Critical Elements of Learning as Part of an Audit Team

VerifiedAdded on 2023/06/07

|5

|2165

|102

AI Summary

This document discusses the critical elements of learning as part of an audit team. It covers the duties and responsibilities of an audit assistant and senior, problem-solving and information literacy abilities, and professional conduct. The document includes extracts from the author's reflective journal to support their claims.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1Error! No text of specified style in document.

Auditing Professonal Practice

Name of the Student

Name of the University

Author Note

Page 1

Auditing Professonal Practice

Name of the Student

Name of the University

Author Note

Page 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2Error! No text of specified style in document.

Accountability

Attachment 1 – attach an extract from your Reflective Journal that talks about your team work skills (see C1: i, ii

or iii in the additional assessment information sheet in the Assessment block in Moodle).

Summarise your duties and responsibilities as an Audit Assistant for the Cloud 9 audit for weeks 5 to 8 inclusively.

My duties and responsibilities as an audit assistant include:

Executing functions to verify the precision of cash sales and accounts receivables

Check whether the books and financial statements of the entity are in conformance to industry standards.

Assessing, reviewing and recommending changes in accounting systems and controls of cloud9.

Reviewing and suggesting new modifications to existing internal audit controls

Verify whether all accounting and clients databases are updated and functioning properly

Summarise your duties and responsibilities as an Audit Senior for the Cloud 9 audit.

My duties and responsibilities as a senior auditor include:

Leading audit engagements of clients that includes planning, executing, directing and completing financial

audits

Supervising and mentoring junior auditors and trainees and helping them becoming familiar with the audit

process

Research and analyse financial statements of the entity and audit related issues and trying to find material

misstatements while analysing financial statements

Gaining a thorough understanding of the auditing standards and common audit procedures and techniques.

How did you perform your role as a team member? Identify your team work strengths and weaknesses, or aspects of

the role you found challenging. Use an extract from your Reflective Journal to support your claims.

Being a part of an audit team , I believe the group has met the desired standards of auditing

compliance requirements. I believe that we have performed our due diligence in performing the

responsibilities that we were entrusted to do. There were certain strengths and weaknesses regarding the

team. The team was extremely knowledgeable and always knew what to look for while verifying the

existence and valuation of certain items in the financial statements. The team was effective in getting the

job done within the allocated timeand dealt with the misstatements as evidenced in the reflective journal.

The weaknesses include not being able to communicate effectively as team members. There was a lack of

effective communication and not making optimum use of the talents of the team.

How did you perform your role as a leader? Identify your team work strengths and weaknesses, or aspects of the role

that you found challenging. Refer to your Reflective Journal extract for substantiation.

Being an audit leader, I had an enormous responsibility in overseeing the operations of my audit

associates and team members to see if they are applying the correct audit procedures or not. I believe that

as a leader, I performed my role to the fullest of my abilities. However there was a scope for further

improvement. As a leader, I believe that my strengths included on providing an atmosphere that was

conducive to the overall growth of my team. I am also effective in identifying the priorities and the tasks

upfront in addition to making informed decisions in light of extenuating circumstances. I have a good

problem solving mind as well. My limitations included in not being able to communicate effectively to my

team members in certain decision making areas. I also could not optimise the talents of my team members,

which falls on me.

Performance

Attachment 2 – attach an extract from your Reflective Journal that talks about your performance. Focus on your

problem-solving and information literacy abilities which you used while working with your audit team (see C2: i, ii

or iii in the additional assessment information sheet in the Assessment block in Moodle).

Summarise your overall performance and the role you played in communicating your ideas during the audit process.

Substantiate your claims with your chosen extract from your Reflective Journal.

Being a part of an audit team member, I believe that the group has performed to a desirable standard that is

in conformance with the auditing standards and the other relevant provisions. The group set out to review the

accuracy and precision of certain items in the financial statements and checking whether he book confirm to industry

standards or not. The group has successfully done that. I was tasked with modifying existing internal controls . I made

Page 2

Accountability

Attachment 1 – attach an extract from your Reflective Journal that talks about your team work skills (see C1: i, ii

or iii in the additional assessment information sheet in the Assessment block in Moodle).

Summarise your duties and responsibilities as an Audit Assistant for the Cloud 9 audit for weeks 5 to 8 inclusively.

My duties and responsibilities as an audit assistant include:

Executing functions to verify the precision of cash sales and accounts receivables

Check whether the books and financial statements of the entity are in conformance to industry standards.

