Effect of Audit Reports on Annual Financial Reporting Quality of an Organisation

VerifiedAdded on 2023/06/12

|28

|7946

|372

AI Summary

This research examines the influence of audit quality on financial reporting in Australia. It includes a literature review on measures of financial reporting quality, components of quality, and the influence of auditing on financial reporting. The study aims to augment quality of audit and overall reliability of financial reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING RESEARCH

Accounting Research

University Name

Student Name

Authors’ Note

Accounting Research

University Name

Student Name

Authors’ Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

ACCOUNTING RESEARCH

Topic of Research

Effect of audit reports on Annual financial reporting quality of an organisation

Introduction

This research was undertaken in order to assess the influence of audit quality on financial

reporting in Australia. The study intended to examine, investigate and ascertain the

interaction between quality of audit and corporate financial reporting in Australia. Therefore,

the study can be considered to be a movement towards enhancement of the quality of audit

exercises in Australia.

Aim and objective of the study

The aim of the research study is to augment quality of audit and overall reliability of financial

reporting. Particularly, this study intends to

- Examine the relationship between audit quality in association to financial reporting quality

of business concerns in Australia

Research Question

1) What is the nature of association between audit quality and overall quality of financial

reporting in Australia?

Research Problem

The global financial crises, various failures of corporate and financial scandals worldwide

raise doubts and questions regarding the efficacy of financial reporting as well as quality of

auditing. Several auditing firms, certified and regulatory bodies are therefore under fire and

encounter immense pressures to refurbish confidence in particularly auditing (Sirois et al.,

2018). In essence, regulatory and certified bodies attempted to uphold quality of audit to

ACCOUNTING RESEARCH

Topic of Research

Effect of audit reports on Annual financial reporting quality of an organisation

Introduction

This research was undertaken in order to assess the influence of audit quality on financial

reporting in Australia. The study intended to examine, investigate and ascertain the

interaction between quality of audit and corporate financial reporting in Australia. Therefore,

the study can be considered to be a movement towards enhancement of the quality of audit

exercises in Australia.

Aim and objective of the study

The aim of the research study is to augment quality of audit and overall reliability of financial

reporting. Particularly, this study intends to

- Examine the relationship between audit quality in association to financial reporting quality

of business concerns in Australia

Research Question

1) What is the nature of association between audit quality and overall quality of financial

reporting in Australia?

Research Problem

The global financial crises, various failures of corporate and financial scandals worldwide

raise doubts and questions regarding the efficacy of financial reporting as well as quality of

auditing. Several auditing firms, certified and regulatory bodies are therefore under fire and

encounter immense pressures to refurbish confidence in particularly auditing (Sirois et al.,

2018). In essence, regulatory and certified bodies attempted to uphold quality of audit to

3

ACCOUNTING RESEARCH

restore tarnished image as well as to enhance their legitimacy along with standing. Thus, this

study intends to analyse whether superior audit quality directs the way towards superior

quality of financial reporting that subsequently is a mechanism to avert financial crises.

Section: Literature Review

Introduction

The current section presents articles along research papers cope with control on and

dimensions of quality of financial reporting, as regards focus, concerns, as well as findings.

Essentially the section on review includes different elements of quality of financial reporting,

auditing and influence of auditing on financial reporting.

Measures of Financial Reporting Quality

Components of Quality

As righty put forward by Lennox et al., (2016), the important principle of evaluating the

financial reporting quality can be associated to faithfulness of overall objectives along with

quality of divulged information in financial reports of a business enterprise. In essence, these

qualitative characteristics augment facilitation of process of reviewing the effectiveness of

financial statements. This can show the way to superior level of quality. In order to attain this

level, different financial reports have the need to be faithfully reflected, comparable,

understandable, well timed and verifiable (Gaynor et al., 2016). Therefore, the stress is on

getting transparent financial assertions in place of misleading financial pronouncements. In

this connection it can also be said that there is also significance of preciseness along with

predictability as indicator of a superior quality of financial reporting.

According to the Conceptual Framework for the purpose of accounting, there are various

agreed upon components of superior quality financial pronouncements. In essence, different

ACCOUNTING RESEARCH

restore tarnished image as well as to enhance their legitimacy along with standing. Thus, this

study intends to analyse whether superior audit quality directs the way towards superior

quality of financial reporting that subsequently is a mechanism to avert financial crises.

Section: Literature Review

Introduction

The current section presents articles along research papers cope with control on and

dimensions of quality of financial reporting, as regards focus, concerns, as well as findings.

Essentially the section on review includes different elements of quality of financial reporting,

auditing and influence of auditing on financial reporting.

Measures of Financial Reporting Quality

Components of Quality

As righty put forward by Lennox et al., (2016), the important principle of evaluating the

financial reporting quality can be associated to faithfulness of overall objectives along with

quality of divulged information in financial reports of a business enterprise. In essence, these

qualitative characteristics augment facilitation of process of reviewing the effectiveness of

financial statements. This can show the way to superior level of quality. In order to attain this

level, different financial reports have the need to be faithfully reflected, comparable,

understandable, well timed and verifiable (Gaynor et al., 2016). Therefore, the stress is on

getting transparent financial assertions in place of misleading financial pronouncements. In

this connection it can also be said that there is also significance of preciseness along with

predictability as indicator of a superior quality of financial reporting.

According to the Conceptual Framework for the purpose of accounting, there are various

agreed upon components of superior quality financial pronouncements. In essence, different

4

ACCOUNTING RESEARCH

qualitative characteristics of pecuniary reporting include faithful representation, relevance,

timeliness, verifiability understandability as well as comparability. In actual fact, these are

also divided into different fundamental qualitative characteristics along with enhancing

qualitative features (Badolato et al., 2014). In essence, a theoretical illustration for the said

terms help in stressing and focussing on significance as qualitative characteristics, and also

indicates towards various qualities that are regarded to be fundamental among various

structures.

Relevance

As rightly mentioned by Abbott et al., (2016), relevance can be said to closely related to

terms of usefulness as well as materiality. In particular, relevance depicts ability of

undertaking various business decisions bya users of information presented in the financial

reporting. As such, at the time when information is presented in the financial assertions also

exert influence on economic decisions. This information is said to have the quality and

characteristic of relevance. In addition to this, at the time when this specific information aids

various users to analyse, correct and at the same time substantiate current as well as previous

incidents. The effectiveness of framing a decision that is a significant part of the quality of

relevance is said to be consistent with the framework presented by the conceptual framework.

As suggested by Brasel et al., (2016), fair value can be regarded as one of the most important

indicators or signs of relevance. Utilizing fair value in a business entity, as a foundation for

the enumeration can be regarded as an important sign of higher level of relevance in the

financial reporting information. Essentially annual declarations have an important role in the

process of ascertainment of level of relevance by divulging specific information regarding

opportunities of business along with risks. This can help in delivering feedback on the way

major market incidents and important business transactions can affect operations of business

entities (Pucheta‐Martínez & García‐Meca, 2014).

ACCOUNTING RESEARCH

qualitative characteristics of pecuniary reporting include faithful representation, relevance,

timeliness, verifiability understandability as well as comparability. In actual fact, these are

also divided into different fundamental qualitative characteristics along with enhancing

qualitative features (Badolato et al., 2014). In essence, a theoretical illustration for the said

terms help in stressing and focussing on significance as qualitative characteristics, and also

indicates towards various qualities that are regarded to be fundamental among various

structures.

