Audit Planning Report for Small Entity: Fallow Enterprises

VerifiedAdded on 2023/06/04

|12

|2303

|387

AI Summary

This report highlights audit procedures, audit risks, and fraud risk analysis for Fallow Enterprises. It includes a preliminary analytical review, materiality level determination, and audit assertions for critical accounts. The report recommends fraud risk analysis despite the audit partner's suggestion against it.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Auditing and

Professional Practice

Assignment

Professional Practice

Assignment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

The report has been prepared on the audit planning of one of the small entities. The audit

procedures and the audit risks have been highlighted for few of the critical accounts. Towards the

end, the fraud risk analysis has also been done which will help in identifying the frauds in the

company, if any. The report will be handed over to audit partner of audit firm.

2 | P a g e

Executive Summary

The report has been prepared on the audit planning of one of the small entities. The audit

procedures and the audit risks have been highlighted for few of the critical accounts. Towards the

end, the fraud risk analysis has also been done which will help in identifying the frauds in the

company, if any. The report will be handed over to audit partner of audit firm.

2 | P a g e

3

Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Discussion and Analysis...............................................................................................................................5

Conclusion and Recommendation...............................................................................................................9

References.................................................................................................................................................10

3 | P a g e

Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Discussion and Analysis...............................................................................................................................5

Conclusion and Recommendation...............................................................................................................9

References.................................................................................................................................................10

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

Introduction

An audit planning (ASA 300) report has been prepared for one of the small companies. The trial

balance of the entity has been given and based on the same the preliminary analytical review has

been done. As a part of the audit procedures, the materiality level has been determined and also

the common size income statement and the trend analysis has been prepared for the 2 given years

to find out the major variations and find out the accounts to be audited. Fraud risk analysis has

been done for the given client and the necessary audit procedures have been mentioned in the

report (Marques, 2018). The report has to be handed over to the audit partner who has asked the

same from audit senior.

4 | P a g e

Introduction

An audit planning (ASA 300) report has been prepared for one of the small companies. The trial

balance of the entity has been given and based on the same the preliminary analytical review has

been done. As a part of the audit procedures, the materiality level has been determined and also

the common size income statement and the trend analysis has been prepared for the 2 given years

to find out the major variations and find out the accounts to be audited. Fraud risk analysis has

been done for the given client and the necessary audit procedures have been mentioned in the

report (Marques, 2018). The report has to be handed over to the audit partner who has asked the

same from audit senior.

