ACC320 Semester 2 - Audit Processes & Corporate Failure Proposal

VerifiedAdded on 2023/06/04

|11

|2264

|354

Report

AI Summary

This research proposal investigates the relationship between audit processes and corporate failure in Australian organizations. It highlights the practical motivation stemming from the increasing risk of corporate failure and auditor misconduct in Australia. The theoretical motivation addresses gaps in existing theories by emphasizing the importance of following IFRS and GAAP guidelines, along with the IFAC code of ethics, to mitigate corporate failure risks. The literature review covers the concept of audit and accounting standards, the concept and reasons for corporate failure, and the relationship between audit processes and corporate failure in Australian organizations, referencing various studies and cases. The proposal concludes with a hypothesis stating that audit processes and standards significantly impact corporate failure in Australian organizations. Desklib offers a platform for students to access this and other solved assignments and past papers.

Running head: AUDIT PROCESSES AND CORPORATE FAILURE

ACC320 Contemporary Issues in Accounting

Semester 2 2018

Research Proposal

Student Name:

Student ID:

Title: Audit Processes and Corporate Failure

Submission Date:

ACC320 Contemporary Issues in Accounting

Semester 2 2018

Research Proposal

Student Name:

Student ID:

Title: Audit Processes and Corporate Failure

Submission Date:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUDIT PROCESSES AND CORPORATE FAILURE

Acknowledgement

I certify that I have carefully reviewed the university’s academic misconduct policy. I

understand that the source of ideas must be referenced and that quotation marks and a

reference are required when directly quoting anyone else’s words.

Acknowledgement

I certify that I have carefully reviewed the university’s academic misconduct policy. I

understand that the source of ideas must be referenced and that quotation marks and a

reference are required when directly quoting anyone else’s words.

2AUDIT PROCESSES AND CORPORATE FAILURE

Table of Contents

Introduction................................................................................................................................3

Practical Motivation...............................................................................................................3

Theoretical Motivation...........................................................................................................4

Literature Review.......................................................................................................................4

Concept of Audit and Accounting Standards.........................................................................4

Concept and Reasons of Corporate Failure............................................................................5

Relationship between Audit process and Corporate Failure in Australian Organizations.....6

Hypotheses.................................................................................................................................7

References..................................................................................................................................8

Appendices...............................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Practical Motivation...............................................................................................................3

Theoretical Motivation...........................................................................................................4

Literature Review.......................................................................................................................4

Concept of Audit and Accounting Standards.........................................................................4

Concept and Reasons of Corporate Failure............................................................................5

Relationship between Audit process and Corporate Failure in Australian Organizations.....6

Hypotheses.................................................................................................................................7

References..................................................................................................................................8

Appendices...............................................................................................................................10

3AUDIT PROCESSES AND CORPORATE FAILURE

Introduction

In the fiercely competitive scenario, external auditing processes is considered to act as

a technology that facilitates all the stakeholders of the organization to manage, control and

deal with aspects in presenting risks that might lead to corporate failure (Ahmed and

Ndayisaba 2016). The objective of the current paper is to analyze the impact of audit

processes in resulting to corporate failure within Australian companies.

Practical Motivation

The risk of corporate failure is drastically faced by the stakeholders of the

organization as such situation has become common internationally. A huge number of public

and quoted organizations in Australia attain a misrepresented audit report. The auditors of the

company get involved in fraud knowingly as they are observed to accept bribe for such

misstatements (Appuhami and Bhuyan 2015). Misconducts regarding the auditors

responsibilities are an increasing concern in Australia companies and fraud is observed to be

a vital aspect of the “expectation gap” that is present between expectations of the financial

statement users and the reports developed by the auditors. The negligence from the side of the

auditors is resulting in liquidation of several companies in Australia. The accountants and

managers of the organizations are dealing in issues in establishing more improvement in their

corporate governance structures particularly in its internal control processes along with

potential areas of attaining cost savings and audit efficient in avoiding corporate failure (Ball,

Tyler and Wells 2015). Focused on such serious concern faced by the organizations, the

current research will focus on analyzing the ways in which the responsibilities of

stakeholders can be enhanced in conducting corporate audit in accordance with the auditing

standards. Moreover, the research will also explain the practical implementation of IFRS

guidelines that can facilitate in decreasing the occurrence of corporate failure for Australian

organizations.

