Auditing and Assurance Report: Bendigo Bank's Financials 2018

VerifiedAdded on 2022/09/26

|10

|1646

|19

Report

AI Summary

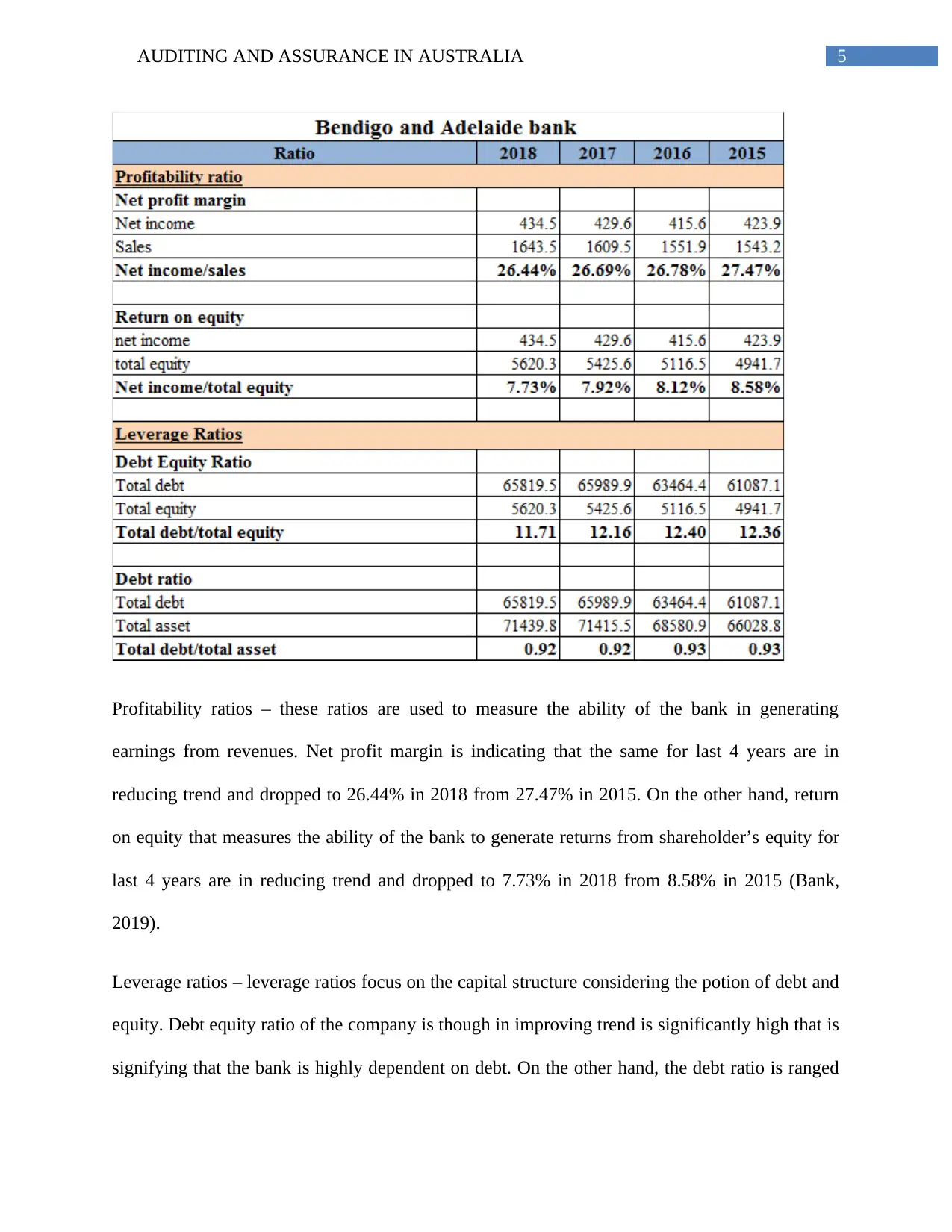

This report provides a comprehensive analysis of the auditing and assurance procedures applied to Bendigo and Adelaide Bank's financial statements for the year ending 2018. It begins by determining the level of materiality, discussing its nature and different bases for calculation, and providing a quantitative estimate. The report then reviews significant items from the annual report, such as contingencies and impairment, outlining necessary audit procedures. Section 2 focuses on preliminary analytical review, including ratio analysis to assess profitability and leverage. Section 3 reviews the cash flow statement, identifying potential going concern issues, and analyzes the audit report issued by Ernst & Young, highlighting key audit issues. The analysis is based on relevant auditing and assurance standards and the provided annual report, with appropriate citations and references.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.