Auditing Assignment: Carmine Enterprises - Professional Practice 1

VerifiedAdded on 2023/06/05

|11

|2481

|356

Report

AI Summary

This auditing assignment solution focuses on Carmine Enterprises, providing an audit planning report that highlights key accounts requiring assessment. It utilizes preliminary analytical procedures such as trend analysis and common size income statements to identify critical areas. The report details how to determine materiality using various percentages and emphasizes its importance in audit planning. Audit assertions and associated risks are outlined for each critical account, and a fraud risk analysis is conducted to examine potential fraudulent activities within the organization. The assignment includes a trial balance, quantitative estimates of materiality, income statement analysis, and suggested audit procedures for accounts like sales, cost of sales, repair and maintenance, and wages.

Auditing and

Professional Practice

Assignment

Professional Practice

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Introduction.................................................................................................................................................3

Discussion and Analysis...............................................................................................................................4

Conclusion and Recommendation...............................................................................................................8

References...................................................................................................................................................9

2 | P a g e

Contents

Introduction.................................................................................................................................................3

Discussion and Analysis...............................................................................................................................4

Conclusion and Recommendation...............................................................................................................8

References...................................................................................................................................................9

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction

An audit planning report has been prepared on the given entity named “Carmine Enterprises”.

The report highlights the key and the critical accounts, which need assessment by the auditors.

The same has been selected using the preliminary audit analytical procedures like the trend

analysis and the common size income statement. The report also mentions how to determine

materiality in the case of the client using the various percentages as it is one of the important

measures of audit planning (Bromwich & Scapens, 2016). The report will be handed over by the

audit senior to the audit partner of the firm post preparation. The audit assertions and the

requisite risks have also been highlighted against each of the critical accounts. Towards the end,

the possibility of fraud in the organization has also been examined through fraud risk analysis.

3 | P a g e

Introduction

An audit planning report has been prepared on the given entity named “Carmine Enterprises”.

The report highlights the key and the critical accounts, which need assessment by the auditors.

The same has been selected using the preliminary audit analytical procedures like the trend

analysis and the common size income statement. The report also mentions how to determine

materiality in the case of the client using the various percentages as it is one of the important

measures of audit planning (Bromwich & Scapens, 2016). The report will be handed over by the

audit senior to the audit partner of the firm post preparation. The audit assertions and the

requisite risks have also been highlighted against each of the critical accounts. Towards the end,

the possibility of fraud in the organization has also been examined through fraud risk analysis.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Discussion and Analysis

The trial balance of the given company “Carmine Enterprises” has been shown below and the

difference in between the debit and the credit side can be assumed the suspense account. This

amount has not been considered in any of the calculations as the nature of the same is not

known as to if it is asset or liability or expense or income, etc. (Choy, 2018).

Carmine Enterprises

Trial Balance

Particulars Jul 1, 16 - Mar 31, 17 Jul 1, 15 - June 30, 16

Debit Credit Debit Credit

Cash at Bank 85,000 80,000

Accounts receivable 118,340 111,000

Inventory 187,500 174,000

Machinery 71,000 65,000

Accumulated Depreciation 30,300 24,375

Motor Vehicles 66,000 66,000

Accumulated Depreciation 26,678 21,000

Furniture 7,400 7,400

Accumulated Depreciation 2,760 2,220

Bank Loan 230,000 230,000

Sales 141,750 187,450

Cost of sales 52,125 63,595

Consultancy fees 44,438 57,000

Interest income 36 50

Bank charges 261 350

Depreciation 12,143 15,863

Interest expense 8,625 11,500

Printing 189 250

Repairs and Maintenance 1,080 5,050

Wages 36,000 53,000

Superannuation 2,670 4,770

Total 648,333 475,962 657,778 522,095

4 | P a g e

Discussion and Analysis

The trial balance of the given company “Carmine Enterprises” has been shown below and the

difference in between the debit and the credit side can be assumed the suspense account. This

amount has not been considered in any of the calculations as the nature of the same is not

known as to if it is asset or liability or expense or income, etc. (Choy, 2018).

