Analysis of Audit Risk, Analysis and Control in Organization

VerifiedAdded on 2022/08/23

|14

|3344

|28

Report

AI Summary

This report delves into the critical aspects of audit risk, material misstatement, and internal controls within organizations. It begins by defining material misstatement and its impact on stakeholders' financial decisions, differentiating between intentional fraud and unintentional errors. The report explores factors influencing the risk of material misstatement, such as fluctuations in interest rates, the influence of majority shareholders, management's accounting estimate failures, and the implementation of new computer systems. Furthermore, it examines specific audit risks, including material misstatements, revenue recognition issues, and the effectiveness of entity controls. The report highlights the importance of auditor responses to mitigate these risks, emphasizing the need for professional skepticism and thorough evaluation of financial data to ensure accuracy and reliability. The analysis covers the financial data of Darfield Electronics, assessing audit risks associated with revenue recognition, internal controls, and potential misstatements, with a focus on auditor's responsibilities in identifying and mitigating these risks. The report emphasizes the importance of ASA 315 in the context of auditing.

Running head: AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

Audit Risk, Analysis and Control in Organization

Name of the Student

Name of the University

Author Note

Audit Risk, Analysis and Control in Organization

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

Table of Contents

Answer 1....................................................................................................................................2

Factors that affect the Risk of Material Misstatement...............................................................3

1. Fluctuations in the Rate of Interest.................................................................................3

2. The positioning of the majority shareholder...................................................................3

3. Management’s failure in accounting estimates...............................................................4

4. Installation of a new computer system............................................................................5

Answer 2....................................................................................................................................5

Audit Risks.................................................................................................................................6

1. Material Misstatement.....................................................................................................7

2. Revenue Recognition......................................................................................................7

3. Entity’s Control...............................................................................................................8

Auditor’s response.....................................................................................................................8

Material misstatement at the assertion level..........................................................................8

Material misstatement at the financial statement level..........................................................9

Material misstatement Due to fraud.......................................................................................9

Management overrides of control..........................................................................................9

References................................................................................................................................11

Table of Contents

Answer 1....................................................................................................................................2

Factors that affect the Risk of Material Misstatement...............................................................3

1. Fluctuations in the Rate of Interest.................................................................................3

2. The positioning of the majority shareholder...................................................................3

3. Management’s failure in accounting estimates...............................................................4

4. Installation of a new computer system............................................................................5

Answer 2....................................................................................................................................5

Audit Risks.................................................................................................................................6

1. Material Misstatement.....................................................................................................7

2. Revenue Recognition......................................................................................................7

3. Entity’s Control...............................................................................................................8

Auditor’s response.....................................................................................................................8

Material misstatement at the assertion level..........................................................................8

Material misstatement at the financial statement level..........................................................9

Material misstatement Due to fraud.......................................................................................9

Management overrides of control..........................................................................................9

References................................................................................................................................11

2AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

Answer 1

Risk of Material Misstatement

Such information that has been reported incorrectly in the financial reports, and

consequently, it has a negative impact on the stakeholders for their financial decisions, is

known as a material misstatement. The misstatement in the financial reports is considered as

material when it has the ability to influence the decisions made by any stakeholder based on

such reports (Knechel and Salterio 2016). For example, a loan advanced on either small or

big amount to a company’s director is material due to the user of the financial reports will

consider the information provided for decision-making. The information provided in the

reports can be misstated due to either fraud that is intentionally done or error that is an

unintentional misstatement and does not come under fraudulent activity (Kramer 2015).

According to paragraph A136 of ASA 315, there is a possibility to be material of a potential

misstatement, which can also be judged through its extent of nature and circumstance of the

item.

The risk of material misstatement refers to such risk that exists within the financial

report, which is being audited and has the potential of being material either individually or in

aggregate. As per paragraph 25 (a) of ASA 315, an auditor has the option to proceed for risk

assessment in two different levels for material misstatement, which are Assertion level and

Financial report level. Paragraph A122 of ASA 315 states that the risks of material

misstatement at the level of the financial reports have the potential to affect several assertions

(Auasb.gov.au 2020). The material misstatement’s risk in context with the balance of the

account, transactions as well as disclosures at the assertion level requires special

consideration. In obtaining the evidence at the assertion level, the auditor will get help

Answer 1

Risk of Material Misstatement

Such information that has been reported incorrectly in the financial reports, and

consequently, it has a negative impact on the stakeholders for their financial decisions, is

known as a material misstatement. The misstatement in the financial reports is considered as

material when it has the ability to influence the decisions made by any stakeholder based on

such reports (Knechel and Salterio 2016). For example, a loan advanced on either small or

big amount to a company’s director is material due to the user of the financial reports will

consider the information provided for decision-making. The information provided in the

reports can be misstated due to either fraud that is intentionally done or error that is an

unintentional misstatement and does not come under fraudulent activity (Kramer 2015).

