Auditing and Assurance Report: Analysis of Double Ink Printers Limited

VerifiedAdded on 2020/02/18

|13

|2606

|118

Report

AI Summary

This report offers a comprehensive auditing and assurance analysis of Double Ink Printers Limited (DIPL). The analysis begins with an implementation of analytical processes to the financial report, evaluating profitability, liquidity, efficiency, and solvency ratios over three years. It examines the decline in gross profit and return on assets, improvements in liquidity, and the implications of efficiency and solvency ratios. The report then identifies inherent risks stemming from DIPL's business operations, including financial risks related to debt covenants and risks associated with information technology and potential misstatements. Finally, it discusses important risk facets associated with material misstatement in financial reporting, particularly debt covenants and improper segmentation of work, and their impact on audit planning, including the influence of control environment and the need to verify inventory balances and order quantities. The report references several academic sources to support its findings and recommendations.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

University Name

Student Name

Authors’ Note

Auditing and Assurance

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

AUDITING AND ASSURANCE

Solution to Question 1:

Part A

Implementation of analytical process to the financial report of Double Ink Printers

Limited (DIPL)

Proper employment of specific analytical processes to different financial declarations of the

corporation can back the process of improvement of the design of audit. Basically, audit

planning can replicate particular guideline that need to be monitored during a particular time

of execution of audit exercise. Essentially, strategy of analysis also helps assessors in

supporting and examining audit expends at sensible phase (Eilifsen et al. 2013). Additionally,

this also helps in the elucidating the misapprehension along with miscommunication with

different consumers of particular corporation. Inspective mechanism of mainly common

sizing supports analysis of financial statements in a particular way. Essentially, evaluators

can also speak about diverse categories of elements detected in the financial assertions.

Subsequently, this can help in assessment of the overall manner of disclosing different

economic announcements. Again, this mechanism can be appropriately implemented for

evaluating financial assertions and simultaneously evaluating idea of financial evaluation.

Ratio analysis system can be implemented for the analytical assessment after analysis of

financial information of the company Double Ink Printers Limited (DIPL) for three

successive years (Beasley 2015)

Analysis of Profitability of DIPL

AUDITING AND ASSURANCE

Solution to Question 1:

Part A

Implementation of analytical process to the financial report of Double Ink Printers

Limited (DIPL)

Proper employment of specific analytical processes to different financial declarations of the

corporation can back the process of improvement of the design of audit. Basically, audit

planning can replicate particular guideline that need to be monitored during a particular time

of execution of audit exercise. Essentially, strategy of analysis also helps assessors in

supporting and examining audit expends at sensible phase (Eilifsen et al. 2013). Additionally,

this also helps in the elucidating the misapprehension along with miscommunication with

different consumers of particular corporation. Inspective mechanism of mainly common

sizing supports analysis of financial statements in a particular way. Essentially, evaluators

can also speak about diverse categories of elements detected in the financial assertions.

Subsequently, this can help in assessment of the overall manner of disclosing different

economic announcements. Again, this mechanism can be appropriately implemented for

evaluating financial assertions and simultaneously evaluating idea of financial evaluation.

Ratio analysis system can be implemented for the analytical assessment after analysis of

financial information of the company Double Ink Printers Limited (DIPL) for three

successive years (Beasley 2015)

