Comprehensive Audit Plan and Testing for Fuchsia Enterprises Report

VerifiedAdded on 2020/04/01

|10

|2361

|44

Report

AI Summary

This report presents an audit plan for Fuchsia Enterprises, analyzing its trial balance and identifying seven key accounts requiring significant attention. The analysis includes interest income, bank loans, miscellaneous expenses, accumulated depreciation on machinery, accounts receivables, depreciation, and wages. For each account, the report provides an analytical review, highlighting percentage changes and potential risks. It recommends specific audit procedures, such as recalculating interest income, testing sales controls, verifying machinery depreciation, confirming accounts receivables, and checking wage calculations. The report emphasizes the importance of verifying financial records, tracing transactions, and employing analytical procedures to ensure the accuracy and completeness of financial statements, with a focus on mitigating potential misstatements and fraud. Additionally, it suggests reviewing supporting documentation and comparing financial data to identify discrepancies.

Audit Testing 1

Student Name

Course and Section Number

Class Time

Instructor Name

Student Name

Course and Section Number

Class Time

Instructor Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit Testing 2

Audit Planning

An Audit plan is considered to be specific guidelines to be followed when performing an

audit. It helps the auditor in obtaining sufficient appropriate evidence for the situations, helps

keep the cost of auditing at a reasonable level and also helps the auditor in avoiding

misunderstandings with the client1. Audit planning is usually an important area in auditing

that is basically performed at the beginning of the audit in order to ensure that sustainable

attention is devoted to particular areas and potential issues are quickly identified. Before audit

testing, the auditor usually plans to carry out an audit an effective and timely manner through

designing detailed procedures in order to obtain sufficient appropriate audit evidence. This

particular assignment entails planning of an audit for Fuchsia Enterprises after checking its

preliminary Trial Balance2. This assignment also extracts information from the enterprises

trial balance and identifies the accounts that are likely to require substantial attention, provide

analytical procedures for each of the item and the possible recommendation for the audit

procedure to be used in the auditing. According to Fuchsia Enterprises trial balance, the

selected seven accounts for audit that require attention are;