According to paragraph A136 of ASA 315, there is a possibility to be material of a potential

misstatement, which can also be judged through its extent of nature and circumstance of the

item.

The risk of material misstatement refers to such risk that exists within the financial

report, which is being audited and has the potential of being material either individually or in

aggregate. As per paragraph 25 (a) of ASA 315, an auditor has the option to proceed for risk

assessment in two different levels for material misstatement, which are Assertion level and

Financial report level. Paragraph A122 of ASA 315 states that the risks of material

misstatement at the level of the financial reports have the potential to affect several assertions

(Auasb.gov.au 2020). The material misstatement’s risk in context with the balance of the

account, transactions as well as disclosures at the assertion level requires special

consideration. In obtaining the evidence at the assertion level, the auditor will get help

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

through these considerations so that to determine the time, nature, and other procedures of an

audit.

Factors that affect the Risk of Material Misstatement

There are several factors present within the entity or environment. The auditors need

these factors to obtain and assess the risk of material misstatement. J Audrey Pearce, who is

an audit partner within an accountant’s firm while planning an audit for Homes South Ltd

that is a finance company, found several risks of material misstatement at the financial

statement level. She has found several information concerns about the company’s

environment. Based on the gathered information by her, the factors that would affect the risk

of material misstatement are as follows:

1. Fluctuations in the Rate of Interest

According to the first information, the company HS is more profitable as compared to

the industry averages. The HS packages and sells the mortgages to the large investments

trusts even after there has been recent volatility in the interest rates. The external factors, in

terms of entity and environment, have the potential to affect the risk of material misstatement.

Paragraph A30 of ASA 315 states about the external factor that the auditor is required to

consider, which is financing availability, economic conditions, inflation, and interest rates.

The value of mortgages can be increased or decrease by the volatility in the interest

rate. However, HS Company has considerable growth in recent years. The differences in the

interest rates can be there while dealing with large investment trusts. The auditors thus have

to consider the value reported within the reports. If the auditor finds any misstated figure,

then it reflects the existence of a risk to material misstatement.

through these considerations so that to determine the time, nature, and other procedures of an

audit.

Factors that affect the Risk of Material Misstatement

There are several factors present within the entity or environment. The auditors need

these factors to obtain and assess the risk of material misstatement. J Audrey Pearce, who is

an audit partner within an accountant’s firm while planning an audit for Homes South Ltd

that is a finance company, found several risks of material misstatement at the financial

statement level. She has found several information concerns about the company’s

environment. Based on the gathered information by her, the factors that would affect the risk

of material misstatement are as follows:

1. Fluctuations in the Rate of Interest

According to the first information, the company HS is more profitable as compared to

the industry averages. The HS packages and sells the mortgages to the large investments

trusts even after there has been recent volatility in the interest rates. The external factors, in

terms of entity and environment, have the potential to affect the risk of material misstatement.

Paragraph A30 of ASA 315 states about the external factor that the auditor is required to

consider, which is financing availability, economic conditions, inflation, and interest rates.

The value of mortgages can be increased or decrease by the volatility in the interest

rate. However, HS Company has considerable growth in recent years. The differences in the

interest rates can be there while dealing with large investment trusts. The auditors thus have

to consider the value reported within the reports. If the auditor finds any misstated figure,

then it reflects the existence of a risk to material misstatement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

2. The positioning of the majority shareholder

In the second information, she has found that George Watson controls the Board of

Directors of HS Ltd. He is the majority shareholder who also acts as the power of Chief

Executive Officer. The branch office’s management has the authority for directing and

controlling the operation of the company and compensate as per the profitability of the

branch. The information collected here can be combined so that to get an extent to the truth of

the reporting.

