University Audit Report: Account Selection and Recommended Procedures

VerifiedAdded on 2020/04/01

|13

|2113

|408

Report

AI Summary

This report presents an audit analysis focusing on the selection of key accounts for review and the rationale behind their selection. The report begins with an overview of audit planning, including analytical review and preliminary materiality judgments, setting the stage for the selection of specific accounts. Seven accounts are selected for detailed examination: accounts receivable, depreciation, repair and maintenance, inventory, fixed assets, wages, and cash. For each account, the report provides a rationale for its selection, an explanation of the assertions being made, and recommended audit procedures. The procedures include verification of sales and credit processes for accounts receivable, assessment of depreciation methods, examination of repair and maintenance contracts, inventory control checks, physical verification of fixed assets, wage register reviews, and cash handling procedures. The report references several academic sources to support the audit methodologies and recommendations. This report aims to provide a structured approach to auditing, emphasizing the importance of account selection and the application of appropriate audit procedures.

Audit

Name of the Student:

Name of the University:

Authors note:

Name of the Student:

Name of the University:

Authors note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. Audit planning:............................................................................................................................3

1.1. Analytical review:.....................................................................................................................3

1.2. Preliminary judgment of materiality:........................................................................................4

2.0 Frist account selected:................................................................................................................4

2.1 Rationale for selection:..............................................................................................................4

2.2 Assertion and explanation:........................................................................................................4

2.3 Recommended Audit procedure:...............................................................................................4

3.0 Second account selected:...........................................................................................................5

3.1 Rationale for selection:..............................................................................................................5

3.2 Assertion and explanation:........................................................................................................5

4.0 Third account selected:..............................................................................................................6

4.1 Rationale for selection:..............................................................................................................6

5.0 Fourth account selected:............................................................................................................6

5.1 Rationale for selection:..............................................................................................................6

5.2Assertation and explanation:.......................................................................................................7

5.3 recommended audit procedure:..................................................................................................7

6.0 Fifth account selected:...............................................................................................................7

6.1 Rationale for selection:..............................................................................................................7

6.2 Assertion and explanation:........................................................................................................7

6.3 Recommended audit procedure:................................................................................................8

7.1 Sixth account selected:..............................................................................................................8

7.1 Rationale for selection:..............................................................................................................8

7.3 Assertion and explanation:........................................................................................................8

7.3 Recommendation audit procedure:............................................................................................8

8.0 Seven account selected:.............................................................................................................8

8.1 Rationale for selection:..............................................................................................................9

8.2 Assertion and explanation:........................................................................................................9

8.3 Recommended audit procedure:................................................................................................9

Reference.......................................................................................................................................12

1. Audit planning:............................................................................................................................3

1.1. Analytical review:.....................................................................................................................3

1.2. Preliminary judgment of materiality:........................................................................................4

2.0 Frist account selected:................................................................................................................4

2.1 Rationale for selection:..............................................................................................................4

2.2 Assertion and explanation:........................................................................................................4

2.3 Recommended Audit procedure:...............................................................................................4

3.0 Second account selected:...........................................................................................................5

3.1 Rationale for selection:..............................................................................................................5

3.2 Assertion and explanation:........................................................................................................5

4.0 Third account selected:..............................................................................................................6

4.1 Rationale for selection:..............................................................................................................6

5.0 Fourth account selected:............................................................................................................6

5.1 Rationale for selection:..............................................................................................................6

5.2Assertation and explanation:.......................................................................................................7

5.3 recommended audit procedure:..................................................................................................7

6.0 Fifth account selected:...............................................................................................................7

6.1 Rationale for selection:..............................................................................................................7

6.2 Assertion and explanation:........................................................................................................7

6.3 Recommended audit procedure:................................................................................................8

7.1 Sixth account selected:..............................................................................................................8

7.1 Rationale for selection:..............................................................................................................8

7.3 Assertion and explanation:........................................................................................................8

7.3 Recommendation audit procedure:............................................................................................8

8.0 Seven account selected:.............................................................................................................8

8.1 Rationale for selection:..............................................................................................................9

8.2 Assertion and explanation:........................................................................................................9

8.3 Recommended audit procedure:................................................................................................9

Reference.......................................................................................................................................12

1. Audit planning:

An innovative methods has been found in the process of auditing which enhances the auditing

methods and determines seven accounts at least in this process. Organization’s fluctuations in

debit and credit items are being measured on the basis of the fluctuation model that has been

formed on the basis of the figures containing trail balance (Knechel and Salterio 2016). Selection

of seven accounts have been made in order to check the purpose of abnormal fluctuation in

certain items and also helps to identify the cause of fluctuation. The percentage of fluctuation in

items along the fluctuation in tribal balances of June 30, 2016 has been taken as a base.

1.1. Analytical review:

Analytical review shows the abnormal fluctuation in the present year by using different

mathematical and statistical techniques through fluctuation model, ratio analysis has also been

used to check the abnormal changes in liquidity or solidarity ratio of an organization along with

the abnormal change in profitability in an organization (Simnett et al. 2016).

A little increase of sale by mere of 0.83% in the year ending on June 30, 2017 from the sale

of the previous year that belongs to the situation of Cerise Enterprise. However, at the same time

the sales have been increased by almost 10%, exactly 9.29% which amounts to $69500 from the

amount $63595. Thus from the previous year 9% of the gross profit ratio of the organization has

plunged in the present year. Audit system professionally finds out the reason of the increase in

the profit in the audit system that they will be achieve.

An innovative methods has been found in the process of auditing which enhances the auditing

methods and determines seven accounts at least in this process. Organization’s fluctuations in

debit and credit items are being measured on the basis of the fluctuation model that has been

formed on the basis of the figures containing trail balance (Knechel and Salterio 2016). Selection

of seven accounts have been made in order to check the purpose of abnormal fluctuation in

certain items and also helps to identify the cause of fluctuation. The percentage of fluctuation in

items along the fluctuation in tribal balances of June 30, 2016 has been taken as a base.