Carmine Enterprises

Trial Balance

Particulars Jul 1, 16 - Mar 31, 17 Jul 1, 15 - June 30, 16

Debit Credit Debit Credit

Cash at Bank 85,000 80,000

Accounts receivable 118,340 111,000

Inventory 187,500 174,000

Machinery 71,000 65,000

Accumulated Depreciation 30,300 24,375

Motor Vehicles 66,000 66,000

Accumulated Depreciation 26,678 21,000

Furniture 7,400 7,400

Accumulated Depreciation 2,760 2,220

Bank Loan 230,000 230,000

Sales 141,750 187,450

Cost of sales 52,125 63,595

Consultancy fees 44,438 57,000

Interest income 36 50

Bank charges 261 350

Depreciation 12,143 15,863

Interest expense 8,625 11,500

Printing 189 250

Repairs and Maintenance 1,080 5,050

Wages 36,000 53,000

Superannuation 2,670 4,770

Total 648,333 475,962 657,778 522,095

4 | P a g e

5

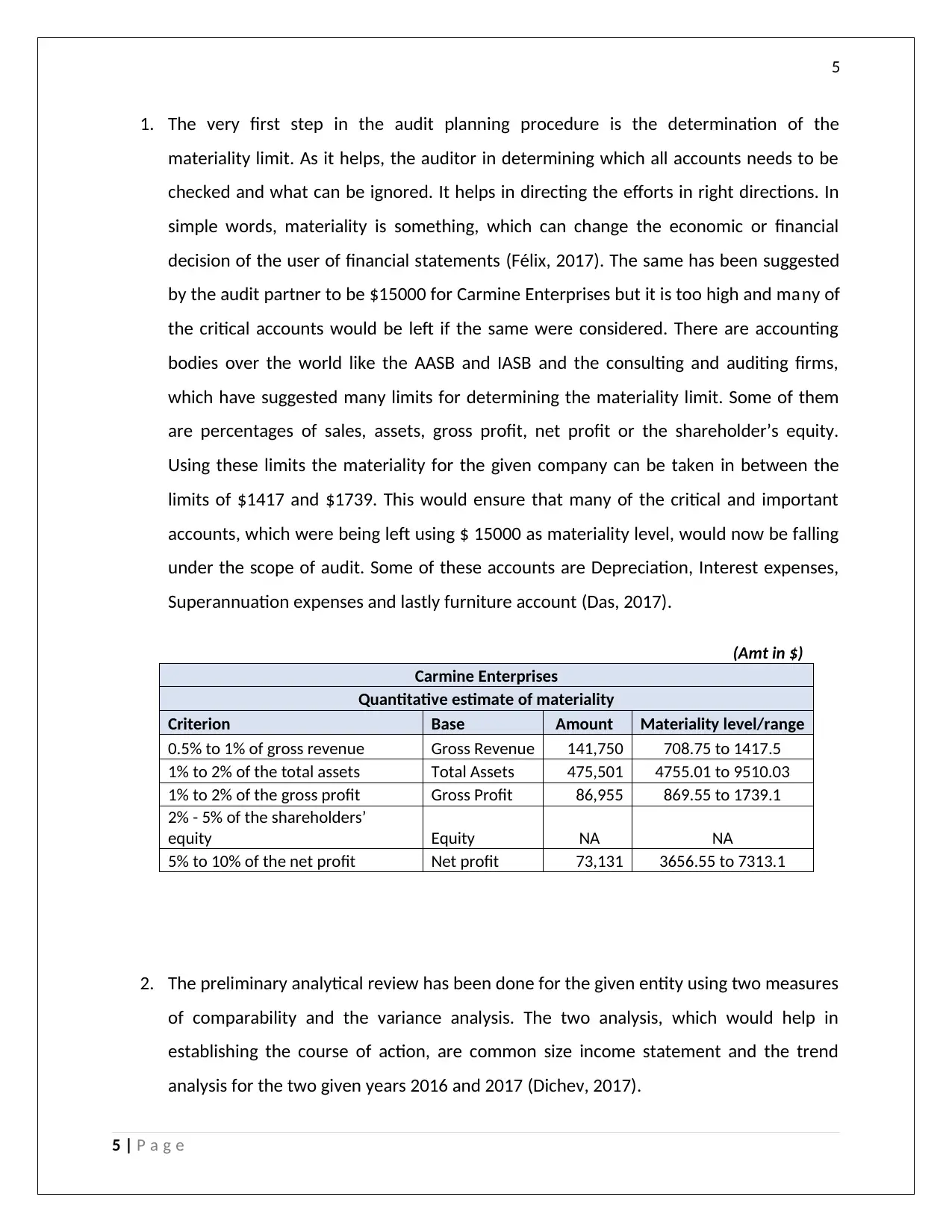

1. The very first step in the audit planning procedure is the determination of the

materiality limit. As it helps, the auditor in determining which all accounts needs to be

checked and what can be ignored. It helps in directing the efforts in right directions. In

simple words, materiality is something, which can change the economic or financial

decision of the user of financial statements (Félix, 2017). The same has been suggested

by the audit partner to be $15000 for Carmine Enterprises but it is too high and many of

the critical accounts would be left if the same were considered. There are accounting

bodies over the world like the AASB and IASB and the consulting and auditing firms,

which have suggested many limits for determining the materiality limit. Some of them

are percentages of sales, assets, gross profit, net profit or the shareholder’s equity.