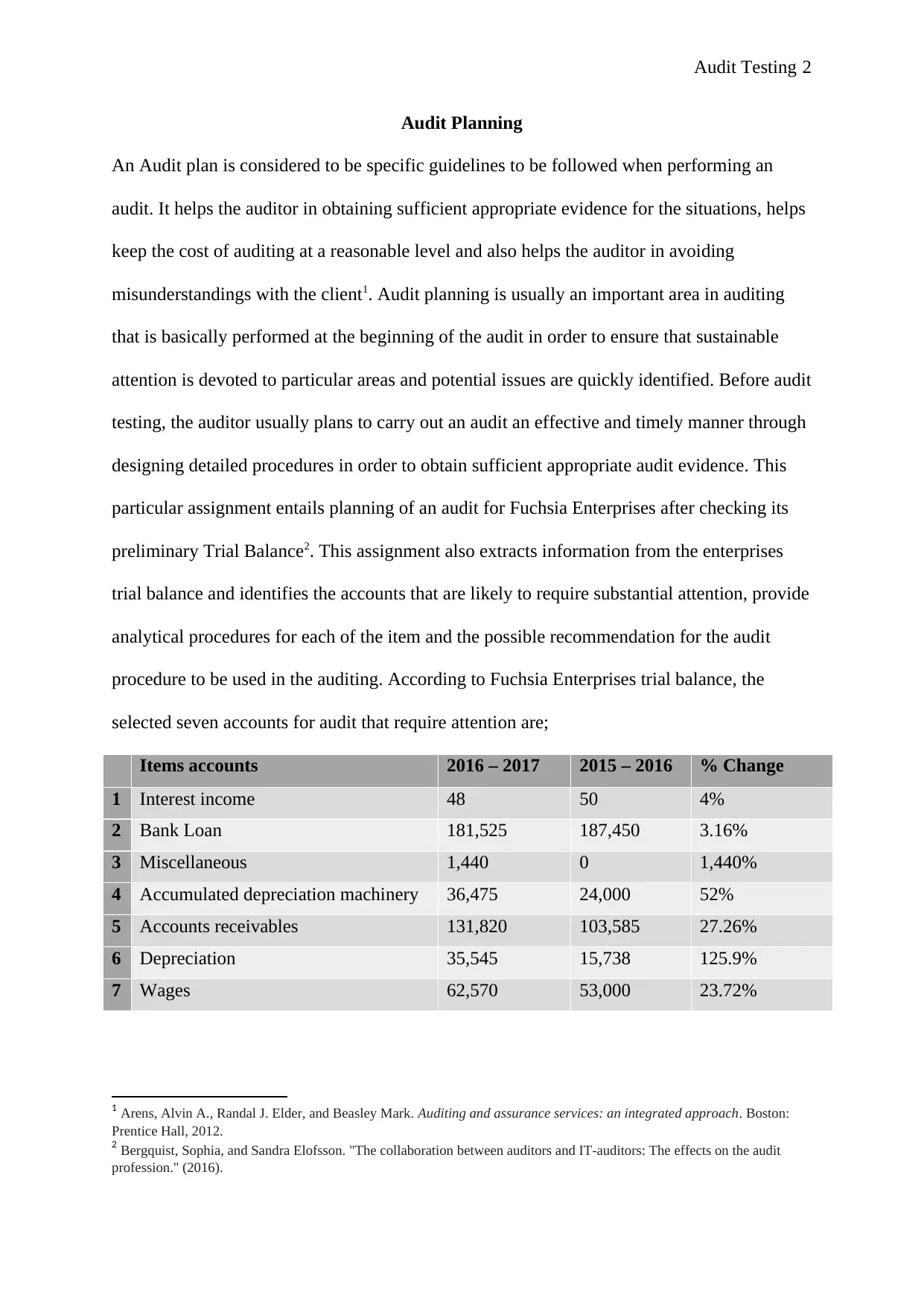

Items accounts 2016 – 2017 2015 – 2016 % Change

1 Interest income 48 50 4%

2 Bank Loan 181,525 187,450 3.16%

3 Miscellaneous 1,440 0 1,440%

4 Accumulated depreciation machinery 36,475 24,000 52%

5 Accounts receivables 131,820 103,585 27.26%

6 Depreciation 35,545 15,738 125.9%

7 Wages 62,570 53,000 23.72%

1 Arens, Alvin A., Randal J. Elder, and Beasley Mark. Auditing and assurance services: an integrated approach. Boston:

Prentice Hall, 2012.

2 Bergquist, Sophia, and Sandra Elofsson. "The collaboration between auditors and IT-auditors: The effects on the audit

profession." (2016).

Audit Planning

An Audit plan is considered to be specific guidelines to be followed when performing an

audit. It helps the auditor in obtaining sufficient appropriate evidence for the situations, helps

keep the cost of auditing at a reasonable level and also helps the auditor in avoiding

misunderstandings with the client1. Audit planning is usually an important area in auditing

that is basically performed at the beginning of the audit in order to ensure that sustainable

attention is devoted to particular areas and potential issues are quickly identified. Before audit

testing, the auditor usually plans to carry out an audit an effective and timely manner through

designing detailed procedures in order to obtain sufficient appropriate audit evidence. This

particular assignment entails planning of an audit for Fuchsia Enterprises after checking its

preliminary Trial Balance2. This assignment also extracts information from the enterprises

trial balance and identifies the accounts that are likely to require substantial attention, provide

analytical procedures for each of the item and the possible recommendation for the audit

procedure to be used in the auditing. According to Fuchsia Enterprises trial balance, the

selected seven accounts for audit that require attention are;

Items accounts 2016 – 2017 2015 – 2016 % Change

1 Interest income 48 50 4%

2 Bank Loan 181,525 187,450 3.16%

3 Miscellaneous 1,440 0 1,440%

4 Accumulated depreciation machinery 36,475 24,000 52%

5 Accounts receivables 131,820 103,585 27.26%

6 Depreciation 35,545 15,738 125.9%

7 Wages 62,570 53,000 23.72%

1 Arens, Alvin A., Randal J. Elder, and Beasley Mark. Auditing and assurance services: an integrated approach. Boston:

Prentice Hall, 2012.