4 | P a g e

5

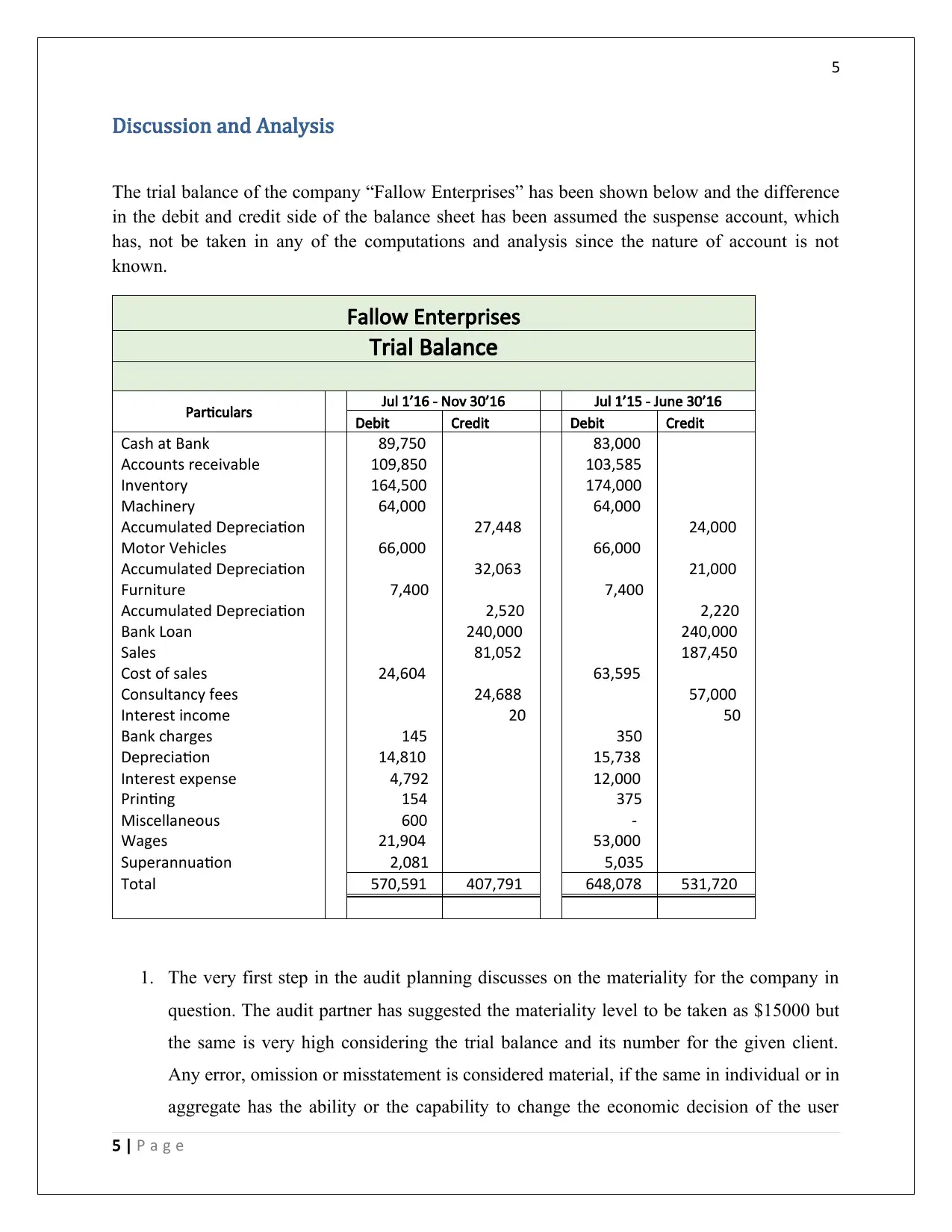

Discussion and Analysis

The trial balance of the company “Fallow Enterprises” has been shown below and the difference

in the debit and credit side of the balance sheet has been assumed the suspense account, which

has, not be taken in any of the computations and analysis since the nature of account is not

known.

Fallow Enterprises

Trial Balance

Particulars Jul 1’16 - Nov 30’16 Jul 1’15 - June 30’16

Debit Credit Debit Credit

Cash at Bank 89,750 83,000

Accounts receivable 109,850 103,585

Inventory 164,500 174,000

Machinery 64,000 64,000

Accumulated Depreciation 27,448 24,000

Motor Vehicles 66,000 66,000

Accumulated Depreciation 32,063 21,000

Furniture 7,400 7,400

Accumulated Depreciation 2,520 2,220

Bank Loan 240,000 240,000

Sales 81,052 187,450

Cost of sales 24,604 63,595

Consultancy fees 24,688 57,000

Interest income 20 50

Bank charges 145 350

Depreciation 14,810 15,738

Interest expense 4,792 12,000

Printing 154 375

Miscellaneous 600 -

Wages 21,904 53,000

Superannuation 2,081 5,035

Total 570,591 407,791 648,078 531,720

1. The very first step in the audit planning discusses on the materiality for the company in

question. The audit partner has suggested the materiality level to be taken as $15000 but

the same is very high considering the trial balance and its number for the given client.

Any error, omission or misstatement is considered material, if the same in individual or in

aggregate has the ability or the capability to change the economic decision of the user

5 | P a g e

Discussion and Analysis

The trial balance of the company “Fallow Enterprises” has been shown below and the difference

in the debit and credit side of the balance sheet has been assumed the suspense account, which

has, not be taken in any of the computations and analysis since the nature of account is not

known.

Fallow Enterprises

Trial Balance

Particulars Jul 1’16 - Nov 30’16 Jul 1’15 - June 30’16

Debit Credit Debit Credit

Cash at Bank 89,750 83,000

Accounts receivable 109,850 103,585

Inventory 164,500 174,000

Machinery 64,000 64,000

Accumulated Depreciation 27,448 24,000

Motor Vehicles 66,000 66,000

Accumulated Depreciation 32,063 21,000

Furniture 7,400 7,400

Accumulated Depreciation 2,520 2,220

Bank Loan 240,000 240,000

Sales 81,052 187,450

Cost of sales 24,604 63,595

Consultancy fees 24,688 57,000

Interest income 20 50

Bank charges 145 350

Depreciation 14,810 15,738

Interest expense 4,792 12,000

Printing 154 375

Miscellaneous 600 -

Wages 21,904 53,000

Superannuation 2,081 5,035

Total 570,591 407,791 648,078 531,720

1. The very first step in the audit planning discusses on the materiality for the company in

question. The audit partner has suggested the materiality level to be taken as $15000 but

the same is very high considering the trial balance and its number for the given client.

Any error, omission or misstatement is considered material, if the same in individual or in

aggregate has the ability or the capability to change the economic decision of the user

