Auditing and Assurance in Australia

Added on 2023-06-07

21 Pages5541 Words439 Views

Running head: AUDITING AND ASSURANCE IN AUSTRALIA

Auditing and Assurance in Australia

University Name

Student Name

Authors’ Note

Auditing and Assurance in Australia

University Name

Student Name

Authors’ Note

2

AUDITING AND ASSURANCE IN AUSTRALIA

Executive summary

The study elucidates about the audit risk that indicates towards the issue that is encountered

by the assessor while examining the material misstatement. This may perhaps occur by

reason of error or else fraud. The study presents ways to assess the business risks by

conducting thorough analysis of a ratio that can assist in acquiring a quick indication of the

health and financial of the firm. It also can help the management to identify the strength as

well as weaknesses of the firm and assist in taking a variety of initiatives and framing of

strategies. In the current case, the chosen firm TCW has been evaluated in the present report.

AUDITING AND ASSURANCE IN AUSTRALIA

Executive summary

The study elucidates about the audit risk that indicates towards the issue that is encountered

by the assessor while examining the material misstatement. This may perhaps occur by

reason of error or else fraud. The study presents ways to assess the business risks by

conducting thorough analysis of a ratio that can assist in acquiring a quick indication of the

health and financial of the firm. It also can help the management to identify the strength as

well as weaknesses of the firm and assist in taking a variety of initiatives and framing of

strategies. In the current case, the chosen firm TCW has been evaluated in the present report.

3

AUDITING AND ASSURANCE IN AUSTRALIA

Table of Contents

Solution to Task 1A...................................................................................................................2

Solution to Task 1B....................................................................................................................6

Solution to Task 2A.................................................................................................................12

Solution to Task 2B..................................................................................................................16

References................................................................................................................................18

AUDITING AND ASSURANCE IN AUSTRALIA

Table of Contents

Solution to Task 1A...................................................................................................................2

Solution to Task 1B....................................................................................................................6

Solution to Task 2A.................................................................................................................12

Solution to Task 2B..................................................................................................................16

References................................................................................................................................18

