Audit Report: Financial Statement Review, Procedures & Audit Quality

VerifiedAdded on 2023/04/21

|12

|3168

|439

Report

AI Summary

This report provides an analysis of AMP Ltd's annual report for 2017, focusing on auditing and assurance. It includes an analytical review of the financial statements to identify areas of concern, such as liquidity risks indicated by the current ratio. The report formulates audit procedures to address these concerns, emphasizing the importance of Enterprise Risk Management (ERM). It also explores the concept of audit quality, highlighting the roles of IASB and ASIC in maintaining and improving audit standards in Australia. Three steps taken by Australian accounting bodies to improve audit quality are identified, including bridging the audit expectation gap, implementing audit regulations, and promoting financial reporting initiatives. The report concludes by emphasizing the significance of maintaining audit quality through continuous improvement and adherence to professional standards, ensuring accurate financial reporting and stakeholder confidence. Desklib provides access to this document and other solved assignments for students.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Table of Contents

Introduction..........................................................................................................................2

Part A...............................................................................................................................2

1. Conducting Analytical review of the financial statement for identifying areas of

concern.........................................................................................................................................2

2. Formulating the audit procedures and responding to the areas of concern.................3

Part B...................................................................................................................................4

1. Explaining the team’s understanding of the concept of audit quality.........................4

2. Explaining and identifying 3 steps the accounting bodies have taken in Australia to

improve the quality of audit.........................................................................................................5

3. Importance of maintaining audit quality in carrying out an audit...............................6

Conclusion...........................................................................................................................7

References............................................................................................................................9

List of Appendix................................................................................................................11

Table of Contents

Introduction..........................................................................................................................2

Part A...............................................................................................................................2

1. Conducting Analytical review of the financial statement for identifying areas of

concern.........................................................................................................................................2

2. Formulating the audit procedures and responding to the areas of concern.................3

Part B...................................................................................................................................4

1. Explaining the team’s understanding of the concept of audit quality.........................4

2. Explaining and identifying 3 steps the accounting bodies have taken in Australia to

improve the quality of audit.........................................................................................................5

3. Importance of maintaining audit quality in carrying out an audit...............................6

Conclusion...........................................................................................................................7

References............................................................................................................................9

List of Appendix................................................................................................................11

2AUDITING AND ASSURANCE

Introduction

The reporting aspects of the study will focus on evaluating the annual report of AMP Ltd

for the year ended 31 December 2017. The study will include analytical review of the financial

statements put forward in the planning phase and included the concerns on how the relevant

assertions and accounts are impacted. The next step is seen with formulating the relevant audit

procedures for responding to the areas of concern in the planning phase. The second section of

the study has been able to focus on the concept of the audit quality as per the given case study. In

addition to this, it has also explained about identifying three steps for the initiatives taken by the

accounting bodies of Australia for improving the quality of audit. The final section of the study

has been further able to provide the relevant analysis on how the teams will be able to maintain

the adequate quality for carrying out the relevant audit procedure and provide the justification for

the same.

Part A

1. Conducting Analytical review of the financial statement for identifying areas of concern

As per the assessment of the annual report Risk is inherent in the business of AMP. The

company has faced key business challenge in terms of adverse impact of the delivery of the

strategies. A significant aspect of the business risk faced by the company are discerned with

competitor and customer environment. In addition to this, some of the other risk aspects of the

company are seen with the risk of liquidity concerns. The high amount of liquidity has created

major concerns for the company which are associated with improper utilization of available

short-term finances. This risk is seen with current ratio of 8.18 in 2017. Such a figure of the

current ratio is considered to pose a significant concern of liquidity. A similar finding is seen to

Introduction

The reporting aspects of the study will focus on evaluating the annual report of AMP Ltd

for the year ended 31 December 2017. The study will include analytical review of the financial

statements put forward in the planning phase and included the concerns on how the relevant

assertions and accounts are impacted. The next step is seen with formulating the relevant audit

procedures for responding to the areas of concern in the planning phase. The second section of

the study has been able to focus on the concept of the audit quality as per the given case study. In

addition to this, it has also explained about identifying three steps for the initiatives taken by the

accounting bodies of Australia for improving the quality of audit. The final section of the study

has been further able to provide the relevant analysis on how the teams will be able to maintain

the adequate quality for carrying out the relevant audit procedure and provide the justification for

the same.

