ACC621 Audit Report: Analysis of Ateneo Enterprise Financials

VerifiedAdded on 2023/06/07

|12

|2165

|361

Report

AI Summary

This report provides an in-depth analysis of an audit conducted on Ateneo Enterprise, examining various aspects of the financial statements. The report begins with an introduction discussing auditing standards and their implications, followed by an analysis of the trial balance. It assesses materiality levels based on the partner's suggestion and auditing standards, conducts a trend analysis to identify potential misstatements, and pinpoints income statement accounts at risk. The report then outlines necessary audit procedures to address the identified risks, emphasizing existence, occurrence, rights, obligations, valuation, and sampling. It also addresses the partner's perspective on fraud risk, referencing relevant auditing standards. The report concludes with a summary of key findings and insights, referencing relevant research papers.

Running head: AUDIT

Audit

Name of the Student:

Name of the University:

Authors Note:

Audit

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT

Table of Contents

Introduction:...............................................................................................................................2

Task 1: materiality level.............................................................................................................2

2. Trend analysis:.......................................................................................................................3

3. Income statement account that appear to be at risk of misstatement.....................................4

4. Audit procedure......................................................................................................................7

5. Fraud risk...............................................................................................................................9

Conclusion:................................................................................................................................9

Reference..................................................................................................................................10

Table of Contents

Introduction:...............................................................................................................................2

Task 1: materiality level.............................................................................................................2

2. Trend analysis:.......................................................................................................................3

3. Income statement account that appear to be at risk of misstatement.....................................4

4. Audit procedure......................................................................................................................7

5. Fraud risk...............................................................................................................................9

Conclusion:................................................................................................................................9

Reference..................................................................................................................................10

2AUDIT

Introduction:

In the given case various auditing standards and their implication procedure in the

process of audit have been disused. The report analyses the trial balance and sheet of the

company Ateneo Enterprise Trial Balance for the purpose of audit. The report highlights

auditing assumptions and their reasoning are also discussed. In addition to this, the trend

analysis is conducted to define the materiality, and to understand components of the financial

statement in which the auditor has identified material risks (Knechel & Salterio 2016). The

analytical review procedure are applied for identifying the material misstatement in the

financial statements. Further, the auditing procedures that are required to deal with the

misstatement is discussed in the contents of the report.

Task 1: materiality level

In the given case, the partner or the client suggested that for the primary assessment of

materiality for the financial statement as a whole is be set as $ 15000. In accordance with the

Auditing Standard 580, the management representations are one of the many sources of audit

evidences. In the given case the partner had suggested the auditor a materiality level of $

15000 so substantial audit procedure will be adopted for items above the materiality

(Groomer & Murthy 2018). This is not an obligation to the auditor but is an optional to the

auditor weather to exercise on them or not. In addition to that, in accordance with the ASA

540 Auditing accounting estimates provides guidance to the auditor to fix the materiality of

the statements and various components of the company. In accordance with the ASA, the

auditor must personally assess the materiality of the primary assessment task. The ASA 540

suggested the auditor to make the following procedure to understand the reliability

The materiality concept is applicable and applied by the auditor in both the

audit planning and at the time of auditing.

Introduction:

In the given case various auditing standards and their implication procedure in the

process of audit have been disused. The report analyses the trial balance and sheet of the

company Ateneo Enterprise Trial Balance for the purpose of audit. The report highlights

auditing assumptions and their reasoning are also discussed. In addition to this, the trend

analysis is conducted to define the materiality, and to understand components of the financial

statement in which the auditor has identified material risks (Knechel & Salterio 2016). The

analytical review procedure are applied for identifying the material misstatement in the

financial statements. Further, the auditing procedures that are required to deal with the

misstatement is discussed in the contents of the report.

Task 1: materiality level

In the given case, the partner or the client suggested that for the primary assessment of

materiality for the financial statement as a whole is be set as $ 15000. In accordance with the

Auditing Standard 580, the management representations are one of the many sources of audit

evidences. In the given case the partner had suggested the auditor a materiality level of $

15000 so substantial audit procedure will be adopted for items above the materiality

(Groomer & Murthy 2018). This is not an obligation to the auditor but is an optional to the

auditor weather to exercise on them or not. In addition to that, in accordance with the ASA

540 Auditing accounting estimates provides guidance to the auditor to fix the materiality of

the statements and various components of the company. In accordance with the ASA, the

auditor must personally assess the materiality of the primary assessment task. The ASA 540

suggested the auditor to make the following procedure to understand the reliability

