Audit Planning and Control: Trunkey Creek Wines Limited

VerifiedAdded on 2023/06/08

|15

|3394

|135

AI Summary

This report emphasizes the importance of audit planning and control for Trunkey Creek Wines Limited. It includes ratio analysis, business risks, and internal control mechanisms.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

Auditing & Assurance

Services

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

Auditing & Assurance

Services

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit control

Executive Summary

An organization can function smoothly when the audit procedure is well defined and meets

the standards. Hence, it is vital for the organization to have strong audit techniques followed

by an effective internal control mechanism that helps to steer the business. In this report, the

major emphasis is on the audit planning of Trunkey Creek Wines Limited for the year ended

30 June 2018. The audit planning is done by Miller Yates Howarth (MYH), an accounting

firm and the second largest regional accounting firm in Australia. The report proceeds with

the evaluation part where the computation of the ratio is done for the accounts that are listed

by the audit partners and it is followed by the evaluation, audit risk, and audit steps to lessen

the risk. Apart from ratio computation, additional information is procured to assess the

business risk that is faced by Trunkey Creek Wines (TCW). Further, another part deals with

the control mechanism, risk control, and test control is projected in a tabular format.

Moreover, the weakness in the internal control is highlighted for the contract payroll.

2

Executive Summary

An organization can function smoothly when the audit procedure is well defined and meets

the standards. Hence, it is vital for the organization to have strong audit techniques followed

by an effective internal control mechanism that helps to steer the business. In this report, the

major emphasis is on the audit planning of Trunkey Creek Wines Limited for the year ended

30 June 2018. The audit planning is done by Miller Yates Howarth (MYH), an accounting

firm and the second largest regional accounting firm in Australia. The report proceeds with

the evaluation part where the computation of the ratio is done for the accounts that are listed

by the audit partners and it is followed by the evaluation, audit risk, and audit steps to lessen

the risk. Apart from ratio computation, additional information is procured to assess the

business risk that is faced by Trunkey Creek Wines (TCW). Further, another part deals with

the control mechanism, risk control, and test control is projected in a tabular format.

Moreover, the weakness in the internal control is highlighted for the contract payroll.

2

Audit control

Contents

ntroductionI .............................................................................................................................................3

A Ratio Analysis1 - ...................................................................................................................................3

usiness risks that C is likely to face1 B - B TW .........................................................................................7

A nternal Control2 – I .............................................................................................................................8

b ustification of the weakness in nternal control2 – J I ................................................................................10

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

3

Contents

ntroductionI .............................................................................................................................................3

A Ratio Analysis1 - ...................................................................................................................................3

usiness risks that C is likely to face1 B - B TW .........................................................................................7

A nternal Control2 – I .............................................................................................................................8

b ustification of the weakness in nternal control2 – J I ................................................................................10

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

3

Audit control

Introduction

Audit planning and control can be said to be the major tool for the company in terms of risk

assessment and evaluation. In this report, the major emphasis is on the auditing tool and

techniques. Further in the report, the demonstration of risk management methodologies

together with the role of internal control will be done. Moreover, an audit plan will be

designed and audit procedure will be conducted for the financial statement audit. In the light

of the case, ethical practice will be highlighted and the same will be put to discussion. In

short, development of a strong series of audit steps will be developed to evaluate the

importance of internal control.

1A- Ratio Analysis

Audit planning in Trunkey Creek Wines (TCW)

The report stresses upon the major domains like ratio evaluation, as well as risks pertaining to

the business that helps in conducting the company’s audit plan. Further, the efficiency in the

internal control together with the pitfalls pertaining to the case needs to be discussed.

As per the information provided about the company, following is the analysis of the ratios

and the potential audit risks associated:

Account Analysis Audit Risk Audit Steps to

reduce risks

Accounts Receivable The number of days

of collection of debts

has increased

substantially in the

year 2018 in

comparison to the

year 2017 and year

2018.

The bad debts or

uncollectible debts

can show a false

impression of the

company’s

performance. The

aging of debtors can

be misled by the

company as well.

The aging register of

the debtors should be

verified by the

auditors.

The bad debts should

be cross-checked

with the allowances

for bad debts as

approved by the

4

Introduction

Audit planning and control can be said to be the major tool for the company in terms of risk

assessment and evaluation. In this report, the major emphasis is on the auditing tool and

techniques. Further in the report, the demonstration of risk management methodologies

together with the role of internal control will be done. Moreover, an audit plan will be

designed and audit procedure will be conducted for the financial statement audit. In the light

of the case, ethical practice will be highlighted and the same will be put to discussion. In

short, development of a strong series of audit steps will be developed to evaluate the

importance of internal control.

1A- Ratio Analysis

Audit planning in Trunkey Creek Wines (TCW)

The report stresses upon the major domains like ratio evaluation, as well as risks pertaining to

the business that helps in conducting the company’s audit plan. Further, the efficiency in the

internal control together with the pitfalls pertaining to the case needs to be discussed.

As per the information provided about the company, following is the analysis of the ratios

and the potential audit risks associated:

Account Analysis Audit Risk Audit Steps to

reduce risks

Accounts Receivable The number of days

of collection of debts

has increased

substantially in the

year 2018 in

comparison to the

year 2017 and year

2018.

The bad debts or

uncollectible debts

can show a false

impression of the

company’s

performance. The

aging of debtors can

be misled by the

company as well.

The aging register of

the debtors should be

verified by the

auditors.

The bad debts should

be cross-checked

with the allowances

for bad debts as

approved by the

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit control

management.

It should be ensured

by the auditors that

the debtors’ ledgers

are checked with the

debtor confirmation

statements.

The auditor should

also verify the

collection letters

issued to the debtors

by the company to

analyse the collection

procedures adopted

by the company.

