Audit Strategy for JB Hi Fi Group Pty Limited

VerifiedAdded on 2023/04/21

|16

|4289

|291

AI Summary

This report evaluates the various aspects of audit in relation to JB Hi Fi Group Pty Limited, including corporate, regulatory, accounting, and operational aspects.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDIT STRATEGY

STRATEGIC AUDIT

STRATEGIC AUDIT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT 1

Contents

Introduction................................................................................................................................2

Part A: The Client......................................................................................................................2

Information about the client.......................................................................................................2

Industry, regulatory and other external factors..........................................................................3

Nature of the entity.....................................................................................................................3

Accounting Policy......................................................................................................................4

Related Parties and Transactions with Related Parties..............................................................5

Part B: Analysis of the client and impacts on the future audit work..........................................7

Changes in accounting policies and the impact of the changes.................................................7

Ratio Analysis............................................................................................................................7

Measurement and Review of Financial Performance..............................................................10

Objectives, Strategies, and related business risks....................................................................11

Conclusion................................................................................................................................11

References................................................................................................................................13

Contents

Introduction................................................................................................................................2

Part A: The Client......................................................................................................................2

Information about the client.......................................................................................................2

Industry, regulatory and other external factors..........................................................................3

Nature of the entity.....................................................................................................................3

Accounting Policy......................................................................................................................4

Related Parties and Transactions with Related Parties..............................................................5

Part B: Analysis of the client and impacts on the future audit work..........................................7

Changes in accounting policies and the impact of the changes.................................................7

Ratio Analysis............................................................................................................................7

Measurement and Review of Financial Performance..............................................................10

Objectives, Strategies, and related business risks....................................................................11

Conclusion................................................................................................................................11

References................................................................................................................................13

AUDIT 2

Introduction

The following report is aimed at evaluating the various aspects of audit in relation to the

entity “JB Hi Fi Group Pty Limited.” The report will shed light on the corporate, regulatory,

accounting, and operational aspects of the company. These would be in addition to the

analysis of the various factors such as changes in accounting policies and the impacts of the

same in future years, major ratios and their significance in terms of comparison with the last

year performance, business risks and their impacts; and the overall evaluation of the financial

performance of the enterprise.

Part A: The Client

Information about the client

Mr. John Barbuto (JB) had established the entity JB Hi-Fi in the year 1974, with an aim to be

Australia's largest and fastest growing company in terms of the retailer of home entertainment

(JB Hi Fi, 2019a). Back then, the entity had a single store in East Keilor, Victoria. The

company’s current headquarters and registered office are located at Office Tower 2, Level 4,

Chadstone Shopping Centre, 1341 Dandenong Rd Chadstone, Victoria. The company JB Hi-

Fi was floated on the Australian Stock Exchange in the month of October 2003. The

company’s ASX code is “JBH.”

The company is engaged in the business of retailing the branded home entertainment

products. The standalone destination sites and the shopping centres are the primary means of

operation of the entity. These are in addition to the company’s online stores mainly in New

Zealand and Australia. The products of the company are mainly comprised of the consumer

electronics, appliances, whitegoods, and a varied range of software including the games,

music, and movies (JB Hi Fi, 2019a). Further, the primary services include the

telecommunication services, digital content, consulting and information technology services.

Thus, company earns its revenues mainly through the sale of the consumer electronics

products and services.

The year in consideration for the report is the financial ended on 30th June 2018. The financial

statements that would be evaluated would be the consolidated financial statements.

Introduction

The following report is aimed at evaluating the various aspects of audit in relation to the

entity “JB Hi Fi Group Pty Limited.” The report will shed light on the corporate, regulatory,

accounting, and operational aspects of the company. These would be in addition to the

analysis of the various factors such as changes in accounting policies and the impacts of the

same in future years, major ratios and their significance in terms of comparison with the last

year performance, business risks and their impacts; and the overall evaluation of the financial

performance of the enterprise.

Part A: The Client

Information about the client

Mr. John Barbuto (JB) had established the entity JB Hi-Fi in the year 1974, with an aim to be

Australia's largest and fastest growing company in terms of the retailer of home entertainment

(JB Hi Fi, 2019a). Back then, the entity had a single store in East Keilor, Victoria. The

company’s current headquarters and registered office are located at Office Tower 2, Level 4,

Chadstone Shopping Centre, 1341 Dandenong Rd Chadstone, Victoria. The company JB Hi-

Fi was floated on the Australian Stock Exchange in the month of October 2003. The

company’s ASX code is “JBH.”

The company is engaged in the business of retailing the branded home entertainment

products. The standalone destination sites and the shopping centres are the primary means of

operation of the entity. These are in addition to the company’s online stores mainly in New

Zealand and Australia. The products of the company are mainly comprised of the consumer

electronics, appliances, whitegoods, and a varied range of software including the games,

music, and movies (JB Hi Fi, 2019a). Further, the primary services include the

telecommunication services, digital content, consulting and information technology services.

Thus, company earns its revenues mainly through the sale of the consumer electronics

products and services.

The year in consideration for the report is the financial ended on 30th June 2018. The financial

statements that would be evaluated would be the consolidated financial statements.

AUDIT 3

Industry, regulatory and other external factors

There have been recent growth trends in Victoria for the retail industry. It is significant to

note that retail trade in Victoria grew up by 4.5 percent as reported in the beginning of the

year 2018, as compared to last year figures (Premier of Victoria, 2018). This accounted for

the highest growth in retail industry as compared to the other states. The growth trends have

driven positive results for the company in terms of revenue generation.

Some of the chief laws that are applicable to the entity are stated as follows. One of the chief

set of laws are the discrimination laws in the form of Fair Work Act 2009 (Cth), Sex

Discrimination Act 1984, and others. In addition, the Employment laws such as the Equal

Opportunity Act 2010 and the data protection and privacy laws such as the Privacy Act 1988

are also applicable on the company. Further, the Anti-trust law in Retailing industry,

Copyright, patents / Intellectual property laws, Environmental legislations, Corporations Act,

2001 (Cth), ASX Corporate Governance Council Corporate Governance Principles are also to

be abided by the entity.

With the increase in the e commerce practices, globalisation and increased use of the

technology driven and mobile-based products, there has been consistent increase in the

demands of the electronics, mobiles, and other such technology driven products.

The company faces a high level of competition in terms of retailing industry both in terms of

the local medium and big players and the global giants like that of Amazon. Some of the

main competitors of the company are the Harvey Norman, Fantastic Furniture, Scaale

Capital, IKEA, Simon, Ashley, Freedom Furniture, and GPT Group among others in the

speciality retailing industry.

Nature of the entity

The JB Hi Fi stores are engaged in offering leading brands of computers, cameras, speakers,

TVs, portable audio systems, varied range of games, recorded music, DVD movies, TV

shows, home appliances, DJ and musical instruments, drones and robotics, software,

consulting services, information technology, telecommunication services and more. The

company serves wide range of customers form government agencies, schools and colleges,

organisations, households and others. Because of wide variety of products, the consumers are

not limited to one class; rather belong to varied income and spending capacity groups.

However, one significant characteristics about the consumers is that they are tech savvy.

Industry, regulatory and other external factors

There have been recent growth trends in Victoria for the retail industry. It is significant to

note that retail trade in Victoria grew up by 4.5 percent as reported in the beginning of the

year 2018, as compared to last year figures (Premier of Victoria, 2018). This accounted for

the highest growth in retail industry as compared to the other states. The growth trends have

driven positive results for the company in terms of revenue generation.