The materiality concept is applicable and applied by the auditor in both the

audit planning and at the time of auditing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT

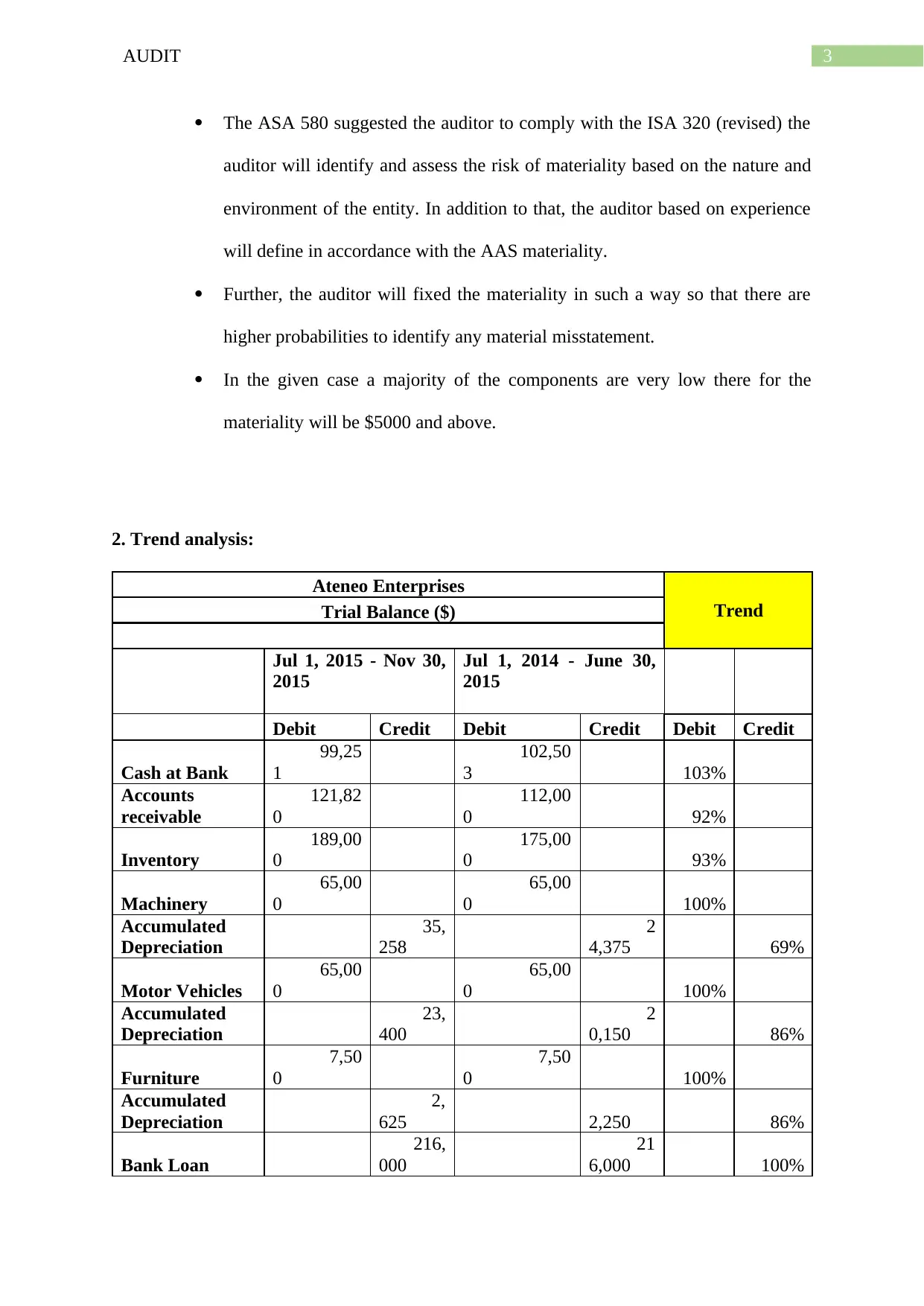

The ASA 580 suggested the auditor to comply with the ISA 320 (revised) the

auditor will identify and assess the risk of materiality based on the nature and

environment of the entity. In addition to that, the auditor based on experience

will define in accordance with the AAS materiality.

Further, the auditor will fixed the materiality in such a way so that there are

higher probabilities to identify any material misstatement.

In the given case a majority of the components are very low there for the

materiality will be $5000 and above.

