Auditing and Assurance | Assignment | Answers

VerifiedAdded on 2022/08/28

|9

|1779

|19

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUDITING AND ASSURANCE

Table of Contents

Answer to Question 1......................................................................................................................2

Introduction..................................................................................................................................2

Answer to Requirement 1............................................................................................................2

Answer to Requirement 2............................................................................................................2

Answer to Requirement 3............................................................................................................3

Answer to Requirement 4............................................................................................................3

Conclusion...................................................................................................................................3

Answer to Question 2......................................................................................................................4

Advise to Jack regarding the Information of the Audit of Switch Ltd........................................4

References........................................................................................................................................8

Table of Contents

Answer to Question 1......................................................................................................................2

Introduction..................................................................................................................................2

Answer to Requirement 1............................................................................................................2

Answer to Requirement 2............................................................................................................2

Answer to Requirement 3............................................................................................................3

Answer to Requirement 4............................................................................................................3

Conclusion...................................................................................................................................3

Answer to Question 2......................................................................................................................4

Advise to Jack regarding the Information of the Audit of Switch Ltd........................................4

References........................................................................................................................................8

2AUDITING AND ASSURANCE

Answer to Question 1

Introduction

In case a plaintiff wants to win a lawsuit for negligence against the defendant, he/she is

needed to prove all the elements of tort of negligence (Dobson, 2015). The same aspects is also

applicable in audit-client relationship as the client or any other third party is required to prove the

presence of all elements of tort of negligence winning the lawsuit against the auditor.

Answer to Requirement 1

Duty of care, Breach of duty of care, Cause in fact and Damages are the four elements of

tort of negligence and these are further discussed below:

1. Duty of Care – The result of the negligence cases depend on whether the defendant owed a

duty of care to the plaintiff (Pappalardo, 2015). The facts of the case demonstrates that Oscar

Edwards Vance (OEV) is the audit partner of Framed Ltd; and as per law, there is a relationship

between OEV and Framed Ltd that requires OEV to act in the best interest of Framed Ltd.

2. Breach of Duty of Care – Along with proving the presence of duty of care, the plaintiff needs

to prove that there is violation of duty of care. There might be violation of duty of care in Framed

Ltd as OEV issued unmodified audit opinion even in the presence of materially overstated sales

and receivables (Buckley, 2018).

3. Cause in Fact – This requires proving that the actions of the defendant are the actual reason

of the plaintiff’s damage. The damages of Framed Ltd’s creditors were due to the issue of wrong

audit opinion by OEV.

4. Damages – It is required for the plaintiff to prove a legally recognized harm or damage. For

example, VicBank had to face financial loss due to extending credit to Framed Ltd.

Answer to Requirement 2

The audit-client relationship between OEV and Framed Ltd proves that OEV owed duty

of care to Framed Ltd; and this was violated when OEV failed in recognizing the fraud carried

out by two of Framed Ltd’s sales representatives for earning bonus which materially overstated

sales and receivables. This proves that whatever damage is caused to Framed Ltd was because of

Answer to Question 1

Introduction

In case a plaintiff wants to win a lawsuit for negligence against the defendant, he/she is

needed to prove all the elements of tort of negligence (Dobson, 2015). The same aspects is also

applicable in audit-client relationship as the client or any other third party is required to prove the

presence of all elements of tort of negligence winning the lawsuit against the auditor.

Answer to Requirement 1

Duty of care, Breach of duty of care, Cause in fact and Damages are the four elements of

tort of negligence and these are further discussed below:

1. Duty of Care – The result of the negligence cases depend on whether the defendant owed a

duty of care to the plaintiff (Pappalardo, 2015). The facts of the case demonstrates that Oscar

Edwards Vance (OEV) is the audit partner of Framed Ltd; and as per law, there is a relationship

between OEV and Framed Ltd that requires OEV to act in the best interest of Framed Ltd.

2. Breach of Duty of Care – Along with proving the presence of duty of care, the plaintiff needs

to prove that there is violation of duty of care. There might be violation of duty of care in Framed

Ltd as OEV issued unmodified audit opinion even in the presence of materially overstated sales

and receivables (Buckley, 2018).

