Audit and Ethics Assignment on ANZ Banking Limited Company

VerifiedAdded on 2023/06/07

|13

|2194

|356

AI Summary

This assignment deals with making relevant assertions on the financial statements of ANZ Banking Limited Company. It includes materiality concern, preliminary analytical review, and review of the cash flow statement of the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Audit and Ethics

Assignment

Assignment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

In the given assignment the company that has been selected is ANZ banking limited company.

The assignment is divided into three sections and each deals with making relevant assertions on

the financial statements of the company. The annual report of the company has been downloaded

and key data has been taken from them.

2 | P a g e

Executive Summary

In the given assignment the company that has been selected is ANZ banking limited company.

The assignment is divided into three sections and each deals with making relevant assertions on

the financial statements of the company. The annual report of the company has been downloaded

and key data has been taken from them.

2 | P a g e

3

Contents

Section 1: Materiality concern of the entity................................................................................................3

Section 2: Preliminary analytical review of the company............................................................................5

Section 3: Review of the cash flow statement of the company...................................................................7

References.................................................................................................................................................10

3 | P a g e

Contents

Section 1: Materiality concern of the entity................................................................................................3

Section 2: Preliminary analytical review of the company............................................................................5

Section 3: Review of the cash flow statement of the company...................................................................7

References.................................................................................................................................................10