Analysis of Profitability of DIPL

3

AUDITING AND ASSURANCE

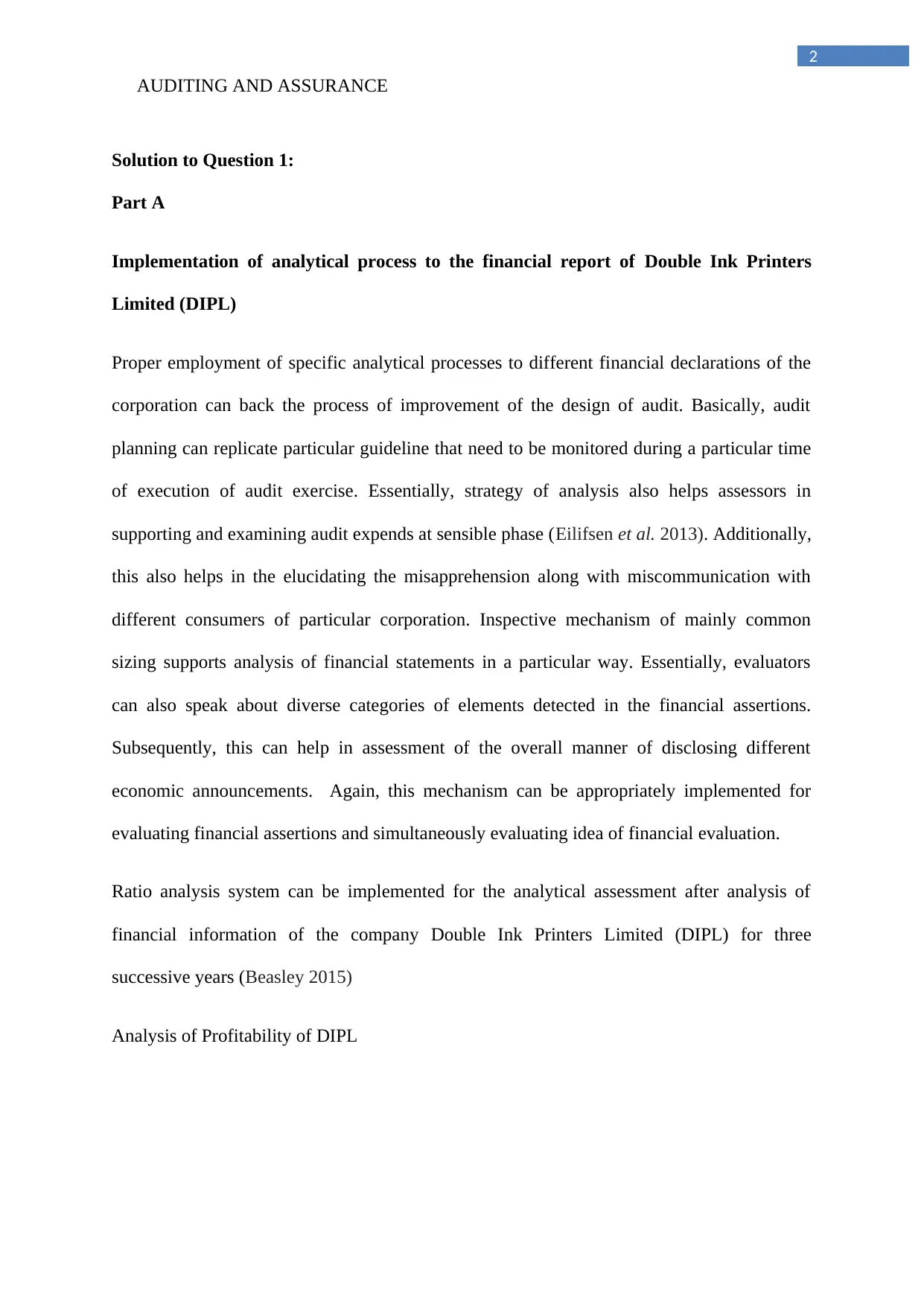

The table presented above reflects the profitability ratio of the company Double Ink Printers

and each one of ratio represents the overall profitability position of the business corporation.

- Analysis of the gross profit ratio of the firm for 3 successive years reveals the

profitability condition of the firm. This gross profit ratio of the corporation has

declined from 17.55% to around 16.13% and further to 15.20% during the year 2015.

- Net profit of the firm DIPL for the 3 successive years is recorded to be 6.09% during

2013, 6.08% registered 2014 and 6.84% recorded during the year 2015. Enhanced net

profit ratio of the firm documented during the year 2015 is mainly due to high interest

expends of the firm for that specific year incurred by DIPL (Humphrey et al. 2014)

- Return on Assets (ROA) of firm DIPL is calculated to be 18.25% during the year

2013, 14.41% during the year 2014 and 11.3% during the year 2015. Downward trend

of ROA for the firm is not desirable and therefore this calls for the need for

AUDITING AND ASSURANCE

The table presented above reflects the profitability ratio of the company Double Ink Printers

and each one of ratio represents the overall profitability position of the business corporation.

- Analysis of the gross profit ratio of the firm for 3 successive years reveals the

profitability condition of the firm. This gross profit ratio of the corporation has

declined from 17.55% to around 16.13% and further to 15.20% during the year 2015.

- Net profit of the firm DIPL for the 3 successive years is recorded to be 6.09% during

2013, 6.08% registered 2014 and 6.84% recorded during the year 2015. Enhanced net

profit ratio of the firm documented during the year 2015 is mainly due to high interest

expends of the firm for that specific year incurred by DIPL (Humphrey et al. 2014)

- Return on Assets (ROA) of firm DIPL is calculated to be 18.25% during the year

2013, 14.41% during the year 2014 and 11.3% during the year 2015. Downward trend

of ROA for the firm is not desirable and therefore this calls for the need for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

AUDITING AND ASSURANCE

engagement in further acquirement of assets in the upcoming future (Broberg et al.

2013).

- Return on Equity (ROE) of the corporation DIPL for 3 successive years is enumerated

to be 25.78% during the year 2013, 21.25% during the year 2014 and 24.26% during

the year 2015.