Some of the chief laws that are applicable to the entity are stated as follows. One of the chief

set of laws are the discrimination laws in the form of Fair Work Act 2009 (Cth), Sex

Discrimination Act 1984, and others. In addition, the Employment laws such as the Equal

Opportunity Act 2010 and the data protection and privacy laws such as the Privacy Act 1988

are also applicable on the company. Further, the Anti-trust law in Retailing industry,

Copyright, patents / Intellectual property laws, Environmental legislations, Corporations Act,

2001 (Cth), ASX Corporate Governance Council Corporate Governance Principles are also to

be abided by the entity.

With the increase in the e commerce practices, globalisation and increased use of the

technology driven and mobile-based products, there has been consistent increase in the

demands of the electronics, mobiles, and other such technology driven products.

The company faces a high level of competition in terms of retailing industry both in terms of

the local medium and big players and the global giants like that of Amazon. Some of the

main competitors of the company are the Harvey Norman, Fantastic Furniture, Scaale

Capital, IKEA, Simon, Ashley, Freedom Furniture, and GPT Group among others in the

speciality retailing industry.

Nature of the entity

The JB Hi Fi stores are engaged in offering leading brands of computers, cameras, speakers,

TVs, portable audio systems, varied range of games, recorded music, DVD movies, TV

shows, home appliances, DJ and musical instruments, drones and robotics, software,

consulting services, information technology, telecommunication services and more. The

company serves wide range of customers form government agencies, schools and colleges,

organisations, households and others. Because of wide variety of products, the consumers are

not limited to one class; rather belong to varied income and spending capacity groups.

However, one significant characteristics about the consumers is that they are tech savvy.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT 4

It is significant to note that with the recent annual sales of $6.85 billion, the company has

climbed up the ladder in terms of global standing to 7th position on lines of the largest

consumer electronics (CE) and home appliance (HA) retailer in the world (Bencic, 2018).

The mix of consumer electronics (CE) and home appliances (HA) and the 300 stores around

the globe has led to the said feat. Some of the noted suppliers in terms of overseas tech and

appliance companies who sell goods via JB Hi Fi are the Microsoft, Google, Apple, Dell, HP,

Hisense Nokia, LG, Sony, Panasonic, Nikon, Casio, Kicker and others. The featured

suppliers and brands in fitness and home appliance sector are the Fitbit, Fossil, Misfit,

Samsung, Dyson, Nespresso and others (JB Hi Fi, 2019b).

In terms of operational structure, the group operates through its two chief subsidiaries namely

the JB Hi- Fi and The Good Guys. While the former is specialised in technology and

consumer electronics, the latter has area of focus in the home appliances and consumer

electronics (JB HI FI, 2019c, p. 1). As on 30 June 2018, the group had 311 stores in Australia

and New Zealand.

In terms of the corporate governance structure, the board of the entity is comprised of seven

directors. Out of which six directors are the non- executive directors, including the Chairman

and one director is the executive director (JB HI FI, 2019c, p. 6). The board functions through

various committees namely the remuneration committee, the audit and risk management

committee, and the nominations committee. Mr Greg Richards is the Chairman and Mr

Richard Murray is the Group Chief Executive Officer of the entity. Each of the board

committee reviews its annual performance and reports the results to the board of directors.

Accounting Policy

A glimpse of the major accounting policies of the entity is provided as follows. The financial

statements of the entity are prepared in conjunction with the Australian Accounting standards

and the interpretations applicable of the Australian Accounting Standards Board and the

Corporations Act 2001.

The plants and equipment of the entity are valued at historical cost less accumulated

depreciation. The accounting policy in terms of depreciation is calculation of the same on

straight-line basis. These assets are further tested for the impairment losses, if any at the

whenever the events indicate the same or on a consistent basis.

It is significant to note that with the recent annual sales of $6.85 billion, the company has

climbed up the ladder in terms of global standing to 7th position on lines of the largest

consumer electronics (CE) and home appliance (HA) retailer in the world (Bencic, 2018).

The mix of consumer electronics (CE) and home appliances (HA) and the 300 stores around

the globe has led to the said feat. Some of the noted suppliers in terms of overseas tech and

appliance companies who sell goods via JB Hi Fi are the Microsoft, Google, Apple, Dell, HP,

Hisense Nokia, LG, Sony, Panasonic, Nikon, Casio, Kicker and others. The featured

suppliers and brands in fitness and home appliance sector are the Fitbit, Fossil, Misfit,

Samsung, Dyson, Nespresso and others (JB Hi Fi, 2019b).

In terms of operational structure, the group operates through its two chief subsidiaries namely

the JB Hi- Fi and The Good Guys. While the former is specialised in technology and

consumer electronics, the latter has area of focus in the home appliances and consumer

electronics (JB HI FI, 2019c, p. 1). As on 30 June 2018, the group had 311 stores in Australia

and New Zealand.

In terms of the corporate governance structure, the board of the entity is comprised of seven

directors. Out of which six directors are the non- executive directors, including the Chairman

and one director is the executive director (JB HI FI, 2019c, p. 6). The board functions through

various committees namely the remuneration committee, the audit and risk management

committee, and the nominations committee. Mr Greg Richards is the Chairman and Mr

Richard Murray is the Group Chief Executive Officer of the entity. Each of the board

committee reviews its annual performance and reports the results to the board of directors.

Accounting Policy

A glimpse of the major accounting policies of the entity is provided as follows. The financial

statements of the entity are prepared in conjunction with the Australian Accounting standards

and the interpretations applicable of the Australian Accounting Standards Board and the

Corporations Act 2001.

The plants and equipment of the entity are valued at historical cost less accumulated

depreciation. The accounting policy in terms of depreciation is calculation of the same on

straight-line basis. These assets are further tested for the impairment losses, if any at the

whenever the events indicate the same or on a consistent basis.

AUDIT 5

The accounting policy adopted by the entity in terms of valuation of inventory is to measure

them at lower of cost or net realisable value. Further, the company adopts the weighted

average costing method to value the individual items (JB Hi Fi, 2019c, p. 73).

The accounting policy for the accounts receivable is that the credit period offered to the

debtors is that of 30 days. In addition, the entity does not charges any interest on the amounts

of accounts receivables. The company reviews the collectability of the trade receivables at an

ongoing basis (JB Hi Fi, 2019c, p. 74).

In terms of the financial instruments, the entity values its interest rate swaps, interest rate

caps, and foreign currency forward contracts at fair values (JB Hi Fi, 2019c, p. 87).

The entity has an accounting policy to measure the revenues at the fair value of the

consideration that is received or receivable (JB Hi Fi, 2019c, p. 96). The revenues from the

sales are recognised at the time of transferring of the significant risks and rewards to the

buyer. In case of commission, the revenue recognised is the amount of the commission made

by the group as a whole. In relation to the services, the revenues are recognised as per the

portion of the services provided by the entity.

The entity regards the intangible assets to have unlimited useful lives, the same are not

subject to the amortisation and these are regularly tested by the entity for the impairment JB

Hi Fi, 2019c, p. 76).

Related Parties and Transactions with Related Parties

The evaluation and description of the related parties of the entity is as follows.

