Analytical Review of AMP Ltd: Audit Procedures in Australia 2017

VerifiedAdded on 2023/04/25

|9

|1028

|463

Report

AI Summary

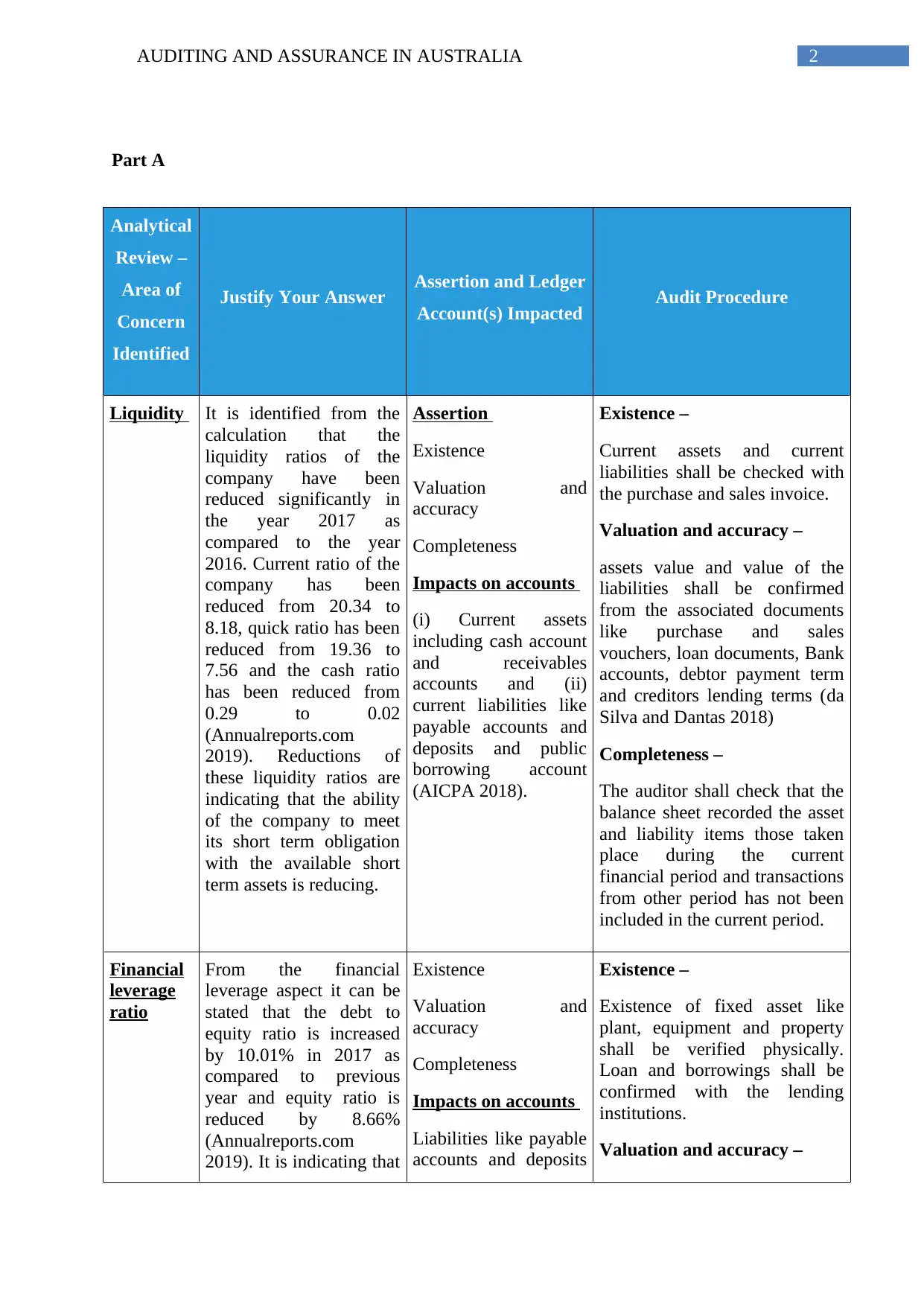

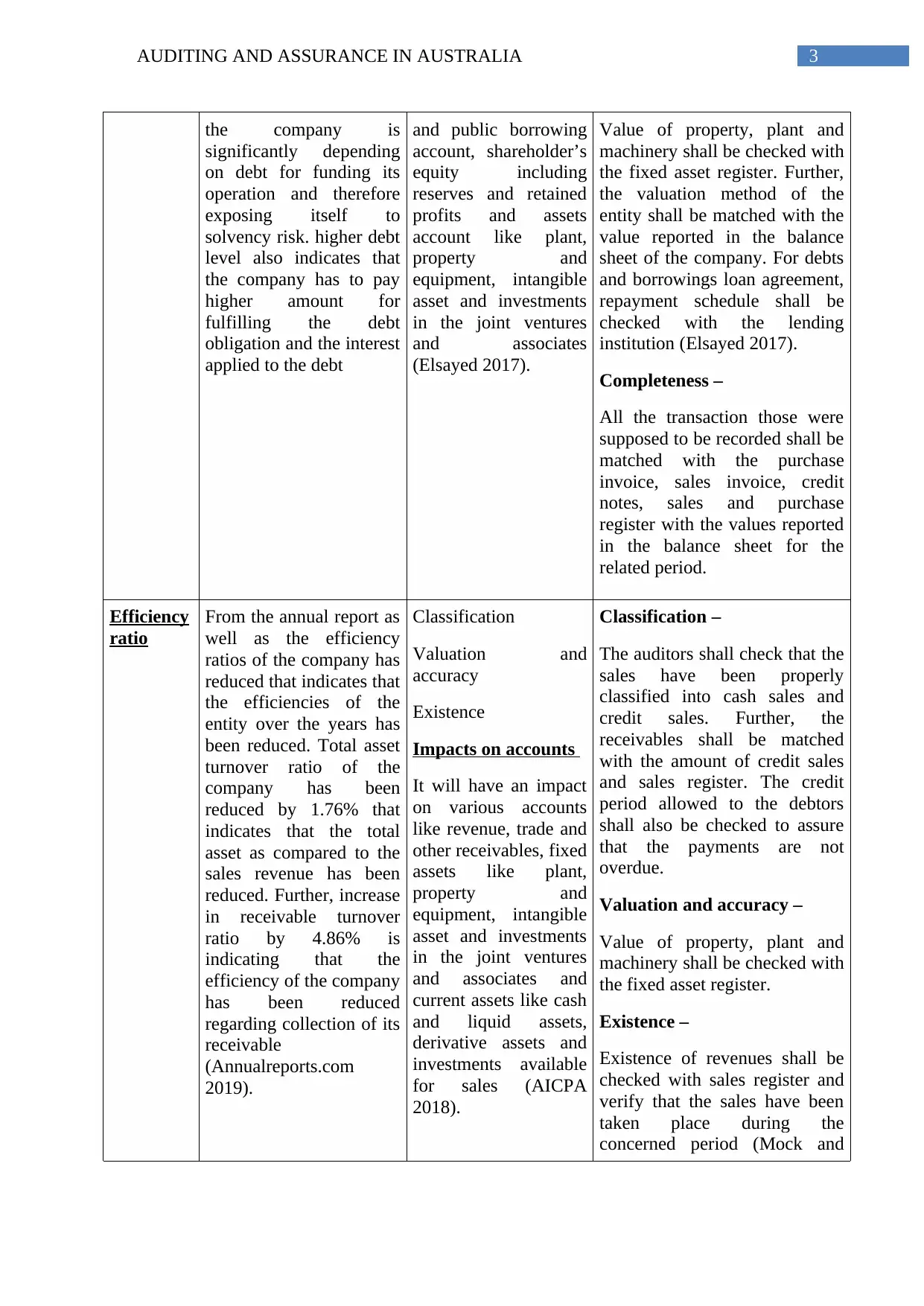