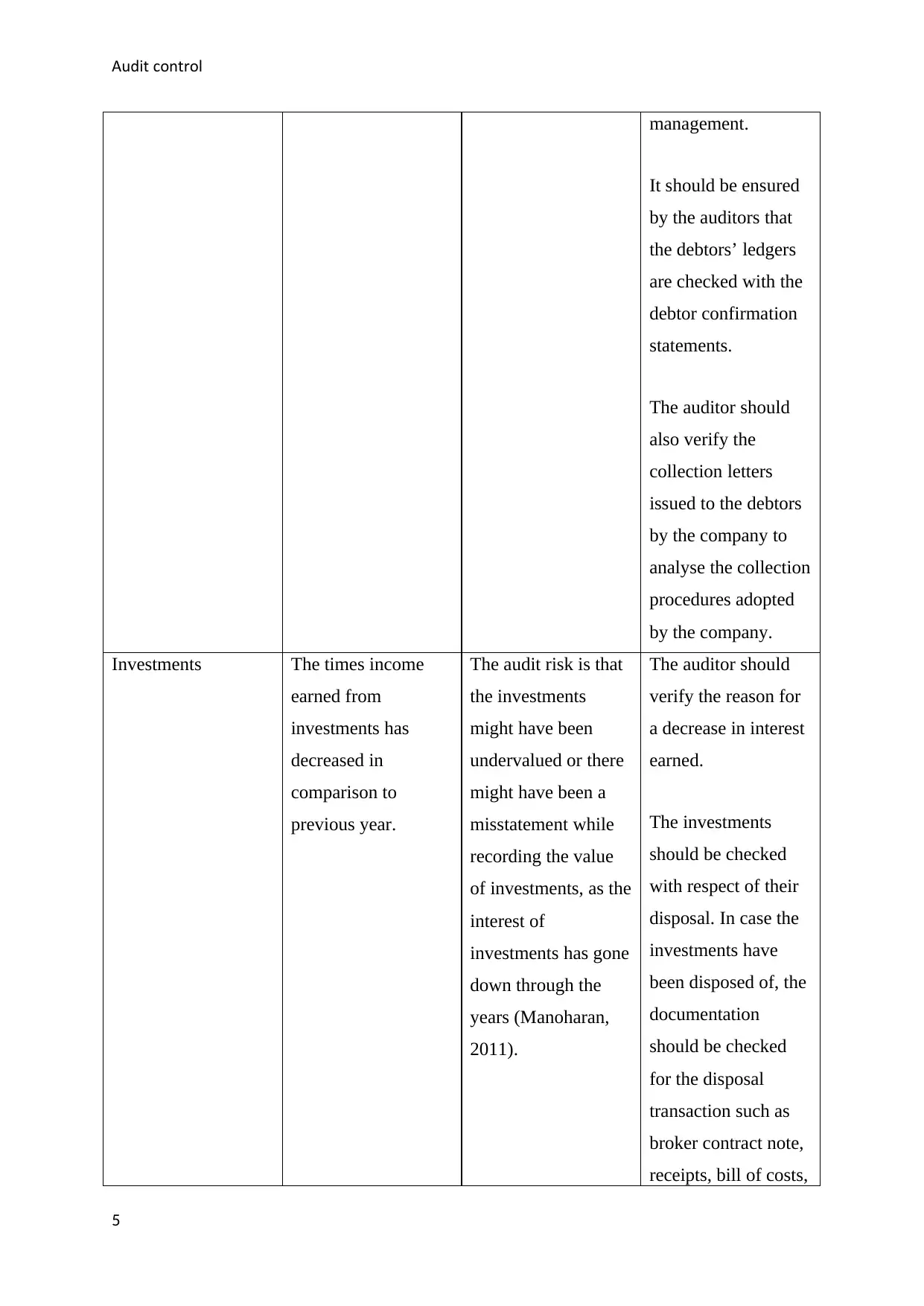

Investments The times income

earned from

investments has

decreased in

comparison to

previous year.

The audit risk is that

the investments

might have been

undervalued or there

might have been a

misstatement while

recording the value

of investments, as the

interest of

investments has gone

down through the

years (Manoharan,

2011).

The auditor should

verify the reason for

a decrease in interest

earned.

The investments

should be checked

with respect of their

disposal. In case the

investments have

been disposed of, the

documentation

should be checked

for the disposal

transaction such as

broker contract note,

receipts, bill of costs,

5

management.

It should be ensured

by the auditors that

the debtors’ ledgers

are checked with the

debtor confirmation

statements.

The auditor should

also verify the

collection letters

issued to the debtors

by the company to

analyse the collection

procedures adopted

by the company.

Investments The times income

earned from

investments has

decreased in

comparison to

previous year.

The audit risk is that

the investments

might have been

undervalued or there

might have been a

misstatement while

recording the value

of investments, as the

interest of

investments has gone

down through the

years (Manoharan,

2011).

The auditor should

verify the reason for

a decrease in interest

earned.

The investments

should be checked

with respect of their

disposal. In case the

investments have

been disposed of, the

documentation

should be checked

for the disposal

transaction such as

broker contract note,

receipts, bill of costs,

5

Audit control

etc.

The receipts from the

sale of such

investments should

be verified by the

auditor (Baldwin,

2010).