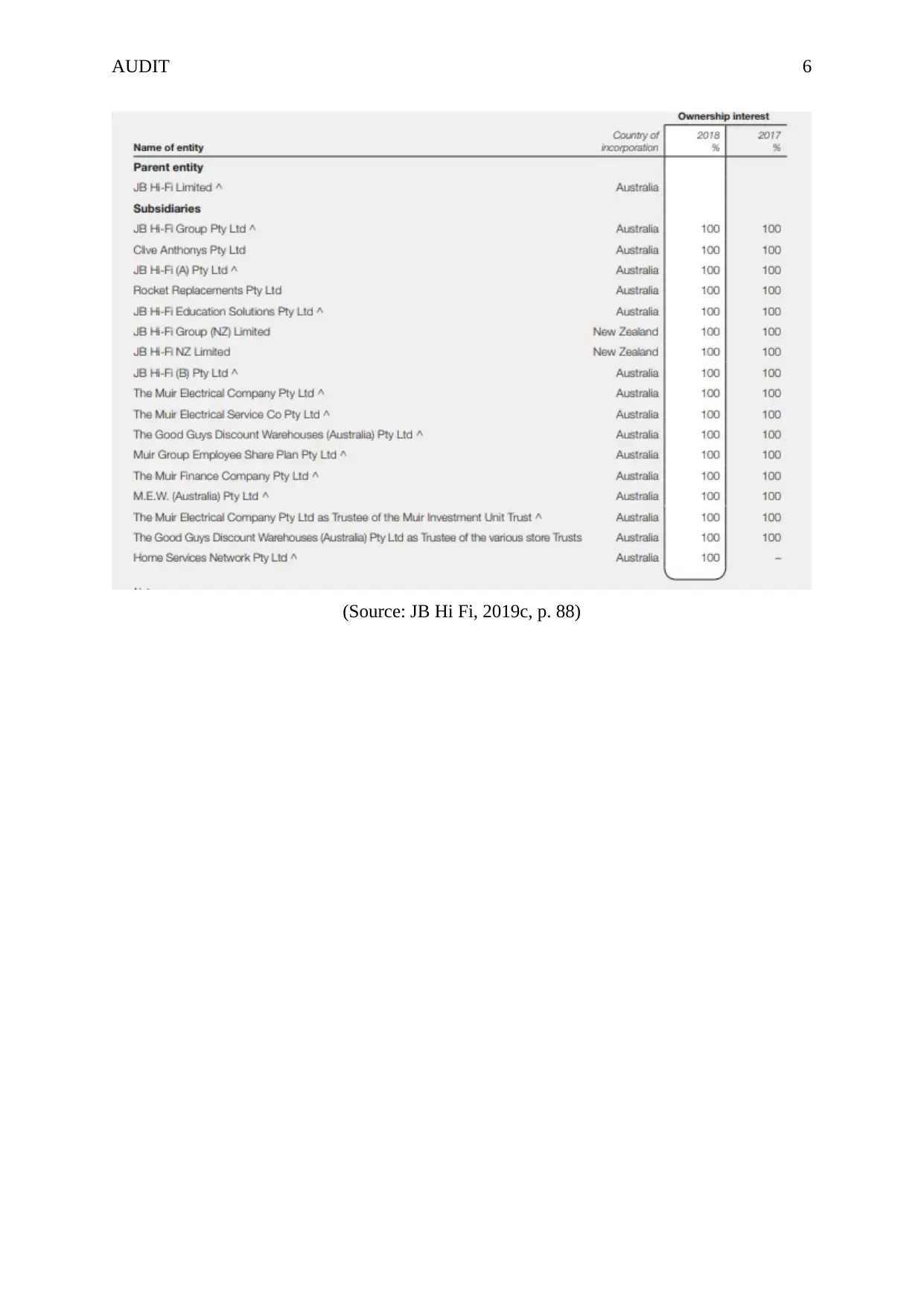

The parent or the controlling entity of the whole of the group is the JB Hi-Fi Limited, which

is a listed public company, incorporated and based at Australia. The following picture gives

an overall summary of the subsidiaries and the ownership interest in relation to them. The

group company consolidates the assets, liabilities and results of the following principal

subsidiaries.

The accounting policy adopted by the entity in terms of valuation of inventory is to measure

them at lower of cost or net realisable value. Further, the company adopts the weighted

average costing method to value the individual items (JB Hi Fi, 2019c, p. 73).

The accounting policy for the accounts receivable is that the credit period offered to the

debtors is that of 30 days. In addition, the entity does not charges any interest on the amounts

of accounts receivables. The company reviews the collectability of the trade receivables at an

ongoing basis (JB Hi Fi, 2019c, p. 74).

In terms of the financial instruments, the entity values its interest rate swaps, interest rate

caps, and foreign currency forward contracts at fair values (JB Hi Fi, 2019c, p. 87).

The entity has an accounting policy to measure the revenues at the fair value of the

consideration that is received or receivable (JB Hi Fi, 2019c, p. 96). The revenues from the

sales are recognised at the time of transferring of the significant risks and rewards to the

buyer. In case of commission, the revenue recognised is the amount of the commission made

by the group as a whole. In relation to the services, the revenues are recognised as per the

portion of the services provided by the entity.

The entity regards the intangible assets to have unlimited useful lives, the same are not

subject to the amortisation and these are regularly tested by the entity for the impairment JB

Hi Fi, 2019c, p. 76).

Related Parties and Transactions with Related Parties

The evaluation and description of the related parties of the entity is as follows.

The parent or the controlling entity of the whole of the group is the JB Hi-Fi Limited, which

is a listed public company, incorporated and based at Australia. The following picture gives

an overall summary of the subsidiaries and the ownership interest in relation to them. The

group company consolidates the assets, liabilities and results of the following principal

subsidiaries.

AUDIT 6

(Source: JB Hi Fi, 2019c, p. 88)

(Source: JB Hi Fi, 2019c, p. 88)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT 7

Part B: Analysis of the client and impacts on the future audit work.

Changes in accounting policies and the impact of the changes

The accounting policies refer to the principles, bases or conventions that are applied by an

entity, while the preparation and presentation of the financial statements. As stated by the

entity in the financial statement there has been no significant changes in terms of the

accounting policies and the principal business activity of the enterprise. The significant

changes refer to the changes that deal with the material amounts or lead to material shift in

the financial performance. In addition, it is stated that there are no significant changes in the

state of affairs of the group.

As per the Paragraph 13 of the accounting standard an entity ids required to consistently

apply the accounting policies, except the changes as mandatorily prescribed by the Australian

Accounting Board itself (AASB, 2015). In case there are material changes in the accounting

policy, the same are required to be mandatorily disclosed by the entity in the financial

statements. The said changes must be applied and accounted for since the initial application

of the accounting standard. Further, these must be stated with the description of the potential

impacts in qualitative and quantitative terms, in the financial statements

The impact of the same on the future audit work can be stated to be that the auditors must

review whether the said changes were necessary to be carried on, on the lines of better

presentation of the financial and other information in the statements. The audit team must

review whether there are items that can individually or in a group influence the decisions of

the stakeholders of the group, have undergone a change in the concerned financial year or

not, in line if the entity’s claim. In addition, the initial application of the said changes must be

reviewed.