Introduction

In the fiercely competitive scenario, external auditing processes is considered to act as

a technology that facilitates all the stakeholders of the organization to manage, control and

deal with aspects in presenting risks that might lead to corporate failure (Ahmed and

Ndayisaba 2016). The objective of the current paper is to analyze the impact of audit

processes in resulting to corporate failure within Australian companies.

Practical Motivation

The risk of corporate failure is drastically faced by the stakeholders of the

organization as such situation has become common internationally. A huge number of public

and quoted organizations in Australia attain a misrepresented audit report. The auditors of the

company get involved in fraud knowingly as they are observed to accept bribe for such

misstatements (Appuhami and Bhuyan 2015). Misconducts regarding the auditors

responsibilities are an increasing concern in Australia companies and fraud is observed to be

a vital aspect of the “expectation gap” that is present between expectations of the financial

statement users and the reports developed by the auditors. The negligence from the side of the

auditors is resulting in liquidation of several companies in Australia. The accountants and

managers of the organizations are dealing in issues in establishing more improvement in their

corporate governance structures particularly in its internal control processes along with

potential areas of attaining cost savings and audit efficient in avoiding corporate failure (Ball,

Tyler and Wells 2015). Focused on such serious concern faced by the organizations, the

current research will focus on analyzing the ways in which the responsibilities of

stakeholders can be enhanced in conducting corporate audit in accordance with the auditing

standards. Moreover, the research will also explain the practical implementation of IFRS

guidelines that can facilitate in decreasing the occurrence of corporate failure for Australian

organizations.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUDIT PROCESSES AND CORPORATE FAILURE

Theoretical Motivation

There exist two major models related with approaches to corporate failure that

includes prospect theory and rigidity effect theory (Ball and Wells 2015). Prospect theory

indicates that the managers turn out to highly prone to risk taking behavior that results them

in committing towards a course of action that can lead to corporate collapses. On the other

hand, “Rigidity effect theory” has a perspective that in a risky condition the managers lack

their decision making power. In such situation, the board of directors acts in dealing with

risky behavior or alter the corporate criteria on other hand. Failing to do so is deemed to

result in corporate failure (Carnegie and O’Connell 2014). It is gathered that these theories

had a gap in explaining the role of accounting standards in avoiding the risks of corporate

failure. Considering such gap, the current research will focus on analyzing the importance of

following the audit processes guidelines explained in “International Financial Reporting

Standards (IFRS)” and “Generally Accepted Accounting Principles (GAAP)” in decreasing

risks of corporate failure. Moreover the current research will also explain the necessity audit

principle framework “IFAC (Professional Code of Ethics)” in order to observe the ways in

which companies can attain audit process regulations and maintain strict regimes of

enforcement and monitoring (Carson, Fargher and Zhang 2016).

Literature Review

Concept of Audit and Accounting Standards

Dobele, Westberg, Steel and Flowers (2014) explained the audit and accounting

standards to be certain important financial reporting authoritative standards that serve as the

major source of “Generally Accepted Accounting Principles (GAAP)”. It is deemed

necessary for the Australian organizations to abide by the regulations of “Financial Reporting

Standards (IFRS)” along with necessary accounting standards that are greatly used by

publically accountable companies. Hay, Stewart and Botica Redmayne (2017) stated that the

Theoretical Motivation

There exist two major models related with approaches to corporate failure that

includes prospect theory and rigidity effect theory (Ball and Wells 2015). Prospect theory

indicates that the managers turn out to highly prone to risk taking behavior that results them

in committing towards a course of action that can lead to corporate collapses. On the other

hand, “Rigidity effect theory” has a perspective that in a risky condition the managers lack

their decision making power. In such situation, the board of directors acts in dealing with

risky behavior or alter the corporate criteria on other hand. Failing to do so is deemed to

result in corporate failure (Carnegie and O’Connell 2014). It is gathered that these theories

had a gap in explaining the role of accounting standards in avoiding the risks of corporate

failure. Considering such gap, the current research will focus on analyzing the importance of

following the audit processes guidelines explained in “International Financial Reporting