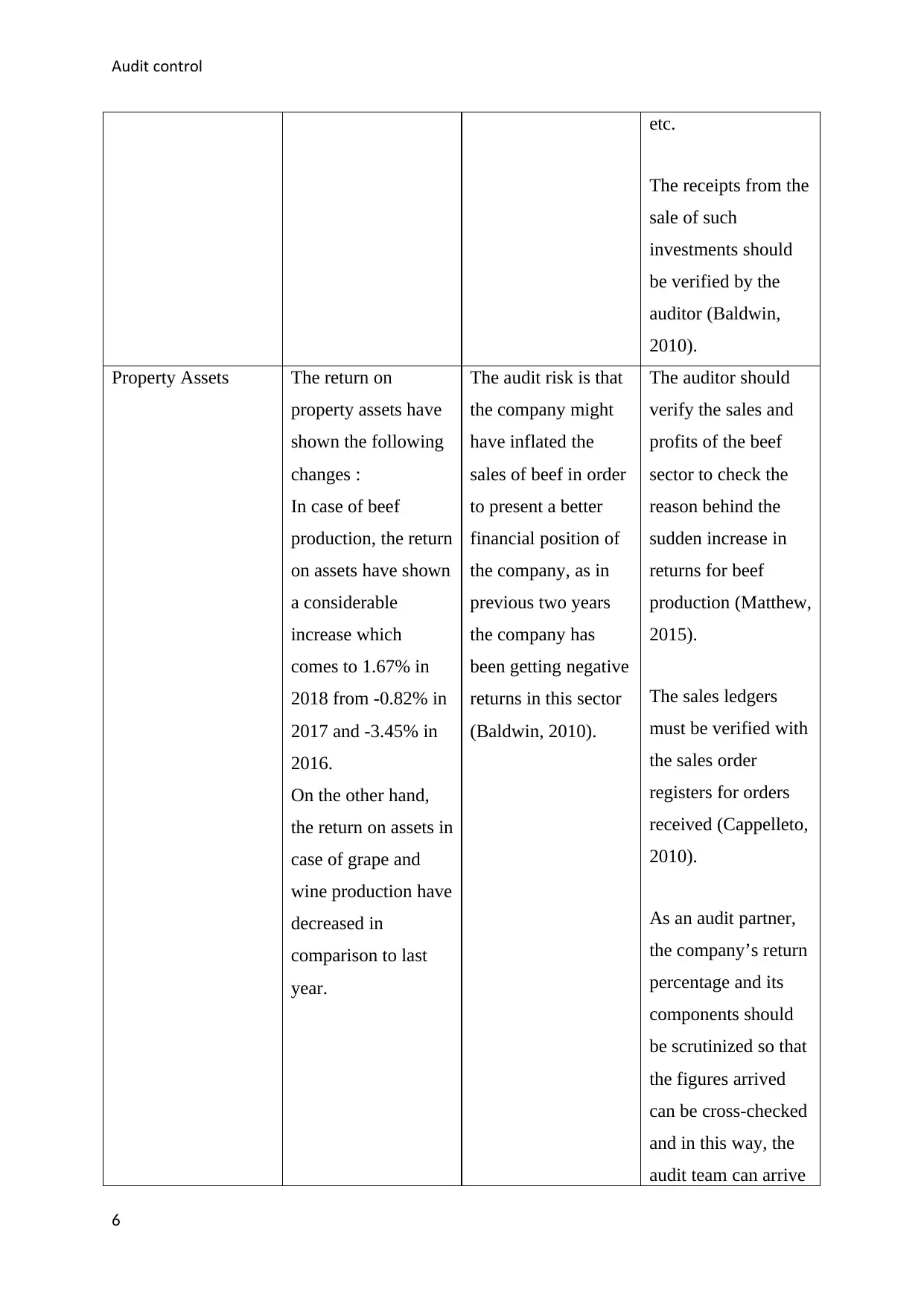

Property Assets The return on

property assets have

shown the following

changes :

In case of beef

production, the return

on assets have shown

a considerable

increase which

comes to 1.67% in

2018 from -0.82% in

2017 and -3.45% in

2016.

On the other hand,

the return on assets in

case of grape and

wine production have

decreased in

comparison to last

year.

The audit risk is that

the company might

have inflated the

sales of beef in order

to present a better

financial position of

the company, as in

previous two years

the company has

been getting negative

returns in this sector

(Baldwin, 2010).

The auditor should

verify the sales and

profits of the beef

sector to check the

reason behind the

sudden increase in

returns for beef

production (Matthew,

2015).

The sales ledgers

must be verified with

the sales order

registers for orders

received (Cappelleto,

2010).

As an audit partner,

the company’s return

percentage and its

components should

be scrutinized so that

the figures arrived

can be cross-checked

and in this way, the

audit team can arrive

6

etc.

The receipts from the

sale of such

investments should

be verified by the

auditor (Baldwin,

2010).

Property Assets The return on

property assets have

shown the following

changes :

In case of beef

production, the return

on assets have shown

a considerable

increase which

comes to 1.67% in

2018 from -0.82% in

2017 and -3.45% in

2016.

On the other hand,

the return on assets in

case of grape and

wine production have

decreased in

comparison to last

year.

The audit risk is that

the company might

have inflated the

sales of beef in order

to present a better

financial position of

the company, as in

previous two years

the company has

been getting negative

returns in this sector

(Baldwin, 2010).

The auditor should

verify the sales and

profits of the beef

sector to check the

reason behind the

sudden increase in

returns for beef

production (Matthew,

2015).

The sales ledgers

must be verified with

the sales order

registers for orders

received (Cappelleto,

2010).

As an audit partner,

the company’s return

percentage and its

components should

be scrutinized so that

the figures arrived

can be cross-checked

and in this way, the

audit team can arrive

6

Audit control

at the genuineness of

the calculation as

well.

The internal controls

related to sales and

returns shall be

verified. This will

ensure the auditor

whether or not proper

recognition of

revenue and sales has

been done by the

company (Deegan,

2011).

Marketing Expense Marketing Expenses

have increased in

comparison to

previous two years.

This might be as a

result of the

increased exposure of

the company towards

the beef sector.

The audit risk is that

the marketing

expenses might

include personal

expenses of directors

or any other expenses

disallowed. This can

be assumed due to

the reason that the

proportion of

increase in the

marketing expenses

does not match with

the proportionate

increase in the sales

or returns of the

current year in

comparison to

previous years

The auditor team

shall cross verify

each and every

voucher of marketing

expenses (Matthew,

2015).

The supporting bills

should be checked.

Also, the auditor

should see whether

these bills were

approved by some

management official

or not.

The expenses bill of

personal nature or

7

at the genuineness of

the calculation as

well.

The internal controls

related to sales and

returns shall be

verified. This will

ensure the auditor

whether or not proper

recognition of

revenue and sales has

been done by the

company (Deegan,

2011).

Marketing Expense Marketing Expenses

have increased in

comparison to

previous two years.

This might be as a

result of the

increased exposure of

the company towards

the beef sector.

The audit risk is that

the marketing

expenses might

include personal

expenses of directors

or any other expenses

disallowed. This can

be assumed due to

the reason that the

proportion of

increase in the

marketing expenses

does not match with

the proportionate

increase in the sales

or returns of the

current year in

comparison to

previous years

The auditor team

shall cross verify

each and every

voucher of marketing

expenses (Matthew,

2015).

The supporting bills

should be checked.

Also, the auditor

should see whether

these bills were

approved by some

management official

or not.