2 Bergquist, Sophia, and Sandra Elofsson. "The collaboration between auditors and IT-auditors: The effects on the audit

profession." (2016).

Audit Testing 3

Analytical review

Generally, use of analytical reviews is considered to be one of the procedures for increasing

the auditor’s efficiency3. Analytical procedures usually consist of an assessment of financial

data prepared by the auditors of and the expected relationship between nonfinancial and

financial data.

Interest income

Interest income is one of the areas in the enterprise trial balance that basically requires

significant attention. The company revenues may be at risks. Interest income area requires

great attention because it is more at risks by the misappropriation by the company

management4. The interest income is usually am accessible funds by the management and

thus making it more vulnerable to misuse. According to Fuchsia Enterprise's trial balance, the

amount of interest income as at FY2015-2016 was A$50,000 and A$48,000 at FY2016-2017.

According to the trial balance analysis, there is an indication that there is a 20% decrease in

the amount recorded as interest income5. The decrease in the amount received should be

scrutinized thoroughly to determine if there is any possibility of the fund's misuse by the

management. The difference in the two amounts should be recalculated so as to check if

proper evaluations were conducted so as to enhance its materiality. Basing on the riskiness of

this item, I recommend that the auditors must recalculate interest income on note receivables

to determine if proper formulas were used.

Sales

Sales is another item that basically requires special attention when planning for the audit.

This is because the item is vulnerable to greater risks when the company is carrying out its

business. According to the company, the business usually sells its products either in cash or

3 Arens, Alvin A., Randal J. Elder, Mark S. Beasley, and Chris E. Hogan. Auditing and assurance services. Pearson, 2016.

4 Vona, Leonard W. Fraud risk assessment: building a fraud audit program. John Wiley & Sons, 2012.

5 Rahim, Siti Rohaya Mat, Fauziah Mahat, Annuar Md Nassir, and Mohamed Hisham Dato Hj Yahya. "Re-thinking: Risk

Governance?." Procedia Economics and Finance 31 (2015): 689-698.

Analytical review

Generally, use of analytical reviews is considered to be one of the procedures for increasing

the auditor’s efficiency3. Analytical procedures usually consist of an assessment of financial

data prepared by the auditors of and the expected relationship between nonfinancial and

financial data.

Interest income

Interest income is one of the areas in the enterprise trial balance that basically requires

significant attention. The company revenues may be at risks. Interest income area requires

great attention because it is more at risks by the misappropriation by the company

management4. The interest income is usually am accessible funds by the management and

thus making it more vulnerable to misuse. According to Fuchsia Enterprise's trial balance, the

amount of interest income as at FY2015-2016 was A$50,000 and A$48,000 at FY2016-2017.

According to the trial balance analysis, there is an indication that there is a 20% decrease in

the amount recorded as interest income5. The decrease in the amount received should be

scrutinized thoroughly to determine if there is any possibility of the fund's misuse by the

management. The difference in the two amounts should be recalculated so as to check if

proper evaluations were conducted so as to enhance its materiality. Basing on the riskiness of

this item, I recommend that the auditors must recalculate interest income on note receivables

to determine if proper formulas were used.

Sales

Sales is another item that basically requires special attention when planning for the audit.

This is because the item is vulnerable to greater risks when the company is carrying out its

business. According to the company, the business usually sells its products either in cash or

3 Arens, Alvin A., Randal J. Elder, Mark S. Beasley, and Chris E. Hogan. Auditing and assurance services. Pearson, 2016.

4 Vona, Leonard W. Fraud risk assessment: building a fraud audit program. John Wiley & Sons, 2012.

5 Rahim, Siti Rohaya Mat, Fauziah Mahat, Annuar Md Nassir, and Mohamed Hisham Dato Hj Yahya. "Re-thinking: Risk

Governance?." Procedia Economics and Finance 31 (2015): 689-698.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit Testing 4

credit terms thus making the item to be at risk. The riskiness of this particular item requires

the auditors to carry out proper analytical procedures to determine its physical existence in

the sales records. The company will also be required to provide a movement schedule that

can be used to compare the amount of sales in the two accounting periods6. Fuchsia

Enterprises trial balance indicates that during the FY2015-2016, the business had

