Auditing Report: Audit Expectation Gap, Threats to Independence, SBF

VerifiedAdded on 2022/10/11

|7

|1326

|43

Report

AI Summary

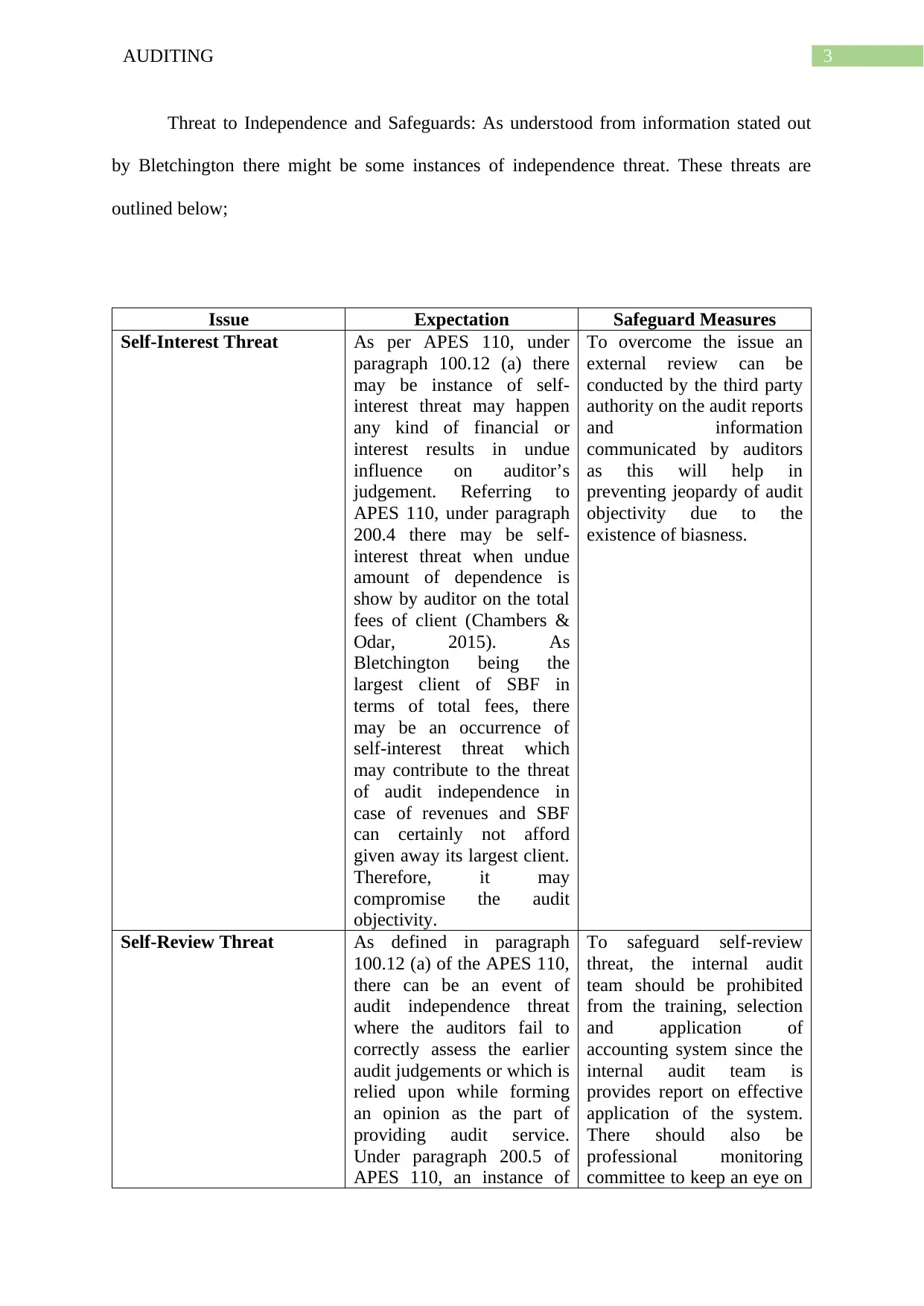

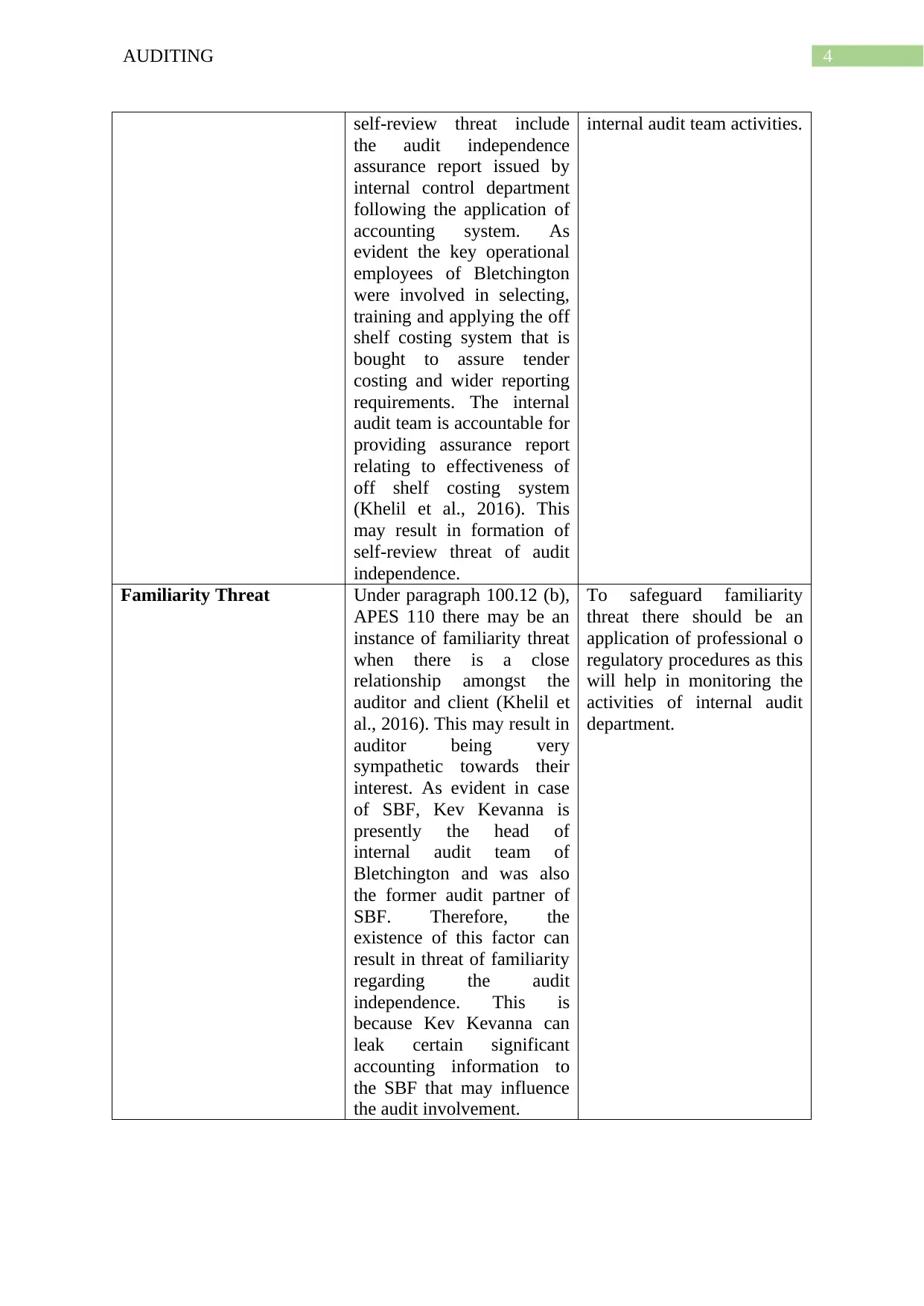

This report, prepared by an audit manager at Samway Baker Fitzgerald (SBF), addresses the audit expectation gap and threats to audit independence in the context of Bletchington Limited, a major client. It defines the audit expectation gap as the difference between financial report users' and auditors' expectations, outlining unrealistic user expectations and auditors' responsibilities. The report identifies and analyzes potential threats to audit independence, including self-interest, self-review, and familiarity threats, providing specific examples related to Bletchington's operations and the relationship between SBF and the client. Safeguard measures are proposed to mitigate each threat, such as external reviews, professional monitoring, and adherence to regulatory procedures. The report references relevant professional standards and provides a comprehensive assessment of the audit engagement, aiming to ensure objectivity and compliance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.