The expenses bill of

personal nature or

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit control

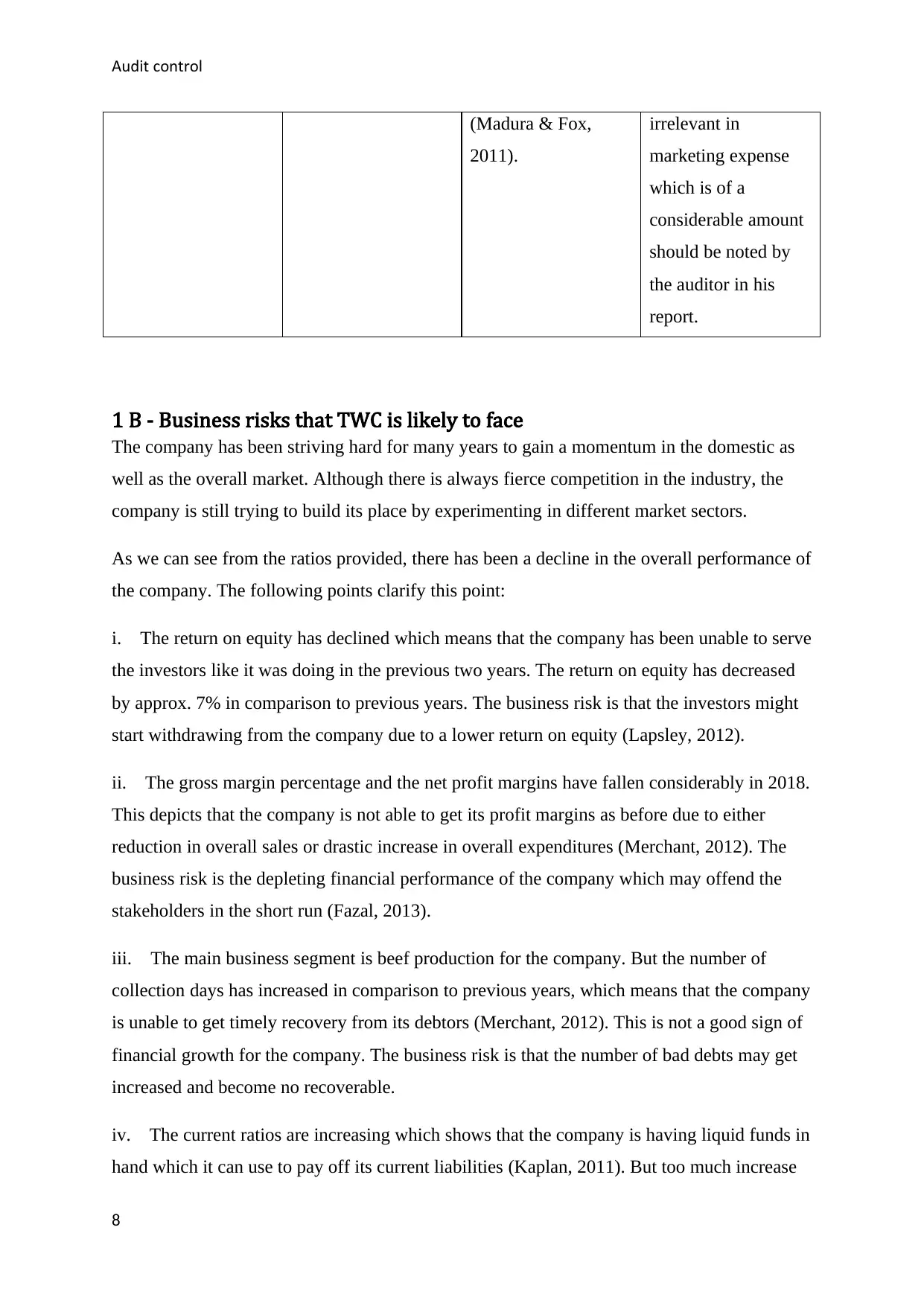

(Madura & Fox,

2011).

irrelevant in

marketing expense

which is of a

considerable amount

should be noted by

the auditor in his

report.

1 B - Business risks that TWC is likely to face

The company has been striving hard for many years to gain a momentum in the domestic as

well as the overall market. Although there is always fierce competition in the industry, the

company is still trying to build its place by experimenting in different market sectors.

As we can see from the ratios provided, there has been a decline in the overall performance of

the company. The following points clarify this point:

i. The return on equity has declined which means that the company has been unable to serve

the investors like it was doing in the previous two years. The return on equity has decreased

by approx. 7% in comparison to previous years. The business risk is that the investors might

start withdrawing from the company due to a lower return on equity (Lapsley, 2012).

ii. The gross margin percentage and the net profit margins have fallen considerably in 2018.

This depicts that the company is not able to get its profit margins as before due to either

reduction in overall sales or drastic increase in overall expenditures (Merchant, 2012). The

business risk is the depleting financial performance of the company which may offend the

stakeholders in the short run (Fazal, 2013).

iii. The main business segment is beef production for the company. But the number of

collection days has increased in comparison to previous years, which means that the company

is unable to get timely recovery from its debtors (Merchant, 2012). This is not a good sign of

financial growth for the company. The business risk is that the number of bad debts may get

increased and become no recoverable.

iv. The current ratios are increasing which shows that the company is having liquid funds in

hand which it can use to pay off its current liabilities (Kaplan, 2011). But too much increase

8

(Madura & Fox,

2011).

irrelevant in

marketing expense

which is of a

considerable amount

should be noted by

the auditor in his

report.

1 B - Business risks that TWC is likely to face

The company has been striving hard for many years to gain a momentum in the domestic as

well as the overall market. Although there is always fierce competition in the industry, the

company is still trying to build its place by experimenting in different market sectors.

As we can see from the ratios provided, there has been a decline in the overall performance of

the company. The following points clarify this point:

i. The return on equity has declined which means that the company has been unable to serve

the investors like it was doing in the previous two years. The return on equity has decreased

by approx. 7% in comparison to previous years. The business risk is that the investors might

start withdrawing from the company due to a lower return on equity (Lapsley, 2012).

ii. The gross margin percentage and the net profit margins have fallen considerably in 2018.

This depicts that the company is not able to get its profit margins as before due to either

reduction in overall sales or drastic increase in overall expenditures (Merchant, 2012). The

business risk is the depleting financial performance of the company which may offend the

stakeholders in the short run (Fazal, 2013).

iii. The main business segment is beef production for the company. But the number of

collection days has increased in comparison to previous years, which means that the company

is unable to get timely recovery from its debtors (Merchant, 2012). This is not a good sign of

financial growth for the company. The business risk is that the number of bad debts may get

increased and become no recoverable.

iv. The current ratios are increasing which shows that the company is having liquid funds in

hand which it can use to pay off its current liabilities (Kaplan, 2011). But too much increase

8

Audit control

in current ratio would mean idleness of liquid funds which is not again a good sign and a

business risk.