4

AUDITING AND ASSURANCE IN AUSTRALIA

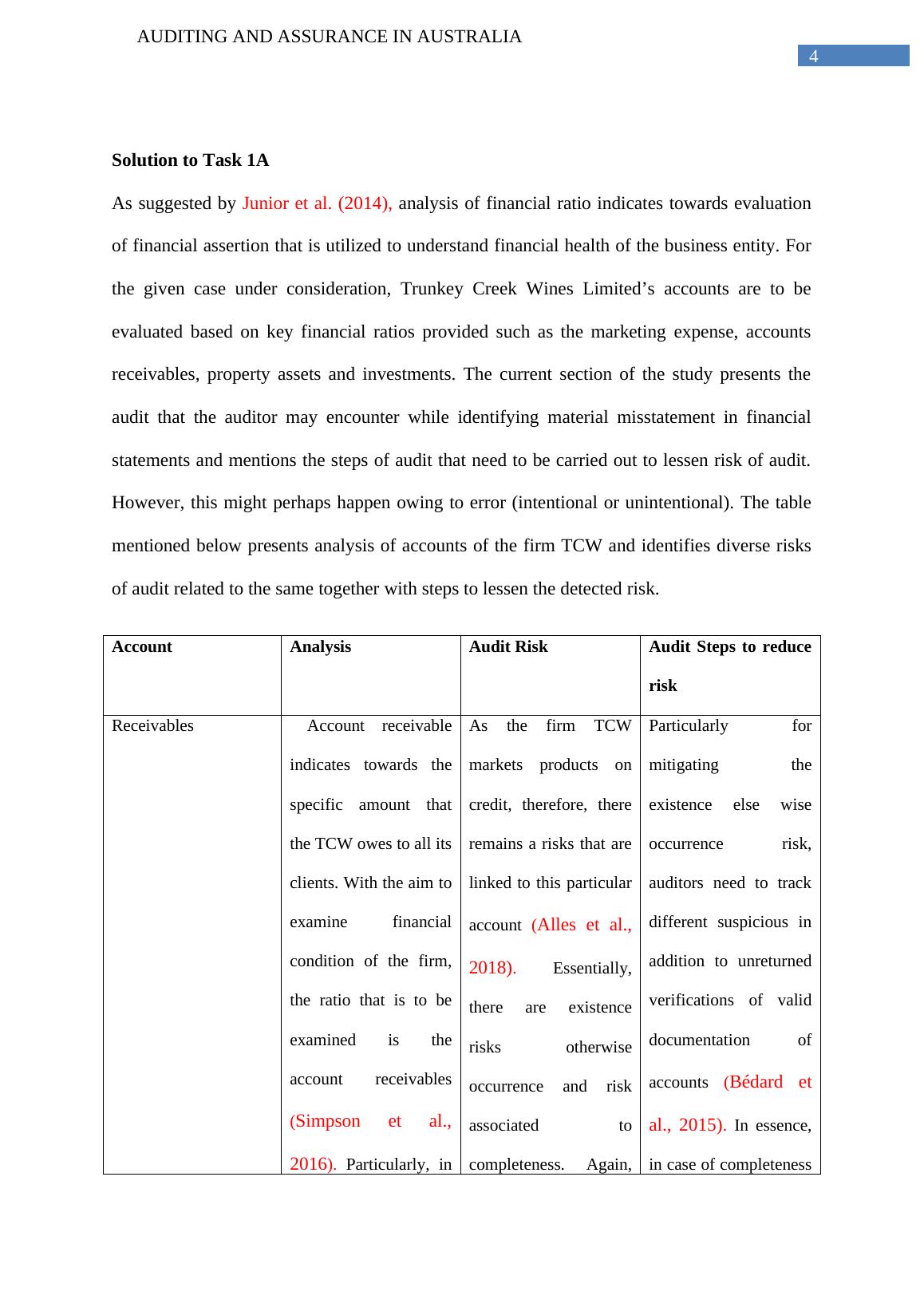

Solution to Task 1A

As suggested by Junior et al. (2014), analysis of financial ratio indicates towards evaluation

of financial assertion that is utilized to understand financial health of the business entity. For

the given case under consideration, Trunkey Creek Wines Limited’s accounts are to be

evaluated based on key financial ratios provided such as the marketing expense, accounts

receivables, property assets and investments. The current section of the study presents the

audit that the auditor may encounter while identifying material misstatement in financial

statements and mentions the steps of audit that need to be carried out to lessen risk of audit.

However, this might perhaps happen owing to error (intentional or unintentional). The table

mentioned below presents analysis of accounts of the firm TCW and identifies diverse risks

of audit related to the same together with steps to lessen the detected risk.

Account Analysis Audit Risk Audit Steps to reduce

risk

Receivables Account receivable

indicates towards the

specific amount that

the TCW owes to all its

clients. With the aim to

examine financial

condition of the firm,

the ratio that is to be

examined is the

account receivables

(Simpson et al.,

2016). Particularly, in

As the firm TCW

markets products on

credit, therefore, there

remains a risks that are

linked to this particular

account (Alles et al.,

2018). Essentially,

there are existence

risks otherwise

occurrence and risk

associated to

completeness. Again,

Particularly for

mitigating the

existence else wise

occurrence risk,

auditors need to track

different suspicious in

addition to unreturned

verifications of valid

documentation of

accounts (Bédard et

al., 2015). In essence,

in case of completeness

AUDITING AND ASSURANCE IN AUSTRALIA

Solution to Task 1A

As suggested by Junior et al. (2014), analysis of financial ratio indicates towards evaluation

of financial assertion that is utilized to understand financial health of the business entity. For

the given case under consideration, Trunkey Creek Wines Limited’s accounts are to be

evaluated based on key financial ratios provided such as the marketing expense, accounts

receivables, property assets and investments. The current section of the study presents the

audit that the auditor may encounter while identifying material misstatement in financial

statements and mentions the steps of audit that need to be carried out to lessen risk of audit.