The performance measure of the company, Homes South Ltd., shows unusual

profitability or growth in its business while working within the same industry. There is a

possibility of risk existing in terms of the biases of the management while maintaining the

financial report. This is due to the factors combined with the data, such as incentives and

bonuses. It is reflecting an unexpected outcome or trend. There may be a possibility to be bias

in context to the company’s profitability or putting data in the reports (Cao, Chychyla and

Stewart 2015). Thus, these factors may also affect the risk of material misstatement. As per

Paragraph A48 of ASA 315, the auditor shall take internal measures that highlight the

unexpected result or trend.

3. Management’s failure in accounting estimates

The company’s accounting department in the last five years has experienced a minor

turnover in personnel. J Audrey Pearce has involved in these auditing processes. During her

past five years auditing HS Ltd., she has found that the company’s formula generally

underestimates the allowances for loan losses. However, its financial controller always tends

to increase its allowance (Backof, Bowlin and Goodson 2014). Further, the company has an

open branch office, which is not yet profitable. Nevertheless, they believe to earn profit by

the year 2021.

2. The positioning of the majority shareholder

In the second information, she has found that George Watson controls the Board of

Directors of HS Ltd. He is the majority shareholder who also acts as the power of Chief

Executive Officer. The branch office’s management has the authority for directing and

controlling the operation of the company and compensate as per the profitability of the

branch. The information collected here can be combined so that to get an extent to the truth of

the reporting.

The performance measure of the company, Homes South Ltd., shows unusual

profitability or growth in its business while working within the same industry. There is a

possibility of risk existing in terms of the biases of the management while maintaining the

financial report. This is due to the factors combined with the data, such as incentives and

bonuses. It is reflecting an unexpected outcome or trend. There may be a possibility to be bias

in context to the company’s profitability or putting data in the reports (Cao, Chychyla and

Stewart 2015). Thus, these factors may also affect the risk of material misstatement. As per

Paragraph A48 of ASA 315, the auditor shall take internal measures that highlight the

unexpected result or trend.

3. Management’s failure in accounting estimates

The company’s accounting department in the last five years has experienced a minor

turnover in personnel. J Audrey Pearce has involved in these auditing processes. During her

past five years auditing HS Ltd., she has found that the company’s formula generally

underestimates the allowances for loan losses. However, its financial controller always tends

to increase its allowance (Backof, Bowlin and Goodson 2014). Further, the company has an

open branch office, which is not yet profitable. Nevertheless, they believe to earn profit by

the year 2021.

5AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

There is an existing factor of risk of material misstatement due to the failure of

accounting estimation. As J Audrey Pearce has been the witness for the last five years. The

company’s reporting can also have an entity risk that is arising from the business’s

expansion. It may be possible that demand has not been weighed accurately while deciding

on an expansion. Therefore, these are contributing to the risk of material misstatement.

Paragraph A40 states some components included in the material misstatement that is new

products or services, industry development, and expansion of the business as well. The

auditor shall consider the risk related to the entity that may have resulted in a material

misstatement.

4. Installation of a new computer system

In the last information collected by J Audrey Pearce, she mentions that the company

has increased its operation’s efficiency by installing a new computer system during the year

2019. The company has the risk associated with the operating style of the management’s

operations. The personnel handling the computer system may reduce the risk, but they cannot

mitigate the management from being bias within their operations to increase their earnings.

The high risk involved in the material misstatement results in the lower level of detecting risk

because of sufficient evidence collected from the audit processes.

According to Paragraph A82, independent boards of directors of the company have

the potential to influence the decision of the management, which includes a maximum chance

of the risk of material misstatement (Auasb.gov.au 2020). An auditor must not ignore the

importance of ASA 315 as the standard mentions different requirements for assessing the risk

of material misstatement. The auditor can reduce the risk by ensuring responsive auditing to

the client or an individual audit through proper use of standards (Defond, Lim and Zang

2016).

There is an existing factor of risk of material misstatement due to the failure of

accounting estimation. As J Audrey Pearce has been the witness for the last five years. The

company’s reporting can also have an entity risk that is arising from the business’s

expansion. It may be possible that demand has not been weighed accurately while deciding

on an expansion. Therefore, these are contributing to the risk of material misstatement.

Paragraph A40 states some components included in the material misstatement that is new

products or services, industry development, and expansion of the business as well. The

auditor shall consider the risk related to the entity that may have resulted in a material

misstatement.

