Audit Issues of SCG: Comprehensive Analysis of Audit and Financials

VerifiedAdded on 2023/01/05

|16

|3203

|65

Report

AI Summary

This report examines the audit issues of Scentre Group (SCG), focusing on materiality, financial performance, and audit assertions. It analyzes key financial ratios, including return on investment, EBITDA margin, and net profit margin, comparing SCG's performance against industry averages. The report covers the application of materiality in auditing, the importance of financial statement assertions (existence, completeness, rights and obligations, accuracy and valuation, and presentation and disclosure), and an overview of SCG's cash flow from operations. The analysis highlights areas of concern, such as declining year-on-year return on investment, and provides insights into the company's financial health and operational efficiency. This report is a valuable resource for understanding the financial aspects of SCG and the related audit considerations.

Running head: AUDIT ISSUES OF SCG

Audit Issues of SCG

Name of the Student

Name of the University

Author note

Audit Issues of SCG

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT ISSUES OF SCG

Table of Contents

Section 1.....................................................................................................................................3

Section 2.....................................................................................................................................6

Section 3...................................................................................................................................11

Reference..................................................................................................................................13

Table of Contents

Section 1.....................................................................................................................................3

Section 2.....................................................................................................................................6

Section 3...................................................................................................................................11

Reference..................................................................................................................................13

2AUDIT ISSUES OF SCG

Section 1

Level of materiality to be used

For financial reporting materiality is the most important factor that is to be considered by the

auditor. The international standard of auditing highlight the following features

The material misstatements are considered if they could influence the decisions of users of

the financial statements.

The materiality can be judged based on the situation including the size and nature of the

misstatements.

The user’s common needs as a group is also considered as base for the judgement of the

materiality.

The importance of materiality from the viewpoint of the auditors is that the auditors

require reasonable assurance regarding the fact that the financial statement based on which

the auditor will give his report is free from any material misstatements. The concept of

materiality is the basic need for any audit work. It is applied by the auditors at the initial stage

of planning and the while performing the audit work and to assess the effect of the identified

misstatements on the audit and of uncorrected misstatements in the financial statements.

The guidance set by the international standard for auditing is the fundamental

principle for determining the concept of materiality. The auditors follow the guidelines of the

ISA requirements on materiality and uses practical examples to highlight good practices, key

challenges and common pitfalls. The rules and framework of the ISA is made with the

objective of helping the audit firms to better understand the materiality concept and to make

proper planning to evaluate any material misstatements in the financial statements (Graham

Bedard & Dutta 2018).

Section 1

Level of materiality to be used

For financial reporting materiality is the most important factor that is to be considered by the

auditor. The international standard of auditing highlight the following features

The material misstatements are considered if they could influence the decisions of users of

the financial statements.

The materiality can be judged based on the situation including the size and nature of the

misstatements.

The user’s common needs as a group is also considered as base for the judgement of the

materiality.

The importance of materiality from the viewpoint of the auditors is that the auditors

require reasonable assurance regarding the fact that the financial statement based on which

the auditor will give his report is free from any material misstatements. The concept of

materiality is the basic need for any audit work. It is applied by the auditors at the initial stage

of planning and the while performing the audit work and to assess the effect of the identified

misstatements on the audit and of uncorrected misstatements in the financial statements.

The guidance set by the international standard for auditing is the fundamental

principle for determining the concept of materiality. The auditors follow the guidelines of the

ISA requirements on materiality and uses practical examples to highlight good practices, key

challenges and common pitfalls. The rules and framework of the ISA is made with the

objective of helping the audit firms to better understand the materiality concept and to make

proper planning to evaluate any material misstatements in the financial statements (Graham

Bedard & Dutta 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT ISSUES OF SCG

There are no fixed formulae to determine the materiality but there are three basic steps

following which the auditors will be able to determine the materiality of the financial

statements these are stated below:

Setting a benchmark

Determining the level of the benchmark

Choice justification

The framework of the IAS looks at these steps and the potential challenges that arise.

It provide rules regarding the fact that what might be appropriate to set specific level of

materiality for individual type of transactions and what to do with the long period

transactions where it is required to reassess the materiality concept. The framework also

explains what performance materiality is, providing the guidelines on how it can be

determined (Chen & Teng 2015).

