Audit Report to Managing Partner, John Richards

VerifiedAdded on 2023/06/05

|24

|5147

|488

AI Summary

This report seeks to analyze and discuss various areas and accounts with regard to the audit of Trunkey Creek Wines (TCW) Limited. These are investments, accounts receivable, marketing expense and property assets. After analyzing the ratios and additional information, it has been noted that there are several business risks faced by Trunkey Creek Wines (TCW) Limited. These are strategic risk, compliance risk, operational risk, financial risk and technological risk.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 1

Audit Report to Managing Partner, John Richards

Name

Professor

Institution

Date

Introduction

Audit Report to Managing Partner, John Richards

Name

Professor

Institution

Date

Introduction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 2

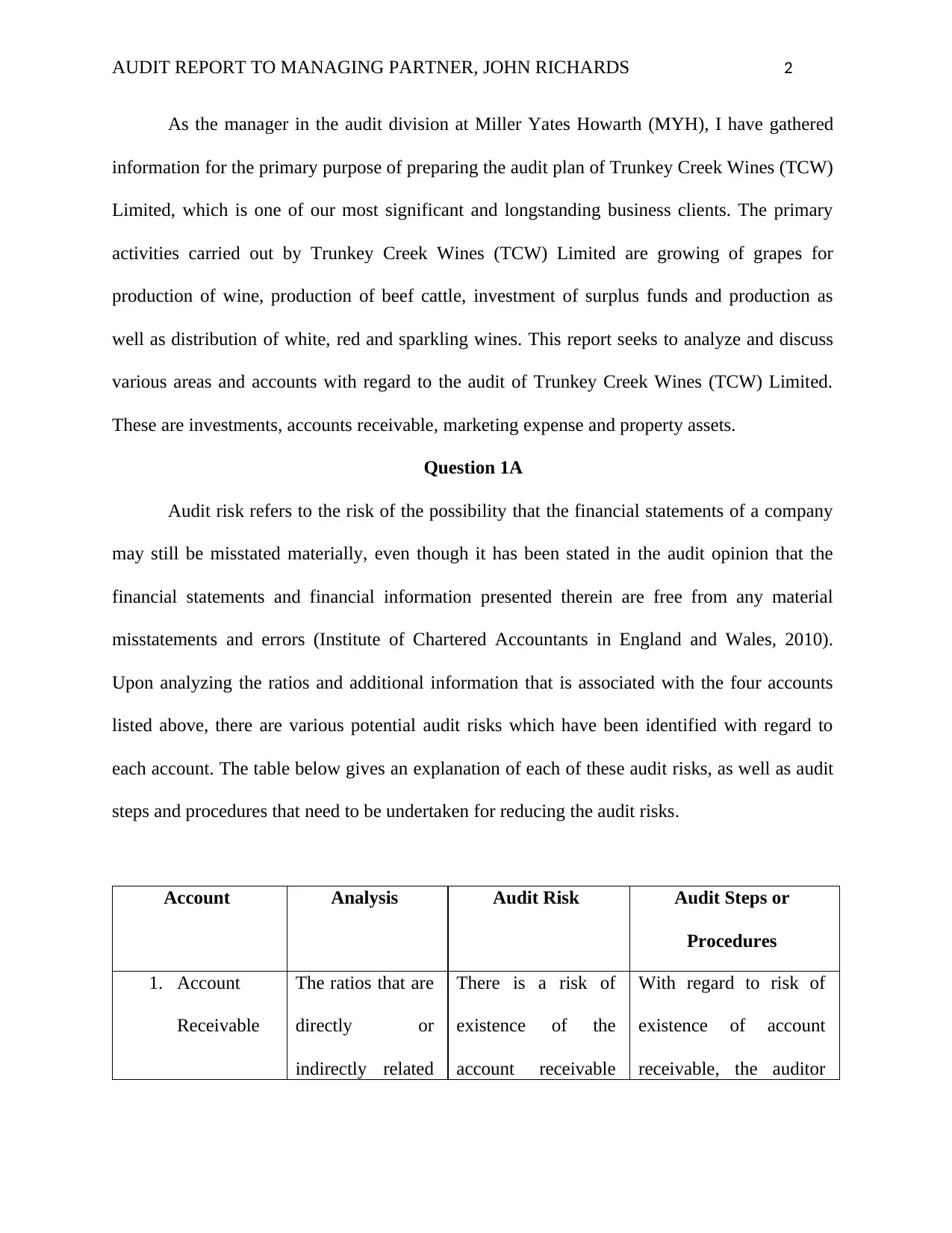

As the manager in the audit division at Miller Yates Howarth (MYH), I have gathered

information for the primary purpose of preparing the audit plan of Trunkey Creek Wines (TCW)

Limited, which is one of our most significant and longstanding business clients. The primary

activities carried out by Trunkey Creek Wines (TCW) Limited are growing of grapes for

production of wine, production of beef cattle, investment of surplus funds and production as

well as distribution of white, red and sparkling wines. This report seeks to analyze and discuss

various areas and accounts with regard to the audit of Trunkey Creek Wines (TCW) Limited.

These are investments, accounts receivable, marketing expense and property assets.

Question 1A

Audit risk refers to the risk of the possibility that the financial statements of a company

may still be misstated materially, even though it has been stated in the audit opinion that the

financial statements and financial information presented therein are free from any material

misstatements and errors (Institute of Chartered Accountants in England and Wales, 2010).

Upon analyzing the ratios and additional information that is associated with the four accounts

listed above, there are various potential audit risks which have been identified with regard to

each account. The table below gives an explanation of each of these audit risks, as well as audit

steps and procedures that need to be undertaken for reducing the audit risks.

Account Analysis Audit Risk Audit Steps or

Procedures

1. Account

Receivable

The ratios that are

directly or

indirectly related

There is a risk of

existence of the

account receivable

With regard to risk of

existence of account

receivable, the auditor

As the manager in the audit division at Miller Yates Howarth (MYH), I have gathered

information for the primary purpose of preparing the audit plan of Trunkey Creek Wines (TCW)

Limited, which is one of our most significant and longstanding business clients. The primary

activities carried out by Trunkey Creek Wines (TCW) Limited are growing of grapes for

production of wine, production of beef cattle, investment of surplus funds and production as

well as distribution of white, red and sparkling wines. This report seeks to analyze and discuss

various areas and accounts with regard to the audit of Trunkey Creek Wines (TCW) Limited.

These are investments, accounts receivable, marketing expense and property assets.

Question 1A

Audit risk refers to the risk of the possibility that the financial statements of a company

may still be misstated materially, even though it has been stated in the audit opinion that the

financial statements and financial information presented therein are free from any material

misstatements and errors (Institute of Chartered Accountants in England and Wales, 2010).

Upon analyzing the ratios and additional information that is associated with the four accounts

listed above, there are various potential audit risks which have been identified with regard to

each account. The table below gives an explanation of each of these audit risks, as well as audit

steps and procedures that need to be undertaken for reducing the audit risks.