5 | P a g e

6

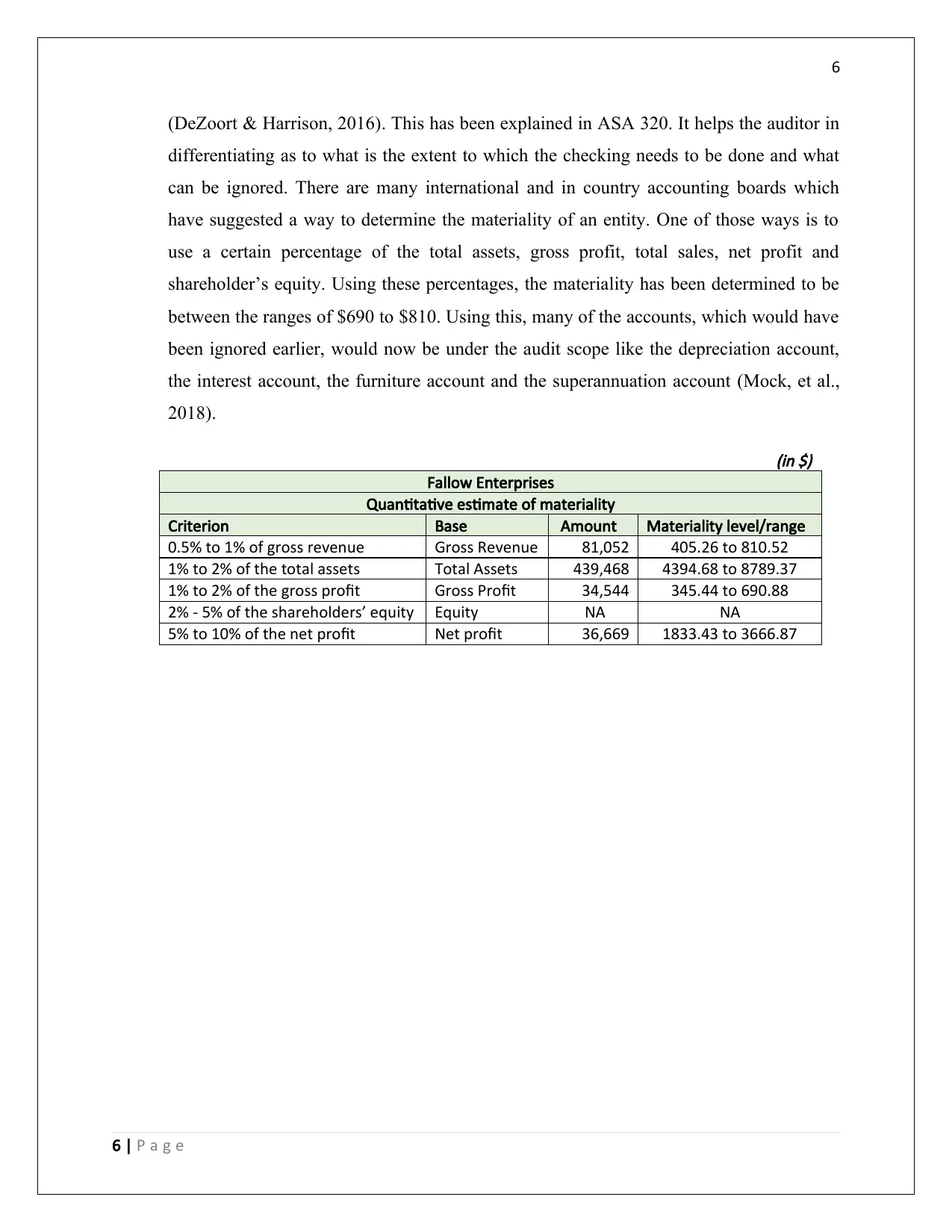

(DeZoort & Harrison, 2016). This has been explained in ASA 320. It helps the auditor in

differentiating as to what is the extent to which the checking needs to be done and what

can be ignored. There are many international and in country accounting boards which

have suggested a way to determine the materiality of an entity. One of those ways is to

use a certain percentage of the total assets, gross profit, total sales, net profit and

shareholder’s equity. Using these percentages, the materiality has been determined to be

between the ranges of $690 to $810. Using this, many of the accounts, which would have

been ignored earlier, would now be under the audit scope like the depreciation account,

the interest account, the furniture account and the superannuation account (Mock, et al.,

2018).

(in $)

Fallow Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 81,052 405.26 to 810.52

1% to 2% of the total assets Total Assets 439,468 4394.68 to 8789.37

1% to 2% of the gross profit Gross Profit 34,544 345.44 to 690.88

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 36,669 1833.43 to 3666.87

6 | P a g e

(DeZoort & Harrison, 2016). This has been explained in ASA 320. It helps the auditor in

differentiating as to what is the extent to which the checking needs to be done and what

can be ignored. There are many international and in country accounting boards which

have suggested a way to determine the materiality of an entity. One of those ways is to

use a certain percentage of the total assets, gross profit, total sales, net profit and

shareholder’s equity. Using these percentages, the materiality has been determined to be

between the ranges of $690 to $810. Using this, many of the accounts, which would have

been ignored earlier, would now be under the audit scope like the depreciation account,

the interest account, the furniture account and the superannuation account (Mock, et al.,

2018).