1.1. Analytical review:

Analytical review shows the abnormal fluctuation in the present year by using different

mathematical and statistical techniques through fluctuation model, ratio analysis has also been

used to check the abnormal changes in liquidity or solidarity ratio of an organization along with

the abnormal change in profitability in an organization (Simnett et al. 2016).

A little increase of sale by mere of 0.83% in the year ending on June 30, 2017 from the sale

of the previous year that belongs to the situation of Cerise Enterprise. However, at the same time

the sales have been increased by almost 10%, exactly 9.29% which amounts to $69500 from the

amount $63595. Thus from the previous year 9% of the gross profit ratio of the organization has

plunged in the present year. Audit system professionally finds out the reason of the increase in

the profit in the audit system that they will be achieve.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2. Preliminary judgment of materiality:

Here the materials has been arbitrated taking into consideration a definite percentage of item’s

amount to the total amount of revenue, liabilities, expenditures and asserts of items which is

concerned. Items are chosen according to income of the item and if the income is at least 5 % of

the total revenue of the organization then such items are taken into consideration and accepted

otherwise no time and strategies are being misused on such times (Greer et al. 2017).

2.0 Frist account selected:

Accounts receivable

2.1 Rationale for selection:

2.2 Assertion and explanation:

In the account books there is an increased in almost 21% from the previous year where

accounts is receivable and thus it should be audited properly in order to maintain the balances of

the accounts.

2.3 Recommended Audit procedure:

As receivable ledger has increased in the substantial year that amounts to increase in 21%, that is

a positive thing but at the same time, it has its disadvantages and concerning at the same time. If

there is increase in sale, which would corresponds to increase in the account receivable balance

that will be justified (Green et al. 2017). Thus when change-taking place in the accounts

receivable balance along with the amplification in the sale from the previous year’s the balances

Here the materials has been arbitrated taking into consideration a definite percentage of item’s

amount to the total amount of revenue, liabilities, expenditures and asserts of items which is

concerned. Items are chosen according to income of the item and if the income is at least 5 % of

the total revenue of the organization then such items are taken into consideration and accepted

otherwise no time and strategies are being misused on such times (Greer et al. 2017).

2.0 Frist account selected:

Accounts receivable

2.1 Rationale for selection:

2.2 Assertion and explanation:

In the account books there is an increased in almost 21% from the previous year where

accounts is receivable and thus it should be audited properly in order to maintain the balances of

the accounts.

2.3 Recommended Audit procedure:

As receivable ledger has increased in the substantial year that amounts to increase in 21%, that is

a positive thing but at the same time, it has its disadvantages and concerning at the same time. If

there is increase in sale, which would corresponds to increase in the account receivable balance

that will be justified (Green et al. 2017). Thus when change-taking place in the accounts

receivable balance along with the amplification in the sale from the previous year’s the balances

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are welcome but if not so increased in 21% of profit will not be a welcoming change. The

verification and checking procedure of the sales are being recorded with the credit. The whole

development of credit sale will have be checked in order to ensure that standard credit sale

procedure is followed in the organization. Report is done to management in case there is any

deviation from the standard process. Customer’s payments are checked to find out any disputes

regarding the system that can be charged by the employee regarding the payment in order to rob

the organization. Due time are also allowed to the customers are also checked along the

management weather they are able to collect the dues properly or not from the customers and

reported accordingly.

3.0 Second account selected:

Accounts of depreciation.

3.1 Rationale for selection:

3.2 Assertion and explanation:

In financial statement a vital element will be the depreciation of accounts. If there increase in

37.84% from the past year then this organization’s annual depreciation will be nominated for the

auditing purpose (Hay et al. 2016).

3.3 Recommended audit procedure:

Checking of the appropriate methods should be done for the organization. Consistency should be

there in order to assess the depreciation and has to be seen changing of methods that had done by

verification and checking procedure of the sales are being recorded with the credit. The whole

development of credit sale will have be checked in order to ensure that standard credit sale

procedure is followed in the organization. Report is done to management in case there is any

deviation from the standard process. Customer’s payments are checked to find out any disputes

regarding the system that can be charged by the employee regarding the payment in order to rob

the organization. Due time are also allowed to the customers are also checked along the

management weather they are able to collect the dues properly or not from the customers and

reported accordingly.

3.0 Second account selected:

Accounts of depreciation.

3.1 Rationale for selection:

3.2 Assertion and explanation:

In financial statement a vital element will be the depreciation of accounts. If there increase in

37.84% from the past year then this organization’s annual depreciation will be nominated for the

auditing purpose (Hay et al. 2016).

3.3 Recommended audit procedure:

Checking of the appropriate methods should be done for the organization. Consistency should be

there in order to assess the depreciation and has to be seen changing of methods that had done by

the organization in order to provide depreciating in recent year and if they did the change then

such change has to be verified.