Standards (IFRS)” and “Generally Accepted Accounting Principles (GAAP)” in decreasing

risks of corporate failure. Moreover the current research will also explain the necessity audit

principle framework “IFAC (Professional Code of Ethics)” in order to observe the ways in

which companies can attain audit process regulations and maintain strict regimes of

enforcement and monitoring (Carson, Fargher and Zhang 2016).

Literature Review

Concept of Audit and Accounting Standards

Dobele, Westberg, Steel and Flowers (2014) explained the audit and accounting

standards to be certain important financial reporting authoritative standards that serve as the

major source of “Generally Accepted Accounting Principles (GAAP)”. It is deemed

necessary for the Australian organizations to abide by the regulations of “Financial Reporting

Standards (IFRS)” along with necessary accounting standards that are greatly used by

publically accountable companies. Hay, Stewart and Botica Redmayne (2017) stated that the

5AUDIT PROCESSES AND CORPORATE FAILURE

objective of the management audit is associated with the management interests like

evaluation of the area efficiency or performance. An audit might also be realized as internal

or external based on the interrelationships among the assoiled participants. These researchers

also revealed that the Australian Auditing Standards maintain necessary requirements and

offer guidelines on the auditor’s responsibilities when engaged to get involved in financial

report audit or accomplish a set of financial statements along with developing a reliable form

and content of auditor’s report. Martinov-Bennie, Soh and Tweedie (2015) added that the

organizations in Australia are liable to obtain a statutory audit to carry out an annual audit

regarding the financial position of the organizations based on the guidelines of such auditing

standards.

Concept and Reasons of Corporate Failure

Miglani, Ahmed and Henry (2015) explained corporate failure to be a situation in

which an organization is facing a situation to deal with lack of legally enforceable debt in

order to address their current obligations. Moreover, can be declared to be liquidated in a

situation where the companies have become insolvent or bankrupt in which the organization

is forced to shut down its business operations. Stafford and Stapleton (2017) also defined

corporate failure to be the cause of ineffective compliance with corporate governance

standards that results in increased economic costs of business failure in which the

stakeholders of the company are drastically affected. Yigitbasioglu (2015) elaborated that

there are several causes of corporate failure in consideration to its accounting processes.

These factors include lack of board effectiveness that is a result of lack in skills and

competence and poor leadership culture followed within the companies that includes inability

to supervise the internal audit or risk management teams in risk reporting. Stafford and

Stapleton (2017) revealed that certain other factors lead to corporate failure in Australia that

includes not abiding by the standards of financial standards fairness. The upper management

objective of the management audit is associated with the management interests like

evaluation of the area efficiency or performance. An audit might also be realized as internal

or external based on the interrelationships among the assoiled participants. These researchers

also revealed that the Australian Auditing Standards maintain necessary requirements and

offer guidelines on the auditor’s responsibilities when engaged to get involved in financial

report audit or accomplish a set of financial statements along with developing a reliable form

and content of auditor’s report. Martinov-Bennie, Soh and Tweedie (2015) added that the

organizations in Australia are liable to obtain a statutory audit to carry out an annual audit

regarding the financial position of the organizations based on the guidelines of such auditing

standards.

Concept and Reasons of Corporate Failure

Miglani, Ahmed and Henry (2015) explained corporate failure to be a situation in

which an organization is facing a situation to deal with lack of legally enforceable debt in

order to address their current obligations. Moreover, can be declared to be liquidated in a

situation where the companies have become insolvent or bankrupt in which the organization

is forced to shut down its business operations. Stafford and Stapleton (2017) also defined

corporate failure to be the cause of ineffective compliance with corporate governance

standards that results in increased economic costs of business failure in which the

stakeholders of the company are drastically affected. Yigitbasioglu (2015) elaborated that

there are several causes of corporate failure in consideration to its accounting processes.

