Audit of JBH-Hi Fi: Inherent Risk Factors, Key Matters and Significant Accounts

VerifiedAdded on 2023/06/07

|17

|3627

|410

AI Summary

This assignment discusses the inherent risk factors that can affect the audit of JBH-Hi Fi, the key matters which they should take into consideration and methods by which they can provide a correct opinion. It also highlights the significant accounts that the auditor needs to check. The assignment provides details about the company, its policies, competitors, and the rules and regulations that affect its operations. It also discusses the importance of corporate governance in the functioning of any company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDIT

2018

2018

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

By student name

Professor

Date: 13th Sep, 2018.

1 | P a g e

By student name

Professor

Date: 13th Sep, 2018.

1 | P a g e

2

Executive Summary

In this assignment, the overall elements that can affect the audit of a public limited company has

been discussed. The company that has been taken in consideration is JBH-Hi Fi which is one of

the top consumer products company in Australia. The audit of the company must be conducted

and various elements that as members of the audit team one should take into consideration is

discussed and stated. The main items that are the details about the competitors, the details about

the key audit matters and key assertions that might affect the company and should be in

knowledge of the auditors.

2 | P a g e

Executive Summary

In this assignment, the overall elements that can affect the audit of a public limited company has

been discussed. The company that has been taken in consideration is JBH-Hi Fi which is one of

the top consumer products company in Australia. The audit of the company must be conducted

and various elements that as members of the audit team one should take into consideration is

discussed and stated. The main items that are the details about the competitors, the details about

the key audit matters and key assertions that might affect the company and should be in

knowledge of the auditors.

2 | P a g e

3

CONTENTS:

Introduction......................……………….....................................................................................3

Analysis…........................……………….....................................................................................3

Conclusion.........................………………..................................................................................12

References......................……………….......................................................................................17

3 | P a g e

CONTENTS:

Introduction......................……………….....................................................................................3

Analysis…........................……………….....................................................................................3

Conclusion.........................………………..................................................................................12

References......................……………….......................................................................................17

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

Introduction

JBH is one of the largest company in Australia that deals in consumer retail products and

specializes in video games, mobile phones, electronics etc. The company was formed in 1974

and the company has expanded to other parts of the world also. The main headquarter of the

company is in Melbourne. The company initially started with selling Hi-Fi equipment and thus

the name came from there and later the company expanded its operations to other products that

were mostly consumer electronics. The aim of the company in the long run is to expand its

operations and deal in more variety of products (Abdullah & Said, 2017). Audit is an

independent examination of the books and the financial statements of the company to comment

whether they are free from all kind of errors and misstatements. In this assignment we shall

discuss various inherent risk factors that might affect the audit of JBH, the key matters which

they should take into consideration and methods by which they can provide a correct opinion.

The stakeholders depends on the audit report to take important decision regarding the company

and its operation and thus it is important that it must be free from errors. Various details

regarding the company, its policies and its competitors is discussed hereunder.

Analysis

1. JBH conducts its operations in various sectors that are mostly related to electronics that

are consumer retail products like mobile phones, CDs, Blue-ray, software and hardware

products. They initially started with selling Hi-Fi products and then moved to products

like CDs and Blue rays (Boghossian, 2017). Their main point of selling lies in CDs and

then in computer games, televisions and car stereos. The company is having 184 stores

across Australia and has now also expanded their operations to New Zealand. It is the

4 | P a g e

Introduction

JBH is one of the largest company in Australia that deals in consumer retail products and

specializes in video games, mobile phones, electronics etc. The company was formed in 1974

and the company has expanded to other parts of the world also. The main headquarter of the

company is in Melbourne. The company initially started with selling Hi-Fi equipment and thus

the name came from there and later the company expanded its operations to other products that

were mostly consumer electronics. The aim of the company in the long run is to expand its

operations and deal in more variety of products (Abdullah & Said, 2017). Audit is an

independent examination of the books and the financial statements of the company to comment

whether they are free from all kind of errors and misstatements. In this assignment we shall

discuss various inherent risk factors that might affect the audit of JBH, the key matters which

they should take into consideration and methods by which they can provide a correct opinion.

The stakeholders depends on the audit report to take important decision regarding the company

and its operation and thus it is important that it must be free from errors. Various details

regarding the company, its policies and its competitors is discussed hereunder.

Analysis

1. JBH conducts its operations in various sectors that are mostly related to electronics that

are consumer retail products like mobile phones, CDs, Blue-ray, software and hardware

products. They initially started with selling Hi-Fi products and then moved to products

like CDs and Blue rays (Boghossian, 2017). Their main point of selling lies in CDs and

then in computer games, televisions and car stereos. The company is having 184 stores

across Australia and has now also expanded their operations to New Zealand. It is the

4 | P a g e

5

seventh largest electronics and home appliance consumer in the world, based on its

overall revenue.