AU$187,450 and AU$181,525 as at FY2016-2017. This aspect demonstrates a 3.16%

material decrease, the audit check should ascertain if its cash or credit sales and as well look

on the amounts of accounts receivables and sales are accurate by verifying each of them and

find possible misstatements. The variations between the two values should be determined to

check the reasonableness of the variations. The auditors should check for existence in the

stock records and ascertain the movement from store to client. Basing n the riskiness of this

item, I recommend the auditor to test for controls of the enterprise set up for sale cycle in

order to ascertain their reliability and existence in the movement schedule7. The auditor ought

also to ascertain if the accounting records for accounts receivables and sales are accurate by

basically verifying individual transactions for the probable misstatement.

Accumulated depreciation on machinery

This is another area that needs great attention that should be done to ascertain compliance and

integrity of the financial statements. This particular item is selected because of its riskiness

that may affect materiality of the financial statements. Audit procedures for accumulated

depreciation on machinery are material so as to ensure that the recorded depreciation is free

of material accounting errors8. The auditor should match the accounts balances to find out for

potential accounting errors or even frauds from demonstrating in the financial records. The

52% increase from AU$24,000 in FY2015-2016 to AU$36,475 in FY2016-2017 should be

6 Elder, Randal J., Mark S. Beasley, and Alvin A. Arens. Auditing and Assurance services. Pearson Higher Ed, 2011.

7 Hammersley, Jacqueline S. "A review and model of auditor judgments in fraud-related planning tasks." Auditing: A

Journal of Practice & Theory 30, no. 4 (2011): 101-128.

8 Rahim, Siti Rohaya Mat, Fauziah Mahat, Annuar Md Nassir, and Mohamed Hisham Dato Hj Yahya. "Re-thinking: Risk

Governance?." Procedia Economics and Finance 31 (2015): 689-698.

credit terms thus making the item to be at risk. The riskiness of this particular item requires

the auditors to carry out proper analytical procedures to determine its physical existence in

the sales records. The company will also be required to provide a movement schedule that

can be used to compare the amount of sales in the two accounting periods6. Fuchsia

Enterprises trial balance indicates that during the FY2015-2016, the business had

AU$187,450 and AU$181,525 as at FY2016-2017. This aspect demonstrates a 3.16%

material decrease, the audit check should ascertain if its cash or credit sales and as well look

on the amounts of accounts receivables and sales are accurate by verifying each of them and

find possible misstatements. The variations between the two values should be determined to

check the reasonableness of the variations. The auditors should check for existence in the

stock records and ascertain the movement from store to client. Basing n the riskiness of this

item, I recommend the auditor to test for controls of the enterprise set up for sale cycle in

order to ascertain their reliability and existence in the movement schedule7. The auditor ought

also to ascertain if the accounting records for accounts receivables and sales are accurate by

basically verifying individual transactions for the probable misstatement.

Accumulated depreciation on machinery

This is another area that needs great attention that should be done to ascertain compliance and

integrity of the financial statements. This particular item is selected because of its riskiness

that may affect materiality of the financial statements. Audit procedures for accumulated

depreciation on machinery are material so as to ensure that the recorded depreciation is free

of material accounting errors8. The auditor should match the accounts balances to find out for

potential accounting errors or even frauds from demonstrating in the financial records. The

52% increase from AU$24,000 in FY2015-2016 to AU$36,475 in FY2016-2017 should be

6 Elder, Randal J., Mark S. Beasley, and Alvin A. Arens. Auditing and Assurance services. Pearson Higher Ed, 2011.

7 Hammersley, Jacqueline S. "A review and model of auditor judgments in fraud-related planning tasks." Auditing: A

Journal of Practice & Theory 30, no. 4 (2011): 101-128.

8 Rahim, Siti Rohaya Mat, Fauziah Mahat, Annuar Md Nassir, and Mohamed Hisham Dato Hj Yahya. "Re-thinking: Risk

Governance?." Procedia Economics and Finance 31 (2015): 689-698.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit Testing 5

determined, and that proper recalculation should be done to determine accuracy. Basing on

the riskiness of the item, I recommend that the auditor must verify the historical value of the

machinery, analyze the related accumulated depreciation accounts for completeness. The

auditor should also recalculate the depreciation expenses and gains or losses on disposal of

fixed assets to ascertain accuracy and completeness of the entire transaction9. The auditor

should also attempt to compare depreciation expenses so as to determine any possible

misstatements.