Liquidity Analysis

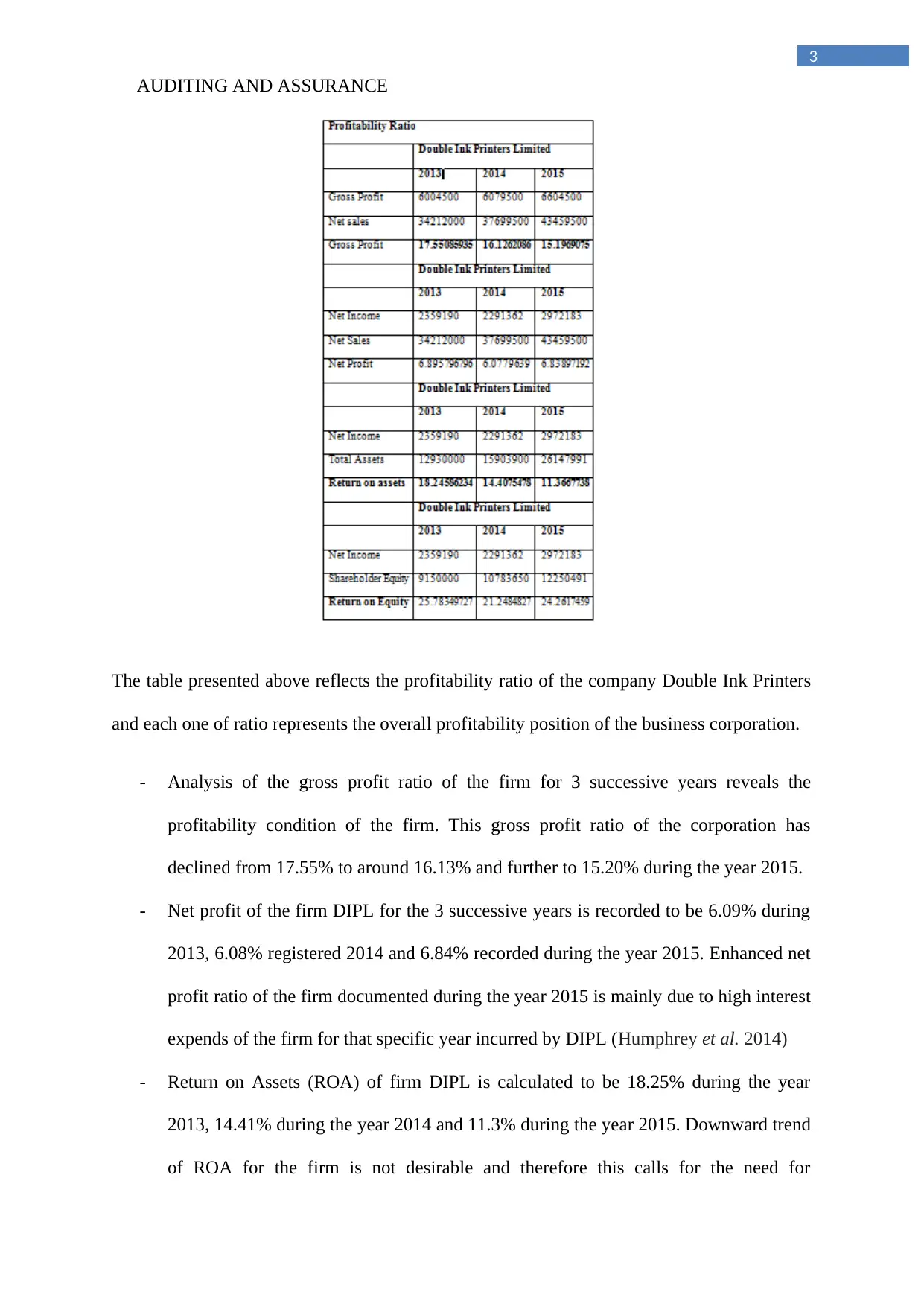

The table presented replicates the liquidity condition of the corporation DIPL and this

table shows that the liquidity condition of the firm has improved considerably over the

three successive years

- Current ratio enumerated from the financial report of the firm DIPL is recorded to be

1.42 during the year 2013, 1.47 during the year 2014 and 1.50 during the year 2015.

In essence, this shows that the liquidity condition of the firm DIPL has considerably

enhanced marginally during the year 2015 (Arens et al. 2014).

AUDITING AND ASSURANCE

engagement in further acquirement of assets in the upcoming future (Broberg et al.

2013).

- Return on Equity (ROE) of the corporation DIPL for 3 successive years is enumerated

to be 25.78% during the year 2013, 21.25% during the year 2014 and 24.26% during

the year 2015.

Liquidity Analysis

The table presented replicates the liquidity condition of the corporation DIPL and this

table shows that the liquidity condition of the firm has improved considerably over the

three successive years

- Current ratio enumerated from the financial report of the firm DIPL is recorded to be

1.42 during the year 2013, 1.47 during the year 2014 and 1.50 during the year 2015.

In essence, this shows that the liquidity condition of the firm DIPL has considerably

enhanced marginally during the year 2015 (Arens et al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

AUDITING AND ASSURANCE

- Quick ratio calculated from the pecuniary declaration of the corporation for the 3

successive years is registered to be 0.83 during the year 2013, 0.94 during the year

2014 and 0.85 during the year 2015. However, the ideal quick ratio is necessarily

1.5:1. Essentially, this divulges the fact that the liquid assets of the firm DIPL have

not considerably improved during the year 2015.