Assessing, reviewing and recommending changes in accounting systems and controls of cloud9.

Reviewing and suggesting new modifications to existing internal audit controls

Verify whether all accounting and clients databases are updated and functioning properly

Summarise your duties and responsibilities as an Audit Senior for the Cloud 9 audit.

My duties and responsibilities as a senior auditor include:

Leading audit engagements of clients that includes planning, executing, directing and completing financial

audits

Supervising and mentoring junior auditors and trainees and helping them becoming familiar with the audit

process

Research and analyse financial statements of the entity and audit related issues and trying to find material

misstatements while analysing financial statements

Gaining a thorough understanding of the auditing standards and common audit procedures and techniques.

How did you perform your role as a team member? Identify your team work strengths and weaknesses, or aspects of

the role you found challenging. Use an extract from your Reflective Journal to support your claims.

Being a part of an audit team , I believe the group has met the desired standards of auditing

compliance requirements. I believe that we have performed our due diligence in performing the

responsibilities that we were entrusted to do. There were certain strengths and weaknesses regarding the

team. The team was extremely knowledgeable and always knew what to look for while verifying the

existence and valuation of certain items in the financial statements. The team was effective in getting the

job done within the allocated timeand dealt with the misstatements as evidenced in the reflective journal.

The weaknesses include not being able to communicate effectively as team members. There was a lack of

effective communication and not making optimum use of the talents of the team.

How did you perform your role as a leader? Identify your team work strengths and weaknesses, or aspects of the role

that you found challenging. Refer to your Reflective Journal extract for substantiation.

Being an audit leader, I had an enormous responsibility in overseeing the operations of my audit

associates and team members to see if they are applying the correct audit procedures or not. I believe that

as a leader, I performed my role to the fullest of my abilities. However there was a scope for further

improvement. As a leader, I believe that my strengths included on providing an atmosphere that was

conducive to the overall growth of my team. I am also effective in identifying the priorities and the tasks

upfront in addition to making informed decisions in light of extenuating circumstances. I have a good

problem solving mind as well. My limitations included in not being able to communicate effectively to my

team members in certain decision making areas. I also could not optimise the talents of my team members,

which falls on me.

Performance

Attachment 2 – attach an extract from your Reflective Journal that talks about your performance. Focus on your

problem-solving and information literacy abilities which you used while working with your audit team (see C2: i, ii

or iii in the additional assessment information sheet in the Assessment block in Moodle).

Summarise your overall performance and the role you played in communicating your ideas during the audit process.

Substantiate your claims with your chosen extract from your Reflective Journal.

Being a part of an audit team member, I believe that the group has performed to a desirable standard that is

in conformance with the auditing standards and the other relevant provisions. The group set out to review the

accuracy and precision of certain items in the financial statements and checking whether he book confirm to industry

standards or not. The group has successfully done that. I was tasked with modifying existing internal controls . I made

Page 2

3Error! No text of specified style in document.