Using these limits the materiality for the given company can be taken in between the

limits of $1417 and $1739. This would ensure that many of the critical and important

accounts, which were being left using $ 15000 as materiality level, would now be falling

under the scope of audit. Some of these accounts are Depreciation, Interest expenses,

Superannuation expenses and lastly furniture account (Das, 2017).

(Amt in $)

Carmine Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 141,750 708.75 to 1417.5

1% to 2% of the total assets Total Assets 475,501 4755.01 to 9510.03

1% to 2% of the gross profit Gross Profit 86,955 869.55 to 1739.1

2% - 5% of the shareholders’

equity Equity NA NA

5% to 10% of the net profit Net profit 73,131 3656.55 to 7313.1

2. The preliminary analytical review has been done for the given entity using two measures

of comparability and the variance analysis. The two analysis, which would help in

establishing the course of action, are common size income statement and the trend

analysis for the two given years 2016 and 2017 (Dichev, 2017).

5 | P a g e

1. The very first step in the audit planning procedure is the determination of the

materiality limit. As it helps, the auditor in determining which all accounts needs to be

checked and what can be ignored. It helps in directing the efforts in right directions. In

simple words, materiality is something, which can change the economic or financial

decision of the user of financial statements (Félix, 2017). The same has been suggested

by the audit partner to be $15000 for Carmine Enterprises but it is too high and many of

the critical accounts would be left if the same were considered. There are accounting

bodies over the world like the AASB and IASB and the consulting and auditing firms,

which have suggested many limits for determining the materiality limit. Some of them

are percentages of sales, assets, gross profit, net profit or the shareholder’s equity.

Using these limits the materiality for the given company can be taken in between the

limits of $1417 and $1739. This would ensure that many of the critical and important

accounts, which were being left using $ 15000 as materiality level, would now be falling

under the scope of audit. Some of these accounts are Depreciation, Interest expenses,

Superannuation expenses and lastly furniture account (Das, 2017).

(Amt in $)

Carmine Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 141,750 708.75 to 1417.5

1% to 2% of the total assets Total Assets 475,501 4755.01 to 9510.03

1% to 2% of the gross profit Gross Profit 86,955 869.55 to 1739.1

2% - 5% of the shareholders’

equity Equity NA NA

5% to 10% of the net profit Net profit 73,131 3656.55 to 7313.1

2. The preliminary analytical review has been done for the given entity using two measures

of comparability and the variance analysis. The two analysis, which would help in

establishing the course of action, are common size income statement and the trend

analysis for the two given years 2016 and 2017 (Dichev, 2017).