(in $)

Fallow Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 81,052 405.26 to 810.52

1% to 2% of the total assets Total Assets 439,468 4394.68 to 8789.37

1% to 2% of the gross profit Gross Profit 34,544 345.44 to 690.88

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 36,669 1833.43 to 3666.87

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

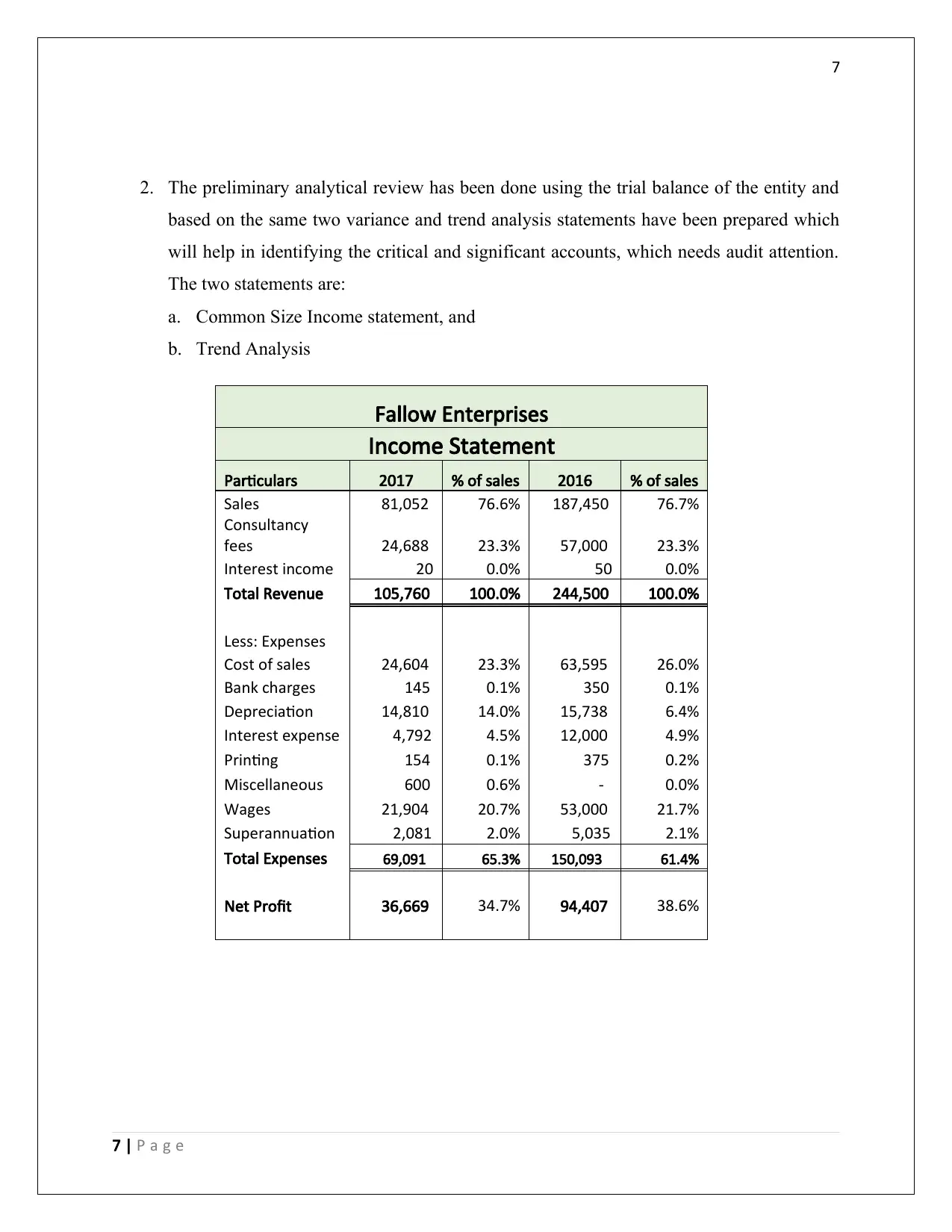

2. The preliminary analytical review has been done using the trial balance of the entity and

based on the same two variance and trend analysis statements have been prepared which

will help in identifying the critical and significant accounts, which needs audit attention.

The two statements are:

a. Common Size Income statement, and

b. Trend Analysis

Fallow Enterprises

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 81,052 76.6% 187,450 76.7%

Consultancy

fees 24,688 23.3% 57,000 23.3%

Interest income 20 0.0% 50 0.0%

Total Revenue 105,760 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 24,604 23.3% 63,595 26.0%

Bank charges 145 0.1% 350 0.1%

Depreciation 14,810 14.0% 15,738 6.4%

Interest expense 4,792 4.5% 12,000 4.9%

Printing 154 0.1% 375 0.2%

Miscellaneous 600 0.6% - 0.0%

Wages 21,904 20.7% 53,000 21.7%

Superannuation 2,081 2.0% 5,035 2.1%

Total Expenses 69,091 65.3% 150,093 61.4%

Net Profit 36,669 34.7% 94,407 38.6%

7 | P a g e

2. The preliminary analytical review has been done using the trial balance of the entity and

based on the same two variance and trend analysis statements have been prepared which

will help in identifying the critical and significant accounts, which needs audit attention.