Part A

1. Conducting Analytical review of the financial statement for identifying areas of concern

As per the assessment of the annual report Risk is inherent in the business of AMP. The

company has faced key business challenge in terms of adverse impact of the delivery of the

strategies. A significant aspect of the business risk faced by the company are discerned with

competitor and customer environment. In addition to this, some of the other risk aspects of the

company are seen with the risk of liquidity concerns. The high amount of liquidity has created

major concerns for the company which are associated with improper utilization of available

short-term finances. This risk is seen with current ratio of 8.18 in 2017. Such a figure of the

current ratio is considered to pose a significant concern of liquidity. A similar finding is seen to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

be evident in case of quick ratio. The financial risk of the company is further inferred with

reducing Fixed Asset Turnover Ratio (Tepalagul & Lin, 2015).

Additionally, some of the various types of the other areas of concern for the company can

be determined in form of strategic risk, credit risk, market risk, insurance risk, operational risk

and concentration risk. The strategic risk loss of AMP Ltd. can be directly considered with loss

of forgone value linked with competitive positioning and strategic decisions. Additionally, the

credit risk of AMP Ltd. is identified in terms of risk of forgone value pertaining to the non-

payment of contractually required payment by a counterparty. The market concerns can be

determined with forgone value pertaining to the negative fluctuations of the investment values

and market prices (Bryce, Ali & Mather, 2015). The various types of the insurance risk concerns

are taken into account pertaining to the adverse development in the mortality rate, changes in the

behaviour of the policyholder and including the longevity and expense. The concentration risk is

seen with a series of exposures for producing losses. Additionally, the operational risk is inferred

with risk of loss which is a resultant from the failure of the internal process pertaining to the

external events (Ball, Tyler & Wells, 2015).

2. Formulating the audit procedures and responding to the areas of concern

As per the information published in the annual report of AMP Ltd. it may be discerned

that risk is inherent in the business and AMP takes the measured risk for achieving the strategic

objectives. The company has been able to set a clear strategic plan for identification of the

enterprise risk and aiding the overall process of the business. This is important for the company

in understanding and identification of the preliminary risk. The “Enterprise Risk Management

(ERM)” framework maintained by the company has enabled the company in identifying,

reviewing and monitoring the emerging risk factors which may affect the business. AMP has

recognised that the effective risk management with “Enterprise Risk Management (ERM)”

be evident in case of quick ratio. The financial risk of the company is further inferred with

reducing Fixed Asset Turnover Ratio (Tepalagul & Lin, 2015).

Additionally, some of the various types of the other areas of concern for the company can

be determined in form of strategic risk, credit risk, market risk, insurance risk, operational risk

and concentration risk. The strategic risk loss of AMP Ltd. can be directly considered with loss

of forgone value linked with competitive positioning and strategic decisions. Additionally, the

credit risk of AMP Ltd. is identified in terms of risk of forgone value pertaining to the non-

payment of contractually required payment by a counterparty. The market concerns can be

determined with forgone value pertaining to the negative fluctuations of the investment values

and market prices (Bryce, Ali & Mather, 2015). The various types of the insurance risk concerns

are taken into account pertaining to the adverse development in the mortality rate, changes in the

behaviour of the policyholder and including the longevity and expense. The concentration risk is

seen with a series of exposures for producing losses. Additionally, the operational risk is inferred

with risk of loss which is a resultant from the failure of the internal process pertaining to the

external events (Ball, Tyler & Wells, 2015).

2. Formulating the audit procedures and responding to the areas of concern

As per the information published in the annual report of AMP Ltd. it may be discerned

that risk is inherent in the business and AMP takes the measured risk for achieving the strategic

objectives. The company has been able to set a clear strategic plan for identification of the

enterprise risk and aiding the overall process of the business. This is important for the company

in understanding and identification of the preliminary risk. The “Enterprise Risk Management

(ERM)” framework maintained by the company has enabled the company in identifying,

reviewing and monitoring the emerging risk factors which may affect the business. AMP has

recognised that the effective risk management with “Enterprise Risk Management (ERM)”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

framework. This has enabled the company in assessing, responding, reviewing and monitoring

the emerging risk which may affect the business of the company. The recognition of the effective

risk management can be further supported by adequate behaviour of the employees and

commitment to drive risk awareness culture. The ERM framework of the company has included

a risk management strategy which is established with appropriate roles, principles and

responsibilities for the management to include the risk for AMP. The risk appetite statement will

be articulated for the nature of risk the board is willing to accept which are in relevance with

strategic objectives. This is further depicted in alignment with the corporate strategy of AMP and

risk appetite considered by the AMP limited board for ensuring that the risks are taken as per the

consistency of the board to accept the risk (Campbell et al., 2015).

