BAO3306 - Auditing: Financial Audit Planning for Monash IVF Group

VerifiedAdded on 2023/06/05

|19

|4235

|270

Report

AI Summary

This report provides a comprehensive audit planning and risk assessment for Monash IVF Group, focusing on the identification of significant accounts and the evaluation of potential risks. It begins with an introduction to Monash IVF Group, highlighting its core business and competitive landscape. The report identifies five significant accounts—intangible assets, borrowings, contingent considerations, revenue, and income tax—and explains the rationale for their detailed assessment. Analytical procedures, including ratio analysis, are applied to assess the risk of going concern and understand key areas requiring in-depth analysis. The report also discusses the concept of materiality, its importance in auditing, and the calculation of the materiality limit for Monash IVF Group, using the revenue method. Finally, it provides a detailed audit risk assessment for each of the selected significant accounts, emphasizing potential misstatements and areas requiring further investigation. Desklib offers a wide range of solved assignments and past papers to support students in their studies.

BAO3306 Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive summary.........................................................................................................................3

Introduction......................................................................................................................................4

Key information...............................................................................................................................4

Understanding of client................................................................................................................4

Identification of the five significant accounts.............................................................................5

Planning materiality level............................................................................................................6

Identification of the audit risk assessment of the selected 5 significant accounts.......................8

Conclusion.....................................................................................................................................13

Appendices....................................................................................................................................14

References......................................................................................................................................17

Executive summary.........................................................................................................................3

Introduction......................................................................................................................................4

Key information...............................................................................................................................4

Understanding of client................................................................................................................4

Identification of the five significant accounts.............................................................................5

Planning materiality level............................................................................................................6

Identification of the audit risk assessment of the selected 5 significant accounts.......................8

Conclusion.....................................................................................................................................13

Appendices....................................................................................................................................14

References......................................................................................................................................17

EXECUTIVE SUMMARY

Audit planning is referred to as the most crucial area of the entire audit that is performed at the

beginning of the audit process in order to make sure that suitable consideration is provided to the

most significant areas. The main objective behind the same is the prompt identification of

possible problems so that the whole audit procedure can be conducted in a coordinated and

expeditious manner. The present report is based on providing full and meaningful audit aspects

with the proper identification of potential risks and assessment of the same. Further, the report

covers the insights of the Monash IVF Group to reach the identification of the main five accounts

inclusive of audit assessment risks and processes relating to same. Along with this, the Monash

IVF Group’s performance and progress will be analyzed through the analytical procedure, which

will help in facilitating calculations and to reach the objective of the study that is to help the

client in conducting audit planning and preparing audit reports effectively.

Audit planning is referred to as the most crucial area of the entire audit that is performed at the

beginning of the audit process in order to make sure that suitable consideration is provided to the

most significant areas. The main objective behind the same is the prompt identification of

possible problems so that the whole audit procedure can be conducted in a coordinated and

expeditious manner. The present report is based on providing full and meaningful audit aspects

with the proper identification of potential risks and assessment of the same. Further, the report

covers the insights of the Monash IVF Group to reach the identification of the main five accounts

inclusive of audit assessment risks and processes relating to same. Along with this, the Monash

IVF Group’s performance and progress will be analyzed through the analytical procedure, which

will help in facilitating calculations and to reach the objective of the study that is to help the

client in conducting audit planning and preparing audit reports effectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The prevailing study aims to support the auditors in making effective decisions in auditing and

offering them the appropriate and justifiable information regarding the financial performance and

needs of clients. It concentrates on those improvement areas that are required to be handled in

depth. The concerned auditing planning process will make a contribution by establishing

significant accounts that are most expected to possess materialistic misstatement risks, along

with the audit risks assessments. The entire study and audit plan will be based in accordance with

the ASA 300 Planning an Audit of a Financial Report, plus full consideration will be given

towards ethical standards and auditor professionalism and client satisfaction.

KEY INFORMATION

Understanding of client

Monash IVF Group Limited is based in Australia and Malaysia engaged in offering assistive

reproductive and professional women services. It offers quality services such as tertiary level

prenatal diagnostic, fertility research, diagnostic ultrasound and low intervention IVF

respectively. The company was established in 2014 and now is a key leader in the in the Assisted

Reproductive Services provisions in the based countries (Monash IVF Group, 2018).