3. Cause in Fact – This requires proving that the actions of the defendant are the actual reason

of the plaintiff’s damage. The damages of Framed Ltd’s creditors were due to the issue of wrong

audit opinion by OEV.

4. Damages – It is required for the plaintiff to prove a legally recognized harm or damage. For

example, VicBank had to face financial loss due to extending credit to Framed Ltd.

Answer to Requirement 2

The audit-client relationship between OEV and Framed Ltd proves that OEV owed duty

of care to Framed Ltd; and this was violated when OEV failed in recognizing the fraud carried

out by two of Framed Ltd’s sales representatives for earning bonus which materially overstated

sales and receivables. This proves that whatever damage is caused to Framed Ltd was because of

3AUDITING AND ASSURANCE

OEV as the auditors overlooked the fact that Framed Ltd had reasonable revenue even after the

cash flows issues; and they did not feel the necessity of assessing the company’s going concern

status. Now, it is needed for the liquidators of Framed Ltd to prove a legally recognized harm

(Zipser, 2017). Thus, the liquidators of Framed Ltd are likely to succeed in their actions against

OEV as negligence was there.

Answer to Requirement 3

The liability of the auditors is generated from negligence and the same can be seen from

the auditors of OEV. They were negligent in the audit of Framed Ltd as neither had they assessed

the going concern position of Framed Ltd even after major cash flow issues nor they considered

the abnormal increase in revenue even in the cash flow issues (Goudkamp, 2017). Thus, they

failed in identifying the ongoing fraud by the sales representatives that caused material

overstatement in sales and receivables. Since, it is proved that OEV was negligent in the audit of

Framed Ltd; their liability to the liquidators cannot be reduced.

Answer to Requirement 4

Since VicBank was an user of the audited financial statements issued by OEV, OEV also

owed a duty of care to VicBank and this was breached because of the issue of inappropriate audit

report by neglecting the major audit risk areas in Framed Ltd’s financial statements. Therefore,

the actions of OEV was the reason for the damage caused to VicBank; and the damage can easily

be expressed into monetary terms as VicBank extended overdraft opportunity to Framed Ltd

(Barker, 2015). All these increase the likelihood of success of the actions of VicBank agasint

OEV.

Conclusion

The above discussion indicates towards the importance of fulfilling all the four conditions

or elements of tort of negligence in case the plaintiff wants to be successful in the lawsuits

against the defendant. Moreover, in case there is clear negligence from the auditors, their

liabilities cannot be reduced.

OEV as the auditors overlooked the fact that Framed Ltd had reasonable revenue even after the

cash flows issues; and they did not feel the necessity of assessing the company’s going concern

status. Now, it is needed for the liquidators of Framed Ltd to prove a legally recognized harm

(Zipser, 2017). Thus, the liquidators of Framed Ltd are likely to succeed in their actions against

OEV as negligence was there.

Answer to Requirement 3

The liability of the auditors is generated from negligence and the same can be seen from

the auditors of OEV. They were negligent in the audit of Framed Ltd as neither had they assessed

the going concern position of Framed Ltd even after major cash flow issues nor they considered

the abnormal increase in revenue even in the cash flow issues (Goudkamp, 2017). Thus, they

failed in identifying the ongoing fraud by the sales representatives that caused material

overstatement in sales and receivables. Since, it is proved that OEV was negligent in the audit of

Framed Ltd; their liability to the liquidators cannot be reduced.

Answer to Requirement 4

Since VicBank was an user of the audited financial statements issued by OEV, OEV also

owed a duty of care to VicBank and this was breached because of the issue of inappropriate audit

report by neglecting the major audit risk areas in Framed Ltd’s financial statements. Therefore,

the actions of OEV was the reason for the damage caused to VicBank; and the damage can easily

be expressed into monetary terms as VicBank extended overdraft opportunity to Framed Ltd

(Barker, 2015). All these increase the likelihood of success of the actions of VicBank agasint

OEV.

