Audit Report on Alice Queen Limited

VerifiedAdded on 2023/06/12

|14

|3349

|77

AI Summary

This audit report provides insights into the financial performance and position of Alice Queen Limited, an exploration company listed on the Australian Stock Exchange. The report covers investment and finance activities, financial reporting practices, and performance of analytic procedures on the financial statements. The report also discusses the materiality of various accounts, including inventory, receivables, plant and equipment, trade and other payables, cash and cash equivalents, investments, exploration and evaluation expenditure, pre-payments, and security deposits.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDIT

Audit

Name of the Student:

Name of the University:

Authors Note:

Audit

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

AUDIT

Table of Contents

Introduction:...............................................................................................................................2

Nature of the entity:...................................................................................................................2

Business operations:...............................................................................................................2

Investment and investment activities:....................................................................................3

Finance and the financing activities:......................................................................................4

Financial reporting practices:.................................................................................................5

Performance of Analytic procedures on the financial statement of the company:....................5

Ascertainment of the materiality of the accounts of the company:............................................7

Conclusion:..............................................................................................................................12

Reference..................................................................................................................................13

AUDIT

Table of Contents

Introduction:...............................................................................................................................2

Nature of the entity:...................................................................................................................2

Business operations:...............................................................................................................2

Investment and investment activities:....................................................................................3

Finance and the financing activities:......................................................................................4

Financial reporting practices:.................................................................................................5

Performance of Analytic procedures on the financial statement of the company:....................5

Ascertainment of the materiality of the accounts of the company:............................................7

Conclusion:..............................................................................................................................12

Reference..................................................................................................................................13

2

AUDIT

Introduction:

In the present report, an effort has been made towards developing an understanding of

the financial performance and the financial positon of the company. The understanding

regarding the financial positon and the performance of the company will be developed with

the help of the financial statements that have been prepared and presented by the company.

After the analysis of the financial statements of the company is carried out, the relevance of

the various matters that have been stated out in it in respect of the materiality in the audit

procedure to be conducted by the auditor will be ascertained (Australia and Australia 2015).

The factors that were being considered for categorising a particular account as material will

be discussed in detail. The material relevance of around 10 accounts will be computed and

the materiality in respect of each FO the accounts will be determined objectively.

The company that has been selected for conducting the following presentation is Alice

Queen Limited. The company has its listing on the Australian Stock Exchange. The company

is engaged in the business of exploration and has the majority interest in two projects that are

located in Torres Strait Queensland and Menorah copper (Redfern et al. 2014).

Nature of the entity:

Business operations:

The company is engaged in the activities that are concerned with the exploration and the

extraction of the various minerals by the company. Some FO the most significant business

projects that are presently held by the company and on which the activities have commenced

are continuing are as follows:

a) Horn Island:

For the present reporting period, the Group commenced its phase 2 Exploration

program that is situated in the Horn Island. In pursuance of that, the entity embarked

AUDIT

Introduction:

In the present report, an effort has been made towards developing an understanding of

the financial performance and the financial positon of the company. The understanding

regarding the financial positon and the performance of the company will be developed with

the help of the financial statements that have been prepared and presented by the company.

After the analysis of the financial statements of the company is carried out, the relevance of

the various matters that have been stated out in it in respect of the materiality in the audit

procedure to be conducted by the auditor will be ascertained (Australia and Australia 2015).

The factors that were being considered for categorising a particular account as material will

be discussed in detail. The material relevance of around 10 accounts will be computed and

the materiality in respect of each FO the accounts will be determined objectively.

The company that has been selected for conducting the following presentation is Alice

Queen Limited. The company has its listing on the Australian Stock Exchange. The company

is engaged in the business of exploration and has the majority interest in two projects that are

located in Torres Strait Queensland and Menorah copper (Redfern et al. 2014).

Nature of the entity:

Business operations:

The company is engaged in the activities that are concerned with the exploration and the

extraction of the various minerals by the company. Some FO the most significant business

projects that are presently held by the company and on which the activities have commenced

are continuing are as follows:

a) Horn Island:

For the present reporting period, the Group commenced its phase 2 Exploration

program that is situated in the Horn Island. In pursuance of that, the entity embarked

3

AUDIT

itself on an extensive geological mapping and sampling program that was conducted

in the Horn Island (Harish et al. 2015). The main purpose of these activates was to

determine the scope and the scale of the Horn Island Mineral Field and to

significantly firm up the target in respect of the further drilling that were to be

conducted by the company just outside the present area wherein the company is

conducting its exploration activities.

b) New South Wales(Looking Glass EL 8225):

In the month of October, the company announced that operations regarding the

drilling have been commenced in respect of its Looking Glass project on the Moong

Volcanic Belt of NSW (Gibberd et al. 2016). The drilling project of the company

involves the drilling of two deep diamond core holes that are being respectively

directed towards two different magnetic anomalies.

Investment and investment activities:

The constituents of the investing activities are as follows:

a) Payments that are being made by the company in respect of the exploration evaluation

expenditure: this item represents the amount that is paid by the company in respect of

the various exploration that are being conducted by the company these are considered

to be investing activities because the company has to incur all these for the purpose of

generation of revenue in the future (Campbell et al. 2015).

b) Property, plant and equipment:

This represents that amount that the company has to incur for the purpose of purchase

of property plant and equipment that are going to be used by the company for carrying

out its everyday activities.

c) Payments for the security deposits:

AUDIT

itself on an extensive geological mapping and sampling program that was conducted

in the Horn Island (Harish et al. 2015). The main purpose of these activates was to

determine the scope and the scale of the Horn Island Mineral Field and to

significantly firm up the target in respect of the further drilling that were to be

conducted by the company just outside the present area wherein the company is

conducting its exploration activities.

b) New South Wales(Looking Glass EL 8225):

In the month of October, the company announced that operations regarding the

drilling have been commenced in respect of its Looking Glass project on the Moong

Volcanic Belt of NSW (Gibberd et al. 2016). The drilling project of the company

involves the drilling of two deep diamond core holes that are being respectively

directed towards two different magnetic anomalies.

Investment and investment activities:

The constituents of the investing activities are as follows:

a) Payments that are being made by the company in respect of the exploration evaluation

expenditure: this item represents the amount that is paid by the company in respect of

the various exploration that are being conducted by the company these are considered

to be investing activities because the company has to incur all these for the purpose of

generation of revenue in the future (Campbell et al. 2015).

b) Property, plant and equipment:

This represents that amount that the company has to incur for the purpose of purchase

of property plant and equipment that are going to be used by the company for carrying

out its everyday activities.

c) Payments for the security deposits:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

AUDIT

This amount is being incurred by the company in respect of the various payments that

are being made by the company in respect of the security deposits to different

suppliers of the company.

d) Cash and cash equivalent that have been acquired on acquisition:

This represents that amount that is present with the company as cash and cash

equivalents that has been received by the company from the various acquisitions that

have been made by the company.