Relevance

As rightly mentioned by Abbott et al., (2016), relevance can be said to closely related to

terms of usefulness as well as materiality. In particular, relevance depicts ability of

undertaking various business decisions bya users of information presented in the financial

reporting. As such, at the time when information is presented in the financial assertions also

exert influence on economic decisions. This information is said to have the quality and

characteristic of relevance. In addition to this, at the time when this specific information aids

various users to analyse, correct and at the same time substantiate current as well as previous

incidents. The effectiveness of framing a decision that is a significant part of the quality of

relevance is said to be consistent with the framework presented by the conceptual framework.

As suggested by Brasel et al., (2016), fair value can be regarded as one of the most important

indicators or signs of relevance. Utilizing fair value in a business entity, as a foundation for

the enumeration can be regarded as an important sign of higher level of relevance in the

financial reporting information. Essentially annual declarations have an important role in the

process of ascertainment of level of relevance by divulging specific information regarding

opportunities of business along with risks. This can help in delivering feedback on the way

major market incidents and important business transactions can affect operations of business

entities (Pucheta‐Martínez & García‐Meca, 2014).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

ACCOUNTING RESEARCH

Reliability

As correctly put forward by Robert Knechel et al., (2015), reliability can be considered to be

an important facet of quality of financial reporting. In particular, in case of financial

reporting, specific information has the need of quality of specifically reliability in a bid to be

effective. In essence, this quality can be attained at the time when information that users

depend upon is free from primarily bias as well as material errors.

Comparability

Cohen et al., (2013) suggests that comparability can be considered to be an important theme

of permitting various users to ascertain financial health and position, flow of cash and

performance of business entity. In essence, this process of comparison can help in the process

of carrying out comparisons across different time period and among different other

corporations during the same period of time. Particularly, comparability calls for the need

that similar incidents in the two different situations need to be represented by identical

accounting facts as well as numerals (Abbott et al., 2010). There are essentially different

events that can be represented by diverse accounting facts as well as figures in a manner that

can quantitatively represent the variances in both a comparable and at the same time and

interpretable way.

In a bid to point out towards this point, specific notes presented in financial statement have

the need to divulge as well as illustrate all the requisite alterations in the policies of the

accounting (Carcello & Nagy, 2014). In addition to this, notes also need to present the

implications of the alterations and applications of accounting principles as well as principles.

Furthermore, the present accounting period also have the need to compare with the ones from

prior ones. Finally, presentation of financial index along with financial ratios can contribute

towards comparison to other corporations.

ACCOUNTING RESEARCH

Reliability

As correctly put forward by Robert Knechel et al., (2015), reliability can be considered to be

an important facet of quality of financial reporting. In particular, in case of financial

reporting, specific information has the need of quality of specifically reliability in a bid to be

effective. In essence, this quality can be attained at the time when information that users

depend upon is free from primarily bias as well as material errors.

Comparability

Cohen et al., (2013) suggests that comparability can be considered to be an important theme

of permitting various users to ascertain financial health and position, flow of cash and

performance of business entity. In essence, this process of comparison can help in the process

of carrying out comparisons across different time period and among different other

corporations during the same period of time. Particularly, comparability calls for the need

that similar incidents in the two different situations need to be represented by identical

accounting facts as well as numerals (Abbott et al., 2010). There are essentially different

events that can be represented by diverse accounting facts as well as figures in a manner that

can quantitatively represent the variances in both a comparable and at the same time and

interpretable way.

In a bid to point out towards this point, specific notes presented in financial statement have

the need to divulge as well as illustrate all the requisite alterations in the policies of the

accounting (Carcello & Nagy, 2014). In addition to this, notes also need to present the

implications of the alterations and applications of accounting principles as well as principles.

Furthermore, the present accounting period also have the need to compare with the ones from

prior ones. Finally, presentation of financial index along with financial ratios can contribute

towards comparison to other corporations.

6

ACCOUNTING RESEARCH

Understandability

Understandability is one of the essential qualities of information in financial reports.

Achieving the quality of understandability is through effective communication. Thus, the

better the understanding of the information from users, the higher the quality that will be

achieved (Robert Knechel et al., 2015). It is one of the enhancing qualitative characteristics

that will increase when information is presented and classified clearly and sufficiently. When

annual reports are well organized, users can comprehend what their needs are (Robert

Knechel et al., 2015). Usage of graphs and tables helps to present information clearly, and the

usage of language and technical jargon can be followed easily.

Timeliness

As recommended by Krishnan et al., (2016), timeliness can be considered to be enhancing

qualitative features. In a bid to illustrate specific information in a well timed manner there is

need to present financial information to decision makers before losing its authority as well as

appropriate influences. Therefore, in a bid to assess overall quality of financial reporting in a

yearly financial reporting, timeliness can be analysed utilizing the time period between year-

end and issuing date of report of auditor.

Faithful Representation

Christ et al., (2015) says that faithful representation can be referred to as the notion of

representing the actual economic position of financial information that is presented in the

reports. In essence, this notion has the value of illustrating the way the obligations as well as

economic resources, counting real economic position of financial information, transactions,

and various incidents are entirely represented in financial reports. Furthermore, this specific

quality has neutrality has a theme that is regarding objectivity along with balance. As

ACCOUNTING RESEARCH

Understandability

Understandability is one of the essential qualities of information in financial reports.

Achieving the quality of understandability is through effective communication. Thus, the

better the understanding of the information from users, the higher the quality that will be

achieved (Robert Knechel et al., 2015). It is one of the enhancing qualitative characteristics

that will increase when information is presented and classified clearly and sufficiently. When

annual reports are well organized, users can comprehend what their needs are (Robert

Knechel et al., 2015). Usage of graphs and tables helps to present information clearly, and the

usage of language and technical jargon can be followed easily.

Timeliness

As recommended by Krishnan et al., (2016), timeliness can be considered to be enhancing

qualitative features. In a bid to illustrate specific information in a well timed manner there is

need to present financial information to decision makers before losing its authority as well as

appropriate influences. Therefore, in a bid to assess overall quality of financial reporting in a

yearly financial reporting, timeliness can be analysed utilizing the time period between year-

end and issuing date of report of auditor.

Faithful Representation

Christ et al., (2015) says that faithful representation can be referred to as the notion of

representing the actual economic position of financial information that is presented in the

reports. In essence, this notion has the value of illustrating the way the obligations as well as

economic resources, counting real economic position of financial information, transactions,

and various incidents are entirely represented in financial reports. Furthermore, this specific

quality has neutrality has a theme that is regarding objectivity along with balance. As

7

ACCOUNTING RESEARCH

recommended by Bowlin et al., (2015), scholars concluded that reports of the auditor can

necessarily add value to the entire financial reporting by delivering reasonable assurance

regarding degree to which yearly pronouncements an reflect specific economic phenomenon.

Additionally, how business organizations are controlled and directed affects the faithful

presentation quality; this, in fact, is represented as a corporate governance factor when there

is extensively disclosed information on corporate governance issues in the annual report

(Rezaee et al., 2018). Besides, the annual report clarifies assumptions and estimates and

explains the usage of the accounting principles in the company clearly. It also highlights

positive and negative changes and events by discussing them in the annual results. The last

important factor that strengthens this quality is having an unqualified auditor‘s report in the

annual report (Berger et al., 2017).