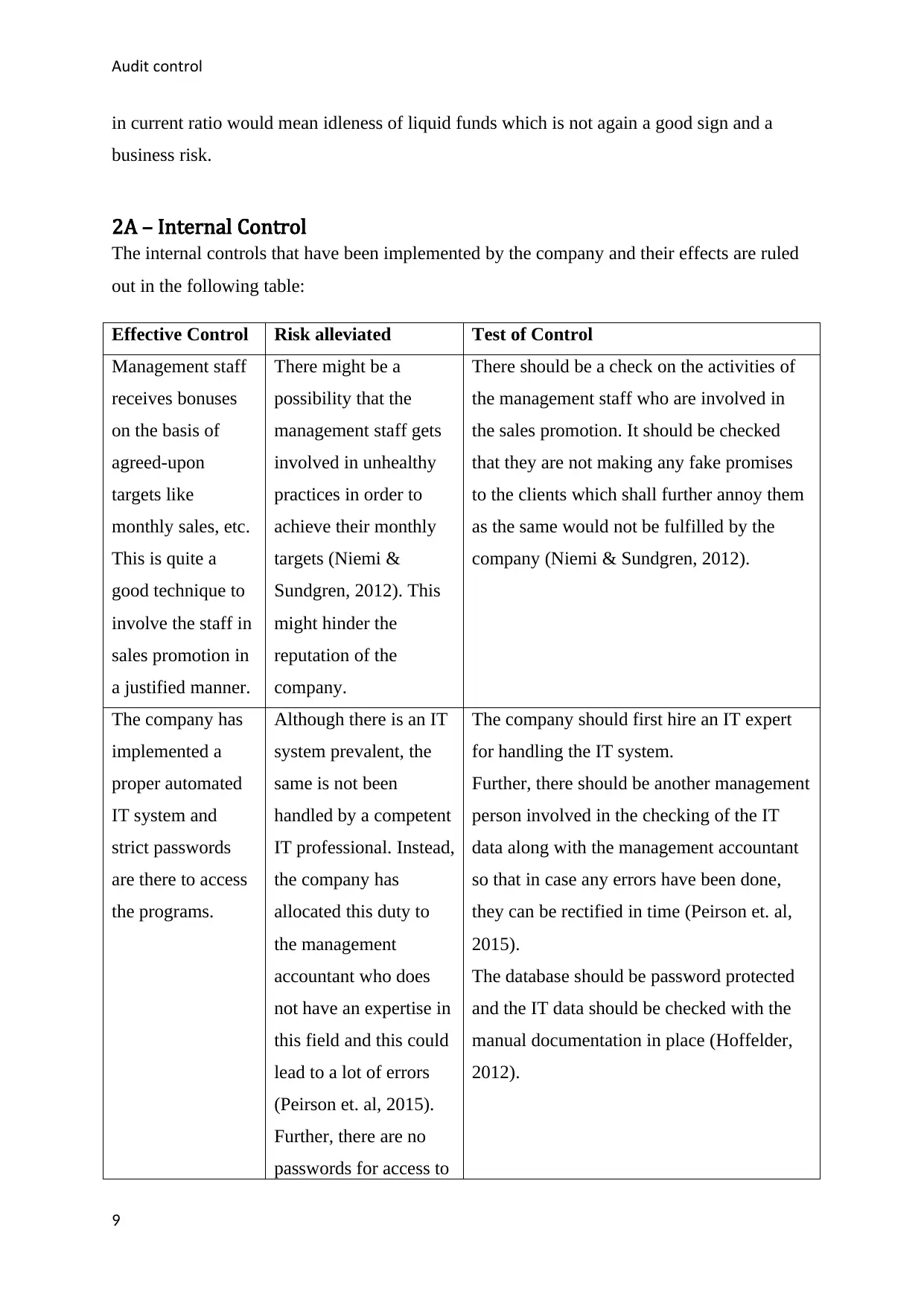

2A – Internal Control

The internal controls that have been implemented by the company and their effects are ruled

out in the following table:

Effective Control Risk alleviated Test of Control

Management staff

receives bonuses

on the basis of

agreed-upon

targets like

monthly sales, etc.

This is quite a

good technique to

involve the staff in

sales promotion in

a justified manner.

There might be a

possibility that the

management staff gets

involved in unhealthy

practices in order to

achieve their monthly

targets (Niemi &

Sundgren, 2012). This

might hinder the

reputation of the

company.

There should be a check on the activities of

the management staff who are involved in

the sales promotion. It should be checked

that they are not making any fake promises

to the clients which shall further annoy them

as the same would not be fulfilled by the

company (Niemi & Sundgren, 2012).

The company has

implemented a

proper automated

IT system and

strict passwords

are there to access

the programs.

Although there is an IT

system prevalent, the

same is not been

handled by a competent

IT professional. Instead,

the company has

allocated this duty to

the management

accountant who does

not have an expertise in

this field and this could

lead to a lot of errors

(Peirson et. al, 2015).

Further, there are no

passwords for access to

The company should first hire an IT expert

for handling the IT system.

Further, there should be another management

person involved in the checking of the IT

data along with the management accountant

so that in case any errors have been done,

they can be rectified in time (Peirson et. al,

2015).

The database should be password protected

and the IT data should be checked with the

manual documentation in place (Hoffelder,

2012).

9

in current ratio would mean idleness of liquid funds which is not again a good sign and a

business risk.

2A – Internal Control

The internal controls that have been implemented by the company and their effects are ruled

out in the following table:

Effective Control Risk alleviated Test of Control

Management staff

receives bonuses

on the basis of

agreed-upon

targets like

monthly sales, etc.

This is quite a

good technique to

involve the staff in

sales promotion in

a justified manner.

There might be a

possibility that the

management staff gets

involved in unhealthy

practices in order to

achieve their monthly

targets (Niemi &

Sundgren, 2012). This

might hinder the

reputation of the

company.

There should be a check on the activities of

the management staff who are involved in

the sales promotion. It should be checked

that they are not making any fake promises

to the clients which shall further annoy them

as the same would not be fulfilled by the

company (Niemi & Sundgren, 2012).

The company has

implemented a

proper automated

IT system and

strict passwords

are there to access

the programs.

Although there is an IT

system prevalent, the

same is not been

handled by a competent

IT professional. Instead,

the company has

allocated this duty to

the management

accountant who does

not have an expertise in

this field and this could

lead to a lot of errors

(Peirson et. al, 2015).

Further, there are no

passwords for access to

The company should first hire an IT expert

for handling the IT system.

Further, there should be another management

person involved in the checking of the IT

data along with the management accountant

so that in case any errors have been done,

they can be rectified in time (Peirson et. al,

2015).

The database should be password protected

and the IT data should be checked with the

manual documentation in place (Hoffelder,

2012).

9

Audit control

the databases which

again is a major risk.