Finance and the financing activities:

The finance activities are those activities that are concerned with the collection of the funds

required by the company for carrying out its commercial activities. The finance activities that

are conducted by the company are as follows:

a) Proceeds from the issue of the shares:

This represents the amount that has been arranged by the company from the issue of

the equity shares of the company to the equity shareholders of the company.

b) Payments for share issue costs:

This represents that amount that has been paid by the company in respect of the shares

that were being issued by it.

c) Proceeds from the borrowings:

This represents the amount that has been arranged by the company from the third

parties in the nature of loan, borrowed funds in respect of which the company will

have to pay regular interest, and needs to repay back the amount that had been

borrowed by the company (Clark et al. 2015).

AUDIT

This amount is being incurred by the company in respect of the various payments that

are being made by the company in respect of the security deposits to different

suppliers of the company.

d) Cash and cash equivalent that have been acquired on acquisition:

This represents that amount that is present with the company as cash and cash

equivalents that has been received by the company from the various acquisitions that

have been made by the company.

Finance and the financing activities:

The finance activities are those activities that are concerned with the collection of the funds

required by the company for carrying out its commercial activities. The finance activities that

are conducted by the company are as follows:

a) Proceeds from the issue of the shares:

This represents the amount that has been arranged by the company from the issue of

the equity shares of the company to the equity shareholders of the company.

b) Payments for share issue costs:

This represents that amount that has been paid by the company in respect of the shares

that were being issued by it.

c) Proceeds from the borrowings:

This represents the amount that has been arranged by the company from the third

parties in the nature of loan, borrowed funds in respect of which the company will

have to pay regular interest, and needs to repay back the amount that had been

borrowed by the company (Clark et al. 2015).

5

AUDIT

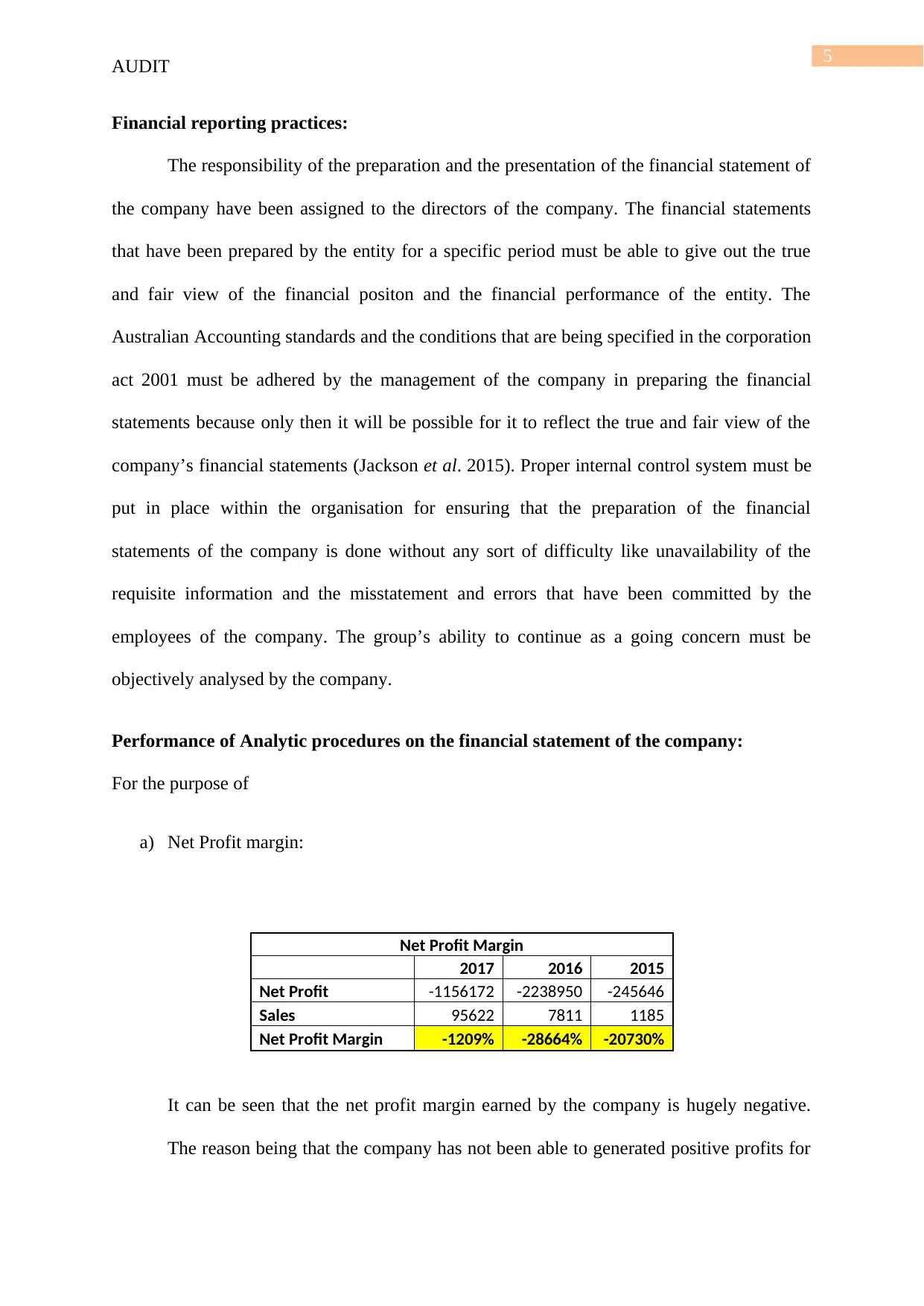

Financial reporting practices:

The responsibility of the preparation and the presentation of the financial statement of

the company have been assigned to the directors of the company. The financial statements

that have been prepared by the entity for a specific period must be able to give out the true

and fair view of the financial positon and the financial performance of the entity. The

Australian Accounting standards and the conditions that are being specified in the corporation

act 2001 must be adhered by the management of the company in preparing the financial

statements because only then it will be possible for it to reflect the true and fair view of the

company’s financial statements (Jackson et al. 2015). Proper internal control system must be

put in place within the organisation for ensuring that the preparation of the financial

statements of the company is done without any sort of difficulty like unavailability of the

requisite information and the misstatement and errors that have been committed by the

employees of the company. The group’s ability to continue as a going concern must be

objectively analysed by the company.