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

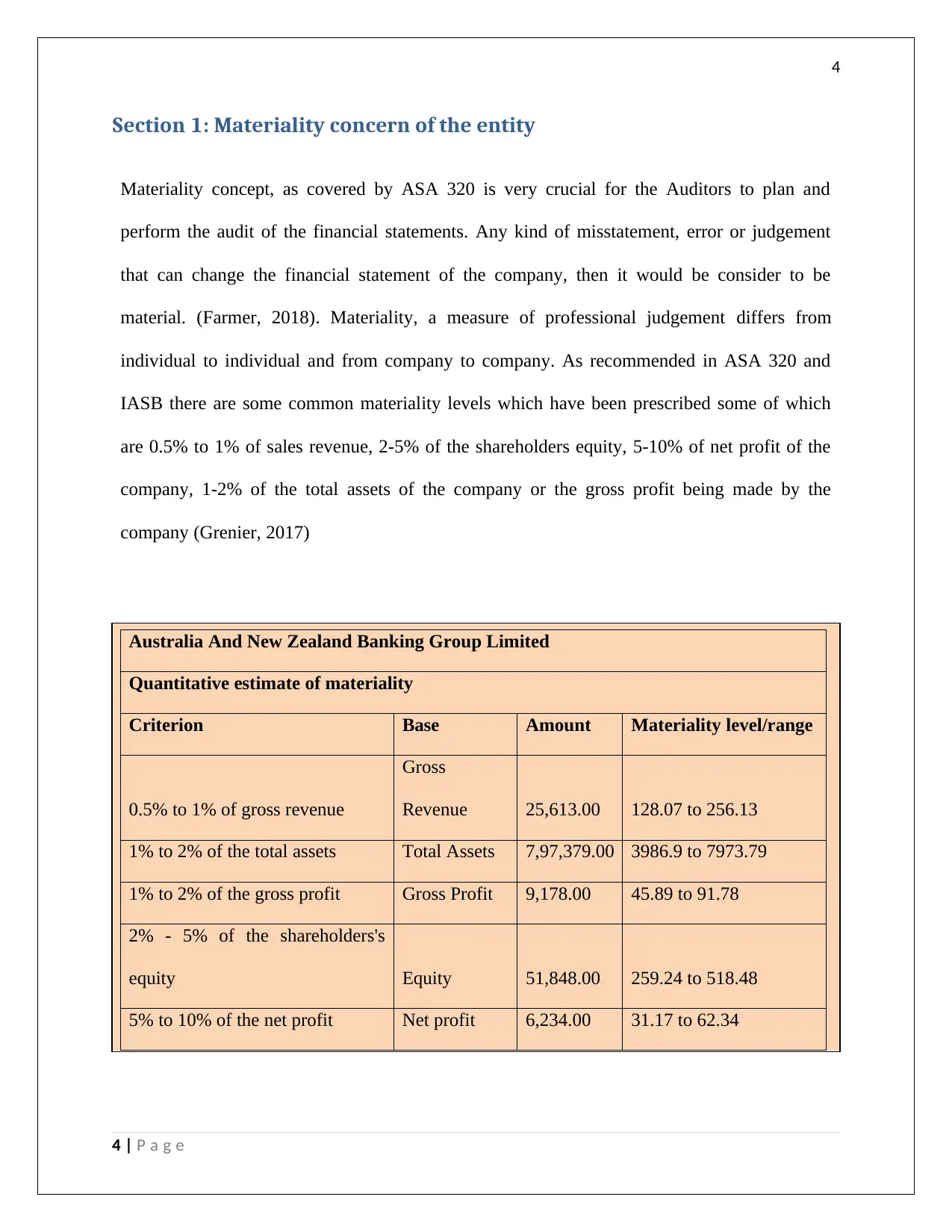

Section 1: Materiality concern of the entity

Materiality concept, as covered by ASA 320 is very crucial for the Auditors to plan and

perform the audit of the financial statements. Any kind of misstatement, error or judgement

that can change the financial statement of the company, then it would be consider to be

material. (Farmer, 2018). Materiality, a measure of professional judgement differs from

individual to individual and from company to company. As recommended in ASA 320 and

IASB there are some common materiality levels which have been prescribed some of which

are 0.5% to 1% of sales revenue, 2-5% of the shareholders equity, 5-10% of net profit of the

company, 1-2% of the total assets of the company or the gross profit being made by the

company (Grenier, 2017)

Australia And New Zealand Banking Group Limited

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue

Gross

Revenue 25,613.00 128.07 to 256.13

1% to 2% of the total assets Total Assets 7,97,379.00 3986.9 to 7973.79

1% to 2% of the gross profit Gross Profit 9,178.00 45.89 to 91.78

2% - 5% of the shareholders's

equity Equity 51,848.00 259.24 to 518.48

5% to 10% of the net profit Net profit 6,234.00 31.17 to 62.34

4 | P a g e

Section 1: Materiality concern of the entity

Materiality concept, as covered by ASA 320 is very crucial for the Auditors to plan and

perform the audit of the financial statements. Any kind of misstatement, error or judgement

that can change the financial statement of the company, then it would be consider to be

material. (Farmer, 2018). Materiality, a measure of professional judgement differs from

individual to individual and from company to company. As recommended in ASA 320 and

IASB there are some common materiality levels which have been prescribed some of which

are 0.5% to 1% of sales revenue, 2-5% of the shareholders equity, 5-10% of net profit of the

company, 1-2% of the total assets of the company or the gross profit being made by the

company (Grenier, 2017)

Australia And New Zealand Banking Group Limited

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue

Gross

Revenue 25,613.00 128.07 to 256.13

1% to 2% of the total assets Total Assets 7,97,379.00 3986.9 to 7973.79

1% to 2% of the gross profit Gross Profit 9,178.00 45.89 to 91.78

2% - 5% of the shareholders's

equity Equity 51,848.00 259.24 to 518.48

5% to 10% of the net profit Net profit 6,234.00 31.17 to 62.34

4 | P a g e

5

Australia and New Zealand Banking Group Limited which has been chosen here for analysis is

listed on the New Zealand Stock Exchange. It is third largest bank by Market capitalisation in

Australia and the largest bank in New Zealand. The company was founded on 2 March 1835.

The company has its domination in the commercial and retail banking sector in both these

countries. The quantitative materiality level of the given company has been derived using the

parameters mentioned above but the auditors have mentioned in the auditor’s report that they

have considered the materiality to be which is slightly above the levels shown in the below

table. Hence, the calculation of materiality is justified.

The drafts and the notes of the financial statements includes disclosure regarding the relevant

accounting policies and standards followed by the company. In case there is any change in the

policy the same has been mentioned. The going concern ability of the company is also mentioned

in the draft notes of the financial statements (Choy, 2018).

Section 2: Preliminary analytical review of the company

Two types of procedures can be applied for the conduction of the audit- substantive test and the

analytical review procedures. Substantive Test is the vouching of income and expenses and

Verification is the checking of completeness, valuation, appropriateness and change in the values

of the assets and liabilities (Trieu, 2017). The Auditor performs preliminary analytical

procedures if he is not able to give any opinion based on substantive test. Preliminary analytical

procedures includes understanding the business environment and his business as whole based on

the financial performance of the entity over the past, the relevant industry and the comparison

groups (Alexander, 2016). The Auditor sets the audit planning based on trend analysis, variance

5 | P a g e

Australia and New Zealand Banking Group Limited which has been chosen here for analysis is

listed on the New Zealand Stock Exchange. It is third largest bank by Market capitalisation in

Australia and the largest bank in New Zealand. The company was founded on 2 March 1835.

