Cash Management and Internal Controls

VerifiedAdded on 2020/04/07

|17

|3177

|122

AI Summary

This assignment focuses on the significance of physical verification of assets and periodic reconciliation statements in managing cash resources effectively. It highlights the need for management to conduct regular physical verifications and prepare reconciliation statements to ensure control over its cash resources. The assignment also stresses the auditor's responsibility in reviewing these statements to evaluate the effectiveness of management's internal controls.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: AUDITING

Audit

Name of the Student:

Name of the University:

Authors Note:

Audit

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2AUDITING

Table of Contents

Trial Balance:...................................................................................................................................4

Income Statement:...........................................................................................................................5

Balance sheet:..................................................................................................................................5

1.0 Audit planning:..........................................................................................................................7

1.1 Analytical Review:............................................................................................................8

1.2 Preliminary judgment of materiality:................................................................................8

2.0 First account selected:................................................................................................................8

2.1 Rationale for selection:..........................................................................................................9

2.2 Assertion and explanation:....................................................................................................9

2.3 Recommended Audit procedure:...........................................................................................9

3.0 Second account selected:.........................................................................................................10

3.1 Rationale for selection:........................................................................................................10

3.2 Assertion and explanation:..................................................................................................10

3.3 Recommended audit procedure:..........................................................................................10

4.0 Third account selected:............................................................................................................10

4.1 Rationale for selection:........................................................................................................10

4.2 Assertion and explanation:..................................................................................................11

4.3 Recommended audit procedure:..........................................................................................11

Table of Contents

Trial Balance:...................................................................................................................................4

Income Statement:...........................................................................................................................5

Balance sheet:..................................................................................................................................5

1.0 Audit planning:..........................................................................................................................7

1.1 Analytical Review:............................................................................................................8

1.2 Preliminary judgment of materiality:................................................................................8

2.0 First account selected:................................................................................................................8

2.1 Rationale for selection:..........................................................................................................9

2.2 Assertion and explanation:....................................................................................................9

2.3 Recommended Audit procedure:...........................................................................................9

3.0 Second account selected:.........................................................................................................10

3.1 Rationale for selection:........................................................................................................10

3.2 Assertion and explanation:..................................................................................................10

3.3 Recommended audit procedure:..........................................................................................10

4.0 Third account selected:............................................................................................................10

4.1 Rationale for selection:........................................................................................................10

4.2 Assertion and explanation:..................................................................................................11

4.3 Recommended audit procedure:..........................................................................................11

3AUDITING

5.0 Fourth account selected:..........................................................................................................11

5.1 Rationale for selection:........................................................................................................11

5.2 Assertion and explanation:..................................................................................................11

5.3 Recommended audit procedure:..........................................................................................12

6.0 Fifth account selected:.............................................................................................................12

6.1 Rationale for selection:........................................................................................................12

6.2 Assertion and explanation:..................................................................................................12

6.3 Recommended audit procedure:..........................................................................................13

7.1 Sixth account selected:.......................................................................................................13

7.1 Rationale for selection:........................................................................................................13

7.2 Assertion and explanation:..............................................................................................13

7.3 Recommended audit procedure:......................................................................................13

8.0 Seventh account selected:........................................................................................................14

8.1 Rationale for selection:........................................................................................................14

8.2 Assertion and explanation:..................................................................................................14

8.3 Recommended audit procedure:..........................................................................................14

References:....................................................................................................................................16

5.0 Fourth account selected:..........................................................................................................11

5.1 Rationale for selection:........................................................................................................11

5.2 Assertion and explanation:..................................................................................................11

5.3 Recommended audit procedure:..........................................................................................12

6.0 Fifth account selected:.............................................................................................................12

6.1 Rationale for selection:........................................................................................................12

6.2 Assertion and explanation:..................................................................................................12

6.3 Recommended audit procedure:..........................................................................................13

7.1 Sixth account selected:.......................................................................................................13

7.1 Rationale for selection:........................................................................................................13

7.2 Assertion and explanation:..............................................................................................13

7.3 Recommended audit procedure:......................................................................................13

8.0 Seventh account selected:........................................................................................................14

8.1 Rationale for selection:........................................................................................................14

8.2 Assertion and explanation:..................................................................................................14

8.3 Recommended audit procedure:..........................................................................................14

References:....................................................................................................................................16

4AUDITING

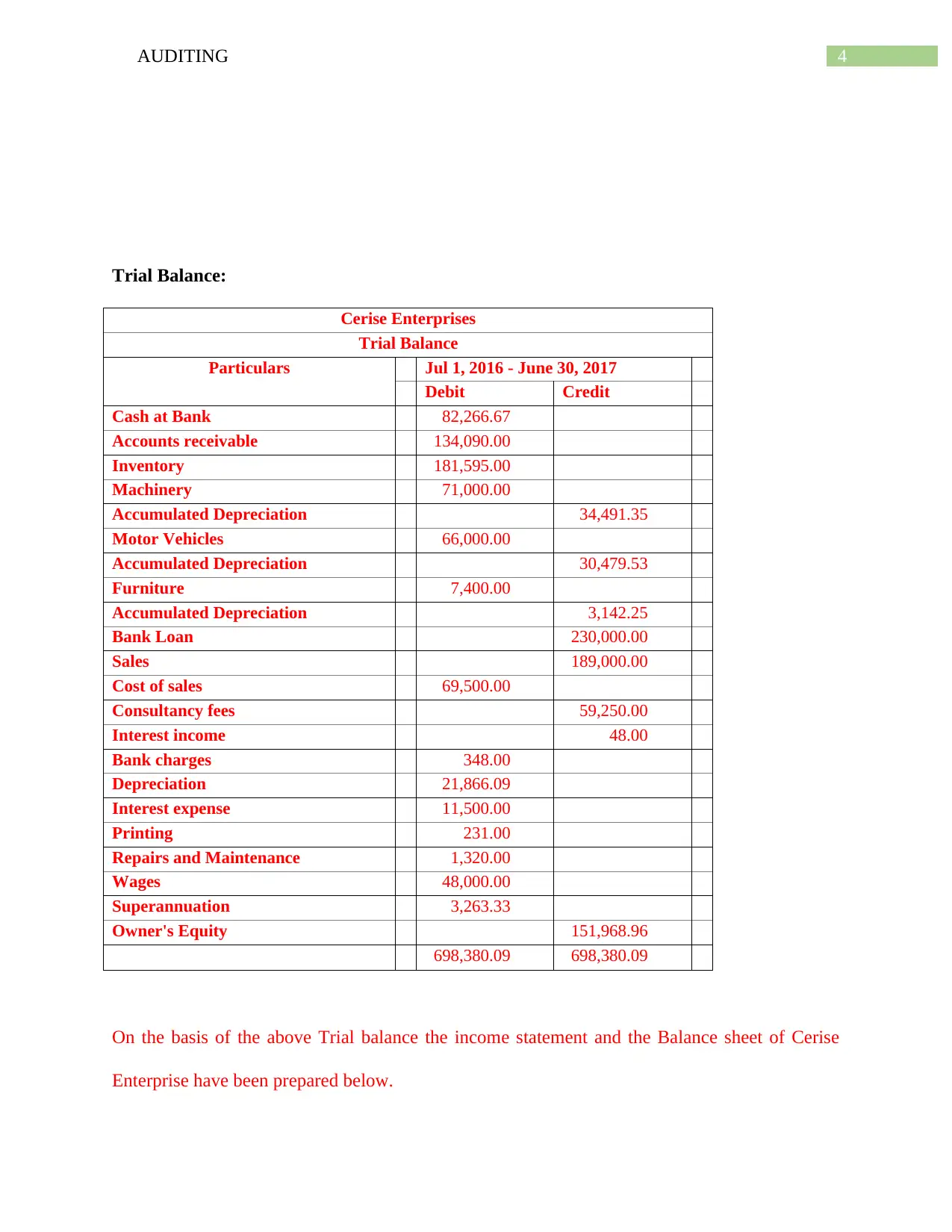

Trial Balance:

Cerise Enterprises

Trial Balance

Particulars Jul 1, 2016 - June 30, 2017

Debit Credit

Cash at Bank 82,266.67

Accounts receivable 134,090.00

Inventory 181,595.00

Machinery 71,000.00

Accumulated Depreciation 34,491.35

Motor Vehicles 66,000.00

Accumulated Depreciation 30,479.53

Furniture 7,400.00

Accumulated Depreciation 3,142.25

Bank Loan 230,000.00

Sales 189,000.00

Cost of sales 69,500.00

Consultancy fees 59,250.00

Interest income 48.00

Bank charges 348.00

Depreciation 21,866.09

Interest expense 11,500.00

Printing 231.00

Repairs and Maintenance 1,320.00

Wages 48,000.00

Superannuation 3,263.33

Owner's Equity 151,968.96

698,380.09 698,380.09

On the basis of the above Trial balance the income statement and the Balance sheet of Cerise

Enterprise have been prepared below.

