Auditing Materiality & New Evidence

VerifiedAdded on 2020/02/24

|14

|3800

|71

AI Summary

This auditing assignment delves into the concept of materiality in financial reporting. It presents a scenario where new purchase documents emerge after the initial audit fieldwork, potentially impacting the auditor's assessment of risk and material misstatement. The student is tasked with analyzing the situation, considering the implications for audit procedures and the overall audit opinion, and applying relevant auditing standards (like ISA 315) to reach a conclusion.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDIT & ASSURANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit & assurance

PART-A

Answer- Part A-1

Before accepting an audit engagement, the auditor should consider a number of conditions

with regard to the client and his business. One of such conditions is that the auditor should

consider the facts that whether or not the client is following all the ethical requirements of

conducting business. While conducting a business, the client should consider the

environmental protection and should not use any such technology in business which is

harmful to the environment (Church et. al, 2008). The client firm and its management team

should not indulge in any act which is unethical or illegal.

In the given case, the company Pharmaceuticals Ltd. is under allegations that the chemicals

from the company’s factory are being emitted into the nearby river and hence is creating

environmental pollution. Before accepting the audit engagement, the auditor should consider

this matter and also that the management is involved in the said matter. The auditor will have

to mention all the points relating to environmental hazards in his report as it shall affect the

public in large (Church et. al, 2008). Hence, before accepting the audit engagement, the

auditor needs to judge whether the allegations on the company are correct or not. He should

also communicate with the previous auditor before taking up the audit.

Answer- Part A-2

In the cases where the auditor finds out errors and weaknesses pertaining to hedging where it

is of high level of risk as given in the case of Pharmaceuticals Ltd., such errors were

discovered in the hedging transactions recording and thereafter no actions were taken by the

management, he needs to take following actions:

i. He should perform procedures that he thinks necessary like checking the

authentication of the entries, reconciling with the evidences to determine whether

or not the errors by the management have resulted into any material misstatement

in the financial statements.

ii. In case the misstatement is not material, then also the impact of the same on the

audit report should be determined by the auditor and if the need arises, he should

performer-assessment procedures to check the same (Gay & Simnet, 2015). This

can be done by going to the history of the entires.

2

PART-A

Answer- Part A-1

Before accepting an audit engagement, the auditor should consider a number of conditions

with regard to the client and his business. One of such conditions is that the auditor should

consider the facts that whether or not the client is following all the ethical requirements of

conducting business. While conducting a business, the client should consider the

environmental protection and should not use any such technology in business which is

harmful to the environment (Church et. al, 2008). The client firm and its management team

should not indulge in any act which is unethical or illegal.

In the given case, the company Pharmaceuticals Ltd. is under allegations that the chemicals

from the company’s factory are being emitted into the nearby river and hence is creating

environmental pollution. Before accepting the audit engagement, the auditor should consider

this matter and also that the management is involved in the said matter. The auditor will have

to mention all the points relating to environmental hazards in his report as it shall affect the

public in large (Church et. al, 2008). Hence, before accepting the audit engagement, the

auditor needs to judge whether the allegations on the company are correct or not. He should

also communicate with the previous auditor before taking up the audit.

Answer- Part A-2

In the cases where the auditor finds out errors and weaknesses pertaining to hedging where it

is of high level of risk as given in the case of Pharmaceuticals Ltd., such errors were

discovered in the hedging transactions recording and thereafter no actions were taken by the

management, he needs to take following actions:

i. He should perform procedures that he thinks necessary like checking the

authentication of the entries, reconciling with the evidences to determine whether

or not the errors by the management have resulted into any material misstatement

in the financial statements.

ii. In case the misstatement is not material, then also the impact of the same on the

audit report should be determined by the auditor and if the need arises, he should

performer-assessment procedures to check the same (Gay & Simnet, 2015). This

can be done by going to the history of the entires.

2

Audit & assurance

iii. He should consider and analyze the information in the financial statements

whether or not the errors may lead to hidden frauds. Any suspect be dealt in a

strong manner and must be provided in the footnote if the management fails to

justify. In case there is any indication of fraud, the auditor needs to consider all

the other aspects of audit as the reliability of management will be under suspicion

in such a situation.

iv. He should in the case of Pharmaceuticals ltd., carry out substantive procedures for

the hedging transactions on a random basis to know the intensity of the errors and

the control weaknesses inherent in the company operations. The auditor shall

deeply study the procedures of hedging transactions of the company as well as the

methods followed to record such transactions.

v. The auditor should be very particular in judging the errors, be it small or large,

due to the given fact that there are weaknesses in the internal control by the

management representatives. Where the internal control of an organization is

weak, the procedures that the auditor performs should be performed with

maximized efforts (Gay & Simnet, 2015).

3

iii. He should consider and analyze the information in the financial statements

whether or not the errors may lead to hidden frauds. Any suspect be dealt in a

strong manner and must be provided in the footnote if the management fails to

justify. In case there is any indication of fraud, the auditor needs to consider all

the other aspects of audit as the reliability of management will be under suspicion

in such a situation.

iv. He should in the case of Pharmaceuticals ltd., carry out substantive procedures for

the hedging transactions on a random basis to know the intensity of the errors and

the control weaknesses inherent in the company operations. The auditor shall

deeply study the procedures of hedging transactions of the company as well as the

methods followed to record such transactions.

v. The auditor should be very particular in judging the errors, be it small or large,

due to the given fact that there are weaknesses in the internal control by the

management representatives. Where the internal control of an organization is

weak, the procedures that the auditor performs should be performed with

maximized efforts (Gay & Simnet, 2015).

3

Audit & assurance

Answer- Part A-3

Billing & Associates have given audit engagement letter to Reaction Pty Ltd. for

conducting an audit of the said company. The company has accepted the engagement

letter and the audit firm has conducted the audit. As the audit team was not able to gain

sufficient audit evidence of accounts receivable due to lack of documentation, it had

decided to issue a modified audit report.

In such as case, if the client is now requesting the audit team to cancel the engagement

letter as an audit and rather issue an engagement letter in its place for review of the

company, this is a clear case of audit limitation been set by the company. The

management of the company is now claiming that the company is not required to get

audited. If there was no requirement of the audit, the company should not have accepted

the audit engagement letter in the very beginning. Claiming of no audit requirement after

the audit has been conducted itself shows that the management is trying to cover up its

flaws of documentation (ACCA, 2016). Once the audit has been conducted, the auditor

shall not withdraw the procedures performed and shall issue the modified audit report

because of the limitations being set on the audit as the auditors were not provided with

sufficient audit evidence

Hence, the audit team shall go ahead with its modified audit report in this case.

Answer- Part A-4

1) The given case is the case of self-review threat of the auditor independence. The

auditor has suggested the client about many adjustments to account for impairment of

assets. The auditor’s responsibility is to present a fair opinion about the financial

statements prepared by the management team and not to guide the management about

how to manage the adjustments in the books of accounts so that he can present a

positive opinion only (Cappelleto, 2010). In such cases, as the auditor has himself told

about the adjustments, he will not be able to review and comment independently on

such adjustments done.