However, this might perhaps happen owing to error (intentional or unintentional). The table

mentioned below presents analysis of accounts of the firm TCW and identifies diverse risks

of audit related to the same together with steps to lessen the detected risk.

Account Analysis Audit Risk Audit Steps to reduce

risk

Receivables Account receivable

indicates towards the

specific amount that

the TCW owes to all its

clients. With the aim to

examine financial

condition of the firm,

the ratio that is to be

examined is the

account receivables

(Simpson et al.,

2016). Particularly, in

As the firm TCW

markets products on

credit, therefore, there

remains a risks that are

linked to this particular

account (Alles et al.,

2018). Essentially,

there are existence

risks otherwise

occurrence and risk

associated to

completeness. Again,

Particularly for

mitigating the

existence else wise

occurrence risk,

auditors need to track

different suspicious in

addition to unreturned

verifications of valid

documentation of

accounts (Bédard et

al., 2015). In essence,

in case of completeness

5

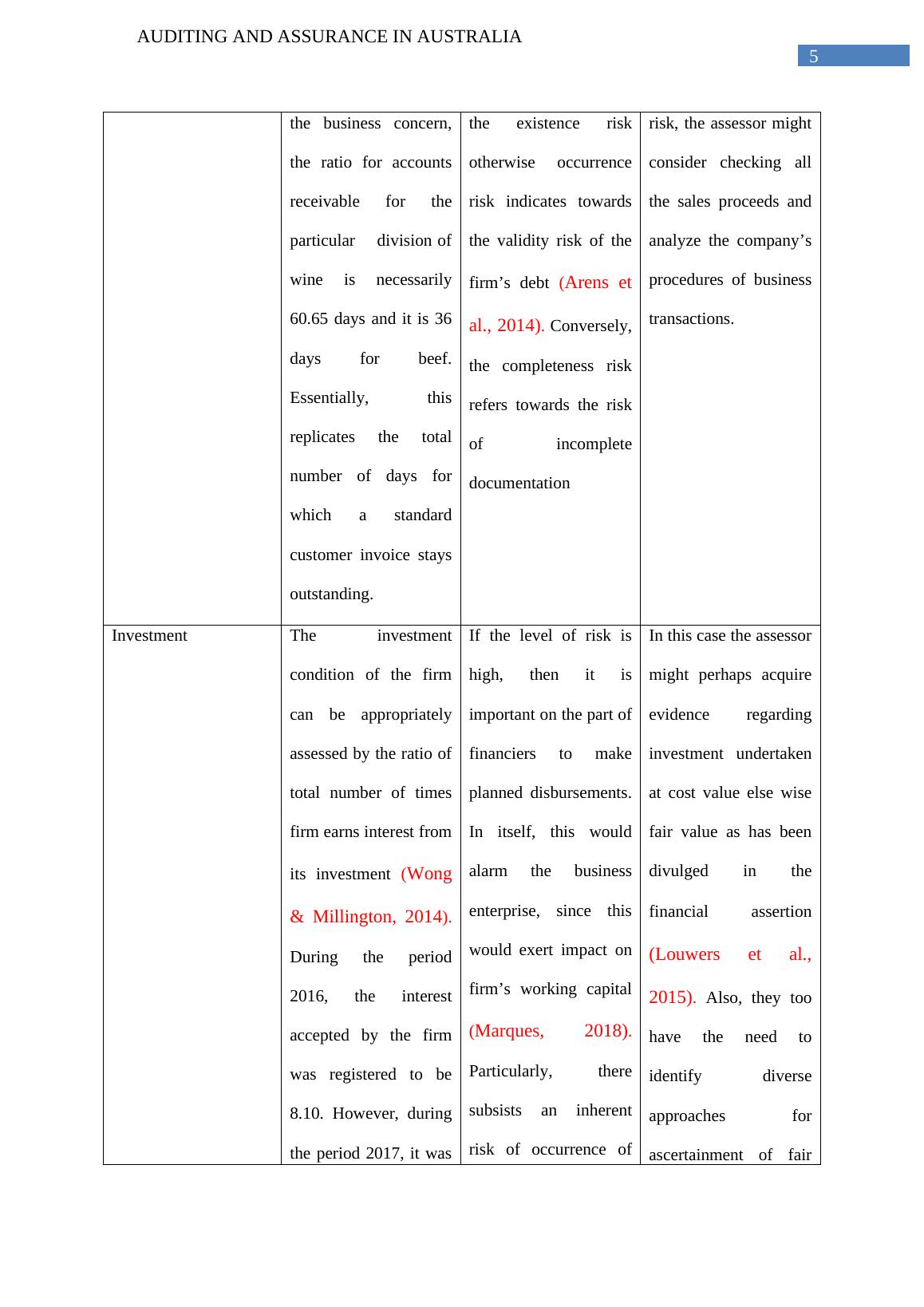

AUDITING AND ASSURANCE IN AUSTRALIA

the business concern,

the ratio for accounts

receivable for the

particular division of

wine is necessarily

60.65 days and it is 36

days for beef.

Essentially, this

replicates the total

number of days for

which a standard

customer invoice stays

outstanding.

the existence risk

otherwise occurrence

risk indicates towards

the validity risk of the

firm’s debt (Arens et

al., 2014). Conversely,

the completeness risk

refers towards the risk

of incomplete

documentation

risk, the assessor might

consider checking all

the sales proceeds and

analyze the company’s

procedures of business

transactions.

Investment The investment

condition of the firm

can be appropriately

assessed by the ratio of

total number of times

firm earns interest from

its investment (Wong