Account Analysis Audit Risk Audit Steps or

Procedures

1. Account

Receivable

The ratios that are

directly or

indirectly related

There is a risk of

existence of the

account receivable

With regard to risk of

existence of account

receivable, the auditor

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 3

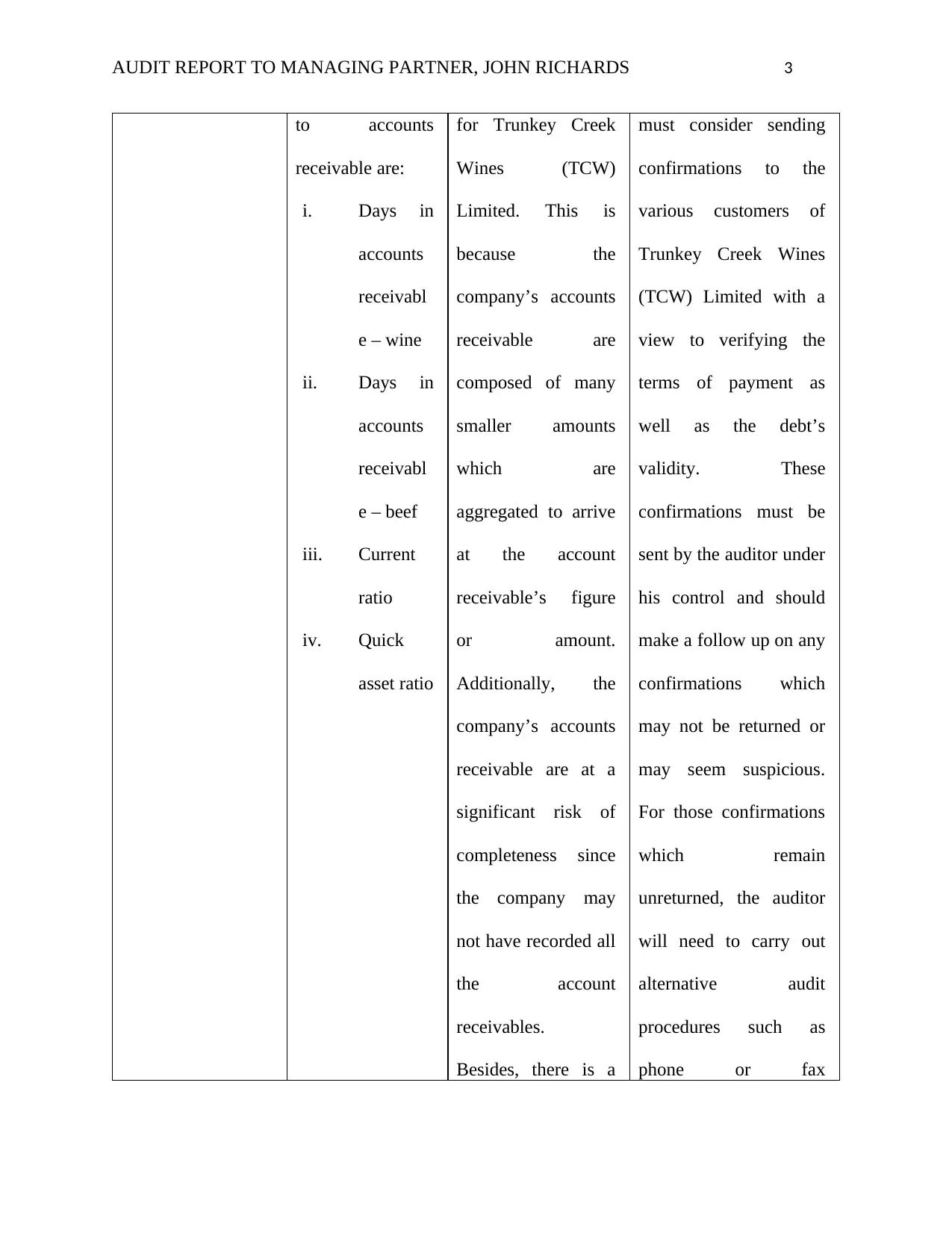

to accounts

receivable are:

i. Days in

accounts

receivabl

e – wine

ii. Days in

accounts

receivabl

e – beef

iii. Current

ratio

iv. Quick

asset ratio

for Trunkey Creek

Wines (TCW)

Limited. This is

because the

company’s accounts

receivable are

composed of many

smaller amounts

which are

aggregated to arrive

at the account

receivable’s figure

or amount.

Additionally, the

company’s accounts

receivable are at a

significant risk of

completeness since

the company may

not have recorded all

the account

receivables.

Besides, there is a

must consider sending

confirmations to the

various customers of

Trunkey Creek Wines

(TCW) Limited with a

view to verifying the

terms of payment as

well as the debt’s

validity. These

confirmations must be

sent by the auditor under

his control and should

make a follow up on any

confirmations which

may not be returned or

may seem suspicious.

For those confirmations

which remain

unreturned, the auditor

will need to carry out

alternative audit

procedures such as

phone or fax

to accounts

receivable are:

i. Days in

accounts

receivabl

e – wine

ii. Days in

accounts

receivabl

e – beef

iii. Current

ratio

iv. Quick

asset ratio

for Trunkey Creek

Wines (TCW)

Limited. This is

because the

company’s accounts

receivable are

composed of many

smaller amounts

which are

aggregated to arrive

at the account

receivable’s figure

or amount.

Additionally, the

company’s accounts

receivable are at a

significant risk of

completeness since

the company may

not have recorded all

the account

receivables.

Besides, there is a

must consider sending

confirmations to the

various customers of

Trunkey Creek Wines

(TCW) Limited with a

view to verifying the

terms of payment as

well as the debt’s

validity. These

confirmations must be

sent by the auditor under

his control and should

make a follow up on any

confirmations which

may not be returned or

may seem suspicious.

For those confirmations

which remain

unreturned, the auditor

will need to carry out

alternative audit

procedures such as

phone or fax

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 4

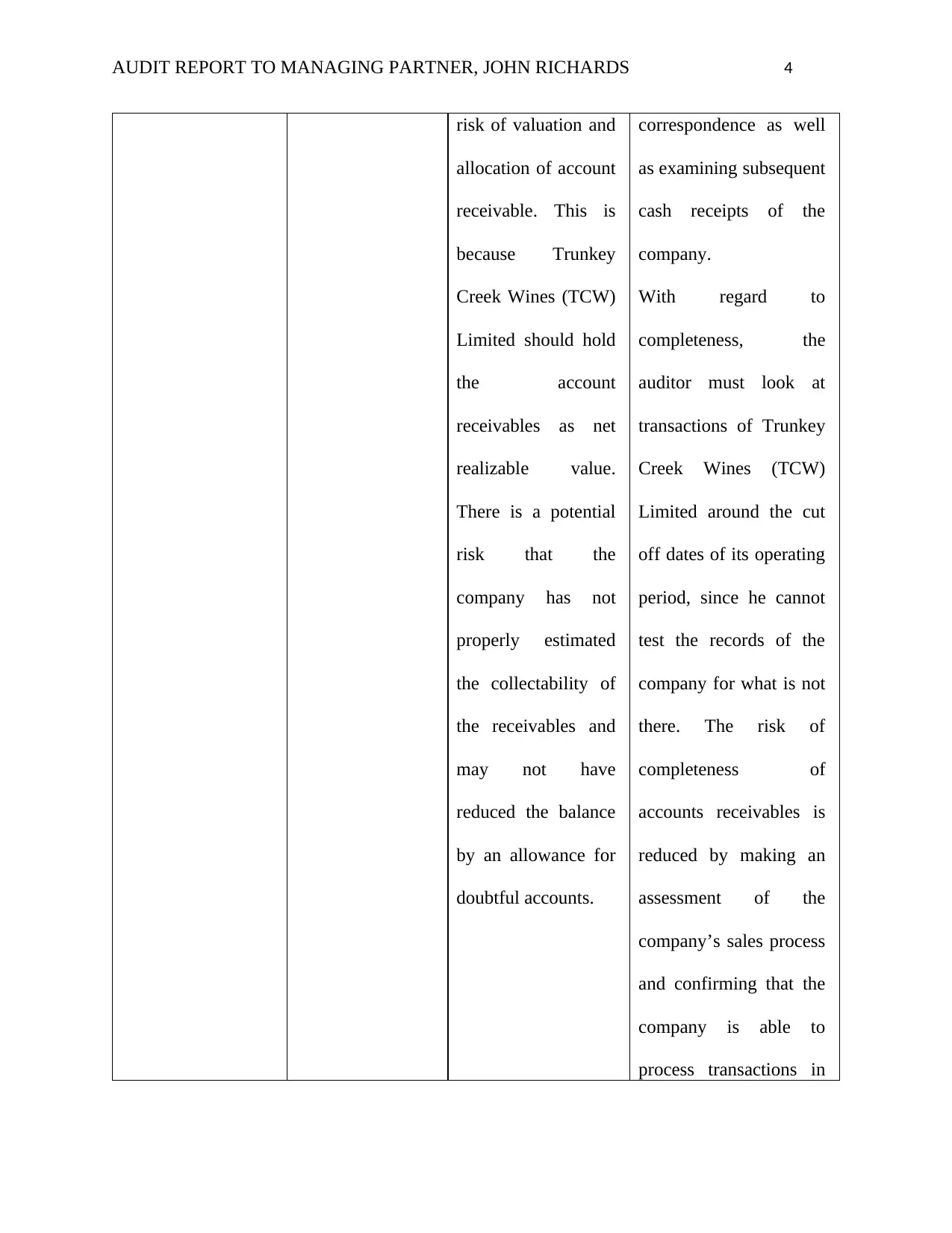

risk of valuation and

allocation of account

receivable. This is

because Trunkey

Creek Wines (TCW)

Limited should hold

the account

receivables as net

realizable value.

There is a potential

risk that the

company has not

properly estimated

the collectability of

the receivables and

may not have

reduced the balance

by an allowance for

doubtful accounts.

correspondence as well

as examining subsequent

cash receipts of the

company.

With regard to

completeness, the

auditor must look at

transactions of Trunkey

Creek Wines (TCW)

Limited around the cut

off dates of its operating

period, since he cannot

test the records of the

company for what is not

there. The risk of

completeness of

accounts receivables is

reduced by making an

assessment of the

company’s sales process

and confirming that the

company is able to

process transactions in

risk of valuation and

allocation of account

receivable. This is

because Trunkey

Creek Wines (TCW)

Limited should hold

the account

receivables as net

realizable value.

There is a potential

risk that the

company has not

properly estimated

the collectability of

the receivables and

may not have

reduced the balance

by an allowance for

doubtful accounts.

correspondence as well

as examining subsequent

cash receipts of the

company.