Ratio Analysis

The various ratios give an insight of the various aspects of the business performance of the

entity, such as the Risk, Profitability, Solvency, Efficiency, and others. In addition, the

analysis is very useful in comparing the trends in relation to the past year and current year

performance and the company’s performance in line of the industry trends. This is one of the

widely used analytical procedure used by the audit teams to evaluate the performance beyond

as mentioned through the numbers and explanations. The chief ratios are calculated as

Part B: Analysis of the client and impacts on the future audit work.

Changes in accounting policies and the impact of the changes

The accounting policies refer to the principles, bases or conventions that are applied by an

entity, while the preparation and presentation of the financial statements. As stated by the

entity in the financial statement there has been no significant changes in terms of the

accounting policies and the principal business activity of the enterprise. The significant

changes refer to the changes that deal with the material amounts or lead to material shift in

the financial performance. In addition, it is stated that there are no significant changes in the

state of affairs of the group.

As per the Paragraph 13 of the accounting standard an entity ids required to consistently

apply the accounting policies, except the changes as mandatorily prescribed by the Australian

Accounting Board itself (AASB, 2015). In case there are material changes in the accounting

policy, the same are required to be mandatorily disclosed by the entity in the financial

statements. The said changes must be applied and accounted for since the initial application

of the accounting standard. Further, these must be stated with the description of the potential

impacts in qualitative and quantitative terms, in the financial statements

The impact of the same on the future audit work can be stated to be that the auditors must

review whether the said changes were necessary to be carried on, on the lines of better

presentation of the financial and other information in the statements. The audit team must

review whether there are items that can individually or in a group influence the decisions of

the stakeholders of the group, have undergone a change in the concerned financial year or

not, in line if the entity’s claim. In addition, the initial application of the said changes must be

reviewed.

Ratio Analysis

The various ratios give an insight of the various aspects of the business performance of the

entity, such as the Risk, Profitability, Solvency, Efficiency, and others. In addition, the

analysis is very useful in comparing the trends in relation to the past year and current year

performance and the company’s performance in line of the industry trends. This is one of the

widely used analytical procedure used by the audit teams to evaluate the performance beyond

as mentioned through the numbers and explanations. The chief ratios are calculated as

AUDIT 8

follows, in relation to the entity JB Hi Fi, together with the reasons for the changes and

potential underlying impacts.

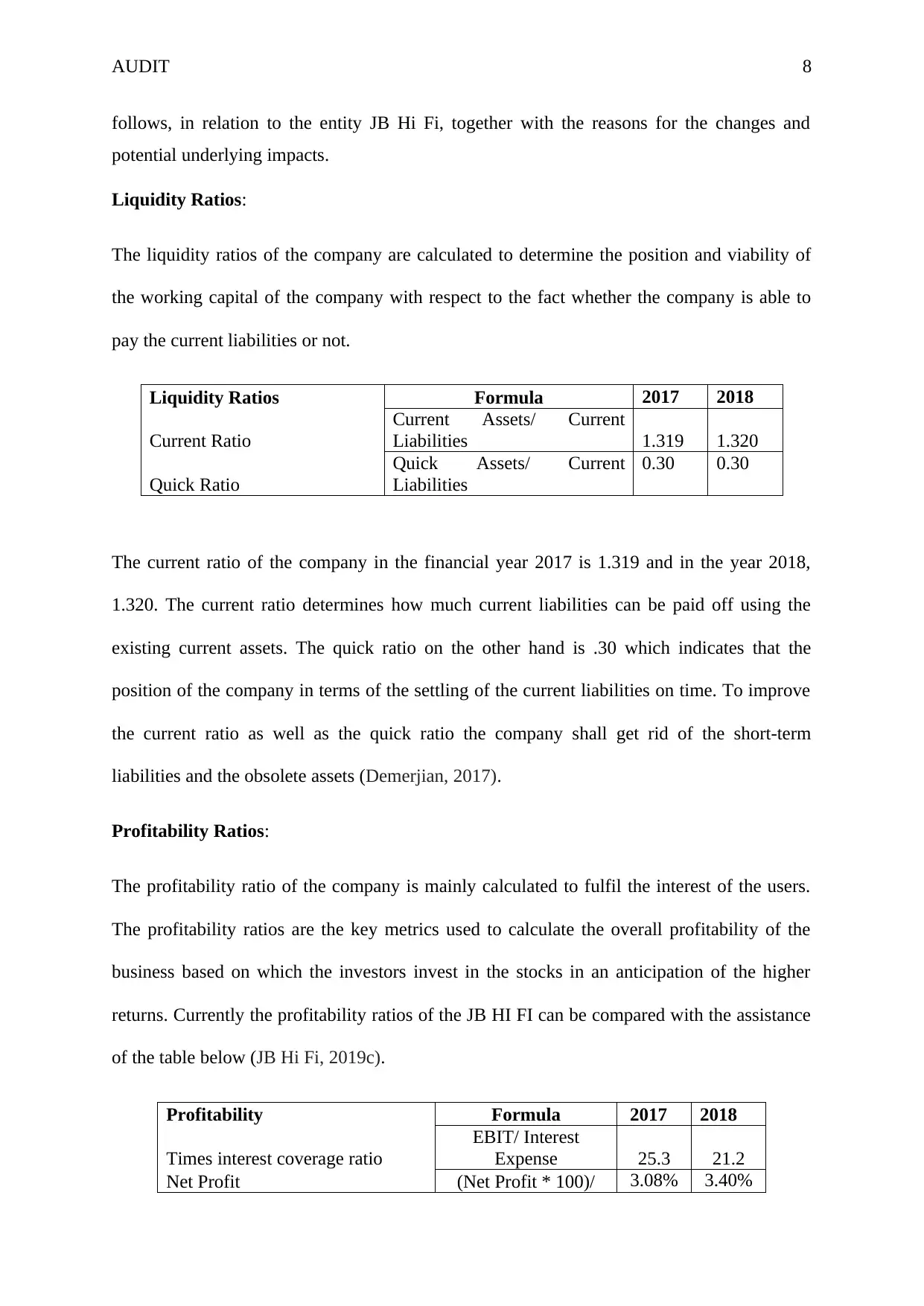

Liquidity Ratios:

The liquidity ratios of the company are calculated to determine the position and viability of

the working capital of the company with respect to the fact whether the company is able to

pay the current liabilities or not.

Liquidity Ratios Formula 2017 2018

Current Ratio

Current Assets/ Current

Liabilities 1.319 1.320

Quick Ratio

Quick Assets/ Current

Liabilities

0.30 0.30

The current ratio of the company in the financial year 2017 is 1.319 and in the year 2018,

1.320. The current ratio determines how much current liabilities can be paid off using the

existing current assets. The quick ratio on the other hand is .30 which indicates that the

position of the company in terms of the settling of the current liabilities on time. To improve

the current ratio as well as the quick ratio the company shall get rid of the short-term

liabilities and the obsolete assets (Demerjian, 2017).