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

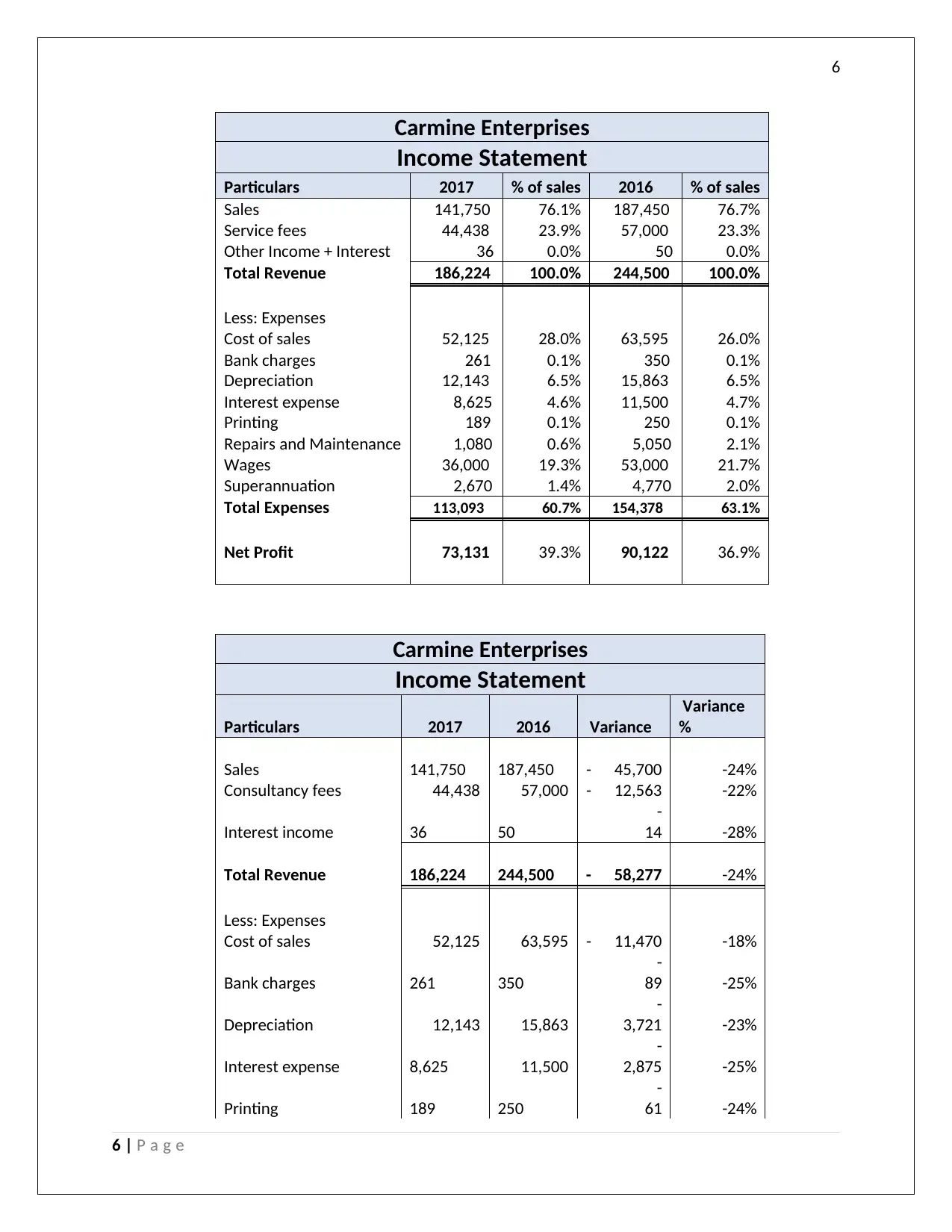

Carmine Enterprises

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 141,750 76.1% 187,450 76.7%

Service fees 44,438 23.9% 57,000 23.3%

Other Income + Interest 36 0.0% 50 0.0%

Total Revenue 186,224 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 52,125 28.0% 63,595 26.0%

Bank charges 261 0.1% 350 0.1%

Depreciation 12,143 6.5% 15,863 6.5%

Interest expense 8,625 4.6% 11,500 4.7%

Printing 189 0.1% 250 0.1%

Repairs and Maintenance 1,080 0.6% 5,050 2.1%

Wages 36,000 19.3% 53,000 21.7%

Superannuation 2,670 1.4% 4,770 2.0%

Total Expenses 113,093 60.7% 154,378 63.1%

Net Profit 73,131 39.3% 90,122 36.9%

Carmine Enterprises

Income Statement

Particulars 2017 2016 Variance

Variance

%

Sales 141,750 187,450 - 45,700 -24%

Consultancy fees 44,438 57,000 - 12,563 -22%

Interest income 36 50

-

14 -28%

Total Revenue 186,224 244,500 - 58,277 -24%

Less: Expenses

Cost of sales 52,125 63,595 - 11,470 -18%

Bank charges 261 350

-

89 -25%

Depreciation 12,143 15,863

-

3,721 -23%

Interest expense 8,625 11,500

-

2,875 -25%

Printing 189 250

-

61 -24%

6 | P a g e

Carmine Enterprises

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 141,750 76.1% 187,450 76.7%

Service fees 44,438 23.9% 57,000 23.3%

Other Income + Interest 36 0.0% 50 0.0%

Total Revenue 186,224 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 52,125 28.0% 63,595 26.0%