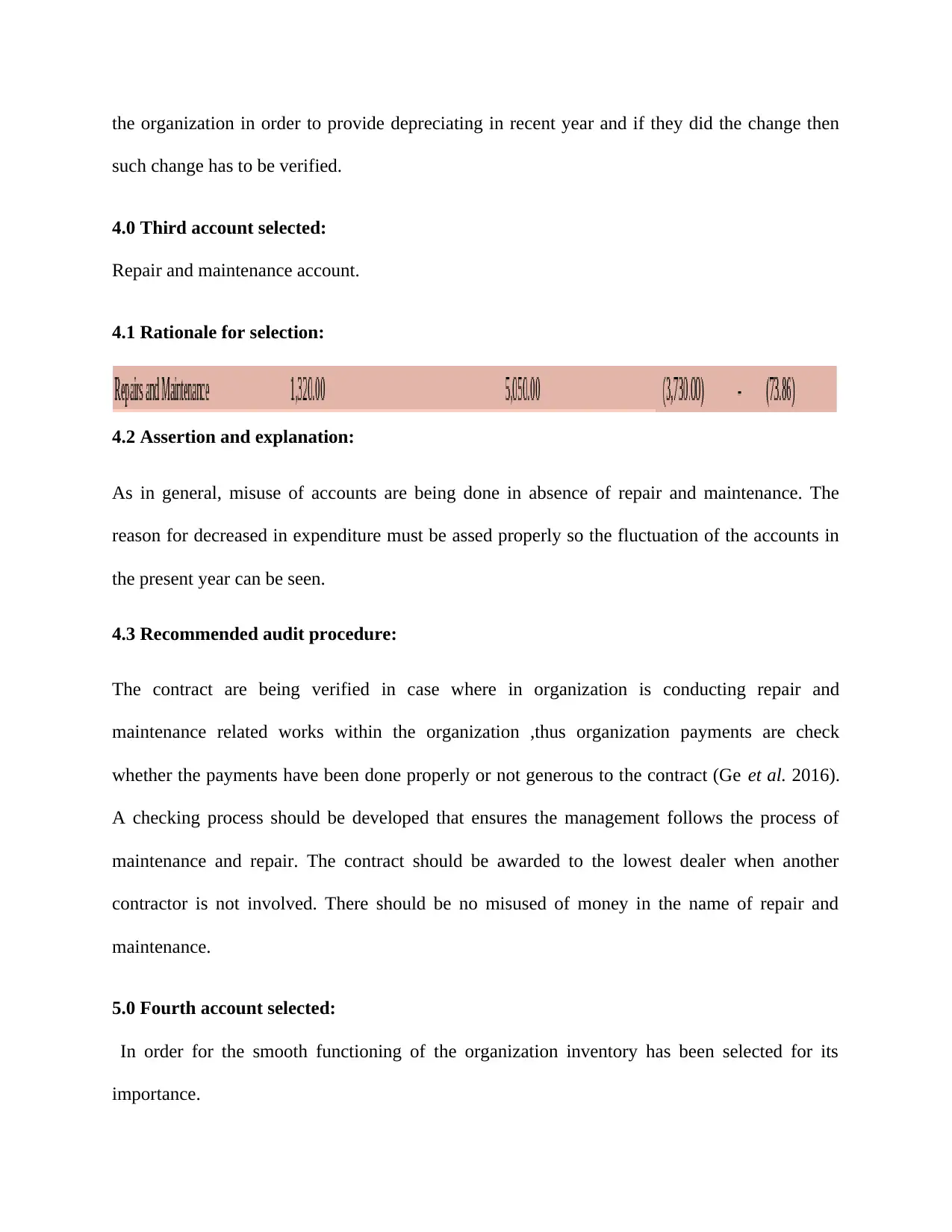

4.0 Third account selected:

Repair and maintenance account.

4.1 Rationale for selection:

4.2 Assertion and explanation:

As in general, misuse of accounts are being done in absence of repair and maintenance. The

reason for decreased in expenditure must be assed properly so the fluctuation of the accounts in

the present year can be seen.

4.3 Recommended audit procedure:

The contract are being verified in case where in organization is conducting repair and

maintenance related works within the organization ,thus organization payments are check

whether the payments have been done properly or not generous to the contract (Ge et al. 2016).

A checking process should be developed that ensures the management follows the process of

maintenance and repair. The contract should be awarded to the lowest dealer when another

contractor is not involved. There should be no misused of money in the name of repair and

maintenance.

5.0 Fourth account selected:

In order for the smooth functioning of the organization inventory has been selected for its

importance.

such change has to be verified.

4.0 Third account selected:

Repair and maintenance account.

4.1 Rationale for selection:

4.2 Assertion and explanation:

As in general, misuse of accounts are being done in absence of repair and maintenance. The

reason for decreased in expenditure must be assed properly so the fluctuation of the accounts in

the present year can be seen.

4.3 Recommended audit procedure:

The contract are being verified in case where in organization is conducting repair and

maintenance related works within the organization ,thus organization payments are check

whether the payments have been done properly or not generous to the contract (Ge et al. 2016).

A checking process should be developed that ensures the management follows the process of

maintenance and repair. The contract should be awarded to the lowest dealer when another

contractor is not involved. There should be no misused of money in the name of repair and

maintenance.

5.0 Fourth account selected:

In order for the smooth functioning of the organization inventory has been selected for its