AMP has recognised the remuneration as the key to drive the performance for ensuring

that it supports the new portfolio strategy and drive the performance within the employees which

is appropriate with the risk management framework. In addition to this, the risk management

framework is protected with the long-term financial viability of AMP.

Part B

1. Explaining the team’s understanding of the concept of audit quality

IASB is the main governing body for developing the framework for audit quality which

describes the output factors, input process responsible to contribute to the quality of audit at

engagement for the financial statement audits. The IASB framework has further demonstrated

the importance of the interactions among the stakeholders along with the significance of audit at

various contextual factors (Bell, Causholli & Knechel, 2015). This framework has further

demonstrated the importance of the contextual factors and interactions with the stakeholders. The

main purpose of the audit has been further able to enhance the degree of confidence for the

framework. This has enabled the company in assessing, responding, reviewing and monitoring

the emerging risk which may affect the business of the company. The recognition of the effective

risk management can be further supported by adequate behaviour of the employees and

commitment to drive risk awareness culture. The ERM framework of the company has included

a risk management strategy which is established with appropriate roles, principles and

responsibilities for the management to include the risk for AMP. The risk appetite statement will

be articulated for the nature of risk the board is willing to accept which are in relevance with

strategic objectives. This is further depicted in alignment with the corporate strategy of AMP and

risk appetite considered by the AMP limited board for ensuring that the risks are taken as per the

consistency of the board to accept the risk (Campbell et al., 2015).

AMP has recognised the remuneration as the key to drive the performance for ensuring

that it supports the new portfolio strategy and drive the performance within the employees which

is appropriate with the risk management framework. In addition to this, the risk management

framework is protected with the long-term financial viability of AMP.

Part B

1. Explaining the team’s understanding of the concept of audit quality

IASB is the main governing body for developing the framework for audit quality which

describes the output factors, input process responsible to contribute to the quality of audit at

engagement for the financial statement audits. The IASB framework has further demonstrated

the importance of the interactions among the stakeholders along with the significance of audit at

various contextual factors (Bell, Causholli & Knechel, 2015). This framework has further

demonstrated the importance of the contextual factors and interactions with the stakeholders. The

main purpose of the audit has been further able to enhance the degree of confidence for the

5AUDITING AND ASSURANCE

intended users in gathering sufficient evidence for audit and expressing an opinion whether the

financial statements are prepared as per reporting framework (IAASB Framework 2019).

The key elements depicted in the audit quality can be seen with including inputs, process,

outputs, key interactions within the financial reporting supply chain and contextual factors. The

inputs are considered with attitudes, values and ethics. This is intern influenced by the culture

prevailing in an audit firm. The experience, knowledge and skills are also considered with the

time allotted to perform the audit. The input factors are inferred with the quality attributes which

are attributed directly among the firms as per the audit engagement level, national level and level

of an audit firm. The outputs from the audit are often seen to be inferred with considering the

legislative requirement. On the other hand, some stakeholders will be able to influence the nature

of outputs while other having less influence. Some outputs pertaining to the audit are often

included with the legislative requirement. Although some stakeholders are able to influence the

nature of the outputs, other are seen to be having less influence (Corbella et al., 2015).

2. Explaining and identifying 3 steps the accounting bodies have taken in Australia to

improve the quality of audit

ASIC acts as the key regulator as per the Corporations Act which has been seen with the

responsibility of investigation, surveillance and enforcement of the financial reporting

requirements. The audit inspection program conducted by the board has aimed to promote high

quality external audit of the financial report listed as per the other public interest entities of

Australia. Three steps taken by the accounting body in defining the audit quality are listed as

follows:

Bridging the gap of audit expectation along with shared responsibility- The audit expectation

gap has been referred with the differences among the public and other financial statement the

users perceive as per the auditor’s responsibility. The expectation gap is required with the

intended users in gathering sufficient evidence for audit and expressing an opinion whether the

financial statements are prepared as per reporting framework (IAASB Framework 2019).