With regard to

completeness, the

auditor must look at

transactions of Trunkey

Creek Wines (TCW)

Limited around the cut

off dates of its operating

period, since he cannot

test the records of the

company for what is not

there. The risk of

completeness of

accounts receivables is

reduced by making an

assessment of the

company’s sales process

and confirming that the

company is able to

process transactions in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 5

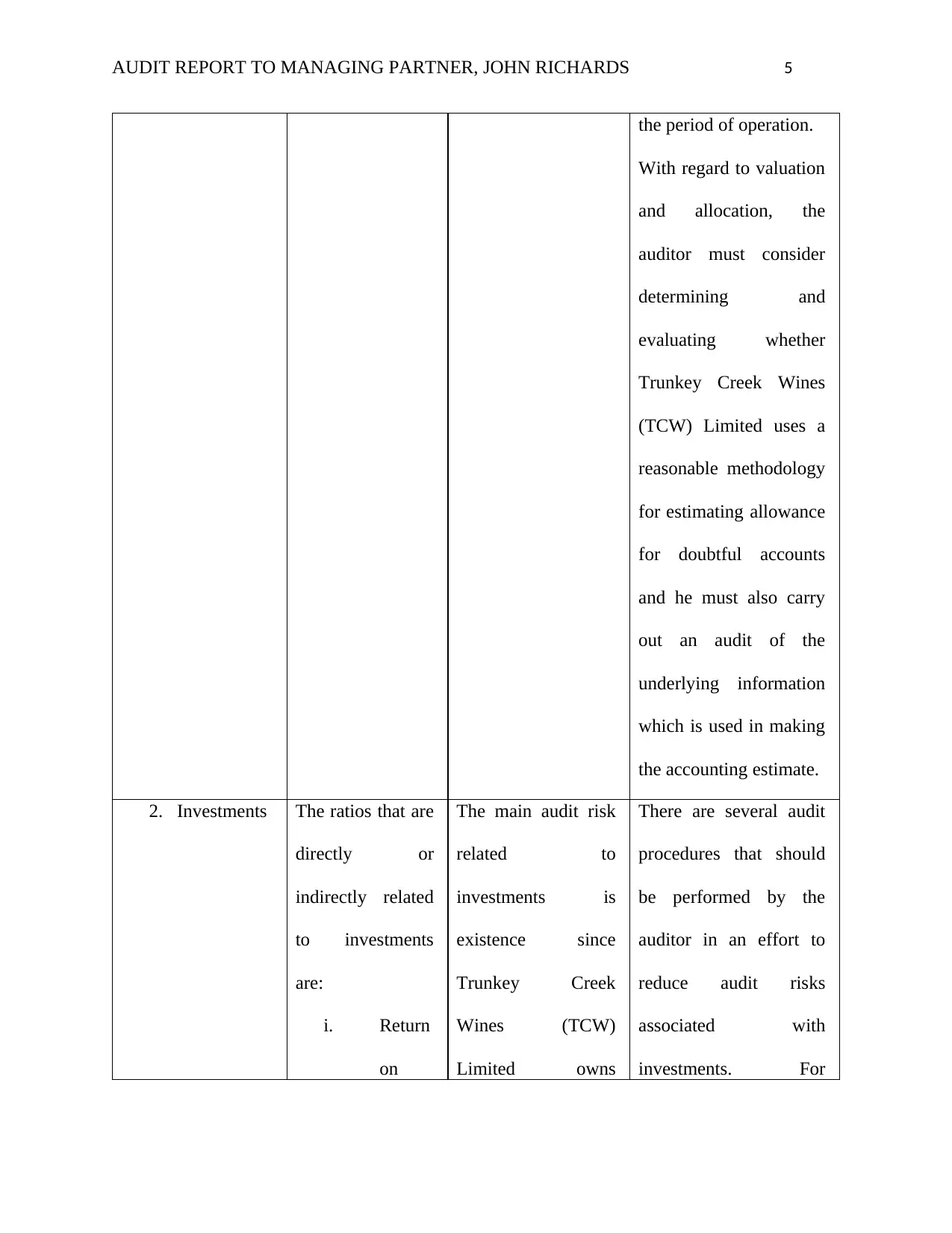

the period of operation.

With regard to valuation

and allocation, the

auditor must consider

determining and

evaluating whether

Trunkey Creek Wines

(TCW) Limited uses a

reasonable methodology

for estimating allowance

for doubtful accounts

and he must also carry

out an audit of the

underlying information

which is used in making

the accounting estimate.

2. Investments The ratios that are

directly or

indirectly related

to investments

are:

i. Return

on

The main audit risk

related to

investments is

existence since

Trunkey Creek

Wines (TCW)

Limited owns

There are several audit

procedures that should

be performed by the

auditor in an effort to

reduce audit risks

associated with

investments. For

the period of operation.

With regard to valuation

and allocation, the

auditor must consider

determining and

evaluating whether

Trunkey Creek Wines

(TCW) Limited uses a

reasonable methodology

for estimating allowance

for doubtful accounts

and he must also carry

out an audit of the

underlying information

which is used in making

the accounting estimate.

2. Investments The ratios that are

directly or

indirectly related

to investments

are:

i. Return

on

The main audit risk

related to

investments is

existence since

Trunkey Creek

Wines (TCW)

Limited owns

There are several audit

procedures that should

be performed by the

auditor in an effort to

reduce audit risks

associated with

investments. For

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 6

equity

ii. Net

profit

margin

iii. Debt

to

equity

numerous

investments which

need to be verified

by the auditor.

Additionally, there is

a risk of

completeness of

investments since

these may not be

recorded in the

books of Trunkey

Creek Wines (TCW)

Limited in correct

amounts.

instance, regarding

existence assertion risks,

the auditor must

consider requesting a

confirmation from the

custodians used by the

company for

safeguarding the

securities. The

confirmation must seek

to address the types of

investments and

securities owned by

Trunkey Creek Wines

(TCW) Limited. The

auditor must also

examine physically the

investments of Trunkey

Creek Wines (TCW)

Limited if the company

maintains custody of its

securities.

With regard to

equity

ii. Net

profit

margin

iii. Debt

to

equity

numerous

investments which

need to be verified

by the auditor.

Additionally, there is

a risk of

completeness of

investments since

these may not be

recorded in the

books of Trunkey

Creek Wines (TCW)

Limited in correct

amounts.

instance, regarding

existence assertion risks,

the auditor must

consider requesting a

confirmation from the

custodians used by the

company for

safeguarding the

securities. The

confirmation must seek

to address the types of

investments and

securities owned by

Trunkey Creek Wines

(TCW) Limited. The

auditor must also

examine physically the

investments of Trunkey

Creek Wines (TCW)

Limited if the company

maintains custody of its

securities.

With regard to

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 7

completeness, the

auditor must consider

confirming whether the

company has properly

recorded the amount of

its investments in its

financial records.

Furthermore, he must

ensure that dividend and

interest related to

investments is recorded

in the financial

statements of Trunkey

Creek Wines (TCW)

Limited as revenue.

3. Property

Assets

The ratios which

are directly or

indirectly related

to property assets

include:

i. Return

on

beef

Existence,

completeness and

valuation or

allocation are the

main audit risk

assertions that are

related to property

assets with regard to

With regard to risk of

existence of property

assets, the auditor must

consider physically

examining the various

production with a view

to ascertaining and

confirming that the

completeness, the

auditor must consider

confirming whether the

company has properly

recorded the amount of

its investments in its

financial records.

Furthermore, he must

ensure that dividend and

interest related to

investments is recorded

in the financial

statements of Trunkey

Creek Wines (TCW)

Limited as revenue.

3. Property

Assets

The ratios which

are directly or

indirectly related

to property assets

include:

i. Return

on

beef

Existence,

completeness and

valuation or

allocation are the

main audit risk

assertions that are

related to property

assets with regard to

With regard to risk of

existence of property

assets, the auditor must

consider physically

examining the various

production with a view

to ascertaining and

confirming that the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 8

produc

tion

assets

ii. Return

on

grape

and

wine

produc

tion

assets

Trunkey Creek

Wines (TCW)

Limited. This is

because the

company has several

production sections

including beef

production and

production of grapes

and wine.

The assertion risk of

valuation and

completeness of

property assets may

arise if Trunkey

Creek Wines (TCW)

Limited does not

correctly record its

property assets in its

financial records.

property assets actually

exist.

With regard to

completeness, the

auditor must look at the

financial records of

Trunkey Creek Wines

(TCW) Limited for

ascertaining what has

not been recorded.

With regard to valuation

and allocation, the

auditor must consider

evaluating whether

Trunkey Creek Wines

(TCW) Limited values

its property assets at

lower of cost or net

realizable value. He

must also examine the

underlying information

which is used in making

valuing the assets.

produc

tion

assets

ii. Return

on

grape

and

wine

produc

tion

assets

Trunkey Creek

Wines (TCW)

Limited. This is

because the

company has several

production sections

including beef

production and

production of grapes

and wine.

The assertion risk of

valuation and

completeness of

property assets may

arise if Trunkey

Creek Wines (TCW)

Limited does not

correctly record its

property assets in its

financial records.

property assets actually

exist.

With regard to

completeness, the

auditor must look at the

financial records of

Trunkey Creek Wines

(TCW) Limited for

ascertaining what has

not been recorded.

With regard to valuation

and allocation, the

auditor must consider

evaluating whether

Trunkey Creek Wines

(TCW) Limited values

its property assets at

lower of cost or net

realizable value. He

must also examine the

underlying information

which is used in making

valuing the assets.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 9

4. Marketing

Expense

The ratio which is

directly or

indirectly related

to marketing

expense is

marketing

expense

percentage of

total S & A

expenses.

The main audit risk

related to marketing

expense is existence,

since Trunkey Creek

Wines (TCW)

Limited may have

included amounts of

expenses that were

not actually incurred.

The auditor must review

the marketing expenses

of Trunkey Creek Wines

(TCW) Limited in order

to ensure that were

actually incurred and

they have been recorded

appropriately. He should

examine carefully

vouchers related to

expenses of marketing

activities.