The safeguard to such self-review threat can be that opinion of another professional

shall be taken along with the auditor so that the audit report shall present an unbiased

opinion.

4

Answer- Part A-3

Billing & Associates have given audit engagement letter to Reaction Pty Ltd. for

conducting an audit of the said company. The company has accepted the engagement

letter and the audit firm has conducted the audit. As the audit team was not able to gain

sufficient audit evidence of accounts receivable due to lack of documentation, it had

decided to issue a modified audit report.

In such as case, if the client is now requesting the audit team to cancel the engagement

letter as an audit and rather issue an engagement letter in its place for review of the

company, this is a clear case of audit limitation been set by the company. The

management of the company is now claiming that the company is not required to get

audited. If there was no requirement of the audit, the company should not have accepted

the audit engagement letter in the very beginning. Claiming of no audit requirement after

the audit has been conducted itself shows that the management is trying to cover up its

flaws of documentation (ACCA, 2016). Once the audit has been conducted, the auditor

shall not withdraw the procedures performed and shall issue the modified audit report

because of the limitations being set on the audit as the auditors were not provided with

sufficient audit evidence

Hence, the audit team shall go ahead with its modified audit report in this case.

Answer- Part A-4

1) The given case is the case of self-review threat of the auditor independence. The

auditor has suggested the client about many adjustments to account for impairment of

assets. The auditor’s responsibility is to present a fair opinion about the financial

statements prepared by the management team and not to guide the management about

how to manage the adjustments in the books of accounts so that he can present a

positive opinion only (Cappelleto, 2010). In such cases, as the auditor has himself told

about the adjustments, he will not be able to review and comment independently on

such adjustments done.

The safeguard to such self-review threat can be that opinion of another professional

shall be taken along with the auditor so that the audit report shall present an unbiased

opinion.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit & assurance

2) This is a case of self-interest threat as the auditors may be afraid that if they do not

recommend the client’s travel services, the audit firm may lose their client. Here the

client has requested the auditors to give recommendations for travel services provided

by the client firm.

The safeguard is that the auditors should be in a total professional relationship with

the client and shall not undertake any work for the client. If the client initiates any

pressure, the audit firm should leave the engagement so that the auditor’s

independence is not questioned.

3) In this case, there is a familiarity threat to auditor independence as the wife of one of

the auditor has a substantial shareholding in the client company. Familiarity threat

occurs when the auditor becomes very sympathetic to the interest of the clients due to

the reason of close relationship with the client (Philomena, 2015).

The safeguard can be to involve another chartered accountant outside the audit team

to review the work done and monitoring the work of auditor having interest in the

client firm.

4) This is a case of intimidation threat as the auditors are not sure whether or not they

will receive their fees. Although the client has not directly threatened the auditor for

non-payment of fees the same is implied (Philomena, 2015).

The safeguard is that the auditor shall first demand their fees prior to issuing the

report as there is a risk that their fees may remain unpaid once the report is issued in

the hands of the client (Philomena, 2015).

5

2) This is a case of self-interest threat as the auditors may be afraid that if they do not

recommend the client’s travel services, the audit firm may lose their client. Here the

client has requested the auditors to give recommendations for travel services provided

by the client firm.

The safeguard is that the auditors should be in a total professional relationship with

the client and shall not undertake any work for the client. If the client initiates any

pressure, the audit firm should leave the engagement so that the auditor’s

independence is not questioned.

3) In this case, there is a familiarity threat to auditor independence as the wife of one of

the auditor has a substantial shareholding in the client company. Familiarity threat

occurs when the auditor becomes very sympathetic to the interest of the clients due to

the reason of close relationship with the client (Philomena, 2015).

The safeguard can be to involve another chartered accountant outside the audit team

to review the work done and monitoring the work of auditor having interest in the

client firm.

4) This is a case of intimidation threat as the auditors are not sure whether or not they

will receive their fees. Although the client has not directly threatened the auditor for

non-payment of fees the same is implied (Philomena, 2015).

The safeguard is that the auditor shall first demand their fees prior to issuing the

report as there is a risk that their fees may remain unpaid once the report is issued in

the hands of the client (Philomena, 2015).