Conclusion

The above discussion indicates towards the importance of fulfilling all the four conditions

or elements of tort of negligence in case the plaintiff wants to be successful in the lawsuits

against the defendant. Moreover, in case there is clear negligence from the auditors, their

liabilities cannot be reduced.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUDITING AND ASSURANCE

Answer to Question 2

Advise to Jack regarding the Information of the Audit of Switch Ltd

American Accounting Association Model Decision-making process

1. Determine the facts

The facts are that Jack is supposed to

provide the senior audit manager with the

information on the material cut-off error that

caused revenue to be materially misstated

by documenting it in the working paper; but

his audit manager, Bruce, told him not to

mention the adjustment related information

in the working papers.

2. Define the ethical issues

Determining whether Jack should provide

the information to the senior audit partner

through documenting the adjustment in the

working paper or he should not do this as

per Bruce is the main ethical issue in this

case which is associated with the ethical

codes and principles of APES 110 (Clayton

& van Staden, 2015).

3. Identify the major principles, rules, and

values

Three APES 110 principles having

association with this case are Integrity,

Objectivity and Professional Behavior.

1) It is mentioned under Subsection 111 of

APES 110 that there must be honesty and

integrity from the auditors’ end in the audit

Answer to Question 2

Advise to Jack regarding the Information of the Audit of Switch Ltd

American Accounting Association Model Decision-making process

1. Determine the facts

The facts are that Jack is supposed to

provide the senior audit manager with the

information on the material cut-off error that

caused revenue to be materially misstated

by documenting it in the working paper; but

his audit manager, Bruce, told him not to

mention the adjustment related information

in the working papers.

2. Define the ethical issues

Determining whether Jack should provide

the information to the senior audit partner

through documenting the adjustment in the

working paper or he should not do this as

per Bruce is the main ethical issue in this

case which is associated with the ethical

codes and principles of APES 110 (Clayton

& van Staden, 2015).

3. Identify the major principles, rules, and

values

Three APES 110 principles having

association with this case are Integrity,

Objectivity and Professional Behavior.