Bank charges 261 0.1% 350 0.1%

Depreciation 12,143 6.5% 15,863 6.5%

Interest expense 8,625 4.6% 11,500 4.7%

Printing 189 0.1% 250 0.1%

Repairs and Maintenance 1,080 0.6% 5,050 2.1%

Wages 36,000 19.3% 53,000 21.7%

Superannuation 2,670 1.4% 4,770 2.0%

Total Expenses 113,093 60.7% 154,378 63.1%

Net Profit 73,131 39.3% 90,122 36.9%

Carmine Enterprises

Income Statement

Particulars 2017 2016 Variance

Variance

%

Sales 141,750 187,450 - 45,700 -24%

Consultancy fees 44,438 57,000 - 12,563 -22%

Interest income 36 50

-

14 -28%

Total Revenue 186,224 244,500 - 58,277 -24%

Less: Expenses

Cost of sales 52,125 63,595 - 11,470 -18%

Bank charges 261 350

-

89 -25%

Depreciation 12,143 15,863

-

3,721 -23%

Interest expense 8,625 11,500

-

2,875 -25%

Printing 189 250

-

61 -24%

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

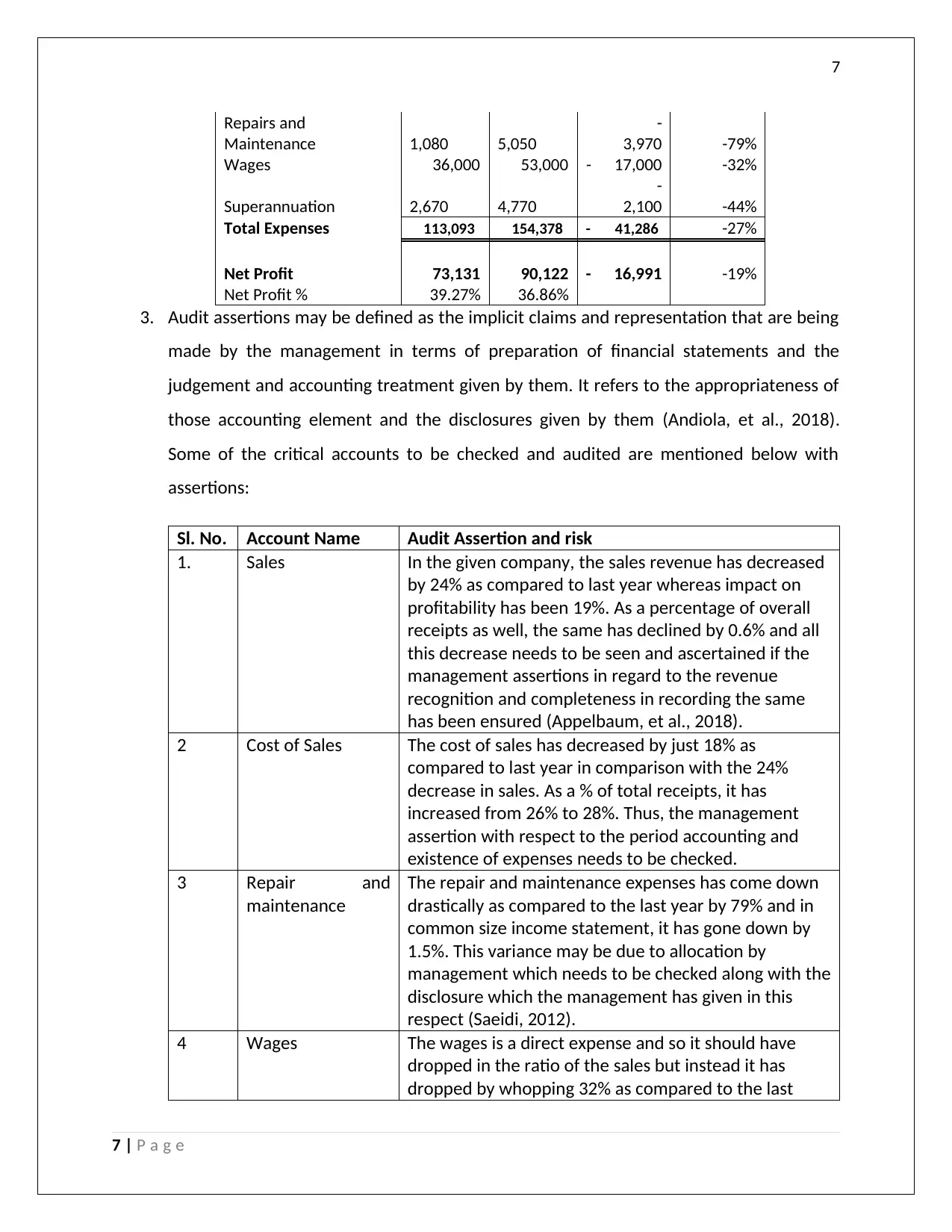

Repairs and

Maintenance 1,080 5,050

-

3,970 -79%

Wages 36,000 53,000 - 17,000 -32%

Superannuation 2,670 4,770

-

2,100 -44%

Total Expenses 113,093 154,378 - 41,286 -27%

Net Profit 73,131 90,122 - 16,991 -19%

Net Profit % 39.27% 36.86%

3. Audit assertions may be defined as the implicit claims and representation that are being

made by the management in terms of preparation of financial statements and the

judgement and accounting treatment given by them. It refers to the appropriateness of

those accounting element and the disclosures given by them (Andiola, et al., 2018).

Some of the critical accounts to be checked and audited are mentioned below with

assertions:

Sl. No. Account Name Audit Assertion and risk

1. Sales In the given company, the sales revenue has decreased

by 24% as compared to last year whereas impact on

profitability has been 19%. As a percentage of overall

receipts as well, the same has declined by 0.6% and all

this decrease needs to be seen and ascertained if the

management assertions in regard to the revenue

recognition and completeness in recording the same

has been ensured (Appelbaum, et al., 2018).