Richard has been engaged in working for InvoCare for twenty years till 2018. For most of the

time, the position of CEO belonged to him and management of the business growth was in his

hand via a number of ownership changes and more than 200 acquisitions, inclusive of offshore

within Singapore (Monash IVF Group, 2018). On the other hand, the joining of Mr James

Thiedeman in the Group was in the year 2009, 25 years have been spent by James in working

with the company healthcare department in public as well as private sector. Finding a new CEO

as well as a managing director for the Group can be a challenging task, and it is anticipated that

the company shall make an announcement regarding the same in upcoming months.

With the experience of 40 years, the Group has developed into professional fertility as well as

women’s imaging group and gained a global identification for scientific and innovative purposes.

The Group is a driver in the development force of assisted reproductive technologies; they are

The prevailing study aims to support the auditors in making effective decisions in auditing and

offering them the appropriate and justifiable information regarding the financial performance and

needs of clients. It concentrates on those improvement areas that are required to be handled in

depth. The concerned auditing planning process will make a contribution by establishing

significant accounts that are most expected to possess materialistic misstatement risks, along

with the audit risks assessments. The entire study and audit plan will be based in accordance with

the ASA 300 Planning an Audit of a Financial Report, plus full consideration will be given

towards ethical standards and auditor professionalism and client satisfaction.

KEY INFORMATION

Understanding of client

Monash IVF Group Limited is based in Australia and Malaysia engaged in offering assistive

reproductive and professional women services. It offers quality services such as tertiary level

prenatal diagnostic, fertility research, diagnostic ultrasound and low intervention IVF

respectively. The company was established in 2014 and now is a key leader in the in the Assisted

Reproductive Services provisions in the based countries (Monash IVF Group, 2018).

Richard has been engaged in working for InvoCare for twenty years till 2018. For most of the

time, the position of CEO belonged to him and management of the business growth was in his

hand via a number of ownership changes and more than 200 acquisitions, inclusive of offshore

within Singapore (Monash IVF Group, 2018). On the other hand, the joining of Mr James

Thiedeman in the Group was in the year 2009, 25 years have been spent by James in working

with the company healthcare department in public as well as private sector. Finding a new CEO

as well as a managing director for the Group can be a challenging task, and it is anticipated that

the company shall make an announcement regarding the same in upcoming months.

With the experience of 40 years, the Group has developed into professional fertility as well as

women’s imaging group and gained a global identification for scientific and innovative purposes.

The Group is a driver in the development force of assisted reproductive technologies; they are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

involved in offering a variety of treatments and services with the goal to provide the utmost care

to the patient (AnnualReports.com, 2018). Their services are served in a specialized and caring

manner, with the help of the specialized team, scientists, nurses, doctors and the leading pursuits

in this field.

The Monash IVF Group has positioned considerable significance on the collaboration based in

operations, science and clinics. Further, this collaboration generally takes place in a formal

manner in their medical advisory committee, and research meetings, wherein the scientists and

professionals consider the success rates and make discussion on the insights based on new

treatments and emerging opportunities related with the research and any other mutual projects

(Bloomberg, 2018).

Competitors of company

The major competitor of Monash IVF Group is the provider of the reproductive treatment and