Analysis of efficiency

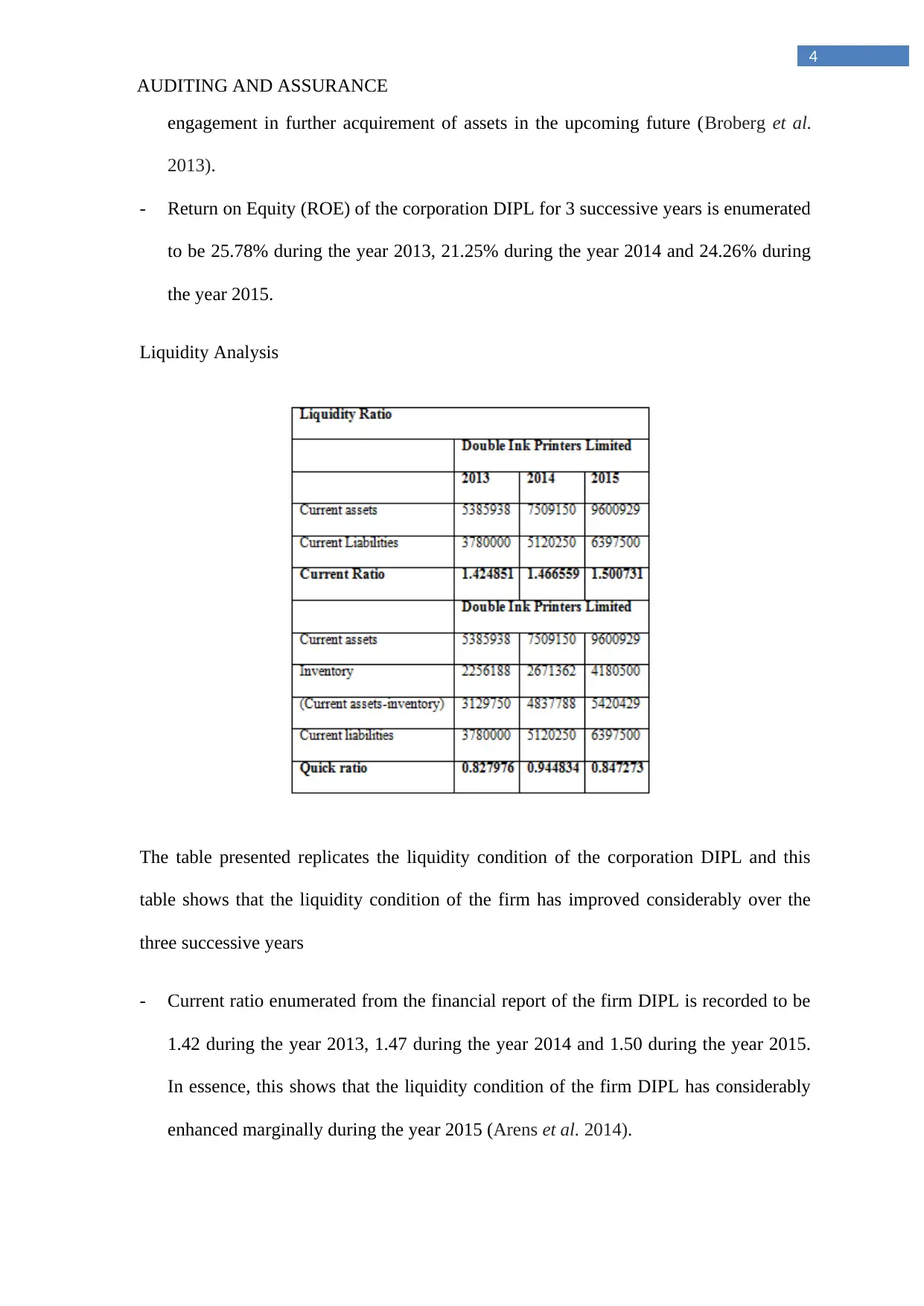

The table presented above reflects the efficiency ratio of the company DIPL for three

successive years

- Ratio of DIPL’s Inventory turnover derived from the monetary statement of the firm

for the specified 3 following years is derived to be nearly12.50 in FY 2013, 11.84 in

FY 2014 and 8.82 during the year 2015.

- DIPL’s Debtor’s turnover estimated from the monetary account of the business for

three following years is found to be roughly 13.78% during FY 2013, 8.73% in FY

2014 and 8.57 in FY 2015.

AUDITING AND ASSURANCE

- Quick ratio calculated from the pecuniary declaration of the corporation for the 3

successive years is registered to be 0.83 during the year 2013, 0.94 during the year

2014 and 0.85 during the year 2015. However, the ideal quick ratio is necessarily

1.5:1. Essentially, this divulges the fact that the liquid assets of the firm DIPL have

not considerably improved during the year 2015.

Analysis of efficiency

The table presented above reflects the efficiency ratio of the company DIPL for three

successive years

- Ratio of DIPL’s Inventory turnover derived from the monetary statement of the firm

for the specified 3 following years is derived to be nearly12.50 in FY 2013, 11.84 in

FY 2014 and 8.82 during the year 2015.

- DIPL’s Debtor’s turnover estimated from the monetary account of the business for

three following years is found to be roughly 13.78% during FY 2013, 8.73% in FY

2014 and 8.57 in FY 2015.