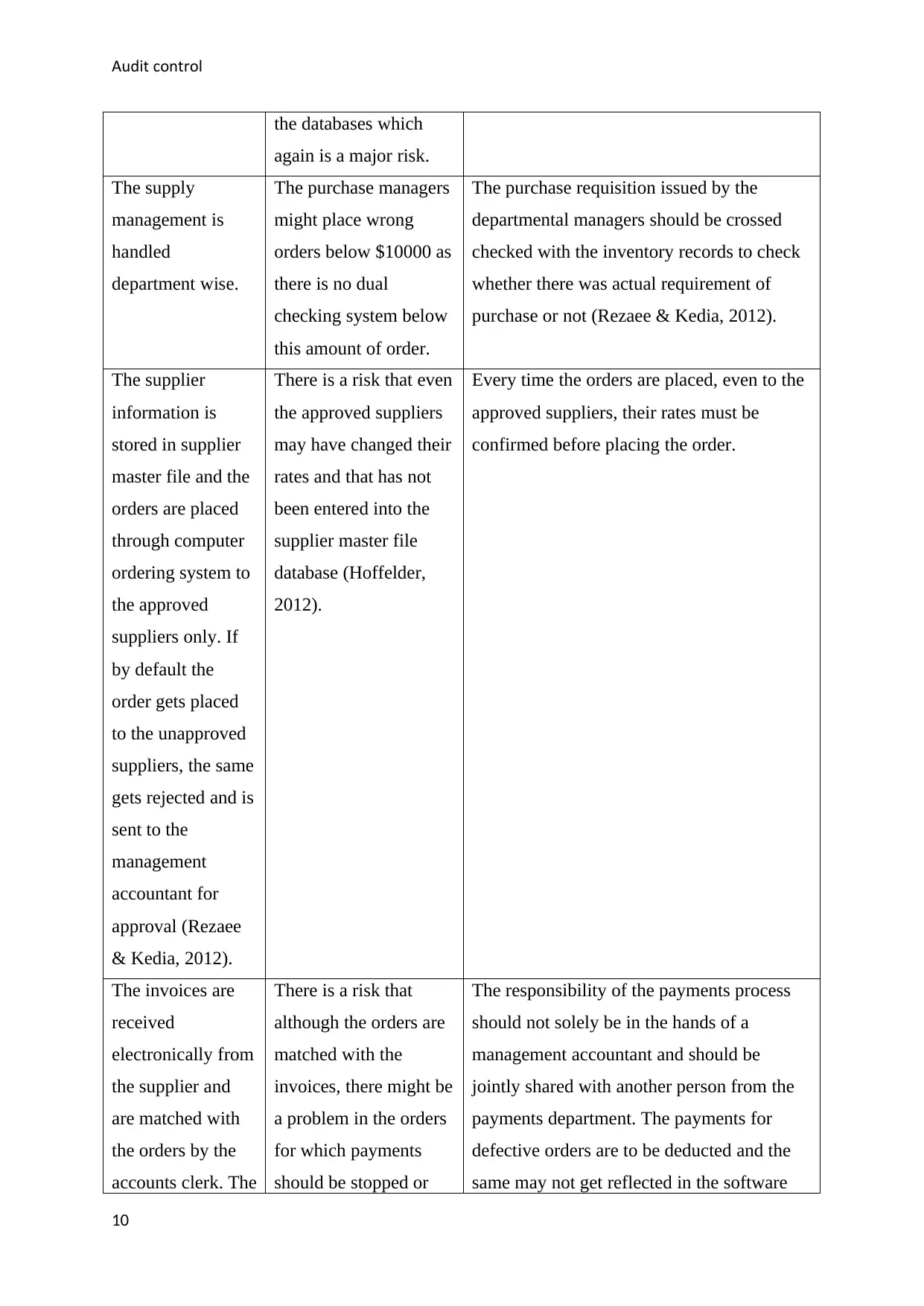

The supply

management is

handled

department wise.

The purchase managers

might place wrong

orders below $10000 as

there is no dual

checking system below

this amount of order.

The purchase requisition issued by the

departmental managers should be crossed

checked with the inventory records to check

whether there was actual requirement of

purchase or not (Rezaee & Kedia, 2012).

The supplier

information is

stored in supplier

master file and the

orders are placed

through computer

ordering system to

the approved

suppliers only. If

by default the

order gets placed

to the unapproved

suppliers, the same

gets rejected and is

sent to the

management

accountant for

approval (Rezaee

& Kedia, 2012).

There is a risk that even

the approved suppliers

may have changed their

rates and that has not

been entered into the

supplier master file

database (Hoffelder,

2012).

Every time the orders are placed, even to the

approved suppliers, their rates must be

confirmed before placing the order.

The invoices are

received

electronically from

the supplier and

are matched with

the orders by the

accounts clerk. The

There is a risk that

although the orders are

matched with the

invoices, there might be

a problem in the orders

for which payments

should be stopped or

The responsibility of the payments process

should not solely be in the hands of a

management accountant and should be

jointly shared with another person from the

payments department. The payments for

defective orders are to be deducted and the

same may not get reflected in the software

10

the databases which

again is a major risk.

The supply

management is

handled

department wise.

The purchase managers

might place wrong

orders below $10000 as

there is no dual

checking system below

this amount of order.

The purchase requisition issued by the

departmental managers should be crossed

checked with the inventory records to check

whether there was actual requirement of

purchase or not (Rezaee & Kedia, 2012).

The supplier

information is

stored in supplier

master file and the

orders are placed

through computer

ordering system to

the approved

suppliers only. If

by default the

order gets placed

to the unapproved

suppliers, the same

gets rejected and is

sent to the

management

accountant for

approval (Rezaee

& Kedia, 2012).

There is a risk that even

the approved suppliers

may have changed their

rates and that has not

been entered into the

supplier master file

database (Hoffelder,

2012).

Every time the orders are placed, even to the

approved suppliers, their rates must be

confirmed before placing the order.

The invoices are

received

electronically from

the supplier and

are matched with

the orders by the

accounts clerk. The

There is a risk that

although the orders are

matched with the

invoices, there might be

a problem in the orders

for which payments

should be stopped or

The responsibility of the payments process

should not solely be in the hands of a

management accountant and should be

jointly shared with another person from the

payments department. The payments for

defective orders are to be deducted and the

same may not get reflected in the software

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit control

payment file for

the same is verified

weekly by the

management

accountant.

deferred (Rezaee &

Kedia, 2012). But after

matching the order file

and invoice, the

payments file is

approved and sent to

the bank.