The application of the materiality concept to identify the misstatements can be done

by following the guidelines

Accumulating misstatements during the course of audit

Categorising misstatement according to the nature

Assessment of the materiality of the misstatements

Impact of misstatements on the audit

Just like the audit of single entity group auditors the auditors of the group companies

must use judgement to determine the group materiality and group performance materiality.

the key difference between the group company audit is that the in group companies the

auditors also have to determine levels of component materiality for companies that have

audits for the purpose of the group audits. the framework of the international standard for

audit give the auditors an idea about the process to determine the component materiality and

There are no fixed formulae to determine the materiality but there are three basic steps

following which the auditors will be able to determine the materiality of the financial

statements these are stated below:

Setting a benchmark

Determining the level of the benchmark

Choice justification

The framework of the IAS looks at these steps and the potential challenges that arise.

It provide rules regarding the fact that what might be appropriate to set specific level of

materiality for individual type of transactions and what to do with the long period

transactions where it is required to reassess the materiality concept. The framework also

explains what performance materiality is, providing the guidelines on how it can be

determined (Chen & Teng 2015).

The application of the materiality concept to identify the misstatements can be done

by following the guidelines

Accumulating misstatements during the course of audit

Categorising misstatement according to the nature

Assessment of the materiality of the misstatements

Impact of misstatements on the audit

Just like the audit of single entity group auditors the auditors of the group companies

must use judgement to determine the group materiality and group performance materiality.

the key difference between the group company audit is that the in group companies the

auditors also have to determine levels of component materiality for companies that have

audits for the purpose of the group audits. the framework of the international standard for

audit give the auditors an idea about the process to determine the component materiality and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT ISSUES OF SCG

component performance materiality , component materiality of associates and joint ventures

and the effect of changes in group materiality (Brooks & Guo 2015).

There is no rule to determine the level of materiality but it is determined on the basis

of the professional judgement of the auditor. The two examples of applying a percentage to a

benchmark are for a profit making manufacturing unit, which is 5 percentage of profit before

tax, and for not for profit the benchmark is 1 percentage of before tax profit (Zhukova &

Zhukov 2018).

The 5-percentage rule is the best quantitative estimates to help the auditor to identify

the potential material transactions and events. The 5-percentage rule states that the reasonable

investors would not be influenced in their investment decisions by a fluctuation in net income

of 5 percentage or less than that. Nor would the investor be persuaded by a series of

fluctuation of less than 5 percentage in income statement line items as long as the net change

in percentage is less than the 5 percentage. This theory has been the fundamental behind the

working materiality estimates and that is the reason why this method has been used to

determine the materiality level of Scentre group staples securities ltd (Glover Taylor & Wu

2016).

In the draft report the company has disclosed the following matters

Basis of accounting

The financial report has been prepared using the same accounting principle that has

been used in the preparation of the previous financial year which indicates that the company

has maintained the principle of maintaining uniformity in maintaining a particular standard of

accounting (Tamulevičienė 2016).

component performance materiality , component materiality of associates and joint ventures

and the effect of changes in group materiality (Brooks & Guo 2015).

There is no rule to determine the level of materiality but it is determined on the basis

of the professional judgement of the auditor. The two examples of applying a percentage to a

benchmark are for a profit making manufacturing unit, which is 5 percentage of profit before

tax, and for not for profit the benchmark is 1 percentage of before tax profit (Zhukova &

Zhukov 2018).

The 5-percentage rule is the best quantitative estimates to help the auditor to identify

the potential material transactions and events. The 5-percentage rule states that the reasonable

investors would not be influenced in their investment decisions by a fluctuation in net income

of 5 percentage or less than that. Nor would the investor be persuaded by a series of

fluctuation of less than 5 percentage in income statement line items as long as the net change

in percentage is less than the 5 percentage. This theory has been the fundamental behind the

working materiality estimates and that is the reason why this method has been used to

determine the materiality level of Scentre group staples securities ltd (Glover Taylor & Wu

2016).

In the draft report the company has disclosed the following matters

Basis of accounting

The financial report has been prepared using the same accounting principle that has

been used in the preparation of the previous financial year which indicates that the company

has maintained the principle of maintaining uniformity in maintaining a particular standard of

accounting (Tamulevičienė 2016).

5AUDIT ISSUES OF SCG

Corporate information

The financial report of Scentre group trust and its controlled entities for the year

ended 2018 was approved in accordance with a resolution of the board of directors of Scentre

management limited as a responsible entity of SGT.

Basis of preparation of the financial report

The company has followed all the regulation of the corporation act and that brings

transparency in the preparation in the financial reports. The company has made all necessary

disclosures in the financial report that are necessary to disclose any material interest of the

related parties (Gallizo Larraz & Saladrigues Solé 2016).