Performance of Analytic procedures on the financial statement of the company:

For the purpose of

a) Net Profit margin:

Net Profit Margin

2017 2016 2015

Net Profit -1156172 -2238950 -245646

Sales 95622 7811 1185

Net Profit Margin -1209% -28664% -20730%

It can be seen that the net profit margin earned by the company is hugely negative.

The reason being that the company has not been able to generated positive profits for

AUDIT

Financial reporting practices:

The responsibility of the preparation and the presentation of the financial statement of

the company have been assigned to the directors of the company. The financial statements

that have been prepared by the entity for a specific period must be able to give out the true

and fair view of the financial positon and the financial performance of the entity. The

Australian Accounting standards and the conditions that are being specified in the corporation

act 2001 must be adhered by the management of the company in preparing the financial

statements because only then it will be possible for it to reflect the true and fair view of the

company’s financial statements (Jackson et al. 2015). Proper internal control system must be

put in place within the organisation for ensuring that the preparation of the financial

statements of the company is done without any sort of difficulty like unavailability of the

requisite information and the misstatement and errors that have been committed by the

employees of the company. The group’s ability to continue as a going concern must be

objectively analysed by the company.

Performance of Analytic procedures on the financial statement of the company:

For the purpose of

a) Net Profit margin:

Net Profit Margin

2017 2016 2015

Net Profit -1156172 -2238950 -245646

Sales 95622 7811 1185

Net Profit Margin -1209% -28664% -20730%

It can be seen that the net profit margin earned by the company is hugely negative.

The reason being that the company has not been able to generated positive profits for

6

AUDIT

any of the year. However, the sales of the company are increasing over the periods.

The huge negative figure is the result of the initial expenditure that is to be incurred

by the company for exploration of the resources.

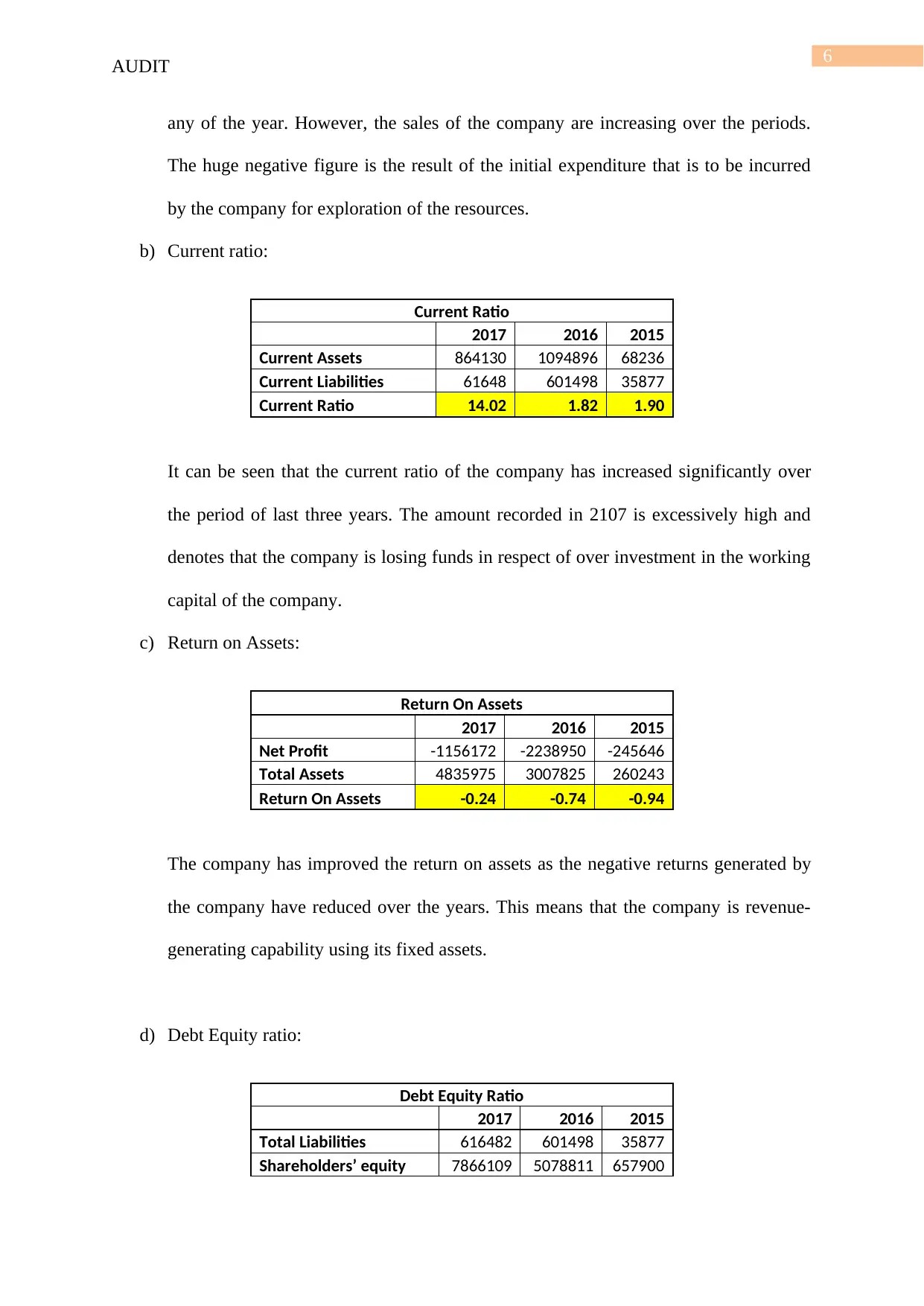

b) Current ratio:

Current Ratio

2017 2016 2015

Current Assets 864130 1094896 68236

Current Liabilities 61648 601498 35877

Current Ratio 14.02 1.82 1.90

It can be seen that the current ratio of the company has increased significantly over

the period of last three years. The amount recorded in 2107 is excessively high and

denotes that the company is losing funds in respect of over investment in the working

capital of the company.

c) Return on Assets:

Return On Assets

2017 2016 2015

Net Profit -1156172 -2238950 -245646

Total Assets 4835975 3007825 260243

Return On Assets -0.24 -0.74 -0.94

The company has improved the return on assets as the negative returns generated by

the company have reduced over the years. This means that the company is revenue-

generating capability using its fixed assets.

d) Debt Equity ratio:

Debt Equity Ratio

2017 2016 2015

Total Liabilities 616482 601498 35877

Shareholders’ equity 7866109 5078811 657900

AUDIT

any of the year. However, the sales of the company are increasing over the periods.

