Auditing and Assurance

Added on 2023-04-08

6 Pages1021 Words260 Views

Running head: AUDITING AND ASSURANCE

Auditing and assurance

Name of the student

Name of the student

Student ID

Author note

Auditing and assurance

Name of the student

Name of the student

Student ID

Author note

1AUDITING AND ASSURANCE

Table of Contents

Answer to question 1 and 2.............................................................................................................2

Reference.........................................................................................................................................5

Table of Contents

Answer to question 1 and 2.............................................................................................................2

Reference.........................................................................................................................................5

2AUDITING AND ASSURANCE

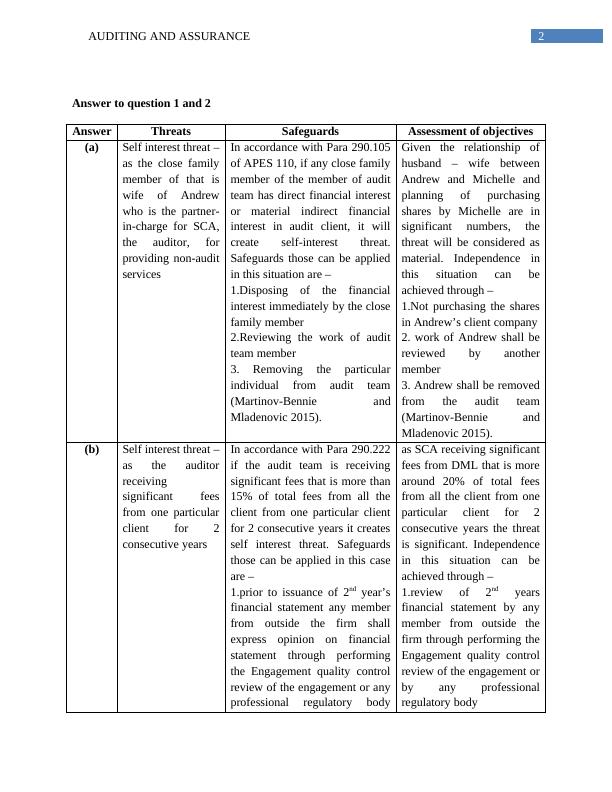

Answer to question 1 and 2

Answer Threats Safeguards Assessment of objectives

(a) Self interest threat –

as the close family

member of that is

wife of Andrew

who is the partner-

in-charge for SCA,

the auditor, for

providing non-audit

services

In accordance with Para 290.105

of APES 110, if any close family

member of the member of audit

team has direct financial interest

or material indirect financial

interest in audit client, it will

create self-interest threat.

Safeguards those can be applied

in this situation are –

1.Disposing of the financial

interest immediately by the close

family member

2.Reviewing the work of audit

team member

3. Removing the particular

individual from audit team

(Martinov-Bennie and

Mladenovic 2015).

Given the relationship of

husband – wife between

Andrew and Michelle and

planning of purchasing

shares by Michelle are in

significant numbers, the

threat will be considered as

material. Independence in

this situation can be

achieved through –

1.Not purchasing the shares

in Andrew’s client company

2. work of Andrew shall be

reviewed by another

member

3. Andrew shall be removed

from the audit team

(Martinov-Bennie and

Mladenovic 2015).

(b) Self interest threat –

as the auditor

receiving

significant fees

from one particular

client for 2

consecutive years

In accordance with Para 290.222

if the audit team is receiving

significant fees that is more than

15% of total fees from all the

client from one particular client

for 2 consecutive years it creates

self interest threat. Safeguards

those can be applied in this case

are –

1.prior to issuance of 2nd year’s

financial statement any member

from outside the firm shall

express opinion on financial

statement through performing

the Engagement quality control

review of the engagement or any

professional regulatory body

as SCA receiving significant

fees from DML that is more

around 20% of total fees

from all the client from one

particular client for 2

consecutive years the threat

is significant. Independence

in this situation can be

achieved through –

1.review of 2nd years

financial statement by any

member from outside the

firm through performing the

Engagement quality control

review of the engagement or

by any professional

regulatory body

Answer to question 1 and 2

Answer Threats Safeguards Assessment of objectives

(a) Self interest threat –

as the close family

member of that is

wife of Andrew

who is the partner-

in-charge for SCA,

the auditor, for

providing non-audit

services

In accordance with Para 290.105

of APES 110, if any close family

member of the member of audit

team has direct financial interest

or material indirect financial

interest in audit client, it will

create self-interest threat.

Safeguards those can be applied

in this situation are –

1.Disposing of the financial

interest immediately by the close

family member

2.Reviewing the work of audit

team member

3. Removing the particular

individual from audit team

(Martinov-Bennie and

Mladenovic 2015).

Given the relationship of

husband – wife between

Andrew and Michelle and

planning of purchasing

shares by Michelle are in

significant numbers, the

threat will be considered as

material. Independence in

this situation can be

achieved through –

1.Not purchasing the shares

in Andrew’s client company

2. work of Andrew shall be

reviewed by another

member

3. Andrew shall be removed

from the audit team

(Martinov-Bennie and

Mladenovic 2015).

(b) Self interest threat –

as the auditor

receiving

significant fees

from one particular

client for 2

consecutive years

In accordance with Para 290.222

if the audit team is receiving

significant fees that is more than

15% of total fees from all the

client from one particular client

for 2 consecutive years it creates

self interest threat. Safeguards

those can be applied in this case

are –

1.prior to issuance of 2nd year’s

financial statement any member

from outside the firm shall

express opinion on financial

statement through performing

the Engagement quality control

review of the engagement or any

professional regulatory body

as SCA receiving significant

fees from DML that is more

around 20% of total fees

from all the client from one

particular client for 2

consecutive years the threat

is significant. Independence

in this situation can be

achieved through –

1.review of 2nd years

financial statement by any

member from outside the

firm through performing the

Engagement quality control

review of the engagement or

by any professional

regulatory body

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Auditing and Ethical Practicelg...

|12

|2168

|30

Auditing and Assurance Servicelg...

|8

|1893

|213

MAA303 - Audit and Assurancelg...

|5

|753

|72

Auditing, Assurance, and Risk Assessment Assignmentlg...

|5

|1202

|153

Audit and Assurance- Documentlg...

|6

|1041

|156

Auditing and Assurance Assignment PDFlg...

|5

|783

|90