The company has its domination in the commercial and retail banking sector in both these

countries. The quantitative materiality level of the given company has been derived using the

parameters mentioned above but the auditors have mentioned in the auditor’s report that they

have considered the materiality to be which is slightly above the levels shown in the below

table. Hence, the calculation of materiality is justified.

The drafts and the notes of the financial statements includes disclosure regarding the relevant

accounting policies and standards followed by the company. In case there is any change in the

policy the same has been mentioned. The going concern ability of the company is also mentioned

in the draft notes of the financial statements (Choy, 2018).

Section 2: Preliminary analytical review of the company

Two types of procedures can be applied for the conduction of the audit- substantive test and the

analytical review procedures. Substantive Test is the vouching of income and expenses and

Verification is the checking of completeness, valuation, appropriateness and change in the values

of the assets and liabilities (Trieu, 2017). The Auditor performs preliminary analytical

procedures if he is not able to give any opinion based on substantive test. Preliminary analytical

procedures includes understanding the business environment and his business as whole based on

the financial performance of the entity over the past, the relevant industry and the comparison

groups (Alexander, 2016). The Auditor sets the audit planning based on trend analysis, variance

5 | P a g e

6

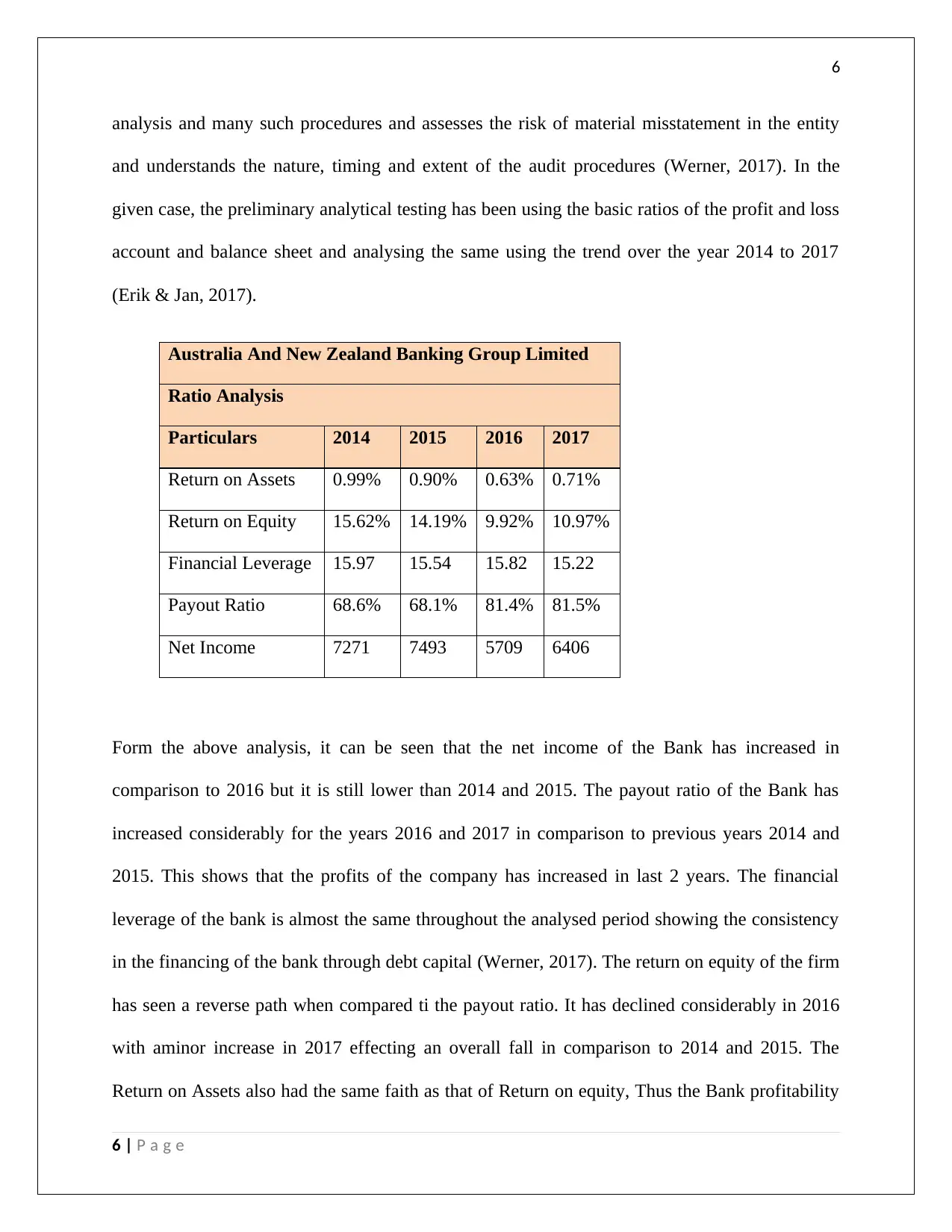

analysis and many such procedures and assesses the risk of material misstatement in the entity