Influence of Auditing on quality of financial reporting

Definition of auditing

Auditing is an independent verification that enhances financial statement reliability and

usefulness. Since auditing is an integral part of the system, the inclusion of auditing variables

better reflects overall financial reporting quality. As rightly put forward by Aobdia et al.,

(2015), auditing can be regarded as an assessment of various books of accounts along with

vouchers of a business by a specific independent individual who need to be qualified for

specific jobs, in a bid to determine the level of accuracy. As correctly indicated by Hayes

(2014), the primary objectives of auditing include verification of various accounts along with

statements, detection of errors along with fraudulent actions and prevention of various errors

along with frauds.

ACCOUNTING RESEARCH

recommended by Bowlin et al., (2015), scholars concluded that reports of the auditor can

necessarily add value to the entire financial reporting by delivering reasonable assurance

regarding degree to which yearly pronouncements an reflect specific economic phenomenon.

Additionally, how business organizations are controlled and directed affects the faithful

presentation quality; this, in fact, is represented as a corporate governance factor when there

is extensively disclosed information on corporate governance issues in the annual report

(Rezaee et al., 2018). Besides, the annual report clarifies assumptions and estimates and

explains the usage of the accounting principles in the company clearly. It also highlights

positive and negative changes and events by discussing them in the annual results. The last

important factor that strengthens this quality is having an unqualified auditor‘s report in the

annual report (Berger et al., 2017).

Influence of Auditing on quality of financial reporting

Definition of auditing

Auditing is an independent verification that enhances financial statement reliability and

usefulness. Since auditing is an integral part of the system, the inclusion of auditing variables

better reflects overall financial reporting quality. As rightly put forward by Aobdia et al.,

(2015), auditing can be regarded as an assessment of various books of accounts along with

vouchers of a business by a specific independent individual who need to be qualified for

specific jobs, in a bid to determine the level of accuracy. As correctly indicated by Hayes

(2014), the primary objectives of auditing include verification of various accounts along with

statements, detection of errors along with fraudulent actions and prevention of various errors

along with frauds.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

ACCOUNTING RESEARCH

Kausar et al., (2016) suggests that auditors are provided free hand to particularly books,

various accounts along with statements that can enable auditors to verify the same. In case if

they get satisfied then they can substantiate that the books are appropriately drawn up and

reflect a true as well as fair view of financial position of the corporation. As such, auditors

provide special attention to different directions of mistakes/errors that might be intentionally

or else unintentionally committed. However, the auditor can find out the unintentional

mistakes by way of vouching various business transactions and by way of comparing as well

as tallying different balances between as well as among different books of accounts.

Nonetheless, in case of intentional mistakes, errors can be categorised as frauds since it

directs the way towards defrauding different proprietors. Chen et al., (2016) recommends that

frauds can be recognized by way of detailed assessment of the books along with documents

namely cash books, various invoices, documents on wage sheet and many others.

Categories of audit

As suggested by Christensen et al., (2014), auditing can be categorised into two different

types namely continuous or else detailed audit and periodical/final audits. Lennox et al.,

(2016) suggests that continuous audit is necessarily effective in case of big business

enterprises with large corporations that have scope for maintaining the audit staff engaged

and business throughout the year. The auditors might perhaps attend to auditing at different

intervals that are fixed and carry out an interim audit. As such, in this specific case, routine

business operations can be carried out all at once with the work of audit. On the other hand,

the periodical auditing refers to a audit work that is carried out continuously till the period of

completion. As such, this can be regarded as the system that can be referred to be the most

satisfying from the viewpoint of the auditors (Gaynor et al., 2016)

ACCOUNTING RESEARCH

Kausar et al., (2016) suggests that auditors are provided free hand to particularly books,

various accounts along with statements that can enable auditors to verify the same. In case if

they get satisfied then they can substantiate that the books are appropriately drawn up and

reflect a true as well as fair view of financial position of the corporation. As such, auditors

provide special attention to different directions of mistakes/errors that might be intentionally

or else unintentionally committed. However, the auditor can find out the unintentional

mistakes by way of vouching various business transactions and by way of comparing as well

as tallying different balances between as well as among different books of accounts.

Nonetheless, in case of intentional mistakes, errors can be categorised as frauds since it

directs the way towards defrauding different proprietors. Chen et al., (2016) recommends that

frauds can be recognized by way of detailed assessment of the books along with documents

namely cash books, various invoices, documents on wage sheet and many others.

Categories of audit

As suggested by Christensen et al., (2014), auditing can be categorised into two different

types namely continuous or else detailed audit and periodical/final audits. Lennox et al.,

(2016) suggests that continuous audit is necessarily effective in case of big business

enterprises with large corporations that have scope for maintaining the audit staff engaged

and business throughout the year. The auditors might perhaps attend to auditing at different

intervals that are fixed and carry out an interim audit. As such, in this specific case, routine

business operations can be carried out all at once with the work of audit. On the other hand,

the periodical auditing refers to a audit work that is carried out continuously till the period of

completion. As such, this can be regarded as the system that can be referred to be the most

satisfying from the viewpoint of the auditors (Gaynor et al., 2016)

9

ACCOUNTING RESEARCH

Audit Processes for detection of fraud

Badolato et al., (2014) says that there are various processes of audit that can help in detection

of fraud. Whilst audits are not formulated to root out all the possibilities of fraudulent actions,

assessors have the accountability to recognize material misstatements in financial assertions

of business enterprises caused by fraudulent actions or else error. As suggested by Brasel et

al., (2016), audit engagements teams have the need to undertake brainstorming sessions at the

start of audit. Essentially, this session directed by the partner liable for audit, is formulated to

deliver time for the entire audit team to take into account the way business enterprises can

commit fraud. In addition to this, brainstorming meeting can be necessarily utilized to

establish a specific tone of professional scepticism in the process of audit. In particular, fraud

specialist also attend meetings to deliver deep insight into different forms of fraud committed

by various business enterprises and recognizes diverse risk factors of the client. Audit process

also helps in the process of testing of audit. Detection of fraud of material misstatement in

financial statements calls for the need of undertaking adjustments in financial records

(Pucheta‐Martínez & García‐Meca, 2014). In this case, assessors would test the journal

entries of the firm for any kind of adjustments and manipulations. In addition to this, in a bid

to carry out the test, after acquiring a clear understanding regarding the controls as well as

procedures of the business enterprise, the evaluator has the need to select from the journal

entries of the business concern. Furthermore, auditors also have the need to typically choose

different entries that are particularly large and designed by upper management of firm and

posted in particular accounting period. Once the process of selections has been carried out,

the evaluator can think about presenting supporting documentation that can substantiate each

and every entry.