2. The four primary competitors of JB Hi-Fi in Australia are –

Best Buy

Ceconomy

Gome

M video

All these companies operate in the same business line of retail distribution and consumer

supplies. Few of the companies are doing better than JBH and few are doing less.

3. JB Hi- Fi is operating in the Australian Region and there are various rules and regulations

that affects the operations of the company. Few of these rules apart from the standard

rules and regulations are stated below:

Australian Securities Exchange Listing Rules – The company is listed on the stock

exchange of Australia and to issue any new shares or any kind of activities related to

the shares the company needs to follow the rules of the listing agreement that has

been issued by the Stock Exchange. In case the management fails, the shares can be

suspended and the company must bear heavy losses (Bouret, 2017).

Fair Trading Act Australia – The aim of this is that the consumers are protected and

they have the correct information about the products and services that they are

availing from the retail market. The Fair-Trading Act Australia is related to the

Australian Federal and State laws and aims to provide the consumers protection from

unfair trade practices. And hence it affects the operations of JBH.

5 | P a g e

seventh largest electronics and home appliance consumer in the world, based on its

overall revenue.

2. The four primary competitors of JB Hi-Fi in Australia are –

Best Buy

Ceconomy

Gome

M video

All these companies operate in the same business line of retail distribution and consumer

supplies. Few of the companies are doing better than JBH and few are doing less.

3. JB Hi- Fi is operating in the Australian Region and there are various rules and regulations

that affects the operations of the company. Few of these rules apart from the standard

rules and regulations are stated below:

Australian Securities Exchange Listing Rules – The company is listed on the stock

exchange of Australia and to issue any new shares or any kind of activities related to

the shares the company needs to follow the rules of the listing agreement that has

been issued by the Stock Exchange. In case the management fails, the shares can be

suspended and the company must bear heavy losses (Bouret, 2017).

Fair Trading Act Australia – The aim of this is that the consumers are protected and

they have the correct information about the products and services that they are

availing from the retail market. The Fair-Trading Act Australia is related to the

Australian Federal and State laws and aims to provide the consumers protection from

unfair trade practices. And hence it affects the operations of JBH.

5 | P a g e

6

International Taxation laws – Given the fact that JBH has operations even in New

Zealand. The company must abide by the international taxation laws, to avoid double

taxation and maintaining the rules and regulations that are related to import and

export. The company needs to abide by the rules of the international tax laws and

regulations of New Zealand when they indulge in business in their area.

Australian Banking Regulation Act – The rules of these laws also extend to Retail

companies in Australia as companies must deal with banks and most of the

transactions are initiated through that. Also, the company has raised loans from

financial institutions thus that is also applicable to the company on how they are

managing the terms and agreement of loans with other financial parties (Delone &

Mclean, 2004).

4. Four key inherent risk factors that can affect the operations of the company are stated

below. These risk factors are due to the operational strategies and other elements that

affects the growth of the company. To mitigate these risk factors, it is important that the

management of the company is having proper internal controls in place. Few of these

material inherent risk factors are stated below:

Competition – The overall competition in the market in which the group operates is

huge. This increased competition often leads to decrease in the overall sales and

profitability for the company. There is also a chance that the auditors end up sharing the

confidential information of the company with the outsider and that might affect the

company badly. Thus the best away company can deal with this kind of risk by providing

6 | P a g e

International Taxation laws – Given the fact that JBH has operations even in New

Zealand. The company must abide by the international taxation laws, to avoid double

taxation and maintaining the rules and regulations that are related to import and

export. The company needs to abide by the rules of the international tax laws and

regulations of New Zealand when they indulge in business in their area.

Australian Banking Regulation Act – The rules of these laws also extend to Retail

companies in Australia as companies must deal with banks and most of the

transactions are initiated through that. Also, the company has raised loans from

financial institutions thus that is also applicable to the company on how they are

managing the terms and agreement of loans with other financial parties (Delone &

Mclean, 2004).

4. Four key inherent risk factors that can affect the operations of the company are stated

below. These risk factors are due to the operational strategies and other elements that

affects the growth of the company. To mitigate these risk factors, it is important that the

management of the company is having proper internal controls in place. Few of these

material inherent risk factors are stated below:

Competition – The overall competition in the market in which the group operates is

huge. This increased competition often leads to decrease in the overall sales and

profitability for the company. There is also a chance that the auditors end up sharing the

confidential information of the company with the outsider and that might affect the

company badly. Thus the best away company can deal with this kind of risk by providing

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

better competitive advantages that would help them in maintaining the position of a top

player in the market.

Loss and erosion of reputation – The groups business have been affected by the

increased claims for price leadership and the services that are provided to the consumers.