These factors include lack of board effectiveness that is a result of lack in skills and

competence and poor leadership culture followed within the companies that includes inability

to supervise the internal audit or risk management teams in risk reporting. Stafford and

Stapleton (2017) revealed that certain other factors lead to corporate failure in Australia that

includes not abiding by the standards of financial standards fairness. The upper management

6AUDIT PROCESSES AND CORPORATE FAILURE

is generally observed to deal with the corporate failure responsibility because of their

ignorance of their own overconfidence, high risk taking behavioral and non-compliance with

necessary auditing standards.

Relationship between Audit process and Corporate Failure in Australian Organizations

Miglani, Ahmed and Henry (2015) evidenced that in case of Australian organizations

corporate governance is observed to be a vital factor that ensures effective financial reporting

and deterring misappropriations of capital within the company. Poor audit processes and

corporate governance is deemed to serve as a major factor that is resulting in financial

institution distress in Australia. These researchers have also revealed certain evidences on

current “Economic and Financial Crimes Commissions” cases against certain bank

executives. Researchers such as Miglani, Ahmed and Henry (2015) have indicated that

certain other renowned companies such as HIH Insurance, ABC Learning and One-Tel

Company failed because of its incapability to comply with the necessary auditing standards.

These researchers also gathered that the absence of the necessary risk management and

internal controls is resulting in inappropriate operation of such procedures. Stafford and

Stapleton (2017) that the legal duties and responsibilities are not maintained by the directors

of certain organizations that is resulting in corporate failure that is resultant from insolvent

trading and not able to retain the discretionary powers along with delegating the director’s

responsibility. These researchers also revealed that after failure of numerous renowned ASX

listed companies, the emerging businesses in Australia are focusing on enhancing their

corporate governance structures and is attempting to abide by the “Corporate Governance

Network (ICGN)” that has offered its own recommended codes and audit guidelines. Hay,

Stewart and Botica Redmayne (2017) added that the independent directors those are relied on

independent auditors in disclosing their unassisted claims taking place from the

is generally observed to deal with the corporate failure responsibility because of their

ignorance of their own overconfidence, high risk taking behavioral and non-compliance with

necessary auditing standards.

Relationship between Audit process and Corporate Failure in Australian Organizations

Miglani, Ahmed and Henry (2015) evidenced that in case of Australian organizations

corporate governance is observed to be a vital factor that ensures effective financial reporting

and deterring misappropriations of capital within the company. Poor audit processes and

corporate governance is deemed to serve as a major factor that is resulting in financial

institution distress in Australia. These researchers have also revealed certain evidences on

current “Economic and Financial Crimes Commissions” cases against certain bank

executives. Researchers such as Miglani, Ahmed and Henry (2015) have indicated that

certain other renowned companies such as HIH Insurance, ABC Learning and One-Tel

Company failed because of its incapability to comply with the necessary auditing standards.

These researchers also gathered that the absence of the necessary risk management and

internal controls is resulting in inappropriate operation of such procedures. Stafford and

Stapleton (2017) that the legal duties and responsibilities are not maintained by the directors

of certain organizations that is resulting in corporate failure that is resultant from insolvent

trading and not able to retain the discretionary powers along with delegating the director’s

responsibility. These researchers also revealed that after failure of numerous renowned ASX

listed companies, the emerging businesses in Australia are focusing on enhancing their

corporate governance structures and is attempting to abide by the “Corporate Governance

Network (ICGN)” that has offered its own recommended codes and audit guidelines. Hay,

Stewart and Botica Redmayne (2017) added that the independent directors those are relied on

independent auditors in disclosing their unassisted claims taking place from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT PROCESSES AND CORPORATE FAILURE

organizational risks must be aware of the limited duties of independent auditors in

investigating such risks.

Hypotheses

The research hypothesis that is to be tested through completion of this research is

indicated below:

Audit processes and standards followed in the Australian organizations have a

significant impact on resulting in corporate failure.

organizational risks must be aware of the limited duties of independent auditors in

investigating such risks.