Accounts receivables

Accounts receivables is another risky item that basically requires significant attention when

planning for the audit. This is because most of the firm’s management may collude with some

of the debtors and record wrong entries into their names so as to gain funds. Some firms may

also post some amounts of trade receivables that actually do not exist and thus may lead the

company losing significant amount of revenues. Enterprise trade receivables should be

examined for existence and accuracy assertions. This aspect is vital since some trade

receivables may be understated or overstated and thus affecting the company revenues. When

planning to audit trade receivables, debtor’s circularization should be carried out, so s to

ascertain the existence of debtors and also to confirm the amount owed to the business.

According to Fuchsia Enterprises trial balance, the 26.27% increase in the accounts

receivables from AU$103,585 in FY2015-2016 to AU$131,820 in FY2016-2017 need to be

ascertained so as to make sure that proper controls and strategies were employed by the

company in order to check the reasons for the increase10. When planning for the audit, I

recommend tracing the trade receivables in the company general ledgers. The auditor must

request for a period end trade receivables with details from which they will assist in outlining

9 Hammersley, Jacqueline S., Karla M. Johnstone, and Kathryn Kadous. "How do audit seniors respond to heightened fraud

risk?." Auditing: A Journal of Practice & Theory 30, no. 3 (2011): 81-101.

10 Cohen, Jeffrey R., Lori L. Holder-Webb, Leda Nath, and David Wood. "Corporate reporting of nonfinancial leading

indicators of economic performance and sustainability." Accounting Horizons26, no. 1 (2012): 65-90.

determined, and that proper recalculation should be done to determine accuracy. Basing on

the riskiness of the item, I recommend that the auditor must verify the historical value of the

machinery, analyze the related accumulated depreciation accounts for completeness. The

auditor should also recalculate the depreciation expenses and gains or losses on disposal of

fixed assets to ascertain accuracy and completeness of the entire transaction9. The auditor

should also attempt to compare depreciation expenses so as to determine any possible

misstatements.

Accounts receivables

Accounts receivables is another risky item that basically requires significant attention when

planning for the audit. This is because most of the firm’s management may collude with some

of the debtors and record wrong entries into their names so as to gain funds. Some firms may

also post some amounts of trade receivables that actually do not exist and thus may lead the

company losing significant amount of revenues. Enterprise trade receivables should be

examined for existence and accuracy assertions. This aspect is vital since some trade

receivables may be understated or overstated and thus affecting the company revenues. When

planning to audit trade receivables, debtor’s circularization should be carried out, so s to

ascertain the existence of debtors and also to confirm the amount owed to the business.

According to Fuchsia Enterprises trial balance, the 26.27% increase in the accounts

receivables from AU$103,585 in FY2015-2016 to AU$131,820 in FY2016-2017 need to be

ascertained so as to make sure that proper controls and strategies were employed by the

company in order to check the reasons for the increase10. When planning for the audit, I

recommend tracing the trade receivables in the company general ledgers. The auditor must

request for a period end trade receivables with details from which they will assist in outlining

9 Hammersley, Jacqueline S., Karla M. Johnstone, and Kathryn Kadous. "How do audit seniors respond to heightened fraud

risk?." Auditing: A Journal of Practice & Theory 30, no. 3 (2011): 81-101.

10 Cohen, Jeffrey R., Lori L. Holder-Webb, Leda Nath, and David Wood. "Corporate reporting of nonfinancial leading

indicators of economic performance and sustainability." Accounting Horizons26, no. 1 (2012): 65-90.

Audit Testing 6

the totals in the trial balance and those in the ledgers. I also recommend the auditors to

confirm the accounts receivables existence by basically calling the debtors and asking them

for personal details and the amount each owes the company. This will also be done by

contacting the business debtors and requesting them to confirm their amounts of unpaid

accounts receivables as of the end of the reporting period being audited for the possible

misstatement.