importance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

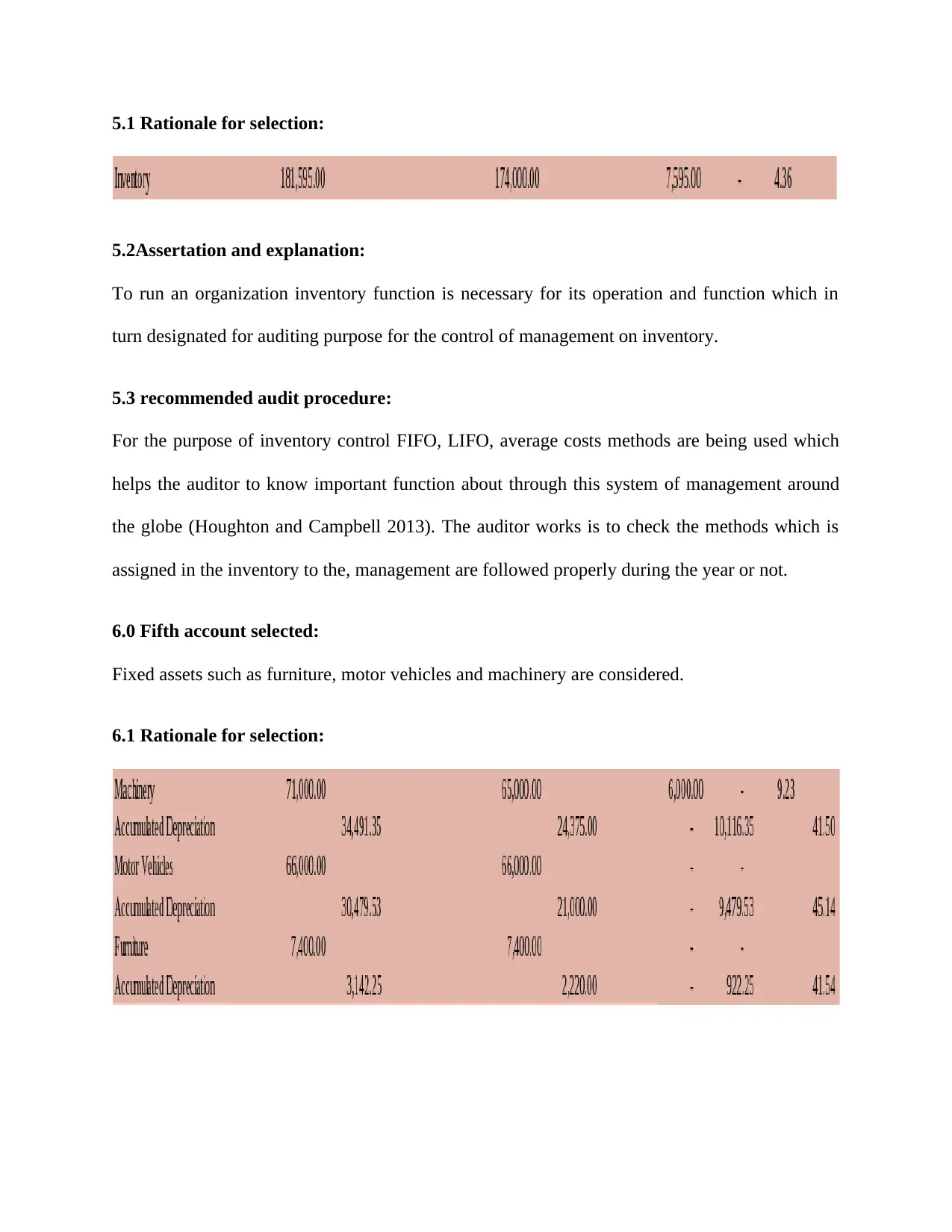

5.1 Rationale for selection:

5.2Assertation and explanation:

To run an organization inventory function is necessary for its operation and function which in

turn designated for auditing purpose for the control of management on inventory.

5.3 recommended audit procedure:

For the purpose of inventory control FIFO, LIFO, average costs methods are being used which

helps the auditor to know important function about through this system of management around

the globe (Houghton and Campbell 2013). The auditor works is to check the methods which is

assigned in the inventory to the, management are followed properly during the year or not.

6.0 Fifth account selected:

Fixed assets such as furniture, motor vehicles and machinery are considered.

6.1 Rationale for selection:

5.2Assertation and explanation:

To run an organization inventory function is necessary for its operation and function which in

turn designated for auditing purpose for the control of management on inventory.

5.3 recommended audit procedure:

For the purpose of inventory control FIFO, LIFO, average costs methods are being used which

helps the auditor to know important function about through this system of management around

the globe (Houghton and Campbell 2013). The auditor works is to check the methods which is

assigned in the inventory to the, management are followed properly during the year or not.

6.0 Fifth account selected:

Fixed assets such as furniture, motor vehicles and machinery are considered.