This can be mitigated by making sure that the activities of the management is properly

monitored when it comes to price fixation and price claiming, also the steps that are taken

by the competitors of the company in this regards should be carefully studied (Durtschi,

2004). The company should see that proper controls are in place that would help in

analyzing those factors that are responsible for fixing of prices. The auditor also needs to

see that there is no loss of information of the company due to fault in the system and the

IT management. This can be very detrimental as competitors can undue advantage in case

they get any information. Thus having proper controls in place is important fro

safeguarding the reputation of the company and the auditor needs to check that.

Key Supplier Relationship – Suppliers are the people who are one of the main asset of

the company and any failure to maintain cordial relations with them can affect the

performance of the company and can also be considered as an inherent risk to the audit

that is been conducted. Given the fact that there are many companies that are competing

in the market and each one wants to tap in the suppliers. Thus suppliers would deal with

only those companies that would give them best resources and best terms on which they

can sale off their goods (Iggers, 2018). Thus the auditor needs to see what is the overall

position of the suppliers in the company, what are the credit rates at which the products

are bought and what are the competitors take on this.

7 | P a g e

better competitive advantages that would help them in maintaining the position of a top

player in the market.

Loss and erosion of reputation – The groups business have been affected by the

increased claims for price leadership and the services that are provided to the consumers.

This can be mitigated by making sure that the activities of the management is properly

monitored when it comes to price fixation and price claiming, also the steps that are taken

by the competitors of the company in this regards should be carefully studied (Durtschi,

2004). The company should see that proper controls are in place that would help in

analyzing those factors that are responsible for fixing of prices. The auditor also needs to

see that there is no loss of information of the company due to fault in the system and the

IT management. This can be very detrimental as competitors can undue advantage in case

they get any information. Thus having proper controls in place is important fro

safeguarding the reputation of the company and the auditor needs to check that.

Key Supplier Relationship – Suppliers are the people who are one of the main asset of

the company and any failure to maintain cordial relations with them can affect the

performance of the company and can also be considered as an inherent risk to the audit

that is been conducted. Given the fact that there are many companies that are competing

in the market and each one wants to tap in the suppliers. Thus suppliers would deal with

only those companies that would give them best resources and best terms on which they

can sale off their goods (Iggers, 2018). Thus the auditor needs to see what is the overall

position of the suppliers in the company, what are the credit rates at which the products

are bought and what are the competitors take on this.

7 | P a g e

8

Leasing Arrangements – It is important for the growth of the company that they are able

to establish leasing negotiations and sutiable sites that can support their business

operations. It is important for the financial success of the company. It is the responsibility

of the senior management to look in that matter and see that proper terms are there. This

is an inherent risk in auditing and the auditors needs to understand that they are managing

that in a correct manner and are checking all the aspects beforehand. There are also

chances that management might fraud with this item and indulge in activities that can

affect their position for their own self interest (Shimamoto, 2018).

5. There are certain accounts in a financial statement that are of significant risk and it is the

responsibility of the auditor to check that and make proper opinion on that. The annual report of

JBH has been downloaded and key points have been discussed hereunder about five accounts

that are significant to the company.

• Acquisition of the Good Guys –

The company had acquired 100% of the Good Guys in November for cash consideration

of $860 million. The overall accounting related to this matter was complex and the company had

kept certain amount of assets and liabilities that was attributable to the company in provision.

The key assertion in this regard was the valuation of the overall assets and liabilities of the

company at their fair value. And the allocation of the purchase consideration to the key

identifiable intangible assets of the company. The size of the transaction was huge and the

overall judgement involved was also very complex (Wellmer, 2018). Thus, this was an

important account for the auditors and they can deal with it be checking whether the terms of the

sale agreement were proper or not. The overall steps taken by the management in the finalizing

8 | P a g e

Leasing Arrangements – It is important for the growth of the company that they are able

to establish leasing negotiations and sutiable sites that can support their business

operations. It is important for the financial success of the company. It is the responsibility

of the senior management to look in that matter and see that proper terms are there. This

is an inherent risk in auditing and the auditors needs to understand that they are managing

that in a correct manner and are checking all the aspects beforehand. There are also

chances that management might fraud with this item and indulge in activities that can

affect their position for their own self interest (Shimamoto, 2018).

5. There are certain accounts in a financial statement that are of significant risk and it is the

responsibility of the auditor to check that and make proper opinion on that. The annual report of

JBH has been downloaded and key points have been discussed hereunder about five accounts

that are significant to the company.

• Acquisition of the Good Guys –

The company had acquired 100% of the Good Guys in November for cash consideration

of $860 million. The overall accounting related to this matter was complex and the company had

kept certain amount of assets and liabilities that was attributable to the company in provision.

The key assertion in this regard was the valuation of the overall assets and liabilities of the

company at their fair value. And the allocation of the purchase consideration to the key

identifiable intangible assets of the company. The size of the transaction was huge and the

overall judgement involved was also very complex (Wellmer, 2018). Thus, this was an

important account for the auditors and they can deal with it be checking whether the terms of the

sale agreement were proper or not. The overall steps taken by the management in the finalizing

8 | P a g e

9

of the value of the assets and liabilities that was undertaken by them should be analyzed by the

auditor of the company.