2 Cost of Sales The cost of sales has decreased by just 18% as

compared to last year in comparison with the 24%

decrease in sales. As a % of total receipts, it has

increased from 26% to 28%. Thus, the management

assertion with respect to the period accounting and

existence of expenses needs to be checked.

3 Repair and

maintenance

The repair and maintenance expenses has come down

drastically as compared to the last year by 79% and in

common size income statement, it has gone down by

1.5%. This variance may be due to allocation by

management which needs to be checked along with the

disclosure which the management has given in this

respect (Saeidi, 2012).

4 Wages The wages is a direct expense and so it should have

dropped in the ratio of the sales but instead it has

dropped by whopping 32% as compared to the last

7 | P a g e

Repairs and

Maintenance 1,080 5,050

-

3,970 -79%

Wages 36,000 53,000 - 17,000 -32%

Superannuation 2,670 4,770

-

2,100 -44%

Total Expenses 113,093 154,378 - 41,286 -27%

Net Profit 73,131 90,122 - 16,991 -19%

Net Profit % 39.27% 36.86%

3. Audit assertions may be defined as the implicit claims and representation that are being

made by the management in terms of preparation of financial statements and the

judgement and accounting treatment given by them. It refers to the appropriateness of

those accounting element and the disclosures given by them (Andiola, et al., 2018).

Some of the critical accounts to be checked and audited are mentioned below with

assertions:

Sl. No. Account Name Audit Assertion and risk

1. Sales In the given company, the sales revenue has decreased

by 24% as compared to last year whereas impact on

profitability has been 19%. As a percentage of overall

receipts as well, the same has declined by 0.6% and all

this decrease needs to be seen and ascertained if the

management assertions in regard to the revenue

recognition and completeness in recording the same

has been ensured (Appelbaum, et al., 2018).

2 Cost of Sales The cost of sales has decreased by just 18% as

compared to last year in comparison with the 24%

decrease in sales. As a % of total receipts, it has

increased from 26% to 28%. Thus, the management

assertion with respect to the period accounting and

existence of expenses needs to be checked.

3 Repair and

maintenance

The repair and maintenance expenses has come down

drastically as compared to the last year by 79% and in

common size income statement, it has gone down by

1.5%. This variance may be due to allocation by

management which needs to be checked along with the

disclosure which the management has given in this

respect (Saeidi, 2012).

4 Wages The wages is a direct expense and so it should have

dropped in the ratio of the sales but instead it has

dropped by whopping 32% as compared to the last

7 | P a g e

8

year. In terms of the common size income statement

again, it has dropped by more than 2.5% and thus it

needs to be checked if management has completely

recorded the expenses and considered appropriate

provision in the books (Solicitors, 2016).