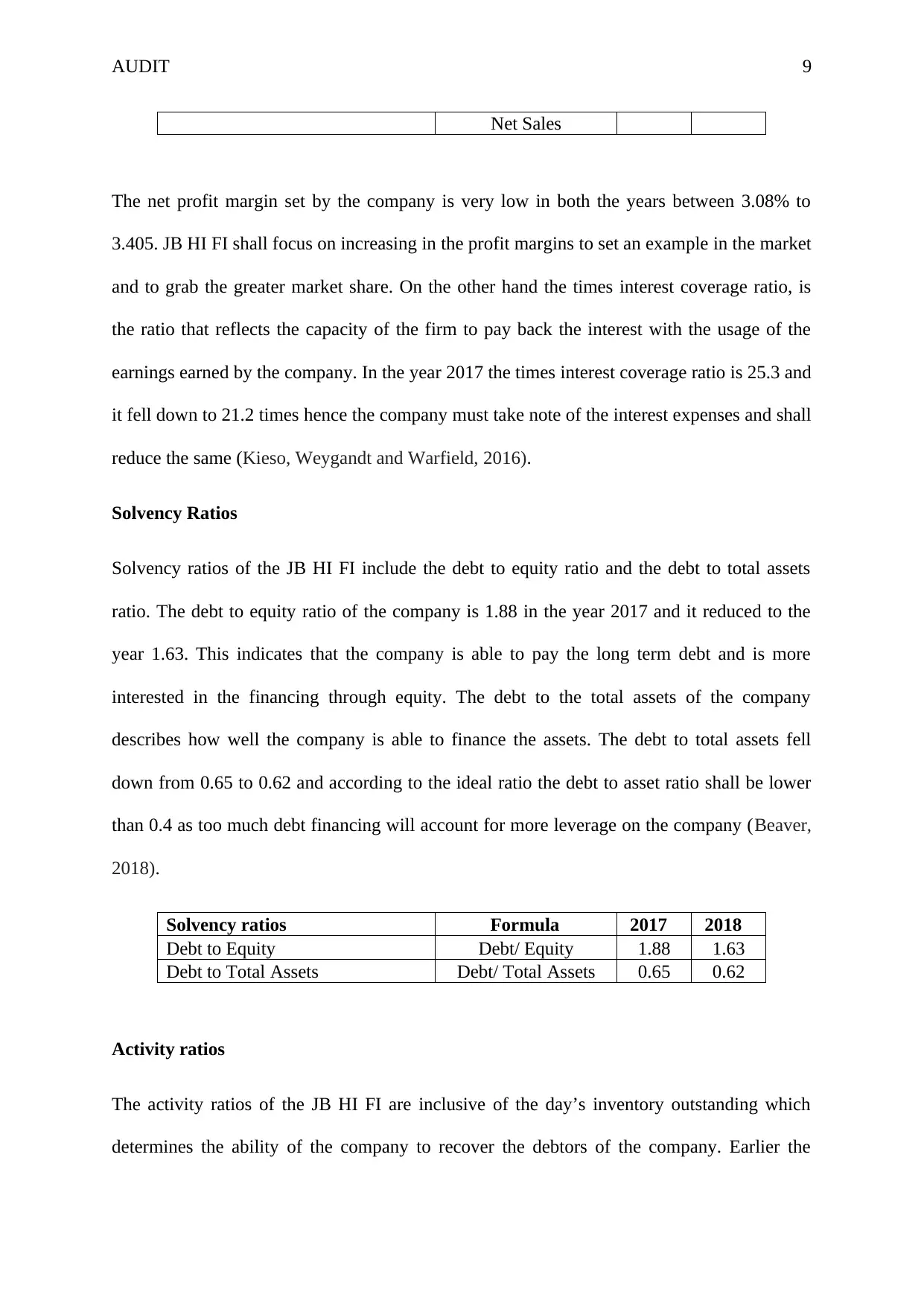

Profitability Ratios:

The profitability ratio of the company is mainly calculated to fulfil the interest of the users.

The profitability ratios are the key metrics used to calculate the overall profitability of the

business based on which the investors invest in the stocks in an anticipation of the higher

returns. Currently the profitability ratios of the JB HI FI can be compared with the assistance

of the table below (JB Hi Fi, 2019c).

Profitability Formula 2017 2018

Times interest coverage ratio

EBIT/ Interest

Expense 25.3 21.2

Net Profit (Net Profit * 100)/ 3.08% 3.40%

follows, in relation to the entity JB Hi Fi, together with the reasons for the changes and

potential underlying impacts.

Liquidity Ratios:

The liquidity ratios of the company are calculated to determine the position and viability of

the working capital of the company with respect to the fact whether the company is able to

pay the current liabilities or not.

Liquidity Ratios Formula 2017 2018

Current Ratio

Current Assets/ Current

Liabilities 1.319 1.320

Quick Ratio

Quick Assets/ Current

Liabilities

0.30 0.30

The current ratio of the company in the financial year 2017 is 1.319 and in the year 2018,

1.320. The current ratio determines how much current liabilities can be paid off using the

existing current assets. The quick ratio on the other hand is .30 which indicates that the

position of the company in terms of the settling of the current liabilities on time. To improve

the current ratio as well as the quick ratio the company shall get rid of the short-term

liabilities and the obsolete assets (Demerjian, 2017).

Profitability Ratios:

The profitability ratio of the company is mainly calculated to fulfil the interest of the users.

The profitability ratios are the key metrics used to calculate the overall profitability of the

business based on which the investors invest in the stocks in an anticipation of the higher

returns. Currently the profitability ratios of the JB HI FI can be compared with the assistance

of the table below (JB Hi Fi, 2019c).

Profitability Formula 2017 2018

Times interest coverage ratio

EBIT/ Interest

Expense 25.3 21.2

Net Profit (Net Profit * 100)/ 3.08% 3.40%

AUDIT 9

Net Sales

The net profit margin set by the company is very low in both the years between 3.08% to

3.405. JB HI FI shall focus on increasing in the profit margins to set an example in the market

and to grab the greater market share. On the other hand the times interest coverage ratio, is

the ratio that reflects the capacity of the firm to pay back the interest with the usage of the

earnings earned by the company. In the year 2017 the times interest coverage ratio is 25.3 and

it fell down to 21.2 times hence the company must take note of the interest expenses and shall

reduce the same (Kieso, Weygandt and Warfield, 2016).

Solvency Ratios

Solvency ratios of the JB HI FI include the debt to equity ratio and the debt to total assets

ratio. The debt to equity ratio of the company is 1.88 in the year 2017 and it reduced to the

year 1.63. This indicates that the company is able to pay the long term debt and is more

interested in the financing through equity. The debt to the total assets of the company

describes how well the company is able to finance the assets. The debt to total assets fell

down from 0.65 to 0.62 and according to the ideal ratio the debt to asset ratio shall be lower

than 0.4 as too much debt financing will account for more leverage on the company (Beaver,

2018).

Solvency ratios Formula 2017 2018

Debt to Equity Debt/ Equity 1.88 1.63

Debt to Total Assets Debt/ Total Assets 0.65 0.62

Activity ratios

The activity ratios of the JB HI FI are inclusive of the day’s inventory outstanding which

determines the ability of the company to recover the debtors of the company. Earlier the

Net Sales

The net profit margin set by the company is very low in both the years between 3.08% to

3.405. JB HI FI shall focus on increasing in the profit margins to set an example in the market

and to grab the greater market share. On the other hand the times interest coverage ratio, is

the ratio that reflects the capacity of the firm to pay back the interest with the usage of the

earnings earned by the company. In the year 2017 the times interest coverage ratio is 25.3 and

it fell down to 21.2 times hence the company must take note of the interest expenses and shall

reduce the same (Kieso, Weygandt and Warfield, 2016).