The huge negative figure is the result of the initial expenditure that is to be incurred

by the company for exploration of the resources.

b) Current ratio:

Current Ratio

2017 2016 2015

Current Assets 864130 1094896 68236

Current Liabilities 61648 601498 35877

Current Ratio 14.02 1.82 1.90

It can be seen that the current ratio of the company has increased significantly over

the period of last three years. The amount recorded in 2107 is excessively high and

denotes that the company is losing funds in respect of over investment in the working

capital of the company.

c) Return on Assets:

Return On Assets

2017 2016 2015

Net Profit -1156172 -2238950 -245646

Total Assets 4835975 3007825 260243

Return On Assets -0.24 -0.74 -0.94

The company has improved the return on assets as the negative returns generated by

the company have reduced over the years. This means that the company is revenue-

generating capability using its fixed assets.

d) Debt Equity ratio:

Debt Equity Ratio

2017 2016 2015

Total Liabilities 616482 601498 35877

Shareholders’ equity 7866109 5078811 657900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT

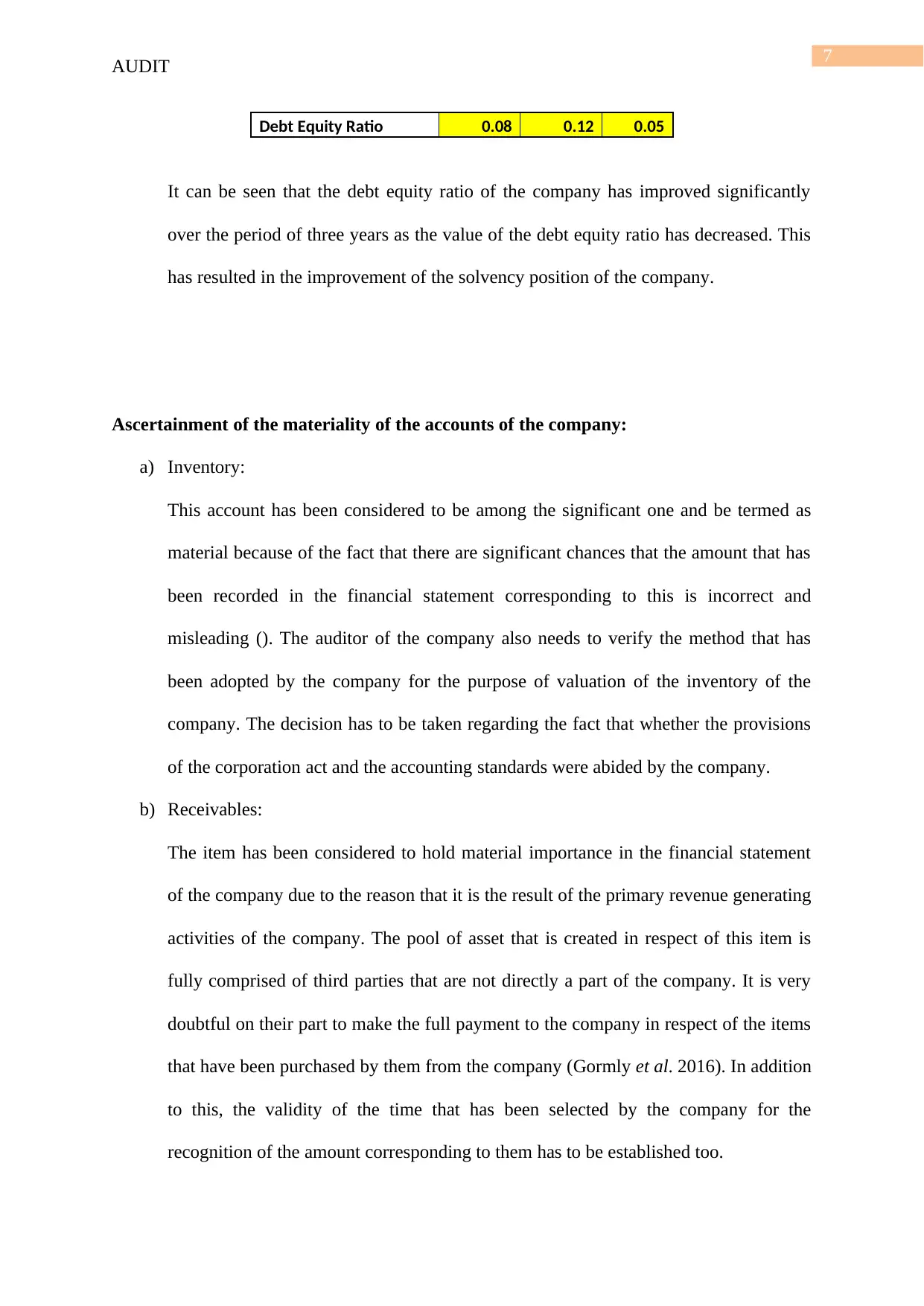

Debt Equity Ratio 0.08 0.12 0.05

It can be seen that the debt equity ratio of the company has improved significantly

over the period of three years as the value of the debt equity ratio has decreased. This

has resulted in the improvement of the solvency position of the company.

Ascertainment of the materiality of the accounts of the company:

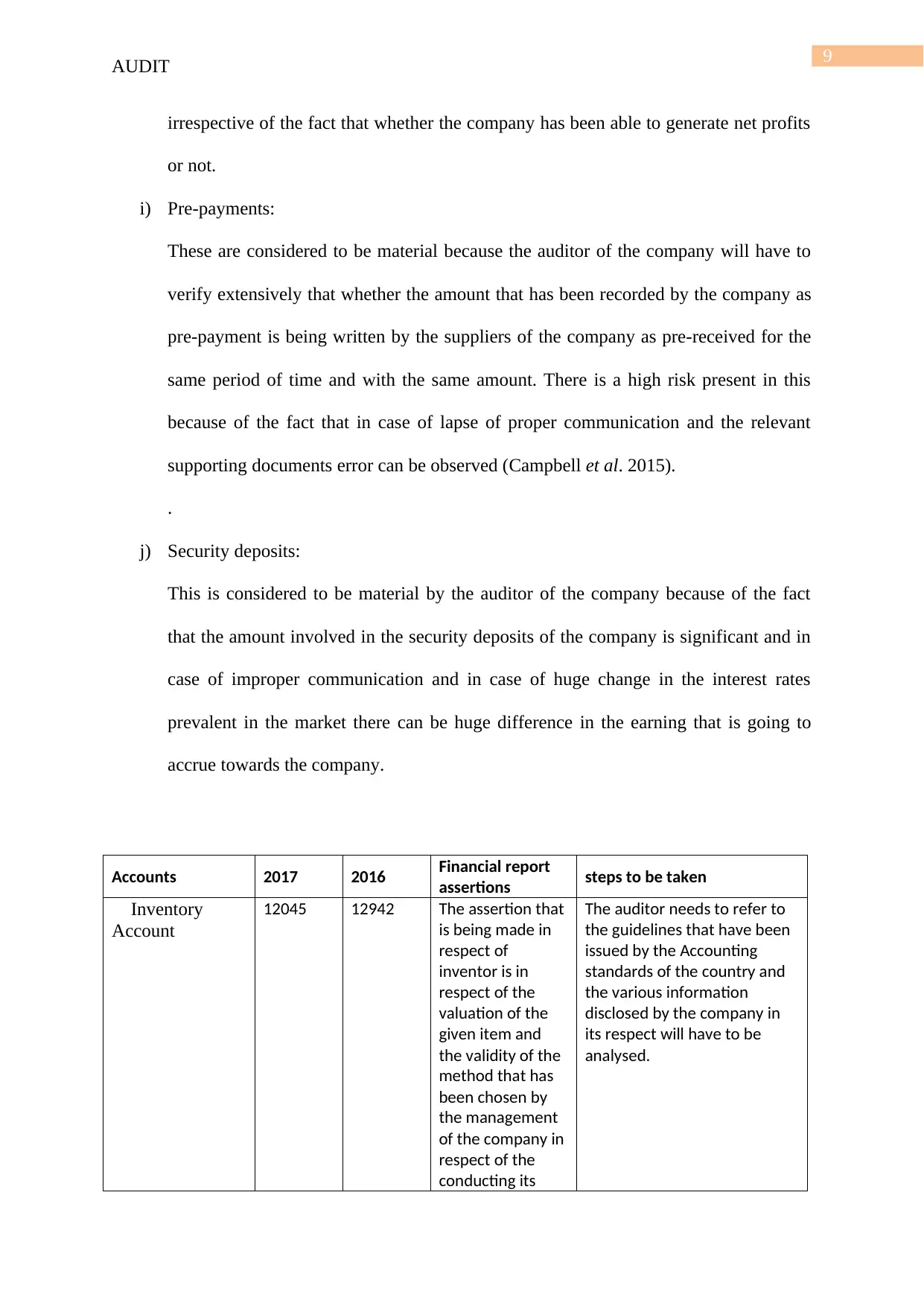

a) Inventory:

This account has been considered to be among the significant one and be termed as

material because of the fact that there are significant chances that the amount that has

been recorded in the financial statement corresponding to this is incorrect and

misleading (). The auditor of the company also needs to verify the method that has

been adopted by the company for the purpose of valuation of the inventory of the

company. The decision has to be taken regarding the fact that whether the provisions

of the corporation act and the accounting standards were abided by the company.

b) Receivables:

The item has been considered to hold material importance in the financial statement

of the company due to the reason that it is the result of the primary revenue generating

activities of the company. The pool of asset that is created in respect of this item is

fully comprised of third parties that are not directly a part of the company. It is very

doubtful on their part to make the full payment to the company in respect of the items

that have been purchased by them from the company (Gormly et al. 2016). In addition

to this, the validity of the time that has been selected by the company for the

recognition of the amount corresponding to them has to be established too.

AUDIT

Debt Equity Ratio 0.08 0.12 0.05

It can be seen that the debt equity ratio of the company has improved significantly

over the period of three years as the value of the debt equity ratio has decreased. This

has resulted in the improvement of the solvency position of the company.

Ascertainment of the materiality of the accounts of the company:

a) Inventory:

This account has been considered to be among the significant one and be termed as

material because of the fact that there are significant chances that the amount that has

been recorded in the financial statement corresponding to this is incorrect and

misleading (). The auditor of the company also needs to verify the method that has

been adopted by the company for the purpose of valuation of the inventory of the

company. The decision has to be taken regarding the fact that whether the provisions

of the corporation act and the accounting standards were abided by the company.

b) Receivables:

The item has been considered to hold material importance in the financial statement

of the company due to the reason that it is the result of the primary revenue generating

activities of the company. The pool of asset that is created in respect of this item is

fully comprised of third parties that are not directly a part of the company. It is very

doubtful on their part to make the full payment to the company in respect of the items

that have been purchased by them from the company (Gormly et al. 2016). In addition

to this, the validity of the time that has been selected by the company for the

recognition of the amount corresponding to them has to be established too.