1) It is mentioned under Subsection 111 of

APES 110 that there must be honesty and

integrity from the auditors’ end in the audit

5AUDITING AND ASSURANCE

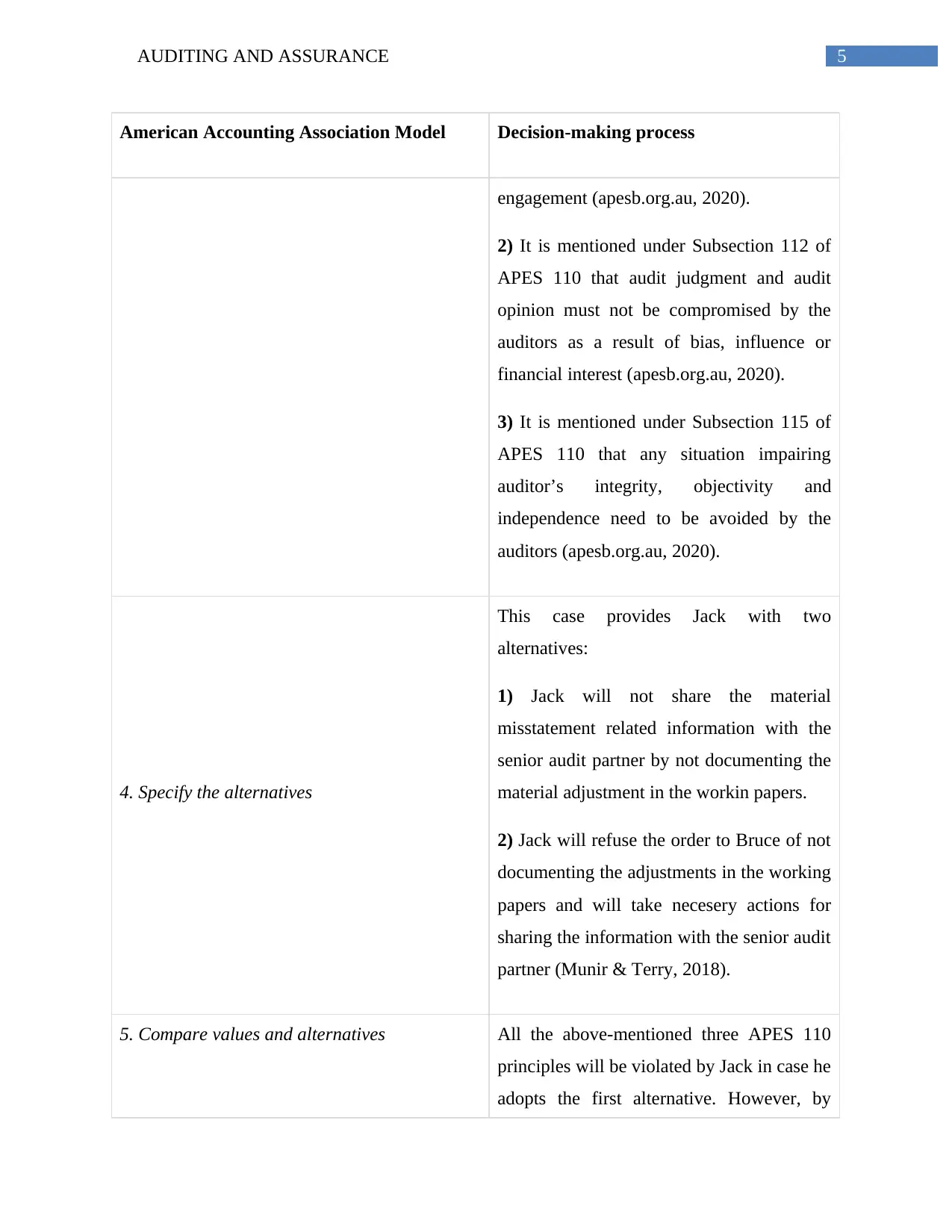

American Accounting Association Model Decision-making process

engagement (apesb.org.au, 2020).

2) It is mentioned under Subsection 112 of

APES 110 that audit judgment and audit

opinion must not be compromised by the

auditors as a result of bias, influence or

financial interest (apesb.org.au, 2020).

3) It is mentioned under Subsection 115 of

APES 110 that any situation impairing

auditor’s integrity, objectivity and

independence need to be avoided by the

auditors (apesb.org.au, 2020).

4. Specify the alternatives

This case provides Jack with two

alternatives:

1) Jack will not share the material

misstatement related information with the

senior audit partner by not documenting the

material adjustment in the workin papers.

2) Jack will refuse the order to Bruce of not

documenting the adjustments in the working

papers and will take necesery actions for

sharing the information with the senior audit

partner (Munir & Terry, 2018).

5. Compare values and alternatives All the above-mentioned three APES 110

principles will be violated by Jack in case he

adopts the first alternative. However, by

American Accounting Association Model Decision-making process

engagement (apesb.org.au, 2020).

2) It is mentioned under Subsection 112 of

APES 110 that audit judgment and audit

opinion must not be compromised by the

auditors as a result of bias, influence or

financial interest (apesb.org.au, 2020).

3) It is mentioned under Subsection 115 of

APES 110 that any situation impairing

auditor’s integrity, objectivity and

independence need to be avoided by the

auditors (apesb.org.au, 2020).

4. Specify the alternatives

This case provides Jack with two

alternatives:

1) Jack will not share the material

misstatement related information with the

senior audit partner by not documenting the

material adjustment in the workin papers.

2) Jack will refuse the order to Bruce of not

documenting the adjustments in the working

papers and will take necesery actions for

sharing the information with the senior audit

partner (Munir & Terry, 2018).