Solvency Ratios

Solvency ratios of the JB HI FI include the debt to equity ratio and the debt to total assets

ratio. The debt to equity ratio of the company is 1.88 in the year 2017 and it reduced to the

year 1.63. This indicates that the company is able to pay the long term debt and is more

interested in the financing through equity. The debt to the total assets of the company

describes how well the company is able to finance the assets. The debt to total assets fell

down from 0.65 to 0.62 and according to the ideal ratio the debt to asset ratio shall be lower

than 0.4 as too much debt financing will account for more leverage on the company (Beaver,

2018).

Solvency ratios Formula 2017 2018

Debt to Equity Debt/ Equity 1.88 1.63

Debt to Total Assets Debt/ Total Assets 0.65 0.62

Activity ratios

The activity ratios of the JB HI FI are inclusive of the day’s inventory outstanding which

determines the ability of the company to recover the debtors of the company. Earlier the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

AUDIT 10

company was able to recover the amount in 55.8 days whereas in the year 2018 the company

was able to realize within 47.5 days (Uechi, Akutsu, Stanley, Marcus, and Kenett, 2015).

Activity Ratios Formula 2017 2018

Days Inventory Outstanding

(Inventory * 365)/

Cost of goods sold 55.8 47.5

Days Receivable Outstanding

(Accounts receivable

* 365)/ Credit sales 12.6 10.9

Days Payable Outstanding

(Average Accounts

Payable * 365)/ Cost

of Goods Sold 53.5 45.1

Hence, the overall impact suggests that the investor shall invest if the net profit margin is

improved, the liquidity position reaches beyond par level, and lastly the company shall

review the statements on regular basis.

It is the duty of the management to assess the ability of the entity to continue as a going

concern. In addition, it is the responsibility of the management to disclose the matters related

to the going concern ability and use the going concern basis of accounting. The audit team is

required to review and conclude the appropriateness of the directors’ claim and the use of the

going concern basis of accounting. In the financial statements of the entity, there have not

been prescribed any matters that threaten the going concern basis of the entity.

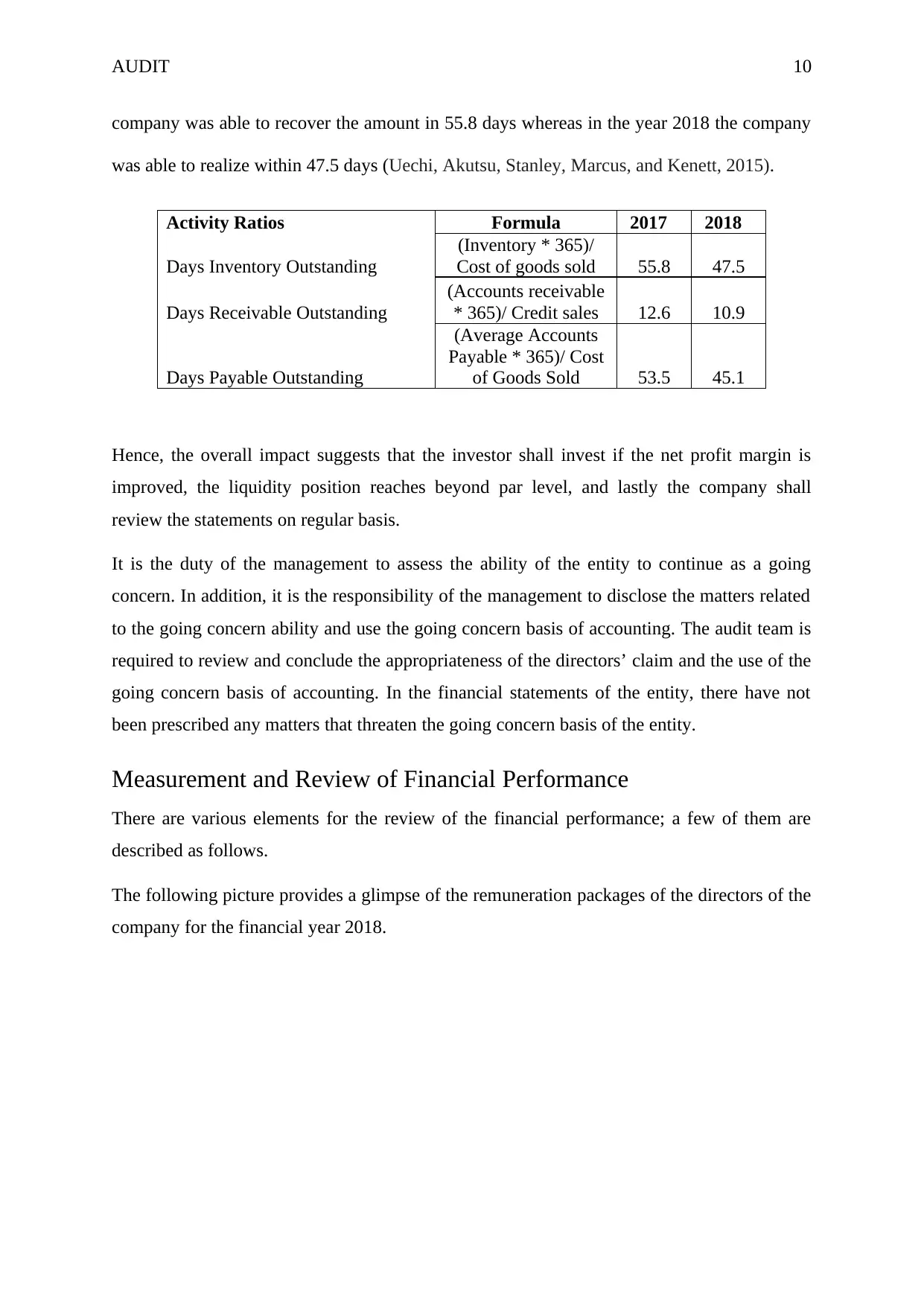

Measurement and Review of Financial Performance

There are various elements for the review of the financial performance; a few of them are

described as follows.

The following picture provides a glimpse of the remuneration packages of the directors of the

company for the financial year 2018.

company was able to recover the amount in 55.8 days whereas in the year 2018 the company

was able to realize within 47.5 days (Uechi, Akutsu, Stanley, Marcus, and Kenett, 2015).

Activity Ratios Formula 2017 2018

Days Inventory Outstanding

(Inventory * 365)/

Cost of goods sold 55.8 47.5

Days Receivable Outstanding

(Accounts receivable

* 365)/ Credit sales 12.6 10.9

Days Payable Outstanding

(Average Accounts

Payable * 365)/ Cost

of Goods Sold 53.5 45.1

Hence, the overall impact suggests that the investor shall invest if the net profit margin is

improved, the liquidity position reaches beyond par level, and lastly the company shall

review the statements on regular basis.

It is the duty of the management to assess the ability of the entity to continue as a going

concern. In addition, it is the responsibility of the management to disclose the matters related

to the going concern ability and use the going concern basis of accounting. The audit team is

required to review and conclude the appropriateness of the directors’ claim and the use of the

going concern basis of accounting. In the financial statements of the entity, there have not

been prescribed any matters that threaten the going concern basis of the entity.

Measurement and Review of Financial Performance

There are various elements for the review of the financial performance; a few of them are

described as follows.

The following picture provides a glimpse of the remuneration packages of the directors of the

company for the financial year 2018.