6

AUDITING AND ASSURANCE

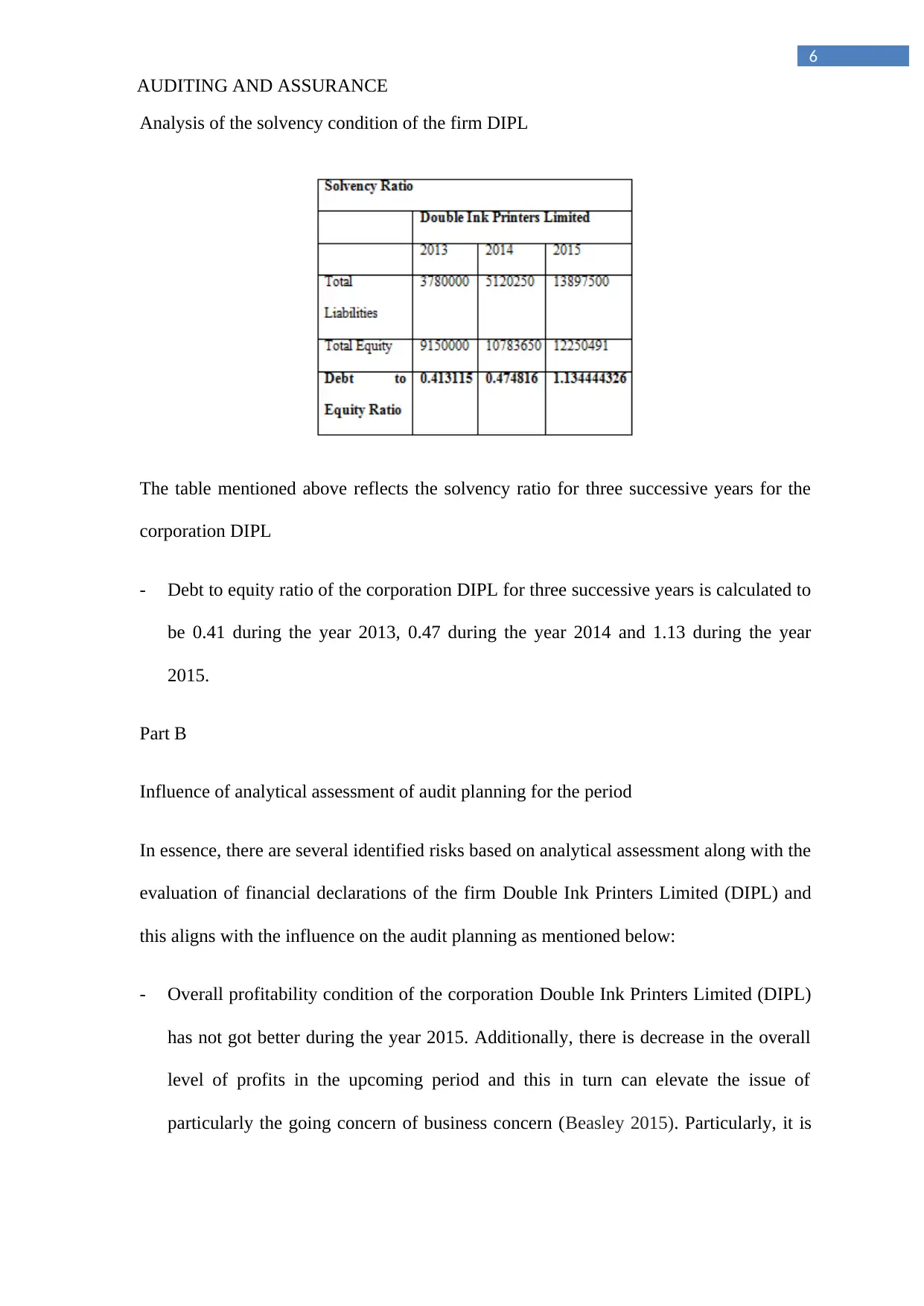

Analysis of the solvency condition of the firm DIPL

The table mentioned above reflects the solvency ratio for three successive years for the

corporation DIPL

- Debt to equity ratio of the corporation DIPL for three successive years is calculated to

be 0.41 during the year 2013, 0.47 during the year 2014 and 1.13 during the year

2015.

Part B

Influence of analytical assessment of audit planning for the period

In essence, there are several identified risks based on analytical assessment along with the

evaluation of financial declarations of the firm Double Ink Printers Limited (DIPL) and

this aligns with the influence on the audit planning as mentioned below:

- Overall profitability condition of the corporation Double Ink Printers Limited (DIPL)

has not got better during the year 2015. Additionally, there is decrease in the overall

level of profits in the upcoming period and this in turn can elevate the issue of

particularly the going concern of business concern (Beasley 2015). Particularly, it is

AUDITING AND ASSURANCE

Analysis of the solvency condition of the firm DIPL

The table mentioned above reflects the solvency ratio for three successive years for the

corporation DIPL

- Debt to equity ratio of the corporation DIPL for three successive years is calculated to

be 0.41 during the year 2013, 0.47 during the year 2014 and 1.13 during the year

2015.

Part B

Influence of analytical assessment of audit planning for the period

In essence, there are several identified risks based on analytical assessment along with the

evaluation of financial declarations of the firm Double Ink Printers Limited (DIPL) and

this aligns with the influence on the audit planning as mentioned below:

- Overall profitability condition of the corporation Double Ink Printers Limited (DIPL)

has not got better during the year 2015. Additionally, there is decrease in the overall

level of profits in the upcoming period and this in turn can elevate the issue of

particularly the going concern of business concern (Beasley 2015). Particularly, it is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

AUDITING AND ASSURANCE

crucial to undertake an in-depth evaluation of the firm that need to be planned for

exploring the future scenario of the firm Double Ink Printers Limited (Dennis 2015).

- There exists greater financial risk in the operations of the corporation Double Ink

Printers Limited (DIPL). However, the disclosures are associated to certain category

of risks that have the need to be assessed after checking the fact whether information

regarding the same has been explicitly mentioned in the declarations (Glover et al.

2016).

- There is considerable shrink in the efficiency of the administration of the firm Double

Ink Printers Limited (DIPL). This leads to issues in the management of the current

assets of the corporation. This reflects the need for the management to make an effort

to recognize the plausible reasons behind the decline in the level of efficiency of the

management of the firm (Eilifsen et al. 2013).