Note 33 contingent liability

The entities of scentre group have provide guarantees in respect of certain Westfield

corporation limited joint venture operations in the united kingdom. Under the restructure and

merger implementation deed the entities of centre group and Westland corporation have cross

indemnified each other for any claims that may be made or payment that may be required

under such guarantees (https://www.scentregroup.com. pg no 68)

Section 2

The company is engaged in the business of ownership development of branded

shopping centre in Australia and New Zealand. It operates with following segments like

property investment and project management. The property investment segments includes net

property income from existing shopping centre and completed developments and other

operational expenses. Property management section includes external fee income from third

Corporate information

The financial report of Scentre group trust and its controlled entities for the year

ended 2018 was approved in accordance with a resolution of the board of directors of Scentre

management limited as a responsible entity of SGT.

Basis of preparation of the financial report

The company has followed all the regulation of the corporation act and that brings

transparency in the preparation in the financial reports. The company has made all necessary

disclosures in the financial report that are necessary to disclose any material interest of the

related parties (Gallizo Larraz & Saladrigues Solé 2016).

Note 33 contingent liability

The entities of scentre group have provide guarantees in respect of certain Westfield

corporation limited joint venture operations in the united kingdom. Under the restructure and

merger implementation deed the entities of centre group and Westland corporation have cross

indemnified each other for any claims that may be made or payment that may be required

under such guarantees (https://www.scentregroup.com. pg no 68)

Section 2

The company is engaged in the business of ownership development of branded

shopping centre in Australia and New Zealand. It operates with following segments like

property investment and project management. The property investment segments includes net

property income from existing shopping centre and completed developments and other

operational expenses. Property management section includes external fee income from third

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT ISSUES OF SCG

parties. The company is increasing its business rapidly and performing very efficiently which

increases the potentiality of the company in the future (Swart 2018).