8

AUDIT

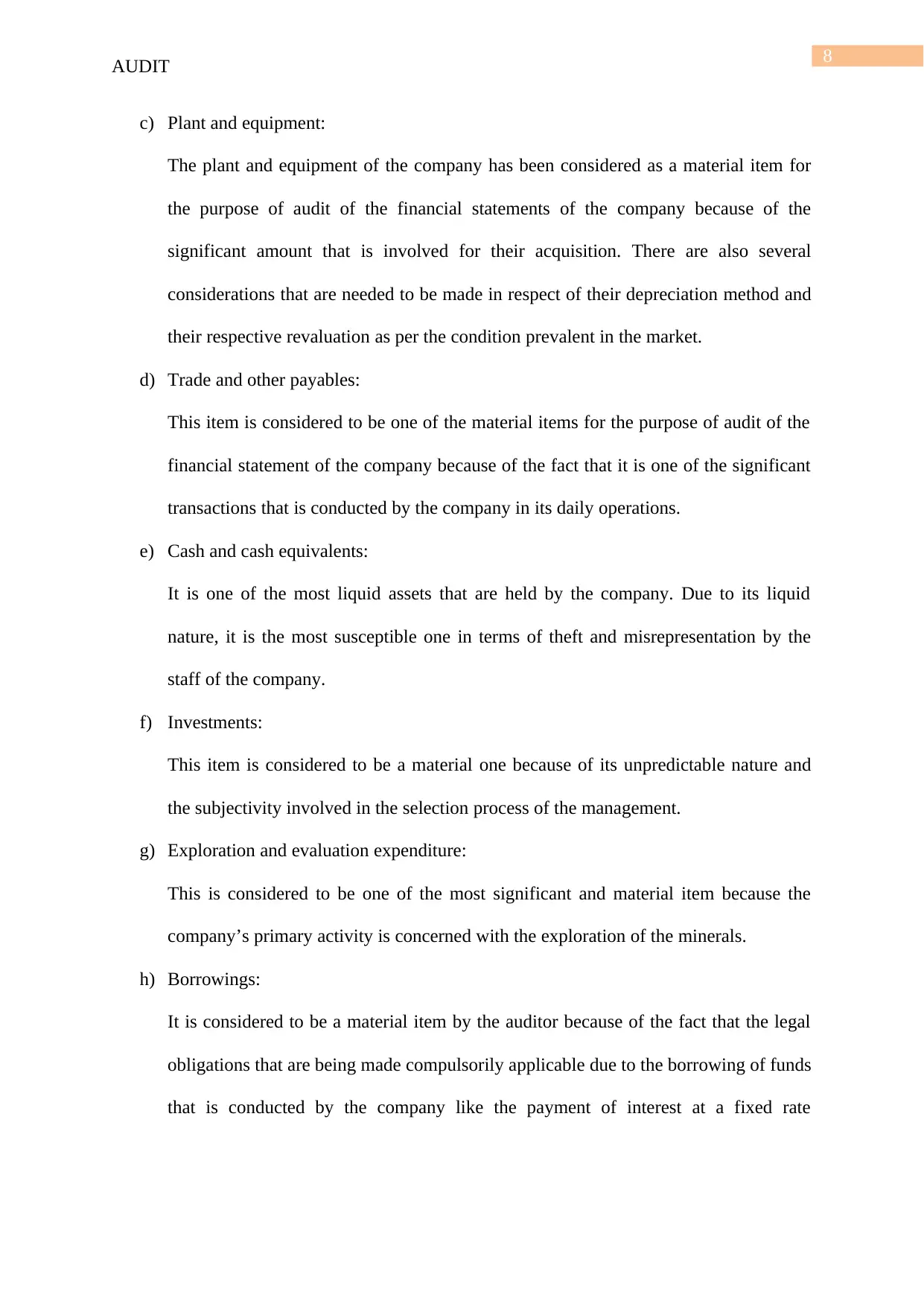

c) Plant and equipment:

The plant and equipment of the company has been considered as a material item for

the purpose of audit of the financial statements of the company because of the

significant amount that is involved for their acquisition. There are also several

considerations that are needed to be made in respect of their depreciation method and

their respective revaluation as per the condition prevalent in the market.

d) Trade and other payables:

This item is considered to be one of the material items for the purpose of audit of the

financial statement of the company because of the fact that it is one of the significant

transactions that is conducted by the company in its daily operations.

e) Cash and cash equivalents:

It is one of the most liquid assets that are held by the company. Due to its liquid

nature, it is the most susceptible one in terms of theft and misrepresentation by the

staff of the company.

f) Investments:

This item is considered to be a material one because of its unpredictable nature and

the subjectivity involved in the selection process of the management.

g) Exploration and evaluation expenditure:

This is considered to be one of the most significant and material item because the

company’s primary activity is concerned with the exploration of the minerals.

h) Borrowings:

It is considered to be a material item by the auditor because of the fact that the legal

obligations that are being made compulsorily applicable due to the borrowing of funds

that is conducted by the company like the payment of interest at a fixed rate

AUDIT

c) Plant and equipment:

The plant and equipment of the company has been considered as a material item for

the purpose of audit of the financial statements of the company because of the

significant amount that is involved for their acquisition. There are also several

considerations that are needed to be made in respect of their depreciation method and

their respective revaluation as per the condition prevalent in the market.

d) Trade and other payables:

This item is considered to be one of the material items for the purpose of audit of the

financial statement of the company because of the fact that it is one of the significant

transactions that is conducted by the company in its daily operations.

e) Cash and cash equivalents:

It is one of the most liquid assets that are held by the company. Due to its liquid

nature, it is the most susceptible one in terms of theft and misrepresentation by the

staff of the company.

f) Investments:

This item is considered to be a material one because of its unpredictable nature and

the subjectivity involved in the selection process of the management.

g) Exploration and evaluation expenditure:

This is considered to be one of the most significant and material item because the

company’s primary activity is concerned with the exploration of the minerals.

h) Borrowings:

It is considered to be a material item by the auditor because of the fact that the legal

obligations that are being made compulsorily applicable due to the borrowing of funds

that is conducted by the company like the payment of interest at a fixed rate

9

AUDIT

irrespective of the fact that whether the company has been able to generate net profits

or not.

i) Pre-payments:

These are considered to be material because the auditor of the company will have to

verify extensively that whether the amount that has been recorded by the company as

pre-payment is being written by the suppliers of the company as pre-received for the

same period of time and with the same amount. There is a high risk present in this

because of the fact that in case of lapse of proper communication and the relevant

supporting documents error can be observed (Campbell et al. 2015).

.

j) Security deposits:

This is considered to be material by the auditor of the company because of the fact

that the amount involved in the security deposits of the company is significant and in

case of improper communication and in case of huge change in the interest rates

prevalent in the market there can be huge difference in the earning that is going to

accrue towards the company.

Accounts 2017 2016 Financial report

assertions steps to be taken

Inventory

Account

12045 12942 The assertion that

is being made in

respect of

inventor is in

respect of the

valuation of the

given item and

the validity of the

method that has

been chosen by

the management

of the company in

respect of the

conducting its

The auditor needs to refer to

the guidelines that have been

issued by the Accounting

standards of the country and

the various information

disclosed by the company in

its respect will have to be

analysed.

AUDIT

irrespective of the fact that whether the company has been able to generate net profits

or not.

i) Pre-payments:

These are considered to be material because the auditor of the company will have to

verify extensively that whether the amount that has been recorded by the company as

pre-payment is being written by the suppliers of the company as pre-received for the

same period of time and with the same amount. There is a high risk present in this

because of the fact that in case of lapse of proper communication and the relevant

supporting documents error can be observed (Campbell et al. 2015).

.

j) Security deposits:

This is considered to be material by the auditor of the company because of the fact

that the amount involved in the security deposits of the company is significant and in

case of improper communication and in case of huge change in the interest rates

prevalent in the market there can be huge difference in the earning that is going to

accrue towards the company.

Accounts 2017 2016 Financial report

assertions steps to be taken

Inventory

Account

12045 12942 The assertion that

is being made in

respect of

inventor is in

respect of the

valuation of the

given item and

the validity of the

method that has

been chosen by

the management

of the company in

respect of the

conducting its

The auditor needs to refer to

the guidelines that have been

issued by the Accounting

standards of the country and

the various information

disclosed by the company in

its respect will have to be

analysed.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

AUDIT

valuation.