Solution to Question 2

Recognition of inherent risk factors stemming from business operations of DIPL

Recognition of Risk Material Misstatement of financial

declaration

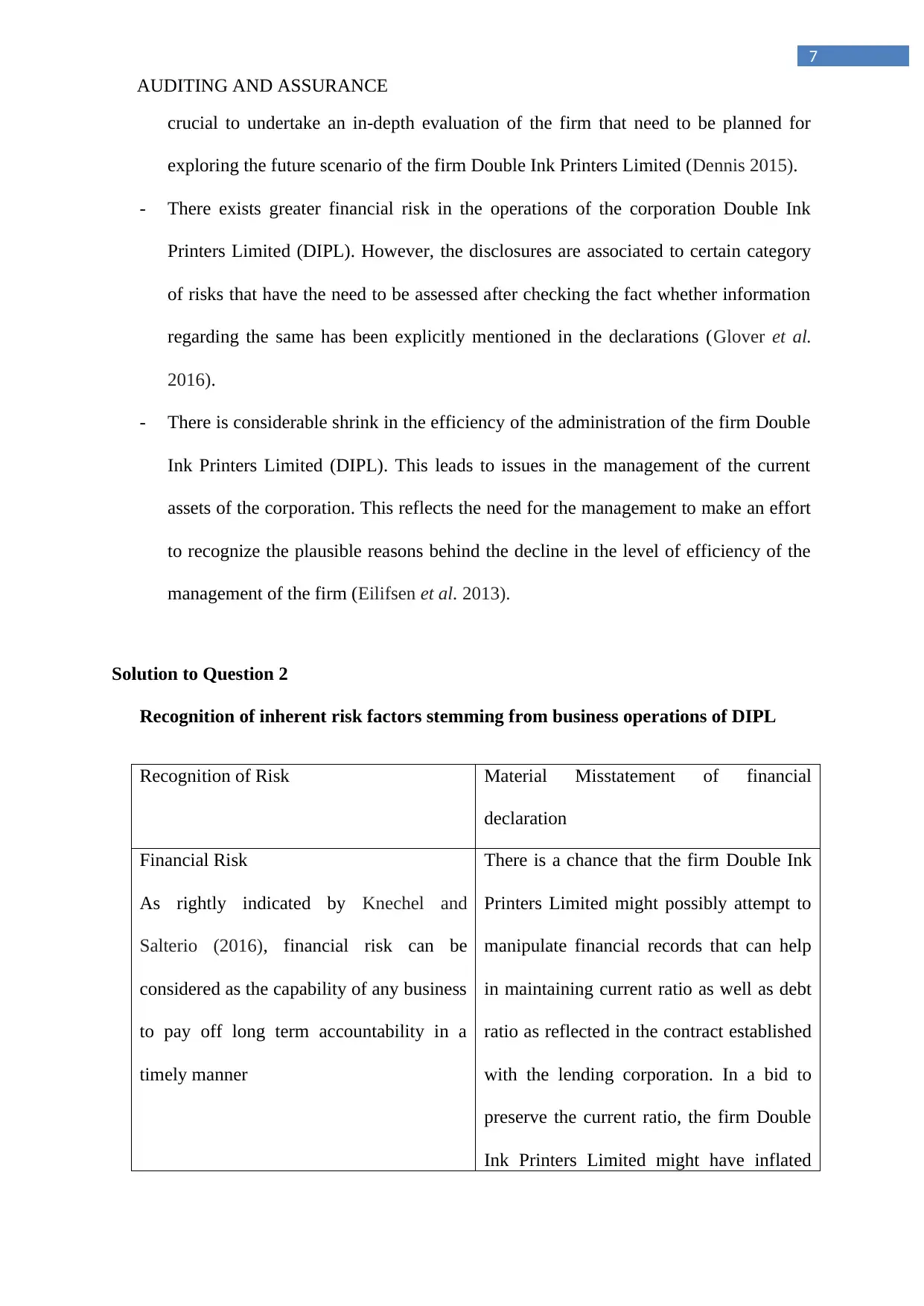

Financial Risk

As rightly indicated by Knechel and

Salterio (2016), financial risk can be

considered as the capability of any business

to pay off long term accountability in a

timely manner

There is a chance that the firm Double Ink

Printers Limited might possibly attempt to

manipulate financial records that can help

in maintaining current ratio as well as debt

ratio as reflected in the contract established

with the lending corporation. In a bid to

preserve the current ratio, the firm Double

Ink Printers Limited might have inflated

AUDITING AND ASSURANCE

crucial to undertake an in-depth evaluation of the firm that need to be planned for

exploring the future scenario of the firm Double Ink Printers Limited (Dennis 2015).

- There exists greater financial risk in the operations of the corporation Double Ink

Printers Limited (DIPL). However, the disclosures are associated to certain category

of risks that have the need to be assessed after checking the fact whether information

regarding the same has been explicitly mentioned in the declarations (Glover et al.

2016).

- There is considerable shrink in the efficiency of the administration of the firm Double

Ink Printers Limited (DIPL). This leads to issues in the management of the current

assets of the corporation. This reflects the need for the management to make an effort

to recognize the plausible reasons behind the decline in the level of efficiency of the

management of the firm (Eilifsen et al. 2013).

Solution to Question 2

Recognition of inherent risk factors stemming from business operations of DIPL

Recognition of Risk Material Misstatement of financial

declaration

Financial Risk

As rightly indicated by Knechel and

Salterio (2016), financial risk can be

considered as the capability of any business

to pay off long term accountability in a

timely manner

There is a chance that the firm Double Ink

Printers Limited might possibly attempt to

manipulate financial records that can help

in maintaining current ratio as well as debt

ratio as reflected in the contract established

with the lending corporation. In a bid to

preserve the current ratio, the firm Double

Ink Printers Limited might have inflated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

AUDITING AND ASSURANCE

the overall current assets by means of

enhanced value of specific receivables or

else stock (Louwers et al. 2015). However,

for maintaining the debt equity ratio,

management of the firm Double Ink

Printers Limited might have inflated the

overall value of equity by means of

enhanced value of retained income (Arens

et al. 2016).