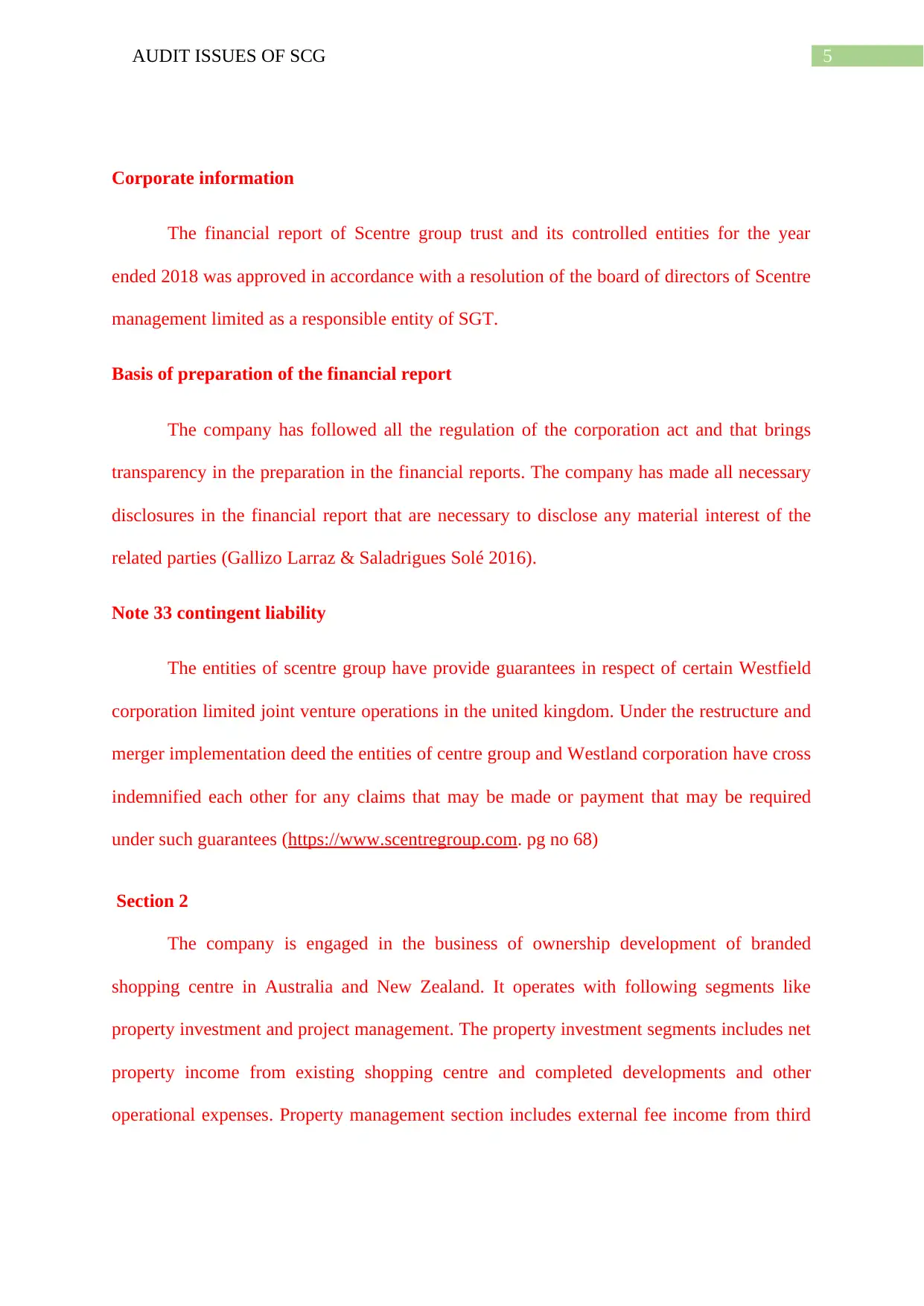

The receivable turnover of the company is moderate that means the company is able

to realise the amount from the debtors to whom it sales its products. The asset turnover ratio

is moderate and at par with the industry average so it indicates that the company is doing its

business in keeping pace with the overall standard of the industry.

Return on investment

parties. The company is increasing its business rapidly and performing very efficiently which

increases the potentiality of the company in the future (Swart 2018).

The receivable turnover of the company is moderate that means the company is able

to realise the amount from the debtors to whom it sales its products. The asset turnover ratio

is moderate and at par with the industry average so it indicates that the company is doing its

business in keeping pace with the overall standard of the industry.

Return on investment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT ISSUES OF SCG