5

Audit & assurance

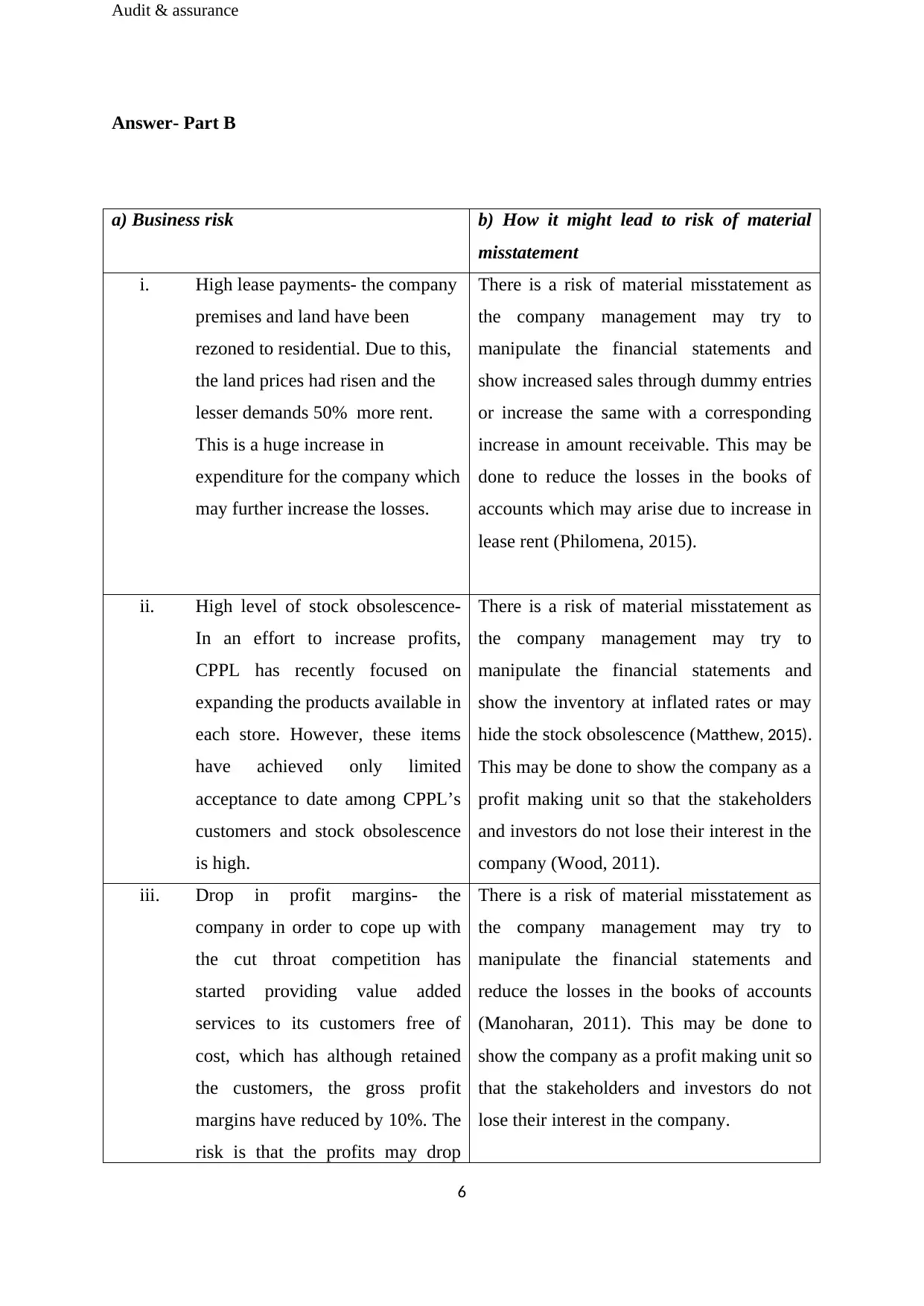

Answer- Part B

a) Business risk b) How it might lead to risk of material

misstatement

i. High lease payments- the company

premises and land have been

rezoned to residential. Due to this,

the land prices had risen and the

lesser demands 50% more rent.

This is a huge increase in

expenditure for the company which

may further increase the losses.

There is a risk of material misstatement as

the company management may try to

manipulate the financial statements and

show increased sales through dummy entries

or increase the same with a corresponding

increase in amount receivable. This may be

done to reduce the losses in the books of

accounts which may arise due to increase in

lease rent (Philomena, 2015).

ii. High level of stock obsolescence-

In an effort to increase profits,

CPPL has recently focused on

expanding the products available in

each store. However, these items

have achieved only limited

acceptance to date among CPPL’s

customers and stock obsolescence

is high.

There is a risk of material misstatement as

the company management may try to

manipulate the financial statements and

show the inventory at inflated rates or may

hide the stock obsolescence (Matthew, 2015).

This may be done to show the company as a

profit making unit so that the stakeholders

and investors do not lose their interest in the

company (Wood, 2011).

iii. Drop in profit margins- the

company in order to cope up with

the cut throat competition has

started providing value added

services to its customers free of

cost, which has although retained

the customers, the gross profit

margins have reduced by 10%. The

risk is that the profits may drop

There is a risk of material misstatement as

the company management may try to

manipulate the financial statements and

reduce the losses in the books of accounts

(Manoharan, 2011). This may be done to

show the company as a profit making unit so

that the stakeholders and investors do not

lose their interest in the company.

6

Answer- Part B

a) Business risk b) How it might lead to risk of material

misstatement

i. High lease payments- the company

premises and land have been

rezoned to residential. Due to this,

the land prices had risen and the

lesser demands 50% more rent.

This is a huge increase in

expenditure for the company which

may further increase the losses.

There is a risk of material misstatement as

the company management may try to

manipulate the financial statements and

show increased sales through dummy entries

or increase the same with a corresponding

increase in amount receivable. This may be

done to reduce the losses in the books of

accounts which may arise due to increase in

lease rent (Philomena, 2015).

ii. High level of stock obsolescence-

In an effort to increase profits,

CPPL has recently focused on

expanding the products available in

each store. However, these items

have achieved only limited

acceptance to date among CPPL’s

customers and stock obsolescence

is high.

There is a risk of material misstatement as

the company management may try to

manipulate the financial statements and

show the inventory at inflated rates or may

hide the stock obsolescence (Matthew, 2015).

This may be done to show the company as a

profit making unit so that the stakeholders

and investors do not lose their interest in the

company (Wood, 2011).

iii. Drop in profit margins- the

company in order to cope up with

the cut throat competition has

started providing value added

services to its customers free of

cost, which has although retained

the customers, the gross profit

margins have reduced by 10%. The

risk is that the profits may drop

There is a risk of material misstatement as

the company management may try to

manipulate the financial statements and

reduce the losses in the books of accounts

(Manoharan, 2011). This may be done to

show the company as a profit making unit so

that the stakeholders and investors do not

lose their interest in the company.

6

Audit & assurance

down more if such free services are

continued in future.

iv. Constraint on the availability of

credit- CPPL is also experiencing

difficulties with two of its major

suppliers, who have withdrawn

their volume rebates and reduced

payment terms from 30 to 14 days.

There is a risk of material misstatement as

the company management may try to

manipulate the financial statements and

show increased cash sales in the books of

accounts so that cash may be available on

the books to pay off the creditors as the

creditors have reduced credit period (Livne,

2015).

v. High level of Competition- there is

an intense competition in the sector

in which the company operates and

the major supermarket chains are

aggressively purchasing smaller

rivals and discounting products

below cost in order to increase

market share.

The company may have to increase

discounts in order to cope up with the

market competition this shall increase the

expenditure. There may be a possibility that

the management may show the heavy

discounts as bad debts or debts

unrecoverable (Hoffelder, 2012).

Answer- Part –C

(a)Deficiency in

internal

control

Explanation of

business risk arising

due to deficiency in

internal control

(b)Control (c )Test of Control

i. The deficiency in

internal control is

that the website of

the company is

not integrated into

the inventory

system and

The orders received

through the

customers are not

directly linked with

the inventory system

which may result in a

loss to the company

ERP system should

be adopted and

linking should be

done between

inventory system

and order placing so

that when a

The auditors can

assess the control

level by checking

through a dummy

order placing that is a

dummy order will be

placed and then it

7

down more if such free services are

continued in future.

iv. Constraint on the availability of

credit- CPPL is also experiencing

difficulties with two of its major

suppliers, who have withdrawn

their volume rebates and reduced

payment terms from 30 to 14 days.

There is a risk of material misstatement as

the company management may try to

manipulate the financial statements and

show increased cash sales in the books of

accounts so that cash may be available on

the books to pay off the creditors as the

creditors have reduced credit period (Livne,

2015).

v. High level of Competition- there is

an intense competition in the sector

in which the company operates and

the major supermarket chains are

aggressively purchasing smaller

rivals and discounting products

below cost in order to increase

market share.

The company may have to increase

discounts in order to cope up with the

market competition this shall increase the

expenditure. There may be a possibility that

the management may show the heavy

discounts as bad debts or debts

unrecoverable (Hoffelder, 2012).