6.1 Rationale for selection:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6.2 Assertion and explanation:

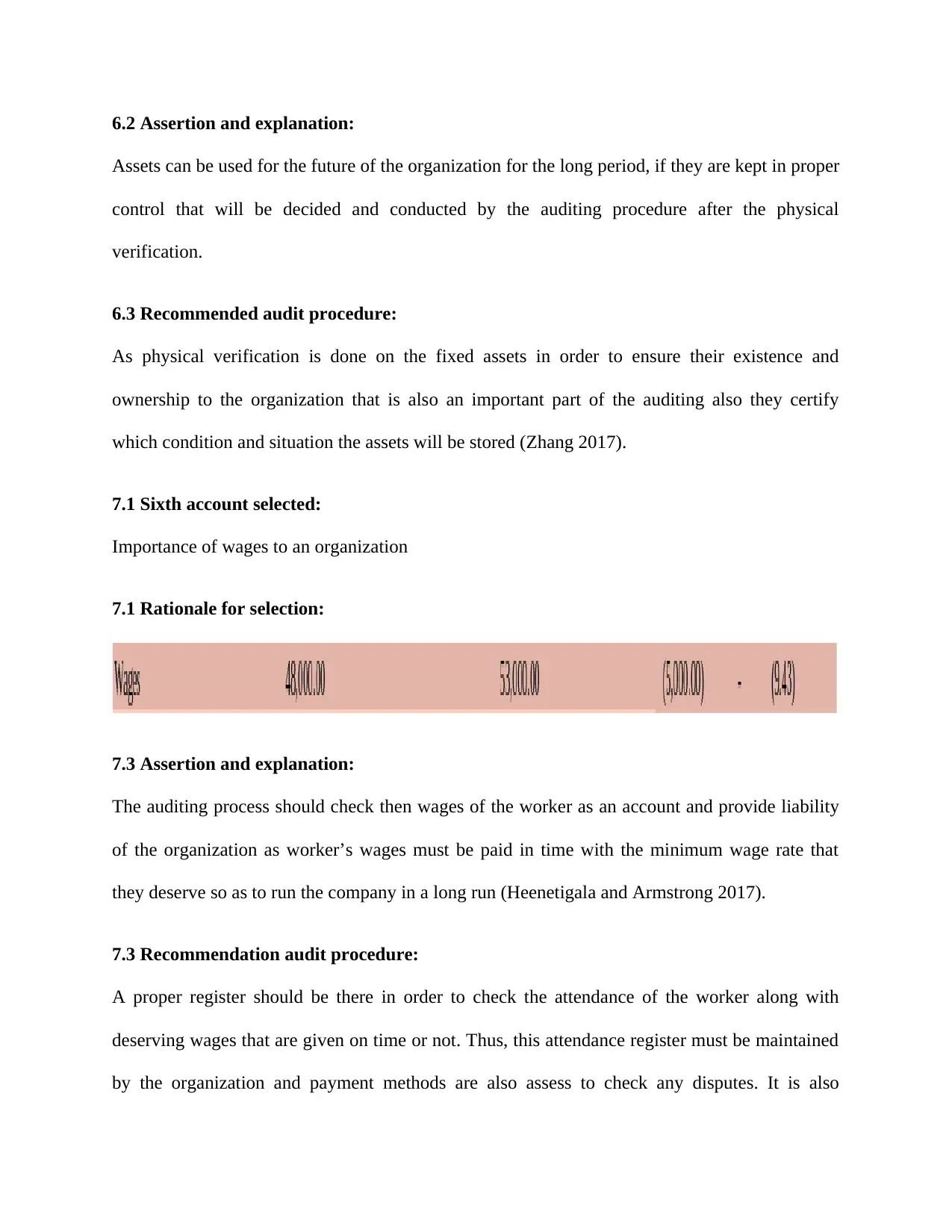

Assets can be used for the future of the organization for the long period, if they are kept in proper

control that will be decided and conducted by the auditing procedure after the physical

verification.

6.3 Recommended audit procedure:

As physical verification is done on the fixed assets in order to ensure their existence and

ownership to the organization that is also an important part of the auditing also they certify

which condition and situation the assets will be stored (Zhang 2017).

7.1 Sixth account selected:

Importance of wages to an organization

7.1 Rationale for selection:

7.3 Assertion and explanation:

The auditing process should check then wages of the worker as an account and provide liability

of the organization as worker’s wages must be paid in time with the minimum wage rate that

they deserve so as to run the company in a long run (Heenetigala and Armstrong 2017).

7.3 Recommendation audit procedure:

A proper register should be there in order to check the attendance of the worker along with

deserving wages that are given on time or not. Thus, this attendance register must be maintained

by the organization and payment methods are also assess to check any disputes. It is also

Assets can be used for the future of the organization for the long period, if they are kept in proper

control that will be decided and conducted by the auditing procedure after the physical

verification.

6.3 Recommended audit procedure:

As physical verification is done on the fixed assets in order to ensure their existence and

ownership to the organization that is also an important part of the auditing also they certify

which condition and situation the assets will be stored (Zhang 2017).

7.1 Sixth account selected:

Importance of wages to an organization

7.1 Rationale for selection:

7.3 Assertion and explanation:

The auditing process should check then wages of the worker as an account and provide liability

of the organization as worker’s wages must be paid in time with the minimum wage rate that

they deserve so as to run the company in a long run (Heenetigala and Armstrong 2017).

7.3 Recommendation audit procedure:

A proper register should be there in order to check the attendance of the worker along with

deserving wages that are given on time or not. Thus, this attendance register must be maintained

by the organization and payment methods are also assess to check any disputes. It is also

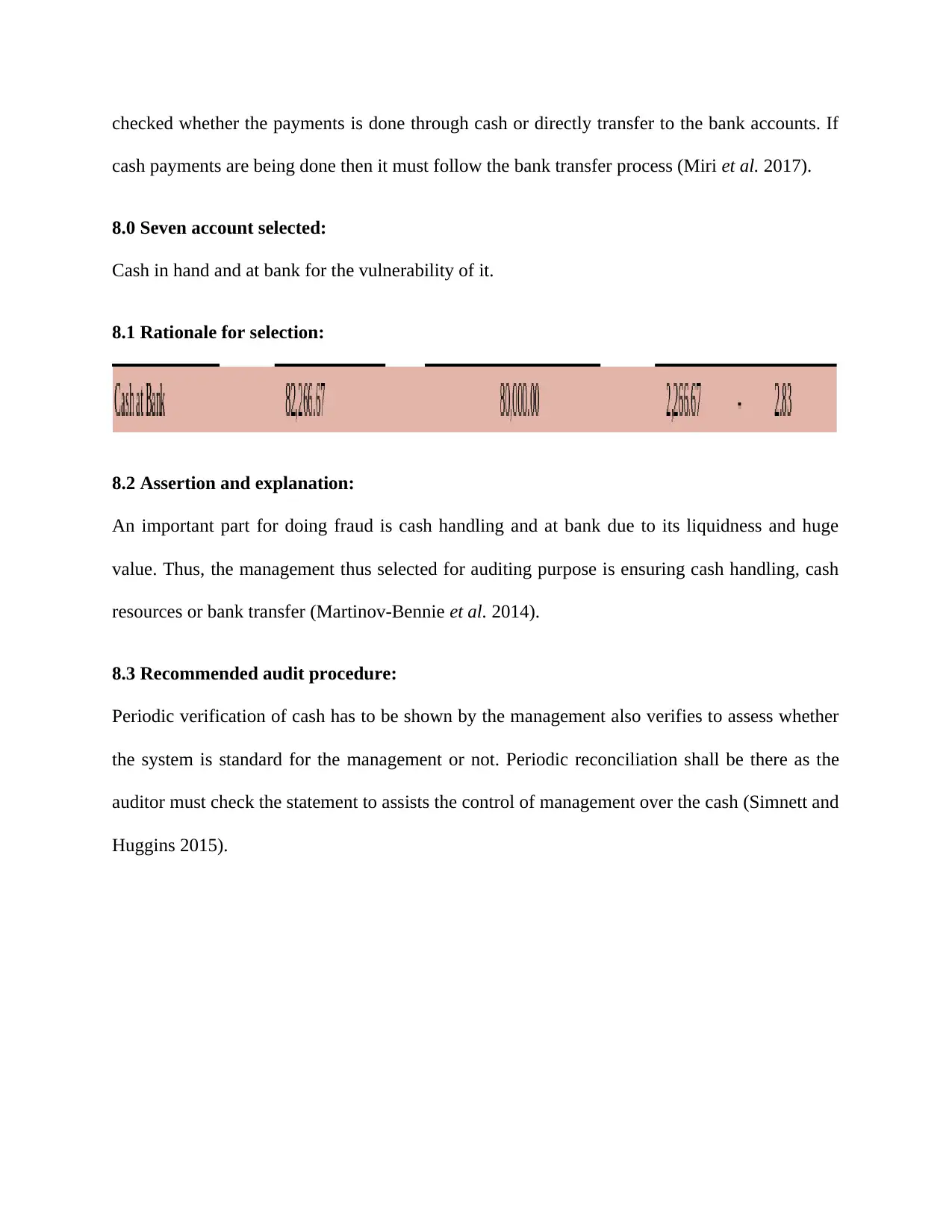

checked whether the payments is done through cash or directly transfer to the bank accounts. If

cash payments are being done then it must follow the bank transfer process (Miri et al. 2017).