Risk related to Information Technology

Hayes et al. (2014) asserts that adoption of

information technology gives rise to severe

threats to any organization. Essentially, in

this case, deficiency in the information

technology control might possibly have

adverse influence on the business

operations of the corporation (Knechel and

Salterio 2016)

Analysis of the operations of the

corporation Double Ink Printers Limited

reveals the fact that the management of the

firm could not maintain an appropriate

balance between new systems of

accounting along with the existing system

of software. Furthermore, there also exists

an issue regarding inadequate allocation of

dealings for a specific period of time

(DeFond and Zhang 2014). However, the

accounting notion of periodicity of the firm

was also not properly followed. This

probably could lead to imprecise

presentation of the condition of profitability

as well as the financial position of the firm

Double Ink Printers Limited (DIPL).

AUDITING AND ASSURANCE

the overall current assets by means of

enhanced value of specific receivables or

else stock (Louwers et al. 2015). However,

for maintaining the debt equity ratio,

management of the firm Double Ink

Printers Limited might have inflated the

overall value of equity by means of

enhanced value of retained income (Arens

et al. 2016).

Risk related to Information Technology

Hayes et al. (2014) asserts that adoption of

information technology gives rise to severe

threats to any organization. Essentially, in

this case, deficiency in the information

technology control might possibly have

adverse influence on the business

operations of the corporation (Knechel and

Salterio 2016)

Analysis of the operations of the

corporation Double Ink Printers Limited

reveals the fact that the management of the

firm could not maintain an appropriate

balance between new systems of

accounting along with the existing system

of software. Furthermore, there also exists

an issue regarding inadequate allocation of

dealings for a specific period of time

(DeFond and Zhang 2014). However, the

accounting notion of periodicity of the firm

was also not properly followed. This

probably could lead to imprecise

presentation of the condition of profitability

as well as the financial position of the firm

Double Ink Printers Limited (DIPL).

9

AUDITING AND ASSURANCE

Possible reasons that lead to the occurrence of inherent risks associated to material

misstatement in the financial assertions of the corporation include the following:

- Excessive stress related to work as well as overload of work on the entire workforce

and management of the corporation

- Risk associated to undertaking various tasks carried out by different professional

accountants in a erroneous way and this might lead to misrepresentation in the

pecuniary declarations of the firm

- Trustworthiness of the entire management as well as board of the corporation Double

Ink Printers Limited (DIPL)

- Strain on the overall administration of the corporation

- Features along with the nature of operation of the business corporation Double Ink

Printers Limited (DIPL).

Solution to Question 3:

Important risk facets associated to material misstatement in financial reporting

- One of the most important risk facets that are encountered by the firm Double Ink

Printers Limited is necessarily debt covenants. Financial statements of the corporation

stating about financial circumstances of the business concern proposes about profit of

the corporation. This also aids in the process of identification of the fact that

corporations have enhanced the overall proceeds of the firm during a particular time

period (FY 2013 and FY 2015). Apart from this, the present business case also

reflects that enumerated revenue from sales together with the sales revenue is

witnessed to have increased.

AUDITING AND ASSURANCE

Possible reasons that lead to the occurrence of inherent risks associated to material

misstatement in the financial assertions of the corporation include the following:

- Excessive stress related to work as well as overload of work on the entire workforce

and management of the corporation

- Risk associated to undertaking various tasks carried out by different professional

accountants in a erroneous way and this might lead to misrepresentation in the

pecuniary declarations of the firm

- Trustworthiness of the entire management as well as board of the corporation Double

Ink Printers Limited (DIPL)

- Strain on the overall administration of the corporation

- Features along with the nature of operation of the business corporation Double Ink

Printers Limited (DIPL).

Solution to Question 3:

Important risk facets associated to material misstatement in financial reporting

- One of the most important risk facets that are encountered by the firm Double Ink

Printers Limited is necessarily debt covenants. Financial statements of the corporation

stating about financial circumstances of the business concern proposes about profit of

the corporation. This also aids in the process of identification of the fact that

corporations have enhanced the overall proceeds of the firm during a particular time

period (FY 2013 and FY 2015). Apart from this, the present business case also

reflects that enumerated revenue from sales together with the sales revenue is

witnessed to have increased.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

AUDITING AND ASSURANCE

Particularly, there exists huge pressure on the entire finance segment of the firm for

meeting up diverse debt covenants. Additionally, a loan amount of approximately 7.5

million was derived from the institution BDO Finance during the year 2015 founded

on two different covenants. The standard current ratio is essentially 2:1 and debt ratio

need not be lower than 1. Again, in case of the corporation Double Ink Printers

Limited fails to satisfy the two different conditions, then the loan might be taken back

and that again can negatively influence the overall operations of business concern

(William Jr et al. 2016). However, there remains a possibility that the specific current

assets of the corporation might have got inflated so that the standard level of current

ratio can be maintained. Again, there can be manipulations of retained income in

which debt ratio need not be lower than 1 (Kogan et al. 2014).

- One of the most significant factors of risk that lead to existence of fraudulent

exercises in financial reporting is presence of improperly defined job descriptions

along with the improper segmentation of work. In addition to this, there also remains

a probability that firm’s inventory can be controlled by means of fewer number of

stock during the time of cash arrival (Mihret 2014). Thus, it can be hereby said that

there is an improper system that can be utilized for documentation and prevention of

fraud. Essentially, the practice of estimation of inventory of particularly raw materials

at specific average cost was not appropriate since the charge of specifically paper was

considerably beyond the mean cost.