The two statements are:

a. Common Size Income statement, and

b. Trend Analysis

Fallow Enterprises

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 81,052 76.6% 187,450 76.7%

Consultancy

fees 24,688 23.3% 57,000 23.3%

Interest income 20 0.0% 50 0.0%

Total Revenue 105,760 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 24,604 23.3% 63,595 26.0%

Bank charges 145 0.1% 350 0.1%

Depreciation 14,810 14.0% 15,738 6.4%

Interest expense 4,792 4.5% 12,000 4.9%

Printing 154 0.1% 375 0.2%

Miscellaneous 600 0.6% - 0.0%

Wages 21,904 20.7% 53,000 21.7%

Superannuation 2,081 2.0% 5,035 2.1%

Total Expenses 69,091 65.3% 150,093 61.4%

Net Profit 36,669 34.7% 94,407 38.6%

7 | P a g e

8

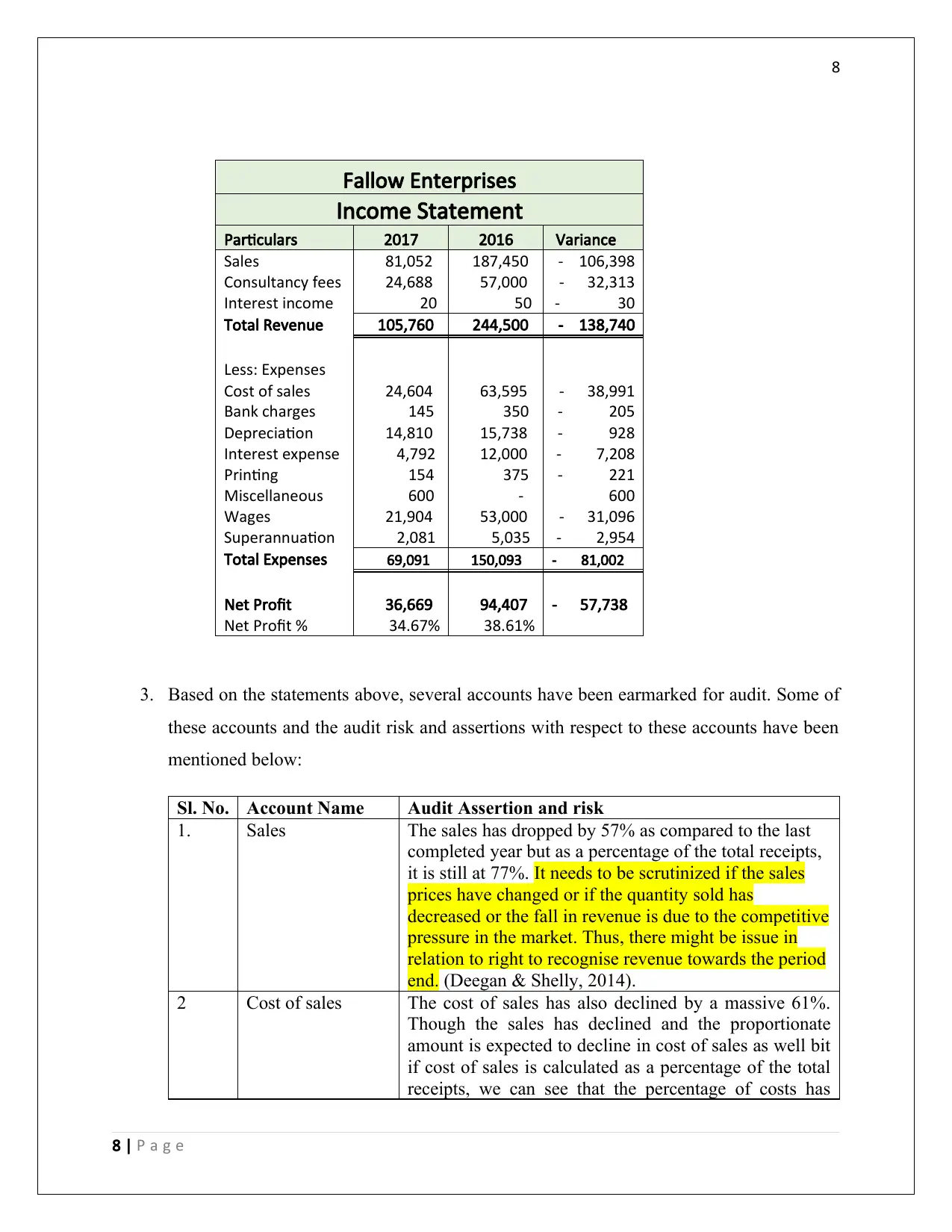

Fallow Enterprises

Income Statement

Particulars 2017 2016 Variance

Sales 81,052 187,450 - 106,398

Consultancy fees 24,688 57,000 - 32,313

Interest income 20 50 - 30

Total Revenue 105,760 244,500 - 138,740

Less: Expenses

Cost of sales 24,604 63,595 - 38,991

Bank charges 145 350 - 205

Depreciation 14,810 15,738 - 928

Interest expense 4,792 12,000 - 7,208

Printing 154 375 - 221

Miscellaneous 600 - 600

Wages 21,904 53,000 - 31,096

Superannuation 2,081 5,035 - 2,954

Total Expenses 69,091 150,093 - 81,002

Net Profit 36,669 94,407 - 57,738

Net Profit % 34.67% 38.61%

3. Based on the statements above, several accounts have been earmarked for audit. Some of

these accounts and the audit risk and assertions with respect to these accounts have been

mentioned below:

Sl. No. Account Name Audit Assertion and risk

1. Sales The sales has dropped by 57% as compared to the last

completed year but as a percentage of the total receipts,

it is still at 77%. It needs to be scrutinized if the sales

prices have changed or if the quantity sold has

decreased or the fall in revenue is due to the competitive

pressure in the market. Thus, there might be issue in

relation to right to recognise revenue towards the period

end. (Deegan & Shelly, 2014).

2 Cost of sales The cost of sales has also declined by a massive 61%.

Though the sales has declined and the proportionate

amount is expected to decline in cost of sales as well bit

if cost of sales is calculated as a percentage of the total

receipts, we can see that the percentage of costs has

8 | P a g e

Fallow Enterprises

Income Statement

Particulars 2017 2016 Variance

Sales 81,052 187,450 - 106,398

Consultancy fees 24,688 57,000 - 32,313

Interest income 20 50 - 30

Total Revenue 105,760 244,500 - 138,740

Less: Expenses

Cost of sales 24,604 63,595 - 38,991

Bank charges 145 350 - 205

Depreciation 14,810 15,738 - 928

Interest expense 4,792 12,000 - 7,208

Printing 154 375 - 221

Miscellaneous 600 - 600

Wages 21,904 53,000 - 31,096

Superannuation 2,081 5,035 - 2,954

Total Expenses 69,091 150,093 - 81,002

Net Profit 36,669 94,407 - 57,738

Net Profit % 34.67% 38.61%

3. Based on the statements above, several accounts have been earmarked for audit. Some of

these accounts and the audit risk and assertions with respect to these accounts have been

mentioned below:

Sl. No. Account Name Audit Assertion and risk

1. Sales The sales has dropped by 57% as compared to the last

completed year but as a percentage of the total receipts,

it is still at 77%. It needs to be scrutinized if the sales

prices have changed or if the quantity sold has

decreased or the fall in revenue is due to the competitive

pressure in the market. Thus, there might be issue in

relation to right to recognise revenue towards the period

end. (Deegan & Shelly, 2014).