Trial Balance:

Cerise Enterprises

Trial Balance

Particulars Jul 1, 2016 - June 30, 2017

Debit Credit

Cash at Bank 82,266.67

Accounts receivable 134,090.00

Inventory 181,595.00

Machinery 71,000.00

Accumulated Depreciation 34,491.35

Motor Vehicles 66,000.00

Accumulated Depreciation 30,479.53

Furniture 7,400.00

Accumulated Depreciation 3,142.25

Bank Loan 230,000.00

Sales 189,000.00

Cost of sales 69,500.00

Consultancy fees 59,250.00

Interest income 48.00

Bank charges 348.00

Depreciation 21,866.09

Interest expense 11,500.00

Printing 231.00

Repairs and Maintenance 1,320.00

Wages 48,000.00

Superannuation 3,263.33

Owner's Equity 151,968.96

698,380.09 698,380.09

On the basis of the above Trial balance the income statement and the Balance sheet of Cerise

Enterprise have been prepared below.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5AUDITING

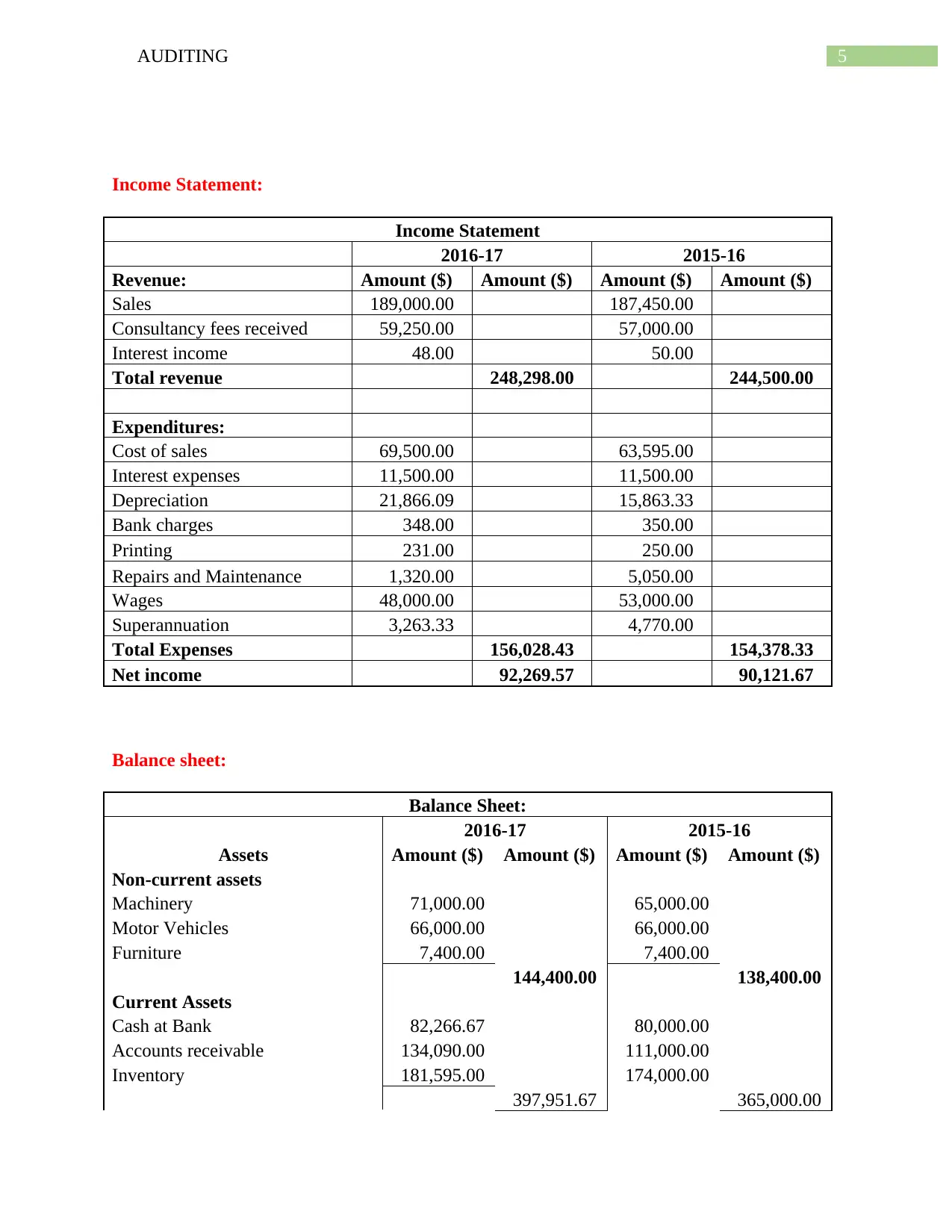

Income Statement:

Income Statement

2016-17 2015-16

Revenue: Amount ($) Amount ($) Amount ($) Amount ($)

Sales 189,000.00 187,450.00

Consultancy fees received 59,250.00 57,000.00

Interest income 48.00 50.00

Total revenue 248,298.00 244,500.00

Expenditures:

Cost of sales 69,500.00 63,595.00

Interest expenses 11,500.00 11,500.00

Depreciation 21,866.09 15,863.33

Bank charges 348.00 350.00

Printing 231.00 250.00

Repairs and Maintenance 1,320.00 5,050.00

Wages 48,000.00 53,000.00

Superannuation 3,263.33 4,770.00

Total Expenses 156,028.43 154,378.33

Net income 92,269.57 90,121.67

Balance sheet:

Balance Sheet:

Assets

2016-17 2015-16

Amount ($) Amount ($) Amount ($) Amount ($)

Non-current assets

Machinery 71,000.00 65,000.00

Motor Vehicles 66,000.00 66,000.00

Furniture 7,400.00 7,400.00

144,400.00 138,400.00

Current Assets

Cash at Bank 82,266.67 80,000.00

Accounts receivable 134,090.00 111,000.00

Inventory 181,595.00 174,000.00

397,951.67 365,000.00

Income Statement:

Income Statement

2016-17 2015-16

Revenue: Amount ($) Amount ($) Amount ($) Amount ($)

Sales 189,000.00 187,450.00

Consultancy fees received 59,250.00 57,000.00

Interest income 48.00 50.00

Total revenue 248,298.00 244,500.00

Expenditures:

Cost of sales 69,500.00 63,595.00

Interest expenses 11,500.00 11,500.00

Depreciation 21,866.09 15,863.33

Bank charges 348.00 350.00

Printing 231.00 250.00

Repairs and Maintenance 1,320.00 5,050.00

Wages 48,000.00 53,000.00

Superannuation 3,263.33 4,770.00

Total Expenses 156,028.43 154,378.33

Net income 92,269.57 90,121.67

Balance sheet:

Balance Sheet:

Assets

2016-17 2015-16

Amount ($) Amount ($) Amount ($) Amount ($)

Non-current assets

Machinery 71,000.00 65,000.00

Motor Vehicles 66,000.00 66,000.00

Furniture 7,400.00 7,400.00

144,400.00 138,400.00

Current Assets

Cash at Bank 82,266.67 80,000.00

Accounts receivable 134,090.00 111,000.00

Inventory 181,595.00 174,000.00

397,951.67 365,000.00

6AUDITING

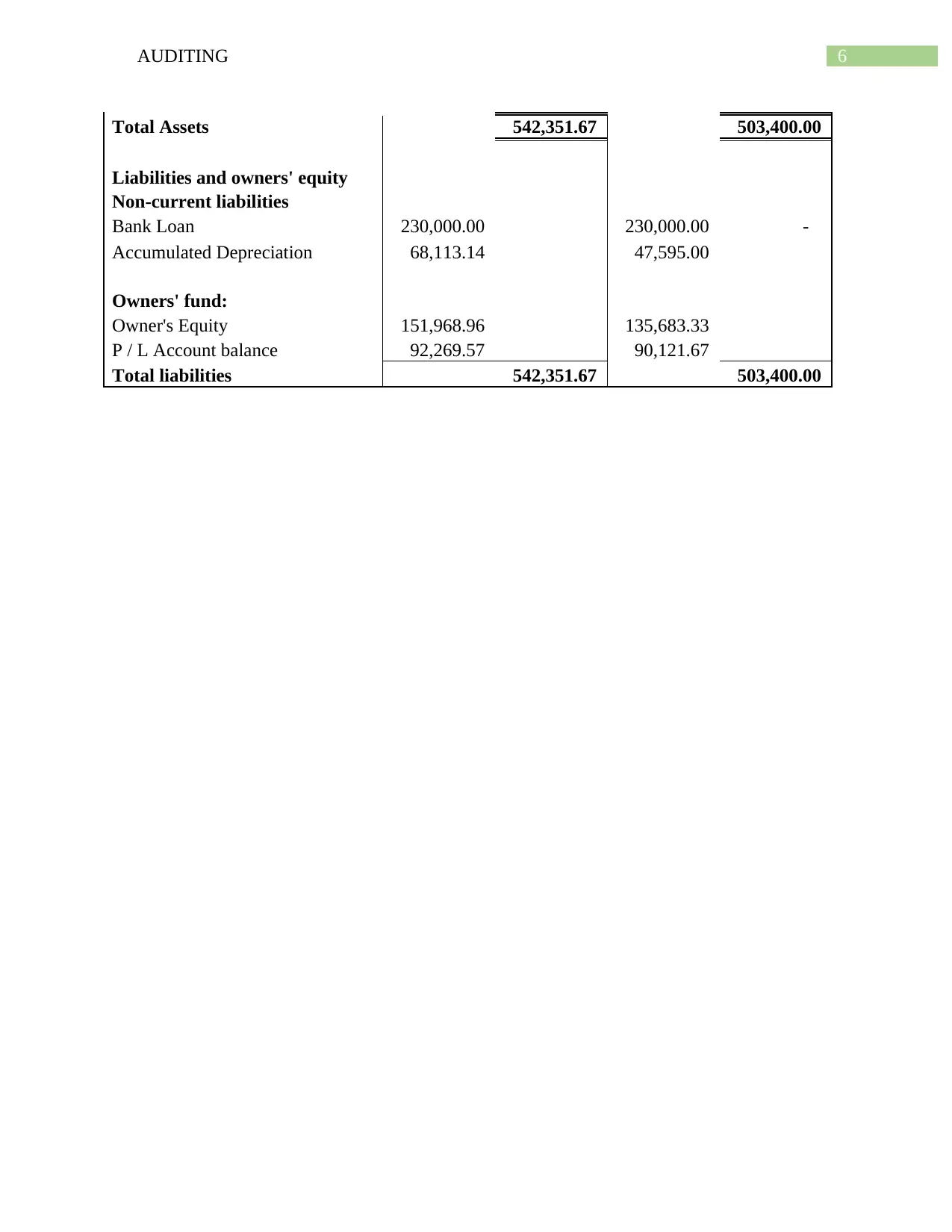

Total Assets 542,351.67 503,400.00

Liabilities and owners' equity

Non-current liabilities

Bank Loan 230,000.00 230,000.00 -

Accumulated Depreciation 68,113.14 47,595.00

Owners' fund:

Owner's Equity 151,968.96 135,683.33

P / L Account balance 92,269.57 90,121.67

Total liabilities 542,351.67 503,400.00

Total Assets 542,351.67 503,400.00

Liabilities and owners' equity

Non-current liabilities

Bank Loan 230,000.00 230,000.00 -

Accumulated Depreciation 68,113.14 47,595.00

Owners' fund:

Owner's Equity 151,968.96 135,683.33

P / L Account balance 92,269.57 90,121.67

Total liabilities 542,351.67 503,400.00

7AUDITING

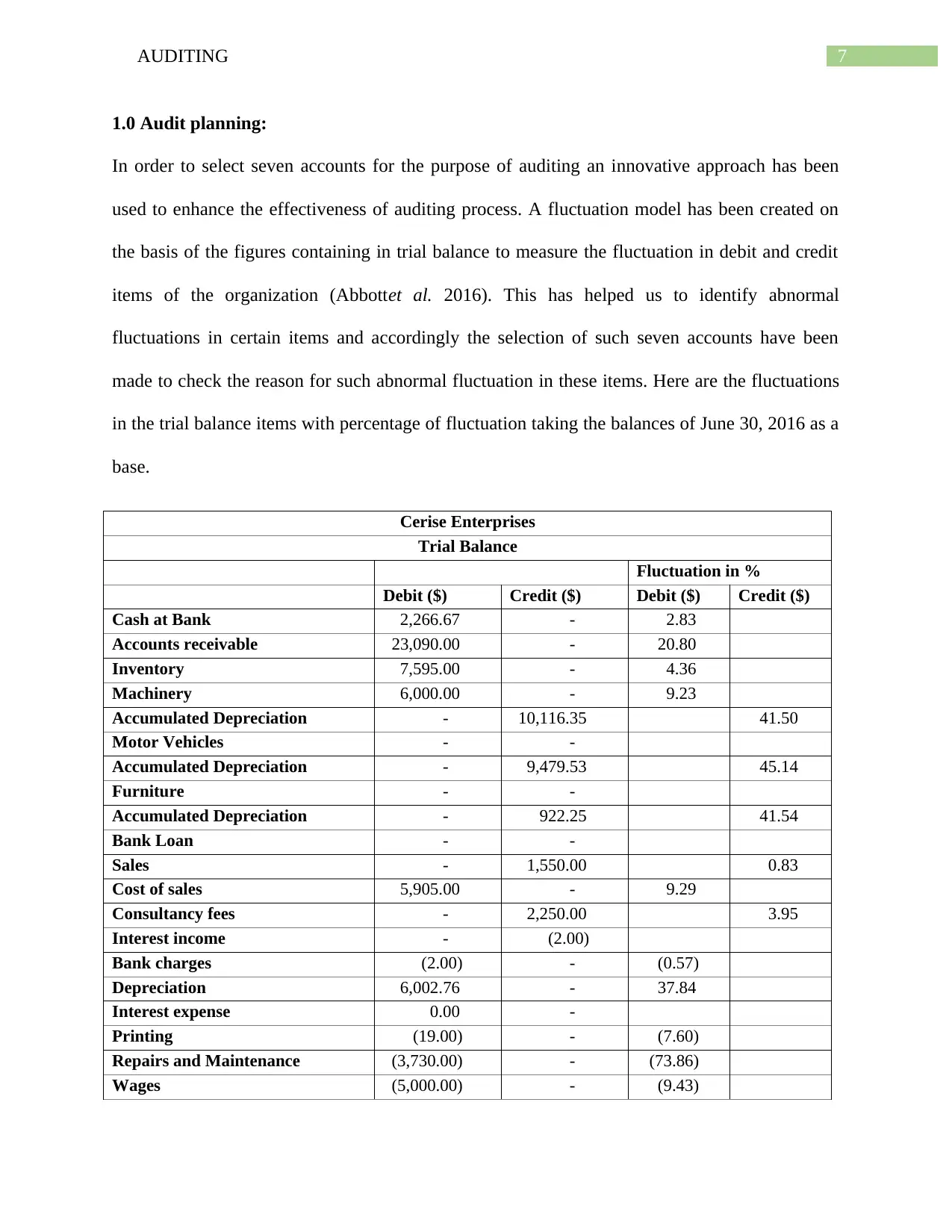

1.0 Audit planning:

In order to select seven accounts for the purpose of auditing an innovative approach has been

used to enhance the effectiveness of auditing process. A fluctuation model has been created on

the basis of the figures containing in trial balance to measure the fluctuation in debit and credit

items of the organization (Abbottet al. 2016). This has helped us to identify abnormal

fluctuations in certain items and accordingly the selection of such seven accounts have been

made to check the reason for such abnormal fluctuation in these items. Here are the fluctuations

in the trial balance items with percentage of fluctuation taking the balances of June 30, 2016 as a

base.

Cerise Enterprises

Trial Balance

Fluctuation in %

Debit ($) Credit ($) Debit ($) Credit ($)

Cash at Bank 2,266.67 - 2.83

Accounts receivable 23,090.00 - 20.80

Inventory 7,595.00 - 4.36

Machinery 6,000.00 - 9.23

Accumulated Depreciation - 10,116.35 41.50

Motor Vehicles - -

Accumulated Depreciation - 9,479.53 45.14

Furniture - -

Accumulated Depreciation - 922.25 41.54

Bank Loan - -

Sales - 1,550.00 0.83

Cost of sales 5,905.00 - 9.29

Consultancy fees - 2,250.00 3.95

Interest income - (2.00)

Bank charges (2.00) - (0.57)

Depreciation 6,002.76 - 37.84

Interest expense 0.00 -

Printing (19.00) - (7.60)

Repairs and Maintenance (3,730.00) - (73.86)

Wages (5,000.00) - (9.43)

1.0 Audit planning:

In order to select seven accounts for the purpose of auditing an innovative approach has been

used to enhance the effectiveness of auditing process. A fluctuation model has been created on

the basis of the figures containing in trial balance to measure the fluctuation in debit and credit

items of the organization (Abbottet al. 2016). This has helped us to identify abnormal

fluctuations in certain items and accordingly the selection of such seven accounts have been

made to check the reason for such abnormal fluctuation in these items. Here are the fluctuations

in the trial balance items with percentage of fluctuation taking the balances of June 30, 2016 as a

base.

Cerise Enterprises

Trial Balance

Fluctuation in %

Debit ($) Credit ($) Debit ($) Credit ($)

Cash at Bank 2,266.67 - 2.83

Accounts receivable 23,090.00 - 20.80

Inventory 7,595.00 - 4.36

Machinery 6,000.00 - 9.23

Accumulated Depreciation - 10,116.35 41.50

Motor Vehicles - -

Accumulated Depreciation - 9,479.53 45.14

Furniture - -

Accumulated Depreciation - 922.25 41.54

Bank Loan - -

Sales - 1,550.00 0.83

Cost of sales 5,905.00 - 9.29

Consultancy fees - 2,250.00 3.95

Interest income - (2.00)

Bank charges (2.00) - (0.57)

Depreciation 6,002.76 - 37.84

Interest expense 0.00 -

Printing (19.00) - (7.60)

Repairs and Maintenance (3,730.00) - (73.86)

Wages (5,000.00) - (9.43)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDITING

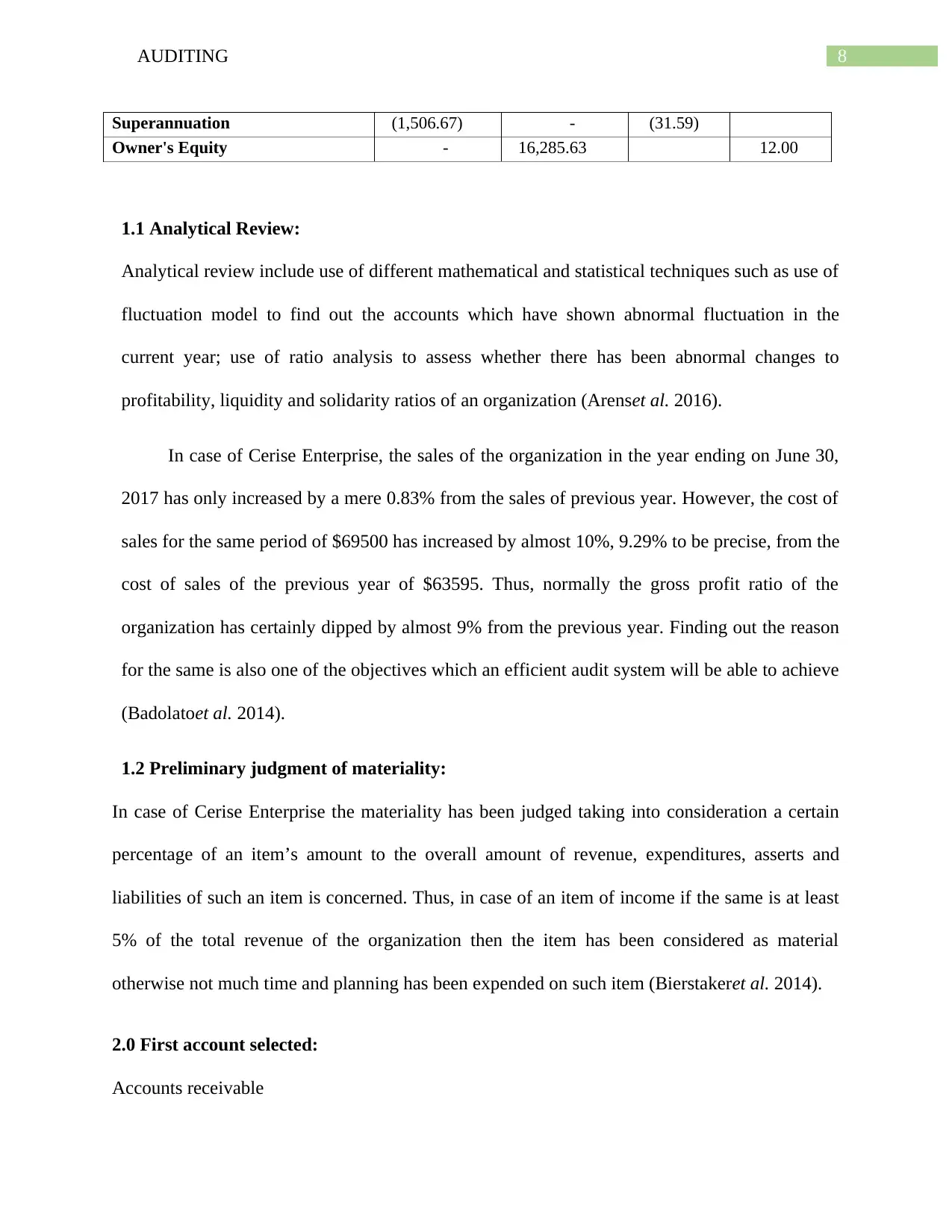

Superannuation (1,506.67) - (31.59)

Owner's Equity - 16,285.63 12.00

1.1 Analytical Review:

Analytical review include use of different mathematical and statistical techniques such as use of

fluctuation model to find out the accounts which have shown abnormal fluctuation in the

current year; use of ratio analysis to assess whether there has been abnormal changes to

profitability, liquidity and solidarity ratios of an organization (Arenset al. 2016).

In case of Cerise Enterprise, the sales of the organization in the year ending on June 30,

2017 has only increased by a mere 0.83% from the sales of previous year. However, the cost of

sales for the same period of $69500 has increased by almost 10%, 9.29% to be precise, from the

cost of sales of the previous year of $63595. Thus, normally the gross profit ratio of the

organization has certainly dipped by almost 9% from the previous year. Finding out the reason

for the same is also one of the objectives which an efficient audit system will be able to achieve

(Badolatoet al. 2014).

1.2 Preliminary judgment of materiality:

In case of Cerise Enterprise the materiality has been judged taking into consideration a certain

percentage of an item’s amount to the overall amount of revenue, expenditures, asserts and

liabilities of such an item is concerned. Thus, in case of an item of income if the same is at least

5% of the total revenue of the organization then the item has been considered as material

otherwise not much time and planning has been expended on such item (Bierstakeret al. 2014).

2.0 First account selected:

Accounts receivable

Superannuation (1,506.67) - (31.59)

Owner's Equity - 16,285.63 12.00

1.1 Analytical Review:

Analytical review include use of different mathematical and statistical techniques such as use of

fluctuation model to find out the accounts which have shown abnormal fluctuation in the

current year; use of ratio analysis to assess whether there has been abnormal changes to

profitability, liquidity and solidarity ratios of an organization (Arenset al. 2016).

In case of Cerise Enterprise, the sales of the organization in the year ending on June 30,

2017 has only increased by a mere 0.83% from the sales of previous year. However, the cost of

sales for the same period of $69500 has increased by almost 10%, 9.29% to be precise, from the

cost of sales of the previous year of $63595. Thus, normally the gross profit ratio of the

organization has certainly dipped by almost 9% from the previous year. Finding out the reason

for the same is also one of the objectives which an efficient audit system will be able to achieve

(Badolatoet al. 2014).

1.2 Preliminary judgment of materiality:

In case of Cerise Enterprise the materiality has been judged taking into consideration a certain

percentage of an item’s amount to the overall amount of revenue, expenditures, asserts and

liabilities of such an item is concerned. Thus, in case of an item of income if the same is at least

5% of the total revenue of the organization then the item has been considered as material

otherwise not much time and planning has been expended on such item (Bierstakeret al. 2014).

2.0 First account selected:

Accounts receivable

9AUDITING

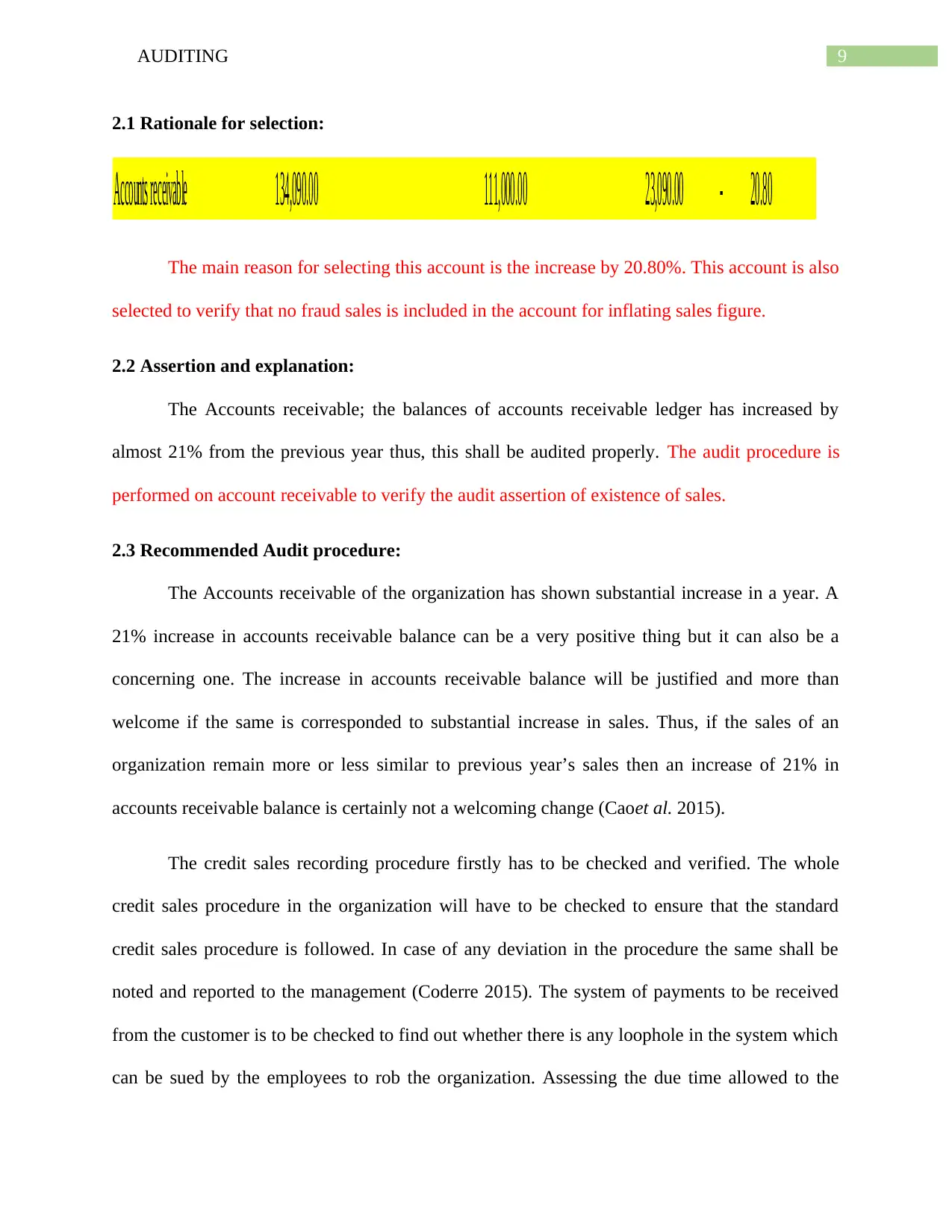

2.1 Rationale for selection:

Accounts receivable 134,090.00 111,000.00 23,090.00 - 20.80

The main reason for selecting this account is the increase by 20.80%. This account is also

selected to verify that no fraud sales is included in the account for inflating sales figure.

2.2 Assertion and explanation:

The Accounts receivable; the balances of accounts receivable ledger has increased by

almost 21% from the previous year thus, this shall be audited properly. The audit procedure is

performed on account receivable to verify the audit assertion of existence of sales.