Answer- Part –C

(a)Deficiency in

internal

control

Explanation of

business risk arising

due to deficiency in

internal control

(b)Control (c )Test of Control

i. The deficiency in

internal control is

that the website of

the company is

not integrated into

the inventory

system and

The orders received

through the

customers are not

directly linked with

the inventory system

which may result in a

loss to the company

ERP system should

be adopted and

linking should be

done between

inventory system

and order placing so

that when a

The auditors can

assess the control

level by checking

through a dummy

order placing that is a

dummy order will be

placed and then it

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit & assurance

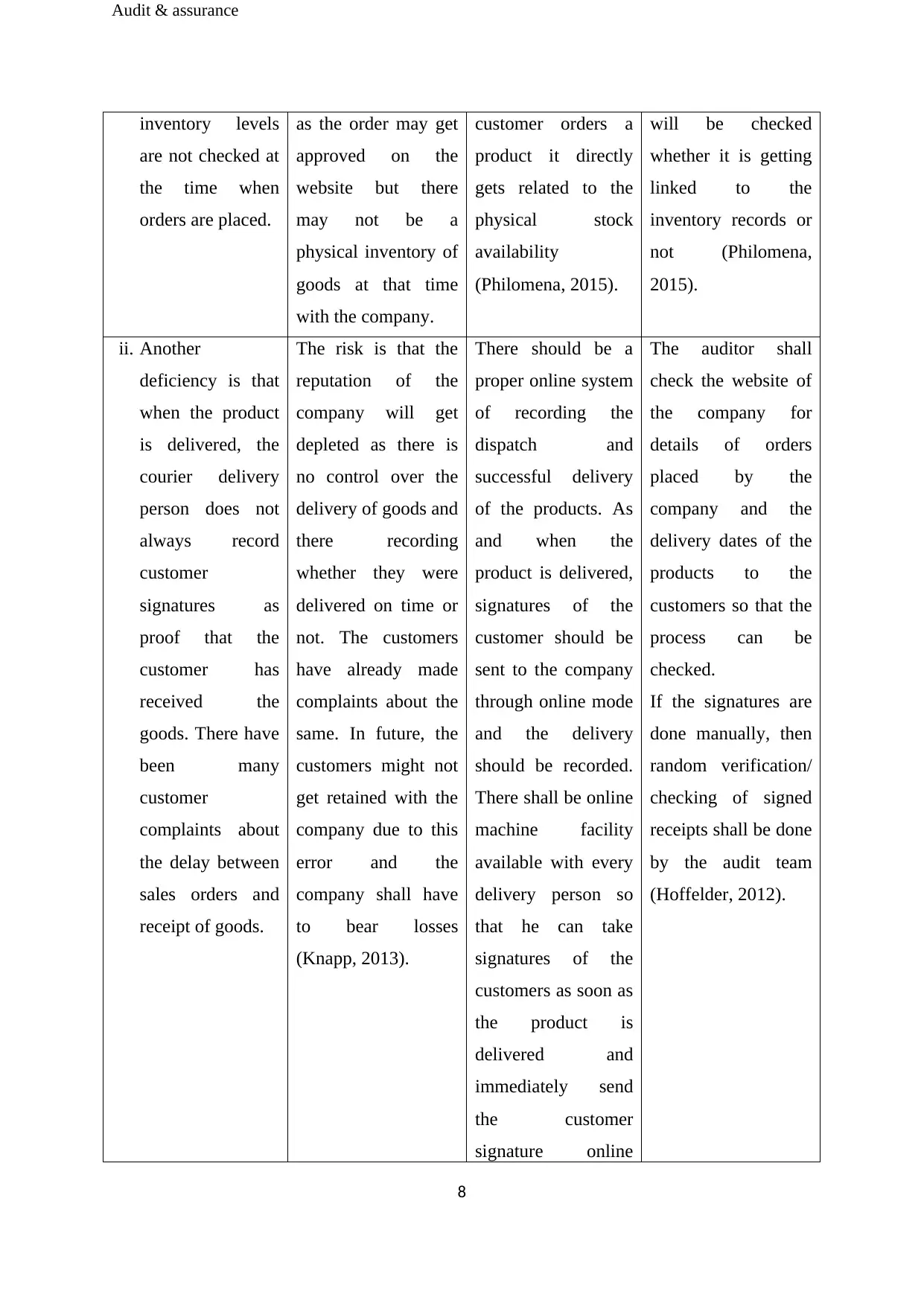

inventory levels

are not checked at

the time when

orders are placed.

as the order may get

approved on the

website but there

may not be a

physical inventory of

goods at that time

with the company.

customer orders a

product it directly

gets related to the

physical stock

availability

(Philomena, 2015).

will be checked

whether it is getting

linked to the

inventory records or

not (Philomena,

2015).

ii. Another

deficiency is that

when the product

is delivered, the

courier delivery

person does not

always record

customer

signatures as

proof that the

customer has

received the

goods. There have

been many

customer

complaints about

the delay between

sales orders and

receipt of goods.

The risk is that the

reputation of the

company will get

depleted as there is

no control over the

delivery of goods and

there recording

whether they were

delivered on time or

not. The customers

have already made

complaints about the

same. In future, the

customers might not

get retained with the

company due to this

error and the

company shall have

to bear losses

(Knapp, 2013).

There should be a

proper online system

of recording the

dispatch and

successful delivery

of the products. As

and when the

product is delivered,

signatures of the

customer should be

sent to the company

through online mode

and the delivery

should be recorded.

There shall be online

machine facility

available with every

delivery person so

that he can take

signatures of the

customers as soon as

the product is

delivered and

immediately send

the customer

signature online

The auditor shall

check the website of

the company for

details of orders

placed by the

company and the

delivery dates of the

products to the

customers so that the

process can be

checked.

If the signatures are

done manually, then

random verification/

checking of signed

receipts shall be done

by the audit team

(Hoffelder, 2012).

8

inventory levels

are not checked at

the time when

orders are placed.

as the order may get

approved on the

website but there

may not be a

physical inventory of

goods at that time

with the company.

customer orders a

product it directly

gets related to the

physical stock

availability

(Philomena, 2015).

will be checked

whether it is getting

linked to the

inventory records or

not (Philomena,

2015).

ii. Another

deficiency is that

when the product

is delivered, the

courier delivery

person does not

always record

customer

signatures as

proof that the

customer has

received the

goods. There have

been many

customer

complaints about

the delay between

sales orders and

receipt of goods.

The risk is that the

reputation of the

company will get

depleted as there is

no control over the

delivery of goods and

there recording

whether they were

delivered on time or

not. The customers

have already made

complaints about the

same. In future, the

customers might not

get retained with the

company due to this

error and the

company shall have

to bear losses

(Knapp, 2013).

There should be a

proper online system

of recording the

dispatch and

successful delivery

of the products. As

and when the

product is delivered,

signatures of the

customer should be

sent to the company

through online mode

and the delivery

should be recorded.

There shall be online

machine facility

available with every

delivery person so

that he can take

signatures of the

customers as soon as

the product is

delivered and

immediately send

the customer

signature online

The auditor shall

check the website of

the company for

details of orders

placed by the

company and the

delivery dates of the

products to the

customers so that the

process can be

checked.

If the signatures are

done manually, then

random verification/

checking of signed

receipts shall be done

by the audit team

(Hoffelder, 2012).