& Millington, 2014).

During the period

2016, the interest

accepted by the firm

was registered to be

8.10. However, during

the period 2017, it was

If the level of risk is

high, then it is

important on the part of

financiers to make

planned disbursements.

In itself, this would

alarm the business

enterprise, since this

would exert impact on

firm’s working capital

(Marques, 2018).

Particularly, there

subsists an inherent

risk of occurrence of

In this case the assessor

might perhaps acquire

evidence regarding

investment undertaken

at cost value else wise

fair value as has been

divulged in the

financial assertion

(Louwers et al.,

2015). Also, they too

have the need to

identify diverse

approaches for

ascertainment of fair

AUDITING AND ASSURANCE IN AUSTRALIA

the business concern,

the ratio for accounts

receivable for the

particular division of

wine is necessarily

60.65 days and it is 36

days for beef.

Essentially, this

replicates the total

number of days for

which a standard

customer invoice stays

outstanding.

the existence risk

otherwise occurrence

risk indicates towards

the validity risk of the

firm’s debt (Arens et

al., 2014). Conversely,

the completeness risk

refers towards the risk

of incomplete

documentation

risk, the assessor might

consider checking all

the sales proceeds and

analyze the company’s

procedures of business

transactions.

Investment The investment

condition of the firm

can be appropriately

assessed by the ratio of

total number of times

firm earns interest from

its investment (Wong

& Millington, 2014).

During the period

2016, the interest

accepted by the firm

was registered to be

8.10. However, during

the period 2017, it was

If the level of risk is

high, then it is

important on the part of

financiers to make

planned disbursements.

In itself, this would

alarm the business

enterprise, since this

would exert impact on

firm’s working capital

(Marques, 2018).