The key elements depicted in the audit quality can be seen with including inputs, process,

outputs, key interactions within the financial reporting supply chain and contextual factors. The

inputs are considered with attitudes, values and ethics. This is intern influenced by the culture

prevailing in an audit firm. The experience, knowledge and skills are also considered with the

time allotted to perform the audit. The input factors are inferred with the quality attributes which

are attributed directly among the firms as per the audit engagement level, national level and level

of an audit firm. The outputs from the audit are often seen to be inferred with considering the

legislative requirement. On the other hand, some stakeholders will be able to influence the nature

of outputs while other having less influence. Some outputs pertaining to the audit are often

included with the legislative requirement. Although some stakeholders are able to influence the

nature of the outputs, other are seen to be having less influence (Corbella et al., 2015).

2. Explaining and identifying 3 steps the accounting bodies have taken in Australia to

improve the quality of audit

ASIC acts as the key regulator as per the Corporations Act which has been seen with the

responsibility of investigation, surveillance and enforcement of the financial reporting

requirements. The audit inspection program conducted by the board has aimed to promote high

quality external audit of the financial report listed as per the other public interest entities of

Australia. Three steps taken by the accounting body in defining the audit quality are listed as

follows:

Bridging the gap of audit expectation along with shared responsibility- The audit expectation

gap has been referred with the differences among the public and other financial statement the

users perceive as per the auditor’s responsibility. The expectation gap is required with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

acknowledgement of the task shared with the responsibility on part of the auditors charged with

investors, governance and regulators (Frc.gov.au, 2019).

Developments impacting the audit in Australia - There are number of changes which are made

by audit regulation of ASIC via “Corporations Legislation Amendment (Audit Enhancement)

Act 2012”. The act has implemented several numbers of recommendations made by the treasury

pertaining to the Audit Quality in Australia. The ASIC has introduced several types of audit

regulations are seen with the introduction of annual transparency reports, independent functions

exercised by the auditors and audit deficiency (Louwers et al., 2015).

Financial Reporting initiatives- The APPC has considered supporting the various types of the

discussions with the stakeholders on including more forward-looking statements at the same time

noting the international initiatives. The accounting body IAASB is seen to be in consultation

with the audit proposals which are seen to be enhancing the auditor’s reporting at a global level.

The accounting body has been also able to issue an exposure draft in view of the ISA 720. The

auditor’s responsibility is also inferred with the accompanying and documenting auditing

responsibilities. The IAASB has continued for pursuing and finalising the related elements as per

revised ISA 700 standards (Nisbet et al., 2018).

3. Importance of maintaining audit quality in carrying out an audit

The process of improving and maintaining the audit quality is depicted with identification

of the relevant need for maintaining the audit quality. The accounting board aims to cover

several topics such as description of the audit quality, impatience of the audit quality and

professional scepticism brought into practice with the audit quality. Some of the other factors for

the audit quality can be seen with initiatives taken by the auditors in improving the relevant

disclosures of the audit quality through suitability of the reviewers, reviewing the coverage,

taking remedial action, reviewing and reporting. The ASIC audit inspections and has sufficiently

acknowledgement of the task shared with the responsibility on part of the auditors charged with

investors, governance and regulators (Frc.gov.au, 2019).

Developments impacting the audit in Australia - There are number of changes which are made

by audit regulation of ASIC via “Corporations Legislation Amendment (Audit Enhancement)

Act 2012”. The act has implemented several numbers of recommendations made by the treasury

pertaining to the Audit Quality in Australia. The ASIC has introduced several types of audit

regulations are seen with the introduction of annual transparency reports, independent functions

exercised by the auditors and audit deficiency (Louwers et al., 2015).

Financial Reporting initiatives- The APPC has considered supporting the various types of the

discussions with the stakeholders on including more forward-looking statements at the same time

noting the international initiatives. The accounting body IAASB is seen to be in consultation

with the audit proposals which are seen to be enhancing the auditor’s reporting at a global level.

The accounting body has been also able to issue an exposure draft in view of the ISA 720. The

auditor’s responsibility is also inferred with the accompanying and documenting auditing

responsibilities. The IAASB has continued for pursuing and finalising the related elements as per

revised ISA 700 standards (Nisbet et al., 2018).