• Carrying value of the Cash generating Units

During the year, the company had impaired goodwill of $14.7 million and PPE OF $1.1

million, that is attributable to the cash generating Units. The management has assessed the value

of the CGU and have incorporated the various judgements about the future growth rate. The

main aim of the auditor would be to check the financial performance of the company in New

Zealand CGU and making judgement regarding future cash flows and main assumptions of the

company. The main audit procedure would involve making and analyzing the key management

steps that they have taken, the overall carrying value of the assets of the company and accessing

the accuracy of the value-in use model. It is also important to verify the appropriateness of the

disclosures of the notes to the financial report (Webster, 2017).

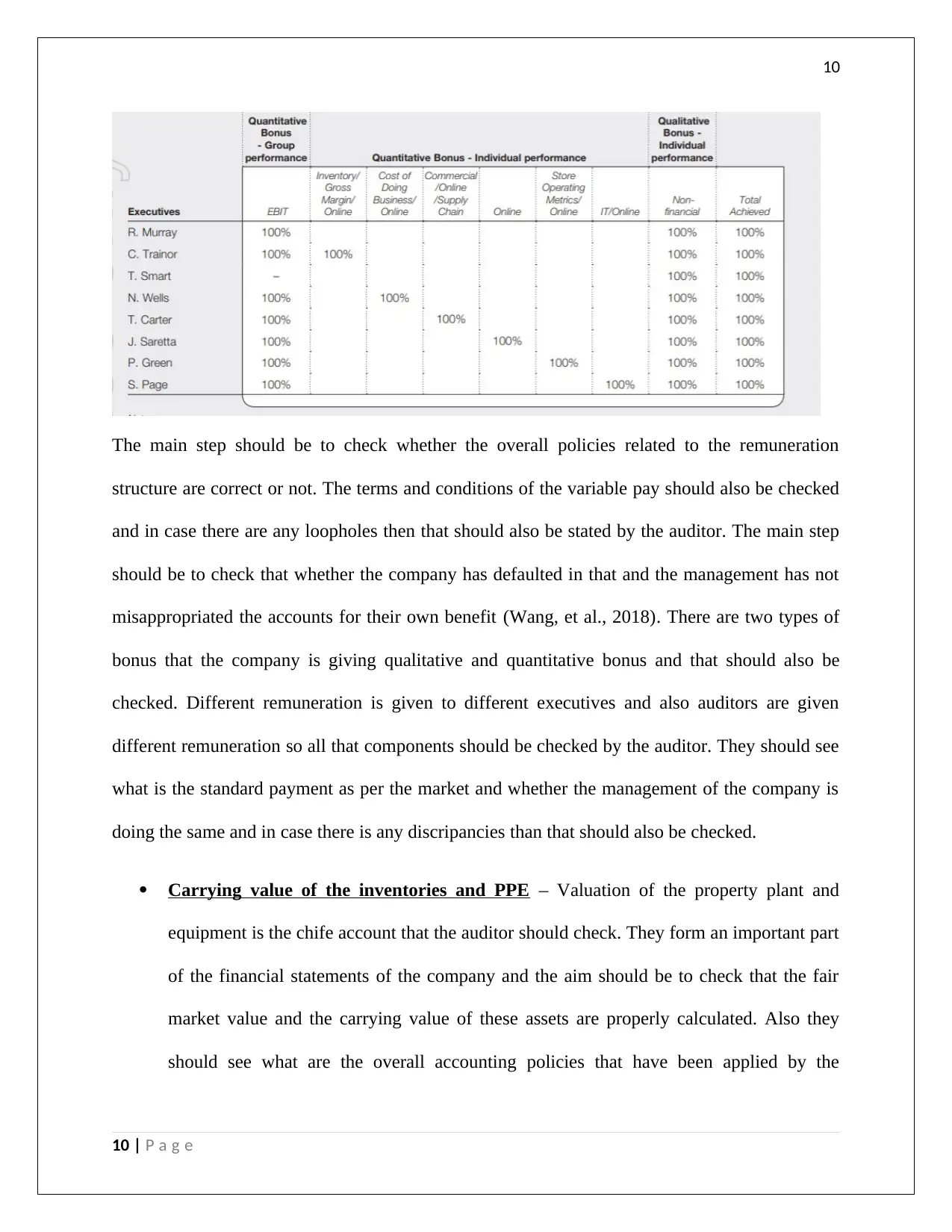

•Remuneration Provided to the executive

This is an important account that the auditor needs to value because there are high

chances that the management of the company can falsify this account for their own self benefit.

There are various components in the remuneration structure that includes fixed remuneration and

variable remuneration. A snapshot of the remuneration structure of the company is given below –

9 | P a g e

of the value of the assets and liabilities that was undertaken by them should be analyzed by the

auditor of the company.