5. Compare values and alternatives All the above-mentioned three APES 110

principles will be violated by Jack in case he

adopts the first alternative. However, by

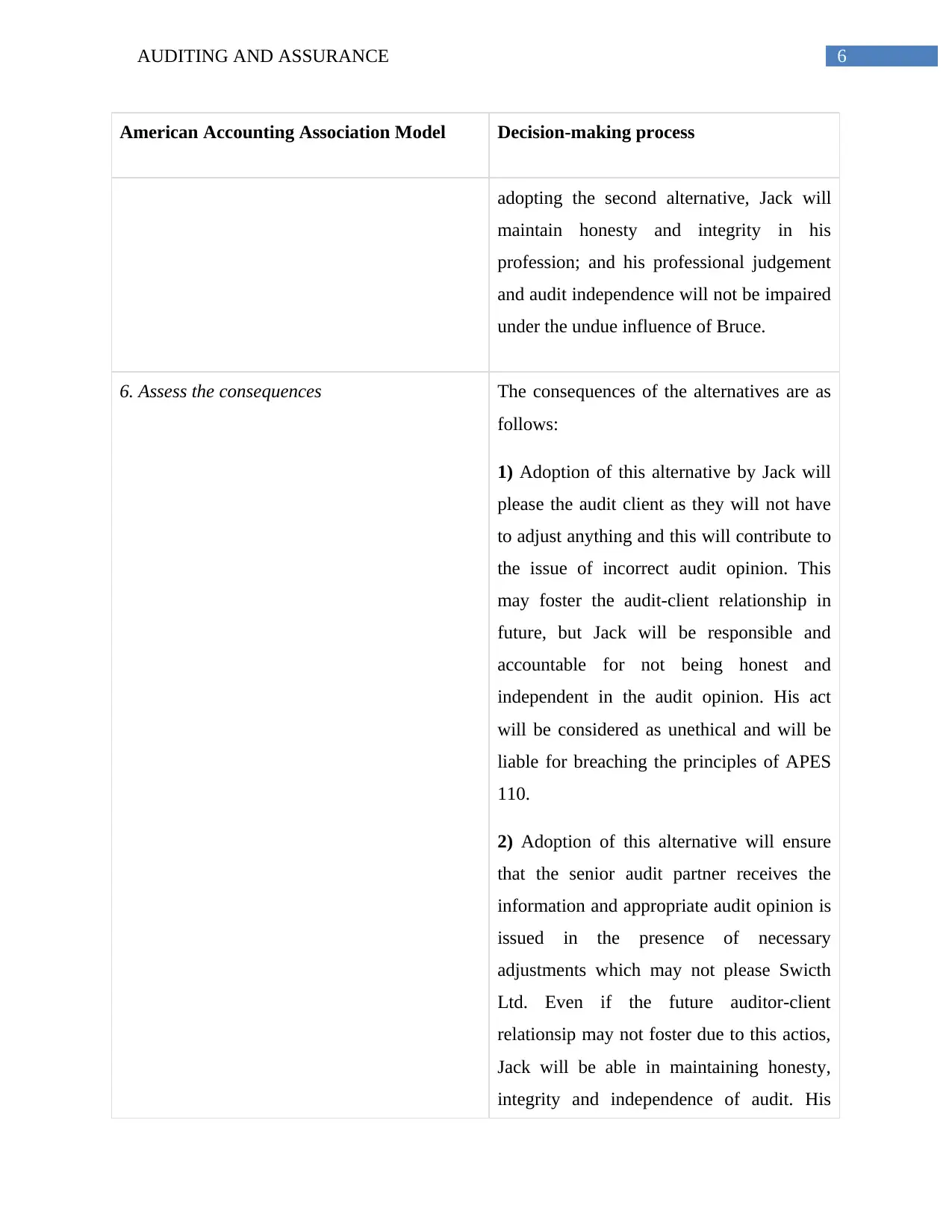

6AUDITING AND ASSURANCE

American Accounting Association Model Decision-making process

adopting the second alternative, Jack will

maintain honesty and integrity in his

profession; and his professional judgement

and audit independence will not be impaired

under the undue influence of Bruce.

6. Assess the consequences The consequences of the alternatives are as

follows:

1) Adoption of this alternative by Jack will

please the audit client as they will not have

to adjust anything and this will contribute to

the issue of incorrect audit opinion. This

may foster the audit-client relationship in

future, but Jack will be responsible and

accountable for not being honest and

independent in the audit opinion. His act

will be considered as unethical and will be

liable for breaching the principles of APES

110.

2) Adoption of this alternative will ensure

that the senior audit partner receives the

information and appropriate audit opinion is

issued in the presence of necessary

adjustments which may not please Swicth

Ltd. Even if the future auditor-client

relationsip may not foster due to this actios,

Jack will be able in maintaining honesty,

integrity and independence of audit. His

American Accounting Association Model Decision-making process

adopting the second alternative, Jack will

maintain honesty and integrity in his

profession; and his professional judgement

and audit independence will not be impaired

under the undue influence of Bruce.