Question 1B

Business risk refers to the likelihood that a company will not achieve its goals and

objectives, and may not generate the desired financial results. Business risk is influenced by

factors such as price per unit, volume of sales, cost of inputs, competition, government

regulations and the overall economic climate (Cosserat & Rodda, 2009). After analyzing the

ratios and additional information, it has been noted that there are several business risks faced by

Trunkey Creek Wines (TCW) Limited. These are discussed below.

a. Strategic Risk

Trunkey Creek Wines (TCW) Limited faces the risk of its strategies becoming less

effective. This may cause the company to struggle in order to be able to reach its

4. Marketing

Expense

The ratio which is

directly or

indirectly related

to marketing

expense is

marketing

expense

percentage of

total S & A

expenses.

The main audit risk

related to marketing

expense is existence,

since Trunkey Creek

Wines (TCW)

Limited may have

included amounts of

expenses that were

not actually incurred.

The auditor must review

the marketing expenses

of Trunkey Creek Wines

(TCW) Limited in order

to ensure that were

actually incurred and

they have been recorded

appropriately. He should

examine carefully

vouchers related to

expenses of marketing

activities.

Question 1B

Business risk refers to the likelihood that a company will not achieve its goals and

objectives, and may not generate the desired financial results. Business risk is influenced by

factors such as price per unit, volume of sales, cost of inputs, competition, government

regulations and the overall economic climate (Cosserat & Rodda, 2009). After analyzing the

ratios and additional information, it has been noted that there are several business risks faced by

Trunkey Creek Wines (TCW) Limited. These are discussed below.

a. Strategic Risk

Trunkey Creek Wines (TCW) Limited faces the risk of its strategies becoming less

effective. This may cause the company to struggle in order to be able to reach its

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 10

objectives and set goals. This may occur if the company’s implementation does not

proceed according to its original plan or model (Wells, 2014). For instance, Trunkey

Creek Wines (TCW) Limited is in the process developing and implementing a new

Information Technology system. Although the financial controller is happy and satisfied

with the functionality of the system, there is a possibility that the system will develop

issues in future, which may hinder it from performing the expected roles thus bringing

consequential inconveniences to the company. This may adversely affect the financial

performance of Trunkey Creek Wines (TCW) Limited (Gay & Simnett, 2018).

b. Compliance Risk

This refers to the risk that arise in industries which are highly regulated. Trunkey Creek

Wines (TCW) Limited partly operates in the wine industry which is very highly

regulated. For instance, the company must ensure adherence to the three tier distribution

system which requires the manufacturing company to sell wine products to a wholesaler

or retailer, who in turn makes a sale to the end consumer or customer (Russell & ASQ

Quality Audit Division, 2013). The manufacturer is not required to sell wine directly to

the final consumer. With regard to this, there is a risk that Trunkey Creek Wines (TCW)

Limited may fail to understand these requirements and become non-compliant to the

state specific laws of distribution, which may cause it to pay heavy penalties and fines

(Fiedler & Fiedler, 2010).

c. Operational risk

Trunkey Creek Wines (TCW) Limited also faces operational risk. This is because the

company’s day to day operations may be curtailed materially or stopped, due to various

factors which may be uncontrollable to some extent (Reding & Institute of Internal

objectives and set goals. This may occur if the company’s implementation does not

proceed according to its original plan or model (Wells, 2014). For instance, Trunkey

Creek Wines (TCW) Limited is in the process developing and implementing a new

Information Technology system. Although the financial controller is happy and satisfied

with the functionality of the system, there is a possibility that the system will develop

issues in future, which may hinder it from performing the expected roles thus bringing

consequential inconveniences to the company. This may adversely affect the financial

performance of Trunkey Creek Wines (TCW) Limited (Gay & Simnett, 2018).

b. Compliance Risk

This refers to the risk that arise in industries which are highly regulated. Trunkey Creek

Wines (TCW) Limited partly operates in the wine industry which is very highly

regulated. For instance, the company must ensure adherence to the three tier distribution

system which requires the manufacturing company to sell wine products to a wholesaler

or retailer, who in turn makes a sale to the end consumer or customer (Russell & ASQ

Quality Audit Division, 2013). The manufacturer is not required to sell wine directly to

the final consumer. With regard to this, there is a risk that Trunkey Creek Wines (TCW)

Limited may fail to understand these requirements and become non-compliant to the

state specific laws of distribution, which may cause it to pay heavy penalties and fines

(Fiedler & Fiedler, 2010).

c. Operational risk

Trunkey Creek Wines (TCW) Limited also faces operational risk. This is because the

company’s day to day operations may be curtailed materially or stopped, due to various

factors which may be uncontrollable to some extent (Reding & Institute of Internal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 11

Auditors Research Foundation, 2013). For instance, the substantial increase in

temperature may stop the operations of Trunkey Creek Wines (TCW) Limited in its

production of sparkling wine. Due to this, the company has to look for and purchase land

in localities with a cooler climate (Fiedler & Brenton Andrew, 2010).

d. Financial Risk

Since Trunkey Creek Wines (TCW) Limited sells its products both locally and

internationally, it faces a risk of lower profits that may result from significant

fluctuations in the financial markets and foreign exchange rates (Maroun, 2018). These

risks may cause Trunkey Creek Wines (TCW) Limited to lose income or even generate

negative cash flows, which can even lead to closure of the company due to insolvency

(Verschoor, 2008). In addition to this, Trunkey Creek Wines (TCW) Limited partly uses

debt to finance its operations. For instance, the company is funding the land purchase in

part from medium term bank loans. This is risky for the company since it is liable for

paying the cost of borrowing, which significantly reduces its net operating profit due to

the high interest expense (Hay, 2014).

e. Technological Risk

Trunkey Creek Wines (TCW) Limited relies much on computerized systems of internal

controls. The company therefore faces a risk since such controls may not be effective in

the event that the system fail to work or become obsolete in future. This may be caused

by possible hardware and software failures as well as malware, which may

inconvenience the company’s operations and efficiency consequentially (Hanson &

Hanson, 2008).

f. Human Risks

Auditors Research Foundation, 2013). For instance, the substantial increase in

temperature may stop the operations of Trunkey Creek Wines (TCW) Limited in its

production of sparkling wine. Due to this, the company has to look for and purchase land

in localities with a cooler climate (Fiedler & Brenton Andrew, 2010).

d. Financial Risk

Since Trunkey Creek Wines (TCW) Limited sells its products both locally and

internationally, it faces a risk of lower profits that may result from significant

fluctuations in the financial markets and foreign exchange rates (Maroun, 2018). These

risks may cause Trunkey Creek Wines (TCW) Limited to lose income or even generate

negative cash flows, which can even lead to closure of the company due to insolvency

(Verschoor, 2008). In addition to this, Trunkey Creek Wines (TCW) Limited partly uses

debt to finance its operations. For instance, the company is funding the land purchase in

part from medium term bank loans. This is risky for the company since it is liable for

paying the cost of borrowing, which significantly reduces its net operating profit due to

the high interest expense (Hay, 2014).

e. Technological Risk

Trunkey Creek Wines (TCW) Limited relies much on computerized systems of internal

controls. The company therefore faces a risk since such controls may not be effective in

the event that the system fail to work or become obsolete in future. This may be caused

by possible hardware and software failures as well as malware, which may

inconvenience the company’s operations and efficiency consequentially (Hanson &

Hanson, 2008).

f. Human Risks

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 12

There are various risks faced by Trunkey Creek Wines (TCW) Limited which are

created by its employees (Key, Riddle & Institute of Internal Auditors, 2012). For

instance, the behavior of the company’s staff in the work place may be risky if they

become non-compliant or incompetent. Additionally, Trunkey Creek Wines (TCW)

Limited may be impacted by the behavior of its employees outside the work place (Jubb,

2010). For instance, if the employees engage in misuse of drugs and substances, they

may not be able to work efficiently as their judgement may be impaired. Another issue

which may cause human risk is the fact that the board of directors of Trunkey Creek

Wines (TCW) Limited is comprised of Mrs. Claire Harewood and Mr. Stephen

Harewood among other members. However, there is a potential conflict of interest since

these two members are related as Stephen is Claire’s son (Pickett, 2013). Furthermore,

there is no segregation of duties since the management accountant is also the controller

and the administrator of the Information Technology function, which has not been

regarded by the company as a full time job (Hayes, Gortemaker & Wallage, 2014).

g. Physical Risks

Like any other business, Trunkey Creek Wines (TCW) Limited faces physical business

risks on its assets, buildings and employees. Such risks include as fire, theft, water

damage and vandalism (Lessambo, 2018). This causes the company to incur costs

related to repairs and replacement. The company may also face legal charges if it is

found liable for the damages to some extent (Takanen, Demott & Miller, 2008).

h. Competitive Risk

Trunkey Creek Wines (TCW) Limited faces the risk that the competition from its peers

in the industry may prevent it from gaining a competitive edge and may consequently

There are various risks faced by Trunkey Creek Wines (TCW) Limited which are

created by its employees (Key, Riddle & Institute of Internal Auditors, 2012). For

instance, the behavior of the company’s staff in the work place may be risky if they

become non-compliant or incompetent. Additionally, Trunkey Creek Wines (TCW)