(Geoffrey et. al, 2016).

In case repairs are

required in the

wine department,

the responsibility

of the same is of

the department

manager. He

generates online

orders and the

ultimate payment

process is

completed by the

approval of

management

accountant.

There is a risk that there

may be undue expenses

on the repairing as there

is no supervision on the

repair service requests

done by the wine

department manager.

The accounts clerk and

the management

accountant come into

picture only once the

service is completed

and the service provider

has raised his invoice to

the company (Gay &

Simnet, 2015).

The repairing function should be cross

checked by some management staff so that

there can be a check on the requirement and

expenses being incurred on the repair

services.

2b – Justification of the weakness in Internal control

Following are the weaknesses in the internal control for purchases and accounts payable:

Purchases:

Weakness Justification

No checking with

stores registers

The purchase orders are not checked independently with the stock of

goods which may result in overstocking of goods in the warehouse.

Over reliability on the The suppliers are only given orders on the basis of their past

11

payment file for

the same is verified

weekly by the

management

accountant.

deferred (Rezaee &

Kedia, 2012). But after

matching the order file

and invoice, the

payments file is

approved and sent to

the bank.

(Geoffrey et. al, 2016).

In case repairs are

required in the

wine department,

the responsibility

of the same is of

the department

manager. He

generates online

orders and the

ultimate payment

process is

completed by the

approval of

management

accountant.

There is a risk that there

may be undue expenses

on the repairing as there

is no supervision on the

repair service requests

done by the wine

department manager.

The accounts clerk and

the management

accountant come into

picture only once the

service is completed

and the service provider

has raised his invoice to

the company (Gay &

Simnet, 2015).

The repairing function should be cross

checked by some management staff so that

there can be a check on the requirement and

expenses being incurred on the repair

services.

2b – Justification of the weakness in Internal control

Following are the weaknesses in the internal control for purchases and accounts payable:

Purchases:

Weakness Justification

No checking with

stores registers

The purchase orders are not checked independently with the stock of

goods which may result in overstocking of goods in the warehouse.

Over reliability on the The suppliers are only given orders on the basis of their past

11

Audit control

approved suppliers reputation and other factors are not considered like change in prices,

change in time of delivery or change in terms.

No separate files

prepared for defective

orders low quality

goods.

The accounts clerk matches the order details and the invoice and

then sends the invoice to the payment file. There might be some

goods which are of low quality or are defective which are nowhere

accounted for by the accounts clerk (Roach, 2010). Only the paper

documentation is checked.

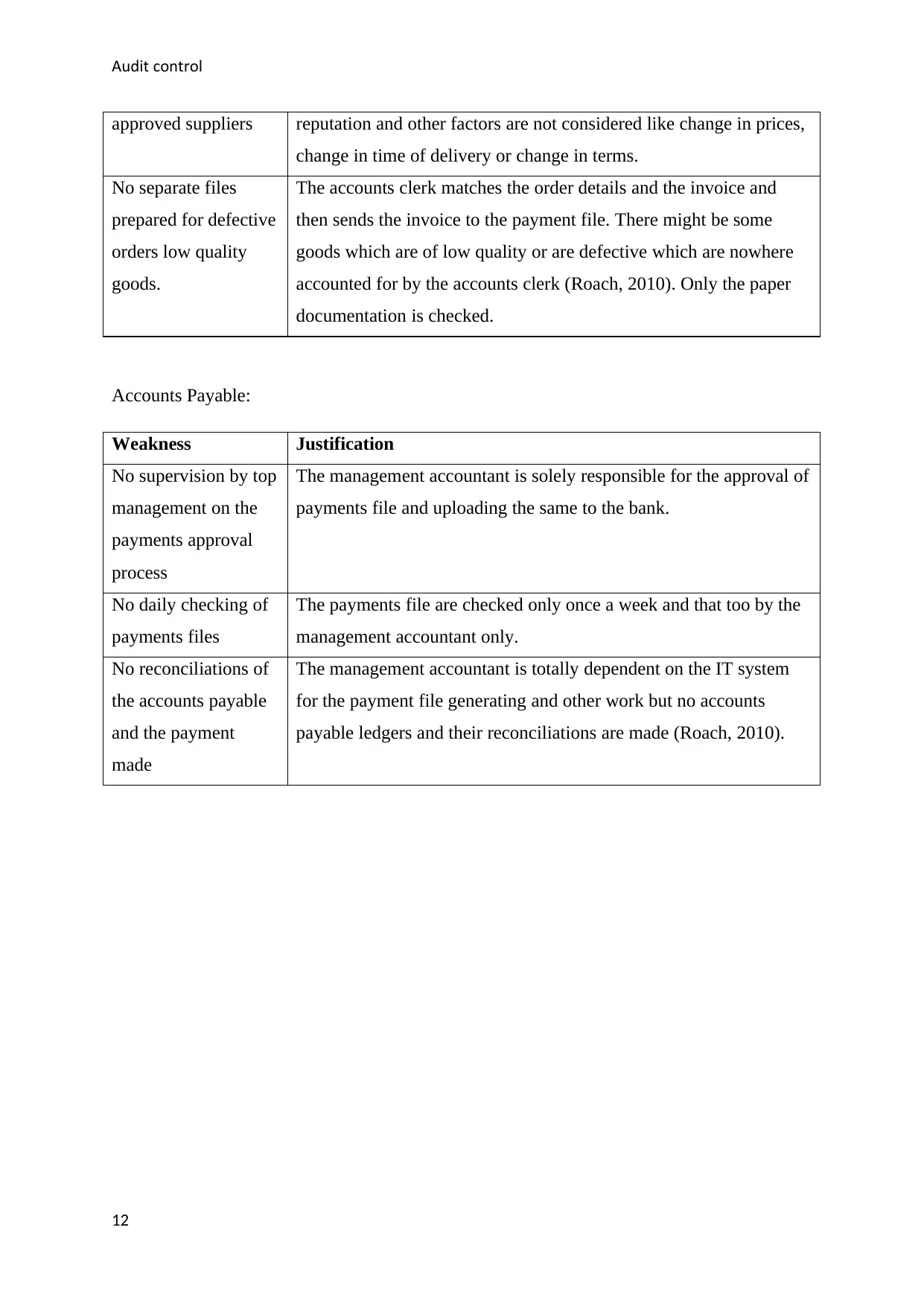

Accounts Payable:

Weakness Justification

No supervision by top

management on the

payments approval

process

The management accountant is solely responsible for the approval of

payments file and uploading the same to the bank.