3. Importance of maintaining audit quality in carrying out an audit

The process of improving and maintaining the audit quality is depicted with identification

of the relevant need for maintaining the audit quality. The accounting board aims to cover

several topics such as description of the audit quality, impatience of the audit quality and

professional scepticism brought into practice with the audit quality. Some of the other factors for

the audit quality can be seen with initiatives taken by the auditors in improving the relevant

disclosures of the audit quality through suitability of the reviewers, reviewing the coverage,

taking remedial action, reviewing and reporting. The ASIC audit inspections and has sufficiently

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

identified the appropriate audit evidence which is taken into account on the need of the forms to

remediate the deficiencies which are necessary to support the audit opinion. The firms and the

partners may not be hesitating for revisiting the audit entity and undertake additional work. This

is required for completing the auditing on a certain reporting period which may be appropriately

informed against any instance of material misstatement. There may be some partners who may

not be willing to address and accept the findings from the internal quality reviews about the audit

inspections (Bunn, Pilcher & Gilchrist, 2018). This may be concerned about the loss of

reputation, disciplinary actions and additional audit cost. The importance of the good dialogue

among ASIC and partners has been able to ensure about the findings which are appropriate with

the interests of the directors, firms and other users of the financial reports. The firms will be able

to process and take the remedial actions. This is seen to be significant about the factors about

issuing an audit deficiency report (Hay, Stewart & Botica Redmayne, 2017).

Conclusion

The revealing on the Analytical review of the financial statement for identifying areas of

concern for AMP limited has shown that the company has faced significant risk pertaining to

liquidity. The high amount of liquidity has created major concerns for the company which are

associated with improper utilization of available short-term finances. This risk is seen with

current ratio of 8.18 in 2017. The current ratio is considered to pose a significant concern of

liquidity. A similar finding is seen to be evident in case of quick ratio. The financial risk of the

company is further inferred with reducing Fixed Asset Turnover Ratio. Formulating the audit

procedures and responding to the areas of concern are done with the “Enterprise Risk

Management (ERM)” framework maintained by the company has enabled the company in

identifying, reviewing and monitoring the emerging risk factors which may affect the business.

AMP has recognised that the effective risk management with “Enterprise Risk Management

identified the appropriate audit evidence which is taken into account on the need of the forms to

remediate the deficiencies which are necessary to support the audit opinion. The firms and the

partners may not be hesitating for revisiting the audit entity and undertake additional work. This

is required for completing the auditing on a certain reporting period which may be appropriately

informed against any instance of material misstatement. There may be some partners who may

not be willing to address and accept the findings from the internal quality reviews about the audit

inspections (Bunn, Pilcher & Gilchrist, 2018). This may be concerned about the loss of

reputation, disciplinary actions and additional audit cost. The importance of the good dialogue

among ASIC and partners has been able to ensure about the findings which are appropriate with

the interests of the directors, firms and other users of the financial reports. The firms will be able

to process and take the remedial actions. This is seen to be significant about the factors about

issuing an audit deficiency report (Hay, Stewart & Botica Redmayne, 2017).

Conclusion

The revealing on the Analytical review of the financial statement for identifying areas of

concern for AMP limited has shown that the company has faced significant risk pertaining to

liquidity. The high amount of liquidity has created major concerns for the company which are

associated with improper utilization of available short-term finances. This risk is seen with

current ratio of 8.18 in 2017. The current ratio is considered to pose a significant concern of

liquidity. A similar finding is seen to be evident in case of quick ratio. The financial risk of the

company is further inferred with reducing Fixed Asset Turnover Ratio. Formulating the audit

procedures and responding to the areas of concern are done with the “Enterprise Risk

Management (ERM)” framework maintained by the company has enabled the company in

identifying, reviewing and monitoring the emerging risk factors which may affect the business.

AMP has recognised that the effective risk management with “Enterprise Risk Management

8AUDITING AND ASSURANCE

(ERM)” framework. The consideration of the team’s understanding of the concept of audit

quality is identified in terms importance of the interactions among the stakeholders along with

the significance of audit at various contextual factors. This framework has further demonstrated

the importance of the contextual factors and interactions with the stakeholders. Accounting

bodies in Australia are seen to be taking various measures for improving the audit quality. These

are inferred as per bridging the gap of audit expectation along with shared responsibility,

developments impacting the audit in Australia and financial developments impacting the audit in

Australia.