AUDITING AND ASSURANCE

Particularly, there exists huge pressure on the entire finance segment of the firm for

meeting up diverse debt covenants. Additionally, a loan amount of approximately 7.5

million was derived from the institution BDO Finance during the year 2015 founded

on two different covenants. The standard current ratio is essentially 2:1 and debt ratio

need not be lower than 1. Again, in case of the corporation Double Ink Printers

Limited fails to satisfy the two different conditions, then the loan might be taken back

and that again can negatively influence the overall operations of business concern

(William Jr et al. 2016). However, there remains a possibility that the specific current

assets of the corporation might have got inflated so that the standard level of current

ratio can be maintained. Again, there can be manipulations of retained income in

which debt ratio need not be lower than 1 (Kogan et al. 2014).

- One of the most significant factors of risk that lead to existence of fraudulent

exercises in financial reporting is presence of improperly defined job descriptions

along with the improper segmentation of work. In addition to this, there also remains

a probability that firm’s inventory can be controlled by means of fewer number of

stock during the time of cash arrival (Mihret 2014). Thus, it can be hereby said that

there is an improper system that can be utilized for documentation and prevention of

fraud. Essentially, the practice of estimation of inventory of particularly raw materials

at specific average cost was not appropriate since the charge of specifically paper was

considerably beyond the mean cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

AUDITING AND ASSURANCE

Part B

Impact of risk factors on conduction of audit

During the process of evaluation of risk, auditing detects as well as examines the overall

likelihood along with the potential influence of diverse risks faced by the corporation.

- Influence of debt covenants on process of planning audit- It is significant to

balance firm’s current assets and liabilities after examining inflation in the current

assets or else deflation of current assets (Nagar et al. 2016). Furthermore, the balance

of equity also needs to be analysed by means of proper verification of retained

income.

- Influence of control environment on planning of audit- It is necessary to examine

the overall balance of inventory of the corporation Double Ink Printers Limited.

Besides, the overall quantity of specific orders placed for buying of stock that aligns

with the quantity received help in recognizing whether manipulation has been carried

out by accounts payable officials (Dennis 2015).

AUDITING AND ASSURANCE

Part B

Impact of risk factors on conduction of audit

During the process of evaluation of risk, auditing detects as well as examines the overall

likelihood along with the potential influence of diverse risks faced by the corporation.

- Influence of debt covenants on process of planning audit- It is significant to

balance firm’s current assets and liabilities after examining inflation in the current

assets or else deflation of current assets (Nagar et al. 2016). Furthermore, the balance

of equity also needs to be analysed by means of proper verification of retained

income.

- Influence of control environment on planning of audit- It is necessary to examine

the overall balance of inventory of the corporation Double Ink Printers Limited.

Besides, the overall quantity of specific orders placed for buying of stock that aligns

with the quantity received help in recognizing whether manipulation has been carried

out by accounts payable officials (Dennis 2015).

12

AUDITING AND ASSURANCE

References

Arens, A., Elder, R. and Beasley, M., 2014. Auditing and assurance services-An integrated

approach; includes coverage of international standards and global auditing issues, in addition

to coverage of. Boston: Aufl.

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Beasley, M.S., 2015. Auditing cases: An interactive learning approach. Prentice Hall.

Broberg, P., Umans, T. and Gerlofstig, C., 2013. Balance between auditing and marketing:

An explorative study. Journal of International Accounting, Auditing and Taxation, 22(1),

pp.57-70.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2), pp.275-326.

Dennis, I., 2015. Auditing Theory. Routledge.

Eilifsen, A., Messier, W.F., Glover, S.M. and Prawitt, D.F., 2013. Auditing and assurance

services. McGraw-Hill.

Glover, S.M., Prawitt, D.F. and Messier, W.F., 2016. Auditing and Assurance Services: A

Systematic Approach 10th.

Hayes, R., Wallage, P. and Gortemaker, H., 2014. Principles of auditing: an introduction to

international standards on auditing. Pearson Higher Ed.

Humphrey, C., Loft, A. and Samsonova-Taddei, A., 2014. The rise of international standards

on auditing. The Routledge Companion to Auditing, p.161.

AUDITING AND ASSURANCE

References

Arens, A., Elder, R. and Beasley, M., 2014. Auditing and assurance services-An integrated

approach; includes coverage of international standards and global auditing issues, in addition

to coverage of. Boston: Aufl.

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Beasley, M.S., 2015. Auditing cases: An interactive learning approach. Prentice Hall.

Broberg, P., Umans, T. and Gerlofstig, C., 2013. Balance between auditing and marketing:

An explorative study. Journal of International Accounting, Auditing and Taxation, 22(1),

pp.57-70.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2), pp.275-326.

Dennis, I., 2015. Auditing Theory. Routledge.

Eilifsen, A., Messier, W.F., Glover, S.M. and Prawitt, D.F., 2013. Auditing and assurance

services. McGraw-Hill.

Glover, S.M., Prawitt, D.F. and Messier, W.F., 2016. Auditing and Assurance Services: A

Systematic Approach 10th.

Hayes, R., Wallage, P. and Gortemaker, H., 2014. Principles of auditing: an introduction to

international standards on auditing. Pearson Higher Ed.

Humphrey, C., Loft, A. and Samsonova-Taddei, A., 2014. The rise of international standards

on auditing. The Routledge Companion to Auditing, p.161.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.