As suggested by Cohen et al., (2013), another probable place for fraudulent actions is in the

estimates for accounting. As accounting estimates are necessarily subjective concepts,

ACCOUNTING RESEARCH

Audit Processes for detection of fraud

Badolato et al., (2014) says that there are various processes of audit that can help in detection

of fraud. Whilst audits are not formulated to root out all the possibilities of fraudulent actions,

assessors have the accountability to recognize material misstatements in financial assertions

of business enterprises caused by fraudulent actions or else error. As suggested by Brasel et

al., (2016), audit engagements teams have the need to undertake brainstorming sessions at the

start of audit. Essentially, this session directed by the partner liable for audit, is formulated to

deliver time for the entire audit team to take into account the way business enterprises can

commit fraud. In addition to this, brainstorming meeting can be necessarily utilized to

establish a specific tone of professional scepticism in the process of audit. In particular, fraud

specialist also attend meetings to deliver deep insight into different forms of fraud committed

by various business enterprises and recognizes diverse risk factors of the client. Audit process

also helps in the process of testing of audit. Detection of fraud of material misstatement in

financial statements calls for the need of undertaking adjustments in financial records

(Pucheta‐Martínez & García‐Meca, 2014). In this case, assessors would test the journal

entries of the firm for any kind of adjustments and manipulations. In addition to this, in a bid

to carry out the test, after acquiring a clear understanding regarding the controls as well as

procedures of the business enterprise, the evaluator has the need to select from the journal

entries of the business concern. Furthermore, auditors also have the need to typically choose

different entries that are particularly large and designed by upper management of firm and

posted in particular accounting period. Once the process of selections has been carried out,

the evaluator can think about presenting supporting documentation that can substantiate each

and every entry.

As suggested by Cohen et al., (2013), another probable place for fraudulent actions is in the

estimates for accounting. As accounting estimates are necessarily subjective concepts,

10

ACCOUNTING RESEARCH

management might perhaps be able to exert influence overall accounting estimates for the

purpose of manipulations of the financial assertions. First, evaluators have the need to

complete an entire look back processes for the purpose of ascertainment in case if the

methods for completing accounting approximations has altered from previous years. Again,

alterations in the methods can be a sign of manipulation. Evaluators can also properly asses

overall directionality of approximations as a whole (Christ et al., 2015). For instance, in case

if around all the approximations in the previous years of declining earnings and

approximations in the present year were of declining earnings, assessors might perhaps be

concerned that the business enterprise is shifting overall earnings from a specific period to

another period.

Audit Committee

As rightly indicated by Abbott et al., (2010), audit committee is said to have the

accountability for carrying out the activities of hiring, assessment of performance and

compensating various external assessors in business entities. In addition to this, the audit

committee accountable for overseeing as well as supervising different financial assertions as

well as various disclosures of the corporation can help in maintenance of financial reporting

quality (Abbott et al., 2010). Essentially, audit committee formed in a specific business entity

can help in the process of tracking different selected policies, principles of accounting and

diverse internal controls that the management of business concerns have utilized.

As presented in the prior literature, audit committees of various business concerns have

contributed towards the process of enhancement of overall quality of firm’s financial

pronouncements (Hayes, 2014). Self-governing, competent, and qualified audit committees

have better capability to recognize material misstatements in particularly financial assertions,

and cam help in avoiding different opportunities of the management of the corporation to

ACCOUNTING RESEARCH

management might perhaps be able to exert influence overall accounting estimates for the

purpose of manipulations of the financial assertions. First, evaluators have the need to

complete an entire look back processes for the purpose of ascertainment in case if the

methods for completing accounting approximations has altered from previous years. Again,

alterations in the methods can be a sign of manipulation. Evaluators can also properly asses

overall directionality of approximations as a whole (Christ et al., 2015). For instance, in case

if around all the approximations in the previous years of declining earnings and

approximations in the present year were of declining earnings, assessors might perhaps be

concerned that the business enterprise is shifting overall earnings from a specific period to

another period.

Audit Committee

As rightly indicated by Abbott et al., (2010), audit committee is said to have the

accountability for carrying out the activities of hiring, assessment of performance and

compensating various external assessors in business entities. In addition to this, the audit

committee accountable for overseeing as well as supervising different financial assertions as

well as various disclosures of the corporation can help in maintenance of financial reporting

quality (Abbott et al., 2010). Essentially, audit committee formed in a specific business entity

can help in the process of tracking different selected policies, principles of accounting and

diverse internal controls that the management of business concerns have utilized.

As presented in the prior literature, audit committees of various business concerns have

contributed towards the process of enhancement of overall quality of firm’s financial

pronouncements (Hayes, 2014). Self-governing, competent, and qualified audit committees

have better capability to recognize material misstatements in particularly financial assertions,

and cam help in avoiding different opportunities of the management of the corporation to

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

ACCOUNTING RESEARCH

carry out manipulations. Therefore, audit committee of a business concern exerts

fundamental influences of quality of financial reporting along with inputs of audit. in addition

to this, alterations in the committee for audit governance can be linked to augmentation of

quality of financial reporting. Prior scholars have delivered specific substantiations that

recommend a relationship between existence of a financial expert on particularly committee

of audit and superior level of quality of financial reporting. Nevertheless, the significance of

including financial accounting expert in the firm’s committee for audit can help in leading to

superior quality of financial declarations (Chen et al., 2016). Thus, financial expertise might

perhaps be wide, and have the need to mention the significance of including financial

accounting specialist in the committee for audit. Essentially having a financial accounting

expert in the committee for audit can help in the process of the forecasting accurately.

Therefore, in this connection it can be said that there exists a positive association between

financial accounting expert and forecast accurateness. In addition to this, there is said to be a

negative association between qualified financial accounting specialist and the forecast

dispersion (Lisowsky et al., 2017).

As regards audit influences it can be mentioned that there exist a positive as well as

considerable influence on quality of financial reporting founded on overall size of auditing

corporations, fees disbursed to different external assessors.

Different advantages of auditing financial reports

As correctly mentioned by Lisowsky et al., (2017), auditing has different advantages that

helps in enhancement of overall quality of financial reporting. Sirois et al., (2018) suggest

that auditing facilitates the process of detection of errors as well as frauds with

recommendations for the prevention. However, in order to avert the mistakes to be

committed, the accounts can be maintained and upgraded on a regular basis. In addition to

ACCOUNTING RESEARCH

carry out manipulations. Therefore, audit committee of a business concern exerts

fundamental influences of quality of financial reporting along with inputs of audit. in addition

to this, alterations in the committee for audit governance can be linked to augmentation of

quality of financial reporting. Prior scholars have delivered specific substantiations that

recommend a relationship between existence of a financial expert on particularly committee

of audit and superior level of quality of financial reporting. Nevertheless, the significance of

including financial accounting expert in the firm’s committee for audit can help in leading to

superior quality of financial declarations (Chen et al., 2016). Thus, financial expertise might

perhaps be wide, and have the need to mention the significance of including financial

accounting specialist in the committee for audit. Essentially having a financial accounting

expert in the committee for audit can help in the process of the forecasting accurately.

Therefore, in this connection it can be said that there exists a positive association between

financial accounting expert and forecast accurateness. In addition to this, there is said to be a

negative association between qualified financial accounting specialist and the forecast

dispersion (Lisowsky et al., 2017).

As regards audit influences it can be mentioned that there exist a positive as well as

considerable influence on quality of financial reporting founded on overall size of auditing

corporations, fees disbursed to different external assessors.

Different advantages of auditing financial reports

As correctly mentioned by Lisowsky et al., (2017), auditing has different advantages that

helps in enhancement of overall quality of financial reporting. Sirois et al., (2018) suggest

that auditing facilitates the process of detection of errors as well as frauds with

recommendations for the prevention. However, in order to avert the mistakes to be

committed, the accounts can be maintained and upgraded on a regular basis. In addition to

12

ACCOUNTING RESEARCH

this, the parties in this case might also feel confident regarding report of the audit as it was

carried out by a specific independent individual or a body. Again, financial accounts after

audit stand to be authentic. As such, the people carrying out work of audit in the field of

accounts are qualified and proficient enough to deliver advice in the management of business

enterprises (DeFond et al., 2016). However, in case of joint stock corporations, the director of

the firm gets no opportunity of acquiring undue benefits. Apart from this, auditing accounts

also helps in the process of settlement among diverse parties.