(ERM)” framework. The consideration of the team’s understanding of the concept of audit

quality is identified in terms importance of the interactions among the stakeholders along with

the significance of audit at various contextual factors. This framework has further demonstrated

the importance of the contextual factors and interactions with the stakeholders. Accounting

bodies in Australia are seen to be taking various measures for improving the audit quality. These

are inferred as per bridging the gap of audit expectation along with shared responsibility,

developments impacting the audit in Australia and financial developments impacting the audit in

Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

References

Ball, F., Tyler, J., & Wells, P. (2015). Is audit quality impacted by auditor

relationships?. Journal of Contemporary Accounting & Economics, 11(2), 166-181.

Bell, T. B., Causholli, M., & Knechel, W. R. (2015). Audit firm tenure, non‐audit services, and

internal assessments of audit quality. Journal of Accounting Research, 53(3), 461-509.

Bryce, M., Ali, M. J., & Mather, P. R. (2015). Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, 163-181.

Bunn, M., Pilcher, R., & Gilchrist, D. (2018). Public sector audit history in Britain and

Australia. Financial Accountability & Management, 34(1), 64-76.

Campbell, I., Scott, N., Seneviratne, S., Kollias, J., Walters, D., Taylor, C., & Roder, D. (2015).

Breast cancer characteristics and survival differences between Maori, Pacific and other

New Zealand women included in the quality audit program of breast surgeons of

Australia and New Zealand.

Corbella, S., Florio, C., Gotti, G., & Mastrolia, S. A. (2015). Audit firm rotation, audit fees and

audit quality: The experience of Italian public companies. Journal of International

Accounting, Auditing and Taxation, 25, 46-66.

Frc.gov.au. (2019). [online] Available at:

http://www.frc.gov.au/files/2014/02/APPC_Audit_Quality_in_Australia.pdf [Accessed

11 Jan. 2019].

References

Ball, F., Tyler, J., & Wells, P. (2015). Is audit quality impacted by auditor

relationships?. Journal of Contemporary Accounting & Economics, 11(2), 166-181.

Bell, T. B., Causholli, M., & Knechel, W. R. (2015). Audit firm tenure, non‐audit services, and

internal assessments of audit quality. Journal of Accounting Research, 53(3), 461-509.

Bryce, M., Ali, M. J., & Mather, P. R. (2015). Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, 163-181.

Bunn, M., Pilcher, R., & Gilchrist, D. (2018). Public sector audit history in Britain and

Australia. Financial Accountability & Management, 34(1), 64-76.

Campbell, I., Scott, N., Seneviratne, S., Kollias, J., Walters, D., Taylor, C., & Roder, D. (2015).

Breast cancer characteristics and survival differences between Maori, Pacific and other

New Zealand women included in the quality audit program of breast surgeons of

Australia and New Zealand.

Corbella, S., Florio, C., Gotti, G., & Mastrolia, S. A. (2015). Audit firm rotation, audit fees and

audit quality: The experience of Italian public companies. Journal of International

Accounting, Auditing and Taxation, 25, 46-66.

Frc.gov.au. (2019). [online] Available at:

http://www.frc.gov.au/files/2014/02/APPC_Audit_Quality_in_Australia.pdf [Accessed

11 Jan. 2019].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE

Hay, D., Stewart, J., & Botica Redmayne, N. (2017). The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis. Australian Accounting

Review, 27(4), 457-479.

IAASB Framework .2019. Available at:

https://www.accaglobal.com/in/en/technical-activities/technical-resources-search/2014/

march/audit-quality-iaasb-frwk.html [Accessed 11 Jan. 2019].

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Nisbet, D., Robertson, A., Mannil, B., Pincham, V., & Mclennan, A. (2018). Quality

management of nuchal translucency ultrasound measurement in Australia. Australian and

New Zealand Journal of Obstetrics and Gynaecology.

Tepalagul, N., & Lin, L. (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), 101-121.

Hay, D., Stewart, J., & Botica Redmayne, N. (2017). The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis. Australian Accounting

Review, 27(4), 457-479.