2. Trend analysis:

Ateneo Enterprises

TrendTrial Balance ($)

Jul 1, 2015 - Nov 30,

2015

Jul 1, 2014 - June 30,

2015

Debit Credit Debit Credit Debit Credit

Cash at Bank

99,25

1

102,50

3 103%

Accounts

receivable

121,82

0

112,00

0 92%

Inventory

189,00

0

175,00

0 93%

Machinery

65,00

0

65,00

0 100%

Accumulated

Depreciation

35,

258

2

4,375 69%

Motor Vehicles

65,00

0

65,00

0 100%

Accumulated

Depreciation

23,

400

2

0,150 86%

Furniture

7,50

0

7,50

0 100%

Accumulated

Depreciation

2,

625 2,250 86%

Bank Loan

216,

000

21

6,000 100%

The ASA 580 suggested the auditor to comply with the ISA 320 (revised) the

auditor will identify and assess the risk of materiality based on the nature and

environment of the entity. In addition to that, the auditor based on experience

will define in accordance with the AAS materiality.

Further, the auditor will fixed the materiality in such a way so that there are

higher probabilities to identify any material misstatement.

In the given case a majority of the components are very low there for the

materiality will be $5000 and above.

2. Trend analysis:

Ateneo Enterprises

TrendTrial Balance ($)

Jul 1, 2015 - Nov 30,

2015

Jul 1, 2014 - June 30,

2015

Debit Credit Debit Credit Debit Credit

Cash at Bank

99,25

1

102,50

3 103%

Accounts

receivable

121,82

0

112,00

0 92%

Inventory

189,00

0

175,00

0 93%

Machinery

65,00

0

65,00

0 100%

Accumulated

Depreciation

35,

258

2

4,375 69%

Motor Vehicles

65,00

0

65,00

0 100%

Accumulated

Depreciation

23,

400

2

0,150 86%

Furniture

7,50

0

7,50

0 100%

Accumulated

Depreciation

2,

625 2,250 86%

Bank Loan

216,

000

21

6,000 100%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT

Sales

101,

562

18

7,450 185%

Cost of sales

27,23

5

63,59

5 234%

Service fees

(revenue)

24,

479

5

8,000 237%

Other income 500

2

5,000 5000%

Interest income 20 50 250%

Bank charges

14

5

35

0 241%

Depreciation

14,50

8

15,59

0 107%

Interest expense

4,50

0

10,80

0 240%

Printing

10

5

25

0 238%

Miscellaneous

1,00

0 - 0%

Wages

23,40

8

53,00

0 226%

Superannuation

2,22

4

4,77

0 215%

3. Income statement account that appear to be at risk of misstatement

From the above trend or analytical analysis the auditor finds some relative data that influence

the auditor in determining some material miss-statement in certain accounts the details are

provided below:

Account Assertion Explanation

Accumulated Depreciation Valuation / allocation After analysing the above case the

auditor finds that then percentage

of change in the allocation of the

accumulate depreciation change

has increased by more than a

Sales

101,

562

18

7,450 185%

Cost of sales

27,23

5

63,59

5 234%

Service fees

(revenue)

24,

479

5

8,000 237%

Other income 500

2

5,000 5000%

Interest income 20 50 250%

Bank charges

14

5

35

0 241%

Depreciation

14,50

8

15,59

0 107%

Interest expense

4,50

0

10,80

0 240%

Printing

10

5

25

0 238%

Miscellaneous

1,00

0 - 0%

Wages

23,40

8

53,00

0 226%

Superannuation

2,22

4

4,77

0 215%

3. Income statement account that appear to be at risk of misstatement

From the above trend or analytical analysis the auditor finds some relative data that influence

the auditor in determining some material miss-statement in certain accounts the details are

provided below:

Account Assertion Explanation

Accumulated Depreciation Valuation / allocation After analysing the above case the