services which is Virtus Health, and it is an ASX listed leading company

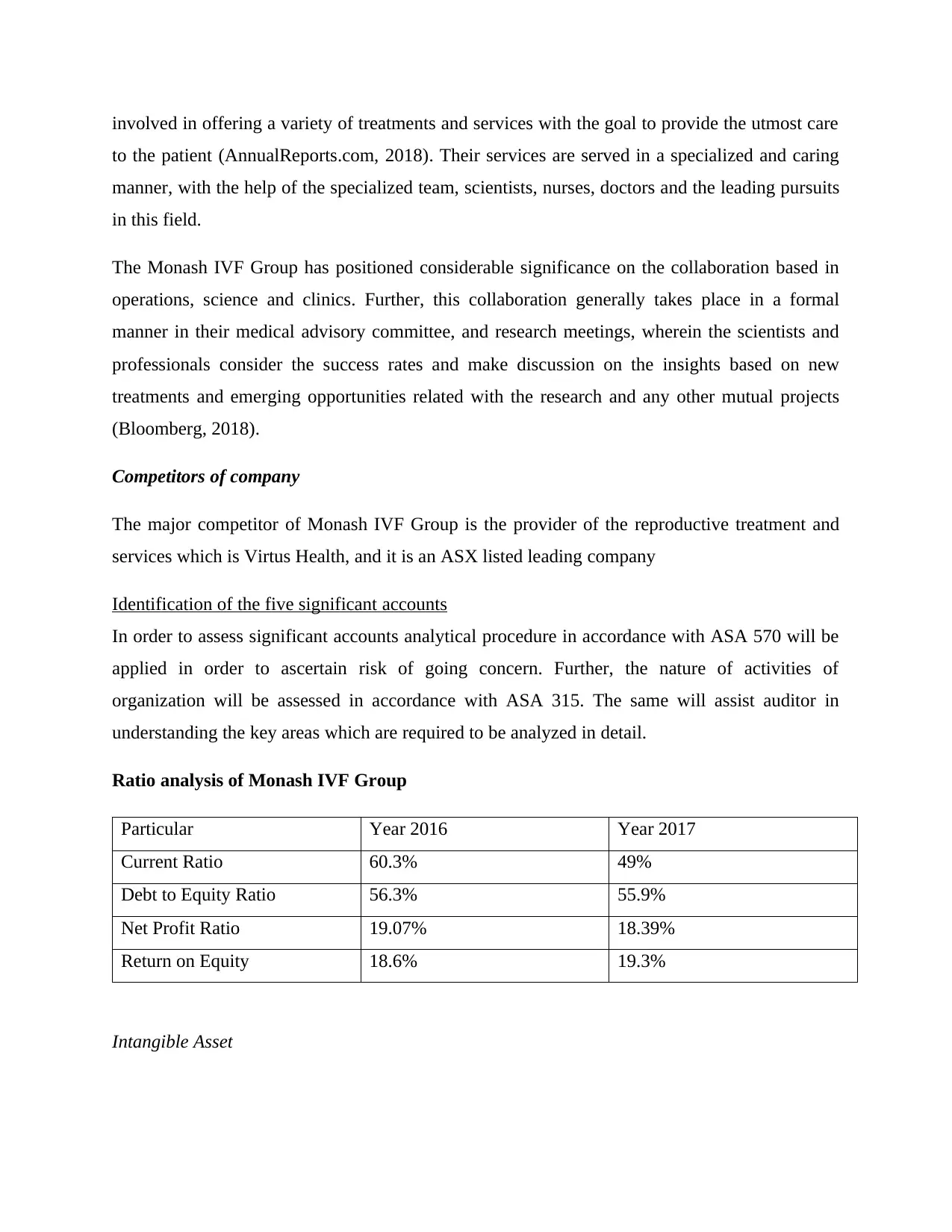

Identification of the five significant accounts

In order to assess significant accounts analytical procedure in accordance with ASA 570 will be

applied in order to ascertain risk of going concern. Further, the nature of activities of

organization will be assessed in accordance with ASA 315. The same will assist auditor in

understanding the key areas which are required to be analyzed in detail.

Ratio analysis of Monash IVF Group

Particular Year 2016 Year 2017

Current Ratio 60.3% 49%

Debt to Equity Ratio 56.3% 55.9%

Net Profit Ratio 19.07% 18.39%

Return on Equity 18.6% 19.3%

Intangible Asset

to the patient (AnnualReports.com, 2018). Their services are served in a specialized and caring

manner, with the help of the specialized team, scientists, nurses, doctors and the leading pursuits

in this field.

The Monash IVF Group has positioned considerable significance on the collaboration based in

operations, science and clinics. Further, this collaboration generally takes place in a formal

manner in their medical advisory committee, and research meetings, wherein the scientists and

professionals consider the success rates and make discussion on the insights based on new

treatments and emerging opportunities related with the research and any other mutual projects

(Bloomberg, 2018).