IAASB Framework .2019. Available at:

https://www.accaglobal.com/in/en/technical-activities/technical-resources-search/2014/

march/audit-quality-iaasb-frwk.html [Accessed 11 Jan. 2019].

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Nisbet, D., Robertson, A., Mannil, B., Pincham, V., & Mclennan, A. (2018). Quality

management of nuchal translucency ultrasound measurement in Australia. Australian and

New Zealand Journal of Obstetrics and Gynaecology.

Tepalagul, N., & Lin, L. (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), 101-121.

11AUDITING AND ASSURANCE

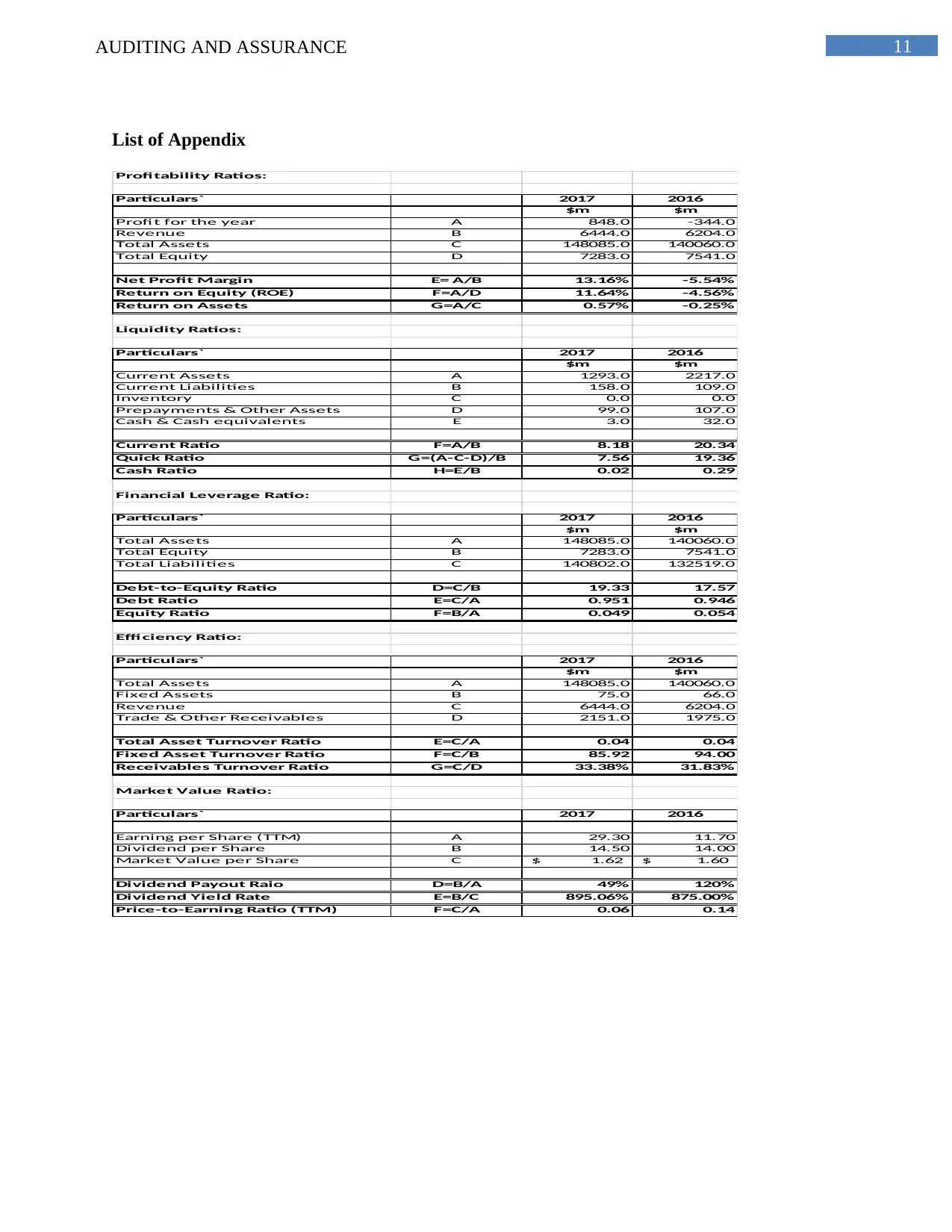

List of Appendix

Profitability Ratios:

Particulars` 2017 2016

$m $m

Profit for the year A 848.0 -344.0

Revenue B 6444.0 6204.0

Total Assets C 148085.0 140060.0

Total Equity D 7283.0 7541.0

Net Profit Margin E= A/B 13.16% -5.54%

Return on Equity (ROE) F=A/D 11.64% -4.56%

Return on Assets G=A/C 0.57% -0.25%

Liquidity Ratios:

Particulars` 2017 2016

$m $m

Current Assets A 1293.0 2217.0

Current Liabilities B 158.0 109.0

Inventory C 0.0 0.0

Prepayments & Other Assets D 99.0 107.0

Cash & Cash equivalents E 3.0 32.0

Current Ratio F=A/B 8.18 20.34

Quick Ratio G=(A-C-D)/B 7.56 19.36

Cash Ratio H=E/B 0.02 0.29

Financial Leverage Ratio:

Particulars` 2017 2016

$m $m

Total Assets A 148085.0 140060.0

Total Equity B 7283.0 7541.0

Total Liabilities C 140802.0 132519.0

Debt-to-Equity Ratio D=C/B 19.33 17.57

Debt Ratio E=C/A 0.951 0.946

Equity Ratio F=B/A 0.049 0.054

Efficiency Ratio:

Particulars` 2017 2016

$m $m

Total Assets A 148085.0 140060.0

Fixed Assets B 75.0 66.0

Revenue C 6444.0 6204.0

Trade & Other Receivables D 2151.0 1975.0

Total Asset Turnover Ratio E=C/A 0.04 0.04

Fixed Asset Turnover Ratio F=C/B 85.92 94.00

Receivables Turnover Ratio G=C/D 33.38% 31.83%

Market Value Ratio:

Particulars` 2017 2016

Earning per Share (TTM) A 29.30 11.70

Dividend per Share B 14.50 14.00

Market Value per Share C 1.62$ 1.60$

Dividend Payout Raio D=B/A 49% 120%

Dividend Yield Rate E=B/C 895.06% 875.00%

Price-to-Earning Ratio (TTM) F=C/A 0.06 0.14

List of Appendix

Profitability Ratios:

Particulars` 2017 2016

$m $m

Profit for the year A 848.0 -344.0

Revenue B 6444.0 6204.0

Total Assets C 148085.0 140060.0

Total Equity D 7283.0 7541.0

Net Profit Margin E= A/B 13.16% -5.54%

Return on Equity (ROE) F=A/D 11.64% -4.56%

Return on Assets G=A/C 0.57% -0.25%

Liquidity Ratios:

Particulars` 2017 2016

$m $m

Current Assets A 1293.0 2217.0

Current Liabilities B 158.0 109.0

Inventory C 0.0 0.0

Prepayments & Other Assets D 99.0 107.0

Cash & Cash equivalents E 3.0 32.0

Current Ratio F=A/B 8.18 20.34

Quick Ratio G=(A-C-D)/B 7.56 19.36

Cash Ratio H=E/B 0.02 0.29

Financial Leverage Ratio:

Particulars` 2017 2016

$m $m

Total Assets A 148085.0 140060.0

Total Equity B 7283.0 7541.0

Total Liabilities C 140802.0 132519.0

Debt-to-Equity Ratio D=C/B 19.33 17.57

Debt Ratio E=C/A 0.951 0.946

Equity Ratio F=B/A 0.049 0.054

Efficiency Ratio:

Particulars` 2017 2016

$m $m

Total Assets A 148085.0 140060.0

Fixed Assets B 75.0 66.0

Revenue C 6444.0 6204.0

Trade & Other Receivables D 2151.0 1975.0

Total Asset Turnover Ratio E=C/A 0.04 0.04

Fixed Asset Turnover Ratio F=C/B 85.92 94.00

Receivables Turnover Ratio G=C/D 33.38% 31.83%

Market Value Ratio:

Particulars` 2017 2016

Earning per Share (TTM) A 29.30 11.70

Dividend per Share B 14.50 14.00

Market Value per Share C 1.62$ 1.60$

Dividend Payout Raio D=B/A 49% 120%

Dividend Yield Rate E=B/C 895.06% 875.00%

Price-to-Earning Ratio (TTM) F=C/A 0.06 0.14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.