Limited may be impacted by the behavior of its employees outside the work place (Jubb,

2010). For instance, if the employees engage in misuse of drugs and substances, they

may not be able to work efficiently as their judgement may be impaired. Another issue

which may cause human risk is the fact that the board of directors of Trunkey Creek

Wines (TCW) Limited is comprised of Mrs. Claire Harewood and Mr. Stephen

Harewood among other members. However, there is a potential conflict of interest since

these two members are related as Stephen is Claire’s son (Pickett, 2013). Furthermore,

there is no segregation of duties since the management accountant is also the controller

and the administrator of the Information Technology function, which has not been

regarded by the company as a full time job (Hayes, Gortemaker & Wallage, 2014).

g. Physical Risks

Like any other business, Trunkey Creek Wines (TCW) Limited faces physical business

risks on its assets, buildings and employees. Such risks include as fire, theft, water

damage and vandalism (Lessambo, 2018). This causes the company to incur costs

related to repairs and replacement. The company may also face legal charges if it is

found liable for the damages to some extent (Takanen, Demott & Miller, 2008).

h. Competitive Risk

Trunkey Creek Wines (TCW) Limited faces the risk that the competition from its peers

in the industry may prevent it from gaining a competitive edge and may consequently

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 13

not reach its goals and objectives. For instance, there is a possibility that the competitors

of the company will fundamentally reduce their cost base, thus making their products

much cheaper than those of Trunkey Creek Wines (TCW) Limited. The competitors may

also have products which are fundamentally of better quality that those of Trunkey

Creek Wines (TCW) Limited, thus making them more preferable by consumers and

customers (Chartered Association of Certified Accountants, 2011).

i. Legal Risk

Trunkey Creek Wines (TCW) Limited faces the risk that its business operations may be

disrupted by new regulations or the possibility that it will incur additional expense and

losses that are related to legal disputes with regard to its business activities (Cascarino,

& Cascarino, 2012).

j. Reputational Risk

Trunkey Creek Wines (TCW) Limited faces reputational risk in the event that its

reputation declines due to incidents or practices which perceived as incompetent,

dishonest and disrespectful. Trunkey Creek Wines (TCW) Limited may therefore incur

significant loses if there is a serious loss of confidence in the company (Bragg, 2011).

Question 2A:

After reviewing the internal control system of Trunkey Creek Wines (TCW) Limited, it

has been noted that the system has the company has potentially effective internal controls

(Liu, 2015). These controls have helped it in alleviating or reducing the various risks that could

have otherwise affected the company adversely (BPP Learning Media, 2012). The table below

gives a summary of the internal controls of Trunkey Creek Wines (TCW) Limited which are

not reach its goals and objectives. For instance, there is a possibility that the competitors

of the company will fundamentally reduce their cost base, thus making their products

much cheaper than those of Trunkey Creek Wines (TCW) Limited. The competitors may

also have products which are fundamentally of better quality that those of Trunkey

Creek Wines (TCW) Limited, thus making them more preferable by consumers and

customers (Chartered Association of Certified Accountants, 2011).

i. Legal Risk

Trunkey Creek Wines (TCW) Limited faces the risk that its business operations may be

disrupted by new regulations or the possibility that it will incur additional expense and

losses that are related to legal disputes with regard to its business activities (Cascarino,

& Cascarino, 2012).

j. Reputational Risk

Trunkey Creek Wines (TCW) Limited faces reputational risk in the event that its

reputation declines due to incidents or practices which perceived as incompetent,

dishonest and disrespectful. Trunkey Creek Wines (TCW) Limited may therefore incur

significant loses if there is a serious loss of confidence in the company (Bragg, 2011).

Question 2A:

After reviewing the internal control system of Trunkey Creek Wines (TCW) Limited, it

has been noted that the system has the company has potentially effective internal controls

(Liu, 2015). These controls have helped it in alleviating or reducing the various risks that could

have otherwise affected the company adversely (BPP Learning Media, 2012). The table below

gives a summary of the internal controls of Trunkey Creek Wines (TCW) Limited which are

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 14

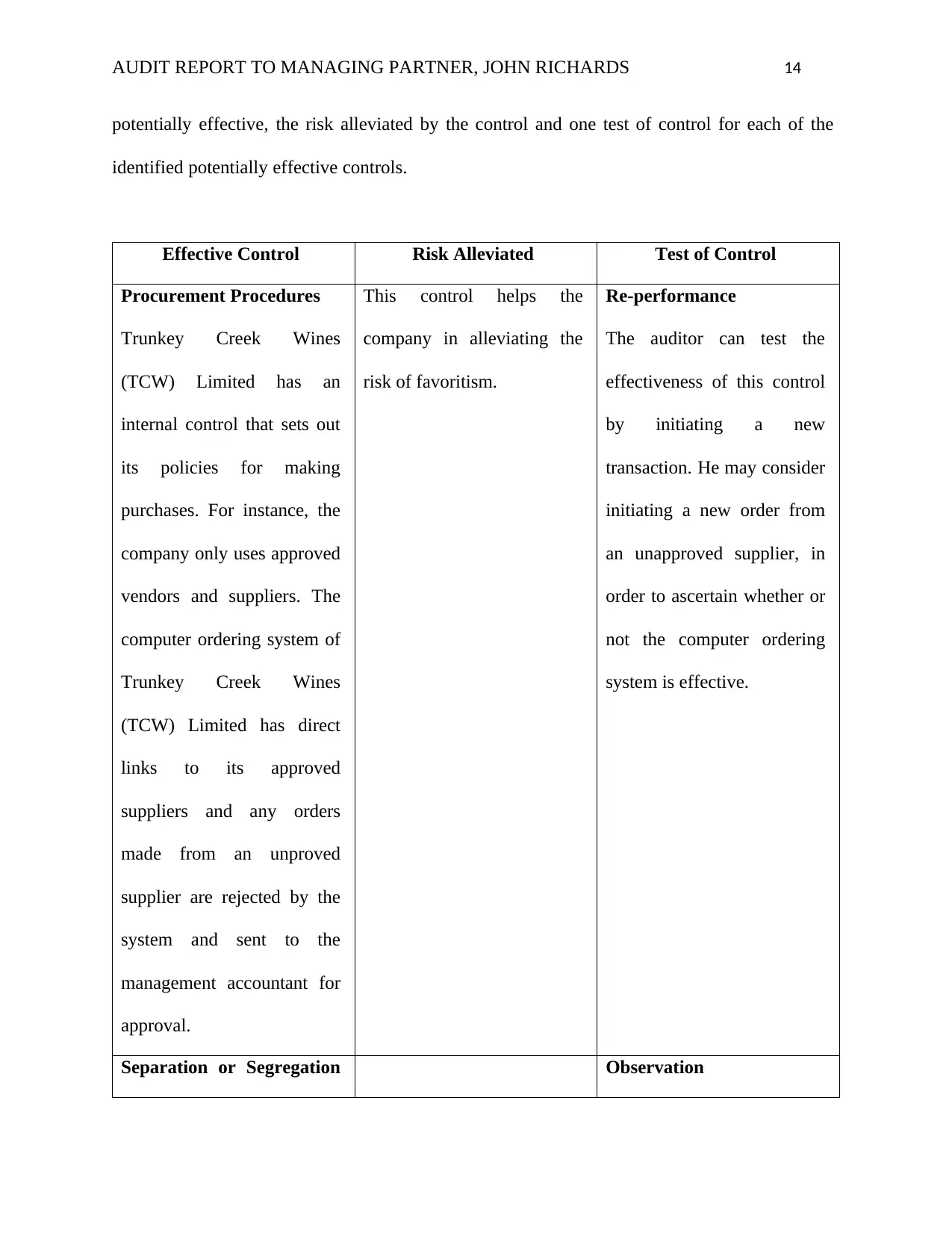

potentially effective, the risk alleviated by the control and one test of control for each of the

identified potentially effective controls.

Effective Control Risk Alleviated Test of Control

Procurement Procedures

Trunkey Creek Wines

(TCW) Limited has an

internal control that sets out

its policies for making

purchases. For instance, the

company only uses approved

vendors and suppliers. The

computer ordering system of

Trunkey Creek Wines

(TCW) Limited has direct

links to its approved

suppliers and any orders

made from an unproved

supplier are rejected by the

system and sent to the

management accountant for

approval.

This control helps the

company in alleviating the

risk of favoritism.

Re-performance

The auditor can test the

effectiveness of this control

by initiating a new

transaction. He may consider

initiating a new order from

an unapproved supplier, in

order to ascertain whether or

not the computer ordering

system is effective.

Separation or Segregation Observation

potentially effective, the risk alleviated by the control and one test of control for each of the

identified potentially effective controls.

Effective Control Risk Alleviated Test of Control

Procurement Procedures

Trunkey Creek Wines

(TCW) Limited has an

internal control that sets out

its policies for making

purchases. For instance, the

company only uses approved

vendors and suppliers. The

computer ordering system of

Trunkey Creek Wines

(TCW) Limited has direct

links to its approved

suppliers and any orders

made from an unproved

supplier are rejected by the

system and sent to the

management accountant for

approval.

This control helps the

company in alleviating the

risk of favoritism.