• Carrying value of the Cash generating Units

During the year, the company had impaired goodwill of $14.7 million and PPE OF $1.1

million, that is attributable to the cash generating Units. The management has assessed the value

of the CGU and have incorporated the various judgements about the future growth rate. The

main aim of the auditor would be to check the financial performance of the company in New

Zealand CGU and making judgement regarding future cash flows and main assumptions of the

company. The main audit procedure would involve making and analyzing the key management

steps that they have taken, the overall carrying value of the assets of the company and accessing

the accuracy of the value-in use model. It is also important to verify the appropriateness of the

disclosures of the notes to the financial report (Webster, 2017).

•Remuneration Provided to the executive

This is an important account that the auditor needs to value because there are high

chances that the management of the company can falsify this account for their own self benefit.

There are various components in the remuneration structure that includes fixed remuneration and

variable remuneration. A snapshot of the remuneration structure of the company is given below –

9 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

The main step should be to check whether the overall policies related to the remuneration

structure are correct or not. The terms and conditions of the variable pay should also be checked

and in case there are any loopholes then that should also be stated by the auditor. The main step

should be to check that whether the company has defaulted in that and the management has not

misappropriated the accounts for their own benefit (Wang, et al., 2018). There are two types of

bonus that the company is giving qualitative and quantitative bonus and that should also be

checked. Different remuneration is given to different executives and also auditors are given

different remuneration so all that components should be checked by the auditor. They should see

what is the standard payment as per the market and whether the management of the company is

doing the same and in case there is any discripancies than that should also be checked.

Carrying value of the inventories and PPE – Valuation of the property plant and

equipment is the chife account that the auditor should check. They form an important part

of the financial statements of the company and the aim should be to check that the fair

market value and the carrying value of these assets are properly calculated. Also they

should see what are the overall accounting policies that have been applied by the

10 | P a g e

The main step should be to check whether the overall policies related to the remuneration

structure are correct or not. The terms and conditions of the variable pay should also be checked

and in case there are any loopholes then that should also be stated by the auditor. The main step

should be to check that whether the company has defaulted in that and the management has not

misappropriated the accounts for their own benefit (Wang, et al., 2018). There are two types of

bonus that the company is giving qualitative and quantitative bonus and that should also be

checked. Different remuneration is given to different executives and also auditors are given

different remuneration so all that components should be checked by the auditor. They should see

what is the standard payment as per the market and whether the management of the company is

doing the same and in case there is any discripancies than that should also be checked.

Carrying value of the inventories and PPE – Valuation of the property plant and

equipment is the chife account that the auditor should check. They form an important part

of the financial statements of the company and the aim should be to check that the fair

market value and the carrying value of these assets are properly calculated. Also they

should see what are the overall accounting policies that have been applied by the

10 | P a g e

11

company in calculation of the depreciation and other expenses that are affecting the

assets. The total amount of PPE as per the financial statements are $208.2 million

In case of inventory they are valued at cost or market price which ever is lower. Thus it

should be checked that proper valuation is done and there should not be any discripancies on

part of the management in their valuation. The key audit assertion would be to check that all

the assets are properly valued and there is no over or under valuation as that would affect the

financial position of the company largely. Experts opinion should be taken and valuation

specialists can be considered when it is required. All the policies of the management should

be double checked and in case there is any issue then they should be informed. The total

amount of inventories as per the balance sheet is $859.9million (Cayon, et al., 2017).