Effectiveness of particularly internal auditing with regard to financial reporting

With the increasing complication of the necessities of financial reporting with regard to

internal control and management of risk and mounting pressure on board to comprehend the

wide range of value-added internal auditing actions in particularly governance, research

concentration has shifted to the empirical contributions of internal auditing (IA) and

recognizing criteria for analysis of performance of IA Robert (Knechel et al., 2015).

In an important body of research, it is necessarily documented that effectual internal audit

function is related to augmented financial reporting with respect to assurance regarding

quality of internal control in financial reporting, low levels of management of earnings and

low incidence of fraud. Robert Knechel et al., (2015) observed that internal audit function as

a vital mechanism to safeguard overall reliability of yearly accounts. Also, this study

reflected that executing IA as a specific function in particularly corporate governance and

their coordination with effectual audit committee could contribute towards minimization of

earnings management.

There are numerous scholars who have empirically confirmed the fact that dynamics

replicating positive influence of internal audits on the procedures of financial reporting.

Rezaee et al., (2018) suggests that corporate governance mainly relies on the definition of

ACCOUNTING RESEARCH

this, the parties in this case might also feel confident regarding report of the audit as it was

carried out by a specific independent individual or a body. Again, financial accounts after

audit stand to be authentic. As such, the people carrying out work of audit in the field of

accounts are qualified and proficient enough to deliver advice in the management of business

enterprises (DeFond et al., 2016). However, in case of joint stock corporations, the director of

the firm gets no opportunity of acquiring undue benefits. Apart from this, auditing accounts

also helps in the process of settlement among diverse parties.

Effectiveness of particularly internal auditing with regard to financial reporting

With the increasing complication of the necessities of financial reporting with regard to

internal control and management of risk and mounting pressure on board to comprehend the

wide range of value-added internal auditing actions in particularly governance, research

concentration has shifted to the empirical contributions of internal auditing (IA) and

recognizing criteria for analysis of performance of IA Robert (Knechel et al., 2015).

In an important body of research, it is necessarily documented that effectual internal audit

function is related to augmented financial reporting with respect to assurance regarding

quality of internal control in financial reporting, low levels of management of earnings and

low incidence of fraud. Robert Knechel et al., (2015) observed that internal audit function as

a vital mechanism to safeguard overall reliability of yearly accounts. Also, this study

reflected that executing IA as a specific function in particularly corporate governance and

their coordination with effectual audit committee could contribute towards minimization of

earnings management.

There are numerous scholars who have empirically confirmed the fact that dynamics

replicating positive influence of internal audits on the procedures of financial reporting.

Rezaee et al., (2018) suggests that corporate governance mainly relies on the definition of

13

ACCOUNTING RESEARCH

different role as well as accountabilities of internal audit function, suitable positioning and

lines of reporting along with professional proficiency. Furthermore, Pucheta‐Martínez &

García‐Meca (2014) emphasized the significance of training of different internal auditors as

per alterations in working procedures and the working environment. In addition to this,

awareness of the top management regarding significance of internal control and management

of risk for the successful management of the corporation has a vital role in ascertaining the

effectiveness of internal audit function. Again, more recurrent meetings particularly between

audit committee and the internal audit function can contribute towards exchange of pertinent

information and elaborate discussion regarding any issue identified in a well-timed manner

(Lisowsky et al., 2017).

Quality of financial reporting

As rightly indicated by Lennox et al., (2016), the primary purpose of general purpose

financial reporting is to deliver effective accounting information to different external users

for the purpose of economic decision making. Essentially, relevance as well as faithful

representation of particularly financial information that in itself reflect comparability,

timeliness, understandability as well as verifiability can make pecuniary reports effective to

different users. However, individual users have diverse perceptions regarding usefulness of

information along with their perceptions concerning quality of financial assertions. Therefore,

evaluating decision usefulness of diverse financial assertions cannot be observed directly

with straightforward process. Krishnan et al., (2016) mentioned that power of communication

of financial reports would not exclusively analyse as diversity of financial information

requests of a broad range of users of financial assertions. In addition to this, there is

subsistence of different alternatives of choice and engages accounting approximations along

with professional judgements in the reflection of the impacts of business transactions along

ACCOUNTING RESEARCH

different role as well as accountabilities of internal audit function, suitable positioning and

lines of reporting along with professional proficiency. Furthermore, Pucheta‐Martínez &

García‐Meca (2014) emphasized the significance of training of different internal auditors as

per alterations in working procedures and the working environment. In addition to this,

awareness of the top management regarding significance of internal control and management

of risk for the successful management of the corporation has a vital role in ascertaining the

effectiveness of internal audit function. Again, more recurrent meetings particularly between

audit committee and the internal audit function can contribute towards exchange of pertinent

information and elaborate discussion regarding any issue identified in a well-timed manner

(Lisowsky et al., 2017).

Quality of financial reporting

As rightly indicated by Lennox et al., (2016), the primary purpose of general purpose

financial reporting is to deliver effective accounting information to different external users

for the purpose of economic decision making. Essentially, relevance as well as faithful

representation of particularly financial information that in itself reflect comparability,

timeliness, understandability as well as verifiability can make pecuniary reports effective to

different users. However, individual users have diverse perceptions regarding usefulness of

information along with their perceptions concerning quality of financial assertions. Therefore,

evaluating decision usefulness of diverse financial assertions cannot be observed directly

with straightforward process. Krishnan et al., (2016) mentioned that power of communication

of financial reports would not exclusively analyse as diversity of financial information

requests of a broad range of users of financial assertions. In addition to this, there is

subsistence of different alternatives of choice and engages accounting approximations along

with professional judgements in the reflection of the impacts of business transactions along

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

ACCOUNTING RESEARCH

with incidents. Therefore, illustrating determinants of quality of particularly financial

information and the manner of quantification can be considered to be fundamental areas of

concern in research on accounting.

As rightly put forward by Kausar et al., (2016), majority of empirical studies intended to

evaluate decision usefulness of pecuniary reports utilizing quantitative dimensions that

concentrate on particular attributes of financial reporting dimensions. Essentially, the

instances of such facets are quality of earnings, specific proxies of value relevance, particular

financial/non financial information divulged in the yearly reports. Conversely, Hayes (2014)

suggests that diverse dimensions of specific information utilizing financial/non financial

along with mandatory as well as voluntary disclosures in pecuniary assertions of corporations

have the need to be analysed simultaneously for suitable analysis of decision usefulness of

financial reporting information. Therefore, they made use of conceptual based tools of

measurement for mainly comprehensive analysis of financial reporting quality. However, in

this regard, it can be said that the scholars have formulated a quality index consisting of 21

items with respect to fundamental as well as enhancing features presented in the conceptual

framework of International Auditing Standards Board. In essence, this tactic of enumerating

financial reporting quality can be used (Gaynor et al., 2016).