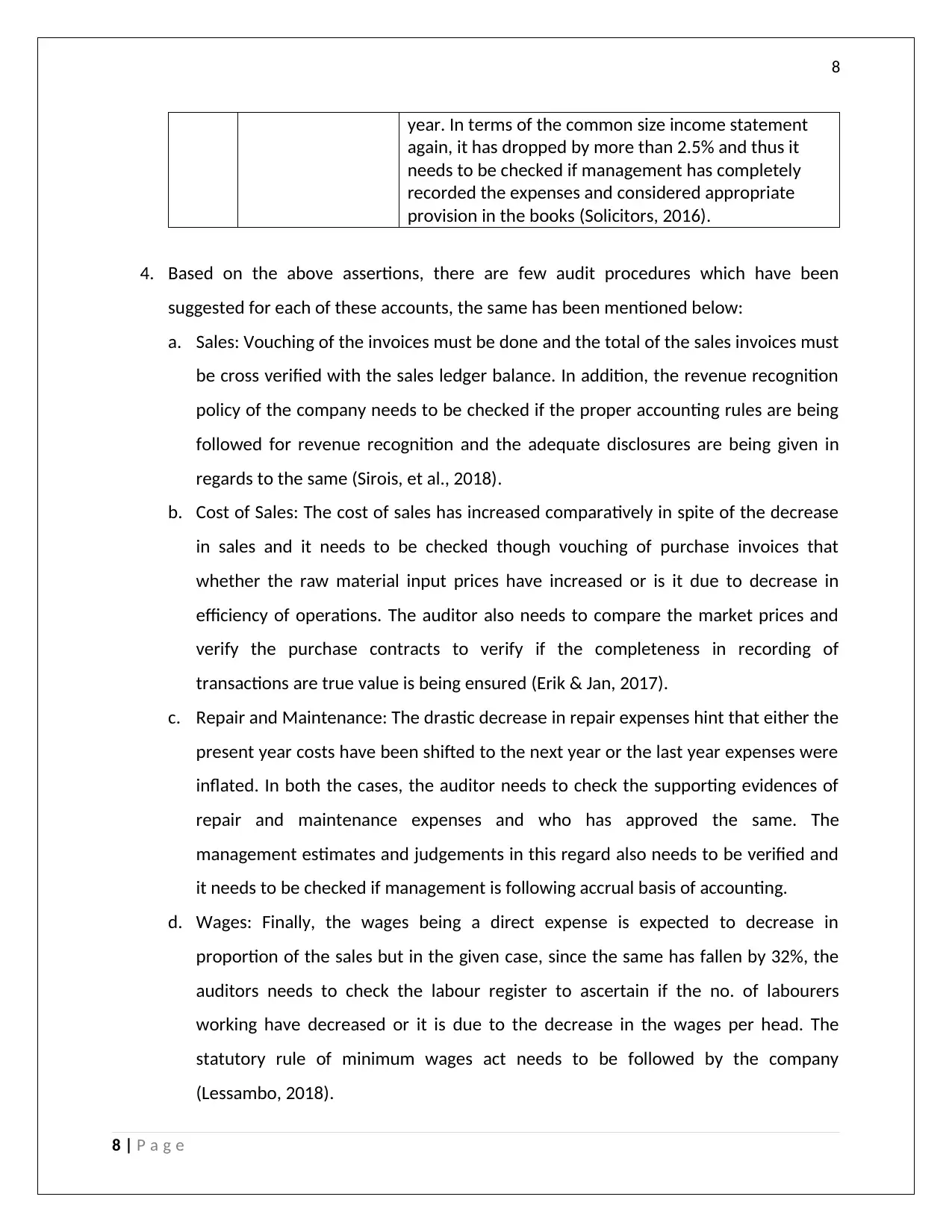

4. Based on the above assertions, there are few audit procedures which have been

suggested for each of these accounts, the same has been mentioned below:

a. Sales: Vouching of the invoices must be done and the total of the sales invoices must

be cross verified with the sales ledger balance. In addition, the revenue recognition

policy of the company needs to be checked if the proper accounting rules are being

followed for revenue recognition and the adequate disclosures are being given in

regards to the same (Sirois, et al., 2018).

b. Cost of Sales: The cost of sales has increased comparatively in spite of the decrease

in sales and it needs to be checked though vouching of purchase invoices that

whether the raw material input prices have increased or is it due to decrease in

efficiency of operations. The auditor also needs to compare the market prices and

verify the purchase contracts to verify if the completeness in recording of

transactions are true value is being ensured (Erik & Jan, 2017).

c. Repair and Maintenance: The drastic decrease in repair expenses hint that either the

present year costs have been shifted to the next year or the last year expenses were

inflated. In both the cases, the auditor needs to check the supporting evidences of

repair and maintenance expenses and who has approved the same. The

management estimates and judgements in this regard also needs to be verified and

it needs to be checked if management is following accrual basis of accounting.

d. Wages: Finally, the wages being a direct expense is expected to decrease in

proportion of the sales but in the given case, since the same has fallen by 32%, the

auditors needs to check the labour register to ascertain if the no. of labourers

working have decreased or it is due to the decrease in the wages per head. The

statutory rule of minimum wages act needs to be followed by the company

(Lessambo, 2018).

8 | P a g e

year. In terms of the common size income statement

again, it has dropped by more than 2.5% and thus it

needs to be checked if management has completely

recorded the expenses and considered appropriate

provision in the books (Solicitors, 2016).

4. Based on the above assertions, there are few audit procedures which have been

suggested for each of these accounts, the same has been mentioned below:

a. Sales: Vouching of the invoices must be done and the total of the sales invoices must

be cross verified with the sales ledger balance. In addition, the revenue recognition

policy of the company needs to be checked if the proper accounting rules are being

followed for revenue recognition and the adequate disclosures are being given in

regards to the same (Sirois, et al., 2018).

b. Cost of Sales: The cost of sales has increased comparatively in spite of the decrease

in sales and it needs to be checked though vouching of purchase invoices that

whether the raw material input prices have increased or is it due to decrease in

efficiency of operations. The auditor also needs to compare the market prices and

verify the purchase contracts to verify if the completeness in recording of

transactions are true value is being ensured (Erik & Jan, 2017).

c. Repair and Maintenance: The drastic decrease in repair expenses hint that either the

present year costs have been shifted to the next year or the last year expenses were

inflated. In both the cases, the auditor needs to check the supporting evidences of

repair and maintenance expenses and who has approved the same. The

management estimates and judgements in this regard also needs to be verified and

it needs to be checked if management is following accrual basis of accounting.

d. Wages: Finally, the wages being a direct expense is expected to decrease in

proportion of the sales but in the given case, since the same has fallen by 32%, the

auditors needs to check the labour register to ascertain if the no. of labourers

working have decreased or it is due to the decrease in the wages per head. The

statutory rule of minimum wages act needs to be followed by the company

(Lessambo, 2018).