Depreciation

Another item that needs significant attention is depreciation. This is a risky item that needs to

be majorly examined because managers may employ wrong calculation methods to

misappropriate some of the company funds11. The basis used to evaluate the amount of

depreciation should be checked to ensure that it is basically free from any manipulation.

Planning for the audit should also ensure that depreciation amount has been recalculated

again in order to ascertain the accuracy of the amount posted in the trial balance. The 125.9%

increase in the amount of depreciation should be re-evaluated and that the company should

provide reasonable support to the assets depreciated. The increase of depreciation amount

from AU$15,738 in FY2015-2016 to AU$35,545 in FY2016-2017 has a bigger margin.

Recalculation should be emphasized so as to ascertain the accurateness and correctness of the

stated amount12. Due to the riskiness of this item, I recommend that the auditor must check

the method used for depreciation and the actual cost of the assets being depreciated so as to

determine any possible misstatement in the trial balance.

Wages

Another item that needs significant attention is wages. This item is considered to seek greater

attention because of its materiality in the financial statements. Wages can be misstated by

11 Messier Jr, William F., Chad A. Simon, and Jason L. Smith. "Two decades of behavioral research on analytical

procedures: What have we learned?." Auditing: A Journal of Practice & Theory 32, no. 1 (2012): 139-181.

12 Titera, William R. "Updating audit standard—Enabling audit data analysis." Journal of Information Systems 27, no. 1

(2013): 325-331.

the totals in the trial balance and those in the ledgers. I also recommend the auditors to

confirm the accounts receivables existence by basically calling the debtors and asking them

for personal details and the amount each owes the company. This will also be done by

contacting the business debtors and requesting them to confirm their amounts of unpaid

accounts receivables as of the end of the reporting period being audited for the possible

misstatement.

Depreciation

Another item that needs significant attention is depreciation. This is a risky item that needs to

be majorly examined because managers may employ wrong calculation methods to

misappropriate some of the company funds11. The basis used to evaluate the amount of

depreciation should be checked to ensure that it is basically free from any manipulation.

Planning for the audit should also ensure that depreciation amount has been recalculated

again in order to ascertain the accuracy of the amount posted in the trial balance. The 125.9%

increase in the amount of depreciation should be re-evaluated and that the company should

provide reasonable support to the assets depreciated. The increase of depreciation amount

from AU$15,738 in FY2015-2016 to AU$35,545 in FY2016-2017 has a bigger margin.

Recalculation should be emphasized so as to ascertain the accurateness and correctness of the

stated amount12. Due to the riskiness of this item, I recommend that the auditor must check

the method used for depreciation and the actual cost of the assets being depreciated so as to

determine any possible misstatement in the trial balance.

Wages

Another item that needs significant attention is wages. This item is considered to seek greater

attention because of its materiality in the financial statements. Wages can be misstated by

11 Messier Jr, William F., Chad A. Simon, and Jason L. Smith. "Two decades of behavioral research on analytical

procedures: What have we learned?." Auditing: A Journal of Practice & Theory 32, no. 1 (2012): 139-181.

12 Titera, William R. "Updating audit standard—Enabling audit data analysis." Journal of Information Systems 27, no. 1

(2013): 325-331.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit Testing 7

firm managers who may seek to misappropriate the funds. When planning for an audit in

wages, the auditor should verify the payroll and compare the amount of wages paid to the

trial balance and the payroll systems. The number of employees on the payroll should tally

with the amount being paid by the company. The auditor should find the appointment letters

to verify the amount of salary that each employee is being paid by the company for the

services rendered. The amount should be calculated manually to ascertain if there is any case

of misappropriation13. The 23.72% increase in the amount of depreciation should be re-

evaluated and that the company should provide reasonable support to the assets depreciated.

The increase of depreciation amount from AU$53,000 in FY2015-2016 to AU$62,570 in

FY2016-2017 should be audited to substantiate the increase. The auditor should also confirm

the number of new employees employed in the latest financial period and compare with the

payroll and the appointment letters. Due to the nature of the item, I recommend that the

auditor should use verification analytical procedure to ascertain the materiality in the

difference of the amount of the company trial balance14.