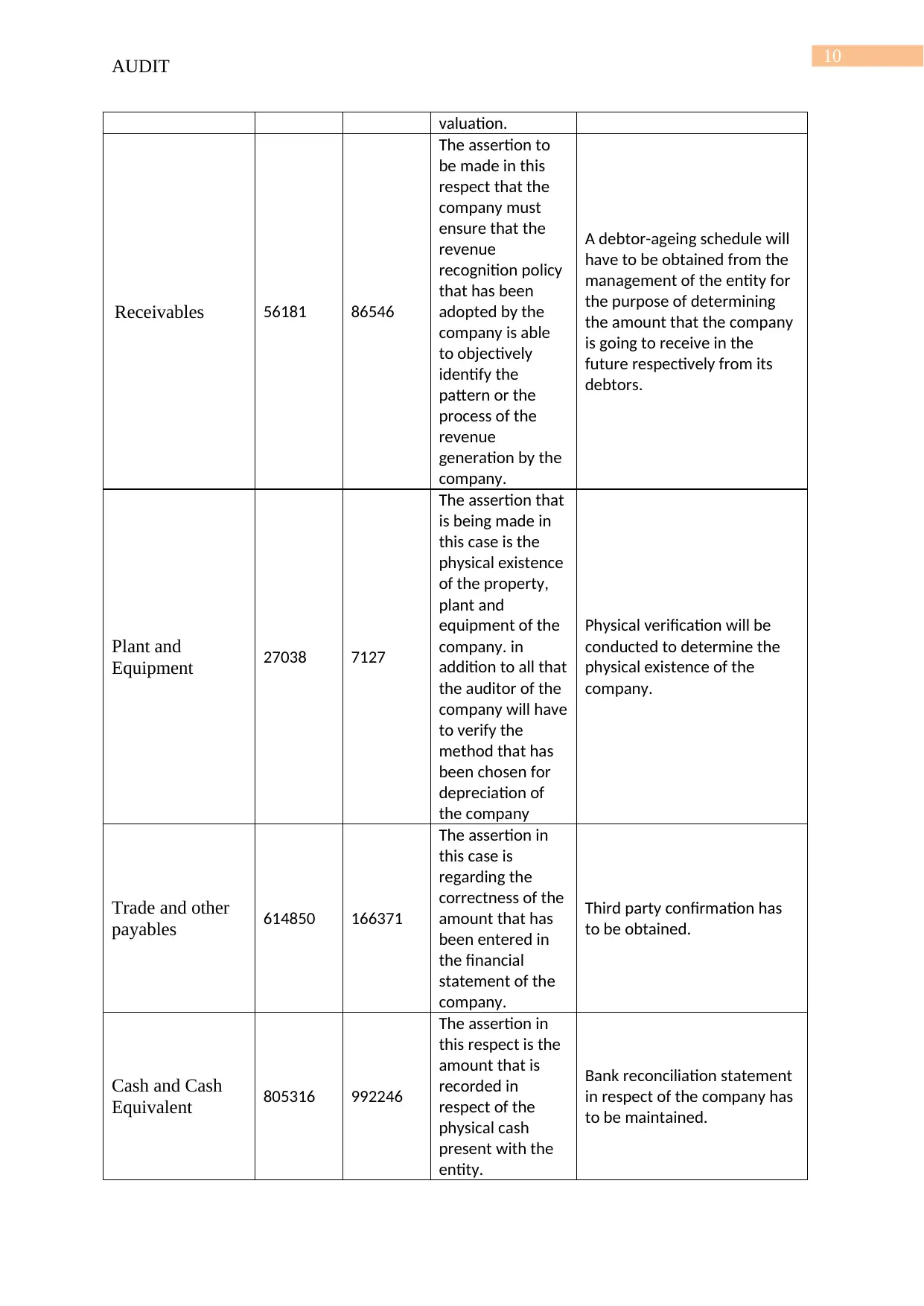

Receivables 56181 86546

The assertion to

be made in this

respect that the

company must

ensure that the

revenue

recognition policy

that has been

adopted by the

company is able

to objectively

identify the

pattern or the

process of the

revenue

generation by the

company.

A debtor-ageing schedule will

have to be obtained from the

management of the entity for

the purpose of determining

the amount that the company

is going to receive in the

future respectively from its

debtors.

Plant and

Equipment 27038 7127

The assertion that

is being made in

this case is the

physical existence

of the property,

plant and

equipment of the

company. in

addition to all that

the auditor of the

company will have

to verify the

method that has

been chosen for

depreciation of

the company

Physical verification will be

conducted to determine the

physical existence of the

company.

Trade and other

payables 614850 166371

The assertion in

this case is

regarding the

correctness of the

amount that has

been entered in

the financial

statement of the

company.

Third party confirmation has

to be obtained.

Cash and Cash

Equivalent 805316 992246

The assertion in

this respect is the

amount that is

recorded in

respect of the

physical cash

present with the

entity.

Bank reconciliation statement

in respect of the company has

to be maintained.

AUDIT

valuation.

Receivables 56181 86546

The assertion to

be made in this

respect that the

company must

ensure that the

revenue

recognition policy

that has been

adopted by the

company is able

to objectively

identify the

pattern or the

process of the

revenue

generation by the

company.

A debtor-ageing schedule will

have to be obtained from the

management of the entity for

the purpose of determining

the amount that the company

is going to receive in the

future respectively from its

debtors.

Plant and

Equipment 27038 7127

The assertion that

is being made in

this case is the

physical existence

of the property,

plant and

equipment of the

company. in

addition to all that

the auditor of the

company will have

to verify the

method that has

been chosen for

depreciation of

the company

Physical verification will be

conducted to determine the

physical existence of the

company.

Trade and other

payables 614850 166371

The assertion in

this case is

regarding the

correctness of the

amount that has

been entered in

the financial

statement of the

company.

Third party confirmation has

to be obtained.

Cash and Cash

Equivalent 805316 992246

The assertion in

this respect is the

amount that is

recorded in

respect of the

physical cash

present with the

entity.

Bank reconciliation statement

in respect of the company has

to be maintained.

11

AUDIT

Investments 16000 15999

The assertion is

being made in

respect of the

measurement of

the investment

based on the

period for which it

is desired to be

held by the

company

An investment schedule will

have to be obtained from the

company.

Exploration and

expenditure 3875504 1856500

The assertion is

made in respect

of the

capitalisation of

the expenses

incurred in this

respect.

The statement of expenditure

and statement of revenue will

have to be prepared.

Borrowings 433771

The assertion is

made in respect

of the terms

mentioned in the

agreement in

respect of interest

to be paid

The interest schedule of the

company has to be obtained

from the management.

Pre-payments 2633 16104

The assertion is

made in respect

of maintenance of

proper records in

this respect

Reconciliation of the amount

recorded by the supplier and

the company has to be

conducted.

Security deposits 53303 33303

The assertion is

made for the

amount that is

being recorded in

the

The statement containing the

records of the security

deposits made by the

company must be maintained

by it.

Conclusion:

The materiality of the items that are being presented in the financial statement of the

company has to be ascertained for the purpose of determining the focus that has to be given

in respect of each of the items of the financial statement. The company in the present scenario

needs to increase its profitability immediately for ascertaining continued operations in the

future.