Hypotheses

The research hypothesis that is to be tested through completion of this research is

indicated below:

Audit processes and standards followed in the Australian organizations have a

significant impact on resulting in corporate failure.

8AUDIT PROCESSES AND CORPORATE FAILURE

References

Ahmed, A.D. and Ndayisaba, G.A., 2016. Effect of corporate governance on ceo pay-risk

taking association: empirical evidence from australian financial institutions. The Journal of

Developing Areas, 50(4), pp.309-344.

Appuhami, R. and Bhuyan, M., 2015. Examining the influence of corporate governance on

intellectual capital efficiency: Evidence from top service firms in Australia. Managerial

Auditing Journal, 30(4/5), pp.347-372.

Ball, F., Tyler, J. and Wells, P., 2015. Is audit quality impacted by auditor

relationships?. Journal of Contemporary Accounting & Economics, 11(2), pp.166-181.

Ball, F., and Wells, P., 2015. Is audit quality impacted by auditor relationships?. Journal of

Contemporary Accounting & Economics, 11(2), pp.166-181.

Carnegie, G.D. and O’Connell, B.T., 2014. A longitudinal study of the interplay of corporate

collapse, accounting failure and governance change in Australia: Early 1890s to early

2000s. Critical Perspectives on Accounting, 25(6), pp.446-468.

Carson, E., Fargher, N. and Zhang, Y., 2016. Trends in auditor reporting in Australia: a

synthesis and opportunities for research. Australian Accounting Review, 26(3), pp.226-242.

Dobele, A.R., Westberg, K., Steel, M. and Flowers, K., 2014. An examination of corporate

social responsibility implementation and stakeholder engagement: A case study in the

Australian mining industry. Business Strategy and the Environment, 23(3), pp.145-159.

Hay, D., Stewart, J. and Botica Redmayne, N., 2017. The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis. Australian Accounting

Review, 27(4), pp.457-479.

References

Ahmed, A.D. and Ndayisaba, G.A., 2016. Effect of corporate governance on ceo pay-risk

taking association: empirical evidence from australian financial institutions. The Journal of

Developing Areas, 50(4), pp.309-344.

Appuhami, R. and Bhuyan, M., 2015. Examining the influence of corporate governance on

intellectual capital efficiency: Evidence from top service firms in Australia. Managerial

Auditing Journal, 30(4/5), pp.347-372.

Ball, F., Tyler, J. and Wells, P., 2015. Is audit quality impacted by auditor

relationships?. Journal of Contemporary Accounting & Economics, 11(2), pp.166-181.

Ball, F., and Wells, P., 2015. Is audit quality impacted by auditor relationships?. Journal of

Contemporary Accounting & Economics, 11(2), pp.166-181.

Carnegie, G.D. and O’Connell, B.T., 2014. A longitudinal study of the interplay of corporate

collapse, accounting failure and governance change in Australia: Early 1890s to early

2000s. Critical Perspectives on Accounting, 25(6), pp.446-468.

Carson, E., Fargher, N. and Zhang, Y., 2016. Trends in auditor reporting in Australia: a

synthesis and opportunities for research. Australian Accounting Review, 26(3), pp.226-242.

Dobele, A.R., Westberg, K., Steel, M. and Flowers, K., 2014. An examination of corporate

social responsibility implementation and stakeholder engagement: A case study in the

Australian mining industry. Business Strategy and the Environment, 23(3), pp.145-159.

Hay, D., Stewart, J. and Botica Redmayne, N., 2017. The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis. Australian Accounting

Review, 27(4), pp.457-479.

9AUDIT PROCESSES AND CORPORATE FAILURE

Martinov-Bennie, N., Soh, D.S. and Tweedie, D., 2015. An investigation into the roles,

characteristics, expectations and evaluation practices of audit committees. Managerial

Auditing Journal, 30(8/9), pp.727-755.