No daily checking of

payments files

The payments file are checked only once a week and that too by the

management accountant only.

No reconciliations of

the accounts payable

and the payment

made

The management accountant is totally dependent on the IT system

for the payment file generating and other work but no accounts

payable ledgers and their reconciliations are made (Roach, 2010).

12

approved suppliers reputation and other factors are not considered like change in prices,

change in time of delivery or change in terms.

No separate files

prepared for defective

orders low quality

goods.

The accounts clerk matches the order details and the invoice and

then sends the invoice to the payment file. There might be some

goods which are of low quality or are defective which are nowhere

accounted for by the accounts clerk (Roach, 2010). Only the paper

documentation is checked.

Accounts Payable:

Weakness Justification

No supervision by top

management on the

payments approval

process

The management accountant is solely responsible for the approval of

payments file and uploading the same to the bank.

No daily checking of

payments files

The payments file are checked only once a week and that too by the

management accountant only.

No reconciliations of

the accounts payable

and the payment

made

The management accountant is totally dependent on the IT system

for the payment file generating and other work but no accounts

payable ledgers and their reconciliations are made (Roach, 2010).

12

Audit control

Conclusion

Hence it can be seen that there is over-dependence on the management accountant by the

company. The duties of IT system management, purchase order placement, payments,

management of accounts payable should be segregated between different officials of the

company so that there are least chances of errors and frauds. If everything is taken care of by

only one person without proper supervision, there are higher chances of frauds also along

with the mistakes and errors. There should be a proper delegation of duties for every work

department. It needs to be noted that the current standard of data evaluation by only one

person will fail to attain the target and hence data evaluation by more than one person should

be a major consideration. This step can help the company to ward off fraud and loopholes.

Overall, it can be commented that an effective risk management should be able to connect

with the system of internal control so that it reduces the risk that is present for the

organization. It is important for the auditor to report the risks that the business is exposed to

so that adequate steps can be taken into consideration. Further, it is the need of the hour to

bring more structural changes so that an internal control mechanism can eliminate the risks.

13

Conclusion

Hence it can be seen that there is over-dependence on the management accountant by the

company. The duties of IT system management, purchase order placement, payments,

management of accounts payable should be segregated between different officials of the

company so that there are least chances of errors and frauds. If everything is taken care of by

only one person without proper supervision, there are higher chances of frauds also along

with the mistakes and errors. There should be a proper delegation of duties for every work

department. It needs to be noted that the current standard of data evaluation by only one

person will fail to attain the target and hence data evaluation by more than one person should

be a major consideration. This step can help the company to ward off fraud and loopholes.

Overall, it can be commented that an effective risk management should be able to connect

with the system of internal control so that it reduces the risk that is present for the

organization. It is important for the auditor to report the risks that the business is exposed to

so that adequate steps can be taken into consideration. Further, it is the need of the hour to

bring more structural changes so that an internal control mechanism can eliminate the risks.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit control

References

Baldwin, S. (2010). Doing a content audit or inventory. Pearson Press.

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia. AFAANZ,

Melbourne

Deegan, C. M. (2011). In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Fazal, H. (2013, May 13). What is Intimidation threat in auditing?.Retrieved from:

http://pakaccountants.com/what-is-intimidation-threat-in-auditing/

Gay, G. and Simnet, R. (2015) Auditing and Assurance Services. McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S. and David A. W. (2016) Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons. [online] 30(1), pp. 143-156. Available from

https://doi.org/10.2308/acch-51309 [Accessed 4 August 2018]

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

Doi:https://doi.org/10.2308/accr.00000031

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

Doi:https://doi.org/10.1111/1468-0408.00081

Madura, R., & Fox, J. (2011). International financial management (2nd ed.). South Western

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The

George Washington University. Livne, G. (2015, May 12). Threats to Auditor

Independence and Possible Remedies. Retrieved from:

http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review, 90(2), 495-527. https://doi.org/10.2308/accr-

50871

14

References

Baldwin, S. (2010). Doing a content audit or inventory. Pearson Press.

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia. AFAANZ,

Melbourne

Deegan, C. M. (2011). In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Fazal, H. (2013, May 13). What is Intimidation threat in auditing?.Retrieved from:

http://pakaccountants.com/what-is-intimidation-threat-in-auditing/

Gay, G. and Simnet, R. (2015) Auditing and Assurance Services. McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S. and David A. W. (2016) Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons. [online] 30(1), pp. 143-156. Available from

https://doi.org/10.2308/acch-51309 [Accessed 4 August 2018]

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

Doi:https://doi.org/10.2308/accr.00000031

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

Doi:https://doi.org/10.1111/1468-0408.00081

Madura, R., & Fox, J. (2011). International financial management (2nd ed.). South Western

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The

George Washington University. Livne, G. (2015, May 12). Threats to Auditor

Independence and Possible Remedies. Retrieved from:

http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review, 90(2), 495-527. https://doi.org/10.2308/accr-

50871

14

Audit control

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. Doi: https://doi.org/10.1108/01140581211283904

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796.

https://doi.org/10.1080/09638180.2012.671465

Peirson, G., Brown, R., Easton, S., Howard, P & Pinder, S. (2015). Business FinanceNorth

Ryde: McGraw-Hill Australia.

Rezaee, Z & Kedia, B. L. (2012). Role of Corporate Governance Participants in Preventing

and Detecting Financial Statement Fraud. Journal of Forensic & Investigative

Accounting. [online]. 4(2), pp. 176-205. Doi: 10.1016/j.sbspro.2014.06.041

Roach, L. (2010). Auditor Liability: Liability Limitation Agreements. Pearson.

15

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. Doi: https://doi.org/10.1108/01140581211283904

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796.

https://doi.org/10.1080/09638180.2012.671465

Peirson, G., Brown, R., Easton, S., Howard, P & Pinder, S. (2015). Business FinanceNorth

Ryde: McGraw-Hill Australia.

Rezaee, Z & Kedia, B. L. (2012). Role of Corporate Governance Participants in Preventing

and Detecting Financial Statement Fraud. Journal of Forensic & Investigative

Accounting. [online]. 4(2), pp. 176-205. Doi: 10.1016/j.sbspro.2014.06.041

Roach, L. (2010). Auditor Liability: Liability Limitation Agreements. Pearson.

15

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.