and understands the nature, timing and extent of the audit procedures (Werner, 2017). In the

given case, the preliminary analytical testing has been using the basic ratios of the profit and loss

account and balance sheet and analysing the same using the trend over the year 2014 to 2017

(Erik & Jan, 2017).

Australia And New Zealand Banking Group Limited

Ratio Analysis

Particulars 2014 2015 2016 2017

Return on Assets 0.99% 0.90% 0.63% 0.71%

Return on Equity 15.62% 14.19% 9.92% 10.97%

Financial Leverage 15.97 15.54 15.82 15.22

Payout Ratio 68.6% 68.1% 81.4% 81.5%

Net Income 7271 7493 5709 6406

Form the above analysis, it can be seen that the net income of the Bank has increased in

comparison to 2016 but it is still lower than 2014 and 2015. The payout ratio of the Bank has

increased considerably for the years 2016 and 2017 in comparison to previous years 2014 and

2015. This shows that the profits of the company has increased in last 2 years. The financial

leverage of the bank is almost the same throughout the analysed period showing the consistency

in the financing of the bank through debt capital (Werner, 2017). The return on equity of the firm

has seen a reverse path when compared ti the payout ratio. It has declined considerably in 2016

with aminor increase in 2017 effecting an overall fall in comparison to 2014 and 2015. The

Return on Assets also had the same faith as that of Return on equity, Thus the Bank profitability

6 | P a g e

analysis and many such procedures and assesses the risk of material misstatement in the entity

and understands the nature, timing and extent of the audit procedures (Werner, 2017). In the

given case, the preliminary analytical testing has been using the basic ratios of the profit and loss

account and balance sheet and analysing the same using the trend over the year 2014 to 2017

(Erik & Jan, 2017).

Australia And New Zealand Banking Group Limited

Ratio Analysis

Particulars 2014 2015 2016 2017

Return on Assets 0.99% 0.90% 0.63% 0.71%

Return on Equity 15.62% 14.19% 9.92% 10.97%

Financial Leverage 15.97 15.54 15.82 15.22

Payout Ratio 68.6% 68.1% 81.4% 81.5%

Net Income 7271 7493 5709 6406

Form the above analysis, it can be seen that the net income of the Bank has increased in

comparison to 2016 but it is still lower than 2014 and 2015. The payout ratio of the Bank has

increased considerably for the years 2016 and 2017 in comparison to previous years 2014 and

2015. This shows that the profits of the company has increased in last 2 years. The financial

leverage of the bank is almost the same throughout the analysed period showing the consistency

in the financing of the bank through debt capital (Werner, 2017). The return on equity of the firm

has seen a reverse path when compared ti the payout ratio. It has declined considerably in 2016

with aminor increase in 2017 effecting an overall fall in comparison to 2014 and 2015. The

Return on Assets also had the same faith as that of Return on equity, Thus the Bank profitability

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

is falling in comparison to the total assets held by it. The Return on Assets of the bank is very

low which indicates that the bank is not able to recover the appropriate return on assets held by

it..