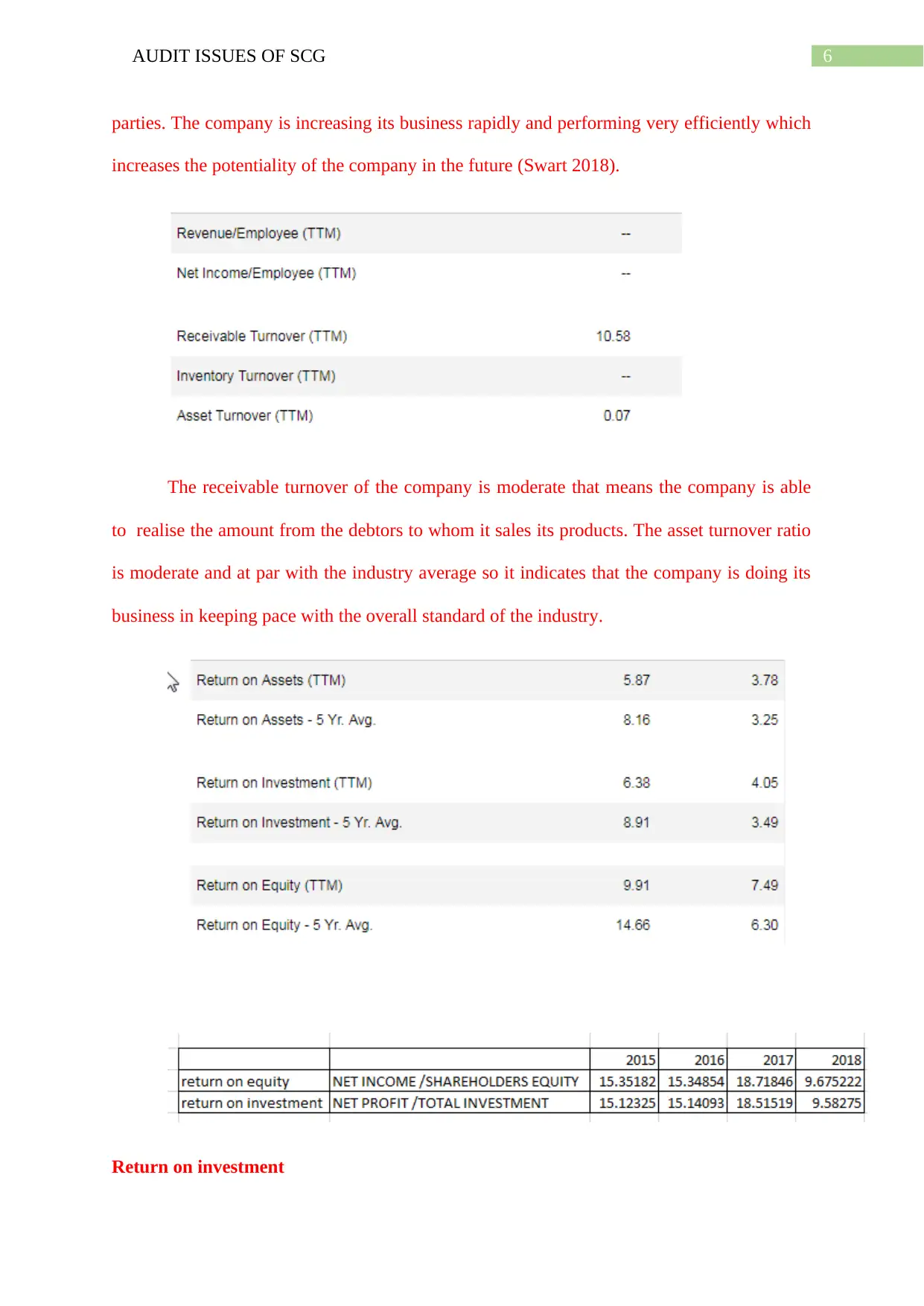

The return on investment indicates that how much the investors can earn by investing

in the company. This ratio is a good indicator that how well the company is performing in

comparison to its competitors. The return on investment ratio of SCG is 8.91 percent and the

industry average ratio is 3.91, which means that the company is performing well and for that,

it is giving good return to its investors. The investors will be able to increase their investment

value by investing in the company. This indicates that the company will be able to sustain for

long period in the industry (Zhang 2018). The auditors found that the company’s year on year

basis return on investment is falling in 2015 is 15.12 percent and that decreased to 9.58

percentage in 2018 which is considered as a major concern for the organisation and the

stakeholders of the company.

Return on equity

The return on equity is the ratio that indicates that the shares of the company is in

uptrend and the how much return the shareholders will get by investing in the equity shares

of the company. The return on equity of the company is 14.66 percentage that means that the

shareholders will get a return of 14.66 percentage if they invest in the shares of the company.

The company in this ratio also beaten the industry average and that indicates the steady

performance of the company. the return on equity has fallen in the last few years the auditors

has analysed this matter and give a note to the management regarding this fact.

Income statement ratios

The return on investment indicates that how much the investors can earn by investing

in the company. This ratio is a good indicator that how well the company is performing in

comparison to its competitors. The return on investment ratio of SCG is 8.91 percent and the

industry average ratio is 3.91, which means that the company is performing well and for that,

it is giving good return to its investors. The investors will be able to increase their investment

value by investing in the company. This indicates that the company will be able to sustain for

long period in the industry (Zhang 2018). The auditors found that the company’s year on year

basis return on investment is falling in 2015 is 15.12 percent and that decreased to 9.58

percentage in 2018 which is considered as a major concern for the organisation and the

stakeholders of the company.

Return on equity

The return on equity is the ratio that indicates that the shares of the company is in

uptrend and the how much return the shareholders will get by investing in the equity shares

of the company. The return on equity of the company is 14.66 percentage that means that the

shareholders will get a return of 14.66 percentage if they invest in the shares of the company.

The company in this ratio also beaten the industry average and that indicates the steady

performance of the company. the return on equity has fallen in the last few years the auditors

has analysed this matter and give a note to the management regarding this fact.