4. Installation of a new computer system

In the last information collected by J Audrey Pearce, she mentions that the company

has increased its operation’s efficiency by installing a new computer system during the year

2019. The company has the risk associated with the operating style of the management’s

operations. The personnel handling the computer system may reduce the risk, but they cannot

mitigate the management from being bias within their operations to increase their earnings.

The high risk involved in the material misstatement results in the lower level of detecting risk

because of sufficient evidence collected from the audit processes.

According to Paragraph A82, independent boards of directors of the company have

the potential to influence the decision of the management, which includes a maximum chance

of the risk of material misstatement (Auasb.gov.au 2020). An auditor must not ignore the

importance of ASA 315 as the standard mentions different requirements for assessing the risk

of material misstatement. The auditor can reduce the risk by ensuring responsive auditing to

the client or an individual audit through proper use of standards (Defond, Lim and Zang

2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

Answer 2

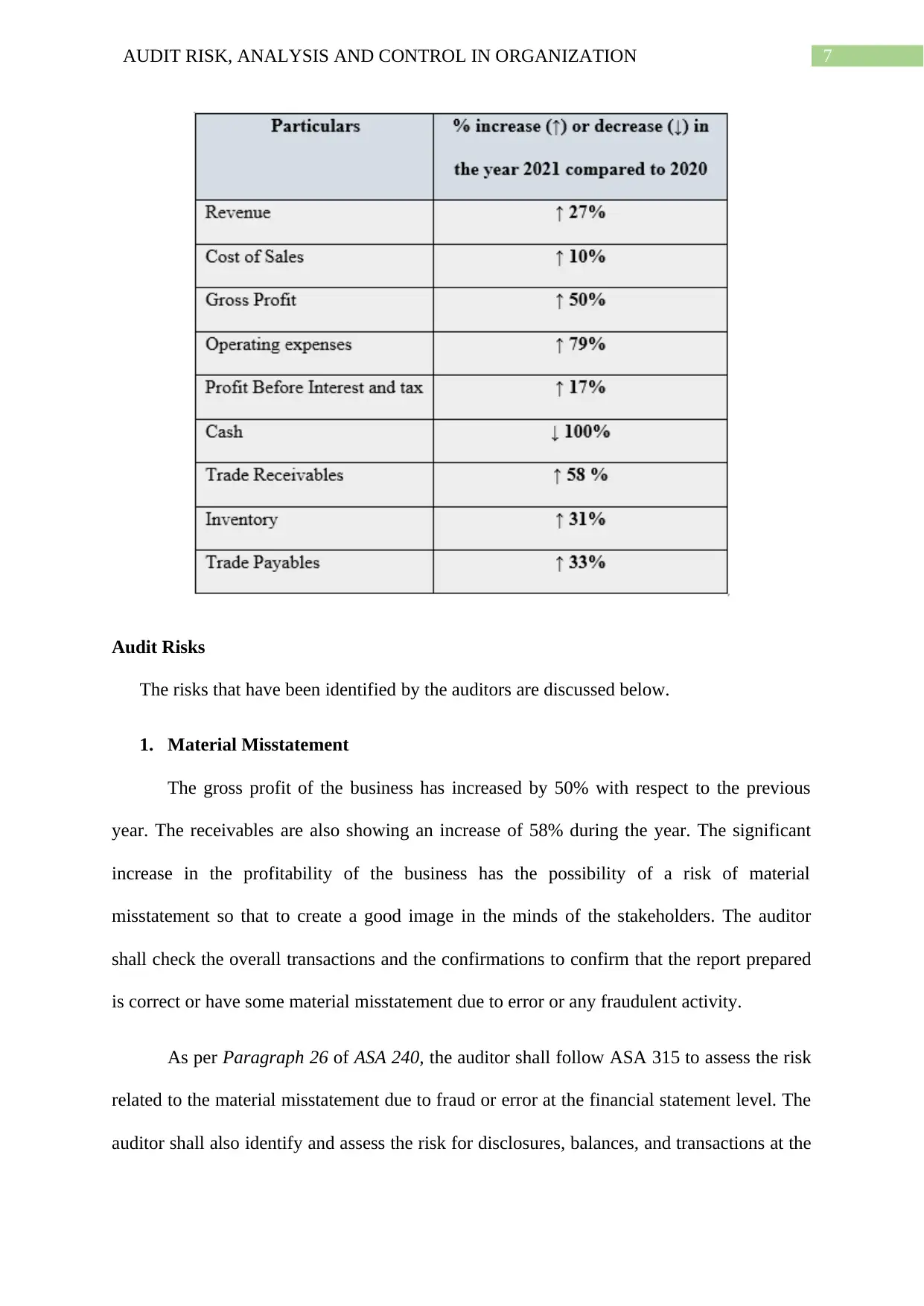

There is a significant increase in the revenue of the Darfield electronics of about 27%