Competitors of company

The major competitor of Monash IVF Group is the provider of the reproductive treatment and

services which is Virtus Health, and it is an ASX listed leading company

Identification of the five significant accounts

In order to assess significant accounts analytical procedure in accordance with ASA 570 will be

applied in order to ascertain risk of going concern. Further, the nature of activities of

organization will be assessed in accordance with ASA 315. The same will assist auditor in

understanding the key areas which are required to be analyzed in detail.

Ratio analysis of Monash IVF Group

Particular Year 2016 Year 2017

Current Ratio 60.3% 49%

Debt to Equity Ratio 56.3% 55.9%

Net Profit Ratio 19.07% 18.39%

Return on Equity 18.6% 19.3%

Intangible Asset

Intangible asset comprises goodwill, software, trademark and others. In the year 2017, an

addition of $134000 has been done in software through acquisition and $3823000 through

business combinations. The company recognizes impairment loss relating to intangible asset in

case carrying the amount of an asset or CGU is more than its recoverable value. Further, the loss

is reversed only to the extent to which the carrying amount of asset does not exceed net carrying

amount in case no impairment loss has been accounted in books of accounts.

Borrowings

The company follows the policy of recognizing loan and borrowing at fair value of the

consideration which is amount received reduced by transaction cost. Further the same are

amortized by application of effective interest method. Loans and borrowing are considered as

non-current liability only in case same can be deferred for a period of twelve months or more.

Current Borrowings of Monash IVF Group comprises derivates and capitalised finance facility

fees. In order to provide that whether classification of current and non-current liabilities have

been appropriately or not both of these accounts required to be assessed in detail.

Contingent considerations

The financial report of the company has been conducted on the basis of accrual and is totally

related on the historical costs (unless and until it is mentioned specifically) exclusive of the

derivative financial instruments and the assumption of the contingent consideration in the

business combination, that is done on fair value measurement. The fair value gaining or loss held

on the contingent consideration is categorized as a financial liability (Chen and et al., 2015). The

contingent consideration was accounted at 150 in the year 2017, which is lower than the previous

year which was 500 in 2016, indicating that contingent payment is a further consideration

(Griffiths, 2016).

Revenue

Monash IVF Group has performed effectively in revenues in FY17, regardless of this fact there

is a reduction in the revenues in the patient treatment and their related revenues. In addition, the

net profit after tax rises by 2.9% or $0.8m to $29.6million in opposition to the past year.

Furthermore, the revenues of Group were declined by 0.9% at $155.2m for the year-end (Chan

addition of $134000 has been done in software through acquisition and $3823000 through

business combinations. The company recognizes impairment loss relating to intangible asset in

case carrying the amount of an asset or CGU is more than its recoverable value. Further, the loss

is reversed only to the extent to which the carrying amount of asset does not exceed net carrying

amount in case no impairment loss has been accounted in books of accounts.

Borrowings

The company follows the policy of recognizing loan and borrowing at fair value of the

consideration which is amount received reduced by transaction cost. Further the same are

amortized by application of effective interest method. Loans and borrowing are considered as

non-current liability only in case same can be deferred for a period of twelve months or more.

Current Borrowings of Monash IVF Group comprises derivates and capitalised finance facility

fees. In order to provide that whether classification of current and non-current liabilities have

been appropriately or not both of these accounts required to be assessed in detail.

Contingent considerations

The financial report of the company has been conducted on the basis of accrual and is totally

related on the historical costs (unless and until it is mentioned specifically) exclusive of the

derivative financial instruments and the assumption of the contingent consideration in the

business combination, that is done on fair value measurement. The fair value gaining or loss held

on the contingent consideration is categorized as a financial liability (Chen and et al., 2015). The

contingent consideration was accounted at 150 in the year 2017, which is lower than the previous

year which was 500 in 2016, indicating that contingent payment is a further consideration

(Griffiths, 2016).

Revenue

Monash IVF Group has performed effectively in revenues in FY17, regardless of this fact there

is a reduction in the revenues in the patient treatment and their related revenues. In addition, the

net profit after tax rises by 2.9% or $0.8m to $29.6million in opposition to the past year.