auditor finds that then percentage

of change in the allocation of the

accumulate depreciation change

has increased by more than a

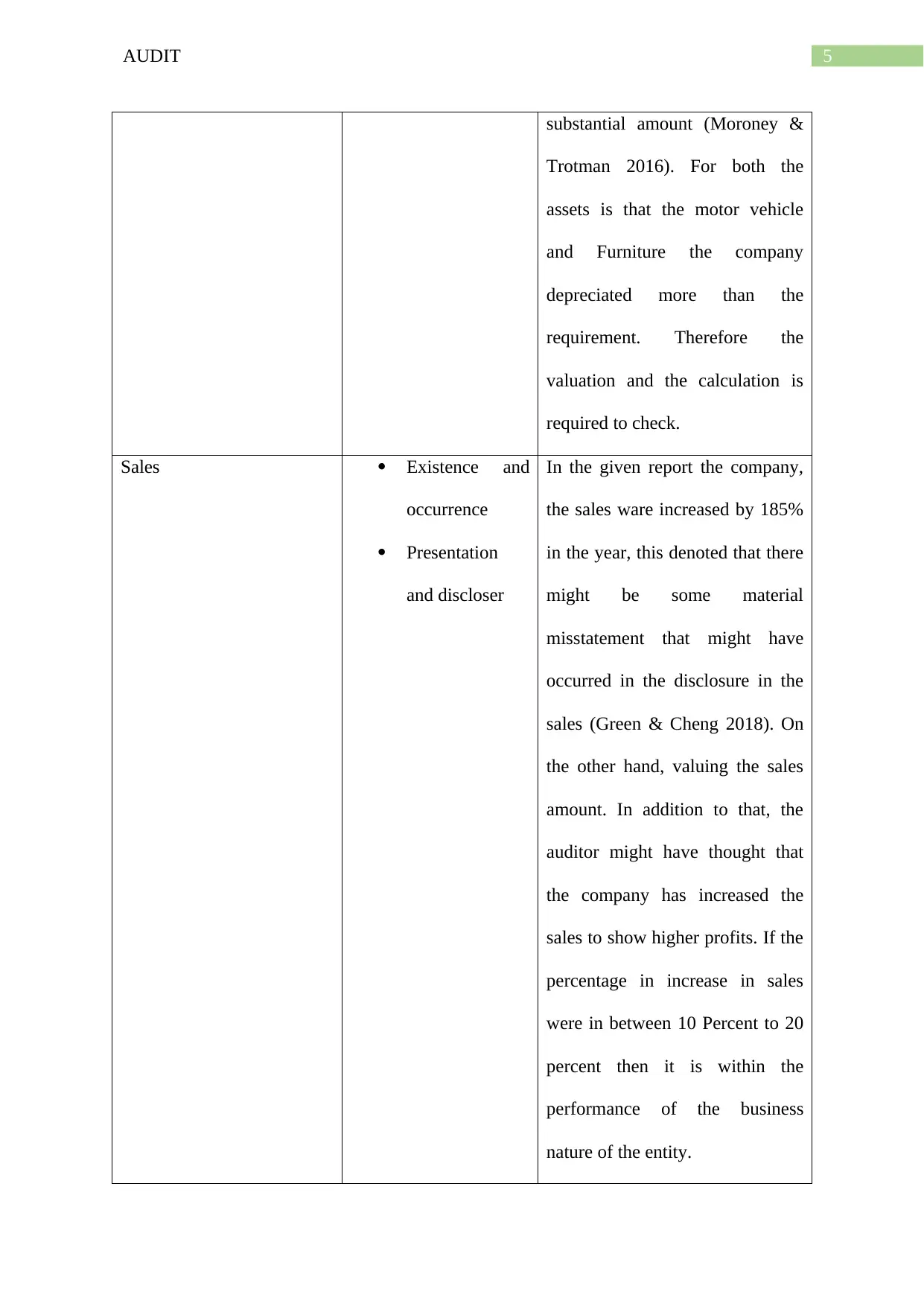

5AUDIT

substantial amount (Moroney &

Trotman 2016). For both the

assets is that the motor vehicle

and Furniture the company

depreciated more than the

requirement. Therefore the

valuation and the calculation is

required to check.

Sales Existence and

occurrence

Presentation

and discloser

In the given report the company,

the sales ware increased by 185%

in the year, this denoted that there

might be some material

misstatement that might have

occurred in the disclosure in the

sales (Green & Cheng 2018). On

the other hand, valuing the sales

amount. In addition to that, the

auditor might have thought that

the company has increased the

sales to show higher profits. If the

percentage in increase in sales

were in between 10 Percent to 20

percent then it is within the

performance of the business

nature of the entity.

substantial amount (Moroney &

Trotman 2016). For both the

assets is that the motor vehicle

and Furniture the company

depreciated more than the

requirement. Therefore the

valuation and the calculation is

required to check.