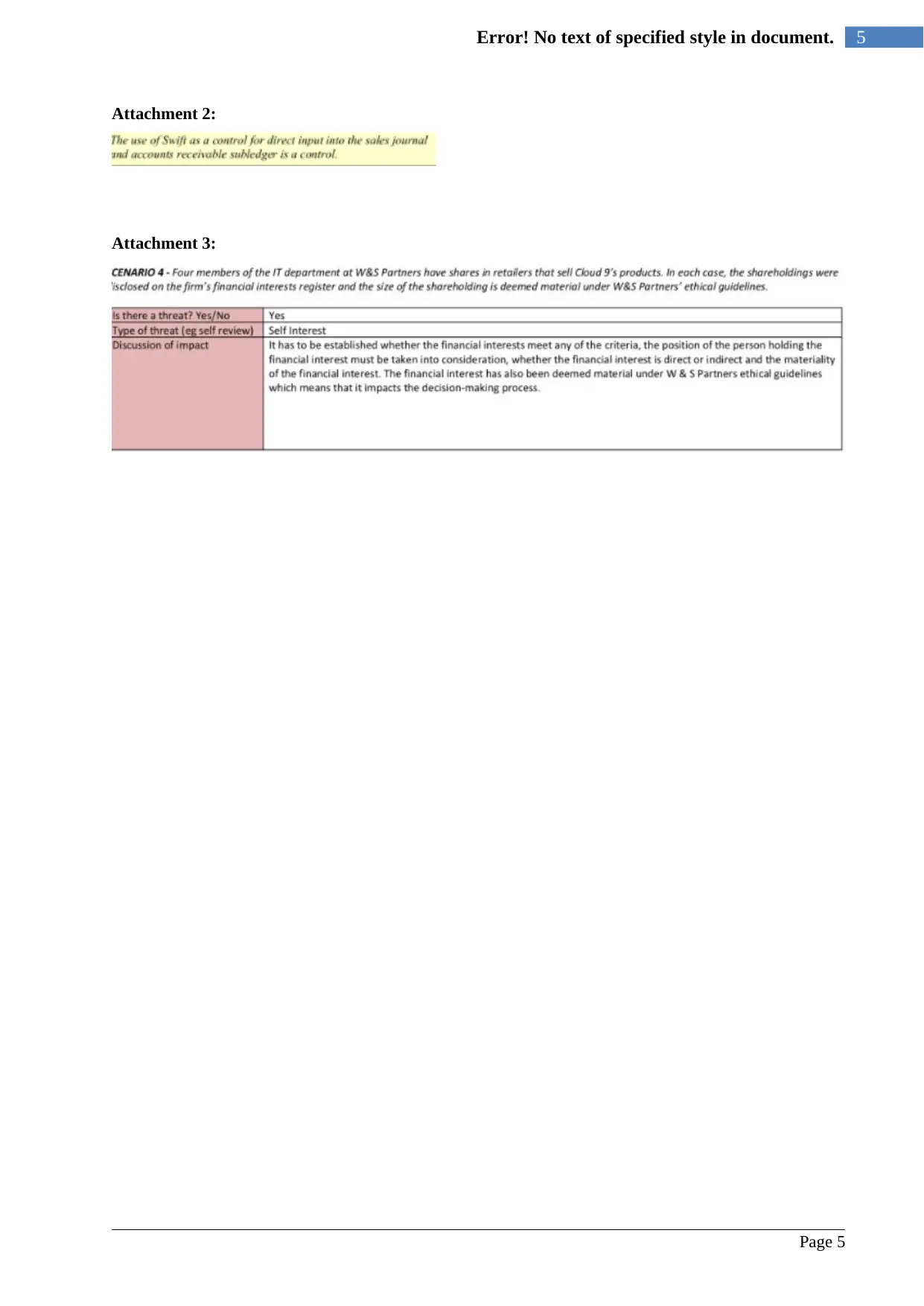

a suggestion to the management of cloud 9 the use of a swift system to help allocate a transaction simultaneously

into sales and accounts receivable system

What did you do? How well did you perform and contribute through problem-solving and information literacy, and

what part did this play in successfully completing the Cloud 9 audit?

I suggested use of a modified version of a Swift system that would help in allocating a transaction

that could simultaneously allocate cash sales and accounts payable at the same time without the need to

make relevant adjustments in either of them. This helped cloud 9 in verifying the mismatch of amounts

relates to accounts receivables and sales figures. The actual figures were not properly reflected in the

accounts. It successfully helped in implementing audit procedures of verifying the accuracy of the figure

statements. This helped in showing the financial statements in a true and fair view, thereby successfully

implementing the basic function of auditing. This helped in completing the cloud 9 audit in a fair and

responsible manner.

Professional conduct

Attachment 3 – attach an extract from your Reflective Journal that talks about your professional conduct,

especially your ethical practice while working with your audit team during the term (see C3: i, ii or iii in the

additional assessment information sheet in the Assessment block in Moodle).

Summarise your thoughts on professionalism and ethical practice, drawing on your experience as an Audit Assistant

for W & S Partners, working independently and as part of a team. For example, how well did you demonstrate your

professional and ethical behaviour towards others? Draw on your Reflective Journal to give some examples of your

approaches.

Being a part of the auditing team at W& s partners, I have drawn on strict and principled code of ethics as

per the auditing standards that have been prescribed. I have displayed integrity in the course of my work and my

conduct has been beyond reproach. I have enjoyed being a part of this team. I have a high degree of professional

respect for my team members . I have been independent in my dealings and have not paid heed to any outside

influences. I have been objective and impartial in the work that was entrusted with me. My behaviour as a whole has

been strictly professional and very much objective while dealing with others.

Explain your awareness in upholding professional values and ethics, e.g. what measures did you personally observe,

or most likely to observe in the future? Support your assertions with an extract from your Reflective Journal.