Furthermore, the revenues of Group were declined by 0.9% at $155.2m for the year-end (Chan

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and Vasarhelyi, 2018). The revenues down by $1.4m by 0.9% to $155.2 million in comparison to

FY16 Revenue which is gauged at fair value measurement of the concern received or receivable.

Income tax

The income tax was reported at $20.1m in the financial year 2017; the income tax expense

includes existing as well as deferred tax. The income tax is held in profit or loss, exclusive of an

extent that it is related with the business combination or to the aspects realized in equity in a

direct manner. Although, the Group is subjected to income tax within Australia as well as its

jurisdiction where it is conducting is foreign operations. Judgement is needed while identifying

the global provision meant for income taxes and while considering if or if not deferred tax

balances is realized on the financial position statements. Also, the changes held in the events will

make modification in expectations, which might affect the extent of provision for the

recognizable income taxes and deferred tax balances (Louwers and et al., 2015).

FY16 Revenue which is gauged at fair value measurement of the concern received or receivable.

Income tax

The income tax was reported at $20.1m in the financial year 2017; the income tax expense

includes existing as well as deferred tax. The income tax is held in profit or loss, exclusive of an

extent that it is related with the business combination or to the aspects realized in equity in a

direct manner. Although, the Group is subjected to income tax within Australia as well as its

jurisdiction where it is conducting is foreign operations. Judgement is needed while identifying

the global provision meant for income taxes and while considering if or if not deferred tax

balances is realized on the financial position statements. Also, the changes held in the events will

make modification in expectations, which might affect the extent of provision for the

recognizable income taxes and deferred tax balances (Louwers and et al., 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Planning materiality level

The core concept of materiality

Materiality is known as, in regards to the information, that the information that is misstated, non-

disclosed or omitted to have the chances to adversely impact the decisions regarding the scares

resources allocation by the financial report users or the discharging of the responsibility by the

Group’s managerial authority and the enterprise’s governing and regulatory bodies.

Specification available in auditing standard of Australia as well as International Standards of

Auditing relating to materiality

The materiality is the prime aspect when it comes to financial reporting, instead of auditing

theory. Although it is not mentioned under ISA 320 Materiality in planning and performing an

audit but some core characteristics have been highlighted by the ISA regarding the same which

are; misstatements are stated to be material if they can impact the financial statement users

(Lakis and Masiulevičius, 2017). The judgement regarding the materiality is based on the

environmental events, inclusive of the nature and extent of the misstatements. It has also been

stated that the judgement is conducted on the basis of the common requirements of the users as a

group. By considering this aspect, compulsory requirements have been established by the

Auditing Standard ASA 320 Materiality and Audit Adjustments to offer descriptive guidance on

the materiality and related relationship on the audit risk. By considering and planning for the

materiality level of the Monash IVF Group, the auditor might assess the materiality and related

relationship on the audit risk in full.

Materiality as mentioned under Accounting Standard AASB 1031 Materiality, possess a

significant role in making decisions which the preparation and representation of financial reports

are done by the business entities. This auditing standard states the materiality role in terms of

audit planning and in the evaluation of the audit evidence (Baldauf, Steller and Steckel, 2015).

The materiality decision of the auditor is considered as a multi-factor engaging quantitative as

well as qualitative terms.

By considering the financial reports of the Group and its performance, it can be cited that the

most appropriate method to assess the risk of material misstatement for the auditor is to evaluate

The core concept of materiality

Materiality is known as, in regards to the information, that the information that is misstated, non-

disclosed or omitted to have the chances to adversely impact the decisions regarding the scares

resources allocation by the financial report users or the discharging of the responsibility by the

Group’s managerial authority and the enterprise’s governing and regulatory bodies.

Specification available in auditing standard of Australia as well as International Standards of

Auditing relating to materiality

The materiality is the prime aspect when it comes to financial reporting, instead of auditing

theory. Although it is not mentioned under ISA 320 Materiality in planning and performing an

audit but some core characteristics have been highlighted by the ISA regarding the same which

are; misstatements are stated to be material if they can impact the financial statement users

(Lakis and Masiulevičius, 2017). The judgement regarding the materiality is based on the

environmental events, inclusive of the nature and extent of the misstatements. It has also been

stated that the judgement is conducted on the basis of the common requirements of the users as a

group. By considering this aspect, compulsory requirements have been established by the

Auditing Standard ASA 320 Materiality and Audit Adjustments to offer descriptive guidance on

the materiality and related relationship on the audit risk. By considering and planning for the

materiality level of the Monash IVF Group, the auditor might assess the materiality and related

relationship on the audit risk in full.