AUDIT 11

(Source: JB Hi Fi, 2019c, p. 40)

As stated by the management in the financial statements, the packages are increased on the

lines of the increased scale of group operations resulting in increased workloads. In addition,

the remuneration has led to the benchmarking against the comparable companies. Thus, it can

be stated that the remuneration of the directors are well in line with the disclosure

requirements, Further, as stated by the company, there has been a consistent positive

correlation in the increase in the director’s remuneration and the increase in the earning per

share of the shareholders, thus justifying the increase in remuneration.

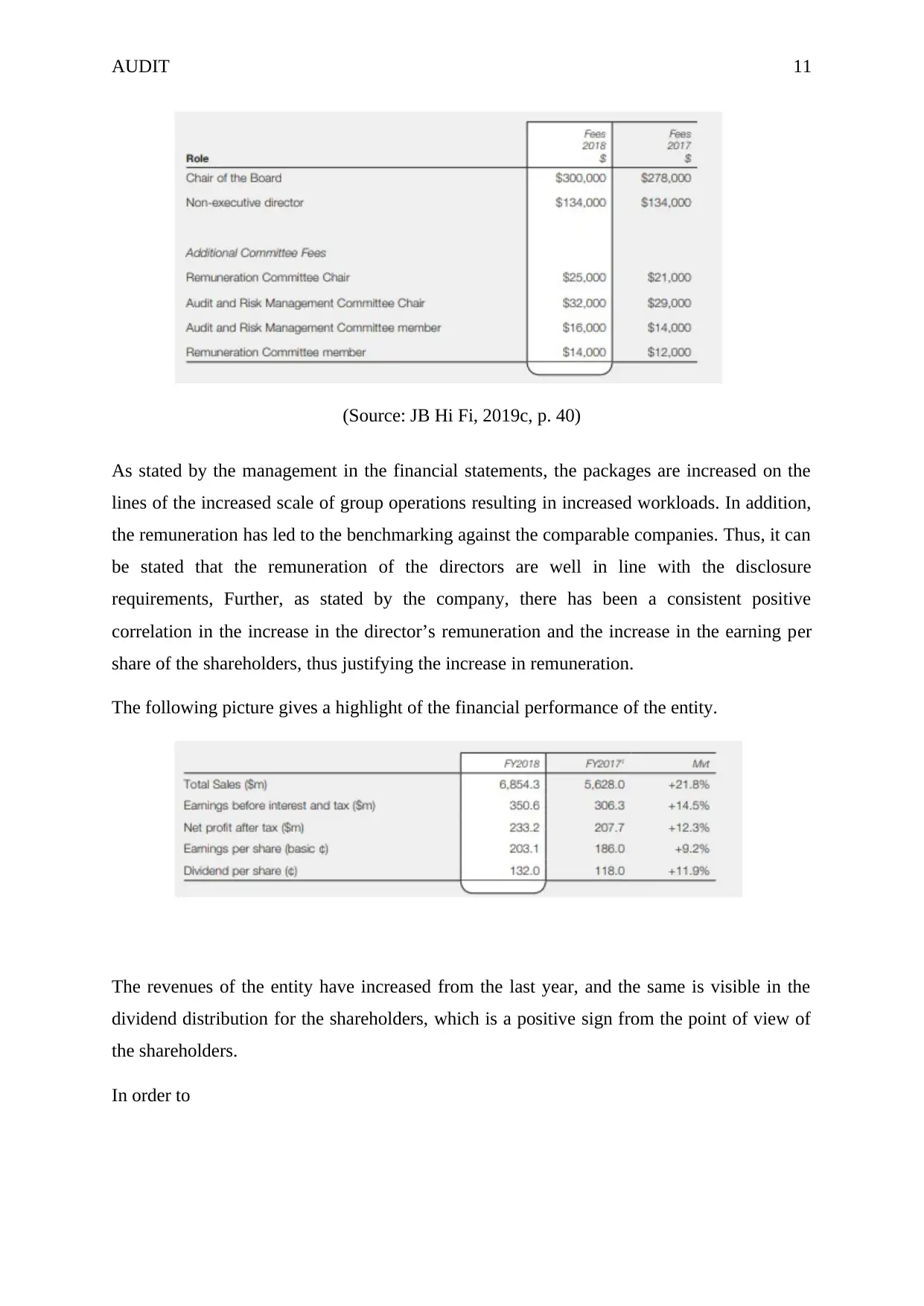

The following picture gives a highlight of the financial performance of the entity.

The revenues of the entity have increased from the last year, and the same is visible in the

dividend distribution for the shareholders, which is a positive sign from the point of view of

the shareholders.

In order to

(Source: JB Hi Fi, 2019c, p. 40)

As stated by the management in the financial statements, the packages are increased on the

lines of the increased scale of group operations resulting in increased workloads. In addition,

the remuneration has led to the benchmarking against the comparable companies. Thus, it can

be stated that the remuneration of the directors are well in line with the disclosure

requirements, Further, as stated by the company, there has been a consistent positive

correlation in the increase in the director’s remuneration and the increase in the earning per

share of the shareholders, thus justifying the increase in remuneration.

The following picture gives a highlight of the financial performance of the entity.

The revenues of the entity have increased from the last year, and the same is visible in the

dividend distribution for the shareholders, which is a positive sign from the point of view of

the shareholders.

In order to

AUDIT 12

Objectives, Strategies, and related business risks

A number of internal and external factors that can pose significant business risks to the entity

affect the operations of the business entity. Glimpses of the factors that pose business risk to

the entity are described as follows.

The entity faces a high risk of competition and loss of reputation in the fragmented Australian

market. In addition, there is a major risk of information security breach of the information

systems of the entity, inadequate health and safety measures and violation of the applicable

legislative, regulatory or the Australian Stock Exchange requirements. The group sales are

largely dependent and affected by the consumer spending capacity and cycles. In addition,

there is a business risk in the form of possible ineffective inventory management, which can

further influence the entity’s financial and operational resources. Another major risk is in the

form of possible obsolete of the technology, which can further affect the demand and supply

of the products and services of the entity. As the group is highly reliant on the IT systems,

their security, and effective functioning is one of the superior business risk and a matter of

concern for the entity. It is essential to grow and develop the IT systems and their security

measures, to mitigate the intrusion, privacy breach and other incidental risks.

Further to note, the entity is consistently facing the risks of corruption and malpractices,

which can be initiated either inside or outside the entity. In addition, the availability of

finance, changes in regulatory and legal requirements, and the possible arise of the lawsuits

against the company and legal claims are major business risks. In order to mitigate the said

risk, it is important that the company reviews its business risks from time to time and

accordingly modify its capabilities and resources.

For instance, the retailers of Australia are currently facing the challenges of falling consumer

spending combined with a high online competition. However, the company is able to beat the

expectations with its latest half-year results (Purcell, 2019). Thus, the future audit work must

take into consideration whether the company reviews the business risks or not. In addition,

the auditor must review that the entity has disclosed the significant business risks and their

potential impacts in the financial statements.

In terms of the future strategies, the company JB Hi Fi plans to open five new JB Hi Fi

Australia stores and two The Good Guys Stores. In addition, one of the JB Hi Fi store in New

Zealand was closed in the month of July 2018.

Objectives, Strategies, and related business risks

A number of internal and external factors that can pose significant business risks to the entity

affect the operations of the business entity. Glimpses of the factors that pose business risk to

the entity are described as follows.