Miscellaneous

Miscellaneous is another item that needs much attention because as compared with the

previous financial period, Fuchsia Enterprises did not have any miscellaneous expenses. The

AU$1,440 in the company trial balance should be accurately examined so as to determine if

the mount was used for business purposes or personal purposes. If this particular amount

were used by managers for personal business, then the amount should not be included in the

company trial balance. This item needs substantive examination to ascertain the

reasonableness of the expense15. The auditor should check the company records to check to

13 Hammersley, Jacqueline S. "A review and model of auditor judgments in fraud-related planning tasks." Auditing: A

Journal of Practice & Theory 30, no. 4 (2011): 101-128.

14 Arens, Alvin A., Randal J. Elder, and Beasley Mark. Auditing and assurance services: an integrated approach. Boston:

Prentice Hall, 2012.

15 Balaniuk, Remis, Pierre Bessiere, Emmanuel Mazer, and Paulo Cobbe. "Risk based government audit planning using

naïve bayes classifiers." In Advances in Knowledge-Based and Intelligent Information and Engineering Systems. 2012.

firm managers who may seek to misappropriate the funds. When planning for an audit in

wages, the auditor should verify the payroll and compare the amount of wages paid to the

trial balance and the payroll systems. The number of employees on the payroll should tally

with the amount being paid by the company. The auditor should find the appointment letters

to verify the amount of salary that each employee is being paid by the company for the

services rendered. The amount should be calculated manually to ascertain if there is any case

of misappropriation13. The 23.72% increase in the amount of depreciation should be re-

evaluated and that the company should provide reasonable support to the assets depreciated.

The increase of depreciation amount from AU$53,000 in FY2015-2016 to AU$62,570 in

FY2016-2017 should be audited to substantiate the increase. The auditor should also confirm

the number of new employees employed in the latest financial period and compare with the

payroll and the appointment letters. Due to the nature of the item, I recommend that the

auditor should use verification analytical procedure to ascertain the materiality in the

difference of the amount of the company trial balance14.

Miscellaneous

Miscellaneous is another item that needs much attention because as compared with the

previous financial period, Fuchsia Enterprises did not have any miscellaneous expenses. The

AU$1,440 in the company trial balance should be accurately examined so as to determine if

the mount was used for business purposes or personal purposes. If this particular amount

were used by managers for personal business, then the amount should not be included in the

company trial balance. This item needs substantive examination to ascertain the

reasonableness of the expense15. The auditor should check the company records to check to

13 Hammersley, Jacqueline S. "A review and model of auditor judgments in fraud-related planning tasks." Auditing: A

Journal of Practice & Theory 30, no. 4 (2011): 101-128.

14 Arens, Alvin A., Randal J. Elder, and Beasley Mark. Auditing and assurance services: an integrated approach. Boston:

Prentice Hall, 2012.

15 Balaniuk, Remis, Pierre Bessiere, Emmanuel Mazer, and Paulo Cobbe. "Risk based government audit planning using

naïve bayes classifiers." In Advances in Knowledge-Based and Intelligent Information and Engineering Systems. 2012.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit Testing 8

ascertain if they are in line with what is considered ordinary by the company. The auditor

should ascertain existence by reviewing the receipts documents that will basically show the

purpose of the spent amount16. I recommend that the auditor randomly chose invoices and ask

to see all the original paperwork that includes the contracts if it exists, invoices and signatures

in order to find mistakes.

16 Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Taylor & Francis, 2016.

ascertain if they are in line with what is considered ordinary by the company. The auditor

should ascertain existence by reviewing the receipts documents that will basically show the

purpose of the spent amount16. I recommend that the auditor randomly chose invoices and ask

to see all the original paperwork that includes the contracts if it exists, invoices and signatures

in order to find mistakes.

16 Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Taylor & Francis, 2016.

Audit Testing 9

Bibliography

Arens, Alvin A., Randal J. Elder, and Beasley Mark. Auditing and assurance services: an

integrated approach. Boston: Prentice Hall, 2012.

Arens, Alvin A., Randal J. Elder, Mark S. Beasley, and Chris E. Hogan. Auditing and

assurance services. Pearson, 2016.

Balaniuk, Remis, Pierre Bessiere, Emmanuel Mazer, and Paulo Cobbe. "Risk based

government audit planning using naïve bayes classifiers." In Advances in Knowledge-Based

and Intelligent Information and Engineering Systems. 2012.