Materiality as mentioned under Accounting Standard AASB 1031 Materiality, possess a

significant role in making decisions which the preparation and representation of financial reports

are done by the business entities. This auditing standard states the materiality role in terms of

audit planning and in the evaluation of the audit evidence (Baldauf, Steller and Steckel, 2015).

The materiality decision of the auditor is considered as a multi-factor engaging quantitative as

well as qualitative terms.

By considering the financial reports of the Group and its performance, it can be cited that the

most appropriate method to assess the risk of material misstatement for the auditor is to evaluate

the historical financial statements and the perspective and judgements of the auditor. Thus, the

assessment of the historic statements might permit the auditor to make a perfect judgment by

which the financial statements can do material misstatements while assisting the auditor in

setting a threshold for examining the potential misstatements (Graham, Bedard and Dutta, 2018).

Hence, the threshold can be implemented by the auditors of the Group in determining the risk

acceptance level or less materiality threshold held for auditors.

Calculation of Materiality limit

The calculation of the Group’s materiality amounts will be derived by making use of the

quantitative approaches that might be increased or reduced on the basis of the professional

judgement of the auditor regarding the potential impacts of the qualitative factors, for example,

risk of gaining manipulations, potential impacts of the misstatements of the patterns, limited debt

covenants, expanding impact of misstatement for the manipulation of share prices, possible

effects of the misstatements held in the segments based information, fraud detection or signs in

historic period, misstatements regarding achievement of project earnings, validity and reliability

of accounting systems(Eilifsen and Messier Jr, 2014). In the present case of Monash IVF Group

Ltd. revenue method has been applied in order to compute the level of materiality. Thus the

materiality level is .5% of total revenue.

Total revenue for the year 2017 is $155182000

Material level =$155182000*.2%

= $310364

Thus, the transaction which is individually or accumulated above the specified materiality limit

is required to be analyzed in detail in order to provide an opinion relating to the existence of a

risk of material misstatement in books of Monash IVF Group Ltd.

Identification of the audit risk assessment of the selected 5 significant accounts

Intangible Asset

Reason due to which specified account require detail assessment

assessment of the historic statements might permit the auditor to make a perfect judgment by

which the financial statements can do material misstatements while assisting the auditor in

setting a threshold for examining the potential misstatements (Graham, Bedard and Dutta, 2018).

Hence, the threshold can be implemented by the auditors of the Group in determining the risk

acceptance level or less materiality threshold held for auditors.

Calculation of Materiality limit

The calculation of the Group’s materiality amounts will be derived by making use of the

quantitative approaches that might be increased or reduced on the basis of the professional

judgement of the auditor regarding the potential impacts of the qualitative factors, for example,

risk of gaining manipulations, potential impacts of the misstatements of the patterns, limited debt

covenants, expanding impact of misstatement for the manipulation of share prices, possible

effects of the misstatements held in the segments based information, fraud detection or signs in

historic period, misstatements regarding achievement of project earnings, validity and reliability

of accounting systems(Eilifsen and Messier Jr, 2014). In the present case of Monash IVF Group

Ltd. revenue method has been applied in order to compute the level of materiality. Thus the

materiality level is .5% of total revenue.

Total revenue for the year 2017 is $155182000

Material level =$155182000*.2%

= $310364

Thus, the transaction which is individually or accumulated above the specified materiality limit

is required to be analyzed in detail in order to provide an opinion relating to the existence of a

risk of material misstatement in books of Monash IVF Group Ltd.

Identification of the audit risk assessment of the selected 5 significant accounts

Intangible Asset

Reason due to which specified account require detail assessment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The intangible asset of Monash IVF Group Ltd comprises a significant part of the total asset, i.e.