2.3 Recommended Audit procedure:

The Accounts receivable of the organization has shown substantial increase in a year. A

21% increase in accounts receivable balance can be a very positive thing but it can also be a

concerning one. The increase in accounts receivable balance will be justified and more than

welcome if the same is corresponded to substantial increase in sales. Thus, if the sales of an

organization remain more or less similar to previous year’s sales then an increase of 21% in

accounts receivable balance is certainly not a welcoming change (Caoet al. 2015).

The credit sales recording procedure firstly has to be checked and verified. The whole

credit sales procedure in the organization will have to be checked to ensure that the standard

credit sales procedure is followed. In case of any deviation in the procedure the same shall be

noted and reported to the management (Coderre 2015). The system of payments to be received

from the customer is to be checked to find out whether there is any loophole in the system which

can be sued by the employees to rob the organization. Assessing the due time allowed to the

2.1 Rationale for selection:

Accounts receivable 134,090.00 111,000.00 23,090.00 - 20.80

The main reason for selecting this account is the increase by 20.80%. This account is also

selected to verify that no fraud sales is included in the account for inflating sales figure.

2.2 Assertion and explanation:

The Accounts receivable; the balances of accounts receivable ledger has increased by

almost 21% from the previous year thus, this shall be audited properly. The audit procedure is

performed on account receivable to verify the audit assertion of existence of sales.

2.3 Recommended Audit procedure:

The Accounts receivable of the organization has shown substantial increase in a year. A

21% increase in accounts receivable balance can be a very positive thing but it can also be a

concerning one. The increase in accounts receivable balance will be justified and more than

welcome if the same is corresponded to substantial increase in sales. Thus, if the sales of an

organization remain more or less similar to previous year’s sales then an increase of 21% in

accounts receivable balance is certainly not a welcoming change (Caoet al. 2015).

The credit sales recording procedure firstly has to be checked and verified. The whole

credit sales procedure in the organization will have to be checked to ensure that the standard

credit sales procedure is followed. In case of any deviation in the procedure the same shall be

noted and reported to the management (Coderre 2015). The system of payments to be received

from the customer is to be checked to find out whether there is any loophole in the system which

can be sued by the employees to rob the organization. Assessing the due time allowed to the

10AUDITING

customers and whether the management is able to collect the dues within such time are also to be

checked and reported accordingly.

3.0 Second account selected:

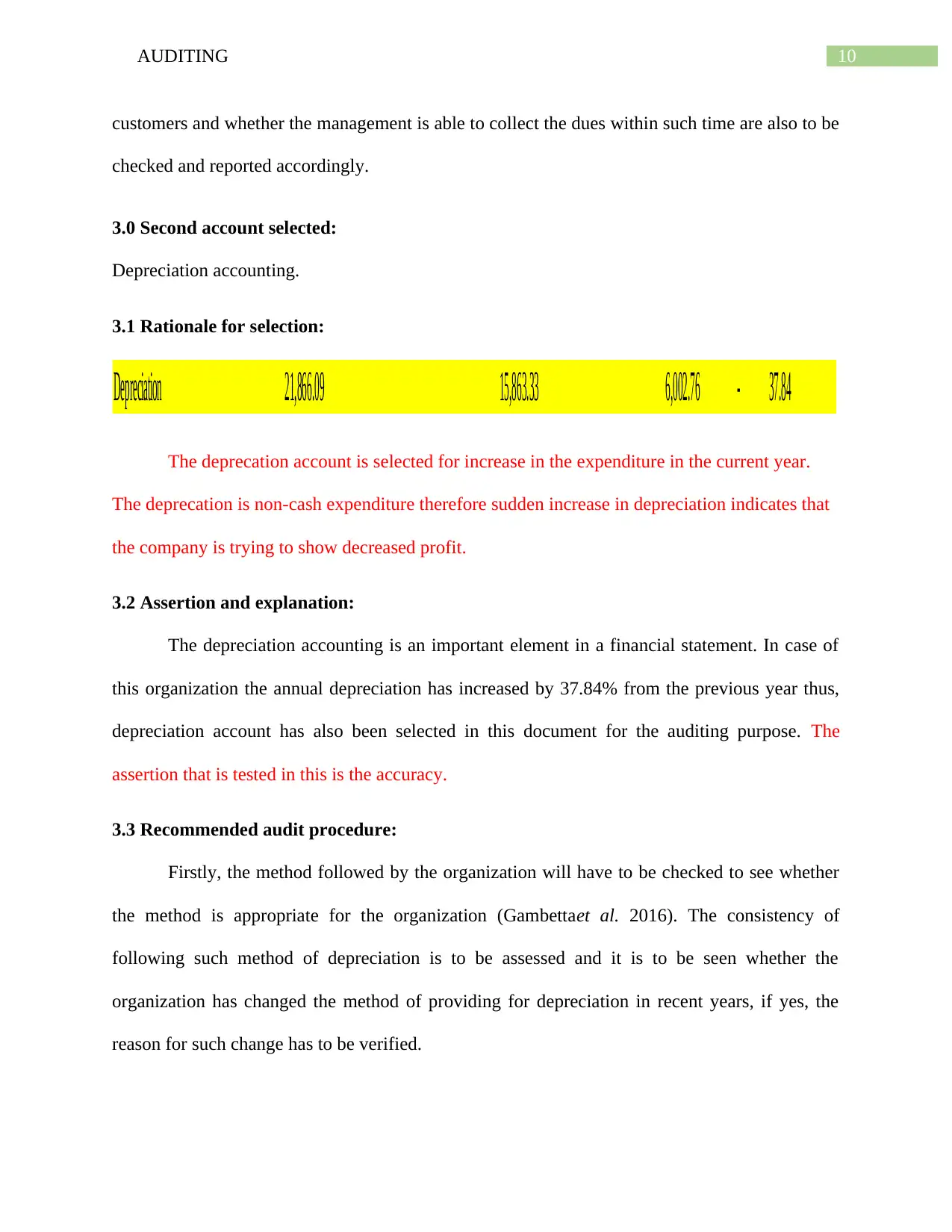

Depreciation accounting.

3.1 Rationale for selection:

Depreciation 21,866.09 15,863.33 6,002.76 - 37.84

The deprecation account is selected for increase in the expenditure in the current year.

The deprecation is non-cash expenditure therefore sudden increase in depreciation indicates that

the company is trying to show decreased profit.

3.2 Assertion and explanation:

The depreciation accounting is an important element in a financial statement. In case of

this organization the annual depreciation has increased by 37.84% from the previous year thus,

depreciation account has also been selected in this document for the auditing purpose. The

assertion that is tested in this is the accuracy.

3.3 Recommended audit procedure:

Firstly, the method followed by the organization will have to be checked to see whether

the method is appropriate for the organization (Gambettaet al. 2016). The consistency of

following such method of depreciation is to be assessed and it is to be seen whether the

organization has changed the method of providing for depreciation in recent years, if yes, the

reason for such change has to be verified.

customers and whether the management is able to collect the dues within such time are also to be

checked and reported accordingly.

3.0 Second account selected:

Depreciation accounting.

3.1 Rationale for selection:

Depreciation 21,866.09 15,863.33 6,002.76 - 37.84

The deprecation account is selected for increase in the expenditure in the current year.

The deprecation is non-cash expenditure therefore sudden increase in depreciation indicates that

the company is trying to show decreased profit.

3.2 Assertion and explanation:

The depreciation accounting is an important element in a financial statement. In case of

this organization the annual depreciation has increased by 37.84% from the previous year thus,

depreciation account has also been selected in this document for the auditing purpose. The

assertion that is tested in this is the accuracy.

3.3 Recommended audit procedure:

Firstly, the method followed by the organization will have to be checked to see whether

the method is appropriate for the organization (Gambettaet al. 2016). The consistency of

following such method of depreciation is to be assessed and it is to be seen whether the

organization has changed the method of providing for depreciation in recent years, if yes, the

reason for such change has to be verified.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11AUDITING

4.0 Third account selected:

Repair and maintenance account.