8.0 Seven account selected:

Cash in hand and at bank for the vulnerability of it.

8.1 Rationale for selection:

8.2 Assertion and explanation:

An important part for doing fraud is cash handling and at bank due to its liquidness and huge

value. Thus, the management thus selected for auditing purpose is ensuring cash handling, cash

resources or bank transfer (Martinov-Bennie et al. 2014).

8.3 Recommended audit procedure:

Periodic verification of cash has to be shown by the management also verifies to assess whether

the system is standard for the management or not. Periodic reconciliation shall be there as the

auditor must check the statement to assists the control of management over the cash (Simnett and

Huggins 2015).

cash payments are being done then it must follow the bank transfer process (Miri et al. 2017).

8.0 Seven account selected:

Cash in hand and at bank for the vulnerability of it.

8.1 Rationale for selection:

8.2 Assertion and explanation:

An important part for doing fraud is cash handling and at bank due to its liquidness and huge

value. Thus, the management thus selected for auditing purpose is ensuring cash handling, cash

resources or bank transfer (Martinov-Bennie et al. 2014).

8.3 Recommended audit procedure:

Periodic verification of cash has to be shown by the management also verifies to assess whether

the system is standard for the management or not. Periodic reconciliation shall be there as the

auditor must check the statement to assists the control of management over the cash (Simnett and

Huggins 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

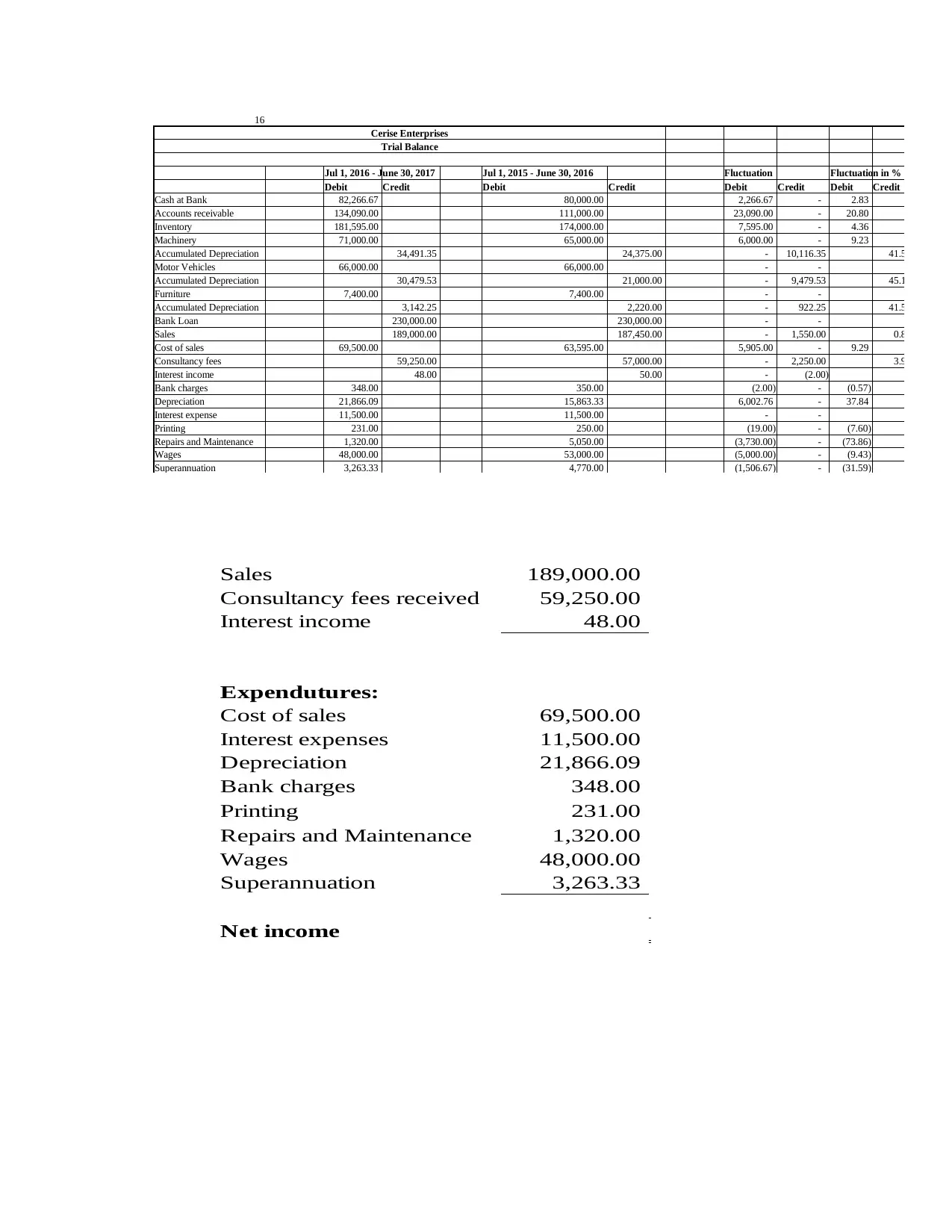

16

Cerise Enterprises

Trial Balance

Jul 1, 2016 - June 30, 2017 Jul 1, 2015 - June 30, 2016 Fluctuation Fluctuation in %