As an auditor, I understand the value of upholding professional ethics and values. It helps in

examining the financial statements in a fair and responsible manner. It is a boundary that draws the line

between what is right and what is wrong. Auditors have a duty to be competent and maintain professional

secrecy in dealings with audit matters. In this case there have seen evidences of some partners in our

company who have bought shares in cloud 9. We have examined that and concluded that the nature of the

association is enough to warrant a change in the decision making process. We have taken appropriate

steps in assessing he threats of self interest and familiarity in other matters as well. Without these standards

of conduct, the financial statements would not reflect a true and fair view. It would affect the users of

financial statements who chose to associate with a particular company after reading the audit report that

certifies that all the dealing that have been done by the company is proper and that there have been no

material disclosures that would adversely affect any stakeholder of the company. I hope that by keeping

this experience in mind, I would like to be more competent in my professional dealings in the future and

try to maintain a professional distance with the clients that I am auditing.

Summary

Page 3

a suggestion to the management of cloud 9 the use of a swift system to help allocate a transaction simultaneously

into sales and accounts receivable system

What did you do? How well did you perform and contribute through problem-solving and information literacy, and

what part did this play in successfully completing the Cloud 9 audit?

I suggested use of a modified version of a Swift system that would help in allocating a transaction

that could simultaneously allocate cash sales and accounts payable at the same time without the need to

make relevant adjustments in either of them. This helped cloud 9 in verifying the mismatch of amounts

relates to accounts receivables and sales figures. The actual figures were not properly reflected in the

accounts. It successfully helped in implementing audit procedures of verifying the accuracy of the figure

statements. This helped in showing the financial statements in a true and fair view, thereby successfully

implementing the basic function of auditing. This helped in completing the cloud 9 audit in a fair and

responsible manner.

Professional conduct

Attachment 3 – attach an extract from your Reflective Journal that talks about your professional conduct,

especially your ethical practice while working with your audit team during the term (see C3: i, ii or iii in the

additional assessment information sheet in the Assessment block in Moodle).

Summarise your thoughts on professionalism and ethical practice, drawing on your experience as an Audit Assistant

for W & S Partners, working independently and as part of a team. For example, how well did you demonstrate your

professional and ethical behaviour towards others? Draw on your Reflective Journal to give some examples of your

approaches.

Being a part of the auditing team at W& s partners, I have drawn on strict and principled code of ethics as

per the auditing standards that have been prescribed. I have displayed integrity in the course of my work and my

conduct has been beyond reproach. I have enjoyed being a part of this team. I have a high degree of professional

respect for my team members . I have been independent in my dealings and have not paid heed to any outside

influences. I have been objective and impartial in the work that was entrusted with me. My behaviour as a whole has

been strictly professional and very much objective while dealing with others.

Explain your awareness in upholding professional values and ethics, e.g. what measures did you personally observe,

or most likely to observe in the future? Support your assertions with an extract from your Reflective Journal.

As an auditor, I understand the value of upholding professional ethics and values. It helps in

examining the financial statements in a fair and responsible manner. It is a boundary that draws the line

between what is right and what is wrong. Auditors have a duty to be competent and maintain professional

secrecy in dealings with audit matters. In this case there have seen evidences of some partners in our

company who have bought shares in cloud 9. We have examined that and concluded that the nature of the

association is enough to warrant a change in the decision making process. We have taken appropriate

steps in assessing he threats of self interest and familiarity in other matters as well. Without these standards

of conduct, the financial statements would not reflect a true and fair view. It would affect the users of

financial statements who chose to associate with a particular company after reading the audit report that

certifies that all the dealing that have been done by the company is proper and that there have been no

material disclosures that would adversely affect any stakeholder of the company. I hope that by keeping

this experience in mind, I would like to be more competent in my professional dealings in the future and

try to maintain a professional distance with the clients that I am auditing.

Summary

Page 3

4Error! No text of specified style in document.

In 500 words or less, discuss the critical elements of your learning as part of an audit team, paying particular

attention to some of the questions outlined within the additional information sheet provided in the Assessment block

in Moodle. You may have already written similar reflections in your Reflective Journal; please feel free to use and

summarise what you have already recorded in your journal. You may also indicate the date of your journal entries to

demonstrate improvement in your professional practice skills. Do not include reflections in this section that you have

included elsewhere in this document.