Income statement ratios

8AUDIT ISSUES OF SCG

EBITDA margin

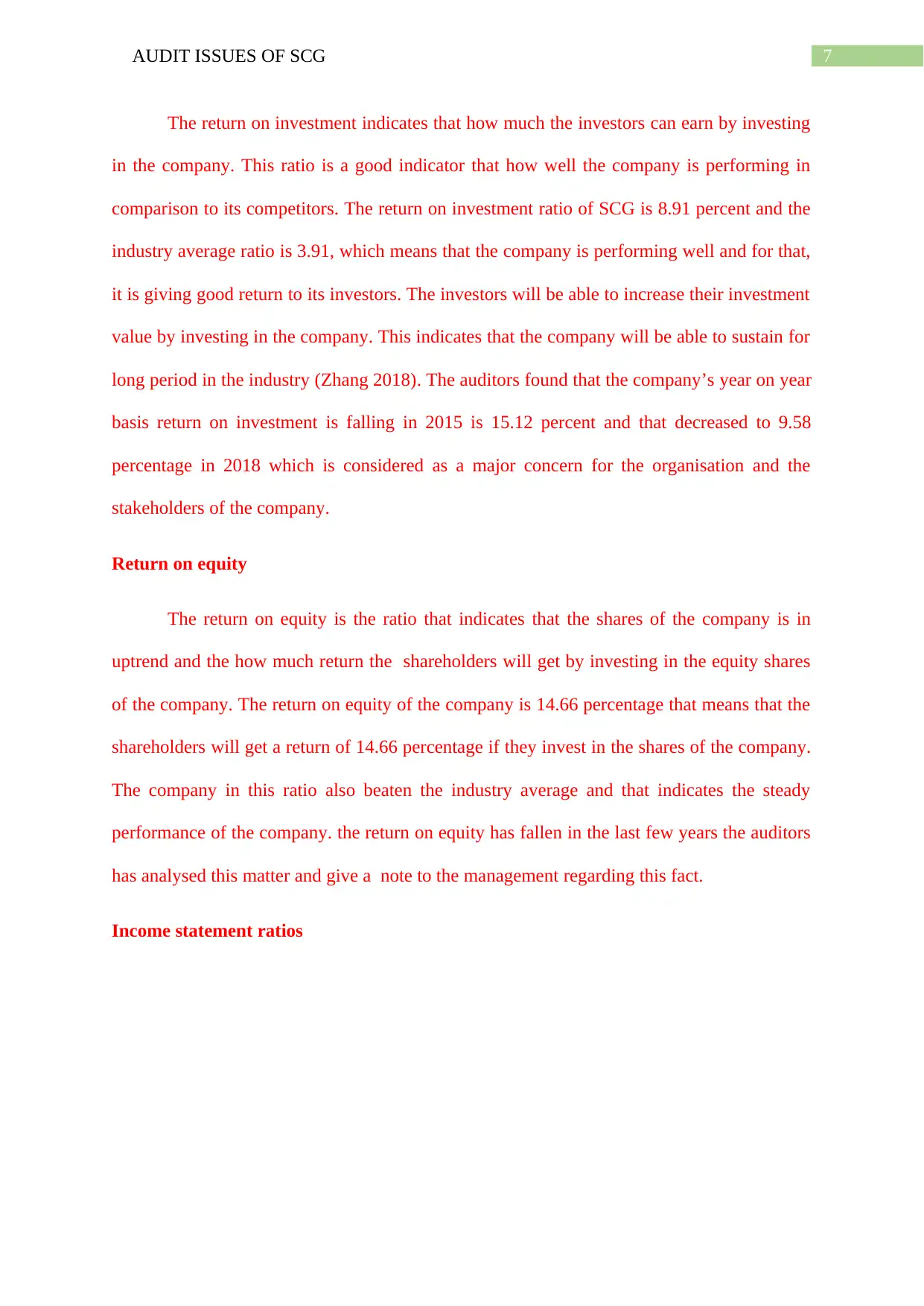

The EBITDA margin indicates that the companies earning capacity before paying

interest, taxes, and other non-cash items. This ratio is decreasing on a continuous basis from

the year 2015 to 2018. The five-year average ratio of the company is 62.88, which is higher

than that of the other companies (Wu et al 2016).

Operating margin

The operating margin of the company is 73.02, which shows the efficiency of the

company to operate with high profit margin. The industry margin is only 52.43 which means

that the company is far more ahead than the industry if the operating ratio is considered as a

benchmark (Salawu Moromoke Oladejo & Godwin 2017). However, the trend of the

company on year to year basis is decreasing which the auditors consider as a major issue for

the company. to inspect this the auditors have decided to take internal audit process to

identify the real reason behind the fall of the operating profit on year to year basis.

Net profit margin

The net profit margin is the most important ratio to determine the overall efficiency of

the company. In this ratio, also, the company is far more ahead of the industry, the industry’s

ratio is 47.73 percentage whereas the net profit margin of the company is 113.26 percentage

EBITDA margin

The EBITDA margin indicates that the companies earning capacity before paying

interest, taxes, and other non-cash items. This ratio is decreasing on a continuous basis from

the year 2015 to 2018. The five-year average ratio of the company is 62.88, which is higher

than that of the other companies (Wu et al 2016).

Operating margin

The operating margin of the company is 73.02, which shows the efficiency of the

company to operate with high profit margin. The industry margin is only 52.43 which means

that the company is far more ahead than the industry if the operating ratio is considered as a

benchmark (Salawu Moromoke Oladejo & Godwin 2017). However, the trend of the

company on year to year basis is decreasing which the auditors consider as a major issue for

the company. to inspect this the auditors have decided to take internal audit process to

identify the real reason behind the fall of the operating profit on year to year basis.

Net profit margin

The net profit margin is the most important ratio to determine the overall efficiency of

the company. In this ratio, also, the company is far more ahead of the industry, the industry’s

ratio is 47.73 percentage whereas the net profit margin of the company is 113.26 percentage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT ISSUES OF SCG

which is double than the industry average this shows how effectively the organisation has

performed.

