout, V., Chapple, L., & Gandhi, N. (2013). The impact of auditor independence

regulations on established and emerging firms. Accounting Research Journal, 26(2),

88-108.

Tepalagul, N., & Lin, L. (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), 101-121.

8AUDIT

Velte, P., & Freidank, C. C. (2015). The link between in-and external rotation of the auditor

and the quality of financial accounting and external audit. European journal of law

and economics, 40(2), 225-246.

Velte, P., & Freidank, C. C. (2015). The link between in-and external rotation of the auditor

and the quality of financial accounting and external audit. European journal of law

and economics, 40(2), 225-246.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.