As a part of the audit team, we found evidence of material misstatement with regards to cash

receipts in terms of not being recorded when it gets received and the amounts differing from the ones that

are actually deposited. There has been an evidence of other misstatement that includes induplication of

sales amounts and credit memos not recognised on a timely basis. The company has modified its existing

system of internal control that includes development of a software that enables transactions to be

formulated into sales and accounts receivable and the company should also implement a tracking software

that tracks voucher numbers and memos. The material misstatements fail to provide auditors with giving

the assertions that they need in verifying the items of financial statements. There has also ben evidence of

conflict of interest among certain things like for instance when the finance director, David Coller is

married to a distant relation of PS Nethercott , a partner in w& s partners consulting department. However

the degree of threat or potential impact was found to be lacking according o APES 110 as the nature of the

relationship was not enough to warrant a conflicting self interest. A couple of our members of the it

department also bought so shares of the company cloud 9 . On review, the financial ipavts were found to

be of a considerable e degree that it could impact the decision making process. The audit was conducted

with due diligence and integrity . The audit was performed with a high degree of standard and keeping in

mind a strict code of conduct and ethics. The material misstatements were found out, their impacts

assessed and adequately disclosed in the auditors report. The level of planning materiality was assessed in

reference to the cloud 9 . It elected the amount of misstatement exceeding which can be considered to be

material. The audit team functioned very well within the responsibilities and framework that was required

to follow. The performance was certainly effective because it helped weed out a lot of misstatements and

inconsistencies while formulating an audit opinion. The importance of holding professional value and

ethics were paramount in this case. The professional code keeps a strict line on maintaining auditors

responsibility in terms of keeping professional distance with clients and not getting swayed by external

influence . the auditor should never allow himself to be compromised. He should always be fair and

impartial. As an auditor, there are important lessons to be learnt here in terms of how to conduct myself

even more better in a professional setting and not getting swayed by external influences. It is very

important to thorough check all important financial matters and see that the auditing procedures the

company ha applied are fair or not.

Journal Extracts

Copy and paste extracts from your online Reflective Journal, under the appropriate headings below.

Attachment 1:

Page 4

In 500 words or less, discuss the critical elements of your learning as part of an audit team, paying particular

attention to some of the questions outlined within the additional information sheet provided in the Assessment block

in Moodle. You may have already written similar reflections in your Reflective Journal; please feel free to use and

summarise what you have already recorded in your journal. You may also indicate the date of your journal entries to

demonstrate improvement in your professional practice skills. Do not include reflections in this section that you have

included elsewhere in this document.

As a part of the audit team, we found evidence of material misstatement with regards to cash

receipts in terms of not being recorded when it gets received and the amounts differing from the ones that

are actually deposited. There has been an evidence of other misstatement that includes induplication of

sales amounts and credit memos not recognised on a timely basis. The company has modified its existing

system of internal control that includes development of a software that enables transactions to be

formulated into sales and accounts receivable and the company should also implement a tracking software

that tracks voucher numbers and memos. The material misstatements fail to provide auditors with giving

the assertions that they need in verifying the items of financial statements. There has also ben evidence of

conflict of interest among certain things like for instance when the finance director, David Coller is

married to a distant relation of PS Nethercott , a partner in w& s partners consulting department. However

the degree of threat or potential impact was found to be lacking according o APES 110 as the nature of the

relationship was not enough to warrant a conflicting self interest. A couple of our members of the it

department also bought so shares of the company cloud 9 . On review, the financial ipavts were found to

be of a considerable e degree that it could impact the decision making process. The audit was conducted

with due diligence and integrity . The audit was performed with a high degree of standard and keeping in

mind a strict code of conduct and ethics. The material misstatements were found out, their impacts

assessed and adequately disclosed in the auditors report. The level of planning materiality was assessed in

reference to the cloud 9 . It elected the amount of misstatement exceeding which can be considered to be

material. The audit team functioned very well within the responsibilities and framework that was required

to follow. The performance was certainly effective because it helped weed out a lot of misstatements and

inconsistencies while formulating an audit opinion. The importance of holding professional value and

ethics were paramount in this case. The professional code keeps a strict line on maintaining auditors

responsibility in terms of keeping professional distance with clients and not getting swayed by external

influence . the auditor should never allow himself to be compromised. He should always be fair and

impartial. As an auditor, there are important lessons to be learnt here in terms of how to conduct myself

even more better in a professional setting and not getting swayed by external influences. It is very

important to thorough check all important financial matters and see that the auditing procedures the

company ha applied are fair or not.

Journal Extracts

Copy and paste extracts from your online Reflective Journal, under the appropriate headings below.

Attachment 1:

Page 4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5Error! No text of specified style in document.

Attachment 2:

Attachment 3:

Page 5

Attachment 2:

Attachment 3:

Page 5

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.