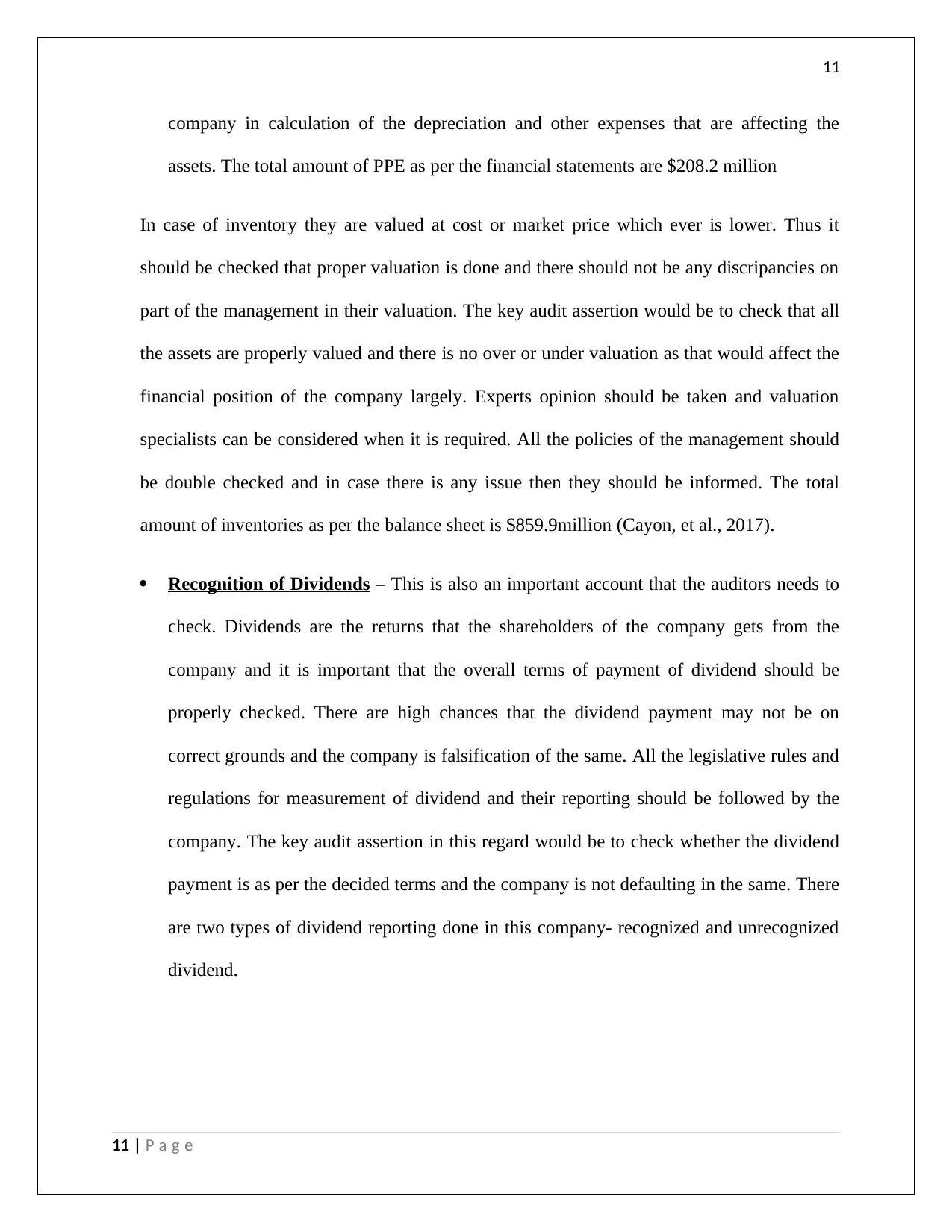

Recognition of Dividends – This is also an important account that the auditors needs to

check. Dividends are the returns that the shareholders of the company gets from the

company and it is important that the overall terms of payment of dividend should be

properly checked. There are high chances that the dividend payment may not be on

correct grounds and the company is falsification of the same. All the legislative rules and

regulations for measurement of dividend and their reporting should be followed by the

company. The key audit assertion in this regard would be to check whether the dividend

payment is as per the decided terms and the company is not defaulting in the same. There

are two types of dividend reporting done in this company- recognized and unrecognized

dividend.

11 | P a g e

company in calculation of the depreciation and other expenses that are affecting the

assets. The total amount of PPE as per the financial statements are $208.2 million

In case of inventory they are valued at cost or market price which ever is lower. Thus it

should be checked that proper valuation is done and there should not be any discripancies on

part of the management in their valuation. The key audit assertion would be to check that all

the assets are properly valued and there is no over or under valuation as that would affect the

financial position of the company largely. Experts opinion should be taken and valuation

specialists can be considered when it is required. All the policies of the management should

be double checked and in case there is any issue then they should be informed. The total

amount of inventories as per the balance sheet is $859.9million (Cayon, et al., 2017).

Recognition of Dividends – This is also an important account that the auditors needs to

check. Dividends are the returns that the shareholders of the company gets from the

company and it is important that the overall terms of payment of dividend should be

properly checked. There are high chances that the dividend payment may not be on

correct grounds and the company is falsification of the same. All the legislative rules and

regulations for measurement of dividend and their reporting should be followed by the

company. The key audit assertion in this regard would be to check whether the dividend

payment is as per the decided terms and the company is not defaulting in the same. There

are two types of dividend reporting done in this company- recognized and unrecognized

dividend.

11 | P a g e

12

6.Corporate Governance is an important aspect for the functioning of any company. It is

important that management of the company should adopt such policies and programs that would

help in the corporate governance (Chron, 2017). They should see that they are managing the

affairs of the business ethically and there is no mismanagement in that. As per the corporate

Governance Statement of JBH, following assurance has been provided :

The policies and programs of the board in all material aspect should comply with the

ASX Corporate Governance Principles and in 2017 they have embodied the spirit of

corporate governance in their overall policies and programs that has been stated by the

ASX board.

12 | P a g e

6.Corporate Governance is an important aspect for the functioning of any company. It is

important that management of the company should adopt such policies and programs that would

help in the corporate governance (Chron, 2017). They should see that they are managing the

affairs of the business ethically and there is no mismanagement in that. As per the corporate

Governance Statement of JBH, following assurance has been provided :

The policies and programs of the board in all material aspect should comply with the

ASX Corporate Governance Principles and in 2017 they have embodied the spirit of

corporate governance in their overall policies and programs that has been stated by the

ASX board.