6. Assess the consequences The consequences of the alternatives are as

follows:

1) Adoption of this alternative by Jack will

please the audit client as they will not have

to adjust anything and this will contribute to

the issue of incorrect audit opinion. This

may foster the audit-client relationship in

future, but Jack will be responsible and

accountable for not being honest and

independent in the audit opinion. His act

will be considered as unethical and will be

liable for breaching the principles of APES

110.

2) Adoption of this alternative will ensure

that the senior audit partner receives the

information and appropriate audit opinion is

issued in the presence of necessary

adjustments which may not please Swicth

Ltd. Even if the future auditor-client

relationsip may not foster due to this actios,

Jack will be able in maintaining honesty,

integrity and independence of audit. His

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

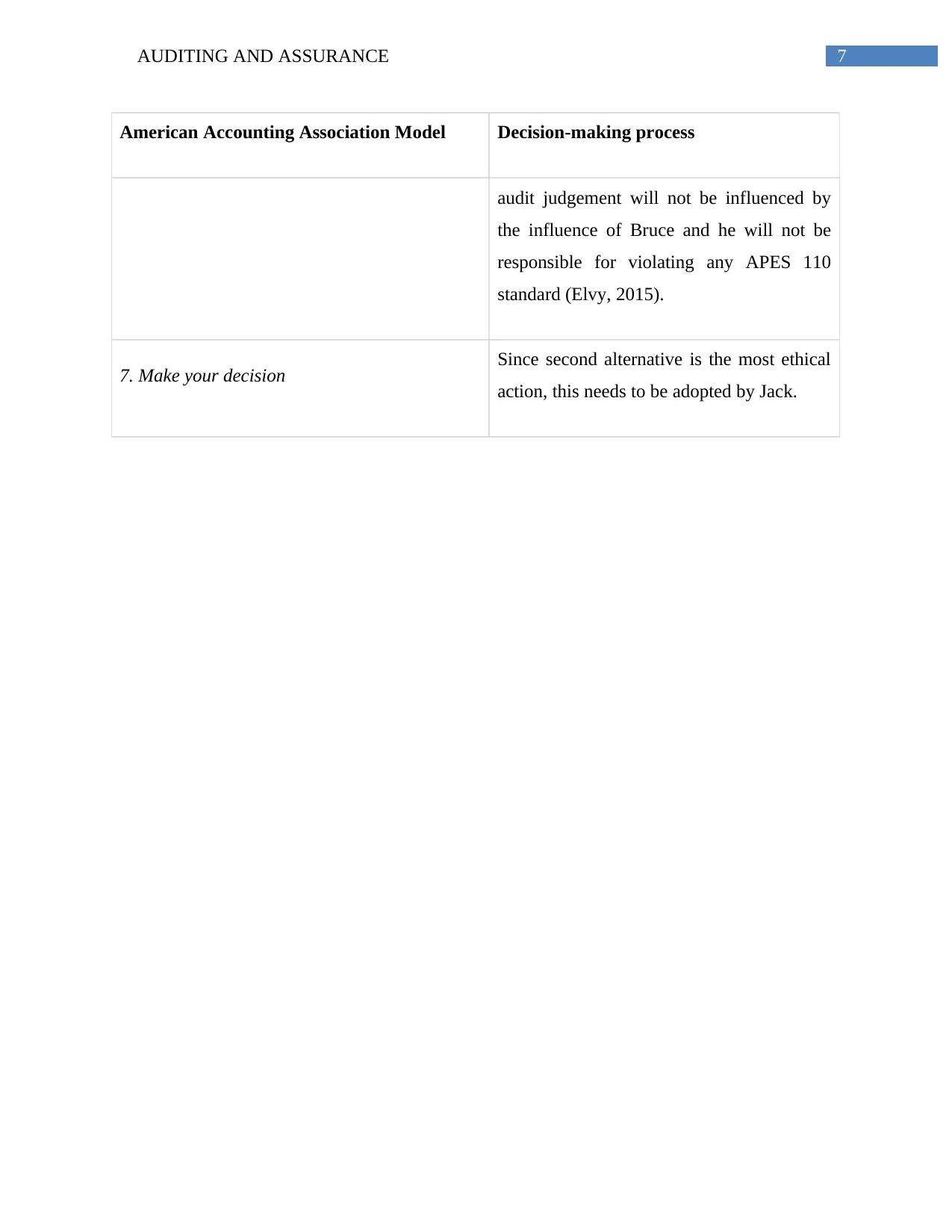

American Accounting Association Model Decision-making process

audit judgement will not be influenced by

the influence of Bruce and he will not be

responsible for violating any APES 110

standard (Elvy, 2015).

7. Make your decision Since second alternative is the most ethical

action, this needs to be adopted by Jack.

American Accounting Association Model Decision-making process

audit judgement will not be influenced by

the influence of Bruce and he will not be

responsible for violating any APES 110

standard (Elvy, 2015).

7. Make your decision Since second alternative is the most ethical

action, this needs to be adopted by Jack.

8AUDITING AND ASSURANCE

References

Apesb.org.au. (2020). APES 110 Code of Ethics for Professional Accountants (including

Independence Standards). Retrieved 23 March 2020, from

https://www.apesb.org.au/uploads/home/02112018000152_APES_110_Restructured_Co

de_Nov_2018.pdf

Barker, K. (2015). Negligent Misstatement in Australia-Resolving the Uncertain Legacy of

Esanda: Chapter 13. Ch, 13, 319-344.

Buckley, R. A. (2018). A History of Australian Tort Law 1901–1945: England’s Obedient

Servant?.

Clayton, B. M., & van Staden, C. J. (2015). The impact of social influence pressure on the