$254688000 approximately 90% of the total asset. Thus, it is covered under to material level

applied in order to assess the risk of materiality. An intangible asset is believed as a crucial part

of a financial asset as the same required to be assessed with more concern and effectiveness in

comparison to other accounts. Moreover, as in the present case, it covers a major portion of the

total asset. Thus a detailed analysis is mandatorily required to assert opinion of the risk of

material misstatement.

Significant Assertion

The key assertion required in the present case is relating to valuation and amortization policies

followed by the company. As amortization of same is a tax-deductible expenditure thus, it is

necessary to assess that whether a specific provision of AASB 138 Intangible asset has been

followed or not.

Steps to be followed for Auditing

Initially, a schedule of al intangible asset should be developed and compared with

previous year balance in order to ascertain the changes.

Accounting entries relating to amortization should be analysed in detail in order to assess

whether amortization has been done in accordance with provision specified in AASB 138

‘Intangibles Asset’ or not.

The analytical procedure should be carried down in order to ascertain whether an

intangible asset is valued at fair market value or not.

Borrowing

Reason due to which specified account require detail assessment

A significant change in current borrowing of Monash IVF group Ltd have been assessed as same

were having a positive balance of $453000 at the end of year 2016 and same have been turned to

$-116000 at the end of year 2017. The reason behind same is that derivates which were available

previous year are now no available. The derivative financial instruments which have been held

by the group are hedged with floating interest exposure rate. Company follows the procedure to

recognize them at fair value along with considering transaction cost which is recognized in profit

$254688000 approximately 90% of the total asset. Thus, it is covered under to material level

applied in order to assess the risk of materiality. An intangible asset is believed as a crucial part

of a financial asset as the same required to be assessed with more concern and effectiveness in

comparison to other accounts. Moreover, as in the present case, it covers a major portion of the

total asset. Thus a detailed analysis is mandatorily required to assert opinion of the risk of

material misstatement.

Significant Assertion

The key assertion required in the present case is relating to valuation and amortization policies

followed by the company. As amortization of same is a tax-deductible expenditure thus, it is

necessary to assess that whether a specific provision of AASB 138 Intangible asset has been

followed or not.

Steps to be followed for Auditing

Initially, a schedule of al intangible asset should be developed and compared with

previous year balance in order to ascertain the changes.

Accounting entries relating to amortization should be analysed in detail in order to assess

whether amortization has been done in accordance with provision specified in AASB 138

‘Intangibles Asset’ or not.

The analytical procedure should be carried down in order to ascertain whether an

intangible asset is valued at fair market value or not.

Borrowing

Reason due to which specified account require detail assessment

A significant change in current borrowing of Monash IVF group Ltd have been assessed as same

were having a positive balance of $453000 at the end of year 2016 and same have been turned to

$-116000 at the end of year 2017. The reason behind same is that derivates which were available

previous year are now no available. The derivative financial instruments which have been held

by the group are hedged with floating interest exposure rate. Company follows the procedure to

recognize them at fair value along with considering transaction cost which is recognized in profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and loss while it has been incurred. Thus, all these transaction require detail analysis to provide

specific appropriate opinion. Hence same has been considered significant account.

Significant Assertion

Appropriate recognition and valuation are the two key assertions required to be ascertained.

Procedure of Auditing

The audit procedure should be initiated by assessing the method of valuation of

derivatives

Moreover, emphasis should be made on reasonableness on management evaluation of the

fair value of other assets, liabilities along with borrowings.

The efficient substantive procedure should be applied to assess the availability of material

risk.

Finally, compliance provision of ASA 520 ‘Analytical procedures’ should be applied in

order to assess the viability of accounting treatment applied for recognition of

borrowings.

Contingent considerations

Reason due to which specified account require detail assessment

A significant decrease in account balance of contingent consideration has been assessed, i.e.

from $500000 to $150000 (Annual report of Monash IVF Group, 2017). Thus, the reason behind

is required to be assessed in detail. It might be possible that a part of revenue might be

recognized as contingent consideration and same will eventually lead to a present unfair position

of books of accounts.

Significant Assertion

The key assertion to be assessed that whether same has been valuing on fair value method or not.

Further, the validity of transaction affected by this account required to be asserted.

Procedure of Auditing

specific appropriate opinion. Hence same has been considered significant account.