during the year. There is a 31% increase in the inventory, as well as a 10% growth in the cost

of sales. The auditors shall go by evaluating the cost of sales as well as inventory within the

period. However, the business has represented an increase of 33% in the net payables, which

is included in deceasing the cash to zero. The reduction of cash od done along with a certain

amount of bank overdraft. The actions arose a question about the requirement of cash and

bank overdraft at the same time. The operating expense also increases after inventories. The

cost of operating expenses is less concerning its revenue. Comparing the operating expense to

the previous year, it shows a certain increase that seems to be detectable for the deterioration

in the operation’s efficiency during the year. There is the possibility of misstatement in the

reports so that the company can reflect a positive side of it rather than the actual one. The

auditor shall investigate the profitability declared by Darfield Electronics. It is because there

is the possibility of declaring the profits and the business’s current position different from the

actual one. Therefore, Darfield electronics may have the existence of the risk of material

misstatement through which the business can show a positive view of them.

Financial Data for Darfield Electronics

Answer 2

There is a significant increase in the revenue of the Darfield electronics of about 27%

during the year. There is a 31% increase in the inventory, as well as a 10% growth in the cost

of sales. The auditors shall go by evaluating the cost of sales as well as inventory within the

period. However, the business has represented an increase of 33% in the net payables, which

is included in deceasing the cash to zero. The reduction of cash od done along with a certain

amount of bank overdraft. The actions arose a question about the requirement of cash and

bank overdraft at the same time. The operating expense also increases after inventories. The

cost of operating expenses is less concerning its revenue. Comparing the operating expense to

the previous year, it shows a certain increase that seems to be detectable for the deterioration

in the operation’s efficiency during the year. There is the possibility of misstatement in the

reports so that the company can reflect a positive side of it rather than the actual one. The

auditor shall investigate the profitability declared by Darfield Electronics. It is because there

is the possibility of declaring the profits and the business’s current position different from the

actual one. Therefore, Darfield electronics may have the existence of the risk of material

misstatement through which the business can show a positive view of them.

Financial Data for Darfield Electronics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

Audit Risks

The risks that have been identified by the auditors are discussed below.

1. Material Misstatement

The gross profit of the business has increased by 50% with respect to the previous

year. The receivables are also showing an increase of 58% during the year. The significant

increase in the profitability of the business has the possibility of a risk of material

misstatement so that to create a good image in the minds of the stakeholders. The auditor

shall check the overall transactions and the confirmations to confirm that the report prepared

is correct or have some material misstatement due to error or any fraudulent activity.

As per Paragraph 26 of ASA 240, the auditor shall follow ASA 315 to assess the risk

related to the material misstatement due to fraud or error at the financial statement level. The

auditor shall also identify and assess the risk for disclosures, balances, and transactions at the

Audit Risks

The risks that have been identified by the auditors are discussed below.

1. Material Misstatement

The gross profit of the business has increased by 50% with respect to the previous

year. The receivables are also showing an increase of 58% during the year. The significant

increase in the profitability of the business has the possibility of a risk of material

misstatement so that to create a good image in the minds of the stakeholders. The auditor

shall check the overall transactions and the confirmations to confirm that the report prepared

is correct or have some material misstatement due to error or any fraudulent activity.

As per Paragraph 26 of ASA 240, the auditor shall follow ASA 315 to assess the risk

related to the material misstatement due to fraud or error at the financial statement level. The

auditor shall also identify and assess the risk for disclosures, balances, and transactions at the

8AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

assertion level (Kassem and Hugson 2016). Professional Scepticism is one of the important

factors that are necessary for an efficient audit of a financial report of the company. The lack

of professional scepticism can also be a factor that leads to the risk of material misstatement.

It can also be to provide favorable support to the company.