The key risk areas for the audit is that the company is beating the industry in all the

ratios though the sector of the business is not giving good results this might be a area where

the auditor may address in the audit plan (Choudhary Merkley & Schipper 2017). In respect

of the year to year basis performance the company’s result is poor but in comparison to the

industry it is far more ahead of the other competitors.

The main five financial assertions are stated below

Existence

The assertion of existence means that the assets liabilities and the shareholders equity

balances that are appearing in the financial reports of the company really exist or not.

Completeness

The assertion of completeness is an assertion that the financial statements made are

thorough and include every item that should be included in the statement for a given

accounting period.

Rights and obligation

The assertion of rights and obligation is a basic assertion that all assets and liabilities

included in a financial statement belong to the company that is issuing the statements.

Accuracy and valuation

which is double than the industry average this shows how effectively the organisation has

performed.

The key risk areas for the audit is that the company is beating the industry in all the

ratios though the sector of the business is not giving good results this might be a area where

the auditor may address in the audit plan (Choudhary Merkley & Schipper 2017). In respect

of the year to year basis performance the company’s result is poor but in comparison to the

industry it is far more ahead of the other competitors.

The main five financial assertions are stated below

Existence

The assertion of existence means that the assets liabilities and the shareholders equity

balances that are appearing in the financial reports of the company really exist or not.

Completeness

The assertion of completeness is an assertion that the financial statements made are

thorough and include every item that should be included in the statement for a given

accounting period.

Rights and obligation

The assertion of rights and obligation is a basic assertion that all assets and liabilities

included in a financial statement belong to the company that is issuing the statements.

Accuracy and valuation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT ISSUES OF SCG

The assertion of valuation is the statement that all the figures that are given in the

financial statements are accurate and based on the proper valuation methods.

Presentation and disclosure

The final assertion of the financial statements is that of presentation and disclosure.

This is the assertion that all appropriate information and disclosure regarding the company’s

financial statements are included in the statement and all the information presented in the

statement is presented in affair and transparent manner that facilitates ease of understanding

the information contained in the statement (Eilifsen Hamilton & Messier Jr 2017).

Section 3

The assertion of valuation is the statement that all the figures that are given in the

financial statements are accurate and based on the proper valuation methods.

Presentation and disclosure

The final assertion of the financial statements is that of presentation and disclosure.

This is the assertion that all appropriate information and disclosure regarding the company’s

financial statements are included in the statement and all the information presented in the

statement is presented in affair and transparent manner that facilitates ease of understanding

the information contained in the statement (Eilifsen Hamilton & Messier Jr 2017).