Re-performance

The auditor can test the

effectiveness of this control

by initiating a new

transaction. He may consider

initiating a new order from

an unapproved supplier, in

order to ascertain whether or

not the computer ordering

system is effective.

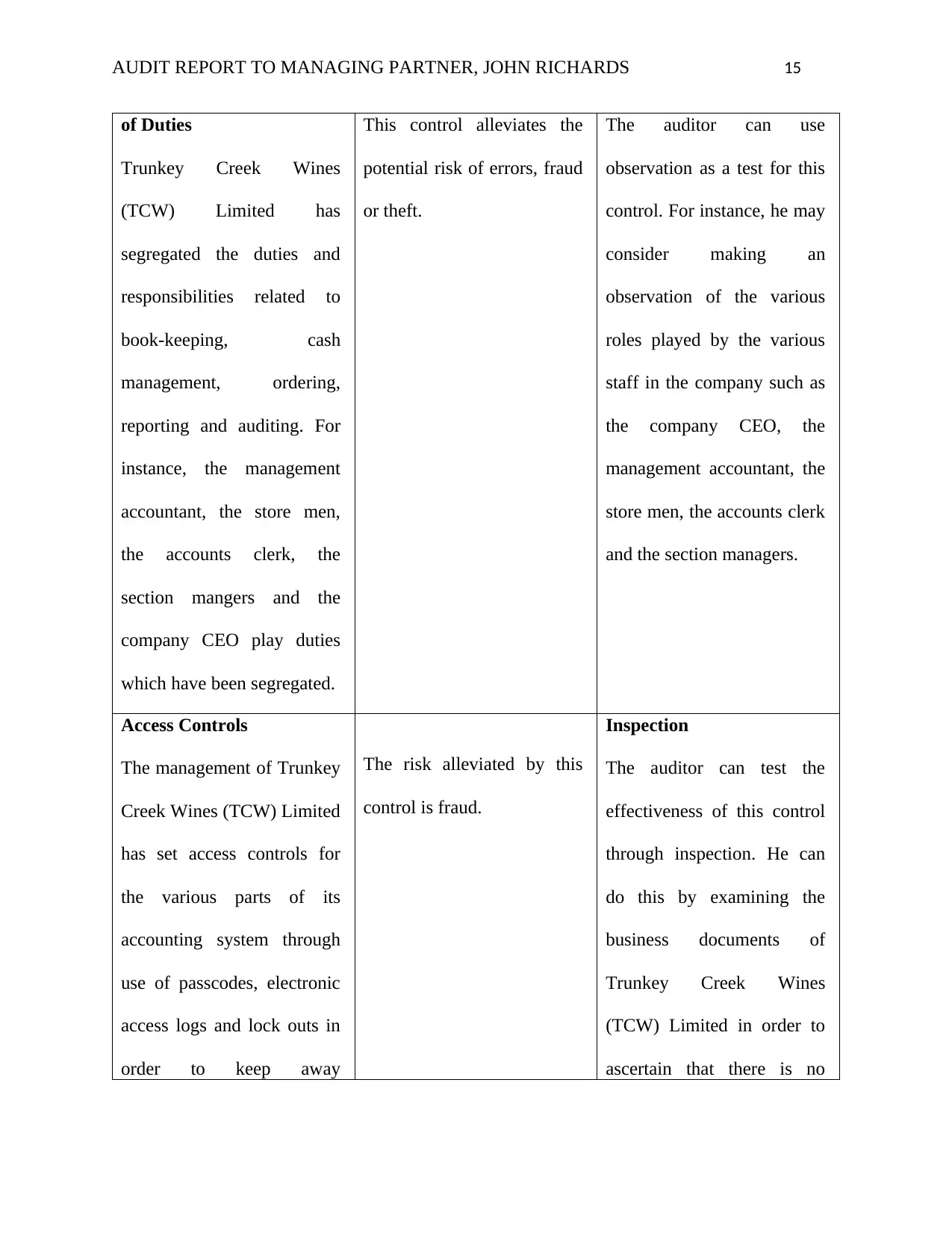

Separation or Segregation Observation

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 15

of Duties

Trunkey Creek Wines

(TCW) Limited has

segregated the duties and

responsibilities related to

book-keeping, cash

management, ordering,

reporting and auditing. For

instance, the management

accountant, the store men,

the accounts clerk, the

section mangers and the

company CEO play duties

which have been segregated.

This control alleviates the

potential risk of errors, fraud

or theft.

The auditor can use

observation as a test for this

control. For instance, he may

consider making an

observation of the various

roles played by the various

staff in the company such as

the company CEO, the

management accountant, the

store men, the accounts clerk

and the section managers.

Access Controls

The management of Trunkey

Creek Wines (TCW) Limited

has set access controls for

the various parts of its

accounting system through

use of passcodes, electronic

access logs and lock outs in

order to keep away

The risk alleviated by this

control is fraud.

Inspection

The auditor can test the

effectiveness of this control

through inspection. He can

do this by examining the

business documents of

Trunkey Creek Wines

(TCW) Limited in order to

ascertain that there is no

of Duties

Trunkey Creek Wines

(TCW) Limited has

segregated the duties and

responsibilities related to

book-keeping, cash

management, ordering,

reporting and auditing. For

instance, the management

accountant, the store men,

the accounts clerk, the

section mangers and the

company CEO play duties

which have been segregated.

This control alleviates the

potential risk of errors, fraud

or theft.

The auditor can use

observation as a test for this

control. For instance, he may

consider making an

observation of the various

roles played by the various

staff in the company such as

the company CEO, the

management accountant, the

store men, the accounts clerk

and the section managers.

Access Controls

The management of Trunkey

Creek Wines (TCW) Limited

has set access controls for

the various parts of its

accounting system through

use of passcodes, electronic

access logs and lock outs in

order to keep away

The risk alleviated by this

control is fraud.

Inspection

The auditor can test the

effectiveness of this control

through inspection. He can

do this by examining the

business documents of

Trunkey Creek Wines

(TCW) Limited in order to

ascertain that there is no

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 16

unauthorized parties. access granted to

unauthorized parties.

Approvals and Authority

According to the set internal

controls of Trunkey Creek

Wines (TCW) Limited, only

certain managers are

required to sign specific

transactions. For instance,

the company has three

section managers, one each

for grape production, wine

production and beef

production. Each can order

supplies for their respective

operations up to a limit of

$10,000 for each order.

Orders between $10,000 and

$30,000 must be approved

by the management

accountant. Orders over

$30,000 must be approved

by the CEO. Orders over

This control helps in

alleviating the risk of theft

and fraud, which may be

perpetuated by the

company’s employees if

given an authority to approve

certain business transactions.

Inspection and

Observation

In order to test the

effectiveness of this control,

the auditor must inspect the

various policies and

procedures of the company

that must be followed in

regard to approval and

authorization of certain

matters and transactions of

the company. He must also

seek to make an observation

as to whether or not the set

procedures and policies are

appropriately adhered to.

unauthorized parties. access granted to

unauthorized parties.

Approvals and Authority

According to the set internal

controls of Trunkey Creek

Wines (TCW) Limited, only

certain managers are

required to sign specific

transactions. For instance,

the company has three

section managers, one each

for grape production, wine

production and beef

production. Each can order

supplies for their respective

operations up to a limit of

$10,000 for each order.

Orders between $10,000 and

$30,000 must be approved

by the management

accountant. Orders over

$30,000 must be approved

by the CEO. Orders over

This control helps in

alleviating the risk of theft

and fraud, which may be

perpetuated by the

company’s employees if

given an authority to approve

certain business transactions.

Inspection and

Observation

In order to test the

effectiveness of this control,

the auditor must inspect the

various policies and

procedures of the company

that must be followed in

regard to approval and

authorization of certain

matters and transactions of

the company. He must also

seek to make an observation

as to whether or not the set

procedures and policies are

appropriately adhered to.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 17