Sales Existence and

occurrence

Presentation

and discloser

In the given report the company,

the sales ware increased by 185%

in the year, this denoted that there

might be some material

misstatement that might have

occurred in the disclosure in the

sales (Green & Cheng 2018). On

the other hand, valuing the sales

amount. In addition to that, the

auditor might have thought that

the company has increased the

sales to show higher profits. If the

percentage in increase in sales

were in between 10 Percent to 20

percent then it is within the

performance of the business

nature of the entity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT

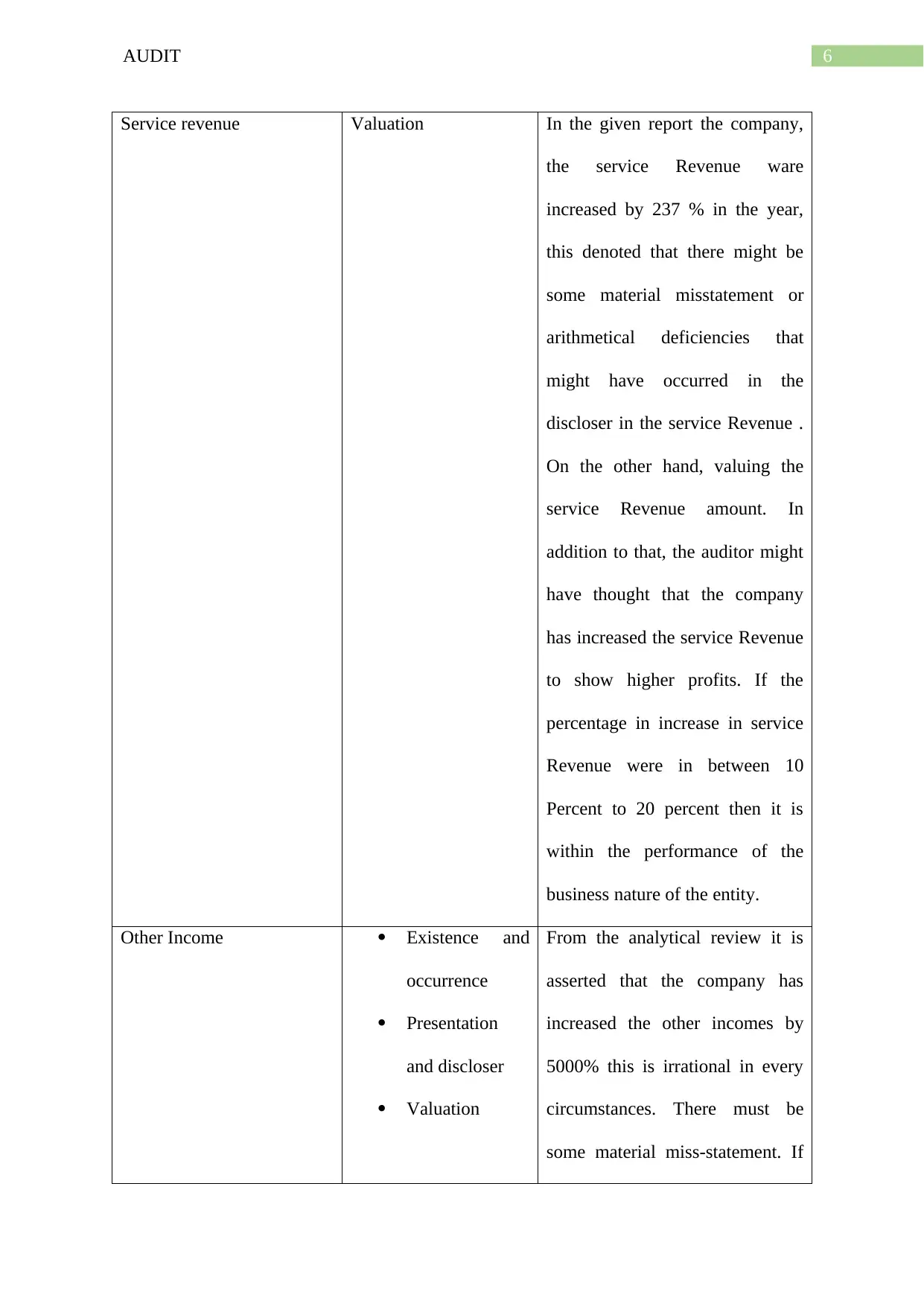

Service revenue Valuation In the given report the company,

the service Revenue ware

increased by 237 % in the year,

this denoted that there might be

some material misstatement or

arithmetical deficiencies that

might have occurred in the

discloser in the service Revenue .

On the other hand, valuing the

service Revenue amount. In

addition to that, the auditor might

have thought that the company

has increased the service Revenue

to show higher profits. If the

percentage in increase in service

Revenue were in between 10

Percent to 20 percent then it is

within the performance of the

business nature of the entity.