12 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

The corporate governance statement has been approved by the board and was effective from

14th August 2017.

There should be effective realiance on the control environment because the company is in an

expanding state and there are increasing their operations to other areas, and thus it becomes

important that they are abiding by the rules and regulations that have been framed by the

audthorities. In 2017 the company has acquired Good Guys and that accqusition was very

crucial for the success of the company as a whole and thus they need to see that there is no

mismanagement in that. It is also one of the key audit matters that has been stated by the

auditors of the company (Durtschi, 2004). Moreover secondly, corporate governance helps in

ensuring that the business of the company is moving on ethical terms and there are no

misstatements in that. JBH is a consumer based company and the aim of the company should

be to see that the cosumer is getting their dues and there is no falsification for them.

Independence is also an important factor that the company and its auditor needs to be aware

of for good corporate governance (Lane & Ferretti, 2017). There should be no self interest

involved in any steps that is taken by the management of the company and they should make

sure that there are should not be no biasness (Ghofiqi, 2018). Control environment are

important as they help in reducing the chances of risk and any kind of inherent risk that

might be there in case of audit of the company. They help in keeping the information of the

company safe and also helps in keeping the management of the company functional as per

the legal and ethical terms and conditions. Thus it is important that proper resliance must be

given on control environment and companies should follow the same in all cases. Corporate

Governance should be incorporated from the various basic start of the company and then

should be moved to higher level (Gullet, et al., 2018).

13 | P a g e

The corporate governance statement has been approved by the board and was effective from

14th August 2017.

There should be effective realiance on the control environment because the company is in an

expanding state and there are increasing their operations to other areas, and thus it becomes

important that they are abiding by the rules and regulations that have been framed by the

audthorities. In 2017 the company has acquired Good Guys and that accqusition was very

crucial for the success of the company as a whole and thus they need to see that there is no

mismanagement in that. It is also one of the key audit matters that has been stated by the

auditors of the company (Durtschi, 2004). Moreover secondly, corporate governance helps in

ensuring that the business of the company is moving on ethical terms and there are no

misstatements in that. JBH is a consumer based company and the aim of the company should

be to see that the cosumer is getting their dues and there is no falsification for them.

Independence is also an important factor that the company and its auditor needs to be aware

of for good corporate governance (Lane & Ferretti, 2017). There should be no self interest

involved in any steps that is taken by the management of the company and they should make

sure that there are should not be no biasness (Ghofiqi, 2018). Control environment are

important as they help in reducing the chances of risk and any kind of inherent risk that

might be there in case of audit of the company. They help in keeping the information of the

company safe and also helps in keeping the management of the company functional as per

the legal and ethical terms and conditions. Thus it is important that proper resliance must be

given on control environment and companies should follow the same in all cases. Corporate

Governance should be incorporated from the various basic start of the company and then

should be moved to higher level (Gullet, et al., 2018).

13 | P a g e

14

Conclusion

Based on the overall analysis it can be said that JBH has been doing very well in terms of their

overall market position and has been able to establish a firm ground for themselves. In case there

are need for some changes with repsect to more focus on certain areas of control and

management and that the company can easily do. Overall it is the duty of the auditor to make

sure that the financial statements are free from any kind of misconduct and there are no

falsification and they should give an unbiased audit opinion that is useful for the stakeholders of

the company.

References

Abdullah, W. & Said, R., 2017. Religious, Educational Background and Corporate Crime Tolerance by

Accounting Professionals. State-of-the-Art Theories and Empirical Evidence, pp. 129-149.

Boghossian, P., 2017. The Socratic method, defeasibility, and doxastic responsibility. Educational

Philosophy and Theory, 50(3), pp. 244-253.

Bouret, I., 2017. Benefits of higher education in mid-life: A life course agency perspective. Journal of

Adult and Continuing Education, 23(1), pp. 15-31.

14 | P a g e

Conclusion

Based on the overall analysis it can be said that JBH has been doing very well in terms of their

overall market position and has been able to establish a firm ground for themselves. In case there

are need for some changes with repsect to more focus on certain areas of control and

management and that the company can easily do. Overall it is the duty of the auditor to make

sure that the financial statements are free from any kind of misconduct and there are no

falsification and they should give an unbiased audit opinion that is useful for the stakeholders of

the company.

References

Abdullah, W. & Said, R., 2017. Religious, Educational Background and Corporate Crime Tolerance by

Accounting Professionals. State-of-the-Art Theories and Empirical Evidence, pp. 129-149.

Boghossian, P., 2017. The Socratic method, defeasibility, and doxastic responsibility. Educational

Philosophy and Theory, 50(3), pp. 244-253.