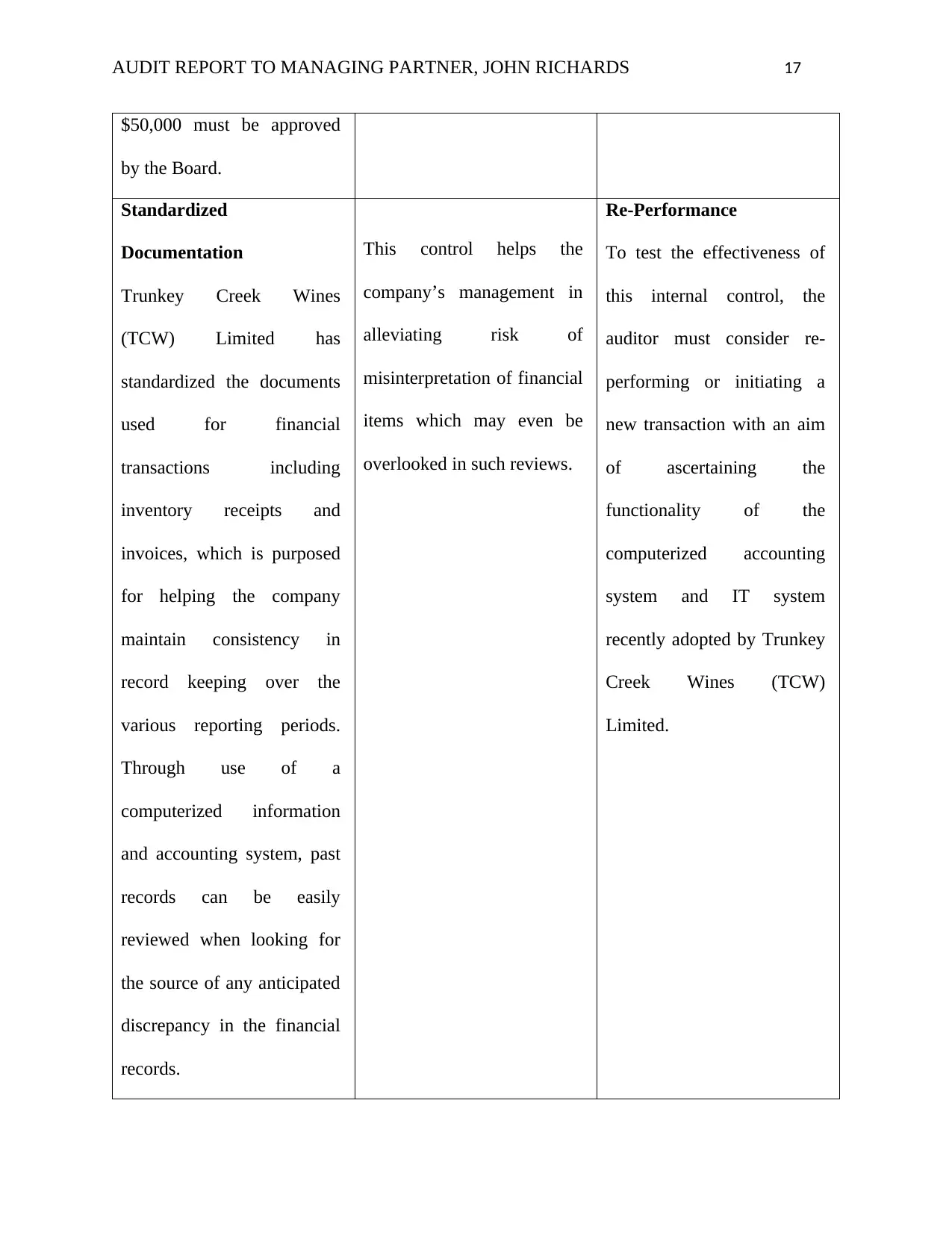

$50,000 must be approved

by the Board.

Standardized

Documentation

Trunkey Creek Wines

(TCW) Limited has

standardized the documents

used for financial

transactions including

inventory receipts and

invoices, which is purposed

for helping the company

maintain consistency in

record keeping over the

various reporting periods.

Through use of a

computerized information

and accounting system, past

records can be easily

reviewed when looking for

the source of any anticipated

discrepancy in the financial

records.

This control helps the

company’s management in

alleviating risk of

misinterpretation of financial

items which may even be

overlooked in such reviews.

Re-Performance

To test the effectiveness of

this internal control, the

auditor must consider re-

performing or initiating a

new transaction with an aim

of ascertaining the

functionality of the

computerized accounting

system and IT system

recently adopted by Trunkey

Creek Wines (TCW)

Limited.

$50,000 must be approved

by the Board.

Standardized

Documentation

Trunkey Creek Wines

(TCW) Limited has

standardized the documents

used for financial

transactions including

inventory receipts and

invoices, which is purposed

for helping the company

maintain consistency in

record keeping over the

various reporting periods.

Through use of a

computerized information

and accounting system, past

records can be easily

reviewed when looking for

the source of any anticipated

discrepancy in the financial

records.

This control helps the

company’s management in

alleviating risk of

misinterpretation of financial

items which may even be

overlooked in such reviews.

Re-Performance

To test the effectiveness of

this internal control, the

auditor must consider re-

performing or initiating a

new transaction with an aim

of ascertaining the

functionality of the

computerized accounting

system and IT system

recently adopted by Trunkey

Creek Wines (TCW)

Limited.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 18

Question 2B

Upon reviewing the internal control system of Trunkey Creek Wines (TCW) Limited,

there were various weaknesses that were observed in internal control for purchases and accounts

payable (Association of Chartered Certified Accountants, 2010). The following table gives a

summary of the internal control weaknesses of purchases and accounts payable for the company

in question.

Weakness Justification

Lack of second person authorization for

services received.

When services such as repairs are ordered for

the winery by the wine production manager,

a service order is generated within the

computer system and automatically sent to

the service provider. When the service has

been delivered, the wine production manager

or the store man signs the service delivery

docket on the service man’s tablet. Any

discrepancies between services delivered and

delivery docket are only approved by the

production manager or the store man.

Therefore, there is no another person who is

authorized for such an approval in case the

manager and the store man are absent.

Question 2B

Upon reviewing the internal control system of Trunkey Creek Wines (TCW) Limited,

there were various weaknesses that were observed in internal control for purchases and accounts

payable (Association of Chartered Certified Accountants, 2010). The following table gives a

summary of the internal control weaknesses of purchases and accounts payable for the company

in question.

Weakness Justification

Lack of second person authorization for

services received.

When services such as repairs are ordered for

the winery by the wine production manager,

a service order is generated within the

computer system and automatically sent to

the service provider. When the service has

been delivered, the wine production manager

or the store man signs the service delivery

docket on the service man’s tablet. Any

discrepancies between services delivered and

delivery docket are only approved by the

production manager or the store man.

Therefore, there is no another person who is

authorized for such an approval in case the

manager and the store man are absent.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 19

Lack of segregation of duties with regard to

payments

For instance, the management accountant is

responsible for approving the payments file

and recording it as paid in the accounting

system at the same time. The payments file is

approved online by the management

accountant once a week and used to generate

an ABA file which is then uploaded to the

bank by the management accountant. When

the payments file is approved by the

management accountant, the invoice is

automatically recorded as being paid in the

accounting system. Again, there is no second

person who approves the file.

Order sequence is not considered.

While making purchase orders, Trunkey

Creek Wines (TCW) Limited does not

consider the sequence of the orders including

those that are cancelled. This puts the

company at a risk of having misplaced orders

that may make the purchase transaction not

to occur.

Lack of a goods inwards or receiving

department.

Trunkey Creek Wines (TCW) Limited does

not have an established department for

receiving all the incoming goods and

Lack of segregation of duties with regard to

payments

For instance, the management accountant is

responsible for approving the payments file

and recording it as paid in the accounting

system at the same time. The payments file is

approved online by the management

accountant once a week and used to generate

an ABA file which is then uploaded to the

bank by the management accountant. When

the payments file is approved by the

management accountant, the invoice is

automatically recorded as being paid in the

accounting system. Again, there is no second

person who approves the file.

Order sequence is not considered.

While making purchase orders, Trunkey

Creek Wines (TCW) Limited does not

consider the sequence of the orders including

those that are cancelled. This puts the

company at a risk of having misplaced orders

that may make the purchase transaction not

to occur.

Lack of a goods inwards or receiving

department.

Trunkey Creek Wines (TCW) Limited does

not have an established department for

receiving all the incoming goods and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 20

inventory, including even the fixed assets of

the company.

Lack of verifiable independent price list. The purchasing officers of Trunkey Creek

Wines (TCW) Limited rely mainly on their

personal knowledge since there is no

verifiable and independent list of prices or

catalogue that helps in ensuring that the

prices of suppliers are accurate. This could

make recording of prices to be overstated or

understated.

Lack of appropriate evidence on invoices

The purchasing system of Trunkey Creek

Wines (TCW) Limited has not does not have

appropriate evidence on invoices for

indicating that various internal checks have

been carried out by the authorized staff of the

company.

Lack of independent checks of stock.

Trunkey Creek Wines (TCW) Limited does

not adopt an approach in which the

company’s stock is independently checked

against the purchase requisition. This may

lead to overstocking.

Lack of comparison checks.

There are no checks for comparisons

between the receiving records and the reports

of inspection. This could lead to no

inventory, including even the fixed assets of

the company.

Lack of verifiable independent price list. The purchasing officers of Trunkey Creek

Wines (TCW) Limited rely mainly on their

personal knowledge since there is no

verifiable and independent list of prices or

catalogue that helps in ensuring that the

prices of suppliers are accurate. This could

make recording of prices to be overstated or

understated.

Lack of appropriate evidence on invoices

The purchasing system of Trunkey Creek

Wines (TCW) Limited has not does not have

appropriate evidence on invoices for

indicating that various internal checks have

been carried out by the authorized staff of the

company.

Lack of independent checks of stock.

Trunkey Creek Wines (TCW) Limited does

not adopt an approach in which the

company’s stock is independently checked

against the purchase requisition. This may

lead to overstocking.

Lack of comparison checks.

There are no checks for comparisons

between the receiving records and the reports

of inspection. This could lead to no

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 21

guarantee as to whether every item of

inventory received is in a perfect condition or

not, as required.