Miglani, S., Ahmed, K. and Henry, D., 2015. Voluntary corporate governance structure and

financial distress: evidence from Australia. Journal of Contemporary Accounting &

Economics, 11(1), pp.18-30.

Stafford, A. and Stapleton, P., 2017. Examining the Use of Corporate Governance

Mechanisms in Public–Private Partnerships: Why Do They Not Deliver Public

Accountability?. Australian Journal of Public Administration, 76(3), pp.378-391.

Yigitbasioglu, O.M., 2015. External auditors' perceptions of cloud computing adoption in

Australia. International Journal of Accounting Information Systems, 18, pp.46-62.

Martinov-Bennie, N., Soh, D.S. and Tweedie, D., 2015. An investigation into the roles,

characteristics, expectations and evaluation practices of audit committees. Managerial

Auditing Journal, 30(8/9), pp.727-755.

Miglani, S., Ahmed, K. and Henry, D., 2015. Voluntary corporate governance structure and

financial distress: evidence from Australia. Journal of Contemporary Accounting &

Economics, 11(1), pp.18-30.

Stafford, A. and Stapleton, P., 2017. Examining the Use of Corporate Governance

Mechanisms in Public–Private Partnerships: Why Do They Not Deliver Public

Accountability?. Australian Journal of Public Administration, 76(3), pp.378-391.

Yigitbasioglu, O.M., 2015. External auditors' perceptions of cloud computing adoption in

Australia. International Journal of Accounting Information Systems, 18, pp.46-62.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10AUDIT PROCESSES AND CORPORATE FAILURE