2 Cost of sales The cost of sales has also declined by a massive 61%.

Though the sales has declined and the proportionate

amount is expected to decline in cost of sales as well bit

if cost of sales is calculated as a percentage of the total

receipts, we can see that the percentage of costs has

8 | P a g e

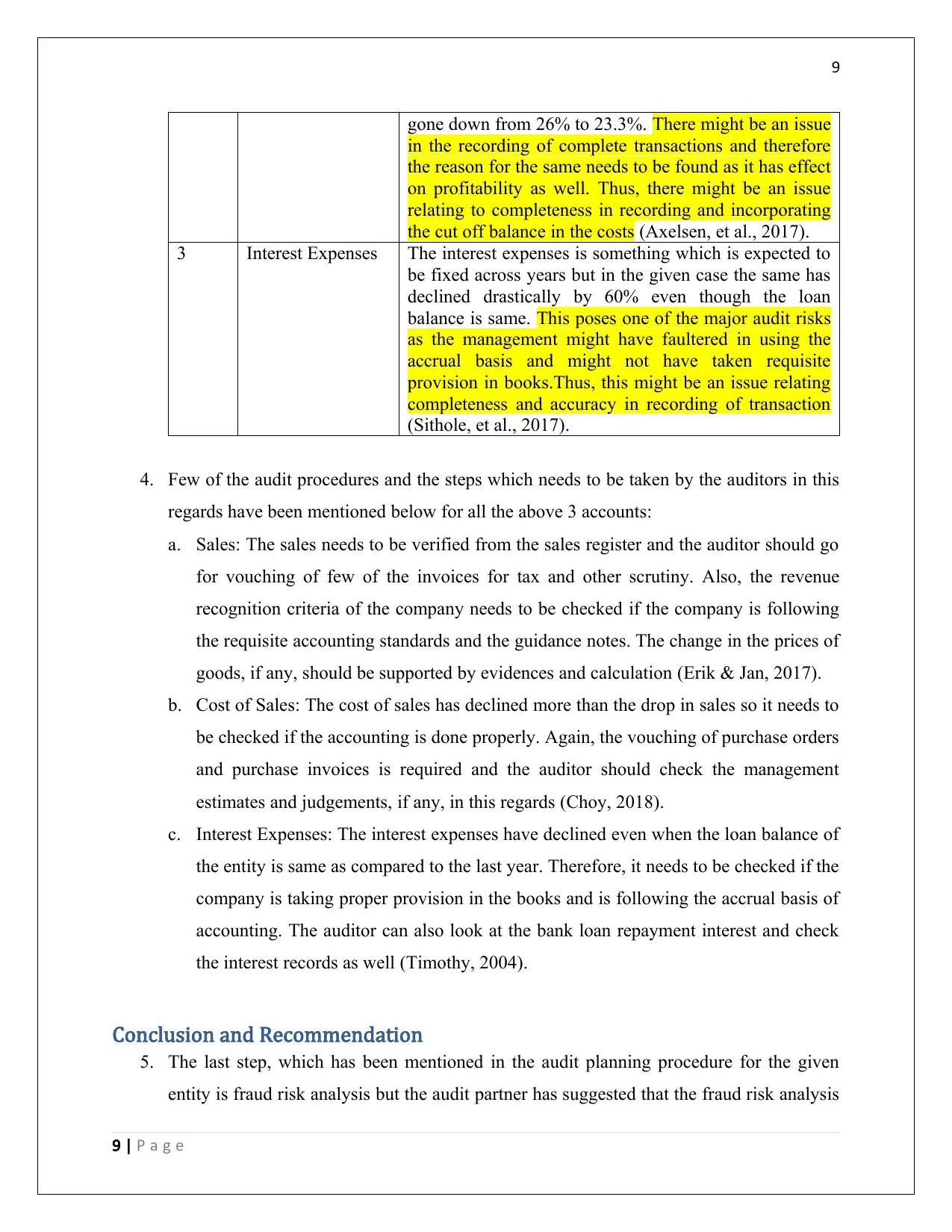

9

gone down from 26% to 23.3%. There might be an issue

in the recording of complete transactions and therefore

the reason for the same needs to be found as it has effect

on profitability as well. Thus, there might be an issue

relating to completeness in recording and incorporating

the cut off balance in the costs (Axelsen, et al., 2017).

3 Interest Expenses The interest expenses is something which is expected to

be fixed across years but in the given case the same has

declined drastically by 60% even though the loan

balance is same. This poses one of the major audit risks

as the management might have faultered in using the

accrual basis and might not have taken requisite

provision in books.Thus, this might be an issue relating

completeness and accuracy in recording of transaction

(Sithole, et al., 2017).

4. Few of the audit procedures and the steps which needs to be taken by the auditors in this

regards have been mentioned below for all the above 3 accounts:

a. Sales: The sales needs to be verified from the sales register and the auditor should go

for vouching of few of the invoices for tax and other scrutiny. Also, the revenue

recognition criteria of the company needs to be checked if the company is following

the requisite accounting standards and the guidance notes. The change in the prices of

goods, if any, should be supported by evidences and calculation (Erik & Jan, 2017).

b. Cost of Sales: The cost of sales has declined more than the drop in sales so it needs to

be checked if the accounting is done properly. Again, the vouching of purchase orders

and purchase invoices is required and the auditor should check the management

estimates and judgements, if any, in this regards (Choy, 2018).

c. Interest Expenses: The interest expenses have declined even when the loan balance of

the entity is same as compared to the last year. Therefore, it needs to be checked if the

company is taking proper provision in the books and is following the accrual basis of

accounting. The auditor can also look at the bank loan repayment interest and check

the interest records as well (Timothy, 2004).

Conclusion and Recommendation

5. The last step, which has been mentioned in the audit planning procedure for the given

entity is fraud risk analysis but the audit partner has suggested that the fraud risk analysis

9 | P a g e

gone down from 26% to 23.3%. There might be an issue

in the recording of complete transactions and therefore

the reason for the same needs to be found as it has effect

on profitability as well. Thus, there might be an issue

relating to completeness in recording and incorporating

the cut off balance in the costs (Axelsen, et al., 2017).

3 Interest Expenses The interest expenses is something which is expected to

be fixed across years but in the given case the same has

declined drastically by 60% even though the loan

balance is same. This poses one of the major audit risks

as the management might have faultered in using the

accrual basis and might not have taken requisite

provision in books.Thus, this might be an issue relating

completeness and accuracy in recording of transaction

(Sithole, et al., 2017).

4. Few of the audit procedures and the steps which needs to be taken by the auditors in this

regards have been mentioned below for all the above 3 accounts:

a. Sales: The sales needs to be verified from the sales register and the auditor should go

for vouching of few of the invoices for tax and other scrutiny. Also, the revenue

recognition criteria of the company needs to be checked if the company is following

the requisite accounting standards and the guidance notes. The change in the prices of

goods, if any, should be supported by evidences and calculation (Erik & Jan, 2017).

b. Cost of Sales: The cost of sales has declined more than the drop in sales so it needs to

be checked if the accounting is done properly. Again, the vouching of purchase orders

and purchase invoices is required and the auditor should check the management

estimates and judgements, if any, in this regards (Choy, 2018).

c. Interest Expenses: The interest expenses have declined even when the loan balance of

the entity is same as compared to the last year. Therefore, it needs to be checked if the

company is taking proper provision in the books and is following the accrual basis of

accounting. The auditor can also look at the bank loan repayment interest and check

the interest records as well (Timothy, 2004).