Bergquist, Sophia, and Sandra Elofsson. "The collaboration between auditors and IT-

auditors: The effects on the audit profession." (2016).

Cohen, Jeffrey R., Lori L. Holder-Webb, Leda Nath, and David Wood. "Corporate reporting

of nonfinancial leading indicators of economic performance and sustainability." Accounting

Horizons26, no. 1 (2012): 65-90.

Elder, Randal J., Mark S. Beasley, and Alvin A. Arens. Auditing and Assurance services.

Pearson Higher Ed, 2011.

Hammersley, Jacqueline S. "A review and model of auditor judgments in fraud-related

planning tasks." Auditing: A Journal of Practice & Theory 30, no. 4 (2011): 101-128.

Hammersley, Jacqueline S., Karla M. Johnstone, and Kathryn Kadous. "How do audit seniors

respond to heightened fraud risk?." Auditing: A Journal of Practice & Theory 30, no. 3

(2011): 81-101.

Rahim, Siti Rohaya Mat, Fauziah Mahat, Annuar Md Nassir, and Mohamed Hisham Dato Hj

Yahya. "Re-thinking: Risk Governance?." Procedia Economics and Finance 31 (2015): 689-

698.

Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Taylor & Francis,

2016.

Bibliography

Arens, Alvin A., Randal J. Elder, and Beasley Mark. Auditing and assurance services: an

integrated approach. Boston: Prentice Hall, 2012.

Arens, Alvin A., Randal J. Elder, Mark S. Beasley, and Chris E. Hogan. Auditing and

assurance services. Pearson, 2016.

Balaniuk, Remis, Pierre Bessiere, Emmanuel Mazer, and Paulo Cobbe. "Risk based

government audit planning using naïve bayes classifiers." In Advances in Knowledge-Based

and Intelligent Information and Engineering Systems. 2012.

Bergquist, Sophia, and Sandra Elofsson. "The collaboration between auditors and IT-

auditors: The effects on the audit profession." (2016).

Cohen, Jeffrey R., Lori L. Holder-Webb, Leda Nath, and David Wood. "Corporate reporting

of nonfinancial leading indicators of economic performance and sustainability." Accounting

Horizons26, no. 1 (2012): 65-90.

Elder, Randal J., Mark S. Beasley, and Alvin A. Arens. Auditing and Assurance services.

Pearson Higher Ed, 2011.

Hammersley, Jacqueline S. "A review and model of auditor judgments in fraud-related

planning tasks." Auditing: A Journal of Practice & Theory 30, no. 4 (2011): 101-128.

Hammersley, Jacqueline S., Karla M. Johnstone, and Kathryn Kadous. "How do audit seniors

respond to heightened fraud risk?." Auditing: A Journal of Practice & Theory 30, no. 3

(2011): 81-101.

Rahim, Siti Rohaya Mat, Fauziah Mahat, Annuar Md Nassir, and Mohamed Hisham Dato Hj

Yahya. "Re-thinking: Risk Governance?." Procedia Economics and Finance 31 (2015): 689-

698.

Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Taylor & Francis,

2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit Testing

10

Messier Jr, William F., Chad A. Simon, and Jason L. Smith. "Two decades of behavioral

research on analytical procedures: What have we learned?." Auditing: A Journal of Practice

& Theory 32, no. 1 (2012): 139-181.

Titera, William R. "Updating audit standard—Enabling audit data analysis." Journal of

Information Systems 27, no. 1 (2013): 325-331.

Vona, Leonard W. Fraud risk assessment: building a fraud audit program. John Wiley &

Sons, 2012.

10

Messier Jr, William F., Chad A. Simon, and Jason L. Smith. "Two decades of behavioral

research on analytical procedures: What have we learned?." Auditing: A Journal of Practice

& Theory 32, no. 1 (2012): 139-181.

Titera, William R. "Updating audit standard—Enabling audit data analysis." Journal of

Information Systems 27, no. 1 (2013): 325-331.

Vona, Leonard W. Fraud risk assessment: building a fraud audit program. John Wiley &

Sons, 2012.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.