Audit Quality and Quality of Financial Reporting

The worldwide financial crisis, failures of corporate and scams in numerous nations raise

noteworthy questions regarding the efficacy of financial reporting as well as quality of

auditing. Several auditing firms, certified and regulatory bodies are therefore under fire and

encounter immense pressures to refurbish confidence in particularly auditing. In essence,

regulatory and certified bodies attempted to uphold quality of audit to restore tarnished image

as well as to enhance their legitimacy along with standing (Abbott et al., 2016). Thus, it is

ACCOUNTING RESEARCH

with incidents. Therefore, illustrating determinants of quality of particularly financial

information and the manner of quantification can be considered to be fundamental areas of

concern in research on accounting.

As rightly put forward by Kausar et al., (2016), majority of empirical studies intended to

evaluate decision usefulness of pecuniary reports utilizing quantitative dimensions that

concentrate on particular attributes of financial reporting dimensions. Essentially, the

instances of such facets are quality of earnings, specific proxies of value relevance, particular

financial/non financial information divulged in the yearly reports. Conversely, Hayes (2014)

suggests that diverse dimensions of specific information utilizing financial/non financial

along with mandatory as well as voluntary disclosures in pecuniary assertions of corporations

have the need to be analysed simultaneously for suitable analysis of decision usefulness of

financial reporting information. Therefore, they made use of conceptual based tools of

measurement for mainly comprehensive analysis of financial reporting quality. However, in

this regard, it can be said that the scholars have formulated a quality index consisting of 21

items with respect to fundamental as well as enhancing features presented in the conceptual

framework of International Auditing Standards Board. In essence, this tactic of enumerating

financial reporting quality can be used (Gaynor et al., 2016).

Audit Quality and Quality of Financial Reporting

The worldwide financial crisis, failures of corporate and scams in numerous nations raise

noteworthy questions regarding the efficacy of financial reporting as well as quality of

auditing. Several auditing firms, certified and regulatory bodies are therefore under fire and

encounter immense pressures to refurbish confidence in particularly auditing. In essence,

regulatory and certified bodies attempted to uphold quality of audit to restore tarnished image

as well as to enhance their legitimacy along with standing (Abbott et al., 2016). Thus, it is

15

ACCOUNTING RESEARCH

anticipated that superior audit quality directs the way towards superior quality of financial

reporting that subsequently is a mechanism to avert financial crises. Abbott et al., (2010)

identify quality of financial reporting as particularly a precision with which different

pecuniary assertion conveys required information regarding operations of the firm,

specifically its anticipated flows of cash that let equity investors know about financial health

of the firm. Also, their characterization is consistent with directives laid down by Financial

Accounting Standards Board (FASB) that mentions that the main objective of financial

assertions is to notify present as well as potential financiers so that they can frame rational

decisions as regards investment and can evaluate the anticipated flows of cash of the

reporting entity (Aobdia et al., 2015).

Nevertheless, quality of audit is not openly observable; for that reason, it is quite complicated

to assess and quantify the same empirically. Yet, there are several proxies to enumerate

quality of audit. Fundamentally, accrual measure can be considered to be one of most

important proxies for ascertainment of quality of audit. Superior quality assessors are more

probable to identify irregularities in accounting, oppose to the employment of different

questionable practices of accounting, as well as restrain discretion specifically over accrual

choices for diverse client corporations (Badolato et al., 2014). As rightly indicated by Berger

et al., (2017), there are five different theoretical constructs that can be used to examine audit

quality. These five different constructs that can be used for assessment of quality of audit

include audit size, audit tenure (experience of auditor, that is to say, industry specialism),

and fees for audit, specific demographics, and category of local government. Bowlin et al.,

(2015) highlights that that there are two important characteristics of the financial reporting

arrangement are that an appraisal is particularly mandated for different publicly traded

corporations. Fundamentally, audit needs to be carried out by professional and expert

accountants who are necessarily independent in nature (that is to say, to have a specific

ACCOUNTING RESEARCH

anticipated that superior audit quality directs the way towards superior quality of financial

reporting that subsequently is a mechanism to avert financial crises. Abbott et al., (2010)

identify quality of financial reporting as particularly a precision with which different

pecuniary assertion conveys required information regarding operations of the firm,

specifically its anticipated flows of cash that let equity investors know about financial health

of the firm. Also, their characterization is consistent with directives laid down by Financial

Accounting Standards Board (FASB) that mentions that the main objective of financial

assertions is to notify present as well as potential financiers so that they can frame rational

decisions as regards investment and can evaluate the anticipated flows of cash of the

reporting entity (Aobdia et al., 2015).

Nevertheless, quality of audit is not openly observable; for that reason, it is quite complicated

to assess and quantify the same empirically. Yet, there are several proxies to enumerate

quality of audit. Fundamentally, accrual measure can be considered to be one of most

important proxies for ascertainment of quality of audit. Superior quality assessors are more

probable to identify irregularities in accounting, oppose to the employment of different

questionable practices of accounting, as well as restrain discretion specifically over accrual

choices for diverse client corporations (Badolato et al., 2014). As rightly indicated by Berger

et al., (2017), there are five different theoretical constructs that can be used to examine audit

quality. These five different constructs that can be used for assessment of quality of audit

include audit size, audit tenure (experience of auditor, that is to say, industry specialism),

and fees for audit, specific demographics, and category of local government. Bowlin et al.,

(2015) highlights that that there are two important characteristics of the financial reporting

arrangement are that an appraisal is particularly mandated for different publicly traded

corporations. Fundamentally, audit needs to be carried out by professional and expert

accountants who are necessarily independent in nature (that is to say, to have a specific

16

ACCOUNTING RESEARCH

objective in mind) and in appearance as well. In itself, both of these magnitudes of

independence can be assumed to be vital for purpose of attainment of superior quality of

audit.

Brasel et al., (2016) suggests that quality of audit refers to appropriate detection, correction

as well as revelation of any kind of material omission else wise misstatements particularly in

the financial assertions. In this regard, Carcello & Nagy (2014) mention that a two-

dimensional illustration of quality of audit hypothesized has set a standard for discussing this

specific issue. Chen et al., (2016) says that a material misstatement essentially needs to be

identified, as well as the detected material misstatement also needs to be appropriately

reported. As per the viewpoints of Christ et al., (2015) there are two different major drivers of

quality of audit, counting costs of litigation as well as loss of reputation. DeFond et al.,

(2016) argue that taking into consideration huge investment on developing reputation as well

as brand equity, the big audit corporations undoubtedly have an inducement to lessen

litigation risk and defend reputational capital by means of delivering more convincing and

trustworthy financial assertions. Basically, these arguments can be considered to be

consistent with the theme that size of the audit firm can be regarded to be a crucial

determinant of quality of audit. Essentially, huge size of audit corporations has two different

consequences. As such, large sized audit firms facilitate audit corporations to spend

considerable amount of money on different training programmes and enhancement of

technology used for audit. Essentially, this can help in enhancing their level of competence,

and enable to resist pressure of auditee to present a clean opinion in audit as they are not

reliant on any specific individual client.

Research Methodology

ACCOUNTING RESEARCH

objective in mind) and in appearance as well. In itself, both of these magnitudes of

independence can be assumed to be vital for purpose of attainment of superior quality of

audit.