8

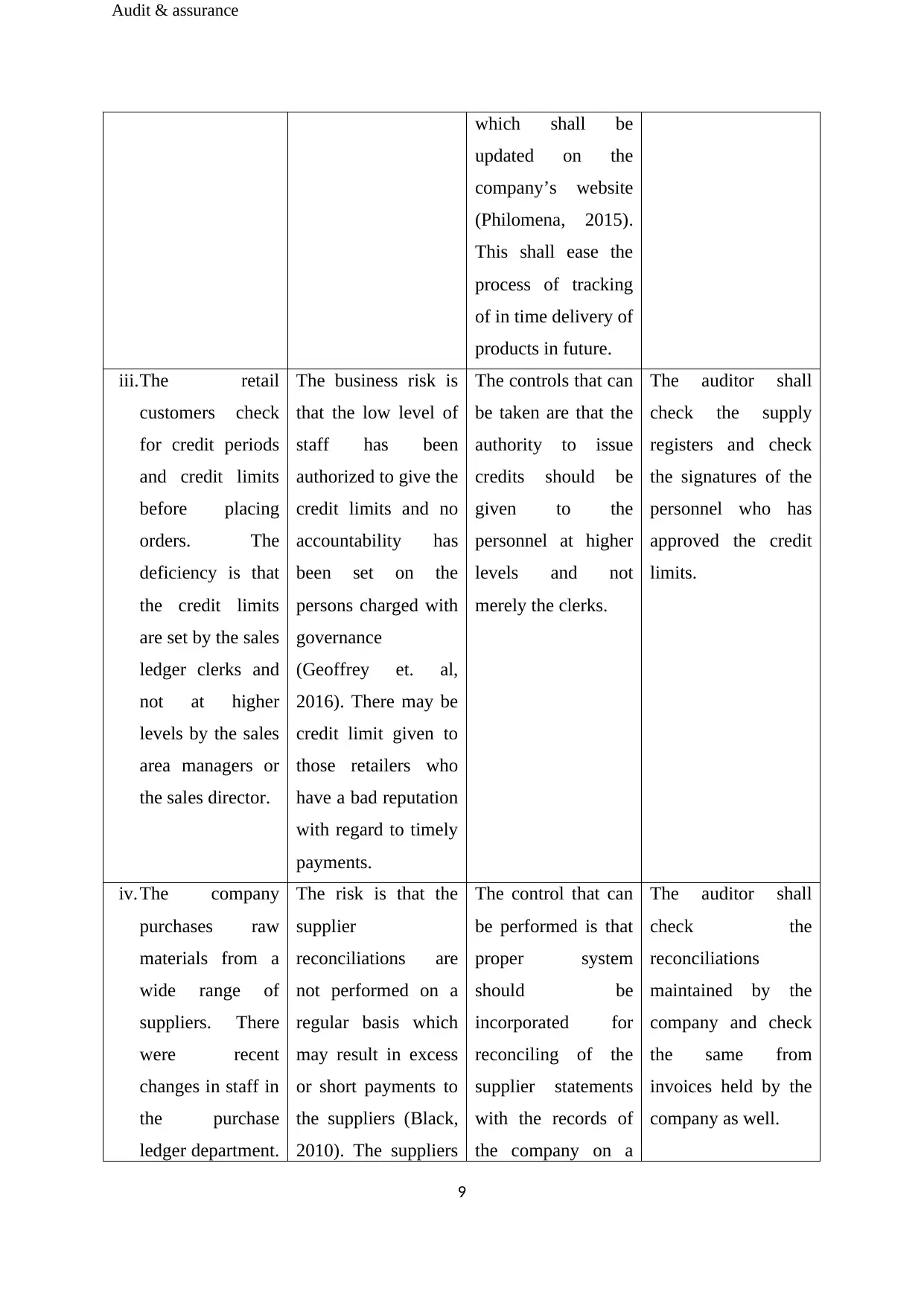

Audit & assurance

which shall be

updated on the

company’s website

(Philomena, 2015).

This shall ease the

process of tracking

of in time delivery of

products in future.

iii.The retail

customers check

for credit periods

and credit limits

before placing

orders. The

deficiency is that

the credit limits

are set by the sales

ledger clerks and

not at higher

levels by the sales

area managers or

the sales director.

The business risk is

that the low level of

staff has been

authorized to give the

credit limits and no

accountability has

been set on the

persons charged with

governance

(Geoffrey et. al,

2016). There may be

credit limit given to

those retailers who

have a bad reputation

with regard to timely

payments.

The controls that can

be taken are that the

authority to issue

credits should be

given to the

personnel at higher

levels and not

merely the clerks.

The auditor shall

check the supply

registers and check

the signatures of the

personnel who has

approved the credit

limits.

iv.The company

purchases raw

materials from a

wide range of

suppliers. There

were recent

changes in staff in

the purchase

ledger department.

The risk is that the

supplier

reconciliations are

not performed on a

regular basis which

may result in excess

or short payments to

the suppliers (Black,

2010). The suppliers

The control that can

be performed is that

proper system

should be

incorporated for

reconciling of the

supplier statements

with the records of

the company on a

The auditor shall

check the

reconciliations

maintained by the

company and check

the same from

invoices held by the

company as well.

9

which shall be

updated on the

company’s website

(Philomena, 2015).

This shall ease the

process of tracking

of in time delivery of

products in future.

iii.The retail

customers check

for credit periods

and credit limits

before placing

orders. The

deficiency is that

the credit limits

are set by the sales

ledger clerks and

not at higher

levels by the sales

area managers or

the sales director.

The business risk is

that the low level of

staff has been

authorized to give the

credit limits and no

accountability has

been set on the

persons charged with

governance

(Geoffrey et. al,

2016). There may be

credit limit given to

those retailers who

have a bad reputation

with regard to timely

payments.

The controls that can

be taken are that the

authority to issue

credits should be

given to the

personnel at higher

levels and not

merely the clerks.

The auditor shall

check the supply

registers and check

the signatures of the

personnel who has

approved the credit

limits.

iv.The company

purchases raw

materials from a

wide range of

suppliers. There

were recent

changes in staff in

the purchase

ledger department.

The risk is that the

supplier

reconciliations are

not performed on a

regular basis which

may result in excess

or short payments to

the suppliers (Black,

2010). The suppliers

The control that can

be performed is that

proper system

should be

incorporated for

reconciling of the

supplier statements

with the records of

the company on a

The auditor shall

check the

reconciliations

maintained by the

company and check

the same from

invoices held by the

company as well.