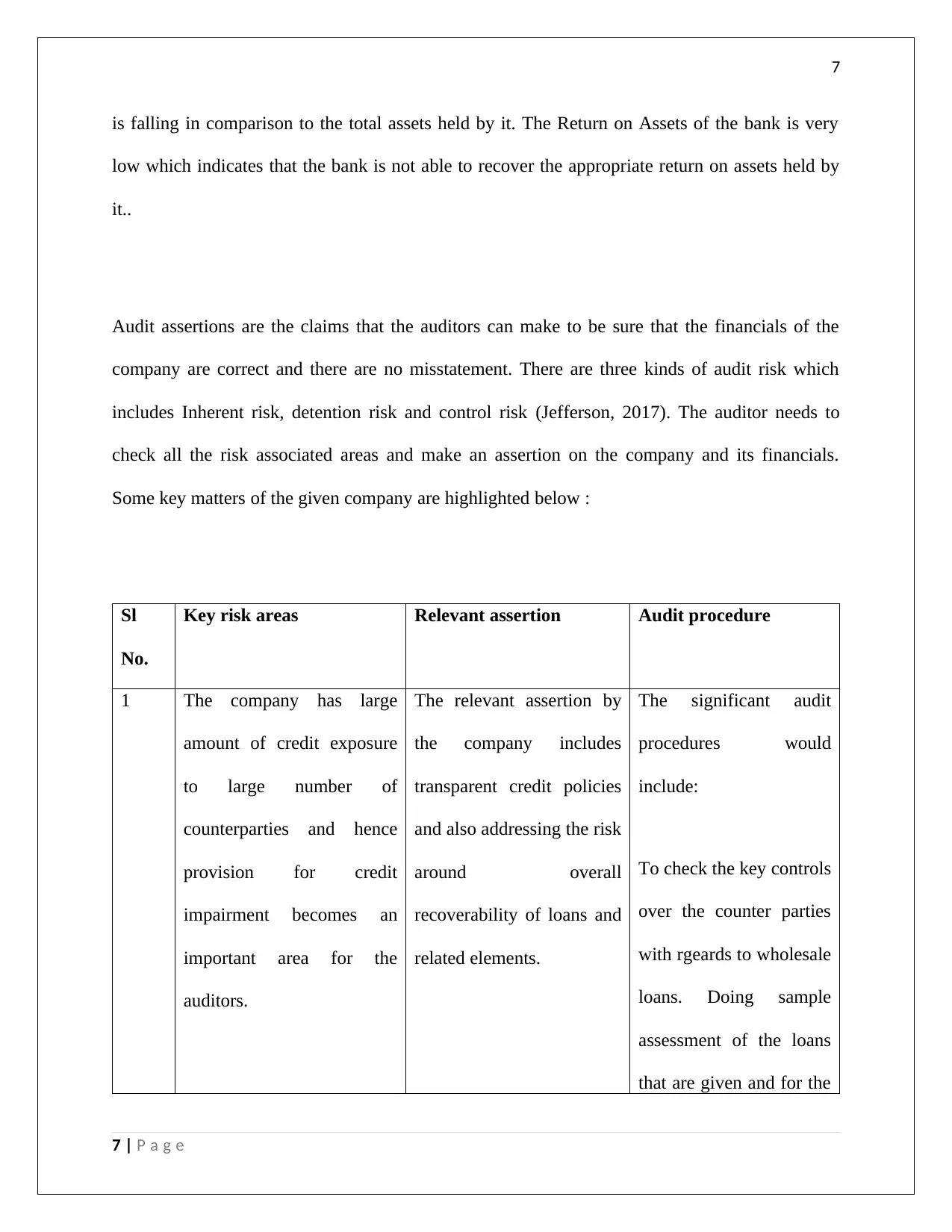

Audit assertions are the claims that the auditors can make to be sure that the financials of the

company are correct and there are no misstatement. There are three kinds of audit risk which

includes Inherent risk, detention risk and control risk (Jefferson, 2017). The auditor needs to

check all the risk associated areas and make an assertion on the company and its financials.

Some key matters of the given company are highlighted below :

Sl

No.

Key risk areas Relevant assertion Audit procedure

1 The company has large

amount of credit exposure

to large number of

counterparties and hence

provision for credit

impairment becomes an

important area for the

auditors.

The relevant assertion by

the company includes

transparent credit policies

and also addressing the risk

around overall

recoverability of loans and

related elements.

The significant audit

procedures would

include:

To check the key controls

over the counter parties

with rgeards to wholesale

loans. Doing sample

assessment of the loans

that are given and for the

7 | P a g e

is falling in comparison to the total assets held by it. The Return on Assets of the bank is very

low which indicates that the bank is not able to recover the appropriate return on assets held by

it..

Audit assertions are the claims that the auditors can make to be sure that the financials of the

company are correct and there are no misstatement. There are three kinds of audit risk which

includes Inherent risk, detention risk and control risk (Jefferson, 2017). The auditor needs to

check all the risk associated areas and make an assertion on the company and its financials.

Some key matters of the given company are highlighted below :

Sl

No.

Key risk areas Relevant assertion Audit procedure

1 The company has large

amount of credit exposure

to large number of

counterparties and hence

provision for credit

impairment becomes an

important area for the

auditors.