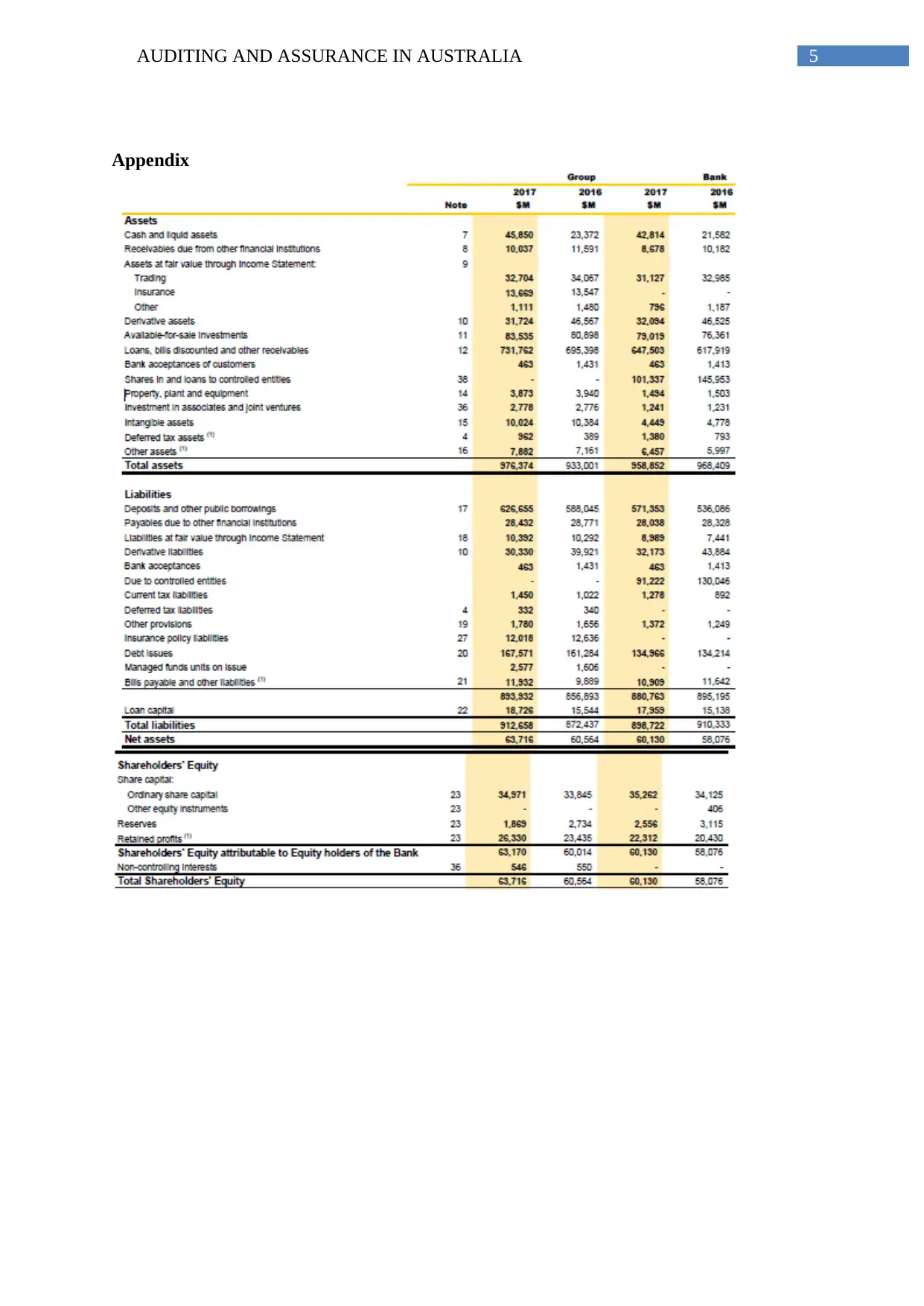

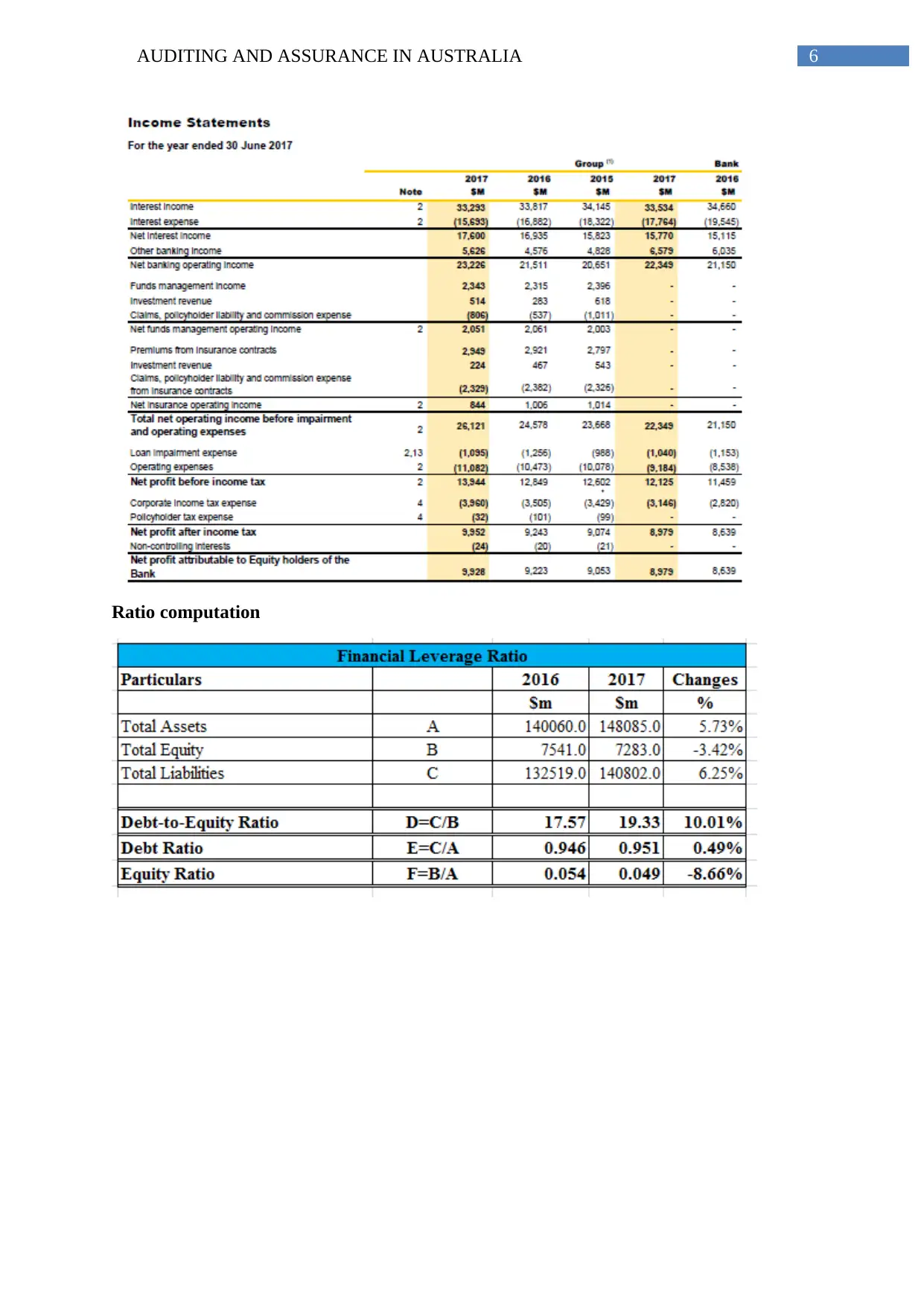

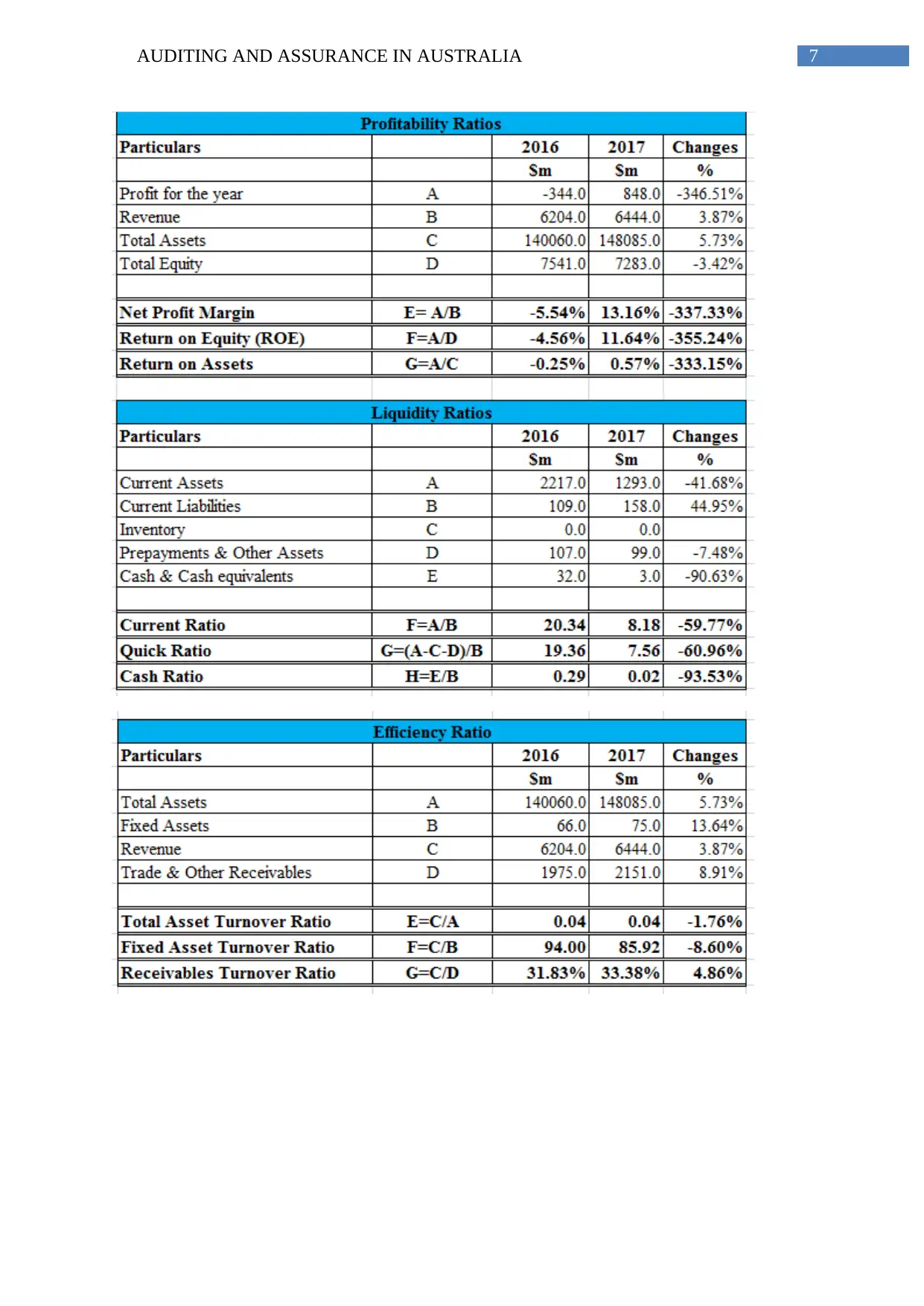

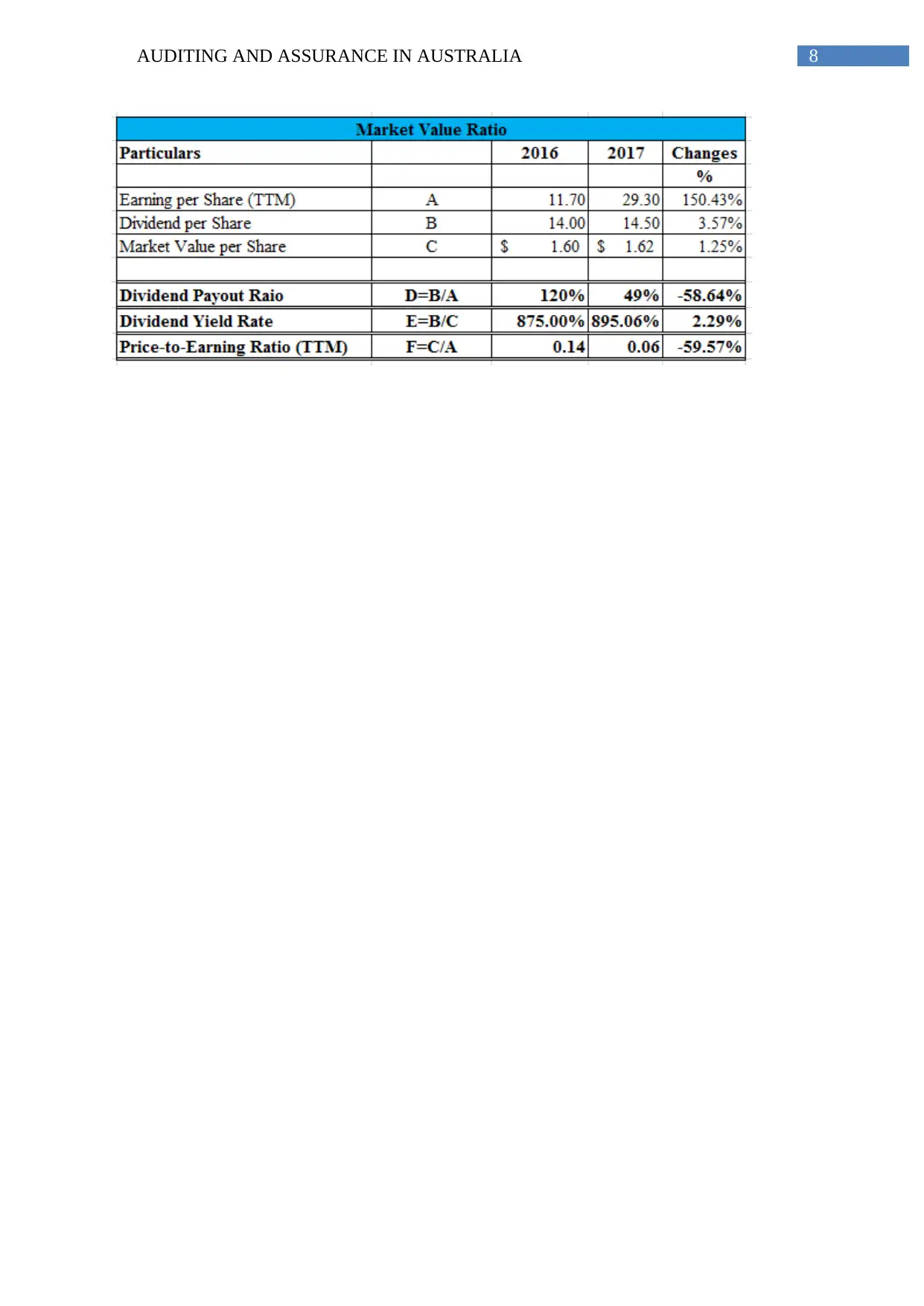

This report presents an analytical review of AMP Ltd's financial statements for the year ended December 31, 2017, as part of an audit assignment. It identifies areas of concern based on ratio analysis, including liquidity, financial leverage, and efficiency, and justifies these concerns with reference to specific financial data. The report details the impact of these concerns on relevant accounts and assertions, such as the existence, valuation, and completeness of assets and liabilities. Furthermore, it formulates relevant audit procedures to respond to these areas of concern, such as verifying asset values, confirming loan agreements, and checking sales classifications. The analysis includes a computation of various financial ratios, presented in the appendix, to support the findings and recommendations related to the audit of AMP Ltd.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.