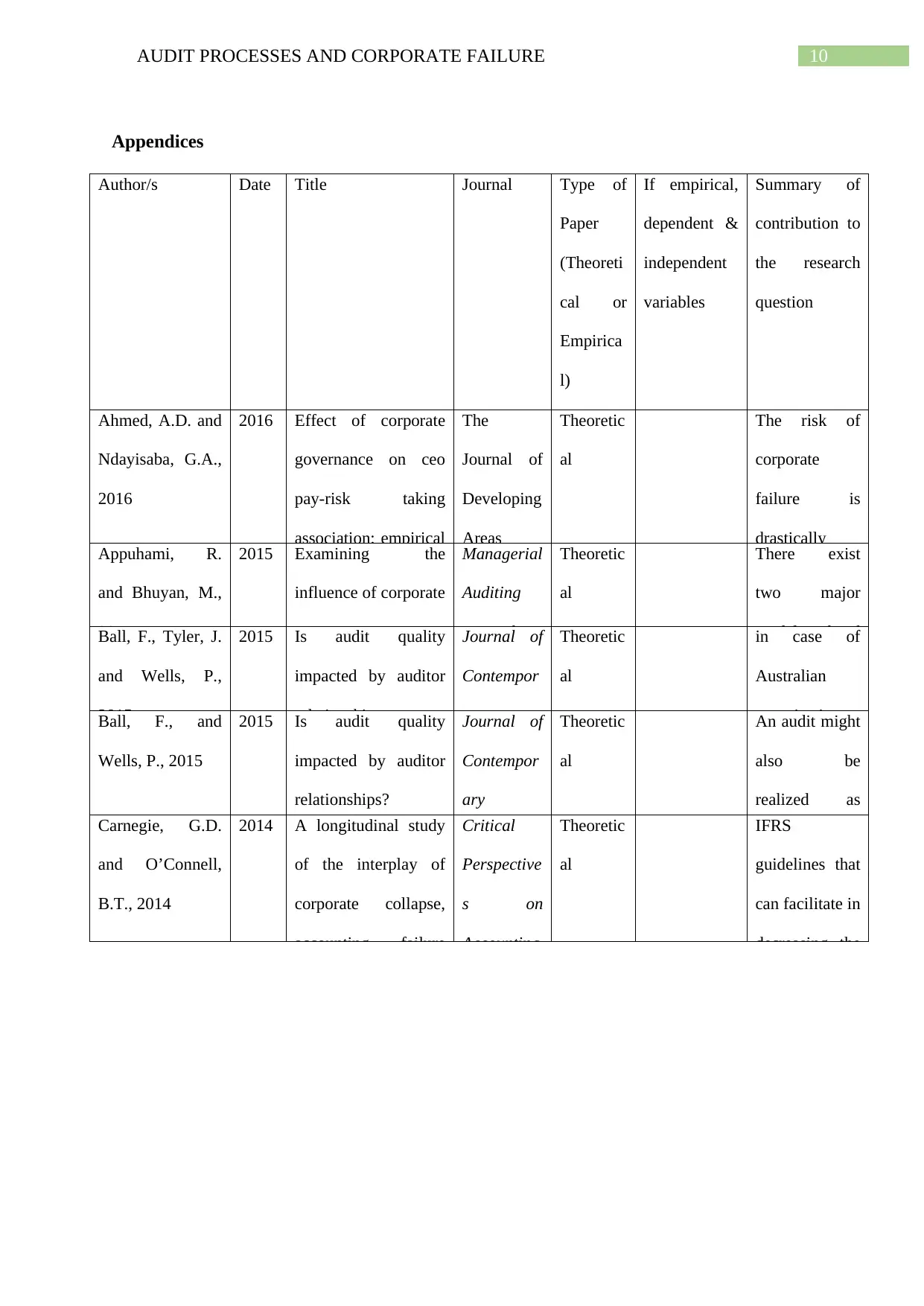

Appendices

Author/s Date Title Journal Type of

Paper

(Theoreti

cal or

Empirica

l)

If empirical,

dependent &

independent

variables

Summary of

contribution to

the research

question

Ahmed, A.D. and

Ndayisaba, G.A.,

2016

2016 Effect of corporate

governance on ceo

pay-risk taking

association: empirical

The

Journal of

Developing

Areas

Theoretic

al

The risk of

corporate

failure is

drastically

Appuhami, R.

and Bhuyan, M.,

2015

2015 Examining the

influence of corporate

governance on

Managerial

Auditing

Journal

Theoretic

al

There exist

two major

models relatedBall, F., Tyler, J.

and Wells, P.,

2015

2015 Is audit quality

impacted by auditor

relationships

Journal of

Contempor

ary

Theoretic

al

in case of

Australian

organizationsBall, F., and

Wells, P., 2015

2015 Is audit quality

impacted by auditor

relationships?

Journal of

Contempor

ary

Accounting

Theoretic

al

An audit might

also be

realized as

internal or

Carnegie, G.D.

and O’Connell,

B.T., 2014

2014 A longitudinal study

of the interplay of

corporate collapse,

accounting failure

Critical

Perspective

s on

Accounting

Theoretic

al

IFRS

guidelines that

can facilitate in

decreasing the

Appendices

Author/s Date Title Journal Type of

Paper

(Theoreti

cal or

Empirica

l)

If empirical,

dependent &

independent

variables

Summary of

contribution to

the research

question

Ahmed, A.D. and

Ndayisaba, G.A.,

2016

2016 Effect of corporate

governance on ceo

pay-risk taking

association: empirical

The

Journal of

Developing

Areas

Theoretic

al

The risk of

corporate

failure is

drastically

Appuhami, R.

and Bhuyan, M.,

2015

2015 Examining the

influence of corporate

governance on

Managerial

Auditing

Journal

Theoretic

al

There exist

two major

models relatedBall, F., Tyler, J.

and Wells, P.,

2015

2015 Is audit quality

impacted by auditor

relationships

Journal of

Contempor

ary

Theoretic

al

in case of

Australian

organizationsBall, F., and

Wells, P., 2015

2015 Is audit quality

impacted by auditor

relationships?

Journal of

Contempor

ary

Accounting

Theoretic

al

An audit might

also be

realized as

internal or

Carnegie, G.D.

and O’Connell,

B.T., 2014

2014 A longitudinal study

of the interplay of

corporate collapse,

accounting failure

Critical

Perspective

s on

Accounting

Theoretic

al

IFRS

guidelines that

can facilitate in

decreasing the

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.