The relevant assertion by

the company includes

transparent credit policies

and also addressing the risk

around overall

recoverability of loans and

related elements.

The significant audit

procedures would

include:

To check the key controls

over the counter parties

with rgeards to wholesale

loans. Doing sample

assessment of the loans

that are given and for the

7 | P a g e

8

retail loans checking the

system that records the

loans and all the arrears

needs to be studied.

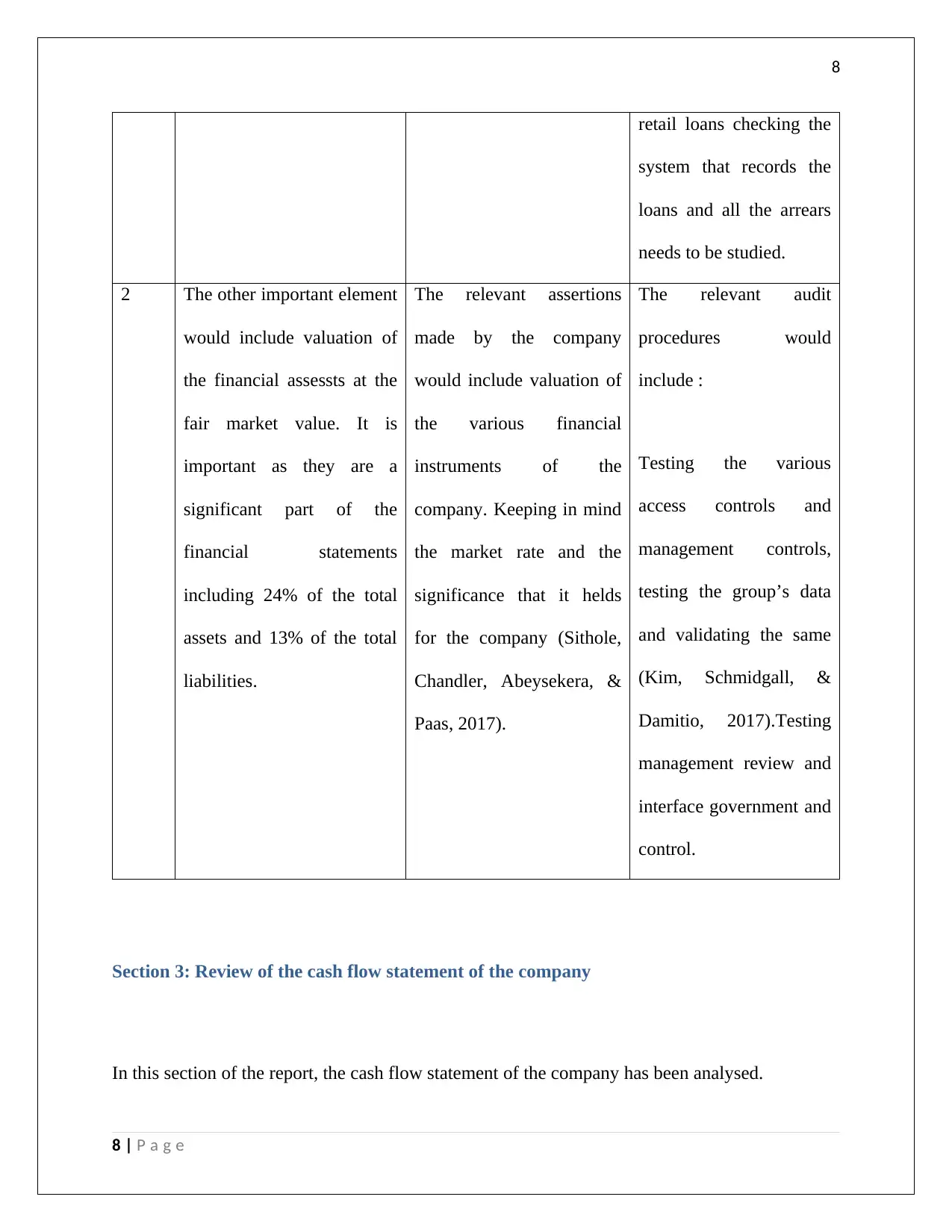

2 The other important element

would include valuation of

the financial assessts at the

fair market value. It is

important as they are a

significant part of the

financial statements

including 24% of the total

assets and 13% of the total

liabilities.

The relevant assertions

made by the company

would include valuation of

the various financial

instruments of the

company. Keeping in mind

the market rate and the

significance that it helds

for the company (Sithole,

Chandler, Abeysekera, &

Paas, 2017).