Debit Credit Debit Credit Debit Credit Debit Credit

Cash at Bank 82,266.67 80,000.00 2,266.67 - 2.83

Accounts receivable 134,090.00 111,000.00 23,090.00 - 20.80

Inventory 181,595.00 174,000.00 7,595.00 - 4.36

Machinery 71,000.00 65,000.00 6,000.00 - 9.23

Accumulated Depreciation 34,491.35 24,375.00 - 10,116.35 41.50

Motor Vehicles 66,000.00 66,000.00 - -

Accumulated Depreciation 30,479.53 21,000.00 - 9,479.53 45.14

Furniture 7,400.00 7,400.00 - -

Accumulated Depreciation 3,142.25 2,220.00 - 922.25 41.54

Bank Loan 230,000.00 230,000.00 - -

Sales 189,000.00 187,450.00 - 1,550.00 0.83

Cost of sales 69,500.00 63,595.00 5,905.00 - 9.29

Consultancy fees 59,250.00 57,000.00 - 2,250.00 3.95

Interest income 48.00 50.00 - (2.00)

Bank charges 348.00 350.00 (2.00) - (0.57)

Depreciation 21,866.09 15,863.33 6,002.76 - 37.84

Interest expense 11,500.00 11,500.00 - -

Printing 231.00 250.00 (19.00) - (7.60)

Repairs and Maintenance 1,320.00 5,050.00 (3,730.00) - (73.86)

Wages 48,000.00 53,000.00 (5,000.00) - (9.43)

Superannuation 3,263.33 4,770.00 (1,506.67) - (31.59)

Sales 189,000.00

Consultancy fees received 59,250.00

Interest income 48.00

Expendutures:

Cost of sales 69,500.00

Interest expenses 11,500.00

Depreciation 21,866.09

Bank charges 348.00

Printing 231.00

Repairs and Maintenance 1,320.00

Wages 48,000.00

Superannuation 3,263.33

Net income

Cerise Enterprises

Trial Balance

Jul 1, 2016 - June 30, 2017 Jul 1, 2015 - June 30, 2016 Fluctuation Fluctuation in %

Debit Credit Debit Credit Debit Credit Debit Credit

Cash at Bank 82,266.67 80,000.00 2,266.67 - 2.83

Accounts receivable 134,090.00 111,000.00 23,090.00 - 20.80

Inventory 181,595.00 174,000.00 7,595.00 - 4.36

Machinery 71,000.00 65,000.00 6,000.00 - 9.23

Accumulated Depreciation 34,491.35 24,375.00 - 10,116.35 41.50

Motor Vehicles 66,000.00 66,000.00 - -

Accumulated Depreciation 30,479.53 21,000.00 - 9,479.53 45.14

Furniture 7,400.00 7,400.00 - -

Accumulated Depreciation 3,142.25 2,220.00 - 922.25 41.54

Bank Loan 230,000.00 230,000.00 - -

Sales 189,000.00 187,450.00 - 1,550.00 0.83

Cost of sales 69,500.00 63,595.00 5,905.00 - 9.29

Consultancy fees 59,250.00 57,000.00 - 2,250.00 3.95

Interest income 48.00 50.00 - (2.00)

Bank charges 348.00 350.00 (2.00) - (0.57)

Depreciation 21,866.09 15,863.33 6,002.76 - 37.84

Interest expense 11,500.00 11,500.00 - -

Printing 231.00 250.00 (19.00) - (7.60)

Repairs and Maintenance 1,320.00 5,050.00 (3,730.00) - (73.86)

Wages 48,000.00 53,000.00 (5,000.00) - (9.43)

Superannuation 3,263.33 4,770.00 (1,506.67) - (31.59)

Sales 189,000.00

Consultancy fees received 59,250.00

Interest income 48.00

Expendutures:

Cost of sales 69,500.00

Interest expenses 11,500.00

Depreciation 21,866.09

Bank charges 348.00

Printing 231.00

Repairs and Maintenance 1,320.00

Wages 48,000.00

Superannuation 3,263.33

Net income

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

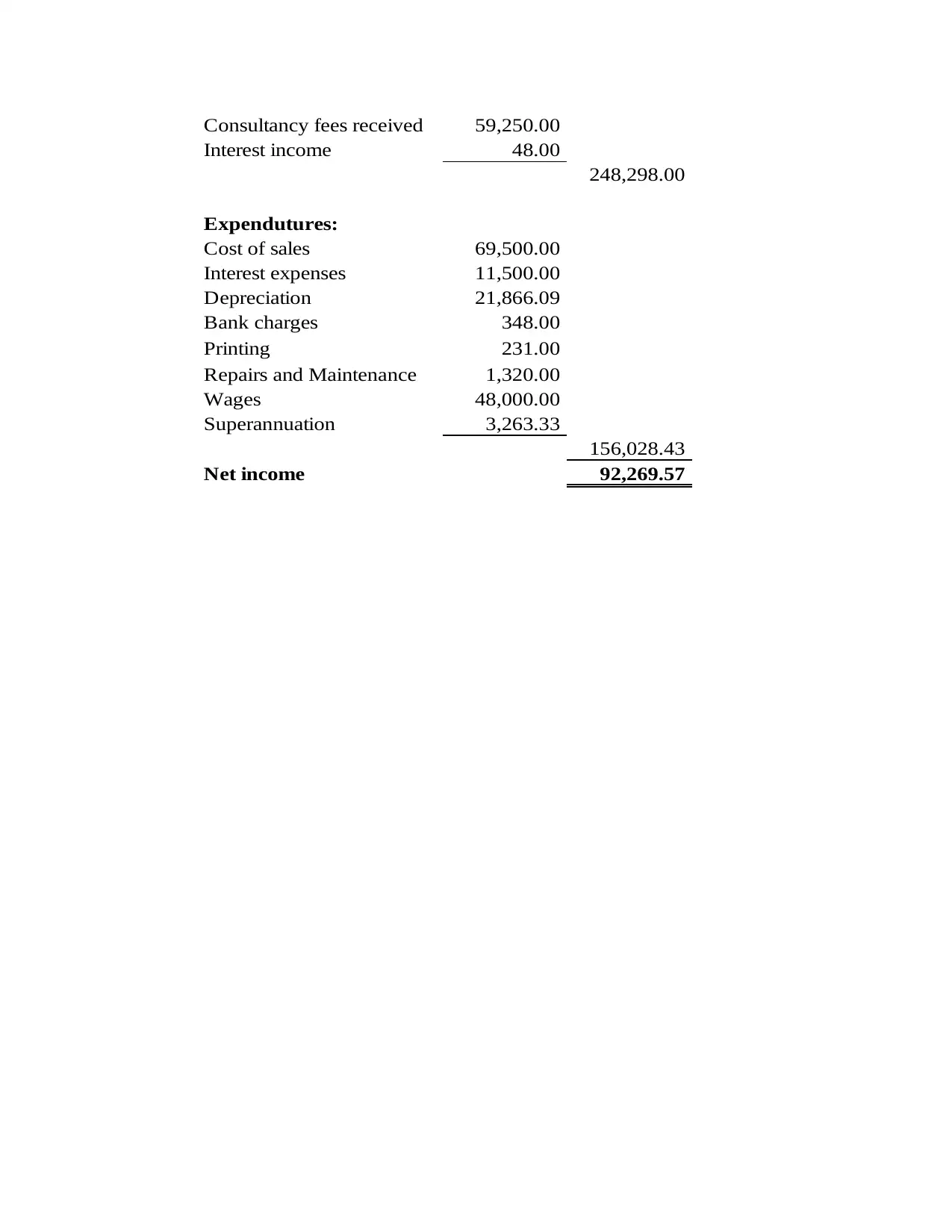

Consultancy fees received 59,250.00

Interest income 48.00

248,298.00

Expendutures:

Cost of sales 69,500.00

Interest expenses 11,500.00

Depreciation 21,866.09

Bank charges 348.00

Printing 231.00

Repairs and Maintenance 1,320.00

Wages 48,000.00

Superannuation 3,263.33

156,028.43

Net income 92,269.57

Interest income 48.00

248,298.00

Expendutures:

Cost of sales 69,500.00

Interest expenses 11,500.00

Depreciation 21,866.09

Bank charges 348.00

Printing 231.00

Repairs and Maintenance 1,320.00

Wages 48,000.00

Superannuation 3,263.33

156,028.43

Net income 92,269.57

Reference

Ge, Q., Simnett, R. and Zhou, S., 2016. Ethical and Quality Control Requirements When

Undertaking Assurance Engagements.

Green, W., Green, W., Taylor, S., Taylor, S., Wu, J. and Wu, J., 2017. Determinants of

greenhouse gas assurance provider choice. Meditari Accountancy Research, 25(1), pp.114-135.

Greer, P., Legge, K., Miri, N., Vial, P., Fuangrod, T. and Lehmann, J., 2017. OC-0537: A remote

EPID-based dosimetric auditing method for VMAT delivery using a digital phantom

concept. Radiotherapy and Oncology, 123, pp.S285-S286.

Hay, D., Stewart, J. and Botica Redmayne, N., 2016. The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis.

Heenetigala, K. and Armstrong, A.F., 2017. CREDIBILITY OF SUSTAINABILITY REPORTS

OF MINING SECTOR COMPANIES IN AUSTRALIA: AN INVESTIGATION OF

EXTERNAL ASSURANCE. Economic and Social Development: Book of Proceedings, p.335.

Houghton, K. and Campbell, T., 2013. Ethics and auditing (p. 354). ANU Press.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Martinov-Bennie, N., O'Neill, S., Cheung, A. and Wolfe, M.K., 2014. Issues in the assurance and

verification of work health and safety information.

Miri, N., Legge, K., Lehmann, J., Vial, P., Zwan, B. and Greer, P., 2017. PO-0907: Remote

auditing of IMRT/VMAT deliveries. Radiotherapy and Oncology, 123, p.S502.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can research add

value?. Sustainability Accounting, Management and Policy Journal, 6(1), pp.29-53.

Ge, Q., Simnett, R. and Zhou, S., 2016. Ethical and Quality Control Requirements When

Undertaking Assurance Engagements.

Green, W., Green, W., Taylor, S., Taylor, S., Wu, J. and Wu, J., 2017. Determinants of

greenhouse gas assurance provider choice. Meditari Accountancy Research, 25(1), pp.114-135.

Greer, P., Legge, K., Miri, N., Vial, P., Fuangrod, T. and Lehmann, J., 2017. OC-0537: A remote

EPID-based dosimetric auditing method for VMAT delivery using a digital phantom

concept. Radiotherapy and Oncology, 123, pp.S285-S286.

Hay, D., Stewart, J. and Botica Redmayne, N., 2016. The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis.

Heenetigala, K. and Armstrong, A.F., 2017. CREDIBILITY OF SUSTAINABILITY REPORTS

OF MINING SECTOR COMPANIES IN AUSTRALIA: AN INVESTIGATION OF

EXTERNAL ASSURANCE. Economic and Social Development: Book of Proceedings, p.335.

Houghton, K. and Campbell, T., 2013. Ethics and auditing (p. 354). ANU Press.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Martinov-Bennie, N., O'Neill, S., Cheung, A. and Wolfe, M.K., 2014. Issues in the assurance and

verification of work health and safety information.

Miri, N., Legge, K., Lehmann, J., Vial, P., Zwan, B. and Greer, P., 2017. PO-0907: Remote

auditing of IMRT/VMAT deliveries. Radiotherapy and Oncology, 123, p.S502.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can research add

value?. Sustainability Accounting, Management and Policy Journal, 6(1), pp.29-53.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.