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Conclusion and Recommendation

5. The fraud risk analysis is one of the important and necessary steps of the audit of an

entity. It involves checking a given entity for possibility of fraud using various

parameters. The audit partner has suggested that the given company should not be

subject to fraud risk analysis since the client is trustworthy but the same is not justified

as per the concept of professional scepticism and as per the standards laid down in

professional ethics in APES 110 which states that all the entities should be subject to

fraud risk analysis irrespective of the status and the past history of the client (Vieira, et

al., 2017). There are few accounts which do hint towards the possibility of the fraud in

the organization like that of repair and maintenance expense account and the wages

account for the reasons explained above and the superannuation account which is also

expected to be the fixed expense but which has decreased by a massive 44% as

compared to the last year. The main reason behind the increase in profitability also

needs to be studied as it indicates that the cost shifting might have taken place (Li,

2018).

References

Andiola, L., Lambert, T. & Lynch, E., 2018. Sprandel, Inc.: Electronic Workpapers, Audit Documentation,

and Closing Review Notes in the Audit of Accounts Receivable. Issues in Accounting Education, 33(2), pp.

43-55.

Appelbaum, D., Kogan, A. & Vasarhelyi, M., 2018. Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics.. Journal of Accounting

Literature, 40(1), pp. 83-101.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), pp. 1-9.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

9 | P a g e

Conclusion and Recommendation

5. The fraud risk analysis is one of the important and necessary steps of the audit of an

entity. It involves checking a given entity for possibility of fraud using various

parameters. The audit partner has suggested that the given company should not be

subject to fraud risk analysis since the client is trustworthy but the same is not justified

as per the concept of professional scepticism and as per the standards laid down in

professional ethics in APES 110 which states that all the entities should be subject to

fraud risk analysis irrespective of the status and the past history of the client (Vieira, et

al., 2017). There are few accounts which do hint towards the possibility of the fraud in

the organization like that of repair and maintenance expense account and the wages

account for the reasons explained above and the superannuation account which is also

expected to be the fixed expense but which has decreased by a massive 44% as

compared to the last year. The main reason behind the increase in profitability also

needs to be studied as it indicates that the cost shifting might have taken place (Li,

2018).

References

Andiola, L., Lambert, T. & Lynch, E., 2018. Sprandel, Inc.: Electronic Workpapers, Audit Documentation,

and Closing Review Notes in the Audit of Accounts Receivable. Issues in Accounting Education, 33(2), pp.

43-55.

Appelbaum, D., Kogan, A. & Vasarhelyi, M., 2018. Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics.. Journal of Accounting

Literature, 40(1), pp. 83-101.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), pp. 1-9.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Erik, H. & Jan, B., 2017. Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management, 47(8),

pp. 712-735.

Félix, M., 2017. A study on the expected impact of IFRS 17 on the transparency of financial statements of

insurance companies. MASTER THESIS, pp. 1-69.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Li, L. M. A. X. J. L. Z. a. S. M., 2018. Industry-wide corporate fraud: The truth behind the Volkswagen

scandal. Journal of Cleaner Production, pp. 3167-3175.

Saeidi, F., 2012. Audit expectations gap and corporate fraud: Empirical evidence from Iran. African

Journal of Business Management, 6(23), pp. 7031-41.

Sirois, L., Bédard, J. & Bera, P., 2018. The informational value of key audit matters in the auditor's report:

evidence from an Eye-tracking study.. Accounting Horizons., 32(2), pp. 141-162.

Solicitors, S., 2016. The Principles of Contract. Contract, p. 13.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1).

10 | P a g e

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Erik, H. & Jan, B., 2017. Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management, 47(8),

pp. 712-735.

Félix, M., 2017. A study on the expected impact of IFRS 17 on the transparency of financial statements of

insurance companies. MASTER THESIS, pp. 1-69.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Li, L. M. A. X. J. L. Z. a. S. M., 2018. Industry-wide corporate fraud: The truth behind the Volkswagen

scandal. Journal of Cleaner Production, pp. 3167-3175.

Saeidi, F., 2012. Audit expectations gap and corporate fraud: Empirical evidence from Iran. African

Journal of Business Management, 6(23), pp. 7031-41.

Sirois, L., Bédard, J. & Bera, P., 2018. The informational value of key audit matters in the auditor's report:

evidence from an Eye-tracking study.. Accounting Horizons., 32(2), pp. 141-162.

Solicitors, S., 2016. The Principles of Contract. Contract, p. 13.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1).

10 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.