The relevant audit

procedures would

include :

Testing the various

access controls and

management controls,

testing the group’s data

and validating the same

(Kim, Schmidgall, &

Damitio, 2017).Testing

management review and

interface government and

control.

Section 3: Review of the cash flow statement of the company

In this section of the report, the cash flow statement of the company has been analysed.

8 | P a g e

retail loans checking the

system that records the

loans and all the arrears

needs to be studied.

2 The other important element

would include valuation of

the financial assessts at the

fair market value. It is

important as they are a

significant part of the

financial statements

including 24% of the total

assets and 13% of the total

liabilities.

The relevant assertions

made by the company

would include valuation of

the various financial

instruments of the

company. Keeping in mind

the market rate and the

significance that it helds

for the company (Sithole,

Chandler, Abeysekera, &

Paas, 2017).

The relevant audit

procedures would

include :

Testing the various

access controls and

management controls,

testing the group’s data

and validating the same

(Kim, Schmidgall, &

Damitio, 2017).Testing

management review and

interface government and

control.

Section 3: Review of the cash flow statement of the company

In this section of the report, the cash flow statement of the company has been analysed.

8 | P a g e

9

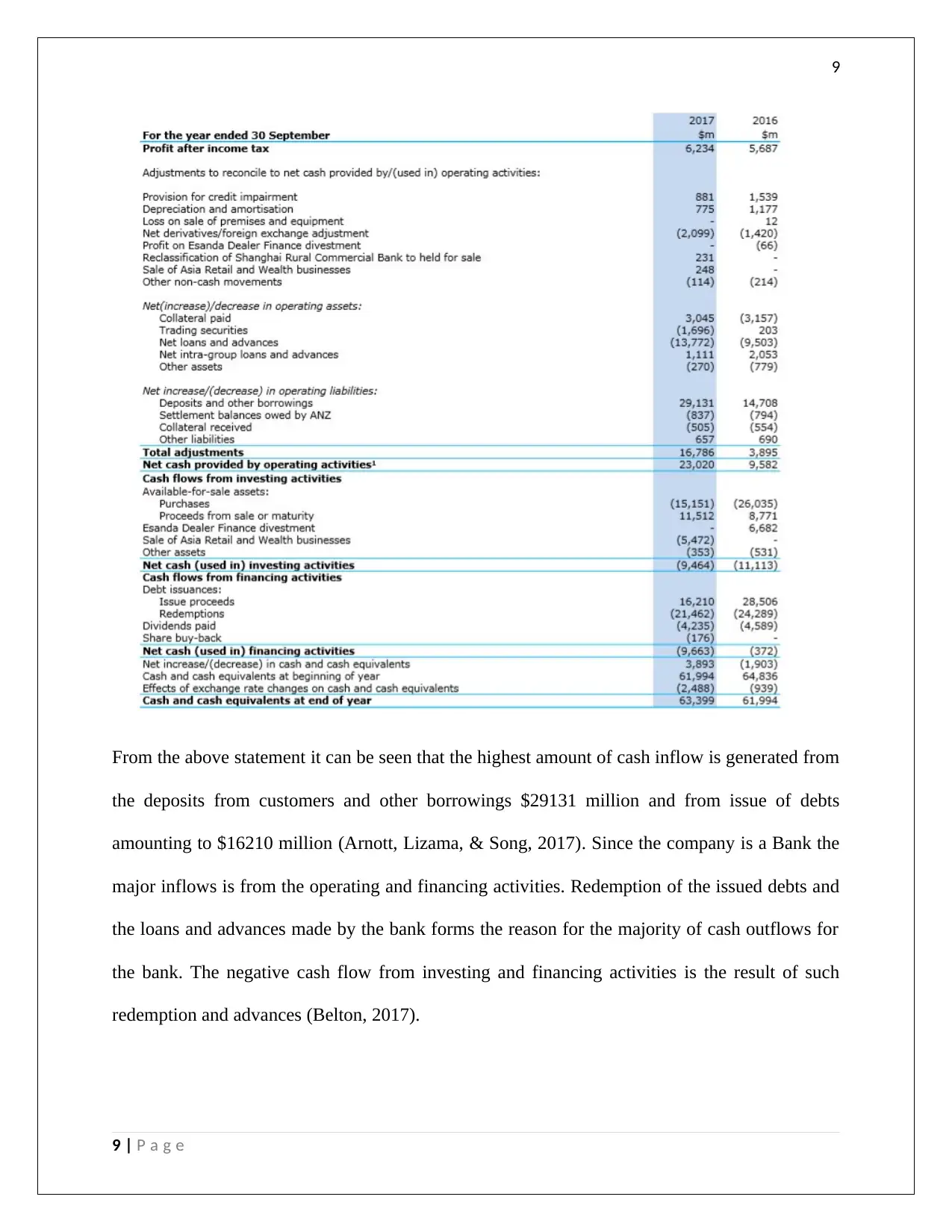

From the above statement it can be seen that the highest amount of cash inflow is generated from