Other Income Existence and

occurrence

Presentation

and discloser

Valuation

From the analytical review it is

asserted that the company has

increased the other incomes by

5000% this is irrational in every

circumstances. There must be

some material miss-statement. If

Service revenue Valuation In the given report the company,

the service Revenue ware

increased by 237 % in the year,

this denoted that there might be

some material misstatement or

arithmetical deficiencies that

might have occurred in the

discloser in the service Revenue .

On the other hand, valuing the

service Revenue amount. In

addition to that, the auditor might

have thought that the company

has increased the service Revenue

to show higher profits. If the

percentage in increase in service

Revenue were in between 10

Percent to 20 percent then it is

within the performance of the

business nature of the entity.

Other Income Existence and

occurrence

Presentation

and discloser

Valuation

From the analytical review it is

asserted that the company has

increased the other incomes by

5000% this is irrational in every

circumstances. There must be

some material miss-statement. If

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT

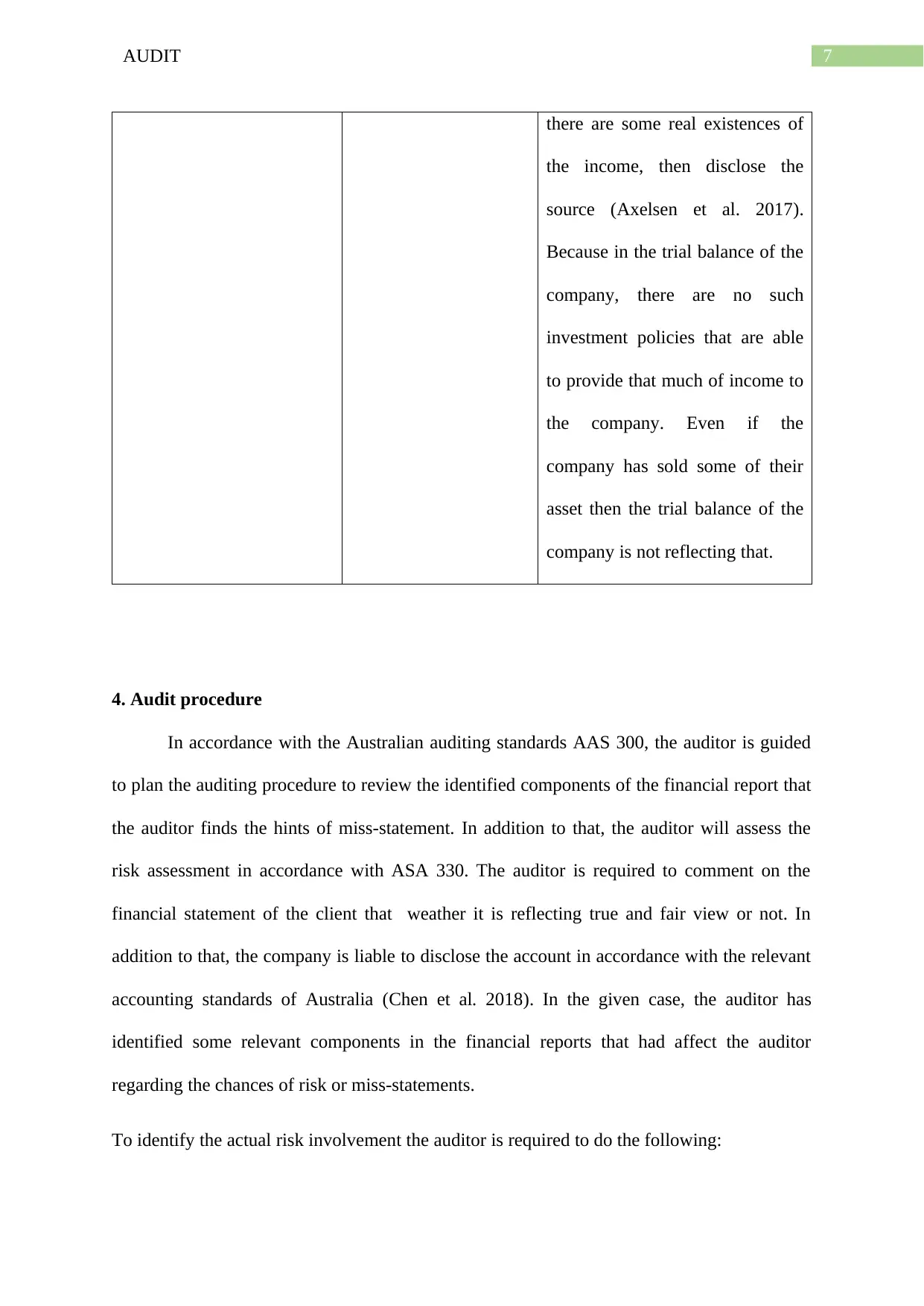

there are some real existences of

the income, then disclose the

source (Axelsen et al. 2017).