2. Revenue Recognition

Cashflow is the lifeblood of any business. For the effective working of the business,

there is a need for cash flow. Thus, the role of revenue is very essential for a company’s

existence. The amount shown by the Darfield of its PBIT is $1030 and revenue of $5267

during the year. There may be the possibility of a risk of material misstatement due to fraud

or control of the management. Paragraph 27 of ASA 240 states that the company shall have a

risk of fraud-related with the revenue recognition that an auditor shall evaluate based on

presumption. The evaluation process includes identifying and assessing the risk of revenue

recognition through evaluating the type of revenue, revenue transactions, or assertions that

have the potential to give rise to the risk of material misstatement.

3. Entity’s Control

It may be possible to have some risk of being affected due to certain limitations of

internal control of the management. Paragraph A54 of ASA 315, the internal control’s

effectiveness provides a reasonable assurance so that to avail the purpose of financial

reporting. Therefore, the risk if material mistreatment can arise due to the management’s

internal control. The decision made within the entity can have some fault or human error.

Further, a situation may arise to override of internal control by not an appropriate

management (Donelson, Ege and Mcinnis 2016). The company may have a possibility that its

management had entered into a separate agreement with the clients. This can be for

assertion level (Kassem and Hugson 2016). Professional Scepticism is one of the important

factors that are necessary for an efficient audit of a financial report of the company. The lack

of professional scepticism can also be a factor that leads to the risk of material misstatement.

It can also be to provide favorable support to the company.

2. Revenue Recognition

Cashflow is the lifeblood of any business. For the effective working of the business,

there is a need for cash flow. Thus, the role of revenue is very essential for a company’s

existence. The amount shown by the Darfield of its PBIT is $1030 and revenue of $5267

during the year. There may be the possibility of a risk of material misstatement due to fraud

or control of the management. Paragraph 27 of ASA 240 states that the company shall have a

risk of fraud-related with the revenue recognition that an auditor shall evaluate based on

presumption. The evaluation process includes identifying and assessing the risk of revenue

recognition through evaluating the type of revenue, revenue transactions, or assertions that

have the potential to give rise to the risk of material misstatement.

3. Entity’s Control

It may be possible to have some risk of being affected due to certain limitations of

internal control of the management. Paragraph A54 of ASA 315, the internal control’s

effectiveness provides a reasonable assurance so that to avail the purpose of financial

reporting. Therefore, the risk if material mistreatment can arise due to the management’s

internal control. The decision made within the entity can have some fault or human error.

Further, a situation may arise to override of internal control by not an appropriate

management (Donelson, Ege and Mcinnis 2016). The company may have a possibility that its

management had entered into a separate agreement with the clients. This can be for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

modifying the terms and conditions of the sales contract, which is resulting in poor revenue

recognition.

Auditor’s response

The response of the auditors consisting of assigning experienced staff or highly

skilled staff so that it provides keen supervision. (Auasb.gov.au 2020) The auditor's response

to address and assessed risk is through highlighting to the audit team so that to maintain the

sustainability of professional scepticism. The auditor shall incorporate some additional

elements of unpredictability or can make general changes concerning the time, nature, and

audit process to a suitable extent.

Material misstatement at the assertion level

The risks at the assertion level are included in inherent risk and controlled risk.

Inherent risk is considered as an assertion to misstatement due to error or fraud before

considering controls. Control risk of the misstatement will not be prevented through reporting

the internal control of an entity. Paragraph 6 of ASA 330 states that the auditor shall plan and

proceed with the process of audit, which is responsive to the time, nature, and extent or based

on the assessed risk of material misstatements (Fortvingler 2016). ASA 330 guides the

auditor to plan and perform the process of audit. The auditor shall consider every transaction,

which is included in its similarity, characteristics, accounts, and disclosure through attaining

evidence.

Material misstatement at the financial statement level

The financial statement of a company is such a report that has several users who make

their economic decisions based on such reports. Therefore, any misstatement incurred to that

can affect the economic conditions of users or nation (Moroney and Trotman 2016).

Paragraph A1 of ASA 330 states that the response of an auditor shall address the risk through

modifying the terms and conditions of the sales contract, which is resulting in poor revenue

recognition.

Auditor’s response

The response of the auditors consisting of assigning experienced staff or highly

skilled staff so that it provides keen supervision. (Auasb.gov.au 2020) The auditor's response

to address and assessed risk is through highlighting to the audit team so that to maintain the

sustainability of professional scepticism. The auditor shall incorporate some additional

elements of unpredictability or can make general changes concerning the time, nature, and

audit process to a suitable extent.