Significant Assertion

Appropriate recognition and valuation are the two key assertions required to be ascertained.

Procedure of Auditing

The audit procedure should be initiated by assessing the method of valuation of

derivatives

Moreover, emphasis should be made on reasonableness on management evaluation of the

fair value of other assets, liabilities along with borrowings.

The efficient substantive procedure should be applied to assess the availability of material

risk.

Finally, compliance provision of ASA 520 ‘Analytical procedures’ should be applied in

order to assess the viability of accounting treatment applied for recognition of

borrowings.

Contingent considerations

Reason due to which specified account require detail assessment

A significant decrease in account balance of contingent consideration has been assessed, i.e.

from $500000 to $150000 (Annual report of Monash IVF Group, 2017). Thus, the reason behind

is required to be assessed in detail. It might be possible that a part of revenue might be

recognized as contingent consideration and same will eventually lead to a present unfair position

of books of accounts.

Significant Assertion

The key assertion to be assessed that whether same has been valuing on fair value method or not.

Further, the validity of transaction affected by this account required to be asserted.

Procedure of Auditing

Checking compliance with para 24 and 25 of FASB statement no. 141 which specifies

that contingency consideration should be accounted when contingency issue becomes

issuable.

Further compliance with the provision of AASB 137 ‘Provision for contingent liabilities’

is required to be assessed to verify the appropriateness of its recognition.

The policy followed by the company to evaluate contingent consideration is required to

be assessed in order to ascertain whether transaction have been valued in accordance with

fair valuation method or not.

Revenue

Reason due to which specified account require detail assessment

A decrease of 0.9% in revenue of Monash Group IVF Ltd., i.e. from $156.6 million to $155.2

can be assessed in comparison to the revenue of the previous year 2016. However, the change in

net profit after tax is 2.9% as it has enhanced from $28.8 million to $29.6 million (Annual report

of Monash IVF Group, 2017). The contradiction requires to be assessed in detail because in

general circumstances profit and revenue have a positive relation. Thus, the unusual scenario is

the reason that account might consist of risk of materiality. Moreover, income is having a

significant impact on other vital accounts such as income tax, Net profit etc. Thus it requires to

be assessed in detail.

Significant Assertion

The two assertions which required to be assessed are occurrence and accuracy.

Procedure of Auditing

General ledgers are assessed in detail in order to assess the manner of accounting.

Sample method can be applied to review specific details relating to revenue such as date

of delivery, date of payment and other information relating to the transaction.

The trend of sales of present year can be compared with previous year trend to ascertain

any significant variance exists (Chan and Vasarhelyi, 2018).

It is necessary to be assured that information of general ledger should be in accordance

with the figure of actual sales.

that contingency consideration should be accounted when contingency issue becomes

issuable.

Further compliance with the provision of AASB 137 ‘Provision for contingent liabilities’

is required to be assessed to verify the appropriateness of its recognition.

The policy followed by the company to evaluate contingent consideration is required to

be assessed in order to ascertain whether transaction have been valued in accordance with

fair valuation method or not.

Revenue

Reason due to which specified account require detail assessment

A decrease of 0.9% in revenue of Monash Group IVF Ltd., i.e. from $156.6 million to $155.2

can be assessed in comparison to the revenue of the previous year 2016. However, the change in

net profit after tax is 2.9% as it has enhanced from $28.8 million to $29.6 million (Annual report

of Monash IVF Group, 2017). The contradiction requires to be assessed in detail because in

general circumstances profit and revenue have a positive relation. Thus, the unusual scenario is

the reason that account might consist of risk of materiality. Moreover, income is having a

significant impact on other vital accounts such as income tax, Net profit etc. Thus it requires to

be assessed in detail.

Significant Assertion

The two assertions which required to be assessed are occurrence and accuracy.

Procedure of Auditing

General ledgers are assessed in detail in order to assess the manner of accounting.

Sample method can be applied to review specific details relating to revenue such as date

of delivery, date of payment and other information relating to the transaction.

The trend of sales of present year can be compared with previous year trend to ascertain

any significant variance exists (Chan and Vasarhelyi, 2018).

It is necessary to be assured that information of general ledger should be in accordance

with the figure of actual sales.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.