Because in the trial balance of the

company, there are no such

investment policies that are able

to provide that much of income to

the company. Even if the

company has sold some of their

asset then the trial balance of the

company is not reflecting that.

4. Audit procedure

In accordance with the Australian auditing standards AAS 300, the auditor is guided

to plan the auditing procedure to review the identified components of the financial report that

the auditor finds the hints of miss-statement. In addition to that, the auditor will assess the

risk assessment in accordance with ASA 330. The auditor is required to comment on the

financial statement of the client that weather it is reflecting true and fair view or not. In

addition to that, the company is liable to disclose the account in accordance with the relevant

accounting standards of Australia (Chen et al. 2018). In the given case, the auditor has

identified some relevant components in the financial reports that had affect the auditor

regarding the chances of risk or miss-statements.

To identify the actual risk involvement the auditor is required to do the following:

there are some real existences of

the income, then disclose the

source (Axelsen et al. 2017).

Because in the trial balance of the

company, there are no such

investment policies that are able

to provide that much of income to

the company. Even if the

company has sold some of their

asset then the trial balance of the

company is not reflecting that.

4. Audit procedure

In accordance with the Australian auditing standards AAS 300, the auditor is guided

to plan the auditing procedure to review the identified components of the financial report that

the auditor finds the hints of miss-statement. In addition to that, the auditor will assess the

risk assessment in accordance with ASA 330. The auditor is required to comment on the

financial statement of the client that weather it is reflecting true and fair view or not. In

addition to that, the company is liable to disclose the account in accordance with the relevant

accounting standards of Australia (Chen et al. 2018). In the given case, the auditor has

identified some relevant components in the financial reports that had affect the auditor

regarding the chances of risk or miss-statements.

To identify the actual risk involvement the auditor is required to do the following:

8AUDIT

Existence and occurrence:

The auditor needs to verify the existence of every assets of the company is actual as

the part of compliance procedure of auditing. In addition to that, the company is able to

include all the asset in the books is actual or fair valuations. As per the standers of auditing

the auditor requires to inspect the books of accounts and the asset and the ownership by

inspecting documents and confirming the sources of valuation and what accounting technic

and assumption are considered in the relevant case.

Rights and obligations:

The auditor needs to understand the accounting procedure and nature of the clients

business to understand what are the rights and obligation of the company to record any data.

Valuation and allocation:

The valuation of the allocation of the asset and liabilities are to be valued in

accordance with the relevant Australian accounting standards. In addition, to that for the

valuation the auditor will cross check the books, accounting measure, assertions, assumptions

and others. In the given case, the valuation of the fixed assets of the company is required to

re-verify as there is significant risk involvement analysed by the auditor (Christensen et al.

2016).

Sampling:

Sampling is an integral part of auditing compliance procedure. In the given case, the

sampling will be required more in the sales, service revenues, and other incomes to determine

weather there are any miss-statement is available in those. In the sampling procedure, the

auditor will inspect the accounts, sales voucher, invoice, bank statement (other income) and

investments of the company.

Existence and occurrence:

The auditor needs to verify the existence of every assets of the company is actual as

the part of compliance procedure of auditing. In addition to that, the company is able to

include all the asset in the books is actual or fair valuations. As per the standers of auditing

the auditor requires to inspect the books of accounts and the asset and the ownership by

inspecting documents and confirming the sources of valuation and what accounting technic

and assumption are considered in the relevant case.

Rights and obligations:

The auditor needs to understand the accounting procedure and nature of the clients

business to understand what are the rights and obligation of the company to record any data.

Valuation and allocation:

The valuation of the allocation of the asset and liabilities are to be valued in

accordance with the relevant Australian accounting standards. In addition, to that for the

valuation the auditor will cross check the books, accounting measure, assertions, assumptions

and others. In the given case, the valuation of the fixed assets of the company is required to

re-verify as there is significant risk involvement analysed by the auditor (Christensen et al.

2016).

Sampling:

Sampling is an integral part of auditing compliance procedure. In the given case, the

sampling will be required more in the sales, service revenues, and other incomes to determine

weather there are any miss-statement is available in those. In the sampling procedure, the

auditor will inspect the accounts, sales voucher, invoice, bank statement (other income) and

investments of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT

5. Fraud risk

In the given case, the partner has assured the auditor to fraud risk should not be

considered for the client, as he feels that the client’s staffs are all very trustworthy. This is not

a valid auditing terms as per the Australian accounting standards ASA 210.