Conclusion and Recommendation

5. The last step, which has been mentioned in the audit planning procedure for the given

entity is fraud risk analysis but the audit partner has suggested that the fraud risk analysis

9 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

need not be carried out for the entity as the client, is a trustworthy one. Here, the audit

partner is wrong in his contention for the reason that the auditor should always maintain

the professional scepticism while auditing the accounts and should exercise his

professional judgement all throughout (Fukukawa & Mock, 2011). In addition, it has

been mentioned in APES 110 that the auditors should subject all the clients to fraud risk

analysis irrespective of what is the situation. Here also in the given case, there have been

certain cases and accounts where there can be a possibility of the fraud. Some of these

accounts are interest expenses account and cost of sales account for which the reasons

have already been explained above. In addition to this, the depreciation account also

needs to be checked as the balances of assets is same as per last year but the expenses

have gone down. Furthermore, the drop in superannuation expenses show that the

employees have left the company and the current head count should be less as compared

to the last year. The same should be checked and verified (Bumgarner & Vasarhelyi,

2018).

References

Axelsen, M., Green, P. & Ridley, G., 2017. Explaining the information systems auditor role in the public

sector financial audit.

International Journal of Accounting Information Systems, 24(1), pp. 15-31.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view..

Continuous Auditing: Theory

and Application, 20(1), pp. 7-51.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.Ecological Economics, p. 145.

Deegan, C. & Shelly, M., 2014. Corporate Social Responsibilities: Alternative Perspectives About the

Need to Legislate.

Springer, 121(1), pp. 499-526.

DeZoort, F. & Harrison, P., 2016. Understanding Auditors sense of Responsibility for detecting fraud

within organization.

Journal of Business Ethics, pp. 1-18.

Erik, H. & Jan, B., 2017. Supply chain management and activity-based costing: Current status and

directions for the future.

International Journal of Physical Distribution & Logistics Management, 47(8),

pp. 712-735.

10 | P a g e

need not be carried out for the entity as the client, is a trustworthy one. Here, the audit

partner is wrong in his contention for the reason that the auditor should always maintain

the professional scepticism while auditing the accounts and should exercise his

professional judgement all throughout (Fukukawa & Mock, 2011). In addition, it has

been mentioned in APES 110 that the auditors should subject all the clients to fraud risk

analysis irrespective of what is the situation. Here also in the given case, there have been

certain cases and accounts where there can be a possibility of the fraud. Some of these

accounts are interest expenses account and cost of sales account for which the reasons

have already been explained above. In addition to this, the depreciation account also

needs to be checked as the balances of assets is same as per last year but the expenses

have gone down. Furthermore, the drop in superannuation expenses show that the

employees have left the company and the current head count should be less as compared

to the last year. The same should be checked and verified (Bumgarner & Vasarhelyi,

2018).

References

Axelsen, M., Green, P. & Ridley, G., 2017. Explaining the information systems auditor role in the public

sector financial audit.

International Journal of Accounting Information Systems, 24(1), pp. 15-31.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view..

Continuous Auditing: Theory

and Application, 20(1), pp. 7-51.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.Ecological Economics, p. 145.

Deegan, C. & Shelly, M., 2014. Corporate Social Responsibilities: Alternative Perspectives About the

Need to Legislate.

Springer, 121(1), pp. 499-526.

DeZoort, F. & Harrison, P., 2016. Understanding Auditors sense of Responsibility for detecting fraud

within organization.

Journal of Business Ethics, pp. 1-18.

Erik, H. & Jan, B., 2017. Supply chain management and activity-based costing: Current status and

directions for the future.

International Journal of Physical Distribution & Logistics Management, 47(8),

pp. 712-735.

10 | P a g e

11

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability.

Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Marques, R. P. F., 2018. Continuous Assurance and the Use of Technology for Business Compliance.Encyclopedia of Information Science and Technology, pp. 820-830.

Mock, T. J., Ragothaman, S. C. & Srivastava, R. P., 2018. Using Evidential Reasoning Technology to

Enhance the Audit Quality Assurance Inspection Process.

Journal of Emerging Technologies in

Accounting, 15(1), pp. 29-43.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting.

Journal of Educational Psychology, 109(2), p. 220.

Timothy, G., 2004. Managing interest rate risk in a rising rate environment.

RMA Journal, Risk

Management Association (RMA), November.

11 | P a g e

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability.

Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Marques, R. P. F., 2018. Continuous Assurance and the Use of Technology for Business Compliance.Encyclopedia of Information Science and Technology, pp. 820-830.

Mock, T. J., Ragothaman, S. C. & Srivastava, R. P., 2018. Using Evidential Reasoning Technology to

Enhance the Audit Quality Assurance Inspection Process.

Journal of Emerging Technologies in

Accounting, 15(1), pp. 29-43.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting.

Journal of Educational Psychology, 109(2), p. 220.

Timothy, G., 2004. Managing interest rate risk in a rising rate environment.

RMA Journal, Risk

Management Association (RMA), November.

11 | P a g e

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.