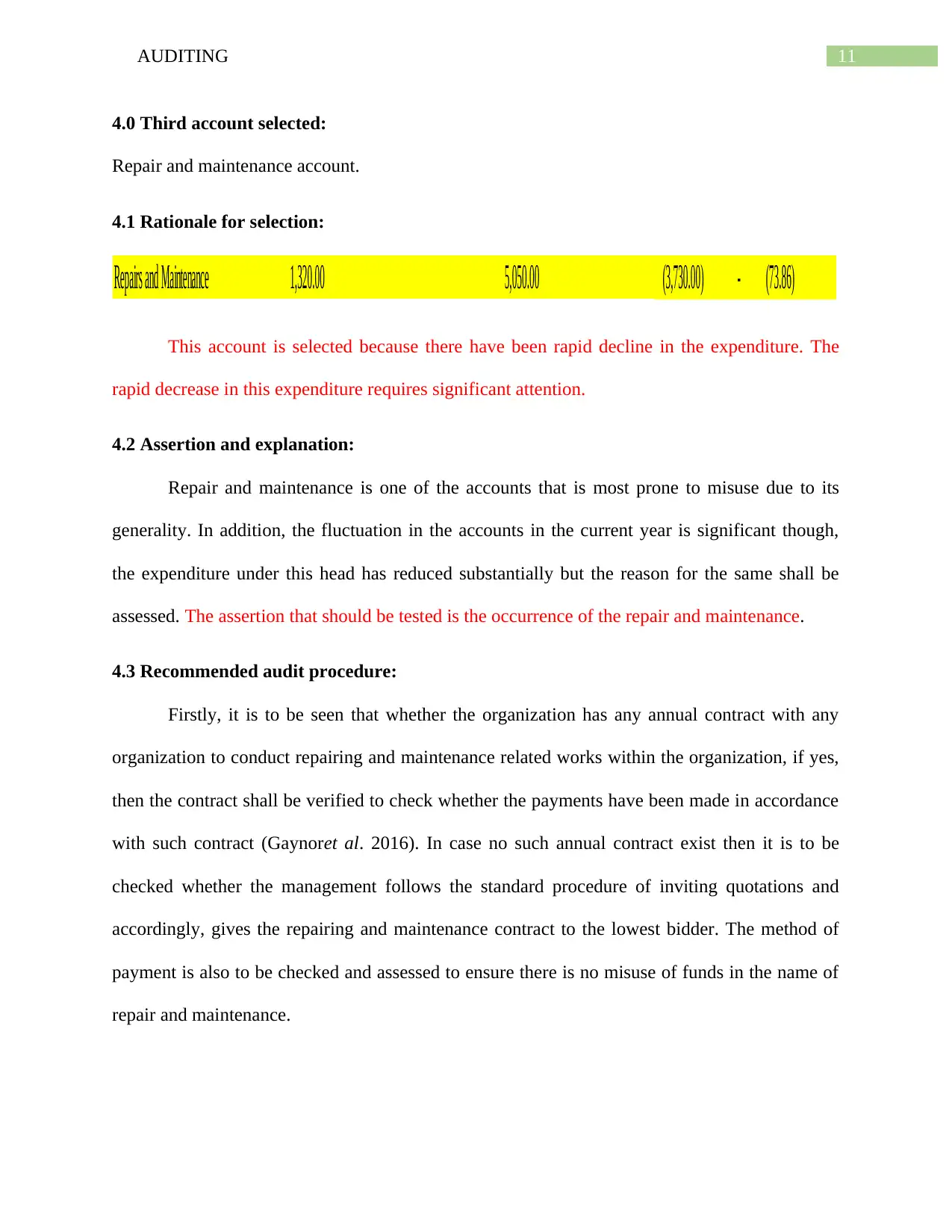

4.1 Rationale for selection:

Repairs and Maintenance 1,320.00 5,050.00 (3,730.00) - (73.86)

This account is selected because there have been rapid decline in the expenditure. The

rapid decrease in this expenditure requires significant attention.

4.2 Assertion and explanation:

Repair and maintenance is one of the accounts that is most prone to misuse due to its

generality. In addition, the fluctuation in the accounts in the current year is significant though,

the expenditure under this head has reduced substantially but the reason for the same shall be

assessed. The assertion that should be tested is the occurrence of the repair and maintenance.

4.3 Recommended audit procedure:

Firstly, it is to be seen that whether the organization has any annual contract with any

organization to conduct repairing and maintenance related works within the organization, if yes,

then the contract shall be verified to check whether the payments have been made in accordance

with such contract (Gaynoret al. 2016). In case no such annual contract exist then it is to be

checked whether the management follows the standard procedure of inviting quotations and

accordingly, gives the repairing and maintenance contract to the lowest bidder. The method of

payment is also to be checked and assessed to ensure there is no misuse of funds in the name of

repair and maintenance.

4.0 Third account selected:

Repair and maintenance account.

4.1 Rationale for selection:

Repairs and Maintenance 1,320.00 5,050.00 (3,730.00) - (73.86)

This account is selected because there have been rapid decline in the expenditure. The

rapid decrease in this expenditure requires significant attention.

4.2 Assertion and explanation:

Repair and maintenance is one of the accounts that is most prone to misuse due to its

generality. In addition, the fluctuation in the accounts in the current year is significant though,

the expenditure under this head has reduced substantially but the reason for the same shall be

assessed. The assertion that should be tested is the occurrence of the repair and maintenance.

4.3 Recommended audit procedure:

Firstly, it is to be seen that whether the organization has any annual contract with any

organization to conduct repairing and maintenance related works within the organization, if yes,

then the contract shall be verified to check whether the payments have been made in accordance

with such contract (Gaynoret al. 2016). In case no such annual contract exist then it is to be

checked whether the management follows the standard procedure of inviting quotations and

accordingly, gives the repairing and maintenance contract to the lowest bidder. The method of

payment is also to be checked and assessed to ensure there is no misuse of funds in the name of

repair and maintenance.

12AUDITING

5.0 Fourth account selected:

Inventory has been selected for its sheer importance to the smooth functioning of the

organization.

5.1 Rationale for selection:

Inventory 181,595.00 174,000.00 7,595.00 - 4.36

The account is selected because inventory has increased by 4.36%. It is an important

account and has impact on the profit.

5.2 Assertion and explanation:

Inventory is the most important resources required by an organization to run its

operations and functions. Considering its huge important it is of utmost importance for the

organization to manage the inventory efficiently hence, it has been selected for auditing purpose

to assess the control of the management on inventory. The assertion that should be checked in

the inventory is the completeness of the recording of the transaction related to inventory.

5.3 Recommended audit procedure:

As an auditor,it would essential to know the system that is in place and used by the

management to manage the inventory of the organization. FIFO, LIFO, average cost are few of

the most used methods followed by management around the globe for inventory control. The

auditor will have to check whether the management follows the appropriate method to manage

inventory and the same method has been followed throughout the year or not (Karimet al. 2017).

6.0 Fifth account selected:

Fixed assets such as machinery, motor vehicles and furniture.

5.0 Fourth account selected:

Inventory has been selected for its sheer importance to the smooth functioning of the

organization.

5.1 Rationale for selection:

Inventory 181,595.00 174,000.00 7,595.00 - 4.36

The account is selected because inventory has increased by 4.36%. It is an important

account and has impact on the profit.

5.2 Assertion and explanation:

Inventory is the most important resources required by an organization to run its

operations and functions. Considering its huge important it is of utmost importance for the

organization to manage the inventory efficiently hence, it has been selected for auditing purpose

to assess the control of the management on inventory. The assertion that should be checked in

the inventory is the completeness of the recording of the transaction related to inventory.

5.3 Recommended audit procedure:

As an auditor,it would essential to know the system that is in place and used by the

management to manage the inventory of the organization. FIFO, LIFO, average cost are few of

the most used methods followed by management around the globe for inventory control. The

auditor will have to check whether the management follows the appropriate method to manage

inventory and the same method has been followed throughout the year or not (Karimet al. 2017).

6.0 Fifth account selected:

Fixed assets such as machinery, motor vehicles and furniture.