9

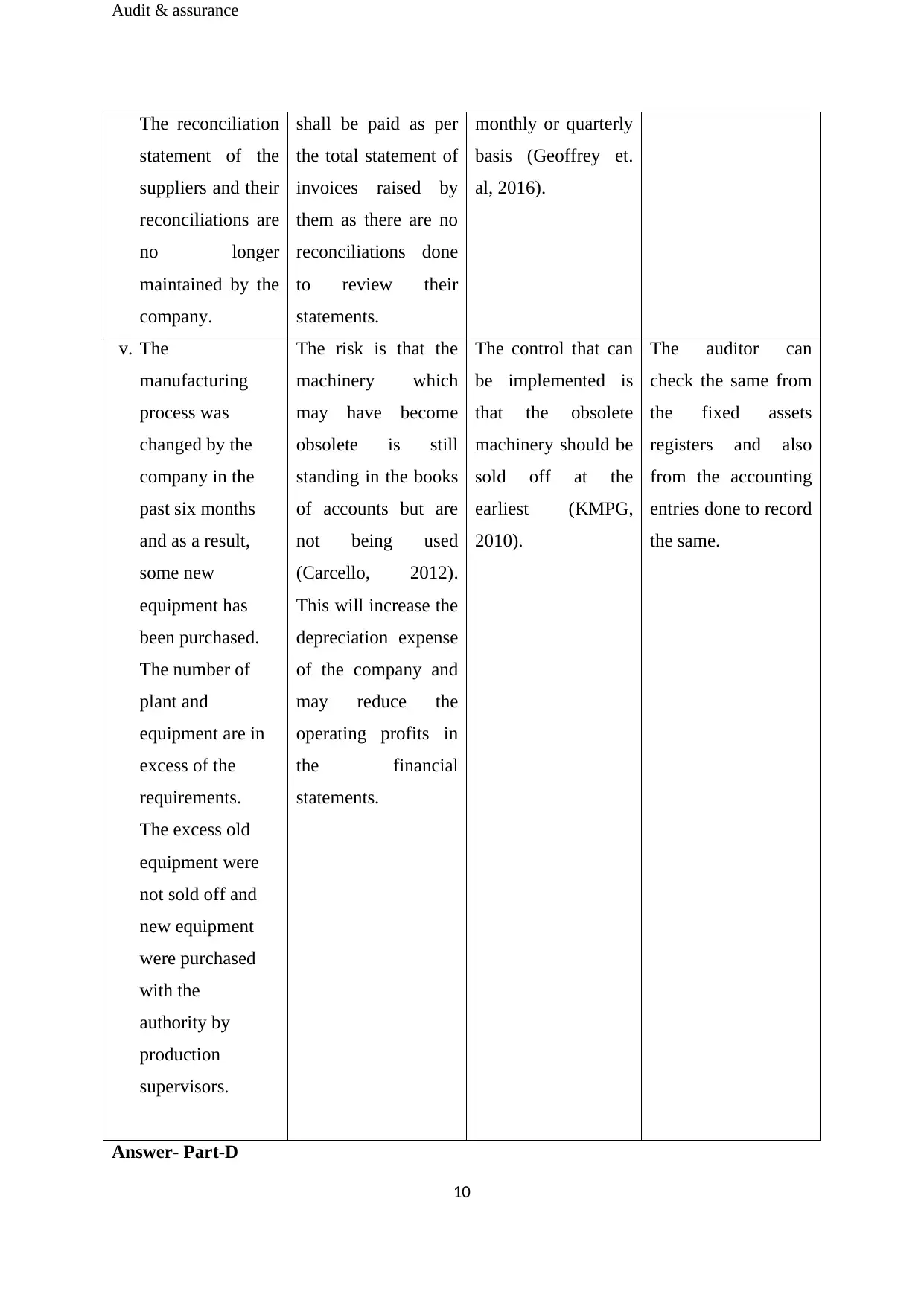

Audit & assurance

The reconciliation

statement of the

suppliers and their

reconciliations are

no longer

maintained by the

company.

shall be paid as per

the total statement of

invoices raised by

them as there are no

reconciliations done

to review their

statements.

monthly or quarterly

basis (Geoffrey et.

al, 2016).

v. The

manufacturing

process was

changed by the

company in the

past six months

and as a result,

some new

equipment has

been purchased.

The number of

plant and

equipment are in

excess of the

requirements.

The excess old

equipment were

not sold off and

new equipment

were purchased

with the

authority by

production

supervisors.

The risk is that the

machinery which

may have become

obsolete is still

standing in the books

of accounts but are

not being used

(Carcello, 2012).

This will increase the

depreciation expense

of the company and

may reduce the

operating profits in

the financial

statements.

The control that can

be implemented is

that the obsolete

machinery should be

sold off at the

earliest (KMPG,

2010).

The auditor can

check the same from

the fixed assets

registers and also

from the accounting

entries done to record

the same.

Answer- Part-D

10

The reconciliation

statement of the

suppliers and their

reconciliations are

no longer

maintained by the

company.

shall be paid as per

the total statement of

invoices raised by

them as there are no

reconciliations done

to review their

statements.

monthly or quarterly

basis (Geoffrey et.

al, 2016).

v. The

manufacturing

process was

changed by the

company in the

past six months

and as a result,

some new

equipment has

been purchased.

The number of

plant and

equipment are in

excess of the

requirements.

The excess old

equipment were

not sold off and

new equipment

were purchased

with the

authority by

production

supervisors.

The risk is that the

machinery which

may have become

obsolete is still

standing in the books

of accounts but are

not being used

(Carcello, 2012).

This will increase the

depreciation expense

of the company and

may reduce the

operating profits in

the financial

statements.

The control that can

be implemented is

that the obsolete

machinery should be

sold off at the

earliest (KMPG,

2010).

The auditor can

check the same from

the fixed assets

registers and also

from the accounting

entries done to record

the same.