Brasel et al., (2016) suggests that quality of audit refers to appropriate detection, correction

as well as revelation of any kind of material omission else wise misstatements particularly in

the financial assertions. In this regard, Carcello & Nagy (2014) mention that a two-

dimensional illustration of quality of audit hypothesized has set a standard for discussing this

specific issue. Chen et al., (2016) says that a material misstatement essentially needs to be

identified, as well as the detected material misstatement also needs to be appropriately

reported. As per the viewpoints of Christ et al., (2015) there are two different major drivers of

quality of audit, counting costs of litigation as well as loss of reputation. DeFond et al.,

(2016) argue that taking into consideration huge investment on developing reputation as well

as brand equity, the big audit corporations undoubtedly have an inducement to lessen

litigation risk and defend reputational capital by means of delivering more convincing and

trustworthy financial assertions. Basically, these arguments can be considered to be

consistent with the theme that size of the audit firm can be regarded to be a crucial

determinant of quality of audit. Essentially, huge size of audit corporations has two different

consequences. As such, large sized audit firms facilitate audit corporations to spend

considerable amount of money on different training programmes and enhancement of

technology used for audit. Essentially, this can help in enhancing their level of competence,

and enable to resist pressure of auditee to present a clean opinion in audit as they are not

reliant on any specific individual client.

Research Methodology

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17

ACCOUNTING RESEARCH

This section elucidates in detail about the research design together with the research

methodology used for the research project.

Research design

The current study has undertaken a descriptive research design that presents a complete set of

mechanisms along with processes that explains variables while postulates that a specific

descriptive design of a research is basically concerned with method of determination of

frequency with which specific things are associated between different variables (Gaynor et

al., 2016).

Target Population

Particularly, the population that is of interest in this study at hand contains different business

corporations operating in Australia.

Data Collection

The learner has employed both secondary data as well as primary data for undertaking this

research. Essentially, primary data is collected from people working in corporations listed

under the Australian Stock Exchange by using a questionnaire. Essentially, questionnaires are

distributed to 50 chief financial officer as well as chief executive officer or else individuals

operating in equivalent positions with a request for response. The questionnaire (refer to

appendix) containing pertinent questions are mailed to the target respondents with a request

for reply. The responses to the questionnaire framed are rated on a 5 point likert scale. The

responses range between Strongly Agree (numerically rated as 5), Agree (rated as 4), Neutral

(Rated as 3), Disagree (rated as 2) and Strongly Disagree (rated as 1). The responses

collected are thereafter analysed using the software Microsoft excel.

ACCOUNTING RESEARCH

This section elucidates in detail about the research design together with the research

methodology used for the research project.

Research design

The current study has undertaken a descriptive research design that presents a complete set of

mechanisms along with processes that explains variables while postulates that a specific

descriptive design of a research is basically concerned with method of determination of

frequency with which specific things are associated between different variables (Gaynor et

al., 2016).

Target Population

Particularly, the population that is of interest in this study at hand contains different business

corporations operating in Australia.

Data Collection

The learner has employed both secondary data as well as primary data for undertaking this

research. Essentially, primary data is collected from people working in corporations listed

under the Australian Stock Exchange by using a questionnaire. Essentially, questionnaires are

distributed to 50 chief financial officer as well as chief executive officer or else individuals

operating in equivalent positions with a request for response. The questionnaire (refer to

appendix) containing pertinent questions are mailed to the target respondents with a request

for reply. The responses to the questionnaire framed are rated on a 5 point likert scale. The

responses range between Strongly Agree (numerically rated as 5), Agree (rated as 4), Neutral

(Rated as 3), Disagree (rated as 2) and Strongly Disagree (rated as 1). The responses

collected are thereafter analysed using the software Microsoft excel.

18

ACCOUNTING RESEARCH

Basically, these can be regarded as the individuals directly engaged in dealing with different

financial facets in the firms (Hayes, 2014). Additionally, secondary data is collected from

yearly audited reports declared by the corporations, various official websites, prior academic

journals, article, magazines as well as report.

Qualitative Analysis technique of collected data

Analysis of Prior cases

As correctly mentioned by Hayes (2014), the typical agency issue existent between

shareholders as well as corporate managers endorses the hiring of different assessors to

deliver independent assurance to varied financiers that the financial assertions of reporting

entities is as per respective regulatory directives. Nevertheless, worldwide financial crisis,

corporate collapse and financial scams in different nations raised concerns and doubts

regarding efficacy of auditing. However, several attempts have been made to reinstate

confidence in work of audit by means of diverse regulatory actions. In essence, passage of

different Acts is believed to enhance quality of audit. For instance, Hayes (2014) observe that

the course of SOX directs the way to sharp decline in the total number of small sized audit

corporations functioning in the market. As per reports, it can be hereby mentioned that

approximately 50%, that is around 607 out of 1,233 small sized audit corporations that were

on the go during the period 2001 to 2008 exited to all intents and purposes the market and

records mention that most of these exits happened during the period 2002 to 2004, concurring

particularly with passage of rules of SOX, along with the advent of registrations rules of

PCAOB, and commencement of inspections (Kausar et al., 2016). Analysis of this specific

case also reveals that existence of smaller number of small sized assessors concurs with a

doubling of particularly mean number of clientele of every small sized audit corporations.

Therefore, they register a considerable transformation in the overall market composition of

ACCOUNTING RESEARCH

Basically, these can be regarded as the individuals directly engaged in dealing with different

financial facets in the firms (Hayes, 2014). Additionally, secondary data is collected from

yearly audited reports declared by the corporations, various official websites, prior academic

journals, article, magazines as well as report.

Qualitative Analysis technique of collected data

Analysis of Prior cases

As correctly mentioned by Hayes (2014), the typical agency issue existent between

shareholders as well as corporate managers endorses the hiring of different assessors to

deliver independent assurance to varied financiers that the financial assertions of reporting

entities is as per respective regulatory directives. Nevertheless, worldwide financial crisis,

corporate collapse and financial scams in different nations raised concerns and doubts

regarding efficacy of auditing. However, several attempts have been made to reinstate

confidence in work of audit by means of diverse regulatory actions. In essence, passage of

different Acts is believed to enhance quality of audit. For instance, Hayes (2014) observe that

the course of SOX directs the way to sharp decline in the total number of small sized audit

corporations functioning in the market. As per reports, it can be hereby mentioned that

approximately 50%, that is around 607 out of 1,233 small sized audit corporations that were

on the go during the period 2001 to 2008 exited to all intents and purposes the market and

records mention that most of these exits happened during the period 2002 to 2004, concurring

particularly with passage of rules of SOX, along with the advent of registrations rules of

PCAOB, and commencement of inspections (Kausar et al., 2016). Analysis of this specific

case also reveals that existence of smaller number of small sized assessors concurs with a

doubling of particularly mean number of clientele of every small sized audit corporations.

Therefore, they register a considerable transformation in the overall market composition of

19

ACCOUNTING RESEARCH

small sized assessors after the process of adoption of particularly SOX. Further, they also

argue that inferior quality assessors are more probable to consider it to be more cost

beneficial, specifically at the margin, to walk out the market for mainly public corporation

audits for the fresh regulatory environment executed under SOX. Analysis of the present case

reflected the fact that the passage of specific Acts enhanced quality of audit in case if size of

audit was thought to be a specific proxy for quality of assessment. Furthermore, Kausar et al.,

(2016) mentions that it is anticipated that superior audit quality show the way to superior

quality of financial reporting. Nevertheless, the passage of Acts can be considered to be an

important factor that leads to enhancement of overall quality of preparation as well as

presentation of financial assertions.