13AUDITING

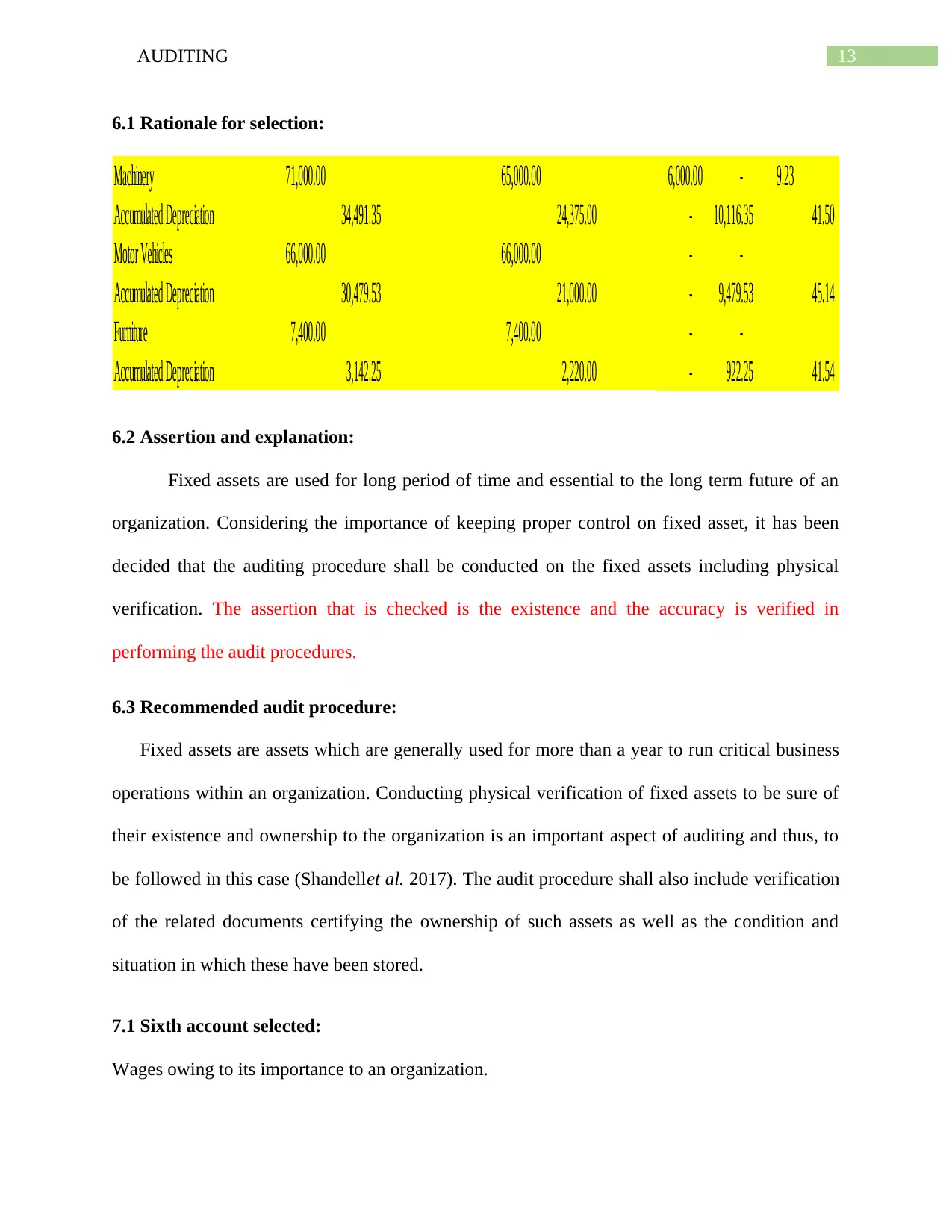

6.1 Rationale for selection:

Machinery 71,000.00 65,000.00 6,000.00 - 9.23

Accumulated Depreciation 34,491.35 24,375.00 - 10,116.35 41.50

Motor Vehicles 66,000.00 66,000.00 - -

Accumulated Depreciation 30,479.53 21,000.00 - 9,479.53 45.14

Furniture 7,400.00 7,400.00 - -

Accumulated Depreciation 3,142.25 2,220.00 - 922.25 41.54

6.2 Assertion and explanation:

Fixed assets are used for long period of time and essential to the long term future of an

organization. Considering the importance of keeping proper control on fixed asset, it has been

decided that the auditing procedure shall be conducted on the fixed assets including physical

verification. The assertion that is checked is the existence and the accuracy is verified in

performing the audit procedures.

6.3 Recommended audit procedure:

Fixed assets are assets which are generally used for more than a year to run critical business

operations within an organization. Conducting physical verification of fixed assets to be sure of

their existence and ownership to the organization is an important aspect of auditing and thus, to

be followed in this case (Shandellet al. 2017). The audit procedure shall also include verification

of the related documents certifying the ownership of such assets as well as the condition and

situation in which these have been stored.

7.1 Sixth account selected:

Wages owing to its importance to an organization.

6.1 Rationale for selection:

Machinery 71,000.00 65,000.00 6,000.00 - 9.23

Accumulated Depreciation 34,491.35 24,375.00 - 10,116.35 41.50

Motor Vehicles 66,000.00 66,000.00 - -

Accumulated Depreciation 30,479.53 21,000.00 - 9,479.53 45.14

Furniture 7,400.00 7,400.00 - -

Accumulated Depreciation 3,142.25 2,220.00 - 922.25 41.54

6.2 Assertion and explanation:

Fixed assets are used for long period of time and essential to the long term future of an

organization. Considering the importance of keeping proper control on fixed asset, it has been

decided that the auditing procedure shall be conducted on the fixed assets including physical

verification. The assertion that is checked is the existence and the accuracy is verified in

performing the audit procedures.

6.3 Recommended audit procedure:

Fixed assets are assets which are generally used for more than a year to run critical business

operations within an organization. Conducting physical verification of fixed assets to be sure of

their existence and ownership to the organization is an important aspect of auditing and thus, to

be followed in this case (Shandellet al. 2017). The audit procedure shall also include verification

of the related documents certifying the ownership of such assets as well as the condition and

situation in which these have been stored.

7.1 Sixth account selected:

Wages owing to its importance to an organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14AUDITING

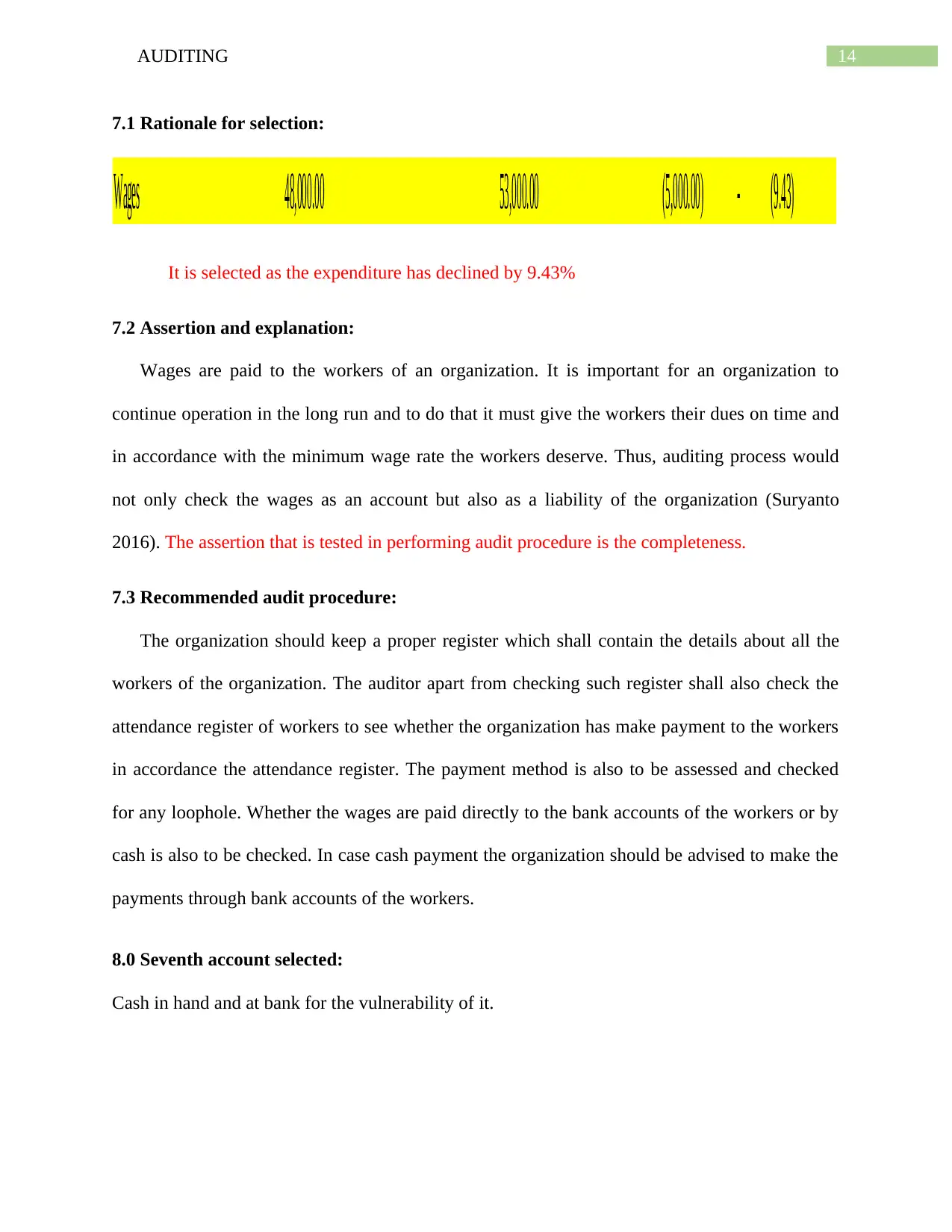

7.1 Rationale for selection:

Wages 48,000.00 53,000.00 (5,000.00) - (9.43)

It is selected as the expenditure has declined by 9.43%

7.2 Assertion and explanation:

Wages are paid to the workers of an organization. It is important for an organization to

continue operation in the long run and to do that it must give the workers their dues on time and

in accordance with the minimum wage rate the workers deserve. Thus, auditing process would

not only check the wages as an account but also as a liability of the organization (Suryanto

2016). The assertion that is tested in performing audit procedure is the completeness.

7.3 Recommended audit procedure:

The organization should keep a proper register which shall contain the details about all the

workers of the organization. The auditor apart from checking such register shall also check the

attendance register of workers to see whether the organization has make payment to the workers

in accordance the attendance register. The payment method is also to be assessed and checked

for any loophole. Whether the wages are paid directly to the bank accounts of the workers or by

cash is also to be checked. In case cash payment the organization should be advised to make the

payments through bank accounts of the workers.

8.0 Seventh account selected:

Cash in hand and at bank for the vulnerability of it.

7.1 Rationale for selection:

Wages 48,000.00 53,000.00 (5,000.00) - (9.43)

It is selected as the expenditure has declined by 9.43%

7.2 Assertion and explanation:

Wages are paid to the workers of an organization. It is important for an organization to

continue operation in the long run and to do that it must give the workers their dues on time and

in accordance with the minimum wage rate the workers deserve. Thus, auditing process would

not only check the wages as an account but also as a liability of the organization (Suryanto

2016). The assertion that is tested in performing audit procedure is the completeness.

7.3 Recommended audit procedure:

The organization should keep a proper register which shall contain the details about all the

workers of the organization. The auditor apart from checking such register shall also check the

attendance register of workers to see whether the organization has make payment to the workers

in accordance the attendance register. The payment method is also to be assessed and checked

for any loophole. Whether the wages are paid directly to the bank accounts of the workers or by

cash is also to be checked. In case cash payment the organization should be advised to make the

payments through bank accounts of the workers.

8.0 Seventh account selected:

Cash in hand and at bank for the vulnerability of it.