Bouret, I., 2017. Benefits of higher education in mid-life: A life course agency perspective. Journal of

Adult and Continuing Education, 23(1), pp. 15-31.

14 | P a g e

15

Cayon, E., Thorp, S. & Wu, E., 2017. Immunity and infection: Emerging and developed market sovereign

spreads over the Global Financial Crisis. Emerging Markets Review.

Chron, 2017. five-common-features-internal-control-system-business. [Online]

Available at: http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

[Accessed 07 december 2017].

Delone, W. & Mclean, E., 2004. Measuring e-Commerce Success: Applying the DeLone & McLean

Information Systems Success Model. International Journal of Electronic Commerce, 9(1).

Durtschi, C. H. W. C., 2004. The Effective Use of Benford’s Law to Assist in Detecting Fraud in Accounting

Data. Journal of Forensic Accounting, pp. 17-34.

Ghofiqi, M., 2018. FORMATION OF VIEWS AND INTERESTS TO THE ACCOUNTANTS PROFESSION IN

MASTER OF ACCOUNTING STUDENTS OF JEMBER UNIVERSITY FORCE OF 2016 USING STRUCTURATION

THEORY ANALYSIS. THE 3RD INTERNATIONAL CONFERENCE ON ECONOMICS, BUSINESS, AND

ACCOUNTING STUDIES.

Gullet, N., Kilgore, R. & Geddie, M., 2018. USE OF FINANCIAL RATIOS TO MEASURE THE QUALITY OF

EARNINGS. Academy of Accounting and Financial Studies Journal, 22(2).

Iggers, J., 2018. Good News, Bad News: Journalism Ethics And The Public Interest. s.l.:s.n.

Lane, P. & Ferretti, G., 2017. International Financial Integration in the Aftermath of the Global Financial

Crisis. IMF working paper No. 17/115.

Shimamoto, D., 2018. Why Accountants Must Embrace Machine Learning. [Online]

Available at: https://www.ifac.org/global-knowledge-gateway/technology/discussion/why-accountants-

must-embrace-machine-learning

Wang, Z., Chiu, Y., li, Y. & Hsiao, L., 2018. Performance appraisal for the operation and management of

listed and OTC Taiwanese companies with DEA benchmarking models.

Webster, T., 2017. Successful Ethical Decision-Making Practices from the Professional Accountants'

Perspective. ProQuest Dissertations Publishing.

Wellmer, A., 2018. The Persistence of Modernity: Aesthetics, Ethics and Postmodernism. fourth ed. UK:

Polity Press.

15 | P a g e

Cayon, E., Thorp, S. & Wu, E., 2017. Immunity and infection: Emerging and developed market sovereign

spreads over the Global Financial Crisis. Emerging Markets Review.

Chron, 2017. five-common-features-internal-control-system-business. [Online]

Available at: http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

[Accessed 07 december 2017].

Delone, W. & Mclean, E., 2004. Measuring e-Commerce Success: Applying the DeLone & McLean

Information Systems Success Model. International Journal of Electronic Commerce, 9(1).

Durtschi, C. H. W. C., 2004. The Effective Use of Benford’s Law to Assist in Detecting Fraud in Accounting

Data. Journal of Forensic Accounting, pp. 17-34.

Ghofiqi, M., 2018. FORMATION OF VIEWS AND INTERESTS TO THE ACCOUNTANTS PROFESSION IN

MASTER OF ACCOUNTING STUDENTS OF JEMBER UNIVERSITY FORCE OF 2016 USING STRUCTURATION

THEORY ANALYSIS. THE 3RD INTERNATIONAL CONFERENCE ON ECONOMICS, BUSINESS, AND

ACCOUNTING STUDIES.

Gullet, N., Kilgore, R. & Geddie, M., 2018. USE OF FINANCIAL RATIOS TO MEASURE THE QUALITY OF

EARNINGS. Academy of Accounting and Financial Studies Journal, 22(2).

Iggers, J., 2018. Good News, Bad News: Journalism Ethics And The Public Interest. s.l.:s.n.

Lane, P. & Ferretti, G., 2017. International Financial Integration in the Aftermath of the Global Financial

Crisis. IMF working paper No. 17/115.

Shimamoto, D., 2018. Why Accountants Must Embrace Machine Learning. [Online]

Available at: https://www.ifac.org/global-knowledge-gateway/technology/discussion/why-accountants-

must-embrace-machine-learning

Wang, Z., Chiu, Y., li, Y. & Hsiao, L., 2018. Performance appraisal for the operation and management of

listed and OTC Taiwanese companies with DEA benchmarking models.

Webster, T., 2017. Successful Ethical Decision-Making Practices from the Professional Accountants'

Perspective. ProQuest Dissertations Publishing.

Wellmer, A., 2018. The Persistence of Modernity: Aesthetics, Ethics and Postmodernism. fourth ed. UK:

Polity Press.

15 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

16 | P a g e

16 | P a g e

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.