Answer- Part-D

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit & assurance

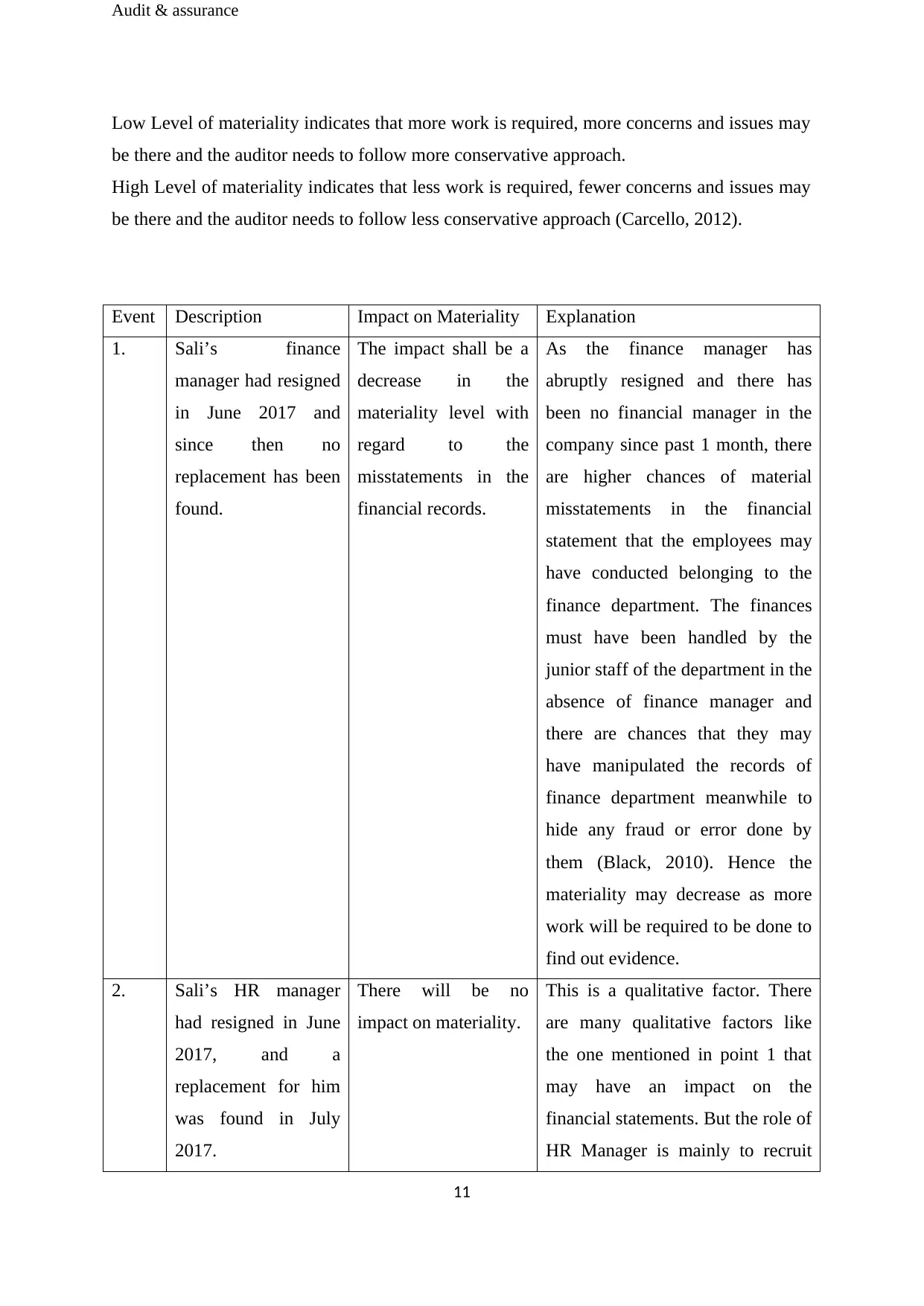

Low Level of materiality indicates that more work is required, more concerns and issues may

be there and the auditor needs to follow more conservative approach.

High Level of materiality indicates that less work is required, fewer concerns and issues may

be there and the auditor needs to follow less conservative approach (Carcello, 2012).

Event Description Impact on Materiality Explanation

1. Sali’s finance

manager had resigned

in June 2017 and

since then no

replacement has been

found.

The impact shall be a

decrease in the

materiality level with

regard to the

misstatements in the

financial records.

As the finance manager has

abruptly resigned and there has

been no financial manager in the

company since past 1 month, there

are higher chances of material

misstatements in the financial

statement that the employees may

have conducted belonging to the

finance department. The finances

must have been handled by the

junior staff of the department in the

absence of finance manager and

there are chances that they may

have manipulated the records of

finance department meanwhile to

hide any fraud or error done by

them (Black, 2010). Hence the

materiality may decrease as more

work will be required to be done to

find out evidence.

2. Sali’s HR manager

had resigned in June

2017, and a

replacement for him

was found in July

2017.

There will be no

impact on materiality.

This is a qualitative factor. There

are many qualitative factors like

the one mentioned in point 1 that

may have an impact on the

financial statements. But the role of

HR Manager is mainly to recruit

11

Low Level of materiality indicates that more work is required, more concerns and issues may

be there and the auditor needs to follow more conservative approach.

High Level of materiality indicates that less work is required, fewer concerns and issues may

be there and the auditor needs to follow less conservative approach (Carcello, 2012).

Event Description Impact on Materiality Explanation

1. Sali’s finance

manager had resigned

in June 2017 and

since then no

replacement has been

found.

The impact shall be a

decrease in the

materiality level with

regard to the

misstatements in the

financial records.

As the finance manager has

abruptly resigned and there has

been no financial manager in the

company since past 1 month, there

are higher chances of material

misstatements in the financial

statement that the employees may

have conducted belonging to the

finance department. The finances

must have been handled by the

junior staff of the department in the

absence of finance manager and

there are chances that they may

have manipulated the records of

finance department meanwhile to

hide any fraud or error done by

them (Black, 2010). Hence the

materiality may decrease as more

work will be required to be done to

find out evidence.

2. Sali’s HR manager

had resigned in June

2017, and a

replacement for him

was found in July

2017.

There will be no

impact on materiality.

This is a qualitative factor. There

are many qualitative factors like

the one mentioned in point 1 that

may have an impact on the

financial statements. But the role of

HR Manager is mainly to recruit

11

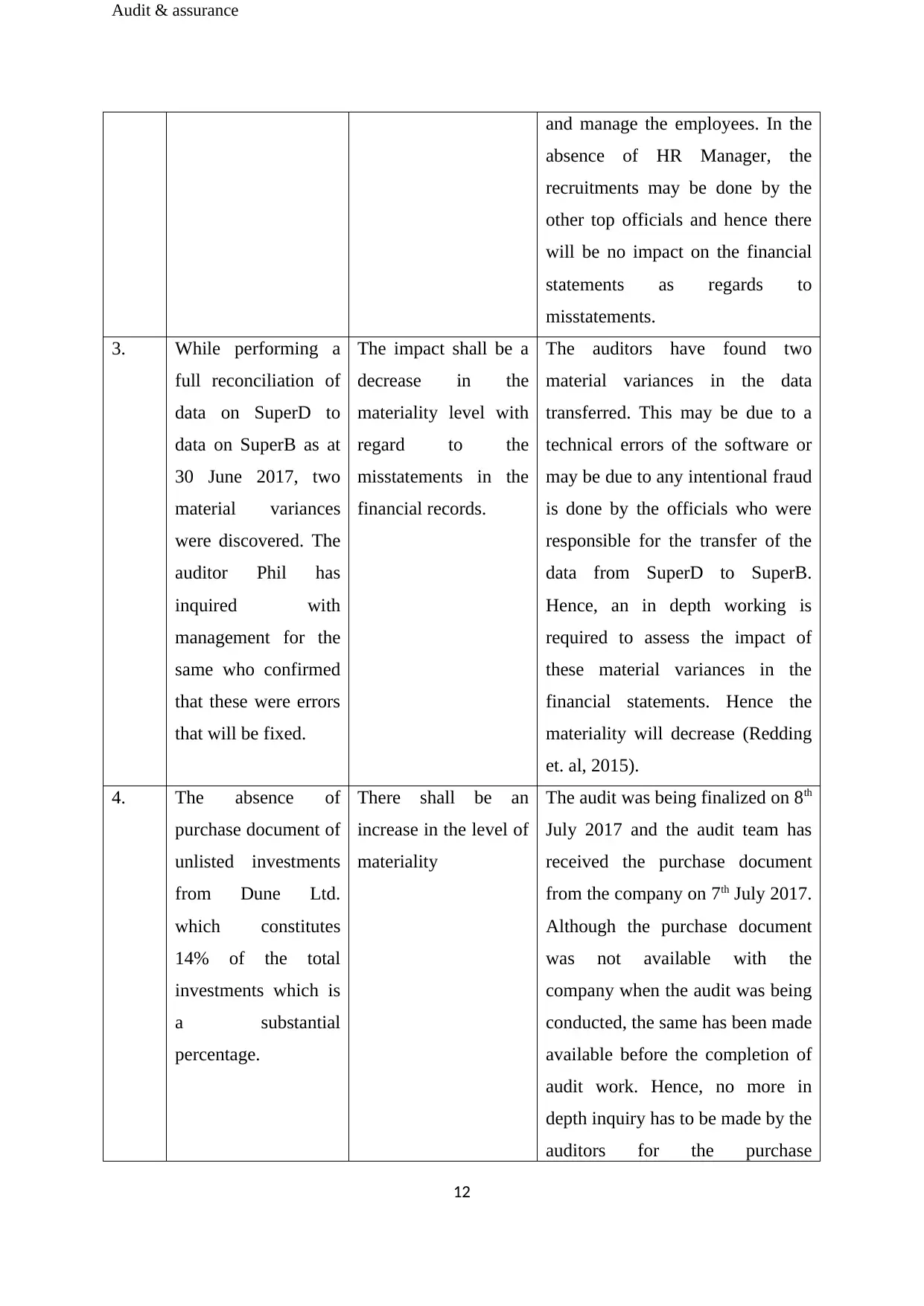

Audit & assurance

and manage the employees. In the

absence of HR Manager, the

recruitments may be done by the

other top officials and hence there

will be no impact on the financial

statements as regards to

misstatements.