15AUDITING

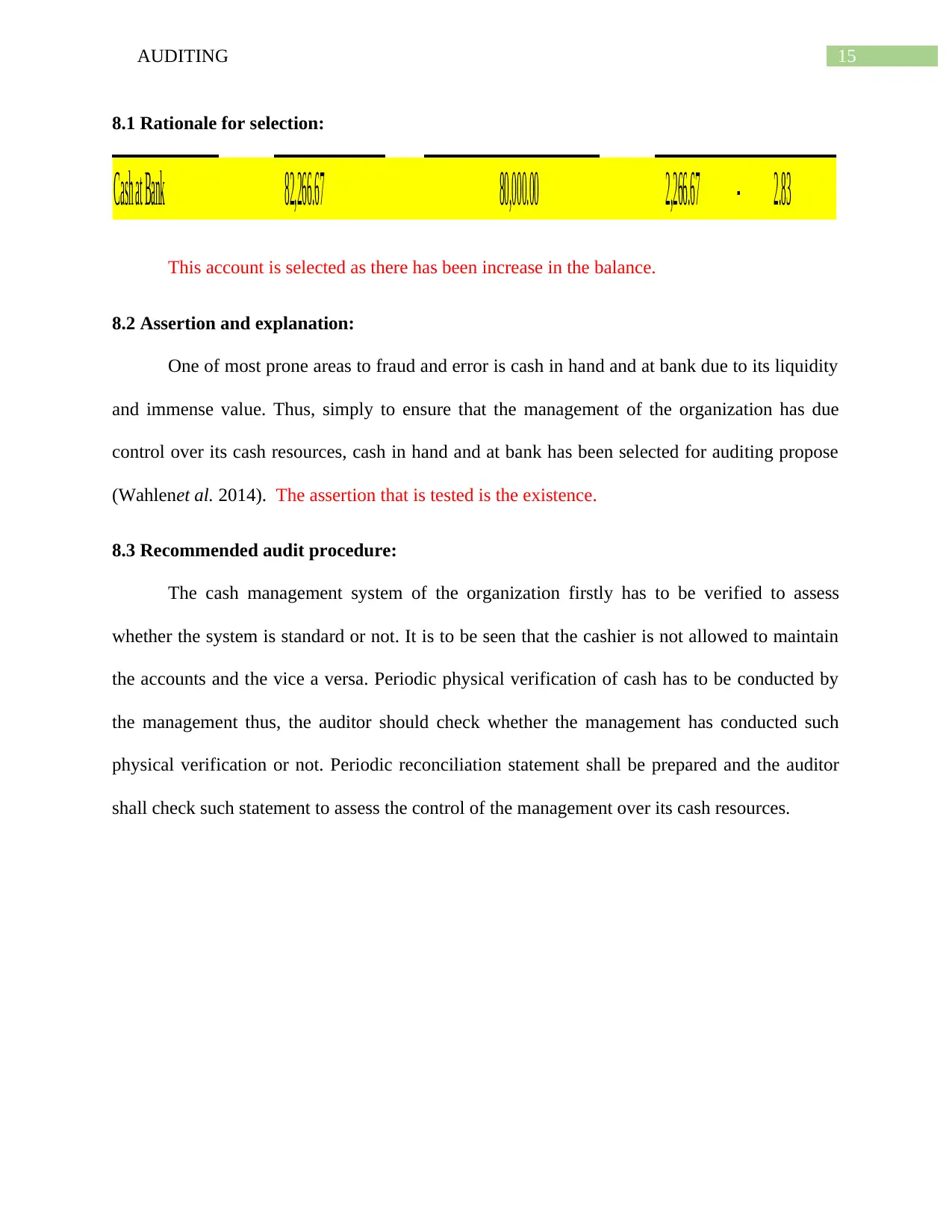

8.1 Rationale for selection:

Cash at Bank 82,266.67 80,000.00 2,266.67 - 2.83

This account is selected as there has been increase in the balance.

8.2 Assertion and explanation:

One of most prone areas to fraud and error is cash in hand and at bank due to its liquidity

and immense value. Thus, simply to ensure that the management of the organization has due

control over its cash resources, cash in hand and at bank has been selected for auditing propose

(Wahlenet al. 2014). The assertion that is tested is the existence.

8.3 Recommended audit procedure:

The cash management system of the organization firstly has to be verified to assess

whether the system is standard or not. It is to be seen that the cashier is not allowed to maintain

the accounts and the vice a versa. Periodic physical verification of cash has to be conducted by

the management thus, the auditor should check whether the management has conducted such

physical verification or not. Periodic reconciliation statement shall be prepared and the auditor

shall check such statement to assess the control of the management over its cash resources.

8.1 Rationale for selection:

Cash at Bank 82,266.67 80,000.00 2,266.67 - 2.83

This account is selected as there has been increase in the balance.

8.2 Assertion and explanation:

One of most prone areas to fraud and error is cash in hand and at bank due to its liquidity

and immense value. Thus, simply to ensure that the management of the organization has due

control over its cash resources, cash in hand and at bank has been selected for auditing propose

(Wahlenet al. 2014). The assertion that is tested is the existence.

8.3 Recommended audit procedure:

The cash management system of the organization firstly has to be verified to assess

whether the system is standard or not. It is to be seen that the cashier is not allowed to maintain

the accounts and the vice a versa. Periodic physical verification of cash has to be conducted by

the management thus, the auditor should check whether the management has conducted such

physical verification or not. Periodic reconciliation statement shall be prepared and the auditor

shall check such statement to assess the control of the management over its cash resources.

16AUDITING

References:

Abbott, L.J., Daugherty, B., Parker, S. and Peters, G.F., 2016. Internal audit quality and financial

reporting quality: The joint importance of independence and competence. Journal of Accounting

Research, 54(1), pp.3-40.

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance services.

Pearson.

Badolato, P.G., Donelson, D.C. and Ege, M., 2014. Audit committee financial expertise and

earnings management: The role of status. Journal of Accounting and Economics, 58(2), pp.208-

230.

Bierstaker, J., Janvrin, D. and Lowe, D.J., 2014. What factors influence auditors' use of

computer-assisted audit techniques?. Advances in Accounting, 30(1), pp.67-74.

Cao, M., Chychyla, R. and Stewart, T., 2015. Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), pp.423-429.

Coderre, D., 2015. Gauge your analytics: by addressing people, processes, and technology,

internal audit can ensure a successful data analytics initiative. Internal Auditor, 72(4), pp.41-46.

Gambetta, N., García-Benau, M.A. and Zorio-Grima, A., 2016. Data analytics in banks' audit:

The case of loan loss provisions in Uruguay. Journal of Business Research, 69(11), pp.4793-

4797.

Gaynor, L.M., Kelton, A.S., Mercer, M. and Yohn, T.L., 2016. Understanding the relation

between financial reporting quality and audit quality. Auditing: A Journal of Practice &

Theory, 35(4), pp.1-22.

References:

Abbott, L.J., Daugherty, B., Parker, S. and Peters, G.F., 2016. Internal audit quality and financial

reporting quality: The joint importance of independence and competence. Journal of Accounting

Research, 54(1), pp.3-40.

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance services.

Pearson.

Badolato, P.G., Donelson, D.C. and Ege, M., 2014. Audit committee financial expertise and

earnings management: The role of status. Journal of Accounting and Economics, 58(2), pp.208-

230.

Bierstaker, J., Janvrin, D. and Lowe, D.J., 2014. What factors influence auditors' use of

computer-assisted audit techniques?. Advances in Accounting, 30(1), pp.67-74.

Cao, M., Chychyla, R. and Stewart, T., 2015. Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), pp.423-429.

Coderre, D., 2015. Gauge your analytics: by addressing people, processes, and technology,

internal audit can ensure a successful data analytics initiative. Internal Auditor, 72(4), pp.41-46.

Gambetta, N., García-Benau, M.A. and Zorio-Grima, A., 2016. Data analytics in banks' audit:

The case of loan loss provisions in Uruguay. Journal of Business Research, 69(11), pp.4793-

4797.

Gaynor, L.M., Kelton, A.S., Mercer, M. and Yohn, T.L., 2016. Understanding the relation

between financial reporting quality and audit quality. Auditing: A Journal of Practice &

Theory, 35(4), pp.1-22.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17AUDITING

Karim, A.M., Shaikh, J.M., Hock, O.Y. and Islam, M.R., 2017. Creative Accounting: Techniques

of Application-An Empirical Study among Auditors and Accountants of Listed Companies in

Bangladesh. Australian Academy of Accounting and Finance Review, 2(3), pp.215-245.

Shandell, R.E., Smith, P. and Schulman, F.A., 2017. The preparation and trial of medical

malpractice cases. Law Journal Press.

Suryanto, T., 2016. Audit Delay and Its Implication for Fraudulent Financial Reporting: A Study

of Companies Listed in the Indonesian Stock Exchange. European Research Studies, 19(1), p.18.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Yuen, J., 2014. ACC 626 Computer Assisted Auditing Techniques Money Laundering Detection.

Karim, A.M., Shaikh, J.M., Hock, O.Y. and Islam, M.R., 2017. Creative Accounting: Techniques

of Application-An Empirical Study among Auditors and Accountants of Listed Companies in

Bangladesh. Australian Academy of Accounting and Finance Review, 2(3), pp.215-245.

Shandell, R.E., Smith, P. and Schulman, F.A., 2017. The preparation and trial of medical

malpractice cases. Law Journal Press.

Suryanto, T., 2016. Audit Delay and Its Implication for Fraudulent Financial Reporting: A Study

of Companies Listed in the Indonesian Stock Exchange. European Research Studies, 19(1), p.18.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Yuen, J., 2014. ACC 626 Computer Assisted Auditing Techniques Money Laundering Detection.

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.