AUDIT

Investments 16000 15999

The assertion is

being made in

respect of the

measurement of

the investment

based on the

period for which it

is desired to be

held by the

company

An investment schedule will

have to be obtained from the

company.

Exploration and

expenditure 3875504 1856500

The assertion is

made in respect

of the

capitalisation of

the expenses

incurred in this

respect.

The statement of expenditure

and statement of revenue will

have to be prepared.

Borrowings 433771

The assertion is

made in respect

of the terms

mentioned in the

agreement in

respect of interest

to be paid

The interest schedule of the

company has to be obtained

from the management.

Pre-payments 2633 16104

The assertion is

made in respect

of maintenance of

proper records in

this respect

Reconciliation of the amount

recorded by the supplier and

the company has to be

conducted.

Security deposits 53303 33303

The assertion is

made for the

amount that is

being recorded in

the

The statement containing the

records of the security

deposits made by the

company must be maintained

by it.

Conclusion:

The materiality of the items that are being presented in the financial statement of the

company has to be ascertained for the purpose of determining the focus that has to be given

in respect of each of the items of the financial statement. The company in the present scenario

needs to increase its profitability immediately for ascertaining continued operations in the

future.

12

AUDIT

Reference

Australia, I. and Australia, D.I., 2015. RE: Australian Infrastructure Audit.

Campbell, I., Scott, N., Seneviratne, S., Kollias, J., Walters, D., Taylor, C. and Roder, D.,

2015. Breast cancer characteristics and survival differences between Maori, Pacific and other

New Zealand women included in the quality audit program of breast surgeons of Australia

and New Zealand. Asian Pac J Cancer Prev, 16(6), pp.2465-2472.

Clark, H., Orme, L., Super, L., Gillam, L., Stern, K., Agresta, A., Moore, P., Downie, P.,

Grover, S. and Jayasinghe, Y., 2015. Addressing fertility in female paediatric and adolescent

patients receiving gonadotoxic therapy: audit of clinical practice at The Royal Children's

Hospital, Melbourne. Bjog: An International Journal of Obstetrics and Gynaecology, 122,

p.380.

Gibberd, A., Supramaniam, R., Dillon, A., Armstrong, B.K. and O’Connell, D.L., 2016. Lung

cancer treatment and mortality for Aboriginal people in New South Wales, Australia: results

from a population-based record linkage study and medical record audit. BMC cancer, 16(1),

p.289.

Gormly, K.L., Coscia, C., Wells, T., Tebbutt, N., Harvey, J.A., Wilson, K., Schmoll, H.J.,

Price, T., Price, T., Hruby, G. and Jeffery, M., 2016. Mri rectal cancer in Australia and New

Zealand: An audit from the Petacc‐6 trial. Journal of medical imaging and radiation

oncology, 60(5), pp.607-615.

Harish, V., Raymond, A.P., Issler, A.C., Lajevardi, S.S., Chang, L.Y., Maitz, P.K. and

Kennedy, P., 2015. Accuracy of burn size estimation in patients transferred to adult Burn

Units in Sydney, Australia: an audit of 698 patients. Burns, 41(1), pp.91-99.

AUDIT

Reference

Australia, I. and Australia, D.I., 2015. RE: Australian Infrastructure Audit.

Campbell, I., Scott, N., Seneviratne, S., Kollias, J., Walters, D., Taylor, C. and Roder, D.,

2015. Breast cancer characteristics and survival differences between Maori, Pacific and other

New Zealand women included in the quality audit program of breast surgeons of Australia

and New Zealand. Asian Pac J Cancer Prev, 16(6), pp.2465-2472.

Clark, H., Orme, L., Super, L., Gillam, L., Stern, K., Agresta, A., Moore, P., Downie, P.,

Grover, S. and Jayasinghe, Y., 2015. Addressing fertility in female paediatric and adolescent

patients receiving gonadotoxic therapy: audit of clinical practice at The Royal Children's

Hospital, Melbourne. Bjog: An International Journal of Obstetrics and Gynaecology, 122,

p.380.

Gibberd, A., Supramaniam, R., Dillon, A., Armstrong, B.K. and O’Connell, D.L., 2016. Lung

cancer treatment and mortality for Aboriginal people in New South Wales, Australia: results

from a population-based record linkage study and medical record audit. BMC cancer, 16(1),

p.289.

Gormly, K.L., Coscia, C., Wells, T., Tebbutt, N., Harvey, J.A., Wilson, K., Schmoll, H.J.,

Price, T., Price, T., Hruby, G. and Jeffery, M., 2016. Mri rectal cancer in Australia and New

Zealand: An audit from the Petacc‐6 trial. Journal of medical imaging and radiation

oncology, 60(5), pp.607-615.

Harish, V., Raymond, A.P., Issler, A.C., Lajevardi, S.S., Chang, L.Y., Maitz, P.K. and

Kennedy, P., 2015. Accuracy of burn size estimation in patients transferred to adult Burn

Units in Sydney, Australia: an audit of 698 patients. Burns, 41(1), pp.91-99.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

AUDIT

Jackson, D., Atkin, K., Bettenay, F., Clark, J., Ditchfield, M.R., Grimm, J.E., Linke, R.,

Long, G., Onikul, E., Pereira, J. and Phillips, M., 2015. Paediatric CT dose: a multicentre

audit of subspecialty practice in Australia and New Zealand. European radiology, 25(11),

pp.3109-3122.

Redfern, J., Hyun, K., Chew, D.P., Astley, C., Chow, C., Aliprandi-Costa, B., Howell, T.,

Carr, B., Lintern, K., Ranasinghe, I. and Nallaiah, K., 2014. Prescription of secondary

prevention medications, lifestyle advice, and referral to rehabilitation among acute coronary

syndrome inpatients: results from a large prospective audit in Australia and New

Zealand. Heart, pp.heartjnl-2013.

AUDIT

Jackson, D., Atkin, K., Bettenay, F., Clark, J., Ditchfield, M.R., Grimm, J.E., Linke, R.,

Long, G., Onikul, E., Pereira, J. and Phillips, M., 2015. Paediatric CT dose: a multicentre

audit of subspecialty practice in Australia and New Zealand. European radiology, 25(11),

pp.3109-3122.

Redfern, J., Hyun, K., Chew, D.P., Astley, C., Chow, C., Aliprandi-Costa, B., Howell, T.,

Carr, B., Lintern, K., Ranasinghe, I. and Nallaiah, K., 2014. Prescription of secondary

prevention medications, lifestyle advice, and referral to rehabilitation among acute coronary

syndrome inpatients: results from a large prospective audit in Australia and New

Zealand. Heart, pp.heartjnl-2013.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.