Detailed Analysis of ASA 220 for Auditing and Assurance (ACCM4400)

VerifiedAdded on 2022/11/17

|7

|1385

|117

Report

AI Summary

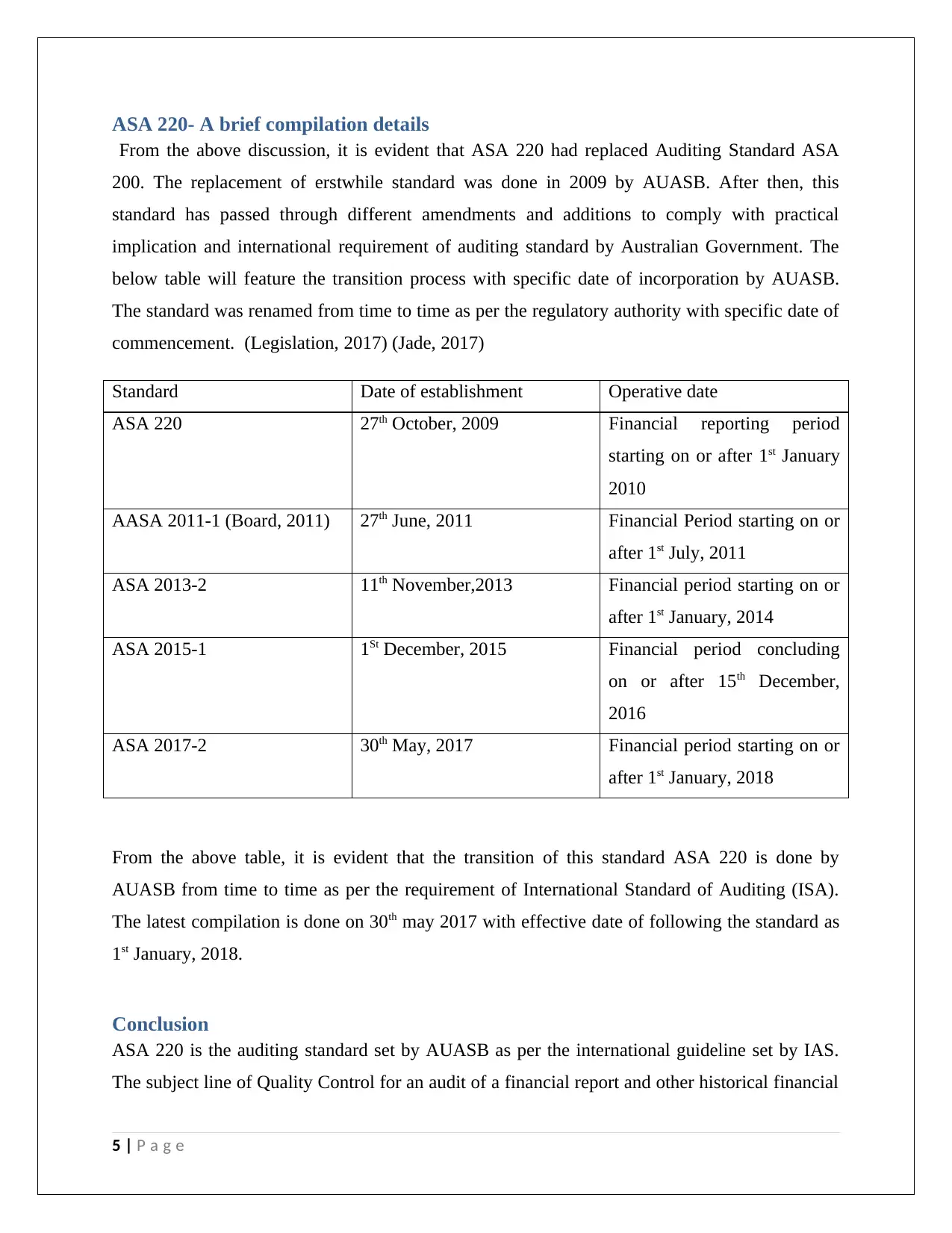

This report provides a comprehensive overview of ASA 220, focusing on quality control for audits of financial reports and other historical financial information in Australia. The report details the standard's objectives, which include establishing leadership accountability, defining ethical requirements, and setting processes for client acceptance, engagement performance, and quality control monitoring. It highlights the evolution of ASA 220, noting its revisions and amendments by the AUASB to align with international auditing standards and ensure the protection of stakeholders. The report explains the standard's key components, such as engagement deliverables, team assignments, and documentation needs, and its relationship with other auditing standards like ASA 101 and ASA 200. The report also includes a table illustrating the timeline of ASA 220's revisions and effective dates, emphasizing the continuous efforts to adapt the standard to meet evolving auditing practices and international requirements, ensuring clarity and prudence in financial reporting.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.