3. While performing a

full reconciliation of

data on SuperD to

data on SuperB as at

30 June 2017, two

material variances

were discovered. The

auditor Phil has

inquired with

management for the

same who confirmed

that these were errors

that will be fixed.

The impact shall be a

decrease in the

materiality level with

regard to the

misstatements in the

financial records.

The auditors have found two

material variances in the data

transferred. This may be due to a

technical errors of the software or

may be due to any intentional fraud

is done by the officials who were

responsible for the transfer of the

data from SuperD to SuperB.

Hence, an in depth working is

required to assess the impact of

these material variances in the

financial statements. Hence the

materiality will decrease (Redding

et. al, 2015).

4. The absence of

purchase document of

unlisted investments

from Dune Ltd.

which constitutes

14% of the total

investments which is

a substantial

percentage.

There shall be an

increase in the level of

materiality

The audit was being finalized on 8th

July 2017 and the audit team has

received the purchase document

from the company on 7th July 2017.

Although the purchase document

was not available with the

company when the audit was being

conducted, the same has been made

available before the completion of

audit work. Hence, no more in

depth inquiry has to be made by the

auditors for the purchase

12

and manage the employees. In the

absence of HR Manager, the

recruitments may be done by the

other top officials and hence there

will be no impact on the financial

statements as regards to

misstatements.

3. While performing a

full reconciliation of

data on SuperD to

data on SuperB as at

30 June 2017, two

material variances

were discovered. The

auditor Phil has

inquired with

management for the

same who confirmed

that these were errors

that will be fixed.

The impact shall be a

decrease in the

materiality level with

regard to the

misstatements in the

financial records.

The auditors have found two

material variances in the data

transferred. This may be due to a

technical errors of the software or

may be due to any intentional fraud

is done by the officials who were

responsible for the transfer of the

data from SuperD to SuperB.

Hence, an in depth working is

required to assess the impact of

these material variances in the

financial statements. Hence the

materiality will decrease (Redding

et. al, 2015).

4. The absence of

purchase document of

unlisted investments

from Dune Ltd.

which constitutes

14% of the total

investments which is

a substantial

percentage.

There shall be an

increase in the level of

materiality

The audit was being finalized on 8th

July 2017 and the audit team has

received the purchase document

from the company on 7th July 2017.

Although the purchase document

was not available with the

company when the audit was being

conducted, the same has been made

available before the completion of

audit work. Hence, no more in

depth inquiry has to be made by the

auditors for the purchase

12

Audit & assurance

documents (Reding et. al, 2015).

So the materiality shall not

decrease.

13

documents (Reding et. al, 2015).

So the materiality shall not

decrease.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit & assurance

References

ACCA 2016, Assessing the risk of material misstatement, viewed 12 September 2017

http://www.accaglobal.com/uk/en/discover/cpd-articles/audit-assurance/material-

misstatement.html

Black, W. K 2010, Epidemics of “Control Fraud” lead to Recurrent, Intensifying Bubbles and

Crises, Working paper, University of Missouri-Kansas City.

Cappelleto, G 2010, Challenges Facing Accounting Education in Australia, AFAANZ,

Melbourne

Carcello, J 2012, ‘What do investors want from the standard audit report?’, CPA Journal

vol.82, no. 1, pp. 7-12

Church, B, Davis, S & McCracken, S 2008, ‘The auditor’s reporting model: A literature

overview and research synthesis’, Accounting Horizons vol. 22, no. 1, pp. 69-90.

Gay, G & Simnet, R 2015, Auditing and Assurance Services, McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S & David A. W 2016, ‘Attracting Applicants for In-House

and Outsourced Internal Audit Positions: Views from External Auditors’, Accounting

Horizons, vol. 30, no. 1, pp. 143-156.

Hoffelder, K 2012, New Audit Standard Encourages More Talking, Harvard Press.

KMPG 2010, An overview of Risk and disclosure, viewed 12 September 2017

https://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/Documents/KPMG-

pharmaceuticals-disclosures-summary.pdf

Knapp, M.C 2013, Contemporary Accounting, Cengage Learning

Livne, G 2015, Threats to Auditor Independence and Possible Remedies, viewed 12 September

2017 http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full.

Manoharan, T.N. 2011, Financial Statement Fraud and Corporate Governance, The George

Washington University.

Matthew S. E 2015, ‘ Does Internal Audit Function Quality Deter Management Misconduct?’,

The Accounting Review, vol. 90, no. 2, pp. 495-527

14

References

ACCA 2016, Assessing the risk of material misstatement, viewed 12 September 2017

http://www.accaglobal.com/uk/en/discover/cpd-articles/audit-assurance/material-

misstatement.html

Black, W. K 2010, Epidemics of “Control Fraud” lead to Recurrent, Intensifying Bubbles and

Crises, Working paper, University of Missouri-Kansas City.

Cappelleto, G 2010, Challenges Facing Accounting Education in Australia, AFAANZ,

Melbourne

Carcello, J 2012, ‘What do investors want from the standard audit report?’, CPA Journal

vol.82, no. 1, pp. 7-12

Church, B, Davis, S & McCracken, S 2008, ‘The auditor’s reporting model: A literature

overview and research synthesis’, Accounting Horizons vol. 22, no. 1, pp. 69-90.

Gay, G & Simnet, R 2015, Auditing and Assurance Services, McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S & David A. W 2016, ‘Attracting Applicants for In-House

and Outsourced Internal Audit Positions: Views from External Auditors’, Accounting

Horizons, vol. 30, no. 1, pp. 143-156.

Hoffelder, K 2012, New Audit Standard Encourages More Talking, Harvard Press.

KMPG 2010, An overview of Risk and disclosure, viewed 12 September 2017

https://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/Documents/KPMG-

pharmaceuticals-disclosures-summary.pdf

Knapp, M.C 2013, Contemporary Accounting, Cengage Learning

Livne, G 2015, Threats to Auditor Independence and Possible Remedies, viewed 12 September

2017 http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full.

Manoharan, T.N. 2011, Financial Statement Fraud and Corporate Governance, The George

Washington University.

Matthew S. E 2015, ‘ Does Internal Audit Function Quality Deter Management Misconduct?’,

The Accounting Review, vol. 90, no. 2, pp. 495-527

14

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.