ethical decision making of professional accountants: Australian and New Zealand

evidence. Australian Accounting Review, 25(4), 372-388.

Dobson, E. (2015). Negligence. Legaldate, 27(1), 4.

Elvy, H. (2015). Ethics and codes: Where to from here?. Professional Planner, (78), 38.

Goudkamp, J. (2017). Breach of Duty: A Disappearing Element of the Action in

Negligence?. The Cambridge Law Journal, 76(3), 480-483.

Munir, R., & Terry, C. (2018). Accountants and the Ethics of Profit: The Case of the Australian

Retail Industry. Journal of business ethics education, 15, 327-347.

Pappalardo, K. (2015). Duty and control in intermediary copyright liability: An Australian

perspective. In Copyright Perspectives (pp. 241-259). Springer, Cham.

Zipser, B. (2017). An update on civil liability. Precedent (Sydney, NSW), (140), 2.

References

Apesb.org.au. (2020). APES 110 Code of Ethics for Professional Accountants (including

Independence Standards). Retrieved 23 March 2020, from

https://www.apesb.org.au/uploads/home/02112018000152_APES_110_Restructured_Co

de_Nov_2018.pdf

Barker, K. (2015). Negligent Misstatement in Australia-Resolving the Uncertain Legacy of

Esanda: Chapter 13. Ch, 13, 319-344.

Buckley, R. A. (2018). A History of Australian Tort Law 1901–1945: England’s Obedient

Servant?.

Clayton, B. M., & van Staden, C. J. (2015). The impact of social influence pressure on the

ethical decision making of professional accountants: Australian and New Zealand

evidence. Australian Accounting Review, 25(4), 372-388.

Dobson, E. (2015). Negligence. Legaldate, 27(1), 4.

Elvy, H. (2015). Ethics and codes: Where to from here?. Professional Planner, (78), 38.

Goudkamp, J. (2017). Breach of Duty: A Disappearing Element of the Action in

Negligence?. The Cambridge Law Journal, 76(3), 480-483.

Munir, R., & Terry, C. (2018). Accountants and the Ethics of Profit: The Case of the Australian

Retail Industry. Journal of business ethics education, 15, 327-347.

Pappalardo, K. (2015). Duty and control in intermediary copyright liability: An Australian

perspective. In Copyright Perspectives (pp. 241-259). Springer, Cham.

Zipser, B. (2017). An update on civil liability. Precedent (Sydney, NSW), (140), 2.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.