Conclusion

As discussed above, there are various audit risks faced by Trunkey Creek Wines (TCW)

Limited with regard to the four areas and accounts, which are account receivable, property

assets, investments and marketing expenses. Audit risk refers to the risk of the possibility that

the financial statements of a company may still be misstated materially, even though it has been

stated in the audit opinion that the financial statements and financial information presented

therein are free from any material misstatements and errors. Trunkey Creek Wines (TCW)

Limited also faces various business risks such as strategic risks, operational risks, compliance

risks, technological risks, legal risks, financial risks, human risks and competitive risks.

Business risk refers to the possibility that an organization will not achieve its goals and

objectives, and may not generate the desired financial results. Business risk is influenced by

factors such as price per unit, volume of sales, cost of inputs, competition, government

regulations and the overall economic climate. Furthermore, Trunkey Creek Wines (TCW)

Limited has internal controls which are potentially effective. These controls have helped it in

alleviating or reducing the various risks that could have otherwise affected the company

adversely. The company also has certain weaknesses in its system of internal controls for

purchases and payments. These have been discussed in the above sections.

guarantee as to whether every item of

inventory received is in a perfect condition or

not, as required.

Conclusion

As discussed above, there are various audit risks faced by Trunkey Creek Wines (TCW)

Limited with regard to the four areas and accounts, which are account receivable, property

assets, investments and marketing expenses. Audit risk refers to the risk of the possibility that

the financial statements of a company may still be misstated materially, even though it has been

stated in the audit opinion that the financial statements and financial information presented

therein are free from any material misstatements and errors. Trunkey Creek Wines (TCW)

Limited also faces various business risks such as strategic risks, operational risks, compliance

risks, technological risks, legal risks, financial risks, human risks and competitive risks.

Business risk refers to the possibility that an organization will not achieve its goals and

objectives, and may not generate the desired financial results. Business risk is influenced by

factors such as price per unit, volume of sales, cost of inputs, competition, government

regulations and the overall economic climate. Furthermore, Trunkey Creek Wines (TCW)

Limited has internal controls which are potentially effective. These controls have helped it in

alleviating or reducing the various risks that could have otherwise affected the company

adversely. The company also has certain weaknesses in its system of internal controls for

purchases and payments. These have been discussed in the above sections.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 22

References

Association of Chartered Certified Accountants (Great Britain). (2010). Implementing audit

procedures (international stream). London: BPP.

BPP Learning Media (Firm). (2012). CPA Australia, for exams in 2012: Passcards. London:

BPP Learning Media.

Bragg, S. M. (2011). Bookkeeping essentials: How to succeed as a bookkeeper. Hoboken, NJ:

Wiley.

Cascarino, R., & Cascarino, R. (2012). Auditor's guide to IT auditing. Hoboken, NJ: Wiley.

Chartered Association of Certified Accountants (Great Britain). (2011). Implementing audit

procedures (UK): FIA FAU foundations in audit (UK). London: BPP.

Cosserat, G. W., & Rodda, N. (2009). Modern auditing. Chichester, UK: John Wiley & Sons.

Fiedler, B., & Fiedler, B. (2010). Student guide to accompany Essentials of auditing, assurance

services and ethics in Australia: An integrated approach [1st ed.]. Frenchs Forest,

NSW: Pearson Australia.

Fiedler, & Brenton Andrew. (2010). Student guide to accompany essentials of auditing,

assurance services and ethics in Australia: an integrated approach. Australia: Pearson

Australia.

Gay, G. E., & Simnett, R. (2018). Auditing and assurance services in Australia. North Ryde,

N.S.W: McGraw-Hill Education (Australia.

Hanson, A. W., & Hanson, A. W. (2008). Auditing theory and its application.

Hay, D. (2014). Auditing, International Auditing and the International Journal of Auditing:

Editorial. International Journal of Auditing, 18(1), 1-1. doi:10.1111/ijau.12020

References

Association of Chartered Certified Accountants (Great Britain). (2010). Implementing audit

procedures (international stream). London: BPP.

BPP Learning Media (Firm). (2012). CPA Australia, for exams in 2012: Passcards. London:

BPP Learning Media.

Bragg, S. M. (2011). Bookkeeping essentials: How to succeed as a bookkeeper. Hoboken, NJ:

Wiley.

Cascarino, R., & Cascarino, R. (2012). Auditor's guide to IT auditing. Hoboken, NJ: Wiley.

Chartered Association of Certified Accountants (Great Britain). (2011). Implementing audit

procedures (UK): FIA FAU foundations in audit (UK). London: BPP.

Cosserat, G. W., & Rodda, N. (2009). Modern auditing. Chichester, UK: John Wiley & Sons.

Fiedler, B., & Fiedler, B. (2010). Student guide to accompany Essentials of auditing, assurance

services and ethics in Australia: An integrated approach [1st ed.]. Frenchs Forest,

NSW: Pearson Australia.

Fiedler, & Brenton Andrew. (2010). Student guide to accompany essentials of auditing,

assurance services and ethics in Australia: an integrated approach. Australia: Pearson

Australia.

Gay, G. E., & Simnett, R. (2018). Auditing and assurance services in Australia. North Ryde,

N.S.W: McGraw-Hill Education (Australia.

Hanson, A. W., & Hanson, A. W. (2008). Auditing theory and its application.

Hay, D. (2014). Auditing, International Auditing and the International Journal of Auditing:

Editorial. International Journal of Auditing, 18(1), 1-1. doi:10.1111/ijau.12020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 23

Hayes, R., Gortemaker, H., & Wallage, P. (2014). Principles of auditing: An introduction to

international standards on auditing. Harlow: Pearson Education Limited.

Institute of Chartered Accountants in England and Wales. (2010). Audit and assurance:

Advanced stage technical integration level: study manual. London: Author.

Jubb, C. (2010). Assurance & auditing: Concepts for a changing environment. s.l.: Thomson

Learning.

Key, J., Riddle, C., & Institute of Internal Auditors. (2012). Sawyer's: Guide for internal

auditors. Altamonte Springs, FL: Institute of Internal Auditors Research Foundation.

Lessambo, F. I. (2018). Forensic Auditing. Auditing, Assurance Services, and Forensics, 447-

468. doi:10.1007/978-3-319-90521-1_25

Liu, J. (2015). Study on the Auditing Theory of Socialism with Chinese Characteristics, Revised

Edition. Hoboken: Wiley.

Maroun, W. (2018). Modifying assurance practices to meet the needs of integrated

reporting. Accounting, Auditing & Accountability Journal, 31(2), 400-427.

doi:10.1108/aaaj-10-2016-2732

Pickett, K. H. (2013). The internal auditing handbook. Hoboken, NJ: Wiley.

Reding, K. F., & Institute of Internal Auditors Research Foundation. IIARF. (2013). Internal

auditing: Assurance & consulting services. Altomonte Springs, Fla.

Russell, J. P., & ASQ Quality Audit Division. (2013). The ASQ auditing handbook: Principles,

implementation, and use. Milwaukee, Wis: ASQ Quality Press.

Takanen, A., Demott, J. D., & Miller, C. (2008). Fuzzing for software security testing and

quality assurance. Boston: Artech House.

Verschoor, C. C. (2008). Audit committee essentials. Hoboken, NJ: John Wiley & Sons, Inc.

Hayes, R., Gortemaker, H., & Wallage, P. (2014). Principles of auditing: An introduction to

international standards on auditing. Harlow: Pearson Education Limited.

Institute of Chartered Accountants in England and Wales. (2010). Audit and assurance:

Advanced stage technical integration level: study manual. London: Author.

Jubb, C. (2010). Assurance & auditing: Concepts for a changing environment. s.l.: Thomson

Learning.

Key, J., Riddle, C., & Institute of Internal Auditors. (2012). Sawyer's: Guide for internal

auditors. Altamonte Springs, FL: Institute of Internal Auditors Research Foundation.

Lessambo, F. I. (2018). Forensic Auditing. Auditing, Assurance Services, and Forensics, 447-

468. doi:10.1007/978-3-319-90521-1_25

Liu, J. (2015). Study on the Auditing Theory of Socialism with Chinese Characteristics, Revised

Edition. Hoboken: Wiley.

Maroun, W. (2018). Modifying assurance practices to meet the needs of integrated

reporting. Accounting, Auditing & Accountability Journal, 31(2), 400-427.

doi:10.1108/aaaj-10-2016-2732

Pickett, K. H. (2013). The internal auditing handbook. Hoboken, NJ: Wiley.

Reding, K. F., & Institute of Internal Auditors Research Foundation. IIARF. (2013). Internal

auditing: Assurance & consulting services. Altomonte Springs, Fla.

Russell, J. P., & ASQ Quality Audit Division. (2013). The ASQ auditing handbook: Principles,

implementation, and use. Milwaukee, Wis: ASQ Quality Press.

Takanen, A., Demott, J. D., & Miller, C. (2008). Fuzzing for software security testing and

quality assurance. Boston: Artech House.

Verschoor, C. C. (2008). Audit committee essentials. Hoboken, NJ: John Wiley & Sons, Inc.

AUDIT REPORT TO MANAGING PARTNER, JOHN RICHARDS 24

Wells, J. T. (2014). Principles of fraud examination. (Online version ---> Principles of fraud

examination.) Hoboken, NJ: Wiley & Sons, Inc.

Wells, J. T. (2014). Principles of fraud examination. (Online version ---> Principles of fraud

examination.) Hoboken, NJ: Wiley & Sons, Inc.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.