Section 3

11AUDIT ISSUES OF SCG

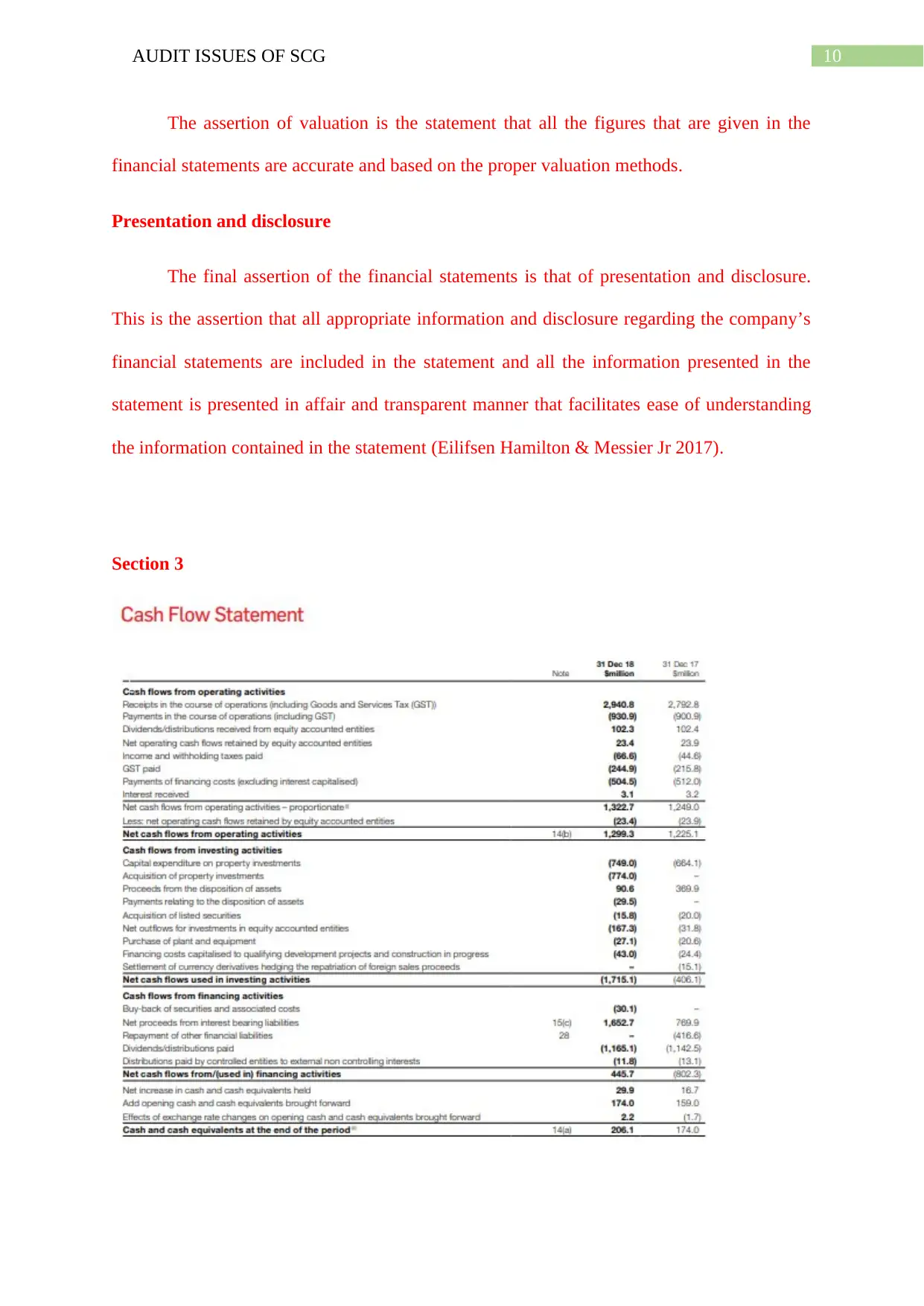

From the above table it is observed that the company’ cash flow from operation

generates the highest of cash inflows the cash inflow from the operating activity is $1322.70

in 2018 and it has increased from $1249.00 in the year 2017. This indicates that the company

is operating with efficiency and generates cash inflows for the

organisation(https://www.scentregroup.com pg no 37).

The company has the greatest outflow in the investing activities the net cash outflow

from the investing activity is $1715.10 in the financial year 2018 and in the year 2017 it was

$406.10, which means that the company has made huge amount of investments during this

period of one year.

The company‘s primary cash receipt is from the operational activity and its main cash

payments are capital expenditure on property investments and the payment statutory

obligation like the GST payment (Lakis & Masiulevičius 2017).

The main non-cash items of the financial activities are the buyback of securities and

associated costs and distribution paid by controlling entities to external non-control interests.

The main non-cash investing activities are the net outflows for investing in equity accounted

entities.

A going concern concept means that a business that does not have any risk of getting

insolvent in the near future. From the review of the cash flow it is observed that the company

has sufficient cash position to sustain in the long run (https://www.scentregroup.com pg no

32). Therefore, there is no risk of the company to declare itself as insolvent in the near future

(Del Giudice De Paola & Cantisani 2017).

From the audit report of SCG, it can be observed that the company has maintained all

the accounting principles properly and that there is no material misstatements in the financial

statements of the company. The auditor also gives a clear certificate, which mentions that the

From the above table it is observed that the company’ cash flow from operation

generates the highest of cash inflows the cash inflow from the operating activity is $1322.70

in 2018 and it has increased from $1249.00 in the year 2017. This indicates that the company

is operating with efficiency and generates cash inflows for the

organisation(https://www.scentregroup.com pg no 37).

The company has the greatest outflow in the investing activities the net cash outflow

from the investing activity is $1715.10 in the financial year 2018 and in the year 2017 it was

$406.10, which means that the company has made huge amount of investments during this

period of one year.

The company‘s primary cash receipt is from the operational activity and its main cash

payments are capital expenditure on property investments and the payment statutory

obligation like the GST payment (Lakis & Masiulevičius 2017).

The main non-cash items of the financial activities are the buyback of securities and

associated costs and distribution paid by controlling entities to external non-control interests.

The main non-cash investing activities are the net outflows for investing in equity accounted

entities.

A going concern concept means that a business that does not have any risk of getting

insolvent in the near future. From the review of the cash flow it is observed that the company

has sufficient cash position to sustain in the long run (https://www.scentregroup.com pg no

32). Therefore, there is no risk of the company to declare itself as insolvent in the near future

(Del Giudice De Paola & Cantisani 2017).

From the audit report of SCG, it can be observed that the company has maintained all

the accounting principles properly and that there is no material misstatements in the financial

statements of the company. The auditor also gives a clear certificate, which mentions that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.