The entity faces a high risk of competition and loss of reputation in the fragmented Australian

market. In addition, there is a major risk of information security breach of the information

systems of the entity, inadequate health and safety measures and violation of the applicable

legislative, regulatory or the Australian Stock Exchange requirements. The group sales are

largely dependent and affected by the consumer spending capacity and cycles. In addition,

there is a business risk in the form of possible ineffective inventory management, which can

further influence the entity’s financial and operational resources. Another major risk is in the

form of possible obsolete of the technology, which can further affect the demand and supply

of the products and services of the entity. As the group is highly reliant on the IT systems,

their security, and effective functioning is one of the superior business risk and a matter of

concern for the entity. It is essential to grow and develop the IT systems and their security

measures, to mitigate the intrusion, privacy breach and other incidental risks.

Further to note, the entity is consistently facing the risks of corruption and malpractices,

which can be initiated either inside or outside the entity. In addition, the availability of

finance, changes in regulatory and legal requirements, and the possible arise of the lawsuits

against the company and legal claims are major business risks. In order to mitigate the said

risk, it is important that the company reviews its business risks from time to time and

accordingly modify its capabilities and resources.

For instance, the retailers of Australia are currently facing the challenges of falling consumer

spending combined with a high online competition. However, the company is able to beat the

expectations with its latest half-year results (Purcell, 2019). Thus, the future audit work must

take into consideration whether the company reviews the business risks or not. In addition,

the auditor must review that the entity has disclosed the significant business risks and their

potential impacts in the financial statements.

In terms of the future strategies, the company JB Hi Fi plans to open five new JB Hi Fi

Australia stores and two The Good Guys Stores. In addition, one of the JB Hi Fi store in New

Zealand was closed in the month of July 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT 13

Conclusion

As per the discussions conducted in the previous parts it can be stated that a number of

factors, both internal and external factors are required to be analysed while preparing the

audit program and implanting the same, in relation to an entity. The report gave insight of the

various industrial, financial, and operational aspects of the entity JB Hi Fi Group. While the

first section of the work dealt with the business information of the client, the second section

dealt with the evaluation of financial and other material aspects. Thus, it can be rightly stated

that the audit team must consider the various industrial, financial, legal, and other factors

before the evaluation of the preparation of the financial statements and forming an opinion

thereon.

Conclusion

As per the discussions conducted in the previous parts it can be stated that a number of

factors, both internal and external factors are required to be analysed while preparing the

audit program and implanting the same, in relation to an entity. The report gave insight of the

various industrial, financial, and operational aspects of the entity JB Hi Fi Group. While the

first section of the work dealt with the business information of the client, the second section

dealt with the evaluation of financial and other material aspects. Thus, it can be rightly stated

that the audit team must consider the various industrial, financial, legal, and other factors

before the evaluation of the preparation of the financial statements and forming an opinion

thereon.

AUDIT 14

References

Australian Accounting Standards Board (2015) AASB 108- Accounting Policies, Changes in

Accounting Estimates and Errors [online] Available from:

https://www.aasb.gov.au/admin/file/content105/c9/AASB108_07-04_COMPjan15_07-15.pdf

[Accessed on 18/02/2019].

Beaver, W. H. (2018) Alternative accounting measures as predictors of failure. The

accounting review, 43(1), pp. 113-122.

Bencic, E. (2018) How JB Hi-Fi moves up global retail ladder [online] Available from:

https://www.applianceretailer.com.au/2018/08/how-jb-hi-fi-moves-up-global-retail-ladder/

[Accessed on 17/02/2019].

Demerjian, P. R. (2017) Calculating efficiency with financial accounting data: Data

envelopment analysis for accounting researchers.

JB Hi Fi Group Pty Ltd (2019a) About Us [online] Available from:

https://www.jbhifi.com.au/General/Corporate/Consumer-Matters/About-Us/ [Accessed on

17/02/2019].

JB Hi Fi Group Pty Ltd (2019b) Current Catalogues [online] Available from:

https://www.jbhifi.com.au/features/current-catalogues/ [Accessed on 17/02/2019].

JB Hi Fi Group Pty Ltd (2019c) Annual Report 2018 [online] Available from:

https://investors.jbhifi.com.au/wp-content/uploads/2018/10/Annual-Report-2018-with-

Chairmans-CEOs-Report.pdf [Accessed on 17/02/2019].

Kieso, D. E., Weygandt, J. J. and Warfield, T. D. (2016) Intermediate Accounting, Binder

Ready Version. UK: John Wiley & Sons.

Premier of Victoria (2018) Victoria’s Retail Sector Growing [online] Available from:

https://www.premier.vic.gov.au/victorias-retail-sector-growing/ [Accessed on 17/02/2019].

Purcell, K. (2019) What JB Hi-fi says about Australia’s economy [online] Available from:

https://www.yourmoney.com.au/business/economy/what-jb-hi-fi-says-about-australias-

economy/ [Accessed on 17/02/2019].

References

Australian Accounting Standards Board (2015) AASB 108- Accounting Policies, Changes in

Accounting Estimates and Errors [online] Available from:

https://www.aasb.gov.au/admin/file/content105/c9/AASB108_07-04_COMPjan15_07-15.pdf

[Accessed on 18/02/2019].

Beaver, W. H. (2018) Alternative accounting measures as predictors of failure. The

accounting review, 43(1), pp. 113-122.

Bencic, E. (2018) How JB Hi-Fi moves up global retail ladder [online] Available from:

https://www.applianceretailer.com.au/2018/08/how-jb-hi-fi-moves-up-global-retail-ladder/

[Accessed on 17/02/2019].

Demerjian, P. R. (2017) Calculating efficiency with financial accounting data: Data

envelopment analysis for accounting researchers.

JB Hi Fi Group Pty Ltd (2019a) About Us [online] Available from:

https://www.jbhifi.com.au/General/Corporate/Consumer-Matters/About-Us/ [Accessed on

17/02/2019].

JB Hi Fi Group Pty Ltd (2019b) Current Catalogues [online] Available from:

https://www.jbhifi.com.au/features/current-catalogues/ [Accessed on 17/02/2019].

JB Hi Fi Group Pty Ltd (2019c) Annual Report 2018 [online] Available from:

https://investors.jbhifi.com.au/wp-content/uploads/2018/10/Annual-Report-2018-with-

Chairmans-CEOs-Report.pdf [Accessed on 17/02/2019].

Kieso, D. E., Weygandt, J. J. and Warfield, T. D. (2016) Intermediate Accounting, Binder

Ready Version. UK: John Wiley & Sons.

Premier of Victoria (2018) Victoria’s Retail Sector Growing [online] Available from:

https://www.premier.vic.gov.au/victorias-retail-sector-growing/ [Accessed on 17/02/2019].

Purcell, K. (2019) What JB Hi-fi says about Australia’s economy [online] Available from:

https://www.yourmoney.com.au/business/economy/what-jb-hi-fi-says-about-australias-

economy/ [Accessed on 17/02/2019].

AUDIT 15

Uechi, L., Akutsu, T., Stanley, H. E., Marcus, A. J. and Kenett, D. Y. (2015) Sector

dominance ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp. 488-509.

Uechi, L., Akutsu, T., Stanley, H. E., Marcus, A. J. and Kenett, D. Y. (2015) Sector

dominance ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp. 488-509.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.