the deposits from customers and other borrowings $29131 million and from issue of debts

amounting to $16210 million (Arnott, Lizama, & Song, 2017). Since the company is a Bank the

major inflows is from the operating and financing activities. Redemption of the issued debts and

the loans and advances made by the bank forms the reason for the majority of cash outflows for

the bank. The negative cash flow from investing and financing activities is the result of such

redemption and advances (Belton, 2017).

9 | P a g e

From the above statement it can be seen that the highest amount of cash inflow is generated from

the deposits from customers and other borrowings $29131 million and from issue of debts

amounting to $16210 million (Arnott, Lizama, & Song, 2017). Since the company is a Bank the

major inflows is from the operating and financing activities. Redemption of the issued debts and

the loans and advances made by the bank forms the reason for the majority of cash outflows for

the bank. The negative cash flow from investing and financing activities is the result of such

redemption and advances (Belton, 2017).

9 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

Among the operating activities the net deposits and other borrowings forms the majority of

inflows compensated by the net loans and advances which forms the majority of outflows. The

deposits for the bank have increased considerably from the previous year which indicates the

increase in the goodwill of the bank. The increase in loans and advances indicates the increase in

profitability of the bank (Das, 2017).

The financing activities involve the highest increase in outflows when compared to the previous

year and is the main reason for the negative cash outflow of the bank. Though the redemption of

debt has reduced, the reduction in the issue proceeds has a higher magnitude. The company has

also bought back shares which show that the bank has huge amount of reserves and is in a

favourable position to continue its business.

Thus finally we can conclude that the Bank is having a very good profitability and also having a

great liquidity position. The financial statement analysis shows that the bank has grown

considerably when compared to the previous year. The only major concern being the huge loss

due to the changes in the exchange rates, the bank should make reserves for such losses as the

bank cannot control such changes in exchange rates (Grenier, 2017).

10 | P a g e

Among the operating activities the net deposits and other borrowings forms the majority of

inflows compensated by the net loans and advances which forms the majority of outflows. The

deposits for the bank have increased considerably from the previous year which indicates the

increase in the goodwill of the bank. The increase in loans and advances indicates the increase in

profitability of the bank (Das, 2017).

The financing activities involve the highest increase in outflows when compared to the previous

year and is the main reason for the negative cash outflow of the bank. Though the redemption of

debt has reduced, the reduction in the issue proceeds has a higher magnitude. The company has

also bought back shares which show that the bank has huge amount of reserves and is in a

favourable position to continue its business.

Thus finally we can conclude that the Bank is having a very good profitability and also having a

great liquidity position. The financial statement analysis shows that the bank has grown

considerably when compared to the previous year. The only major concern being the huge loss

due to the changes in the exchange rates, the bank should make reserves for such losses as the

bank cannot control such changes in exchange rates (Grenier, 2017).

10 | P a g e

11

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97, 58-68.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), 10-17.

Erik, H., & Jan, B. (2017). Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management,

47(8), 712-735.

11 | P a g e

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97, 58-68.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), 10-17.

Erik, H., & Jan, B. (2017). Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management,

47(8), 712-735.

11 | P a g e

12

Farmer, Y. (2018). Ethical Decision Making and Reputation Management in Public Relations. Journal of

Media Ethics, 1-12.

Grenier, J. (2017). Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), 241-256.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kim, M., Schmidgall, R., & Damitio, J. (2017). Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of

Hospitality & Tourism Administration, , 18(1), 23-40.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25, 57-80.

12 | P a g e

Farmer, Y. (2018). Ethical Decision Making and Reputation Management in Public Relations. Journal of

Media Ethics, 1-12.

Grenier, J. (2017). Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), 241-256.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kim, M., Schmidgall, R., & Damitio, J. (2017). Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of

Hospitality & Tourism Administration, , 18(1), 23-40.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25, 57-80.

12 | P a g e

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.