As per the ASA 210 and the ASA 200, the auditor primary responsibility is comment

on the financial reports of the client. The auditor is not obliged to detect fraud and errors

unless specifically asked. Nevertheless, if in the auditing procedure the auditor finds any

hints where fraud has taken place in that case the auditor needs to find out the source of that

hint either to accept or reject the fraud. Even if it is not primary responsibility or

communicated by the client to check or not to check the fraud depends on the auditor

(Bumgarner, N. & Vasarhelyi 2018). As specified in the ASA 240 all adequate provisions

and verification must be conducted by the auditor.

Conclusion

In the relevant case study some important and material information and auditing

procedure is identified and the procedure of audit planning and conduction technical,

reasonability and others are discussed in the statement on the guidance of the ASA’s.

5. Fraud risk

In the given case, the partner has assured the auditor to fraud risk should not be

considered for the client, as he feels that the client’s staffs are all very trustworthy. This is not

a valid auditing terms as per the Australian accounting standards ASA 210.

As per the ASA 210 and the ASA 200, the auditor primary responsibility is comment

on the financial reports of the client. The auditor is not obliged to detect fraud and errors

unless specifically asked. Nevertheless, if in the auditing procedure the auditor finds any

hints where fraud has taken place in that case the auditor needs to find out the source of that

hint either to accept or reject the fraud. Even if it is not primary responsibility or

communicated by the client to check or not to check the fraud depends on the auditor

(Bumgarner, N. & Vasarhelyi 2018). As specified in the ASA 240 all adequate provisions

and verification must be conducted by the auditor.

Conclusion

In the relevant case study some important and material information and auditing

procedure is identified and the procedure of audit planning and conduction technical,

reasonability and others are discussed in the statement on the guidance of the ASA’s.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT

Reference

Axelsen, M., Green, P. & Ridley, G., 2017. Explaining the information systems auditor role

in the public sector financial audit. International Journal of Accounting Information

Systems, 24, pp.15-31.

Bumgarner, N. & Vasarhelyi, M.A., 2018. Continuous auditing—a new view. In Continuous

Auditing: Theory and Application (pp. 7-51). Emerald Publishing Limited.

Chen, W., Khalifa, A.S., Morgan, K.L. & Trotman, K.T., 2018. The effect of brainstorming

guidelines on individual auditors’ identification of potential frauds. Australian Journal of

Management, 43(2), pp.225-240.

Christensen, B.E., Glover, S.M., Omer, T.C. & Shelley, M.K., 2016. Understanding audit

quality: Insights from audit partners and investors. Contemporary Accounting

Research, 33(4), pp.1648-1684.

Green, W.J. & Cheng, M.M., 2018. Materiality judgments in an integrated reporting setting:

The effect of strategic relevance and strategy map. Accounting, Organizations and Society.

Groomer, S. M., & Murthy, U. S. (2018). Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Knechel, W.R. & Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Moroney, R. & Trotman, K.T., 2016. Differences in Auditors' Materiality Assessments When

Auditing Financial Statements and Sustainability Reports. Contemporary Accounting

Research, 33(2), pp.551-575.

Reference

Axelsen, M., Green, P. & Ridley, G., 2017. Explaining the information systems auditor role

in the public sector financial audit. International Journal of Accounting Information

Systems, 24, pp.15-31.

Bumgarner, N. & Vasarhelyi, M.A., 2018. Continuous auditing—a new view. In Continuous

Auditing: Theory and Application (pp. 7-51). Emerald Publishing Limited.

Chen, W., Khalifa, A.S., Morgan, K.L. & Trotman, K.T., 2018. The effect of brainstorming

guidelines on individual auditors’ identification of potential frauds. Australian Journal of

Management, 43(2), pp.225-240.

Christensen, B.E., Glover, S.M., Omer, T.C. & Shelley, M.K., 2016. Understanding audit

quality: Insights from audit partners and investors. Contemporary Accounting

Research, 33(4), pp.1648-1684.

Green, W.J. & Cheng, M.M., 2018. Materiality judgments in an integrated reporting setting:

The effect of strategic relevance and strategy map. Accounting, Organizations and Society.

Groomer, S. M., & Murthy, U. S. (2018). Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Knechel, W.R. & Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Moroney, R. & Trotman, K.T., 2016. Differences in Auditors' Materiality Assessments When

Auditing Financial Statements and Sustainability Reports. Contemporary Accounting

Research, 33(2), pp.551-575.

11AUDIT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.