As rightly put forward by Gaynor et al., (2016) perceptions regarding credit analysts as well

as financial analysts in connection with association between efficacy of audit committee,

auditing firm size and as well as quality can be considered by studying the same in context of

Bahrain. The case on Bahrain shows that results by survey of around 300 credit analysts as

well as financial analysts. This study throws light on four major findings. The case highlights

the finding that both credits with financial analysts perceive trustworthiness and reliability of

financial statements to be a function of the size of the auditing firm. The findings of the prior

study conducted reflect the fact that both the groups suppose that the features of Big-Four

accounting units permit them to deliver superior-quality assertions than varied non-Big

accounting corporations (Lennox et al., 2016). Also, findings of the study suggest that non-

audit services exert impact on independence of auditor and thereby impair quality of audit. In

addition to this, findings of prior research study also suggest that there are large groups of

analysts who are of the view that effectual audit committee can augment overall quality of

audit assertions. Furthermore, financial analysts also perceive pecuniary pronouncements to

be more plausible in comparison to different credit analysts. Lennox et al., (2016) state that

ACCOUNTING RESEARCH

small sized assessors after the process of adoption of particularly SOX. Further, they also

argue that inferior quality assessors are more probable to consider it to be more cost

beneficial, specifically at the margin, to walk out the market for mainly public corporation

audits for the fresh regulatory environment executed under SOX. Analysis of the present case

reflected the fact that the passage of specific Acts enhanced quality of audit in case if size of

audit was thought to be a specific proxy for quality of assessment. Furthermore, Kausar et al.,

(2016) mentions that it is anticipated that superior audit quality show the way to superior

quality of financial reporting. Nevertheless, the passage of Acts can be considered to be an

important factor that leads to enhancement of overall quality of preparation as well as

presentation of financial assertions.

As rightly put forward by Gaynor et al., (2016) perceptions regarding credit analysts as well

as financial analysts in connection with association between efficacy of audit committee,

auditing firm size and as well as quality can be considered by studying the same in context of

Bahrain. The case on Bahrain shows that results by survey of around 300 credit analysts as

well as financial analysts. This study throws light on four major findings. The case highlights

the finding that both credits with financial analysts perceive trustworthiness and reliability of

financial statements to be a function of the size of the auditing firm. The findings of the prior

study conducted reflect the fact that both the groups suppose that the features of Big-Four

accounting units permit them to deliver superior-quality assertions than varied non-Big

accounting corporations (Lennox et al., 2016). Also, findings of the study suggest that non-

audit services exert impact on independence of auditor and thereby impair quality of audit. In

addition to this, findings of prior research study also suggest that there are large groups of

analysts who are of the view that effectual audit committee can augment overall quality of

audit assertions. Furthermore, financial analysts also perceive pecuniary pronouncements to

be more plausible in comparison to different credit analysts. Lennox et al., (2016) state that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20

ACCOUNTING RESEARCH

results of the survey regarding the associations between different auditor mergers, quality of

audit as well as audit fees. Enumerating quality of audit by means of earnings quality of

different clientele they necessarily reflect in the period of post-merger, complete

discretionary accruals of different big-X customer firms declined in comparison to different

non-big-X client corporations, reflecting less amount of management of earnings. Also, these

indicate that during the postmerger period, proceeds of different big-X clients are necessarily

more linked to different stock-market returns, reflecting that quality of income has enhanced

during this period.

Quantitative Analysis technique of collected data

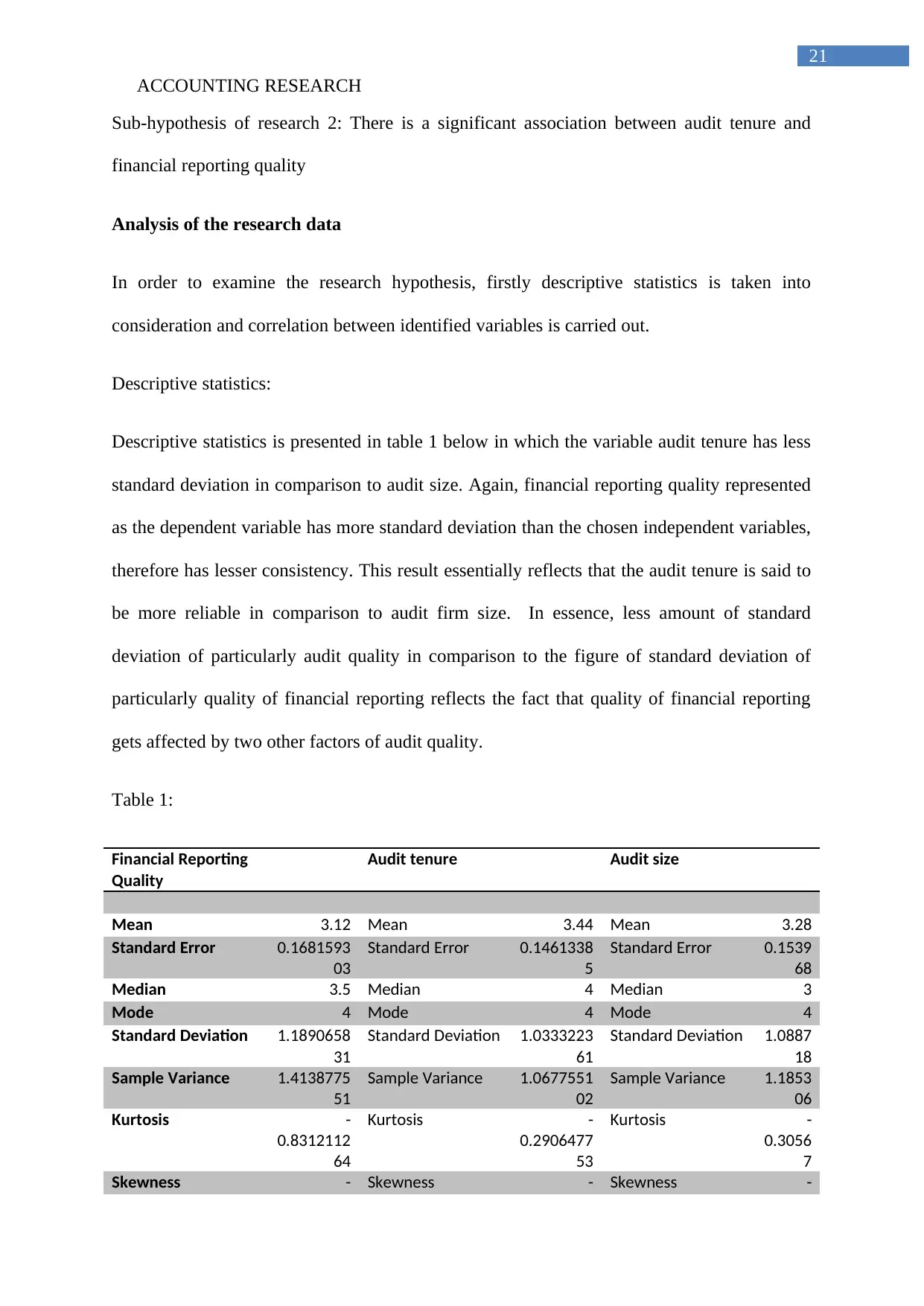

Correlation analysis is used for evaluation of gathered data. In essence, the current study at

hand is both quantitative as well as qualitative in nature. For the purpose of the present study,

quality of audit is regarded as the independent variable and financial reporting quality as the

particular independent variable.

For the purpose of the present study, the variables that are considered for measurement of

audit quality include size of the auditor and tenure of the auditor. In order to examine the