Particularly, there

subsists an inherent

risk of occurrence of

In this case the assessor

might perhaps acquire

evidence regarding

investment undertaken

at cost value else wise

fair value as has been

divulged in the

financial assertion

(Louwers et al.,

2015). Also, they too

have the need to

identify diverse

approaches for

ascertainment of fair

6

AUDITING AND ASSURANCE IN AUSTRALIA

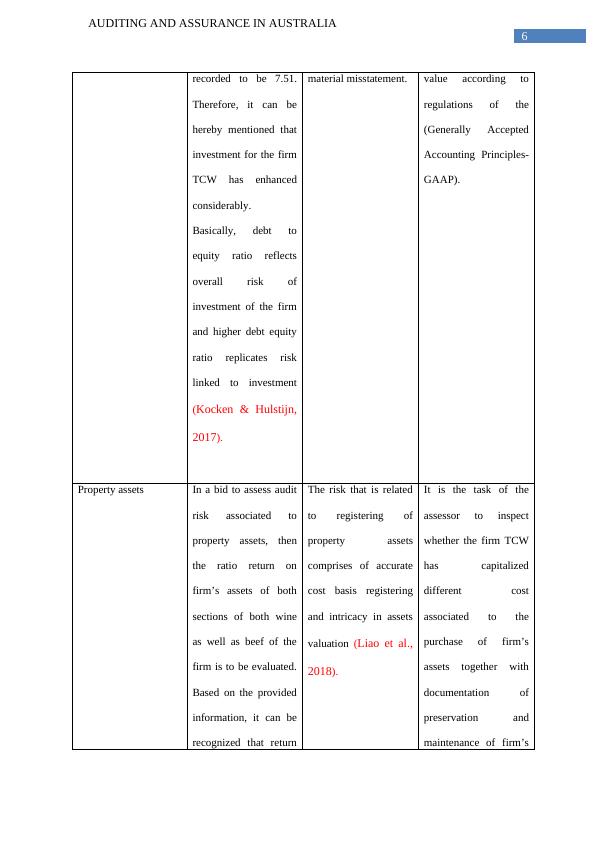

recorded to be 7.51.

Therefore, it can be

hereby mentioned that

investment for the firm

TCW has enhanced

considerably.

Basically, debt to

equity ratio reflects

overall risk of

investment of the firm

and higher debt equity

ratio replicates risk

linked to investment

(Kocken & Hulstijn,

2017).

material misstatement. value according to

regulations of the

(Generally Accepted

Accounting Principles-

GAAP).

Property assets In a bid to assess audit

risk associated to

property assets, then

the ratio return on

firm’s assets of both

sections of both wine

as well as beef of the

firm is to be evaluated.

Based on the provided

information, it can be

recognized that return

The risk that is related

to registering of

property assets

comprises of accurate

cost basis registering

and intricacy in assets

valuation (Liao et al.,

2018).

It is the task of the

assessor to inspect

whether the firm TCW

has capitalized

different cost

associated to the

purchase of firm’s

assets together with

documentation of

preservation and

maintenance of firm’s

AUDITING AND ASSURANCE IN AUSTRALIA

recorded to be 7.51.

Therefore, it can be

hereby mentioned that

investment for the firm

TCW has enhanced

considerably.

Basically, debt to

equity ratio reflects

overall risk of

investment of the firm

and higher debt equity

ratio replicates risk

linked to investment

(Kocken & Hulstijn,

2017).

material misstatement. value according to

regulations of the

(Generally Accepted

Accounting Principles-

GAAP).

Property assets In a bid to assess audit

risk associated to

property assets, then

the ratio return on

firm’s assets of both

sections of both wine

as well as beef of the

firm is to be evaluated.

Based on the provided

information, it can be

recognized that return

The risk that is related

to registering of

property assets

comprises of accurate

cost basis registering

and intricacy in assets

valuation (Liao et al.,

2018).

It is the task of the

assessor to inspect

whether the firm TCW

has capitalized

different cost

associated to the

purchase of firm’s

assets together with

documentation of

preservation and

maintenance of firm’s

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Audit and Assurance- Assignmentlg...

|26

|5526

|26

Auditing Theory and Practicelg...

|16

|3697

|54

Auditing and Assurancelg...

|20

|4919

|304

Auditing Theory and Practice - Risk Analysis and Financial Ratio Evaluationlg...

|19

|4649

|473

Auditing Theory and Practice: Analysis of Audit Risk and Financial Ratios for TCWlg...

|18

|4333

|330

Auditing Theory and Practicelg...

|18

|4452

|202