Material misstatement at the assertion level

The risks at the assertion level are included in inherent risk and controlled risk.

Inherent risk is considered as an assertion to misstatement due to error or fraud before

considering controls. Control risk of the misstatement will not be prevented through reporting

the internal control of an entity. Paragraph 6 of ASA 330 states that the auditor shall plan and

proceed with the process of audit, which is responsive to the time, nature, and extent or based

on the assessed risk of material misstatements (Fortvingler 2016). ASA 330 guides the

auditor to plan and perform the process of audit. The auditor shall consider every transaction,

which is included in its similarity, characteristics, accounts, and disclosure through attaining

evidence.

Material misstatement at the financial statement level

The financial statement of a company is such a report that has several users who make

their economic decisions based on such reports. Therefore, any misstatement incurred to that

can affect the economic conditions of users or nation (Moroney and Trotman 2016).

Paragraph A1 of ASA 330 states that the response of an auditor shall address the risk through

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

sustaining professional scepticism. The staff involved in the audit procedure shall be

experienced or skilled personnel (Czerney, Schmidt and Thompson 2014). There may be

some extent, and an auditor can bring some relevant changes in the audit procedures

according to the requirement.

Material misstatement Due to fraud

An intentional doing that leads to material misstatement within the report of an entity

is considered fraudulent activity and misstatement by fraud. As per ASA 330, the auditor shall

be responsible for determining the entire response to the risk assessed through a proper

assignment and supervision of the personnel involved in the audit. The personnel shall have

responsibilities and evaluating accounting policies that are indicating any fraudulent activity

while preparing the reports (Bhattacharjee, Maletta and Moreno 2016). Moreover, the auditor

shall be needed to incorporate the processes of the audit with unpredictability and revenue

recognition risk.

Management overrides of control

Management overrides of control are the intervention by management in handling the

data related to the financial statements and in making economic decisions as contrary to the

internal control policy. The risk of management override of internal control leads to

inadequate revenue recognition. As per ASA 240 Paragraph 33(a), the auditor shall design

and perform the audit [processes in order to mitigate the risk. The basic step that the auditor

shall take is related to the test appropriateness of the journal ledger that reflects whether the

journal entries are correctly recorded into the ledger. The suitor shall identify the entries in

order to reach an appropriate conclusion of its doubts (Mayes, Landes and Hasty 2018). The

auditor shall review and evaluate the estimation of accounting so that to get any point of

being bias. He/she shall evaluate the rationale for significant transactions and can add any

additional audit procedures.

sustaining professional scepticism. The staff involved in the audit procedure shall be

experienced or skilled personnel (Czerney, Schmidt and Thompson 2014). There may be

some extent, and an auditor can bring some relevant changes in the audit procedures

according to the requirement.

Material misstatement Due to fraud

An intentional doing that leads to material misstatement within the report of an entity

is considered fraudulent activity and misstatement by fraud. As per ASA 330, the auditor shall

be responsible for determining the entire response to the risk assessed through a proper

assignment and supervision of the personnel involved in the audit. The personnel shall have

responsibilities and evaluating accounting policies that are indicating any fraudulent activity

while preparing the reports (Bhattacharjee, Maletta and Moreno 2016). Moreover, the auditor

shall be needed to incorporate the processes of the audit with unpredictability and revenue

recognition risk.

Management overrides of control

Management overrides of control are the intervention by management in handling the

data related to the financial statements and in making economic decisions as contrary to the

internal control policy. The risk of management override of internal control leads to

inadequate revenue recognition. As per ASA 240 Paragraph 33(a), the auditor shall design

and perform the audit [processes in order to mitigate the risk. The basic step that the auditor

shall take is related to the test appropriateness of the journal ledger that reflects whether the

journal entries are correctly recorded into the ledger. The suitor shall identify the entries in

order to reach an appropriate conclusion of its doubts (Mayes, Landes and Hasty 2018). The

auditor shall review and evaluate the estimation of accounting so that to get any point of

being bias. He/she shall evaluate the rationale for significant transactions and can add any

additional audit procedures.

11AUDIT RISK, ANALYSIS AND CONTROL IN ORGANIZATION

1.

1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.